Market Pressure Differential (MPD) [SharpStrat]Market Pressure Differential (MPD)

Concept & Purpose

The Market Pressure Differential (MPD) is a proprietary indicator designed to measure the internal balance of buying and selling pressure directly on the price chart.

Unlike standard momentum or trend indicators, MPD analyzes the structural behavior of each candle—its body, wicks, and overall range—to determine whether the market is dominated by expansion (buying aggression) or contraction (selling absorption).

This indicator provides a visual overlay of market pressure that adapts dynamically to volatility, helping traders see real-time shifts in participation intensity without using oscillators.

In simple terms:

When MPD expands upward → buyer pressure dominates.

When MPD contracts downward → seller pressure dominates.

Calculation Overview

MPD uses a structural candle formula to compute directional pressure:

Body Ratio = (Close − Open) / (High − Low)

Wick Differential = (Lower Wick − Upper Wick) / (High − Low)

Raw Pressure = (Body Ratio × Body Weight) + (Wick Differential × Wick Weight)

Then it applies:

EMA smoothing (to stabilize short-term noise)

Standard deviation normalization (to maintain consistent scaling)

ATR projection (to adapt the signal visually to volatility)

This produces the MPD projection line and the pressure ribbon, drawn directly on the main chart.

Customizable Inputs

Users can adjust color schemes, EMA smoothing length, ATR parameters, normalization length, and body/wick weighting to adapt the indicator’s sensitivity and aesthetic to different markets or chart themes.

How to Use

The Market Pressure Differential (MPD) visualizes the real-time balance between buying and selling pressure. It should be used as a contextual bias tool, not a standalone signal generator.

The white line represents the MPD projection, showing how market pressure evolves in real time based on candle structure and volatility.

The red line represents the ATR envelope, which defines the market’s expected volatility range.

MPD reacts quickly to candle structure, so trend bias is based on how its projection behaves relative to the ATR envelope:

Above the ATR band → positive pressure and bullish bias.

Below the ATR band → negative pressure and bearish bias.

Hovering near the ATR band → neutral or indecisive conditions.

The MPD percentage in the label represents the normalized strength of pressure relative to recent volatility.

Positive % = buying dominance.

Negative % = selling dominance.

Higher absolute values = stronger momentum compared to volatility.

To trade with MPD:

Watch candle colors and the projection line — green or positive % shows buyer control, red or negative % shows seller control.

Note transitions above or below the ATR level for early signs of momentum shifts.

Combine MPD signals with price structure, key levels, or volume for confirmation.

This helps reveal which side controls the market and whether that pressure is strong enough to overcome typical volatility.

Disclaimer

It introduces a novel structural–pressure approach to visualizing market dynamics.

For educational and analytical purposes only; this does not constitute financial advice.

ATR

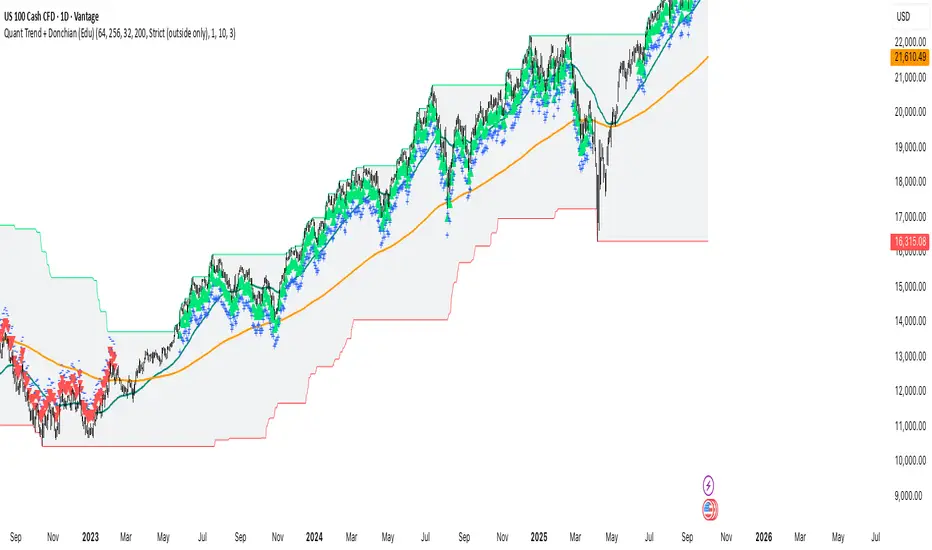

Quant Trend + Donchian (Educational, Public-Safe)What this does

Educational, public-safe visualization of a quant regime model:

• Trend : EMA(64) vs EMA(256) (EWMAC proxy)

• Breakout : Donchian channel (200)

• Volatility-awareness : internal z-scores (not plotted) for concept clarity

Why it’s useful

• Shows when trend & breakout align (clean regimes) vs conflict (chop)

• Helps explain why volatility-aware systems size up in smooth trends and scale down in noise

How to read it

• EMA64 above EMA256 with price near/above Donchian high → trend-following alignment

• EMA64 below EMA256 with price near/below Donchian low → bearish alignment

• Inside channel with EMAs tangled → range/chop risk

Notes

• Indicator is educational only (no orders).

• Built entirely with TradingView built-ins.

• For consistent visuals: enable “Indicator values on price scale” and disable “Scale price chart only” in Settings → Scales .

ATR Horizontal Lines from EMA and SMA with TableHow it works:

The script calculates ATR levels (of your choosing)

Instead of plotting curves, it creates horizontal lines

The lines are deleted and recreated on each bar to show current levels

Lines extend to the right or can be limited to a certain width

Customization options:

Line width (1-10 pixels)

Individual colors for each of the 4 lines

All the original parameters (EMA/SMA lengths, ATR length, multipliers)

The horizontal lines will now show the current ATR-based support/resistance levels and move dynamically as the EMAs, SMA, and ATR values change with new price data.

Vol-Pace Projected-ATR-ADX-Alert-MAThe VolSC indicator analyzes stock volume trends with a focus on the Pace metric, which projects today's volume as a percentage of the 30-day average, highlighting unusual activity (e.g., over 200% turns bright green with alerts). The phantom projection bar, a wide green histogram to the right of the last bar, visually represents this projected volume on daily charts only, aiding quick identification of potential volume surges without cluttering intraday or weekly views. Additional features include ADX strength, ATR averages, and customizable table display for comprehensive insights.

Key Features:

* Primary Indicator: Volume with ADX (Average Directional Index) text.

* Pacing and Alerts: Calculates the volume pace for the day. Features an unusual volume alert with an adjustable threshold (e.g., 200%).

* Volume Projection: Projects a visual "Phantom Volume" for the day, offset to the right of the actual volume bar.

* ATR Indicator: Displays the 2x ATR (Average True Range) value as text.

* Volume Average: Displays the ADV (Average Daily Volume) Moving Average as text.

* Customization: Most settings are adjustable.

Atlantean Sideways / Range Regime DetectorPurpose

When using trend based indicators, you can skip the false signals when there is a sideways action, protecting you from the false signals.

Flags likely sideways/range phases using three checks:

Weak trend (ADX from DMI)

Price compression (Bollinger Band Width, normalized)

Low volatility (NATR = ATR/Price%)

Logic

isSideways = (ADX < adxThresh) AND (bbNorm < 0.25) AND (NATR < natrMax)

When true: bars + background turn teal and a provisional Range High/Low (rolling rangeWin) is drawn.

Key Inputs

DMI: diLen(22)

Optimized for 15 mins Bitcoin, could change it to 14 for more general approach

ADX: adxSmooth(14), adxThresh(18)

Volatility: lenATR(14), natrMax(1.8)

Visuals: rangeWin(20), bar/range toggles

Quick Tuning

More signals: raise adxThresh to 20–25, raise natrMax to 2.5–4.0, increase BB cutoff by editing bbNorm < 0.25 --> 0.35–0.50.

Smoother range lines: increase rangeWin to 30–40.

Use Cases

Mean reversion inside teal ranges.

Breakout prep when price closes outside the drawn range after teal ends. Could be used as a signal although not suggested.

Filter trend systems: skip trades when sidewaysCond is true. This is the main purpose, for it to be combined with trend based indicators, like Supertrend.

Alert

“Sideways Detected” triggers when isSideways is true.

Script could be expanded upon your requests.

ATR Volatility and Trend AnalysisATR Volatility and Trend Analysis

Unlock the power of the Average True Range (ATR) with the ATR Volatility and Trend Analysis indicator. This comprehensive tool is designed to provide traders with a multi-faceted view of market dynamics, combining volatility analysis, dynamic support and resistance levels, and trend detection into a single, easy-to-use indicator.

How It Works

The ATR Volatility and Trend Analysis indicator is built upon the core concept of the ATR, a classic measure of market volatility. It expands on this by providing several key features:

Dynamic ATR Bands: The indicator plots three sets of upper and lower bands around the price. These bands are calculated by multiplying the current ATR value by user-defined multipliers. They act as dynamic support and resistance levels, widening during volatile periods and contracting during calm markets.

Volatility Breakout Signals: Identify potential breakouts with precision. The indicator generates a signal when the current ATR value surges above its own moving average by a specified threshold, indicating a significant increase in volatility that could lead to a strong price move.

Trend Detection: The indicator determines the market trend by analyzing both price action and ATR behavior. A bullish trend is signaled when the price is above its moving average and volatility is increasing. Conversely, a bearish trend is signaled when the price is below its moving average and volatility is increasing.

How to Use the ATR Multi-Band Indicator

Identify Support and Resistance: Use the ATR bands as key levels. Price approaching the outer bands may indicate overbought or oversold conditions, while a break of the bands can signal a strong continuation.

Confirm Breakouts: Look for a volatility breakout signal to confirm the strength behind a price move. A breakout from a consolidation range accompanied by a volatility signal is a strong indicator of a new trend.

Trade with the Trend: Use the background coloring and trend signals to align your trades with the dominant market direction. Enter long positions during confirmed bullish trends and short positions during bearish trends.

Set Up Alerts: The indicator includes alerts for band crosses, trend changes, and volatility breakouts, ensuring you never miss a potential trading opportunity.

What makes it different?

While many indicators use ATR, the ATR Volatility and Trend Analysis tool is unique in its integration of multiple ATR-based concepts into a single, cohesive system. It doesn't just show volatility; it interprets it in the context of price action to deliver actionable trend and breakout signals, making it a complete solution for ATR-based analysis.

Disclaimer

This indicator is designed as a technical analysis tool and should be used in conjunction with other forms of analysis and proper risk management.

Past performance does not guarantee future results, and traders should thoroughly test any strategy before implementing it with real capital.

Volume Percentile Supertrend [BackQuant]Volume Percentile Supertrend

A volatility and participation aware Supertrend that automatically widens or tightens its bands based on where current volume sits inside its recent distribution. The goal is simple: fewer whipsaws when activity surges, faster reaction when the tape is quiet.

What it does

Calculates a standard Supertrend framework from an ATR on a volume weighted price source.

Measures current volume against its recent percentile and converts that context into a dynamic ATR multiplier.

Widens bands when volume is unusually high to reduce chop. Tightens bands when volume is unusually low to catch turns earlier.

Paints candles, draws the active Supertrend line and optional bands, and prints clear Long and Short signal markers.

Why volume percentile

Fixed ATR multipliers assume all bars are equal. They are not. When participation spikes, price swings expand and a static band gets sliced.

Percentiles place the current bar inside a recent distribution. If volume is in the top slice, the Supertrend allows more room. If volume is in the bottom slice, it expects smaller noise and tightens.

This keeps the same playbook usable across busy sessions and sleepy ones without constant manual retuning.

How it works

Volume distribution - A rolling window computes the Pth percentile of volume. Above that is flagged as high volume. A lower reference percentile marks quiet bars.

Dynamic multiplier - Start from a Base Multiplier. If bar is high volume, scale it up by a function of volume-to-average and a Sensitivity knob. If bar is low volume, scale it down. Smooth the result with an EMA to avoid jitter.

VWMA source - The price input for bands is a short volume weighted moving average of close. Heavy prints matter more.

ATR envelope - Compute ATR on your length. UpperBasic = VWMA + Multiplier x ATR. LowerBasic = VWMA - Multiplier x ATR.

Trailing logic - The final lines trail price so they only move in a direction that preserves Supertrend behavior. This prevents sudden flips from transient pokes.

Direction and signals - Direction flips when price crosses through the relevant trailing line. SupertrendLong and SupertrendShort mark those flips. The plotted Supertrend is the active trailing side.

Inputs and what they change

Volume Lookback - Window for percentile and average. Larger window = stabler percentile, smaller = snappier.

Volume Percentile Level - Threshold that defines high volume. Example 70 means top 30 percent of recent bars are treated as high activity.

Volume Sensitivity - Gain from volume ratio to the dynamic multiplier. Higher = bands expand more when volume spikes.

VWMA Source Length - Smoothing of the volume weighted price source for the bands.

ATR Length - Standard ATR window. Larger = slower, smaller = quicker.

Base Multiplier - Core band width before volume adjustment. Think of this as your neutral volatility setting.

Multiplier Smoothing - EMA on the dynamic multiplier. Reduces back and forth changes when volume oscillates around the threshold.

Show Supertrend on chart - Toggles the active line.

Show Upper Lower Bands - Draws both sides even when inactive. Good for context.

Paint candles according to Trend - Colors bars by trend direction.

Show Long and Short Signals - Prints 𝕃 and 𝕊 markers at flips.

Colors - Choose your long and short palette.

Reading the plot

Supertrend line - Thick line that hugs price from above in downtrends and from below in uptrends. Its distance breathes with volume.

Bands - Optional upper and lower rails. Useful to see the inactive side and judge how wide the envelope is right now.

Signals - 𝕃 prints when the trend flips long. 𝕊 prints when the trend flips short.

Candle colors - Quick bias read at a glance when painting is enabled.

Typical workflows

Trend following - Use 𝕃 flips to initiate longs and ride while bars remain colored long and price respects the lower trailing line. Mirror for shorts with 𝕊 and the upper trailing line. During high volume phases the line will give more room, which helps stay in the move.

Pullback adds - In an established trend, shallow tags toward the active line after a high volume expansion can be add points. The dynamic envelope adjusts to the session so your add distance is not fixed to a stale volatility regime.

Mean reversion filter - In quiet tape the multiplier contracts and flips come earlier. If you prefer fading, watch for quick toggles around the bands when volume percentile remains low. In high volume, avoid fading into the widened line unless you have other strong reasons.

Notes on behavior

High volume bar: the percentile gate opens, volRatio > 1 powers up the multiplier through the Sensitivity lever, bands widen, fewer false flips.

Low volume bar: multiplier contracts, bands tighten, flips can happen earlier which is useful when you want to catch regime changes in quiet conditions.

Smoothing matters: both the price source (VWMA) and the multiplier are smoothed to keep structure readable while still adapting.

Quick checklist

If you see frequent chop and today feels busy: check that volume is above your percentile. Wider bands are expected. Consider letting the trend prove itself against the expanded line before acting.

If everything feels slow and you want earlier entries: percentile likely marks low volume, so bands tighten and 𝕃 or 𝕊 can appear sooner.

If you want more or fewer flips overall: adjust Base Multiplier first. If you want more reaction specifically tied to volume surges: raise Volume Sensitivity. If the envelope breathes too fast: raise Multiplier Smoothing.

What the signals mean

SupertrendLong - Direction changed from non-long to long. 𝕃 marker prints. The active line switches to support below price.

SupertrendShort - Direction changed from non-short to short. 𝕊 marker prints. The active line switches to resistance above price.

Trend color - Bars painted long or short help validate context for entries and management.

Summary

Volume Percentile Supertrend adapts the classic Supertrend to the day you are trading. Volume percentile sets the mood, sensitivity translates it into dynamic band width, and smoothing keeps it clean. The result is a single plot that aims to stay conservative when the tape is loud and act decisively when it is quiet, without you having to constantly retune settings.

Opening Candle Zone with ATR Bands by nkChartsThis indicator highlights the opening range of each trading session and projects dynamic ATR-based zones around it.

Key Features

Plots high and low levels of the opening candle for each new daily session.

Extends these levels across the session, providing clear intraday support and resistance zones.

Adds ATR-based offset bands above and below the opening range for volatility-adjusted levels.

Customizable colors, ATR length, and multiplier for flexible use across markets and timeframes.

Adjustable session history limit to control how many past levels remain on the chart.

How to Use:

The opening range high/low often acts as strong intraday support or resistance.

The ATR bands give an adaptive volatility buffer, useful for breakout or mean-reversion strategies.

Works on any market with clear session opens.

This tool is designed for traders who want to combine session-based price action with volatility insights, helping identify potential breakouts, reversals, or consolidation areas throughout the day.

⚠️ Disclaimer: This indicator is for educational purposes only. It does not provide financial advice or guarantee profits. Always perform your own analysis before making trading decisions.

KAMENICZKI PROSCAPLERPROSCAPLER is an advanced trading indicator that combines a dynamic channel with a prediction line for maximum accuracy and trading success. The indicator is designed for professional traders who need reliable signals with high success rates.

Adaptive Intelligence

Automatic optimal period detection - the indicator adapts to various market conditions

Intelligent timeframe settings - automatically optimizes periods based on TF

Dynamic adaptation - the channel changes according to volatility and trend.

High Signal Accuracy

Pearson R correlation - filters only strong trends with high reliability

Multi-timeframe confirmation - confirms signals on higher timeframe

Volatility and volume filters - eliminates false signals

RSI extreme values - captures only the best entry points

Prediction Line

Future price direction - shows where the price will move

Adaptive length - adapts to timeframe

Strong signals - when the entire prediction line is in the center of the channel

Quality Filters

Minimum Pearson R 0.5+ - only strong trends

Volume filter 1.2x - only signals with sufficient volume

ATR volatility filter - eliminates low volatility

RSI extreme levels - only at oversold/overbought values

Anomalies

Anomaly detection - captures exceptional opportunities

Bright yellow/pink color - immediately visible

Fast Reaction

Minimum trend bars = 1 - fast turning

Adaptive detection - immediate reaction to changes

Automatic optimizations - without manual settings

News & Volatility Filters

News filter - disables channel during high impact news

Volatility filter - protects against high volatility

Gap detection - filters dangerous gaps

Combined Filters

All filters must be met - maximum reliability

Multi-timeframe confirmation - double check

Pearson R validation - mathematical accuracy

Volume confirmation - institutional interest

Reaction Speed

Instant signals - without delay

Adaptive settings - automatic optimization

Fast turning - minimum 1 bar trend

Signal Accuracy

Quality filters increase success rate to 70-80%

Anomalies have 80-90% success rate

STRONG signals (prediction line in center) 85-95%

HAVE FUN :)

ATR Bands over 50D SMA (% method)Indicator that shows multiples of ATR% above the 50d SMA as bands on a chart, building off of

Jeff Sun 's methodology. You should tinker with the settings to chose your multiples, colors and which multiple lines to show. I don't know if the negative multiple lines have any use, so I turn mine off. Offered as is. I am not a programmer. Note the other indicators shown on the print screen are not mine.

Rogue 4H ORRogue 4H OR – Opening Range

The Rogue 4H Daily OR is a powerful Opening Range tool designed to help traders identify key intraday levels and capitalize on failed breakout setups.

Key Features:

Custom Opening Range: Define your OR start and end times (default 4H) to suit any market – stocks, forex, or crypto.

Locked Levels: Once the OR session ends, the high and low are locked and projected across the trading day.

Fakeout Signals: Triangular buy/sell markers plot when price breaks out of the OR and then closes back inside, signaling potential reversal entries.

Daily Reset: Signals and ranges reset each trading day for clean analysis.

Session Cutoff: Optional cutoff time prevents late-day signals from cluttering your chart.

How to Use:

Adjust the OR start/end time to match your trading session (e.g., 09:30–13:30 for US stocks, 00:00–04:00 for crypto).

Watch for false breakouts → a close above the OR high that falls back inside signals a short, while a close below the OR low that reclaims the range signals a long.

Use the signals in confluence with trend, volume, or other confirmation tools for best results. **This is not financial advice.**

Designed for traders who thrive on intraday range dynamics and want a visual, session-based tool to spot high-probability setups.

**This is not financial advice**

Uptrick: ATR ModelIntroduction

The Uptrick: ATR Model is a multi-regime directional tool designed to adapt to various trading styles and timeframes. It combines trend assessment, market state evaluation, visual overlays, and signal filtering into a single, highly configurable system. This indicator is intended to help traders interpret directional conditions, structure their entries and exits, and view real-time shifts in market context, all without relying on external scripts or multiple chart layers.

Core Functionality

At its foundation, the Uptrick: ATR Model builds a framework that responds to user-defined structure and market behavior. Through a wide range of inputs, traders can adjust the internal responsiveness, signal frequency, and volatility interaction of the system. The core behavior of the model can be shaped via:

Custom starting date for signal activation

Flexible smoothing structure

Adjustable expansion control for range boundaries

Signal persistence settings to limit noise

Conditional plotting of directional signals

Real-time bar coloring and overlays

Custom routing between long, short, and neutral positioning

This indicator is not tied to a single interpretation of market movement. Instead, it adapts to how the user defines structural behavior, volatility confirmation, and trend alignment.

Multi-Regime Architecture

The script includes four unique operating regimes, each offering a distinct model of interpreting market conditions:

Trend Mode

This regime focuses on trend state transitions over time. Signal behavior is aligned with directional market shifts and transitions are plotted with visual labels. Optional filters and persistence settings help control signal quality and responsiveness.

Cloud Close Mode

Cloud Close mode detects transitions when price interacts with dynamic boundaries. Signals are generated when the asset moves in or out of these ranges. This regime supports state memory to avoid repeated signals and emphasizes confirmation over reactivity.

Lightning Trend Mode

This mode evaluates momentum alignment across selected structures. Its behavior is based on composite assessments and dynamically reflects changes in directional agreement. This regime is well-suited for intraday or high-resolution users seeking visual confirmation of trend shifts.

Final Verdict Mode

A meta-regime that combines the output of the other three modes into a single directional consensus. A live decision table is displayed on-screen, showing the current verdict of each regime and a final, averaged output. This mode is designed for high-conviction or conservative traders who prefer confirmation across multiple systems.

Each regime can be enabled through a single selector, and the indicator adapts its signal behavior and bar coloring to reflect the active mode.

Signal System and Visual Feedback

The indicator generates Long, Short, or Cash (neutral/exit) signals depending on the active regime, directional configuration, and filter conditions. Signal shapes are plotted only once per state transition and are color-coded for clarity.

Users can define:

Whether signals should support both long and short, or long-only

Whether repeated signals are allowed (pyramiding control)

Whether to enforce a minimum number of confirming bars before a signal is allowed (persistence)

Signals are accompanied by real-time bar coloring, giving users an instant visual cue of the current state without relying on shape markers alone. These signals adjust based on the selected regime and are subject to any active confirmation filters.

Confirmation Filters

To reduce noise and improve the relevance of each signal, the model includes two optional filters:

Strength Filter

[Applies a condition based on the asset’s momentum. When enabled, signals will only fire if this condition aligns with the trade direction. Includes parameters for sensitivity and smoothness.

Trend Filter

Applies a directional filter based on a broader trend context. Signals will only trigger when this larger structure supports the directional bias. This filter is useful for avoiding signals during counter-trend moves or consolidations.

Both filters can be toggled independently. When disabled, the model will operate with fewer restrictions.

Dynamic Structure Customization

Users can control how the internal structure of the model behaves using:

Source selection (e.g., close, open, high, etc.)

Smoothing configuration using a tiered structure with up to three stages

Custom length inputs to adjust responsiveness

Selectable method options for each layer

Expansion settings to adjust the distance of dynamic boundaries

Signal persistence threshold to delay entries until confirmation is met

This modular control allows traders to define whether they want faster reaction to movement or more conservative, delayed responses depending on their strategy.

Final Verdict Table

The Final Verdict table is a live display that summarizes the signal output of the three core regimes (Trend, Cloud Close, and Lightning Trend). It includes:

Regime names and their current directional state

Directional scores for each regime

A final averaged score and directional label

The table is updated every bar and is fully customizable:

Position on screen (top left, center, bottom right, etc.)

Text size for readability

Color-coded state labels for fast interpretation

This feature is designed to offer structured decision support by showing consensus or divergence across all logic models in real time.

Static Levels Module

An optional module allows the user to anchor a high point (typically an all-time high) from a user-defined historical date. From that anchor, multiple levels are projected downward using fixed ratios. These levels are:

Automatically updated when new highs occur

Visualized using horizontal step-lines

Fully customizable in terms of count, color, and source

These levels serve as contextual guides and can assist with price projection, risk management, or discretionary confluence zones.

Directional Control

The model supports both Long & Short and Long Only signal modes. In Long Only mode, exit signals are routed to neutral (Cash) instead of Short. This allows users to align the indicator with personal strategy, risk appetite, or portfolio rules. Neutral signals are also plotted with distinct labels and coloring to indicate a directional reset.

Input Summary

All components of the script are user-configurable through the following inputs:

Start date selector to restrict signal generation

Source selection for core price input

Custom lengths and responsiveness settings

Smoothing structure with optional stacking

Expansion control for range width

Signal persistence threshold

Signal type selector (long-only or long & short)

Regime selector between four logic systems

Filters: strength-based and trend-based

Verdict table display settings (position and size)

Static levels: anchor date, count, source, and visual customization

Originality

What sets the Uptrick: ATR Model apart is its integration of multiple directional systems into a single, configurable interface. Each regime is distinct and interprets market behavior from a unique perspective, while the Final Verdict mode offers a consolidated view that few tools provide in a fully visual and non-redundant format. The Lightning Trend scoring engine and modular structural design offer a level of control and flexibility uncommon in single-layer indicators. The combination of signal gating, decision tables, and state tracking creates a cohesive, structured environment for directional evaluation.

Summary

The Uptrick: ATR Model is a complete directional and volatility analysis system designed for customizable trend evaluation, signal clarity, and strategic filtering. It adapts to different trader needs through its configurable regimes, state-aware signals, dynamic overlays, and visual decision tools. It is suitable for discretionary traders seeking structured guidance, as well as systematic users who require configurable state management and signal control.

Disclaimer

This tool is provided for informational and research purposes only. It does not constitute investment advice or a recommendation to buy or sell any financial instrument. All trading involves risk, and past performance does not guarantee future results. Users are solely responsible for their own decisions.

Simplified ATR Trailing Stop (Long & Short, Custom TF + Stop)This indicator plots a dynamic ATR-based trailing stop that adapts to price volatility and keeps you protected whether you’re trading long or short. It’s lightweight, customisable, and designed for traders who want clean risk management without unnecessary complexity.

✨ Key Features:

📅 Custom Entry Date & Price – choose the exact day you want the trailing stop to begin, or let it auto-start from the close.

🔀 Long or Short Mode – flip between bullish and bearish trade setups.

⏱️ Custom Timeframe Support – calculate ATR stops on any higher/lower timeframe (from 10m to 1M) for maximum flexibility.

📏 ATR-Based Logic – trailing stop adjusts dynamically using a multiplier of ATR, keeping stops adaptive to volatility.

🎯 Custom First-Day Stop – set a different ATR factor for day one to handle entries more cautiously.

✅ Stop Trigger Mode – choose between:

Stop on Wick Breach (default intraday aggressiveness)

Stop on Candle Close (extra confirmation, fewer false stops).

📊 How to Use:

Set your entry date and price (or leave price = 0 to use that day’s close).

Select trade direction (Long or Short).

Pick your ATR period, multiplier, and timeframe.

Watch the trailing stop line update automatically until it’s breached.

This tool is great for swing traders, intraday strategists, and anyone who wants a simple yet powerful trailing stop that adapts to price volatility.

Average True Range TrackerThis indicator calculates the daily ATR of the past 14 days. The ATR% indicates the range completed for the day. The ATR indicates the average daily range. The 20% ATR indicates the value of 20% of the daily ATR for retracement purposes.

Daily ATR TrackerThis indicator calculates the daily ATR of the past 14 days. The ATR% indicates the range completed for the day. The ATR indicates the average daily range. The 20% ATR indicates the value of 20% of the daily ATR for retracement purposes.

BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

ATR Enhanced [DCAUT]█ ATR Enhanced

📊 OVERVIEW

Standard ATR uses only RMA smoothing, while ATR Enhanced provides 20+ professional smoothing algorithms , offering precise volatility measurement solutions for different trading scenarios and market environments.

💡 CORE VALUE

- 20+ algorithm choices : SMA, EMA, RMA, WMA, HMA, T3, KAMA, FRAMA, Kalman Filter, etc.

📋 PARAMETER SETUP

ATR Length : Calculation period (default: 14)

Moving Average Type : Choose the most suitable smoothing method from 20+ algorithms

🎨 COLOR CODING

Green : Rising volatility

Red : Falling volatility

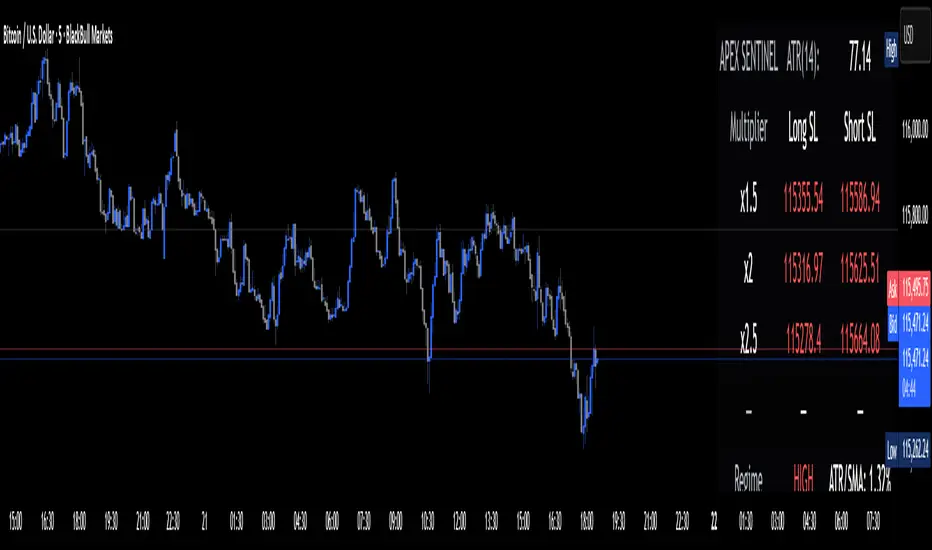

Apex Edge Sentinel - Stop Loss HUDApex Edge – ATR Sentinel Stop Loss HUD

The Apex Edge – ATR Sentinel is a complete stop-loss intelligence system built as a clean, always-on HUD.

It delivers institutional-level risk guidance by calculating and displaying live ATR-based stop levels for both long and short trades at multiple risk tolerances.

Forget cluttered charts and repainting lines — Sentinel gives you a clear stop-loss reference panel that updates dynamically with every bar.

✅ Features

• Triple ATR Multipliers

User-defined (e.g. x1.5 / x2.0 / x2.5). Compare tight, medium, and wide stops instantly.

• Dual-Side SL Levels

Both Long and Short safe stop prices displayed side by side. No more guessing trend

bias.

• ATR Transparency

HUD shows ATR(length) so you always know the calculation basis. Default = 14, adjustable

to your style.

• ATR Regime Meter

Detects volatility conditions (LOW / NORMAL / HIGH) by comparing ATR to its SMA. Helps

you avoid over-tight stops in high-volatility markets.

• Tick-Aware Rounding

Stop levels auto-rounded to the instrument’s tick size (Gold = 0.10, FX = 0.0001, indices =

whole points).

Custom HUD Design

• Location: Top/Bottom, Left/Right

• Sizes: Compact / Medium / Large (desktop or mobile)

• Opacity control (25% default Apex styling)

How to Use

1. Load Sentinel on your chart.

2. Check the HUD:

• ATR(14): 2.6 → base volatility measure.

• x1.5 / x2.0 / x2.5 → instant SL levels for both long & short trades.

3. Before entering a trade → decide which multiplier matches your style (tight scalper vs wider swing).

4. Manually place your SL at the level displayed in the HUD.

Sentinel works as both:

• A pre-trade check (is ATR stop too wide for my RR?).

• A live risk compass (updated stop levels every bar).

Why Apex Sentinel?

Most ATR stop indicators clutter charts with lagging lines or repainting trails. Sentinel strips it back to what matters:

• The numbers.

• The risk levels.

• The context.

It’s a pure stop-loss HUD, designed for serious traders who want clarity, discipline, and instant reference points across any market or timeframe.

Notes

• This is a HUD-only system (no automatic SL line). Traders manually apply the SL level

shown in the panel.

• Defaults: ATR(14), multipliers 1.5 / 2.0 / 2.5. Adjust to your trading style.

• Best used on intraday pairs like XAUUSD, EURUSD, indices, but works universally.

Apex Edge Philosophy: Clean. Smart. Institutional.

No clutter. No gimmicks. Just precision tools for modern markets.

Hammer Candle Detector with ATR Wick ConditionThis script detects Hammer candlesticks on any timeframe chart.

Conditions for a valid Hammer:

1. Small body near the top of the candle range (≤30% of total range)

2. Lower shadow at least 2× the body

3. Small or no upper shadow (≤30% of body)

4. Lower wick height must be greater than half of ATR(14)

A triangle marker is plotted below each candle that meets these conditions.

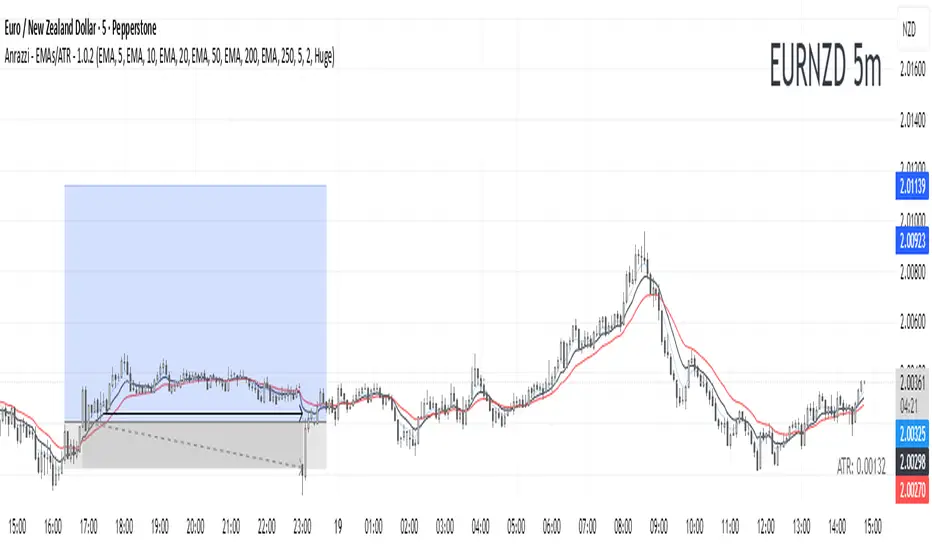

Anrazzi - EMAs/ATR - 1.0.2The Anrazzi – EMAs/ATR indicator is a multi-purpose overlay designed to help traders track trend direction and market volatility in a single clean tool.

It plots up to six customizable moving averages (MAs) and an Average True Range (ATR) value directly on your chart, allowing you to quickly identify market bias, dynamic support/resistance, and volatility levels without switching indicators.

This script is ideal for traders who want a simple, configurable, and efficient way to combine trend-following signals with volatility-based position sizing.

📌 Key Features

Six Moving Averages (MA1 → MA6)

Toggle each MA on/off individually

Choose between EMA or SMA for each

Customize length and color

Perfect for spotting trend direction and pullback zones

ATR Display

Uses Wilder’s ATR formula (ta.rma(ta.tr(true), 14))

Can be calculated on current or higher timeframe

Adjustable multiplier for position sizing (e.g., 1.5× ATR stops)

Displays cleanly in the bottom-right corner

Custom Watermark

Displays symbol + timeframe in top-right

Adjustable color and size for streamers, screenshots, or clear charting

Compact UI

Organized with group and inline inputs for quick configuration

Lightweight and optimized for real-time performance

⚙️ How It Works

MAs: The script uses either ta.ema() or ta.sma() to compute each moving average based on the user-selected type and length.

ATR: The ATR is calculated using ta.rma(ta.tr(true), 14) (Wilder’s smoothing), and optionally scaled by a multiplier for easier use in risk management.

Tables: ATR value and watermark are displayed using table.new() so they stay anchored to the screen regardless of zoom level.

📈 How to Use

Enable the MAs you want to track and adjust their lengths, type, and colors.

Enable ATR if you want to see volatility — optionally select a higher timeframe for broader context.

Use MAs to:

Identify overall trend direction (e.g. price above MA20 = bullish)

Spot pullback zones for entries

See when multiple MAs cluster together as support/resistance zones

Use ATR value to:

Size your stop-loss dynamically (e.g. stop = entry − 1.5×ATR)

Detect volatility breakouts (ATR spikes = market expansion)

🎯 Recommended For

Day traders & swing traders

Trend-following & momentum strategies

Volatility-based risk management

Traders who want a clean, all-in-one dashboard

Wavelet Kernal ATR [BackQuant]Wavelet Kernal ATR

Introduction

Wavelet Kernal ATR is a closed-source, chart-side tool that fuses an edge-preserving “wavelet kernal” smoother with an ATR-aware regime line. The goal is simple: follow the real move, ignore the static, and give you clean, visual places to manage risk. It can color the trend directly on price, flip states when regime changes, and (optionally) add a secondary moving-average overlay for confirmation all while keeping the chart readable.

What it is

A single adaptive baseline designed to act like a “bias rail.” When it’s up, you favor longs; when it’s down, you favor shorts. It updates in a way that’s responsive to fresh information but resistant to insignificant wiggles. Around that baseline, an ATR-scaled envelope governs how and when the line concedes to volatility, which helps avoid flip-flopping in chop. Because this release is closed source, the following focuses on behavior and practical use rather than internal math.

What it’s used for

Bias & context: Read the backdrop with one glance; green = bullish regime, red = bearish regime.

Timing: Use slope changes and pullbacks to the line for entries aligned with the dominant push.

Risk placement: The line and its volatility envelope give intuitive zones for stops and targets.

Clarity: Paint candles by state and keep other overlays to a minimum to reduce decision noise.

Why “Wavelet Kernal” matters (plain English)

A wavelet kernal is a localized, scale-aware weighting profile. Instead of averaging every bar equally—or with a single, fixed decay—it emphasizes the most informative part of the recent window while softly down-weighting points that are either too old or too extreme. Three practical benefits result:

Edge preservation: Turning points are less “smeared” than with conventional smoothers, so the line can pivot sooner on genuine breakouts without chasing every tick.

Multi-scale sensitivity: The kernal “listens” to structure at multiple scales inside a compact window, helping it track swing-sized movement while suppressing micro-chop.

Lag vs. noise balance: Because the weighting is localized and shape-aware, you get a calmer line at similar responsiveness compared to common filters; fewer false flips, more meaningful ones.

You don’t need to know the internals to use it: think of the wavelet kernal as a smart stethoscope for price. It hears the heartbeat (trend/impulse) and ignores the coughs (random spikes).

How it behaves

Trend mode: When price expands directionally, the line “sticks” to the move and stays colored in that direction. Pullbacks that remain shallow relative to volatility usually do not flip the state.

Transition mode: After a large push, the line may flatten as volatility compresses. Flat + frequent small flips is the platform telling you: edge is low, wait for expansion.

Shock handling: On sudden spikes, the ATR envelope acts like a reality check—minor overreactions are absorbed, while statistically meaningful breaks force the baseline to concede and re-anchor.

Reading the line (quick heuristics)

Green + rising: Bias long; look for pullbacks toward the line that stall and resume.

Red + falling: Bias short; look for rallies into the line that fade.

Flat + rapid color flips: Stand down or scale down—let the next expansion choose the side.

Color flip at a prior S/R: Treat as a higher-quality signal than flips in the middle of nowhere.

Baseline + ATR corridor (concept)

The volatility envelope isn’t drawn as two fat bands here; it’s used internally to keep the baseline honest. You can think of it as a “breathing room” rule: the line is allowed to adapt with trend, but it shouldn’t jump the fence unless price movement is large enough relative to recent volatility. That’s why the tool feels calm in chop and decisive during actual breaks.

Optional MA Overlay (confluence)

You can overlay a moving average of the baseline itself for slower-regime confirmation. When both agree (baseline direction and its MA slope), you have trend alignment. When they diverge, expect digestion or a possible transition. Keep this overlay subtle; it’s a context layer, not another signal firehose.

What it plots

Wavelet ATR line — the adaptive baseline that flips color with regime.

Optional MA of the baseline — slower confirmation, on or off.

Candle painting — bars can inherit long/short state for instant read-through.

Alerts — available for state flips up/down.

Inputs explained (effect on behavior)

Wavelet ATR Calculation

Price Source — Default hlc3 ; choose your preferred composite of OHLC.

Kernal Calculation Length — The horizon the kernal “listens to.” Longer = steadier, fewer flips; shorter = snappier, more flips.

Kernal Alpha — How strongly the kernal prioritizes the freshest data inside that horizon. Higher alpha = quicker to acknowledge new pushes; lower alpha = more patience.

ATR Period — Determines the volatility memory. Shorter = envelope reacts faster; longer = envelope demands more evidence to concede.

ATR Factor — Scales how “strict” the envelope is. Larger factor = more tolerance (fewer flips); smaller = more sensitivity (earlier regime shifts).

Confluence

Show Atr Moving Average — Turns on the secondary overlay.

MA Type — Choose the flavor you read best (simple, exponential, linear regression, etc.).

Moving Average Period — The overlay’s horizon; treat it as a background current.

Volume Factor / Sigma (when applicable) — Specialized parameter used by certain MA types to shape smoothness.

Plotting & UI

Plot Wavelet ATR — Toggle the main line.

Paint Candles According to Trend — Color bars by the baseline’s state.

Long/Short Colors — Match your chart theme.

A practical playbook

Trend-pullback continuation

Setup: Baseline is green and rising. Price pulls back toward it, stalls (small bodies or wicks into the line), then resumes upward.

Idea: Enter on the resumption. Protective stop often lives just below the line or the last swing low. Scale targets through prior highs or measured projections.

Breakout + acceptance

Setup: Baseline flattens after consolidation. Price expands away; baseline turns green/red and stays that way as two or three bars “accept” the new area.

Idea: Join on the first controlled retest toward the line. If the line instantly loses color again, treat it as a fakeout.

Failed test / flip-and-go

Setup: Price challenges the line from the wrong side but cannot close through it convincingly; shortly after, the baseline flips color back in the original direction.

Idea: Use that failed test as a springboard—risk tucked beyond the failed side.

Quality checks before you click

Structure context: Is the flip happening near prior highs/lows, session opens, or well-observed levels? Flips at structure carry more information.

Volatility posture: If range is compressing, be picky. If range is expanding, respect the first pullback after the flip.

Clutter discipline: Use the fewest layers that earn their place. Trend line + candle painting is often enough.

Common questions

“Why did the line not flip on that spike?” Because the move wasn’t large or sustained enough relative to recent volatility. The envelope forces patience.

“Why did it flip and then flip back?” That’s what digestion looks like. The kernal preserves edges, but when the market truly has no edge, brief flips are information: sit tight.

“Do I need the overlay MA?” No. It’s optional context. If it helps you filter marginal trades, keep it. If it adds noise, turn it off.

Troubleshooting & fine-tuning (principles, not prescriptions)

Too many flips? Increase the Kernal Calculation Length or the ATR Factor. You’re asking for a steadier bias.

Feels late on strong trends? Nudge Kernal Alpha higher or shorten the Kernal Length. You’re asking for earlier acknowledgment.

Stops feel random? Place initial risk just beyond the baseline (or the last swing beyond it), then trail only when fresh structure appears.

Charts feel crowded? Keep the baseline + candle coloring; hide the overlay and other ornaments.

Alerts

Wavelet ATR Trend Up

Wavelet ATR Trend Down

Final notes

This tool is built to minimize analysis fatigue: one adaptive line, strong visual feedback, and enough discipline from volatility logic to avoid the “every blip is a signal” trap. The internal math, weighting shapes, and state logic are proprietary and intentionally not disclosed here; you still have full control of behavior through the inputs above. As always, align the settings with your own trade plan, keep the chart readable, and let confluence—not clutter—do the heavy lifting.

Anrazzi - EMAs/ATR - 1.0.2Description:

The Anrazzi - EMAs/ATR indicator is a versatile tool for technical traders looking to monitor multiple moving averages alongside the Average True Range (ATR) on any chart. Designed for simplicity and customization, it allows traders to visualize up to six moving averages with configurable type, color, and length, while keeping real-time volatility information via ATR directly on the chart.

This indicator is perfect for spotting trends, identifying support/resistance zones, and gauging market volatility for intraday or swing trading strategies.

Key Features:

Supports up to six independent moving averages (MA1 → MA6)

Each MA is fully customizable:

Enable/disable individually

Type: EMA or SMA

Length

Color

ATR Display:

Custom timeframe

Color and position configurable

Adjustable multiplier

Compact and organized settings for easy configuration

Lightweight and efficient code for smooth chart performance

Watermark

Inputs / Settings:

MA Options: MA1 → MA6 (Enable/Disable, Type, Length, Color)

Additional Settings: ATR (Enable, Timeframe, Color, Multiplier)

How to Use:

Enable the moving averages you want to track

Configure type, length, and color for each MA

Enable ATR if needed and adjust settings

Watch MAs plotted dynamically and ATR in bottom-right corner

Recommended For:

Day traders and swing traders

Trend-following strategies

Volatility analysis and breakout detection

Traders needing a compact multi-MA dashboard

Dynamic EMA x VWAP AlertsDynamic EMA × VWAP Alerts generates buy and sell signals only when an EMA crossover happens in a meaningful VWAP (or standard deviation band) context. By combining classic EMA logic with flexible VWAP anchors (Daily, Weekly, Rolling) and optional advanced filters (ATR, Relative Volume, Deviation, Distance, Time Windows) to trim noise further, the script creates location-aware, filterable alerts rather than “everywhere” crosses. The value for trading and originality here lies in the integration of one or multiple anchors, band gating, combinator logic, and advanced regime filters. It’s designed for use across multiple instruments and timeframes, where EMA/VWAP context is relevant. It can run quietly in the background while you focus on price action and your own S/R levels.

What it does (quick take)

Detects EMA crossovers (double or optional triple) and evaluates them in VWAP context.

Plots Buy/Sell markers only when all chosen conditions are met.

Clean UX: keep all or parts of the engine visible or hide everything and let alerts run based on the silent engine behind your own S/R levels in an uncluttered, practical chart, as illustrated below.

Engine illustration: All selected engines visible

Practical use case: Same snapshot sequence as above but all selected engines invisible

Swing examples (beyond intraday)

Signals-only (clean value view):

Signals + your own S/R lines:

EMA selection (choose your playbook)

Defaults: Fast 9, Medium 21 (common intraday combo).

Modes: Double Cross — Fast vs Medium.

Triple Cross (optional) — adds a Slow EMA trend filter (enable Slow > 0).

Ranges: you can set each EMA 0–200 (0 = hidden/off)

Visuals are optional; you can display or hide each EMA line

EMA cross footprints (optional): Helps you assess trend continuation or change.

Use your own strategy: switch to 9/50, 20/50, 50/200, or whatever EMA set you trust for your instrument/timeframe.

VWAP Selection (the context engine)

Daily VWAP – resets each chart day (00:00–23:59). Typical fit: scalpers and fast intraday decision points.

Weekly VWAP – resets at the start of the calendar week. Typical fit: intraday with higher-timeframe context (aligns day trades with weekly bias).

Rolling VWAP – an adjustable VWMA-based rolling anchor (not session-reset), used as a flexible context reference Typical fit: multi-day swings when you want a flexible anchor that adapts across sessions.

Standard deviation bands (σ ±1/±2/±3) available for each anchor and help you express the “how far from fair value” idea.

Why VWAP matters: it’s a running, volume-weighted anchor where strong moves relative to VWAP and its bands help frame mean-reversion vs. trend-continuation risk. Evaluating crosses relative to VWAP/±σ reduces “everywhere” noise and helps frame potential setups.

How alerts are decided

An alert triggers only when:

Your selected EMA crossover occurs, and

Your chosen VWAP gate(s) and any filters pass. (Computed on bar close to avoid mid-bar noise)

Signals and alerts do not repaint; alerts evaluate and fire once per bar close.

Alert gates (Single / AND / OR)

Select one VWAP source or combine two (e.g., Daily + Weekly) with Single, AND, or OR logic.

Choose gate levels from VWAP or standard deviation bands (±σ). Typical long logic: price at/under VWAP or −σ. Typical short logic: price at/over VWAP or +σ.

Practical recipes:

Trend-follow: Daily AND Weekly at/above VWAP → confirms strength on two anchors.

Mean-reversion probe: Daily OR Rolling at −1σ → allows earlier fades with flexibility.

Advanced filtering: Suitable for advanced/Quant traders

During the research and development of this indicator, the EMA/VWAP cross logic was tested on historical S&P500 Futures data to explore patterns on multiple timeframes. These selected filtering indicators below showed correlation between certain market conditions and chosen indicator thresholds, helping reduce noise and lower-quality alerts. Results were research-oriented and are not predictive of future performance.

Therefore, I have built these indicator filters that run silently in the background. They let you trim noise by requiring alerts to appear only in market regimes you define. Each one constrains alert conditions; using them together helps tailor alerts to your strategy—but overly strict settings may filter out most or all alerts.

Relative Volume (RVOL): compares current volume to a baseline; ensures alerts arrive with participation instead of thin tape.

Deviation Threshold (%): controls how close the cross must be to the VWAP/σ level; tight = anchored signals, loose = more activity.

ATR Gate (+ Relative regime): keeps alerts inside a volatility regime; avoids both dead tape and chaotic spikes.

Distance Guard: requires price to be at least X ticks/% away from VWAP; useful to avoid premature signals near fair value.

Note: It’s not recommended to activate all of them at once or change the values aggressively. Unless you’ve done deeper backtesting or machine learning calibration, you can easily filter out everything. Use small thresholds at first, then adjust to your instrument once you see how each filter changes alert frequency and quality. Advanced/quant users can fine-tune freely.

Case example:

Unfiltered: Timeframe 15 min, EMA Selection 9/21, VWAP gates Rolling (250 bars) OR Weekly

Filtered: Same setup as above + activated filters:

RVOL: 100 bars, Min. RVOL 0.4

Deviation threshold (%): 0.3

ATR Length: 14

Min ATR (%): 0.05

Relative regime: Base length 2000, Min Ratio 0.85, Max Ratio 2

Under the hood

This indicator leans on TradingView built-ins (e.g., EMA, VWMA, ATR, alertcondition) to maximize speed, stability, and compatibility while we implement the custom logic (VWAP anchors, band gating, combinator gates, advanced filters, time windows). Built-ins were easy to work with and reduced edge-case bugs and kept the visuals responsive, while the design gives fine-tuning and clean visuals—so both discretionary traders and quant-minded users can shape the alerts to their strategy and workflow.

Disclaimer

The tools, scripts, and indicators presented here are provided for educational and informational purposes only. They are not financial advice and should not be interpreted as investment recommendations, trading signals, or a solicitation to buy or sell any financial instrument.

All forms of trading and investing involve risk. The past performance of any security, strategy, or market condition does not guarantee future outcomes. Users are solely responsible for their own trading and investment decisions, including evaluating their financial situation, objectives, and risk tolerance.

By using this indicator, you acknowledge that you do so at your own risk. The author accepts no liability for any direct or indirect loss or damage—including, without limitation, loss of profits—that may arise from the use of, or reliance upon, this tool.