BTC Fundamental Value Hypothesis [OmegaTools]BTC Fundamental Value Hypothesis is a macro-valuation and regime-detection model designed to contextualize Bitcoin’s price through relative market-cap comparisons against major capital reservoirs: Gold, Silver, the Altcoin market, and large-cap equities. Instead of relying on traditional on-chain metrics or purely technical signals, this tool frames BTC as an asset competing for global liquidity and “store-of-value mindshare”, then estimates an implied fair value based on how BTC historically coexists (or diverges) from these benchmark universes.

Core concept: relative market-cap anchoring

The indicator builds a reference-based fair price by translating external market capitalizations into implied BTC valuation using a dominance framework. In practice, you choose one or more reference universes (Gold, Silver, Altcoins, Stocks). For each selected universe, the script computes how large BTC “should be” relative to that universe (dominance ratio), and converts that into an implied BTC price. The final fair price is the average of the implied prices from the enabled universes.

Two dominance modes: automatic vs manual

1. Automatic Dominance % (default)

When enabled, the model estimates dominance ratios dynamically using a 252-period simple moving average of BTC market cap divided by each reference market cap. This produces an adaptive baseline that follows structural changes over time and reduces sensitivity to short-term spikes.

2. Manual Dominance %

If you prefer a discretionary macro thesis, you can directly input dominance parameters for each reference universe. This is useful when you want to stress-test scenarios (e.g., “BTC should converge toward X% of Gold’s market cap”) or align the model with a specific long-term adoption narrative.

Reference universes and data construction

- BTC market cap: pulled from CRYPTOCAP:BTC.

- Gold and Silver market caps: derived from the corresponding futures symbols (GC1!, SI1!) multiplied by an assumed total above-ground quantity (constant tonnage converted to troy ounces). This provides a practical and tradable proxy for spot valuation context.

- Altcoin market cap: pulled from CRYPTOCAP:TOTAL2 (total crypto market excluding BTC).

- Stocks market cap proxy (Σ3): a deliberately conservative equity benchmark built from three mega-cap stocks (AAPL, MSFT, AMZN) using total shares outstanding (request.financial) multiplied by price. This avoids index licensing complexity while still tracking a meaningful slice of global equity beta/liquidity.

Valuation output: overvalued vs undervalued (log-based)

The valuation readout is expressed as a percentage derived from the logarithmic distance between BTC price and the model’s fair price. This choice makes valuation comparable across long time horizons and reduces distortion during exponential growth phases. A positive valuation indicates BTC trading below the model’s implied value (undervalued), while a negative valuation indicates trading above it (overvalued).

Oscillator: relative momentum and regime confirmation

In addition to fair value, the indicator includes a momentum differential oscillator built from RSI(50):

- BTC RSI is compared to the average RSI of the selected reference universes.

- The oscillator highlights when BTC strength is leading or lagging the broader macro benchmarks.

- Color is rendered through a gradient to provide immediate regime readability (risk-on vs risk-off behavior, expansion vs contraction phases).

Visualization and UI components

- Fair Price overlay: the computed fair price is plotted directly on the BTC chart for immediate comparison with spot price action.

- Valuation shading: the area between price and fair price is filled to visually emphasize dislocation and potential mean-reversion zones.

- Oscillator panel: a zero-centered oscillator with filled bands helps you identify persistent trend regimes versus transitional conditions.

- Summary table: a right-side table displays the current valuation (over/under) and, when Automatic mode is enabled, the live dominance ratios used in the model (BTC/GOLD, BTC/SILVER, BTC/ALTC, BTC/STOCKS).

How to use it (practical workflows)

- Macro valuation context: use fair price as a structural anchor to assess whether BTC is trading at a premium or discount relative to external liquidity baselines.

- Regime filtering: combine valuation with the oscillator to distinguish “cheap but weak” from “cheap and strengthening” (and the inverse for tops).

- Mean-reversion mapping: large, persistent deviations from fair value often highlight speculative extremes or capitulation zones; this can support systematic entries/exits, position sizing, or hedging decisions.

- Scenario analysis: switch to Manual Dominance % to model adoption outcomes, policy-driven shifts, or multi-year re-rating assumptions.

Important notes and limitations (read before use)

- This is a hypothesis-driven macro model, not a literal intrinsic value calculation. Results depend on dominance assumptions, proxies, and data availability.

- Gold/Silver market caps are approximations based on futures pricing and fixed supply constants; real-world supply dynamics, above-ground estimates, and spot/futures basis can differ.

- The Stocks (Σ3) benchmark is a proxy and intentionally not “the whole market”. It is designed to represent a large-cap liquidity reference, not total equity capitalization.

- Always validate signals with additional context (market structure, volatility regime, risk management rules). This indicator is best used as a macro layer in a broader decision framework.

Designed for clarity, macro discipline, and repeatability

BTC Fundamental Value Hypothesis by OmegaTools is built for traders and investors who want a clean, data-driven way to interpret BTC through the lens of competing asset classes and capital flows. It is particularly effective on higher timeframes (Daily/Weekly) where macro relationships are more stable and valuation signals are less noisy.

© OmegaTools, Eros

Bitcoinprediction

BTC Valuation ZonesBTC Valuation – Distance From 200 MA

This indicator provides a simple but powerful Bitcoin valuation framework based on how far price is from the 200-period Moving Average, a level that has historically acted as Bitcoin’s long-term equilibrium.

Instead of predicting tops or bottoms, this tool focuses on mean-reversion behavior:

When price deviates too far above the 200 MA → risk increases

When price deviates deeply below the 200 MA → long-term opportunity increases

The Oracle: Dip & Top Adaptive Sniper [Hakan Yorganci]█ OVERVIEW

The Oracle: Dip & Top Adaptive Sniper is a precision-focused trend trading strategy designed to solve the biggest problem in swing trading: Timing.

Most trend-following strategies chase price ("FOMO"), buying when the asset is already overextended. The Oracle takes a different approach. It adopts a "Sniper" mentality: it identifies a strong macro trend but patiently waits for a Mean Reversion (pullback) to execute an entry at a discounted price.

By combining the structural strength of Moving Averages (SMA 50/200) with the momentum precision of RSI and the volatility filtering of ADX, this script filters out noise and targets high-probability setups.

█ HOW IT WORKS

This strategy operates on a strictly algorithmic protocol known as "The Yorganci Protocol," which involves three distinct phases: Filter, Target, and Execute.

1. The Macro Filter (Trend Identification)

* SMA 200 Rule: By default, the strategy only scans for buy signals when the price is trading above the 200-period Simple Moving Average. This ensures we are always trading in the direction of the long-term bull market.

* Adaptive Switch: A new feature allows users to toggle the Only Buy Above SMA 200? filter OFF. This enables the strategy to hunt for oversold bounces (dead cat bounces) even during bearish or neutral market structures.

2. The Volatility Filter (ADX Integration)

* Sideways Protection: One of the main weaknesses of moving average strategies is "whipsaw" losses during choppy, ranging markets.

* Solution: The Oracle utilizes the ADX (Average Directional Index). It will BLOCK any trade entry if the ADX is below the threshold (Default: 20). This ensures capital is only deployed when a genuine trend is present.

3. The Sniper Entry (Buying the Dip)

* Instead of buying on breakout strength (e.g., RSI > 60), The Oracle waits for the RSI Moving Average to dip into the "Value Zone" (Default: 45) and cross back up. This technique allows for tighter stops and higher Risk/Reward ratios compared to traditional breakout systems.

█ EXIT STRATEGY

The Oracle employs a dynamic dual-exit mechanism to maximize gains and protect capital:

* Take Profit (The Peak): The strategy monitors RSI heat. When the RSI Moving Average breaches the Overbought Threshold (Default: 75), it signals a "Take Profit", securing gains near the local top before a potential reversal.

* Stop Loss (Trend Invalidated): If the market structure fails and the price closes below the 50-period SMA, the position is immediately closed to prevent deep drawdowns.

█ SETTINGS & CONFIGURATION

* Moving Averages: Fully customizable lengths for Support (SMA 50) and Trend (SMA 200).

* Trend Filter: Checkbox to enable/disable the "Bull Market Only" rule.

* RSI Thresholds:

* Sniper Buy Level: Adjustable (Default: 45). Lower values = Deeper dips, fewer trades.

* Peak Sell Level: Adjustable (Default: 75). Higher values = Longer holds, potentially higher profit.

* ADX Filter: Checkbox to enable/disable volatility filtering.

█ BEST PRACTICES

* Timeframe: Designed primarily for 4H (4-Hour) charts for swing trading. It can also be used on 1H for more frequent signals.

* Assets: Highly effective on trending assets such as Bitcoin (BTC), Ethereum (ETH), and high-volume Altcoins.

* Risk Warning: This strategy is designed for "Long Only" spot or leverage trading. Always use proper risk management.

█ CREDITS

* Original Concept: Inspired by the foundational work of Murat Besiroglu (@muratkbesiroglu).

* Algorithm Development & Enhancements: Developed by Hakan Yorganci (@hknyrgnc).

* Modifications include: Integration of ADX filters, Mean Reversion entry logic (RSI Dip), and Dynamic Peak Profit taking.

BTC Cycle Halving Thirds NicoThe bold black vertical lines are the INDEX:BTCUSD halvings.

The background speak for itself.

Time to be bearish?

Spiderlines BTCUSD - daily/weekly📘 Documentation – Daily and Weekly Spider Lines for Bitcoin

🔹 Purpose of the Script

This script draws dynamic “Spider Lines” in the Bitcoin chart.

The lines connect certain historical candles with a reference candle and extend to the right.

These act as guideline levels that can serve as potential support or resistance zones.

🔹 How It Works

The script operates in two modes, depending on the active chart timeframe:

Weekly Mode (timeframe.isweekly)

The reference date is July 1, 2019.

The number of weeks since that date is calculated.

This defines the connection candle (connection_candle).

Several predefined offsets (e.g., +32, +34, +36 …) are added to the reference to determine starting candles.

Lines are drawn from these candles toward the connection candle.

→ Line color: green

Daily Mode (timeframe.isdaily)

Same reference date: July 1, 2019.

The number of days since that date is calculated.

Again, a connection candle is set.

A different set of offsets (e.g., +224, +238, +252 …) defines the starting candles.

Lines are drawn accordingly.

→ Line color: red

🔹 Line Logic

Each line connects:

Start → bar_index at high

End → bar_index at close

Lines are extended indefinitely to the right (extend.right).

Appearance: dashed style, width 2.

🔹 Error Handling

If a calculated candle index does not exist in the chart history (e.g., chart data does not go back far enough),

a label is plotted in the chart showing the message:

"Daily idx out of range: 252"

This way, missing lines can be diagnosed easily.

🔹 Color Convention

Weekly Spider Lines → Green

Daily Spider Lines → Red

🔹 Use Cases

Visualization of historical cyclic line patterns.

Helps in technical chart analysis: spotting potential reaction zones in price movement.

Designed mainly for long-term traders and analysts observing Bitcoin in Daily or Weekly timeframes.

🔹 Limitations

Works only on Daily and Weekly charts.

Requires chart data going back to July 1, 2019.

Based purely on fixed offsets → not a classical indicator like Moving Averages or RSI.

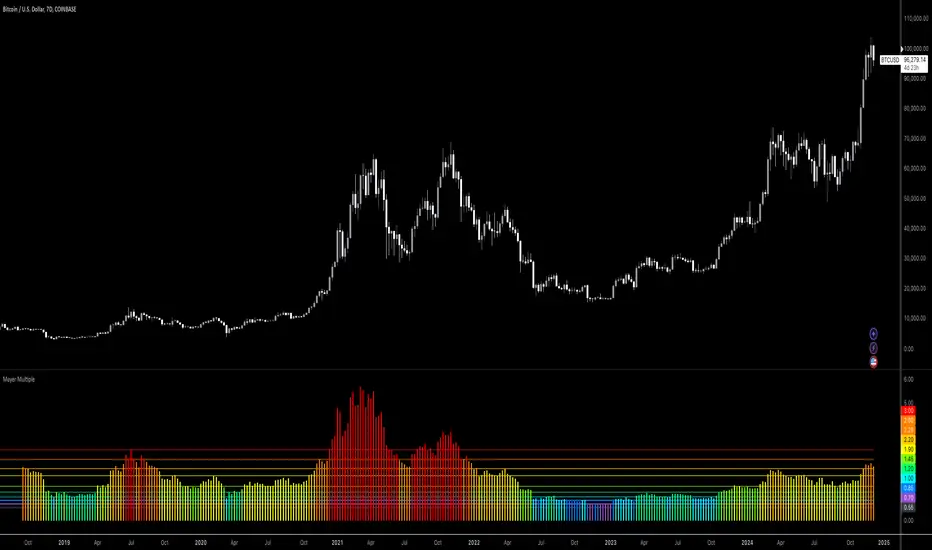

Bitcoin: Mayer MultipleMayer Multiple Indicator

The Mayer Multiple is a powerful tool designed to help traders assess market conditions and identify optimal buying or selling opportunities. It calculates the ratio between the current price and its 200-day simple moving average (SMA), visualizing key thresholds that indicate value zones, caution areas, and overheated markets.

Key Features:

Dynamic Market Zones: Clearly marked levels like "Smash Buy," "Boost DCA," and "Extreme Euphoria" to guide your trading decisions.

Customizable Input: Adjust the SMA length to fit your strategy.

Color-Coded Signals: Intuitive visualization of market sentiment for quick analysis.

Comprehensive Thresholds: Historical insights into price behavior with plotted reference levels based on probabilities.

This indicator is ideal for traders aiming to enhance their long-term strategies and improve decision-making in volatile markets. Use it to gain an edge in identifying potential turning points and managing risk effectively.

Cabal Dev IndicatorThis is a TradingView Pine Script (version 6) that creates a technical analysis indicator called the "Cabal Dev Indicator." Here's what it does:

1. Core Functionality:

- It calculates a modified version of the Stochastic Momentum Index (SMI), which is a momentum indicator that shows where the current close is relative to the high/low range over a period

- The indicator combines elements of stochastic oscillator calculations with exponential moving averages (EMA)

2. Key Components:

- Uses configurable input parameters for:

- Percent K Length (default 15)

- Percent D Length (default 3)

- EMA Signal Length (default 15)

- Smoothing Period (default 5)

- Overbought level (default 40)

- Oversold level (default -40)

3. Calculation Method:

- Calculates the highest high and lowest low over the specified period

- Finds the difference between current close and the midpoint of the high-low range

- Applies EMA smoothing to both the range and relative differences

- Generates an SMI value and further smooths it using a simple moving average (SMA)

- Creates an EMA signal line based on the smoothed SMI

4. Visual Output:

- Plots the smoothed SMI line in green

- Plots an EMA signal line in red

- Shows overbought and oversold levels as gray horizontal lines

- Fills the areas above the overbought level with light red

- Fills the areas below the oversold level with light green

This indicator appears designed to help traders identify potential overbought and oversold conditions in the market, as well as momentum shifts, which could be used for trading decisions.

Would you like me to explain any specific part of the indicator in more detail?

Bitcoin Cycle High/Low with functional Alert [heswaikcrypt]Introduction

Just as machines are fine-tuned for maximum efficiency, trading indicators must evolve to meet the demands of ever-changing markets.

Credit goes to the initial author, @NoCreditsLeft I only improved the existing Pi-cycle indicator with a functional alert and included a bull mode indicator in the script. The alert can help you get a live alert at candle close when the cycle tops, bottoms, and the potential bull phase switch occurs.

Philip Swift’s Pi Cycle Top Indicator is a brilliant example of leveraging mathematical relationships to signal critical turning points in Bitcoin’s price cycles. Historically, it has identified market and local tops with some relative accuracy, often within three days, as demonstrated in all the previous bull run cycles.

At its core, the Pi Cycle Indicator derives its name from the mathematical constant π (pi), achieved by using simple moving averages (MAs) in a specific ratio: 𝜋 = Long MA/short MA

The Bull mode switch is calculated using a crossover of the short exponentia moving average and the long moving average.

.

.

.

Knowing when Bitcoin reaches its top—and receiving timely alerts about it—is crucial for successful trading. The indicator is designed to signal;

Potential Bitcoin tops: Purple label

Potential Bitcoin bottoms : green Label, and

Parabolic swing : Yellow diamond shape (relating to the market switching to a potential bull mode)

"Please note: This indicator is tailored for Bitcoin using historical data analysis and should not be considered definitive. However accurate it might be."

Setting alerts

To set the alert conditions, select any alert function call to get alert whenever the conditions are met. The script is configured on dialy TF; you can set it on 1D or weekly TF.

Enjoy and Trade smartly

2024 - Median High-Low % Change - Monthly, Weekly, DailyDescription:

This indicator provides a statistical overview of Bitcoin's volatility by displaying the median high-to-low percentage changes for monthly, weekly, and daily timeframes. It allows traders to visualize typical price fluctuations within each period, supporting range and volatility-based trading strategies.

How It Works:

Calculation of High-Low % Change: For each selected timeframe (monthly, weekly, and daily), the script calculates the percentage change from the high to the low price within the period.

Median Calculation: The median of these high-to-low changes is determined for each timeframe, offering a robust central measure that minimizes the impact of extreme price swings.

Table Display: At the end of the chart, the script displays a table in the top-right corner with the median values for each selected timeframe. This table is updated dynamically to show the latest data.

Usage Notes:

This script includes input options to toggle the visibility of each timeframe (monthly, weekly, and daily) in the table.

Designed to be used with Bitcoin on daily and higher timeframes for accurate statistical insights.

Ideal for traders looking to understand Bitcoin's typical volatility and adjust their strategies accordingly.

This indicator does not provide specific buy or sell signals but serves as an analytical tool for understanding volatility patterns.

Leonid's Bitcoin Sharpe RatioThe Sharpe ratio is an old formula used to value the risk-adjusted return of an asset. It was developed by Nobel Laureate William F. Sharpe. In this case, I have applied it to Bitcoin with an adjustable look-back date.

The Sharpe Ratio shows you the average return earned after subtracting out the risk-free rate per unit of volatility (I've defaulted this to 0.02 ).

Volatility is a measure of the price fluctuations of an asset or portfolio. Subtracting the risk-free rate from the mean return allows you to understand what the extra returns are for taking the risk.

If the indicator is flashing red, Bitcoin is temporarily overbought (expensive).

If the indicator is flashing green, Bitcoin is temporarily oversold (cheap).

The goal of this indicator is to signal out local tops & bottoms. It can be adjusted as far as the lookback time but I have found 25-26 days to be ideal.

E9 PLRRThe E9 PLRR (Power Law Residual Ratio) is a custom-built indicator designed to evaluate the overvaluation or undervaluation of an asset, specifically by utilizing logarithmic price data and a power law-based model. It leverages a dynamic regression technique to assess the deviation of the current price from its expected value, giving insights into how much the price deviates from its long-term trend.

This indicator is primarily used to detect market extremes and cycles, often used in the analysis of long-term price movements in assets like Bitcoin, where cyclical behavior and significant price deviations are common.

This chart is back from 2019 and shows (From left to right) 2018 Bear market bottom at $3.5k (Dark Blue) , following a peak at 12k (dark red) before the Covid crash back down to EUROTLX:4K (Dark blue)

Key Components

Logarithmic Price Data:

The indicator works with logarithmic price data (ohlc4), which represents the average of open, high, low, and close prices. The logarithmic transformation is crucial in financial modeling, especially when analyzing long-term price data, as it normalizes exponential price growth patterns.

Dynamic Exponent 𝑘:

The model calculates a dynamic exponent k using regression, which defines the power law relationship between time and price. This exponent is essential in determining the expected power law price return and how far the current price deviates from that expected trend.

Power Law Price Return:

The power law price return is computed using the dynamic exponent

k over a defined period, such as 365 days (1 year). It represents the theoretical price return based on a power law relationship, which is used to compare against the actual logarithmic price data.

Risk-Free Rate:

The indicator incorporates an adjustable risk-free rate, allowing users to model the opportunity cost of holding an asset compared to risk-free alternatives. By default, the risk-free rate is set to 0%, but this can be modified depending on the user's requirements.

Volatility Adjustment:

A key feature of the PLRR is its ability to adjust for price volatility. The indicator smooths out short-term price fluctuations using a moving average, helping to detect longer-term cycles and trends.

PLRR Calculation:

The core of the indicator is the calculation of the Power Law Residual Ratio (PLRR). This is derived by subtracting the expected power law price return and risk-free rate from the logarithmic price return, then multiplying the result by a user-defined multiplier.

Color Gradient:

The PLRR values are represented visually using a color gradient. This gradient helps the user quickly identify whether the asset is in an undervalued, fair value, or overvalued state:

Dark Blue to Light Blue: Indicates undervaluation, with increasing blue tones representing a higher degree of undervaluation.

Green to Yellow: Represents fair value, where the price is aligned with the expected power law return.

Orange to Dark Red: Indicates overvaluation, with increasing red tones representing a higher degree of overvaluation.

Zero Line:

A zero line is plotted on the indicator chart, serving as a reference point. Values above the zero line suggest potential overvaluation, while values below indicate potential undervaluation.

Dots Visualization:

The PLRR is plotted using dots, with each dot color-coded based on the PLRR value. This dot-based visualization makes it easier to spot significant changes or reversals in market sentiment without overwhelming the user with continuous lines.

Bar Coloring:

The chart’s bars are colored in accordance with the PLRR value at each point in time, making it visually clear when an asset is potentially overvalued or undervalued.

Indicator Functionality

Cycle Identification : The E9 PLRR is especially useful for identifying cyclical market behavior. In assets like Bitcoin, which are known for their boom-bust cycles, the PLRR can help pinpoint when the market is likely entering a peak (overvaluation) or a trough (undervaluation).

Overvaluation and Undervaluation Detection: By comparing the current price to its expected power law return, the PLRR helps traders assess whether an asset is trading above or below its fair value. This is critical for long-term investors seeking to enter the market at undervalued levels and exit during periods of overvaluation.

Trend Following: The indicator helps users identify the broader trend by smoothing out short-term volatility. This makes it useful for both momentum traders looking to ride trends and contrarian traders seeking to capitalize on market extremes.

Customization

The E9 PLRR allows users to fine-tune several parameters based on their preferences or specific market conditions:

Lookback Period:

The user can adjust the lookback period (default: 100) to modify how the moving average and regression are calculated.

Risk-Free Rate:

Adjusting the risk-free rate allows for more realistic modeling of the opportunity cost of holding the asset.

Multiplier:

The multiplier (default: 5.688) amplifies the sensitivity of the PLRR, allowing users to adjust how aggressively the indicator responds to price movements.

This indicator was inspired by the works of Ashwin & PlanG and their work around powerLaw. Thank you. I hall be working on the calculation of this indicator moving forward to make improvements and optomisations.

Bitcoin wave modelBitcoin wave model is based on the logarithmic regression model and the sinusoidal waves, induced by the halving events.

This chart presents the outcome of an in-depth analysis of the complete set of Bitcoin price data available from October 2009 to August 2023.

The central concept is that the logarithm of the Bitcoin price closely adheres to the logarithmic regression model. If we plot the logarithm of the price against the logarithm of time, it forms a nearly straight line.

The parameters of this model are provided in the script as follows: log (BTCUSD) = 1.48 + 5.44log(h).

The secondary concept involves employing the inherent time unit of Bitcoin instead of days:

'h' denotes a slightly adjusted time measurement intrinsic to the Bitcoin blockchain. It can be approximated as (days since the genesis block) * 0.0007. Precisely, 'h' is defined as follows: h = 0 at the genesis block, h = 1 at the first halving block, and so forth. In general, h = block height / 210,000.

Adjustments are made to account for variations in block creation time.

The third concept revolves around investigating halving waves triggered by supply shock events resulting from the halvings. These halvings occur at regular intervals in Bitcoin's native time 'h'. All halvings transpire when 'h' is an integer. These events induce waves with intervals denoted as h = 1.

Consequently, we can model these waves using a sin(2pih - a) function. The parameter determining the time shift is assessed as 'a = 0.4', aligning with earlier expectations for halving events and their subsequent outcomes.

The fourth concept introduces the notion that the waves gradually diminish in amplitude over the progression of "time h," diminishing at a rate of 0.7^h.

Lastly, we can create bands around the modeled sinusoidal waves. The upper band is derived by multiplying the sine wave by a factor of 3.1*(1-0.16)^h, while the lower band is obtained by dividing the sine wave by the same factor, 3.1*(1-0.16)^h.

The current bandwidth is 2.5x. That means that the upper band is 2.5 times the lower band. These bands are forming an exceptionally narrow predictive channel for Bitcoin. Consequently, a highly accurate estimation of the peak of the next cycle can be derived.

The prediction indicates that the zenith past the fourth halving, expected around the summer of 2025, could result in prices ranging between 200,000 and 240,000 USD.

Enjoy the mathematical insights!

Bitcoin Economics Adaptive MultipleBEAM (Bitcoin Economics Adaptive Multiple) is an indicator that assesses the valuation of Bitcoin by dividing the current price of Bitcoin by a moving average of past prices. Its purpose is to provide insights into whether Bitcoin is under or overvalued at any given time. The thresholds for the buy and sell zones in BEAM are adjustable, allowing users to customize the indicator based on their preferences and trading strategies.

BEAM categorizes Bitcoin's valuation into two distinct zones: the green buy zone and the red sell zone.

Green Buy Zone:

The green buy zone in BEAM indicates that Bitcoin is potentially undervalued. Traders and investors may interpret this zone as a favorable buying opportunity. The threshold for the buy zone can be adjusted to suit individual preferences or trading strategies.

Red Sell Zone:

The red sell zone in BEAM suggests that Bitcoin is potentially overvalued. Traders and investors may consider selling their Bitcoin holdings during this zone to secure profits or manage risk. The threshold for the sell zone is adjustable, allowing users to adapt the indicator based on their trading preferences.

Methodology:

BEAM calculates the indicator value using the following formula:

beam = math.log(close / ta.sma(close, math.min(count, 1400))) / 2.5

The calculation involves taking the natural logarithm of the ratio between the current price of Bitcoin and a simple moving average of past prices. The moving average period used is a minimum of the specified count or 1400, providing a suitable historical reference for valuation assessment.

The resulting value of BEAM provides a standardized measure that can be compared across different time periods. By adjusting the thresholds for the buy and sell zones, users can customize BEAM to their preferred levels of undervaluation and overvaluation.

Utility:

BEAM serves as a tool for investors in the Bitcoin market, offering insights into Bitcoin's valuation and potential buying or selling opportunities. By monitoring BEAM, market participants can gauge whether Bitcoin is potentially undervalued or overvalued, helping them make informed decisions regarding their Bitcoin positions.

It is important to note that BEAM should be used in conjunction with other technical and fundamental analysis tools to validate signals and avoid relying solely on this indicator for trading decisions. Additionally, traders and investors are encouraged to adjust the threshold values based on their specific trading strategies, risk tolerance, and market conditions.

Credit: The BEAM (Bitcoin Economics Adaptive Multiple) indicator was originally developed by BitcoinEcon

Bitcoin Limited Growth ModelThe Bitcoin Limeted Growth is a model proposed by QuantMario that offers an alternative approach to estimating Bitcoin's price based on the Stock-to-Flow (S2F) ratio. This model takes into account the limitations of the traditional S2F model and introduces refinements to enhance its analysis.

The S2F model is commonly used to analyze Bitcoin's price by considering the scarcity of the asset, measured by the stock (existing supply) relative to the flow (new supply). However, the LGS-S2F Bitcoin Price Formula recognizes the need for improvements and presents an updated perspective on Bitcoin's price dynamics.

Invalidation of the Normal S2F Model:

The normal S2F model has faced criticisms and challenges. One of the limitations is its assumption of a linear relationship between the S2F ratio and Bitcoin's price, overlooking potential nonlinearities and other market dynamics. Additionally, the normal S2F model does not account for external influences, such as market sentiment, regulatory developments, and technological advancements, which can significantly impact Bitcoin's price.

Addressing the Issues:

The LGS-S2F Bitcoin Price Formula introduces refinements to address the limitations of the traditional S2F model. These refinements aim to provide a more comprehensive analysis of Bitcoin's price dynamics:

Nonlinearity: The LGS-S2F model recognizes that the relationship between the S2F ratio and Bitcoin's price may not be linear. It incorporates a logistic growth function that considers the diminishing returns of scarcity and the saturation of market demand.

Data Analysis: The LGS-S2F model employs statistical analysis and data-driven techniques to validate its predictions. It leverages historical data and econometric modeling to support its analysis of Bitcoin's price.

Utility:

The LGS-S2F Bitcoin Price Formula offers insights for traders and investors in the cryptocurrency market. By incorporating a more refined approach to analyzing Bitcoin's price, this model provides an alternative perspective. It allows market participants to consider various factors beyond the S2F ratio alone, potentially aiding in their decision-making processes.

Key Features:

Adjustable Coefficients

Sigma calculation methods: Normal or Stdev

Credit:

The LGS-S2F Bitcoin Price Formula was developed by QuantMario, who has contributed to the field of cryptocurrency analysis through their research and modeling efforts.

MA Multiplier with FibonacciThis implementation of the "2-Year MA Multiplier" gives you some control over the indicator, you can change the multiplier from it's default of 5, you can change the lookback from it's default of 730 days and I've also added three fibonacci traces between the moving average and it's multiple that you can play with. Oh and you can also choose the data source ('close' or 'hl2' make most sense).

The formula for this indicator was created by Philip Swift.

Thanks to @Pladizow for pointing me to this indicator.

BTC Fibonacci DMA350 TrendlinesAdapted from Tim Graham's Code.

See Original Inspiring Article from Phillip Swift at: @positivecrypto

When looking into BITSTAMP:BTCUSD 1D data in spreadsheet. Historically, BTC Highs Hit (Simple Daily Moving Average 350 Days) DMA350 in reverse Fibonacci Sequence Order

2013 Hit DMA350*8 before All Time High (ATH)

2017 Hit DMA350*5 before ATH

I expect 2021 to hit DMA350*3 ATH. When BTC hits DMA350*3 ATH, I suggest selling!