BTC-D

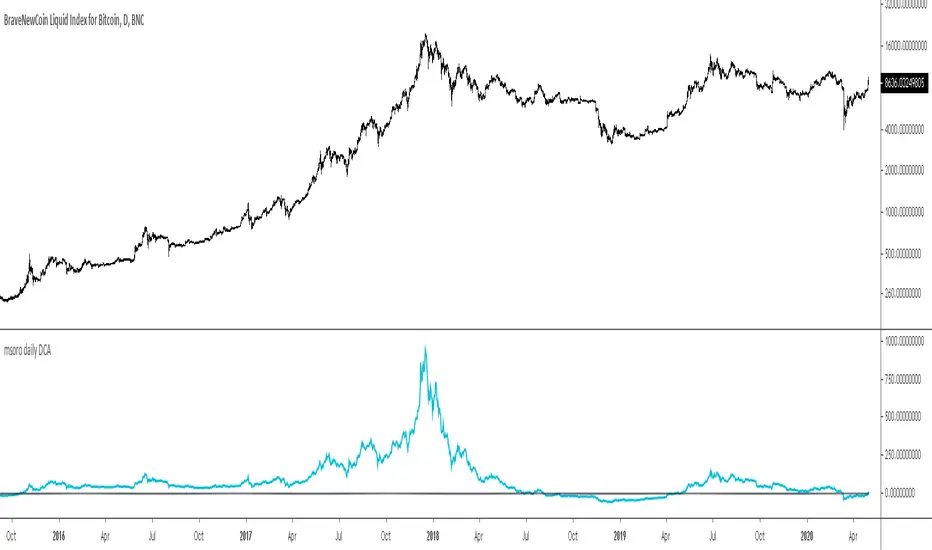

msoro daily DCATool to estimate PnL of your investment if you put in a fixed $ amount daily into btc for past year. It takes input as 365 days which can be changed as per need.

Bitcoin Implied VolatilityThis simple script collects data from FTX:BVOLUSD to plot BTC’s implied volatility as a standalone indicator instead of a chart.

Implied volatility is used to gauge future volatility and often used in options trading.

Crypto Market CorrelationThis script utilized some new functions in Pine Script, which compares the correlation between the current symbol to a basket of crypto indexes that are listed on the FTX exchange.

By tracking these indexes we can gauge the reaction across markets that have a different market cap. By that I mean we can have a better idea about where the money is flowing into a specific market.

This script uses data from FTX:BTCPERP, FTX:ALTPERP, FTX:MIDPERP, FTX:SHITPERP, FTX:EXCHPERP, FTX:DRGNPERP.

A value closer to 1 equals to more correlation, closer to 0 equals to less correlation.

eha MA CrossIn the study of time series, and specifically technical analysis of the stock market, a moving-average cross occurs when, the traces of plotting of two moving averages each based on different degrees of smoothing cross each other. Although it does not predict future direction but at least shows trends.

This indicator uses two moving averages, a slower moving average and a faster-moving average. The faster moving average is a short term moving average. A short term moving average is faster because it only considers prices over a short period of time and is thus more reactive to daily price changes.

On the other hand, a long term moving average is deemed slower as it encapsulates prices over a longer period and is more passive. However, it tends to smooth out price noises which are often reflected in short term moving averages.

There are a bunch of parameters that you can set on this indicator based on your needs.

Moving Averages Algorithm

You can choose between three types provided of Algorithms

Simple Moving Average

Exponential Moving Average

Weighted Moving Average

I will update this study with more educational materials in the near future so be informed by following the study and let me know what you think about it.

Please hit the like button if this study is useful for you.

eha Moving Averages StrategyMoving Average based strategies are very popular ones among both long-term investors and short-term traders as they can be tailored to any time frame. One of the main moving average strategies are crossovers. The very simple type is a price crossover , which is when the price crosses above or below a moving average to signal a potential change in trend.

Another strategy is to apply two moving averages to a chart: one longer (or slow) and one shorter (or fast). When the shorter-term MA crosses above the longer-term MA, it's a buy signal, as it indicates that the trend is shifting up (also known as “ Golden Cross ”). Meanwhile, when the shorter-term MA crosses below the longer-term MA, it's a sell signal, as it indicates that the trend is shifting down (which is also known as “ Dead/Death Cross ”).

This is a study to find a suitable trading strategy for 4-6 hour time frames. As you can see the performance is currently very poor. It has just generated almost 90 trades in a very long period from January 2017 to the time of publishing the study for the first time.

Moving averages work quite well in strong trending conditions but poorly in choppy or ranging conditions. Adjusting the time frame can correct this problem temporarily, although, at some point, these issues are likely to occur regardless of the time frame chosen for the moving average(s).

I am working on this basic strategy to make its performance better and I will update the post in the future. So keep in touch by following the post.

Why have I republished my study?

It sounds like TradingView stores and indexes scripts based on the title of the post rather than the actual title of the scripts and if one chose general terms as the title of the post, the TradingView script search engine may be unable to find it. So I decided to repost the strategy with a more searchable and unique prefix of " eha ".

Please provide me with your precious feedback.

Cryptocurrency Spot RatesThis is an overlay indicator on the chart that will plot cryptocurrency spot prices of the following exchanges:

- Coinbase

- Poloniex

- OKCOIN

- Binance

- Huobi

- Bittrex

- HitBTC

- Kraken

- Bitfinex

Additionally it plots the price average of all those exchanges.

This overlay is intended to be used on charts with derivatives/futures such as BitMEX/Deribit/...

It works with all USD and Tether pairs on the main chart (for example BTCUSD, ETHUSD, BCHUSD,...)

XBT % ContangoSimilar to my other indicators, but measures XBTUSD Contango in terms of percent.

Also, built it so you could change the values that give the red and green signals. Default values are 0% or less (backwardation) indicates green. However, i found that a 0.5% setting worked will finding local bottoms for current contract of XBTH20 (March 2020). The upper value default is at 5%, and signals red when the next contract reaches over 5%.

My assumption is as BTC increases in value over time, measuring contango in terms of percent will be a better measure of the XBT futures curve.

Ichimoku Clouds Strong Bullish/Bearish signals and alertsIchimoku Clouds Strong Bullish/Bearish signals with allerts

The Ichimoku cloud was developed by Goichi Hosoda, a Japanese journalist, and published in the late 1960s. It provides more data points than the standard candlestick chart. While it seems complicated at first glance, those familiar with how to read the charts often find it easy to understand with well-defined trading signals.

We provide you easy-to-use script which helps to decrypt meaning of lines in the indicator. The script takes Ichimoku clouds indicator formulas to calculate Tenkan, Kijun, SenkouA, SenkouB values and examines them in order to produce buy ( Bullish ) and sell ( Bearish ) signals which are displayed at the chart

The most appropriate time frame is 30m

Custom alerts are added to send you a notice with a webhook when bullish or bearish signal arrives.

You can easily add weak and neutral signals alerts by removing "//" in a specified place

Feel free to copy and use this script for your ideas and trading. You can modify the script by adding Parabolic SAR in order to increase accuracy of positions closure

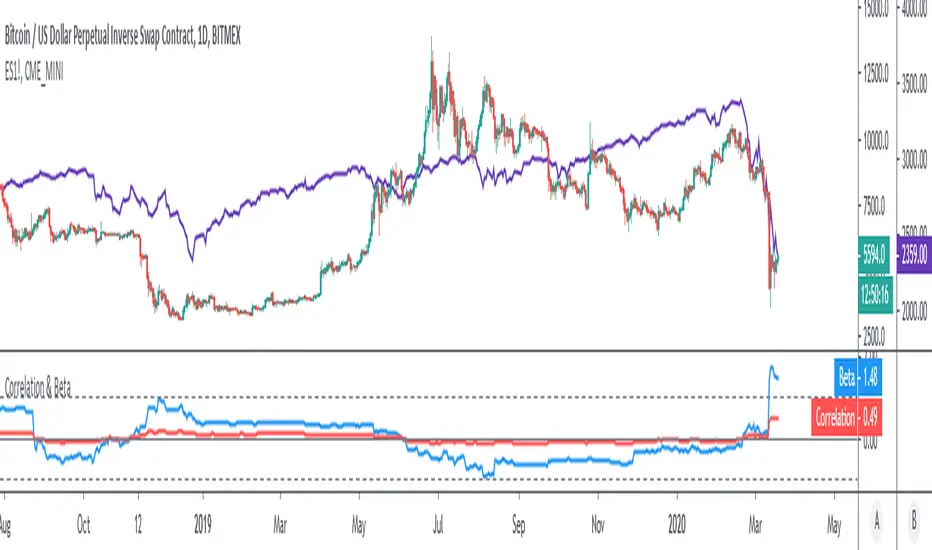

VIX MonitorSimple VIX Monitor to track spikes.

Spikes in VIX are often followed by big moves up in stocks.

Useful when paired with "Correlation & Beta" Indicator.

For Bitcoin Traders: when Bitcoin is highly correlated to Stocks (such as now) it could be a good opportunity for a short-term long trade.

Correlation & BetaDisplay the correlation coefficient and/or Beta of an asset to a specified market.

Options to:

- Specify market (S&P500 futures by default)

- Display one or other metrics

- Modify assessment period (200 bars by default)

- Calculate on price, returns or log-returns

Bitcoin Worse DaysHello, here is a simple script to scan for BTC worse days.

In input you tell the script what are the minimum percent drops to look for.

By default it is 0.3, here I set it at 0.25 or it would not show anything except the 12 March (which is 40.07%).

The indicator has a precision of 1% I think.

It does not look at how low the body closed, it will show all days that closed below where they opened looking at how far below the high of the day the low was.

It can also work on any timeframe.

Here were the previous worse days from the late 2017 crash start of the bear market:

You could modify the script and look for the worse bodies with open - close instead of high - low

You could also add a filter to only look at days where the body is > 90% the whole candle (in this case it's got to be about 99%)

We can look back at BTC past a bit

Every bear market started with a large drop so we can expect...

As you can see we can look at the weekly chart too:

I won't lie, I am pretty happy. Russia, China bat eating community, and Greta were a big help. Thanks guys.

BTC FS Diff / Percentage (XBTH20)Shows price difference by a percentage of future (BITMEX:XBTH20) and spot index (BITMEX:XTB) .

Bitcoin CME Gaps [NeoButane]Simple script that checks for gaps in price from CME. tickerid(x, y, sess) doesn't seem to be applying correctly for the ticker specified at the moment so there are a couple of 'gaps' peppered on lower timeframes.

Gaps are legitimate price levels to look as a support or resistance. The theory is that volume needs to be gap filled, but I currently believe it's an easy entry/exit trade for those who can move the market. I don't think there is sound analysis behind the why, but it is real.

Intraday S/RPlots yesterday's low and high, and the current day's open, as intraday support/resistance levels.

Bitcoin East vs WestPlots the volume weighted price difference between the top spot exchanges in the "East" (Asian markets) versus the "West" (US/UK/EU markets).

Optional: view the volume difference between the two.

Deadband cross detection for BTC (XBT)Description: meant to be used with BTCUSD (or XBTUSD ) on 3 mins to 1h candles charts.

Idea is to provide a tool to detect break-out's from a dead band around an EMA, and to detect back-in's to the dead band.

Detection is fundamentally based on how much %, at least, a certain candle body has ruptured the dead band (adjustable).

Long and short flags are placed on the chart, as well as the deadband. Can be used to generate alers.

With minimal modifications, can be convert to a Strategy script.

Following are ideas to play around if you want. Room for improvements:

- convert constants into inputs, and diversify thresholds assimetrically

- play around with wether or not using pyramiding (here pyramiding is blocked)

- look at several bars in a sequence, not only current

Bitcoin Halving CountdownHello traders,

I offer you today the BTC halving countdown updated in real-time on your charts

I inspired myself greatly from the gentleman @everget's script LTC halving countdown below

(

The countdown date is coming from that source www.bitcoinblockhalf.com.

The halving date is estimated to be around May 13th, 2020 .

That date is hardcoded in the script and is used for the countdown calculation.

The Bitcoin block mining reward halves every 210,000 blocks, the coin reward will decrease from 12.5 to 6.25 coins.

Enjoy the weekend

Dave

Bitcoin Stock to FlowModeling Bitcoin's Value With Scarcity

The Stock to Flow model for Bitcoin suggests that Bitcoin price is driven by scarcity over time.

Bitcoin is the first scarce digital object the world has ever seen. It is scarce like silver & gold, and can be sent over the internet, radio, satellite etc. Bitcoin includes a mathematical mechanism to restrict its supply over time making it more rare as time goes on. Digital Scarcity.

In 2017 BTC exceeded the market capitalization of Silver. After the next halving in 2024, Bitcoin will become the hardest asset the world has ever seen, rarer than Gold.

There is only enough Bitcoin in the world for each person to own .0023 BTC. Because of this, Bitcoin's value should continue to rise over time.

BTC Transaction/On-Chain Volume (Basic)Description:

Whale: Whale utilizing discounted prices (increasing on-chain volume & decreasing price)

Recovering: Positive momentum in price after potential whale activity

Cycle Volume Support: The transaction volume support during a cycle

What’s the best time to invest?

After institutions make up their mind at low price levels.

How’s on-chain volume related to whales or institutional money?

On-chain volume is contributed not only by using BTC as payment methods, but more importantly by large custodians using the BTC chain to settle internal whale trades. When OTC volume is estimated 2-3 times of exchange volume, and when total on-chain volume is only a small fraction of the exchange volume, the OTC settlement plays a big factor in moving the on-chain volume around.

Why does the price drop further after spotting whale money?

Does new money equal higher true value? Yes.

Does new money equal higher price? No.

Whales could not only ladder in when they see the price on discount, but also push the price further down to accumulate at better price levels. However, either route chosen, it’s most likely for the price to rise to a higher level compared to the level when the whales enter. Whales are here to make money after all.

ANN BTC MTF CM Sling Shot SystemHi all, this script was created as a result of ANN training in all time frames of bitcoin data.

Trained data is built on Chris Moody's Sling Shot system.

CM Sling Shot System :

This system automatically generates the ANN output for all time periods.

Therefore, it has multi-time-frame feature.

Artificial Neural Networks training details:

Average Errors

1 minute = 0.005570

3 minutes = 0.006674

5 minutes = 0.007067

15 minutes = 0.010000

30 minutes = 0.009398

45 minutes = 0.010000

1 Hour = 0.006848

2 Hours = 0.006901

3 Hours = 0.009608

4 Hours = 0.009774

1 Day = 0.010000

1 Week = 0.010000

The results look good (All Average Error <= 0.01 ), the Sling Shot Method is also good, but you can also refer to historically slower period averages to filter these arrows a bit more. I leave the decision to you.

Best regards.

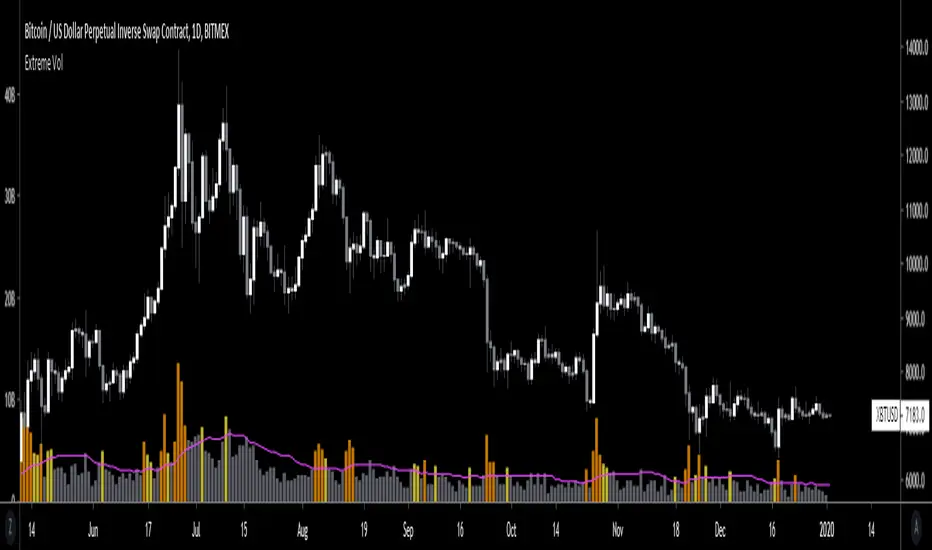

Extreme VolumeThis indicator colors volume bars that are significantly higher volume than the vol moving average ( SMA ). Utilizes two multiplier that can be adjusted by user. Defaults are that the indicator colors volume bars yellow if 20% higher than average, and orange if over 50% higher than average.

Reason why i created this indicator is i typically don't care about volume unless it is significantly higher than average. I find extreme volume useful for confirmation of a breakout, etc. This is why the rest of the volume bars are gray, they are still available for reference, but I dont pay much attention until volume is higher than average.

Also, when you load this indicator it will be in its own pane below the chart. To try and figure out how to add it to same pane as the chart was a huge pain in the ass. Once you figure it out it is pretty easy. I'll try to explain below...

Next to the indicator name you have the following options ... Hide, Settings, Show Source Code{}, Delete(X), and More (3 dots)

1) Click on "More" (3 dots)

2) Click on "Move To" then chose "Existing Pane Above"

3) Volume will likely be too large. Volume scale should be on left side, use your mouse to adjust volume smaller

4) Volume will likely be in the middle of your chart, click on it and drag it down.