BTC perpetual swaps volumeIndicator with aggregated volume for all the most actively traded bitcoin perpetual swaps.

Can be denominated in either US dollars or the number of coins traded.

Can be displayed as stacked volume or an index that shows the percentage market share each contract has.

In the settings you can exclude any contract so that it only shows the individual and total volume of the markets you're interested in.

"Linear" or "inverse" refers to the type of perpetual swap contract it is.

Inverse contracts use coin margin, so in this case BTC.

Linear contracts use some type of dollar equivalent margin like USDT for example.

The margin is always specified for the linear contracts.

It's public and free for anyone to use.

BTC-D

Heiken Ashi & Super TrendThis is one of my open source 1h strategies

It works on Binance: BTCUSDTPERP charts

This strategy involves two indicators

1. Heiken Ashi - a typical technical indicator to help highlight and clarify the current trend. This somehow allows the chart to ignore unnecessary fluctuations and make the trend more visible.

2.Super Trend - - One of the most common ATR-based indicators, the SuperTrend indicator is useful to help you catch big trends.

Buy entry conditions are as follows.

1. The Super Trend indicator running on the Heiken Ashi chart gives a buy signal.

2. Buy at the current market price and take profit at 1% of the normal k-line at this time.

Take profit

TP - 1%

Stop Loss

None

Auto Fibonacci Levels + Auto Trend Line generatorAnother indicator for you guys!!!

This indicator consists of the 5 key Fibonacci retracement levels, plotted automatically to user input settings. I also have included an auto support/resistance trend line generator.

What is a Fibonacci retracement?

'Fibonacci retracement is a method of technical analysis for determining support and resistance levels. It is named after the Fibonacci sequence of numbers, whose ratios provide price levels to which markets tend to retrace a portion of a move before a trend continues in the original direction.' - Wikipedia

How to use the Fibonacci retracement?

- The Fibonacci levels are default. These percentiles from price to the average of the high in a sample and low in a sample give you a guideline of where a bottom may be, where a top may be, and where a range is being created.

- Look for the price to reject from 61.8% and 76.4%, and also look for price to bounce from 38.2% and 23.6%. If a lower low/higher high is made, the fib levels will follow and the percentiles within will be recalculated after a 5 candle offset period.

- If you see price trending towards the lower percentiles (38&23) and using the 50% as resistance, look for a break downwards and vice versa.

-This Fibonacci set as all others is subject to fake-out, always use this with another series indicator, or don't use it as a signal for entry at all (unless you have a backdated strategy)

How to use the trend line generator?

-The trend line generator will only plot when a lower low/higher high has taken place within the input amount of candles. It is also offset by a user amount.

-The check box will give the option to have the trend line's plot or not.

- If you see a green/red dot it means that that will be your first coordinate for the trend line, and until the computations are complete it will give you an idea of which direction it will be in (resistance or support)

-When opening this indicator zoom out all the way to connect any trend lines that do not load automatically.

Let me know if you have any questions, suggestions or issues! Thank you everyone!

-Cheatcode1 :)

SP:SPX TVC:DXY BMFBOVESPA:EUR1! CME:BTC1! BINANCE:BTCUSDT

Volume Buy/Sell (by iammaximov)Buy/Sell Volume

Buy/Sell volume based on total bar amplitude (high/low price) and close/open (for calculate vbuy > vsell or vbuy < vsell)

Bitfinex Shorts StratOverview

This strat applies the data from BITFINEX:USDSHORTS to the RSI indicator in order to provide SHORT/LONG entries as the number of contracts goes up and down. Although Bitfinex has lost relevance over the years its generally considered an exchange dominated by smart money rather than retail. I'd like to see if any insights can be gained by following their trading behaviour.

How to use

Select the underlying security you wish to trade and load the indicator. Select the appropriate short security by searching in the Bitfinex Short Symbol. RSI settings apply to short symbol not the actual asset. Strategy shorts the underlying asset when shorts rise and longs when they drop. The shorts symbol will follow the value of the loaded chart. Works best on 4 hour chart.

Why use shorts only rather than both long/shorts?

Bitfinex longs seem to be on a long-term uptrend accounting for 25x the number of shorts. Might be enormous confidence on part of the whales, but more likely reflects selling spot and buying perp. Given the size disparity and price action I don't think longs info is adding much.

Problems with script:

a) We don't really know the intentions of short players (e.g. speculation or hedging spot)

b) The script uses a decline in shorts as a long signal

c) RSI is a blunt tool there are probably better options for calculating high/lows in shorts

d) Shorts are accumulated both at highs and also when BTC price is already heavily trending down. This suggests some are speculative (at the highs) or protective/hedging during a decline

Takeaways:

Based on this strat Bitfinex whales are more wrong than right.

Results don't carry across well into altcoins using the accompanying short symbol. However, what is interesting is that applying the BITFINEX:BTCUSDSHORTS to altcoin charts does work pretty well.

Strat needs some refinement to control for entries under different circumstances.

Probably not a great idea to use this as a strategy in isolation, but highlights how Bitfinex whale behaviour is a good gauge to follow.

Directional Index Macro IndicatorWhat is This For?

The default settings for this indicator are for BINANCE:BTCUSDT and intended to be used on the 3D timeframe to identify market trends. This indicator does a great job identifying whether the market is bullish, bearish, or consolidating. This can also work well on lower time frames to help identify when a trend is strong or when it's reversing.

Directional Index Rate of Change

Core to this indicator is the rate at which DI+ and DI- are moving away or towards each other. This is called The Rate of Change (ROC). "The ROC length dictates how many bars back you want to compare to the current bar to see how much it has changed. It is calculated like this:

(source - source /source ) * 100"

The rate of change is smoothed using an EMA. A shorter EMA length will cause the ROC to flip back and forth between positive and negative while a larger EMA length will cause the ROC to change less often. Since the rate of change is used to indicate periods of 'consolidation', you want to find a setting that doesn't flip back and forth too often. Between the DI+ and DI- is a blue centerline. Offset from this centerline is a channel that is used to filter out false crosses of the DI+ and DI-. Sometimes, the DI+ and DI- lines will come together in this channel and cross momentarily before resuming the direction prior to the cross. When this happens, you don't want to flip your bias too soon. The wider the channel, the later the indicator will signal a DI reversal. A narrower channel will call it sooner but risks being more choppy and indicating a false cross.

Indicator Status Line

This indicator has 4 values in the status line (in order):

DI+

DI-

Distance between DI+ and DI-

DI Rate of Change ( how quickly are DI+ and DI- moving away or towards center )

Indicator Plots

This indicator plots DI+ (green), DI- (red), and a center channel between DI- and DI+. Across the top of the indicator, red and green triangles indicate the market trend while the background changes to show whether the price is in an impulse wave or consolidating. This makes up 4 possible scenarios:

Bullish impulse wave ( green triangle up + green background )

Bullish consolidation ( green triangle up + yellow background )

Bearish impulse wave ( red triangle down + red background )

Bearish consolidation ( red triangle down + yellow background )

Summary

Combined with support and resistance levels, volume, and your other favorite indicators, this can be a useful tool for validating that your entries are not going against the trend.

Disclaimer

This is not financial advice. Do not take trades only based on the DI+ and DI- crossing. Always use multiple indicators to validate your entries and never take a trade when you aren’t emotionally grounded. Have a plan. Stick to the plan.

The screenshot for this strategy is of a manual historical review of BTC on the 3 day chart. The indicator was built to try and mimic the chart above. You’ll see that it nails it sometimes, is a little late sometimes, and chops around between consolidation and impulse waves when it should stay in consolidation. Share your settings if you are able to improve the choppiness without sacrificing catching the reversals early.

Blockchain Fundamentals - Active Address Sentiment Osc. [CR]Blockchain Fundamentals: Active Address Sentiment Oscillator AASO

Back with another script today, this one is a useful tool in helping to determine bitcoins value. We are looking at 2 data sources: the daily active addresses on the BTC blockchain, and the daily returns of BTC.

THIS INDICATOR WILL ONLY GIVE YOU THE CORRECT RESULTS ON THE DAILY TIMEFRAME

There is an interesting relationship that you can see by comparing the two timeseries. But for us to create a good indicator we first need to normalize the data. So we look at the percent change over the past 28 days for each metric (DAA and price).

THIS INDICATOR WILL ONLY GIVE YOU THE CORRECT RESULTS ON THE DAILY TIMEFRAME

We then calculate standard deviation bands around the DAA metric. We finalize them by averaging the bands over a 28 day period.

When the Price series (yellow line) is higher than the SD bands BTC is considered overvalued or price is overheated. A pullback could be expected soon. When the Price series is below the SD bands BTC is considered undervalued or price is oversold.

THIS INDICATOR WILL ONLY GIVE YOU THE CORRECT RESULTS ON THE DAILY TIMEFRAME

This tool doesnt give signals on the one minute chart or tell you exactly when to buy or sell. BUT what it does do is act as a convenient macro sentiment indicator that is not based completely upon price.

In an attempt to narrow down the really juicy areas, if you seen the background color highlights with white, that means its likely a top or bottom. At the very least on a local sense and many times in a cyclical macro sense as well. It also narrows down the signal to a generally more profitable area.

This indicator is not meant to be used on timeframes other than daily (did I mention that already?). I am lazy and did not code the calculations to be MTF (which is why you have to use on the daily chart). If you want to code this, please forward it on to me and I will post an update with a heartfelt credit to you.

Fast v Slow Moving Averages Strategy (Variable) [divonn1994]This is a simple moving average based strategy that takes 2 moving averages, a Fast and a Slow one, plots them both, and then decides to enter a 'long' position or exit it based on whether the two lines have crossed each other. It goes 'long when the Fast Moving Average crosses above the Slow Moving Average. This could indicate upwards momentum in prices in the future. It then exits the position when the the Fast Moving Average crosses back below. This could indicate downwards momentum in prices in the future. This is only speculative, though, but sometimes it can be a very good indicator/strategy to predict future action.

I've tried some strategy settings and I found different promising strategies. Here are a few:

BTCUSD ( BitStamp ) 1 Day Timeframe : EMA, Fast length 25 bars, Slow length 62 bars => 28,792x net profit (default)

BTCUSD ( BitStamp ) 1 Day Timeframe : VWMA, Fast length 21 bars, Slow length 60 bars => 15,603x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : SMA, Fast length 18 bars, Slow length 51 bars => 19,507x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : RMA, Fast length 20 bars, Slow length 52 bars => 5,729x net profit

BTCUSD ( BitStamp ) 1 Day Timeframe : WMA, Fast length 29 bars, Slow length 60 bars => 19,869x net profit

Features:

-You can choose your preferred moving average: SMA , EMA , WMA , RMA & VWMA .

-You can change the length average for each moving average

-I made the background color Green when you're currently in a long position and Red when not. I made it so you can see when you'd be actively in a trade or not. The Red and Green background colors can be toggled on/off in order to see other indicators more clearly overlayed in the chart, or if you prefer a cleaner look on your charts.

-I also have a plot of the Fast moving average and Slow moving average together. The Opening moving average is Purple, the Closing moving average is White. White on top is a sign of a potential upswing and purple on top is a sign of a potential downswing. I've made this also able to be toggled on/off.

Let me know if you think I should change anything with my script, I'm always open to constructive criticism so feel free to comment below :)

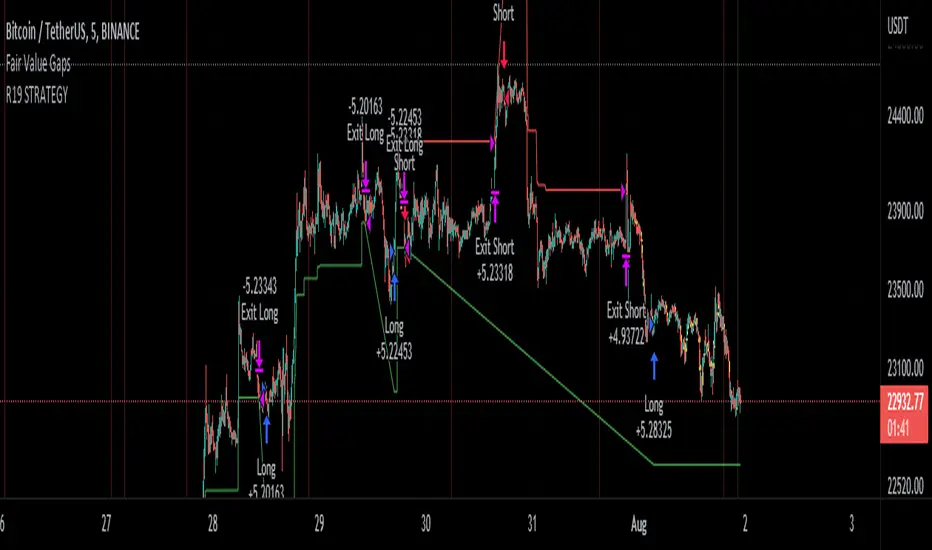

R19 STRATEGYHello again.

Let me introduce you R19 Strategy I wrote for mostly BTC long/short signals

This is an upgrated version of STRATEGY R18 F BTC strategy.

I checked this strategy on different timeframes and different assest and found it very usefull for BTC 1 Hour and 5 minutes chart.

Strategy is basically takes BTC/USDT as a main indicator, so you can apply this strategy to all cryptocurrencies as they mostly acts accordingly with BTC itself (Of course you can change main indicator to different assets if you think that there is a positive corelation with. i.e. for BTC signals you can sellect DXY index for main indicator to act for BTC long/short signals)

Default variables of the inticator is calibrated to BTC/USDT 5 minute chart. I gained above %77 success.

Strategy simply uses, ADX, MACD, SMA, Fibo, RSI combination and opens positions accordingly. Timeframe variable is very important that, strategy decides according the timeframe you've sellected but acts within the timeframe in the chart. For example, if you're on the 5 minutes chart, but you've selected 1 hour for the time frame variable, strategy looks for 1 hour MACD crossover for opening a position, but this happens in 5 minutes candle, It acts quickly and opens the position.

Strategy also uses a trailing stop loss feature. You can determine max stoploss, at which point trailing starts and at which distance trailing follows. The green and red lines will show your stoploss levels according to the position strategy enters (green for long, red for short stop loss levels). When price exceeds to the certaing levels of success, stop loss goes with the profitable price (this means, when strategy opens a position, you can put your stop loss to the green/red line in actual trading)

You can fine tune strategy to all assets.

Please write down your comments if you get more successfull about different time zones and different assets. And please tell me your fine tuning levels of this strategy as well.

See you all.

.srb suite pin-upThe essential suite Indicator

that are well integrated to ensure visibility of essential items for trading.

it is very cumbersome to put symbol in the Tradingview chart and combine essential individual indicators one by one.

Moreover even with such a combination, the chart is messy and visibility is not good.

This is because each indicator is not designed with the others in mind.

This suite was developed as a composite-solution to that situation, and will make you happy.

--> This is steamlined pin-up version of .srb suite.

--> A minimal set of indicators for comparing different symbols.

--> This is well-balanced alternative next version of previous .b pin-up symbol

BTC-agg. Volume

4 BTC-spot & 4 BTC-PERP volume aggregated.

It might helps you don't miss out on important volume flows.

Weighted to spot trading volume when using PERP+spot volume .

If enabled, BTC-agg.Vol automatically applied when selecting BTC-pair.

--> This is used in calculations involving volumes, such as VWAP .

Moving Average

1 x JMA trend ribbon ; Accurately follow short-term trend changes.

2 x EMA ribbon ; zone , not the line.

MA extension line ; It provide high visibility to recognize the direction of the MA.

SPECIAL TOOLS

BB regular (Dev. 2.0, 2.5)

BB Extented (Dev. 2.5, 3.0, 3.5)

SPECIAL TOOLS - Ultra Volume Marking

x2 x4 greater than regular average volume, it will help you can take the reversal

It does not directly indicate volume, but ultra-volume marking is enough for compare.

---------------------------------------------------------------------------------------------------------------------------------------

if you have any questions freely contact to me by message on tradingview

but please understand that responses may be quite late.

Special thanks to all of contributors of community.

The script may be freely distributed under the MIT license.

Bitcoin Support BandsSMA and EMA support/resistance bands for Bitcoin. Based on 4 week multiples; 1 month, 3 month, 6 month, 1 year, 2 year, 4 year.

Bitcoin Weekly Support BandsMy first ever attempt at a custom script. I took Benjamin Cowen's concept of the Bitcoin Bull Market Support Band and applied it to the 100 week and 200 week moving averages. I also added in the 300 week sma. I mainly wanted to have all these in one indicator.

Scalping Support Resistance StrategyScalping strategy for BTC using one line: Support Resistance.

The strategy draws a line based on the minimum value of the average of High, Low, and Close for a given bar. The entries are carried out on the breakdown of this line. Exits are managed by the specified in the script's inputs take-profit and stop-loss percentages.

From Stream:

www.tradingview.com

Three EMAs Trend-following Strategy (by Coinrule)Trend-following strategies are great because they give you the peace of mind that you're trading in line with the market.

However, by definition, you're always following. That means you're always a bit later than your want to be. The main challenges such strategies face are:

Confirming that there is a trend

Following the trend, hopefully, early enough to catch the majority of the move

Hopping off the trade when it seems to have run its course

This EMA Trend-following strategy attempts to address such challenges while allowing for a dynamic stop loss.

ENTRY

The trading system requires three crossovers on the same candle to confirm that a new trend is beginning:

Price crossing over EMA 7

Price crossing over EMA 14

Price crossing over EMA 21

The first benefit of using all three crossovers is to reduce false signals. The second benefit is that you know that a strong trend is likely to develop relatively soon, with the help of the fast setup of the three EMAs.

EXIT

The strategy comes with a fixed take profit and a volatility stop, which acts as a trailing stop to adapt to the trend's strength. That helps you get out of the way as soon as market conditions change. Depending on your long-term confidence in the asset, you can edit the fixed take profit to be more conservative or aggressive.

The position is closed when:

The price increases by 4%

The price crosses below the volatility stop.

The best time frame for this strategy based on our backtest is the 4-hr. Shorter timeframes can also work well, although they exhibit larger volatility in their returns. In general, this approach suits medium timeframes. A trading fee of 0.1% is taken into account. The fee is aligned to the base fee applied on Binance, which is the largest cryptocurrency exchange.

Bitcoin trend RVI and Emastrategy with two emas and rvi.

Only long positions when fast ema above slow ema when rvi gives entry.

Only short positions when slow ema above fast ema when rvi gives entry.

.b pin-up symbolWhen trading cryptocoins, it is necessary to check the price trend of NASDAQ, BTC.D, BTC.OI, BTC spot or other coins of similar groups.

However it is very cumbersome to put a comparison symbol in the Tradingview chart and combine individual indicators one by one.

Moreover even with such a combination, the chart is messy and visibility is not good.

This script was developed as a composite-solution to that situation, and will make you happy.

- NQ1!, USTECH100CFD | symbol fixed

- BTC.Dominance, BTC.OpenInterest, BTC symbol, others pin-up-symbol | selectable

- Pin-up-symbol | selectable

- Pin-up-symbol's candle chart

- Trending

* EMA 9,21,50,200 ribbon classic EMA

* .b price line ; .b price = unique trending price with price-action + relative-volume-action + ATR

* Dynamic S/R Cloud ; BB + donchian band + high/low + atr mixed custom-logic

* VWWMA + .b price Shadow ; Volume-weighted WMA on .b price = unique MA faster than classic VWMA

Trending shadow direction is not bad even on low-timeframe (1, 2, 3, 5m, 15m...)

- Pattern

* Harmonic Pattern ; A simplified version of the harmonic pattern indicator, simply show-up pattern complete position

for reference only - adopted from HeWhoMustNotBeNamed's script.

- Information Panel

* BTC Dominance, BTC Open Interest, Pin-Up-Symbol price

* Trend meter ; 5,15,30,1h,2h,4h Meter Calc with 1 minute-timeframe candles

5 = Green if the current price is higher than the price 5 minutes ago.

1h = Green if the current price is higher than the price 2 hours ago.

4h = Red if the current price is lower than the price 4 hours ago.

* caution ; To use real-time chart of "CME_MINI:NQ1!" you have to additional subscribe CME data,

default setting is 'NQ1!' , you can change to 'USTECH100CFD'

* When you choose symbol which is closed trading hours, the script's update stopped.

Even if the selected pin-up-symbol is on trading hours, the currently selected symbol's chart doesn't update.

* recommended | chart setting > Appearance : Top margin 0%, Bottom margin 0% for optimized screen usage :)

if you have any questions freely contact to me by message on tradingview, or telegram @sr_bt

but please understand that responses may be quite late.

------------------------------------------------------------------------------------------------------------------------------------------------------------

copyright 2022 (sr_b)

Special thanks to all of contributors of community.

The script (originaly .b) may be freely distributed under the MIT license.

The other classic script code also may be freely distributed under the MIT license.

Simplified Harmonic script part | core adopted from 'Multi ZigZag Harmonic Patterns (HeWhoMustNotBeNamed)' MPL2.0 license

.b BTC-Exchange volumeBINANCE:BTCUSDT

It's tool to check exchange trading status.

You can see "BTC-exchange's realtime trading volume, previous closed volume" at once.

You can switch to see 'Previous close volume' on script's panel.

Timeframe recommended ; 15m, 1H, 4H, D, W, whatever.

Each exchange may have a different volume display unit, so I converted it into roughly BTC units. (using hl2 price)

This indicator aims to recognize the difference in the trading volume of the exchange at once.

It's not for the purpose of check the exact trading volume.

All data come from tradingview.

The comparison target exchanges refer to the ranking of CoinMarketCap.

if you have any questions freely contact to me by message on tradingview, or telegram @sr_bt

but please understand that responses may be quite late.

BTC WaveTrend R:R=1:1.5In this strategy, I used Wavetrend indicator (Lazy Bear).

It is very simple and easy to understanding: Long when Wavetrend1 crossover Wavetrend2 and they are less than a limit value (not buy when price overbought). Stoploss at lowest 3 bar previous. R:R = 1:1,5.

About other shortterm strategies for crypto market, you can view my published strategies.

Volatility Calculator for Daily Top and Bottom RangeWith the usage of ATR, applied on the close of the daily candle, I am calculated the volatility channels for the TOP and BOTTOM

Based on this logic, we can estimate, with a huge confidence factor, where the prices are going to be compressed for the trading day.

Having said that, lets take a look at the data gathered among the most important financial markets:

SPX

TOP CROSSES : 2116

BOT CROSSES : 1954

Total Daily Candles : 18908

Occurance ratio = 0.215

NDX

TOP CROSSES : 1212

BOT CROSSES : 1183

Total Daily Candles : 9386

Occurance ratio = 0.255

DIA

TOP CROSSES : 759

BOT CROSSES : 769

Total Daily Candles : 6109

Occurance ratio = 0.25

DXY

TOP CROSSES : 1597

BOT CROSSES : 1598

Total Daily Candles : 13156

Occurance ratio = 0.243

DAX

TOP CROSSES : 1878

BOT CROSSES : 1848

Total Daily Candles : 13155

Occurance ratio = 0.283

BTC USD

TOP CROSSES : 416

BOT CROSSES : 417

Total Daily Candles : 4290

Occurance ratio = 0.194

ETH USD

TOP CROSSES : 247

BOT CROSSES : 268

Total Daily Candles : 2452

Occurance ratio = 0.21

EUR USD

TOP CROSSES : 820

BOT CROSSES : 805

Total Daily Candles : 7489

Occurance ratio = 0.217

GOLD

TOP CROSSES : 1722

BOT CROSSES : 1569

Total Daily Candles : 13747

Occurance ratio = 0.239

USOIL

TOP CROSSES : 1077

BOT CROSSES : 1089

Total Daily Candles : 10231

Occurance ratio = 0.212

US 10Y

TOP CROSSES : 1302

BOT CROSSES : 1365

Total Daily Candles : 9075

Occurance ratio = 0.294

Based on this, we can assume with a very high confidence ( 70-80%) that the market is going to stay, within the range created from the BOT and TOP ATR points.

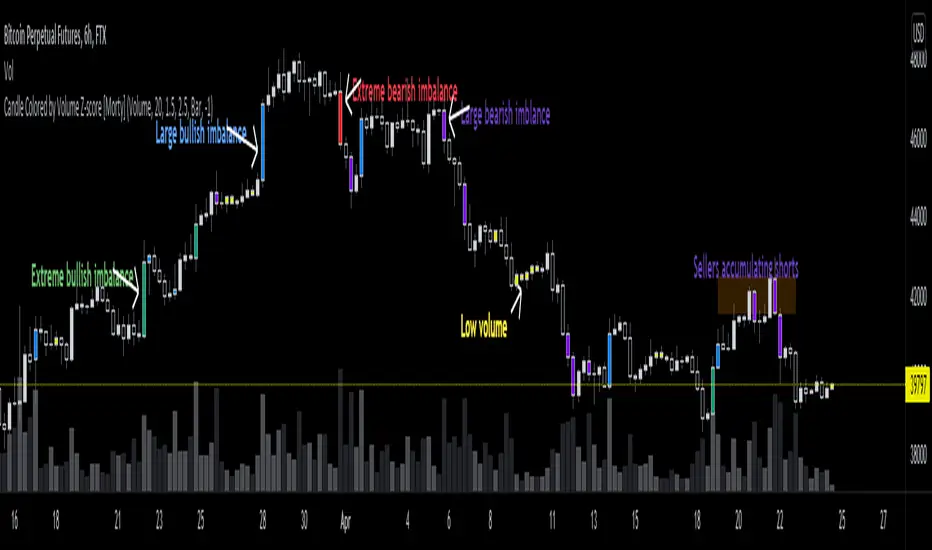

Candle Colored by Volume Z-score [Morty]This indicator colors the candles according to the z-score of the trading volume. You can easily see the imbalance on the chart. You can use it at any timeframe.

In statistics, the standard score (Z-score) is the number of standard deviations by which the value of a raw score (i.e., an observed value or data point) is above or below the mean value of what is being observed or measured. Raw scores above the mean have positive standard scores, while those below the mean have negative standard scores.

This script uses trading volume as source of z-score by default.

Due to the lack of volume data for some index tickers, you can also choose candle body size as source of z-score.

features:

- custom source of z-score

- volume

- candle body size

- any of above two

- all of above two

- custom threshold of z-score

- custom color chemes

- custom chart type

- alerts

default color schemes:

- green -> excheme bullish imbalance

- blue -> large bullish imbalance

- red -> excheme bearish imbalance

- purple -> large bearish imbalance

- yellow -> low volume bars, indicates "balance", after which volatility usually increases and tends to continue the previous trend

Examples:

* Personally, I use dark theme and changed the candle colors to black/white for down/up.

Volume as Z-score source

Any as Z-score source, more imbalances are showed

COT Report BTC Positions█ OVERVIEW

Showing the Commitments of Traders (COT) report(*) for BITCOIN Positions - CHICAGO MERCANTILE EXCHANGE (futures only) with COT charts on TradingView data.

* COT reports are released each Friday (except for U.S. holidays) by the CFTC.

* Each COT report release includes data from the previous Tuesday.

* Original data is www.cftc.gov

Data currently displayed are through April 12, 2022

█ FEATURES

You can switch the display for each of the following Positions :

Long

Short

You can switch the display for each of the following Categories :

Dealer

Asset manager

Leverage funds

Other reportable

Non reportable

█ HOW TO USE IT

This indicator allows you to see changes for each category within TradingView without having to refer directly to each report.

Macro EMA Correlation

This script is useful to see correlation between macroeconomic assets, displayed in different ema line shown in percentage to compare these assets on the same basis. Percentage will depend on the time frame selection. In the higher timeframe you will see higher variation and in small timeframe smaller variation.

You can select the timeframe who suit your trading style. The 1h and 4h fit well for longer trend swing trade and the lower time frame 15m, 5m, 1m are good for scalping or daily trading.

The following asset are available:

Bitcoin

Ethereum

Gold

Crypto total market cap excluding bitcoin (total2)

United state 10-year government bond (US10Y)

Usdt dominance show the concentration of usdt hold. For example, when trader are fearful they sell their crypto position to keep more usdt in their portfolio (USDT.D)

The USD/JPY pair the dollar usd versus the Japanese Yen one of the most forex traded pair.

You can clic on parameter to select the asset you want to analyse.

The main correlation observed are:

bitcoin negatively correlated with the usdt dominance.

bitcoin negatively correlated with the usd/jpy pair

bitcoin is positively correlated to eth, total2 (altcoin)

bitcoin positively correlated with gold

bitcoin is mostly negatively correlated to us10y

The basis of correlation is that positively correlated asset goes in the same direction and that the negatively correlated goes in opposite direction.

So, the idea is to use these information to see trend reversing.

Example 1: when bitcoin and usdt dominance are extended in opposite direction we look for a possible retracement toward 1% wich is the middle base.

Example 2 : when bitcoin make a move we look for ethereum and total 2 to follow