Momentum Table - Felipe📊 Momentum Table – By Felipe

This multi-timeframe momentum dashboard displays a clean and color-coded overview of key trend and momentum indicators across 6 major timeframes (5m to 1W), directly on your chart. It’s ideal for quickly identifying market strength, trend alignment, and potential reversals at a glance.

🔍 Features:

EMA Trend Check (EMA 9, 20, 100, 200):

Compares the current close against each EMA.

✅ Green check = price is above the EMA (bullish bias).

🔻 Red arrow = price is below the EMA (bearish bias).

Visual trend alignment helps you spot strong directional setups.

RSI (Relative Strength Index):

Displays current RSI (14) value per timeframe.

Background color highlights momentum conditions:

🔴 Red = Overbought (>70)

🟢 Green = Oversold (<30)

⚪ Gray = Neutral

Stochastic RSI:

Uses Stoch RSI applied to RSI (14) for sensitivity.

Background color follows the same logic as RSI for quick visual cues.

Compact Visual Table:

Located in the bottom-right corner.

Clean design with headers and rows labeled by timeframe.

Helps traders monitor trend and momentum confluence across multiple timeframes in real time.

This tool supports momentum-based strategies, EMA stacking confirmation, and multi-timeframe alignment, making it ideal for scalpers, swing traders, and trend followers alike.

Центральные осцилляторы

[blackcat] L3 Dark Horse OscillatorOVERVIEW

The L3 Dark Horse Oscillator is a sophisticated technical indicator meticulously crafted to offer traders deep insights into market momentum. By leveraging advanced calculations involving Relative Strength Value (RSV) and proprietary oscillatory techniques, this script provides clear and actionable signals for identifying potential buying and selling opportunities. Its distinctive feature—a vibrant gradient color scheme—enhances readability and makes it easier to visualize trends and reversals on the chart 📈↗️.

FEATURES

Advanced Calculation Methods: Utilizes complex algorithms to compute the Relative Strength Value (RSV) over specific periods, providing a nuanced view of price movements.

Default Period: 27 bars for initial RSV calculation.

Additional Period: 36 bars for extended RSV analysis.

Dual-Oscillator Components:

Component A: Derived using multiple layers of Simple Moving Averages (SMAs) applied to the RSV, offering a smoothed representation of short-term momentum.

Component B: Employs a unique averaging method tailored to capture medium-term trends effectively.

Dynamic Gradient Color Scheme: Enhances visualization through a spectrum of colors that change dynamically based on the calculated values, making trend identification intuitive and engaging 🌈.

Customizable Horizontal Reference Lines: Key levels are marked at 0, 10, 50, and 90 to serve as benchmarks for assessing the oscillator's readings, helping traders make informed decisions quickly.

Comprehensive Visual Representation: Combines the strengths of both components into a single, gradient-colored candlestick plot, providing a holistic view of market sentiment and momentum shifts 📊.

HOW TO USE

Adding the Indicator: Start by adding the L3 Dark Horse Oscillator to your TradingView chart via the indicators menu. This will overlay the necessary plots directly onto your price chart.

Interpreting the Components: Familiarize yourself with the two primary components represented by yellow and fuchsia lines. These lines indicate the underlying momentum derived from the RSV calculations.

Monitoring Momentum Shifts: Pay close attention to the gradient-colored candlesticks, which reflect the combined strength of both components. Notice how these candles transition through various shades, signaling changes in market dynamics.

Utilizing Reference Levels: Leverage the horizontal lines at 0, 10, 50, and 90 as critical thresholds. For instance, values above 50 might suggest bullish conditions, while those below could hint at bearish tendencies.

Combining with Other Tools: To enhance reliability, integrate this indicator with complementary technical analyses such as moving averages, volume profiles, or other oscillators like RSI or MACD.

LIMITATIONS

Market Volatility: In extremely volatile or sideways-trending markets, the indicator might produce false signals due to erratic price movements. Always cross-reference with broader market contexts.

Testing Required: Before deploying the indicator in real-time trading, conduct thorough backtesting across diverse assets and timeframes to understand its performance characteristics fully.

Asset-Specific Performance: The efficacy of the L3 Dark Horse Oscillator can differ significantly across various financial instruments and market conditions. Tailor your strategies accordingly.

NOTES

Historical Data: Ensure ample historical data availability to facilitate precise calculations and avoid inaccuracies stemming from insufficient data points.

Parameter Adjustments: Experiment with adjusting the default periods (27 and 36 bars) if you find them unsuitable for your specific trading style or market conditions.

Visual Customization: Modify the appearance settings, including line styles and gradient colors, to better suit personal preferences without compromising functionality.

Risk Management: While the indicator offers valuable insights, always adhere to robust risk management practices to safeguard against unexpected market fluctuations.

EXAMPLE STRATEGIES

Trend Following: Use the oscillator to confirm existing trends. When Component A crosses above Component B, consider entering long positions; conversely, look for short entries during downward crossovers.

Mean Reversion: Identify extreme readings near the upper (90) or lower (10) bands where prices might revert to mean levels, presenting potential reversal opportunities.

Divergence Analysis: Compare the oscillator's behavior with price action to spot divergences, which often precede trend reversals. Bullish divergence occurs when prices make lower lows but the oscillator shows higher lows, suggesting upward momentum.

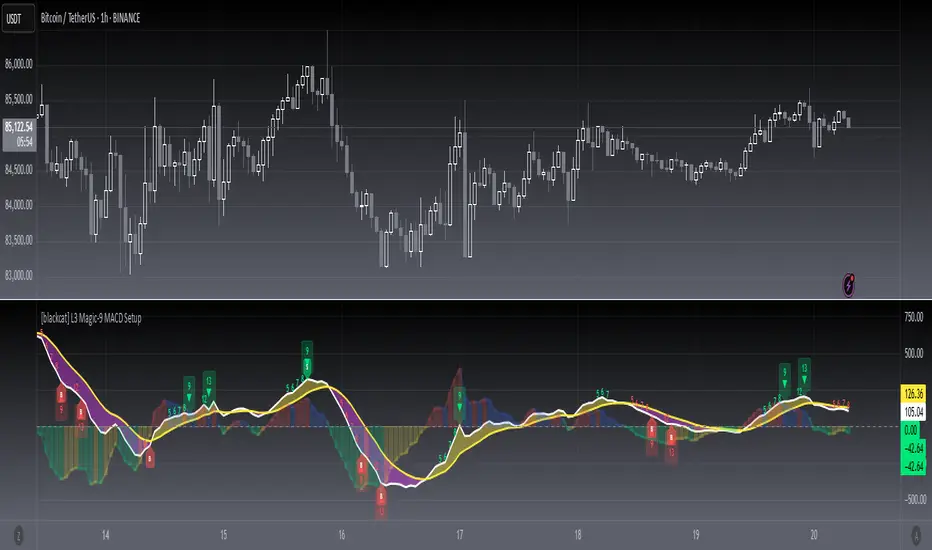

[blackcat] L3 Magic-9 MACD SetupOVERVIEW

The L3 Magic-9 MACD Setup indicator is meticulously crafted to assist traders in identifying precise buy and sell signals through an enhanced Moving Average Convergence Divergence (MACD) methodology. This advanced tool integrates the Magic-9 Sequential technique to refine signal accuracy by filtering out market noise. By providing clear visual cues via labeled charts and real-time alerts, it empowers users to make informed trading decisions swiftly and confidently 📈✅.

FEATURES

Customizable MACD Parameters:

Fast Length: Adjustable parameter to control the sensitivity of the fast moving average.

Slow Length: Configurable setting for the slow moving average to balance responsiveness and stability.

Signal Length: Modifiable value to determine the smoothing factor applied to the MACD line.

Dynamic Plot Visuals:

MACD Line: Representing the difference between short-term and long-term EMAs.

Signal Line: A smoothed version of the MACD line used to generate crossover signals.

Histogram: Illustrating the distance between the MACD and Signal lines, highlighting momentum changes.

All elements feature adjustable colors and styles for personalized visualization preferences 🎨.

Advanced Filtering Mechanism:

Utilizes the Magic-9 Sequential method to analyze consecutive price movements, enhancing signal reliability.

Counts sequential occurrences above or below initial values to detect trends more accurately 🔍.

Sequential Labels:

Displays numerical labels (e.g., '5', '6', etc.) at key points where sequential conditions are met, offering insights into trend strength.

Highlights significant reversals with special labels like '9' and '13' for critical decision-making moments 🏷️.

Buy/Sell Signals:

Generates clear 'B' (buy) and 'S' (sell) labels based on predefined conditions derived from sequential analysis.

Provides actionable trade suggestions directly on the chart for easy interpretation.

Alert System:

Supports customizable alerts to notify users instantly when buy/sell conditions are triggered.

Ensures timely responses to market movements without constant monitoring 🔔.

HOW TO USE

Add Indicator to Chart:

Access the TradingView platform and navigate to the indicators section.

Select ' L3 Magic-9 MACD Setup' from the list and add it to your desired chart.

Configure Settings:

Open the settings panel to adjust MACD parameters such as Fast Length, Slow Length, and Signal Length according to your trading strategy.

Modify plot colors and styles to suit your visual preferences for better readability.

Analyze Chart Labels:

Monitor the chart for sequentially numbered labels indicating trend strength and potential reversal points.

Pay close attention to special labels like '9' and '13' for crucial trading signals.

Combine with Other Tools:

Use additional technical indicators or fundamental analysis to confirm signals generated by the L3 Magic-9 MACD Setup.

Enhance decision-making accuracy by cross-verifying multiple data sources.

LIMITATIONS

Market Conditions Sensitivity:

The indicator may produce fewer reliable signals during periods of low volatility or range-bound markets.

Traders should be cautious of false positives in highly choppy environments 🌪️.

Dependency on Historical Data:

Accurate performance requires sufficient historical price data; insufficient data may lead to inaccurate calculations.

Regular updates and backtesting are essential to maintain effectiveness over time.

Single Indicator Risk:

Relying solely on MACD-based signals can miss broader market context; combining with other analytical tools is recommended.

Always validate signals through multiple lenses to mitigate risks associated with single-indicator strategies.

NOTES

Data Sufficiency:

Ensure your chart has enough historical data loaded to support robust MACD computations.

Periodically review and update data inputs to reflect current market dynamics.

Testing and Validation:

Conduct thorough testing on demo accounts before deploying the indicator in live trading scenarios.

Backtest across various market cycles to assess its resilience under different conditions.

Parameter Optimization:

Experiment with different parameter settings tailored to specific asset classes or trading styles.

Fine-tune the lookback period and other configurable options to align with personal trading objectives.

Multi Timeframe ATR, CCI & RSIMulti Timeframe ATR, CCI & RSI (MTF IND)

This indicator displays ATR, CCI, and RSI values from a custom selected timeframe in a clean table overlay.

It helps monitor volatility and momentum from higher/lower timeframes directly on your current chart.

Features:

• Select custom timeframe for all indicators (e.g., 1D, 1W, 65m, etc.)

• ATR with selectable smoothing type (RMA, SMA, EMA, WMA)

• CCI & RSI with trend arrows (▲ rising, ▼ falling, ▬ neutral)

• Compact summary table

Aesthetic RSI [AlchimistOfCrypto]🌌 Aesthetic RSI – Unveiling the Fractal Forces of Markets 🌌

Category: Momentum Indicators 📈

"The RSI oscillator, formalized through an advanced mathematical prism, reveals the underlying fractal structures of price movements. This indicator draws inspiration from quantum principles of divergence-convergence where the probability of a return to equilibrium increases proportionally to the distance from the median point. Our implementation employs sophisticated algorithmic smoothing to filter out the stochastic noise inherent in financial markets, allowing visualization of the true momentum forces according to thermodynamic entropy principles applied to trading systems."

📊 Professional Trading Application

The Aesthetic RSI is a visually stunning and mathematically refined take on the classic Relative Strength Index. With customizable settings, advanced smoothing, and eight unique visual palettes, it empowers traders to detect momentum shifts and divergences with unparalleled clarity.

⚙️ Indicator Configuration

- Length 📏

The core parameter (default: 20) that determines the calculation period.

- Lower values (8-14): Increase sensitivity for short-term trading.

- Higher values (21-34): Provide stronger signals for position trading.

- OverBought/OverSold Thresholds 🎯

Customizable boundaries (default: 75/25) to identify extreme market conditions.

- Calibrate based on asset volatility: Higher volatility assets may need wider thresholds (80/20) to reduce false signals.

- Style 🎨

Eight meticulously crafted visual palettes optimized for pattern recognition:

- Miami Vice (default): High-contrast cyan/magenta scheme for spotting divergences.

- Cyberpunk: Yellow/purple combo to highlight momentum shifts.

- Classic: Traditional green/red for conventional analysis.

- High Contrast: Maximum visual separation for traders with visual impairments.

- Specialized palettes (Forest, Ocean, Fire, Monochrome): Tailored for diverse market conditions.

- Mode Selection 🔄

- Full: Displays a complete gradient spectrum across the RSI range, emphasizing momentum transitions between 35-65.

- OverZone: Focuses on actionable extreme zones, reducing noise in ranging markets.

🚀 How to Use

1. Adjust Length ⏰: Set the period based on your trading style (short-term or long-term).

2. Fine-Tune Thresholds 🎚️: Customize overbought/oversold levels to match the asset’s volatility.

3. Select a Palette 🌈: Choose a visual style that enhances your pattern recognition.

4. Choose Mode 🔍: Use "Full" for detailed momentum analysis or "OverZone" for extreme zone focus.

5. Spot Divergences ✅: Look for price-RSI divergences to anticipate reversals.

6. Trade with Precision 🛡️: Combine with other indicators for high-probability setups.

📅 Release Notes (April 2025)

Aesthetic RSI blends quantum-inspired mathematics with artistic visualization, redefining momentum analysis. Stay tuned for future enhancements! ✨

🏷️ Tags

#Trading #TechnicalAnalysis #RSI #Momentum #Divergence #MultiTimeframe #TradingStrategy #RiskManagement #Forex #Stocks #Crypto #Bitcoin #AlgoTrading #DayTrading #SwingTrading #TheAlchimist #QuantumTrading #VisualTrading #PatternRecognition

MACD [AlchimistOfCrypto]🌠 MACD Optimized with Python – Decoding the Chaos of Markets 🌠

Category: Trend Analysis 📈

"Like the dynamic systems studied in chaos theory, financial markets appear unpredictable at first glance. Yet, as Edward Lorenz demonstrated, even in apparent chaos reside harmonious mathematical structures. The MACD (Moving Average Convergence Divergence) represents this quest for order within disorder—a mathematical formulation that extracts coherent signals from price noise. By combining moving averages of different periods, this indicator reveals hidden cycles and precise moments when market energy shifts, like a pendulum obeying the immutable laws of physics."

📊 Technical Overview

The MACD Optimized with Python is a revolutionary take on the classic Moving Average Convergence Divergence indicator. Powered by Python-driven optimizations 🐍, it adapts to specific timeframes, delivering razor-sharp signals for traders seeking to navigate the market’s chaos with precision.

⚙️ How It Works

- Python-Optimized Parameters 🔧: Unlike the standard MACD (12,26,9), our version uses mathematically tailored parameters for each timeframe:

- 1H: 11/38/27

- 4H: 9/98/27

- 1D: 45/90/29

- 1W: 9/16/3

- 2W: 5/20/5

- Intuitive Visuals 🎨:

- Crossovers marked by colored dots 🟢🔴 for clear entry/exit signals.

- Histogram with a color gradient 🌈 to show direction and momentum intensity.

- Customizable Signals 🎯: Choose to display long, short, or both signals to match your trading style.

🚀 How to Use This Indicator

1. Select Your Timeframe ⏰: Choose the timeframe aligned with your trading horizon (1H, 4H, 1D, 1W, or 2W).

2. Spot Crossovers 🔍: Watch for the MACD line (green) crossing the signal line (red) to identify potential trend changes.

3. Confirm with Divergence ✅: Combine crossovers with price-MACD divergence for high-probability trend reversal signals.

📅 Release Notes

Unlock the hidden order of markets with this Python-optimized MACD. Stay tuned for future enhancements! ✨

🏷️ Tags

#Trading #TechnicalAnalysis #MACD #TrendAnalysis #Python #MultiTimeframe #Divergence #Momentum #TradingStrategy #RiskManagement #Forex #Stocks #Crypto #ChaosTheory #OptimizedTrading

[blackcat] L3 Magic-9 Sequential MACDOVERVIEW

The L3 Magic-9 Sequential MACD indicator is an advanced tool designed to enhance the traditional Moving Average Convergence Divergence (MACD) by incorporating sequential patterns. This script calculates various MACD components and applies custom logic to identify potential buy and sell signals based on specific sequential conditions 📊💹.

FEATURES

Calculates MACD Line, Signal Line, and enhanced histogram.

Plots colored histograms to visualize differences between MACD line and signal line:

Positive histogram bars indicate bullish momentum.

Negative histogram bars indicate bearish momentum.

Identifies sequential patterns in the MACD line for generating buy ('Buy') and sell ('Sell') signals 🏷️.

Adds numerical labels (e.g., '5', '6', '7', etc.) to mark specific sequential conditions.

Supports customizable colors and styles for plotted elements ⚙️.

Generates alerts for identified sequential patterns 🔔.

HOW TO USE

Add the indicator to your TradingView chart by selecting it from the indicators list.

Adjust the input parameters for Fast Length, Slow Length, and Signal Length.

Monitor the chart for labeled buy/sell signals and numerical markers indicating sequential patterns.

Set up alerts based on the generated signals to receive notifications when conditions are met 📲.

Use the indicator alongside other technical analysis tools for better decision-making.

LIMITATIONS

The effectiveness of sequential patterns may vary depending on market conditions.

False signals can occur in highly volatile or ranging markets 🌪️.

Users should always confirm signals with other forms of analysis before entering trades.

NOTES

Ensure that you have sufficient historical data available for accurate MACD calculations.

Test the indicator thoroughly on demo accounts before applying it to live trading 🔍.

Customize the appearance of the plotted elements as needed to suit your chart layout.

Oath KeeperOath Keeper - Advanced Money Flow & Market Dynamics Indicator

A sophisticated indicator that analyzes market dynamics through money flow patterns, volume analysis, and liquidation detection to identify high-probability trading opportunities.

Core Features:

• Smart Money Flow Analysis: Proprietary calculation of institutional money movement

• Volume-Enhanced Signals: Multi-timeframe volume confirmation

• Liquidation Detection: Identifies potential forced liquidation events

• Advanced Signal Classification: Regular, Super, and Fakeout signals

Signal Types:

1. Regular Signals (Green/Purple Circles)

• Volume-confirmed momentum shifts

• Money flow threshold breaches

• Institutional participation confirmation

2. Super Signals (Green/Purple Squares)

• Deep oversold/overbought reversals

• High-volume rejection patterns

• Liquidation event confirmation

3. Fakeout Signals (Red X)

• Rapid sentiment shifts

• Trap detection

• False breakout warnings

Visual Components:

• Dynamic Money Flow Line (White/Purple)

• Order Flow Clouds (Green/Red with high transparency)

• Reference Levels (20, 50, 80)

• Multi-type Signal Markers

• Color-coded momentum visualization

Interpretation Guide:

• Green Cloud: Bullish money flow dominance

• Red Cloud: Bearish money flow dominance

• Circle Markers: Standard reversals

• Square Markers: High-conviction moves

• X Markers: Potential trap zones

Best Practices:

• Most effective on 1H+ timeframes

• Use with major trading pairs

• Wait for candle close confirmation

• Combine with support/resistance levels

• Monitor volume confirmation

• Use multiple timeframe analysis

This indicator helps traders identify institutional money flow, potential liquidation events, and market reversals by analyzing volume patterns and money flow dynamics, providing multiple confirmation layers for trade decisions.

Note: Performance varies with market conditions and timeframes. Always employ proper risk management.

Liquidity Fracture DetectorThe Liquidity Fracture Detector is an advanced tool designed to identify micro-liquidity traps and structural fakeouts on intraday charts. These occur when the market appears to break out, only to quickly reverse — often triggered by stop hunts, inefficient fills, or manipulated order flow.

The script combines volume spikes, volatility anomalies, and price structure breaks to signal "fractures" — points where the market temporarily breaks its behavior, often followed by strong reversals or trend accelerations.

Detection logic in the script:

Volume spike greater than 2x the average (adjustable)

Volatility spike: candle range is > 1.5x the average

Extreme wicks: wick is larger than the candle body (a classic trap signal)

Structure break: price breaks previous high/low but closes back within the old range

Combine these elements → a “fracture” is marked

Visual representation:

Red background = potential bull trap (fake breakout to the upside)

Green background = potential bear trap (fake breakdown to the downside)

A label appears at each fracture: “Echo” with the number of previous hits

Ideal use cases:

Intraday trading (1m, 5m, 15m)

Crypto, indices, futures, and forex

Detecting reactive zones where the market takes a false direction

Confluence with S/R zones, order blocks, or liquidity pools

Fully customizable:

Volume and range sensitivity

Heatmap intensity

Toggle labels on/off

Note:

This script is intended to support discretionary analysis. It does not provide buy or sell signals and is not an automated strategy. Combine it with your own price action or order flow setup for optimal results.

Frozen Bias Zones – Sentiment Lock-insOverview

The Frozen Bias Zones indicator visualizes market sentiment lock-ins using a combination of RSI, MACD, and OBV. It creates "bias zones" that indicate whether the market is in a sustained bullish or bearish phase. These zones are then highlighted on the chart, helping traders spot when the market is locked in a bias. The script also detects breakout events from these zones and marks them with clear labels for easier decision-making.

Features

Multi-Indicator Sentiment Analysis: Combines RSI, MACD, and OBV to detect synchronized bullish or bearish sentiment.

Frozen Bias Zones: Identifies and visually represents zones where the market has remained in a particular sentiment (bullish or bearish) for a defined period.

Breakout Alerts: Displays labels to indicate when the price breaks out of the established bias zone.

Customizable Inputs: Adjust the zone duration, RSI, MACD, and breakout label visibility.

Input Parameters

Bias Duration (biasLength)

The minimum number of candles the market must stay in a specific sentiment to consider it a "Frozen Bias Zone".

Default: 5 candles.

RSI Period (rsiPeriod)

Period for the Relative Strength Index (RSI) calculation.

Default: 14 periods.

MACD Settings

MACD Fast (macdFast): The fast-moving average period for the MACD calculation.

Default: 12.

MACD Slow (macdSlow): The slow-moving average period for the MACD calculation.

Default: 26.

MACD Signal (macdSig): The signal line period for MACD.

Default: 9.

Show Break Label (showBreakLabel)

Toggle to show labels when the price breaks out of the bias zone.

Default: True (shows label).

Bias Zone Colors

Bullish Bias Color (bullColor): The color for bullish zones (light green).

Bearish Bias Color (bearColor): The color for bearish zones (light red).

How It Works

This indicator analyzes three key market metrics to determine whether the market is in a bullish or bearish phase:

RSI (Relative Strength Index)

Measures the speed and change of price movements. RSI > 50 indicates a bullish phase, while RSI < 50 indicates a bearish phase.

MACD (Moving Average Convergence Divergence)

Measures the relationship between two moving averages of the price. A positive MACD histogram indicates bullish momentum, while a negative histogram indicates bearish momentum.

OBV (On-Balance Volume)

Uses volume flow to determine if a trend is likely to continue. A rising OBV indicates bullish accumulation, while a falling OBV indicates bearish distribution.

Bias Zone Detection

The market sentiment is considered bullish if all three indicators (RSI, MACD, and OBV) are bullish, and bearish if all three indicators are bearish.

Bullish Zone: A zone is created when the market sentiment remains bullish for the duration of the specified biasLength.

Bearish Zone: A zone is created when the market sentiment remains bearish for the duration of the specified biasLength.

These bias zones are visually represented on the chart as colored boxes (green for bullish, red for bearish).

Breakout Detection

The script automatically detects when the market exits a bias zone. If the price moves outside the bounds of the established zone (either up or down), the script will display one of the following labels:

Bias Break (Up): Indicates that the price has broken upwards out of the zone (with a green label).

Bias Break (Down): Indicates that the price has broken downwards out of the zone (with a red label).

These labels help traders easily identify potential breakout points.

Example Use Case

Bullish Market Conditions: If the RSI is above 50, the MACD histogram is positive, and OBV is increasing, the script will highlight a green bias zone. Traders can watch for potential bullish breakouts or trend continuation after the zone ends.

Bearish Market Conditions: If the RSI is below 50, the MACD histogram is negative, and OBV is decreasing, the script will highlight a red bias zone. Traders can look for potential bearish breakouts when the zone ends.

Conclusion

The Frozen Bias Zones indicator is a powerful tool for traders looking to visualize prolonged market sentiment, whether bullish or bearish. By combining RSI, MACD, and OBV, it helps traders spot when the market is "locked in" to a bias. The breakout labels make it easier to take action when the price moves outside of the established zone, potentially signaling the start of a new trend.

Instructions

To use this script:

Add the Frozen Bias Zones indicator to your TradingView chart.

Adjust the input parameters to suit your trading strategy.

Observe the colored bias zones on your chart, along with breakout labels, to make informed decisions on trend continuation or reversal.

Institutional MACD (Z-Score Edition) [VolumeVigilante]📈 Institutional MACD (Z-Score Edition) — Professional-Grade Momentum Signal

This is not your average MACD .

The Institutional MACD (Z-Score Edition) is a statistically enhanced momentum tool, purpose-built for serious traders and breakout hunters . By applying Z-Score normalization to the classic MACD structure, this indicator uncovers statistically significant momentum shifts , enabling cleaner reads on price extremes, trend continuation, and potential reversals.

💡 Why It Matters

The classic MACD is powerful — but raw momentum values can be noisy and relative , especially on volatile assets like BTC/USD . By transforming the MACD line, signal line, and histogram into Z-scores , we anchor these signals in statistical context . This makes the Institutional MACD:

✔️ Timeframe-agnostic and asset-normalized

✔️ Ideal for spotting true breakouts , not false flags

✔️ A reliable tool for detecting momentum divergence and exhaustion

🧪 Key Features

✅ Full Z-Score normalization (MACD, Signal, Histogram)

✅ Highlighted ±Z threshold bands for overbought/oversold zones

✅ Customizable histogram coloring for visual momentum shifts

✅ Built-in alerts for zero-crosses and Z-threshold breaks

✅ Clean overlay with optional display toggles

🔁 Strategy Tip: Mean Reversion Signals with Statistical Confidence

This indicator isn't just for spotting breakouts — it also shines as a mean reversion tool , thanks to its Z-Score normalization .

When the Z-Score histogram crosses beyond ±2, it marks a statistically significant deviation from the mean — often signaling that momentum is overstretched and the asset may be due for a pullback or reversal .

📌 How to use it:

Z > +2 → Price action is in overbought territory. Watch for exhaustion or short setups.

Z < -2 → Momentum is deeply oversold. Look for reversal confirmation or long opportunities.

These zones often precede snap-back moves , especially in range-bound or corrective markets .

🎯 Combine Z-Score extremes with:

Candlestick confirmation

Support/resistance zones

Volume or price divergence

Other mean reversion tools (e.g., RSI, Bollinger Bands)

Unlike the raw MACD, this version delivers statistical thresholds , not guesswork — helping traders make decisions rooted in probability, not emotion.

📢 Trade Smart. Trade Vigilantly.

Published by VolumeVigilante

[blackcat] L3 Ehlers DFT-Adapted RSIOVERVIEW

The L3 Ehlers DFT-Adapted RSI is an advanced technical indicator that combines Digital Fourier Transform (DFT) analysis with traditional RSI calculations to provide enhanced market trend identification and trading signals.

FEATURES

• DFT-based frequency analysis of price movements

• Adaptive RSI calculation using dominant cycle detection

• Fast and slow moving average lines

• Color-coded candlestick visualization

• Horizontal reference lines at 45 and 55

• Intelligent sideways detection and label management

• Customizable parameter inputs

HOW TO USE

Configure the following inputs:

• Price source (default: HL2)

• Window size (default: 50)

• Overbought threshold (default: 70)

• Oversold threshold (default: 30)

• Fraction multiplier (default: 0.5)

Interpret the indicator:

• Yellow candles indicate bullish momentum

• Fuchsia candles indicate bearish momentum

• Crosses between fast and slow lines suggest potential trend changes

• Position relative to the 45/55 lines indicates overall market sentiment

• Labels appear only when sideways conditions break

SIDESWAYS DETECTION

• Sideways conditions are identified when:

The difference between fast and slow lines is less than 0.5

Both lines show minimal movement (< 0.1) • During sideways periods:

Existing labels are removed

No new labels are generated • When sideways ends:

If trend reverses, opposite label is generated

If trend continues, no new label is created

LIMITATIONS

• Requires sufficient historical data for accurate calculations

• Performance may vary across different market conditions

• Parameter sensitivity requires careful calibration

NOTES

• The indicator uses Ehlers' proprietary DFT methodology

• Default settings are optimized for general market conditions

• Consider adjusting parameters based on your trading timeframe and strategy

Altcoin Reversal or Correction DetectionINDICATOR OVERVIEW: Altcoin Reversal or Correction Detection

Altcoin Reversal or Correction Detection is a powerful crypto-specific indicator designed exclusively for altcoins by analyzing their RSI values across multiple timeframes alongside Bitcoin’s RSI. Since BTC's price movements have a strong influence on altcoins, this tool helps traders better understand whether a reversal or correction signal is truly reliable or just noise. Even if an altcoin appears oversold or overbought, it may continue trending with BTC—so this indicator gives you the full picture.

The indicator is optimized for CRYPTO MARKETS only. Not suitable for BTC itself—this is a precision tool built only for ALTCOINS only.

This indicator is not only for signals but also serves as a tool for observing all the information from different timeframes of BTC and altcoins collectively.

How the Calculation Works: Algorithm Overview

The Altcoin Reversal or Correction Detection indicator relies on an algorithm that compares the RSI values of the altcoin across multiple timeframes with Bitcoin's RSI values. This allows the indicator to identify key market moments where a reversal or correction might occur.

BTC-Altcoin RSI Correlation: The algorithm looks for the correlation between Bitcoin's price movements and the altcoin's price actions, as BTC often influences the direction of altcoins. When both Bitcoin and the altcoin show either overbought or oversold conditions in a significant number of timeframes, the indicator signals the potential for a reversal or correction.

Multi-Timeframe Confirmation: Unlike traditional indicators that may focus on a single timeframe, this tool checks multiple timeframes for both BTC and the altcoin. When the same overbought/oversold conditions are met across multiple timeframes, it confirms the likelihood of a trend reversal or correction, providing a more reliable signal. The more timeframes that align with this pattern, the stronger the signal becomes.

Overbought/Oversold Conditions & Extreme RSI Values: The algorithm also takes into account the size of the RSI values, especially focusing on extreme overbought and oversold levels. The greater the RSI values are in these extreme regions, the stronger the potential reversal or correction signal. This means that not only do multiple timeframes need to confirm the condition, but the magnitude of the overbought or oversold RSI level plays a crucial role in determining the strength of the signal.

Signal Strength Levels: The signals are classified into three levels:

Early Signal

Strong Signal

Very Strong Signal

By taking into account the multi-timeframe analysis of both BTC and the altcoin RSI values, along with the magnitude of these RSI values, the indicator offers a highly reliable method for detecting potential reversals and corrections.

Who Is This Indicator Suitable For?

This indicator can also be used to detect reversal points, but it is especially effective for scalping. It highlights potential correction points, making it perfect for quick entries during smaller market pullbacks or short-term trend shifts, which is more suitable for scalpers looking to capitalize on short-term movements

Integration with other tools

Use this tool alongside key Support and Resistance zones to further enhance your trade by filtering for even better quality entries and focusing only on high-quality reversal or correction setups. It can be also used with other indicators and suitable with other personalised strategies.

Gas/Oil SpreadGas/Oil Spread Analyzer with Static Overbought/Oversold Zones

This indicator measures the spread between the actual price of natural gas and its oil-based equivalent, derived from a defined oil/gas ratio. It helps traders identify potential mispricings and mean-reversion opportunities between the two energy commodities.

Key Features:

- Calculates spread: Gas Price – Oil-Based Equivalent Price

- Supports dynamic or static oil/gas ratio

- Plots a smoothed version of the spread (SMA)

- Displays static overbought and oversold zones to highlight extreme deviations

Use Cases:

- Detect overvalued or undervalued gas relative to oil

- Spot potential reversion setups in intermarket trading

- Evaluate energy market dislocations and hedging opportunities

Parabolic RSI [ChartPrime]The Parabolic RSI indicator applies the Parabolic SAR directly to the Relative Strength Index (RSI) . This combination helps traders identify trend shifts and potential reversal points within the RSI framework. The indicator provides both regular and strong signals based on whether the Parabolic SAR crosses above or below key RSI thresholds.

⯁ KEY FEATURES

Parabolic SAR Applied to RSI – Tracks momentum shifts within the RSI indicator.

Dynamic SAR Dots – Plots SAR levels directly on the RSI for visual clarity.

Threshold-Based Signal Filtering – Uses upper (70) and lower (30) RSI levels to determine strong signals.

Simple and Strong Signal System :

Big Diamonds (Strong Signals) – Appear when Parabolic SAR crosses above 70 or below 30 RSI, indicating potential reversals.

Small Diamonds (Regular Signals) – Appear when Parabolic SAR flips inside the RSI range, signaling weaker trend shifts.

Chart Overlay Signals – Highlights strong RSI-based trend shifts directly on the price chart.

Fully Customizable – Modify RSI length, SAR parameters, colors, and signal displays.

⯁ HOW TO USE

Look for strong signals (big diamonds) when SAR flips above 70 RSI (overbought) or below 30 RSI (oversold) for potential reversals.

Use regular signals (small diamonds) for minor trend shifts within the RSI range.

Combine with price action and other indicators to confirm entry and exit points.

Adjust the SAR acceleration factors to fine-tune sensitivity based on market conditions.

⯁ CONCLUSION

The Parabolic RSI indicator merges trend-following and momentum-based analysis by applying the Parabolic SAR to RSI. This allows traders to detect trend shifts inside the RSI space with an intuitive diamond-based signal system . Whether used alone or as part of a broader trading strategy, this indicator provides a clear and structured approach to identifying momentum reversals and potential trading opportunities.

Hamid Double RSIRSI with Moving Average and Another RSI

This script combines two Relative Strength Index (RSI) indicators with configurable moving averages. It allows traders to track momentum and market strength with adjustable periods for both the RSI and moving averages. The script also allows you to choose different data sources for each RSI, offering flexibility in analysis.

Features:

Two RSIs: One with a shorter period and another with a longer period .

Moving Averages: Each RSI has its own configurable moving average . The moving averages help smooth out the RSI and provide clearer trends.

Customizable Inputs: Adjust the RSI period and the length of the moving averages. You can also choose different sources for each RSI (e.g., close, open, high, low).

Mid Line: A horizontal line at 50, which is commonly used as the neutral level for the RSI. It helps identify whether the RSI is above or below neutral, indicating bullish or bearish conditions.

Overbought and Oversold Levels: Horizontal lines at 70 (overbought) and 30 (oversold) to highlight when the asset might be overbought or oversold according to the RSI.

How it works:

RSI Calculation: The script calculates two RSIs using different lengths

Moving Averages: A Simple Moving Average (SMA) is applied to both RSIs to smooth their values and help identify trends.

Overbought/Oversold Indicators: The script includes horizontal lines at 70 and 30 to show overbought and oversold conditions. The mid line is plotted at 50 to highlight neutral levels.

This indicator is useful for traders who want to compare the behavior of two RSIs over different time periods and use the moving averages to filter out noise. The ability to customize the source data for each RSI makes this script adaptable to different trading strategies.

Puts vs Longs vs Price Oscillator SwiftEdgeWhat is this Indicator?

The "Low-Latency Puts vs Longs vs Price Oscillator" is a custom technical indicator built for TradingView to help traders visualize buying and selling activity in a market without access to order book data. It displays three lines in an oscillator below the price chart:

Green Line (Longs): Represents the strength of buying activity (bullish pressure).

Red Line (Puts): Represents the strength of selling activity (bearish pressure).

Yellow Line (Price): Shows the asset’s price in a scaled format for direct comparison.

The indicator uses price movements, volume, and momentum to estimate when buyers or sellers are active, providing a quick snapshot of market dynamics. It’s optimized for fast response to price changes (low latency), making it useful for both short-term and longer-term trading strategies.

How Does it Work?

Since TradingView doesn’t provide direct access to order book data (which shows real-time buy and sell orders), this indicator approximates buying and selling pressure using commonly available data: price, volume, and a momentum measure called Rate of Change (ROC). Here’s how it combines these elements:

Price Movement: The indicator checks if the price is rising or falling compared to the previous candlestick. A rising price suggests buying (longs), while a falling price suggests selling (puts).

Volume: Volume acts as a "weight" to measure the strength of these price moves. Higher volume during a price increase boosts the green line, while higher volume during a price decrease boosts the red line. This mimics how large orders in an order book would influence the market.

Rate of Change (ROC): ROC measures how fast the price is changing over a set period (e.g., 5 candlesticks). It adds a momentum filter—strong upward momentum reinforces buying signals, while strong downward momentum reinforces selling signals.

These components are calculated for each candlestick and summed over a short lookback period (e.g., 5 candlesticks) to create the green and red lines. The yellow line is simply the asset’s closing price scaled down to fit the oscillator’s range, allowing you to compare buying/selling strength directly with price action.

Why Combine These Elements?

The combination of price, volume, and ROC is intentional and synergistic:

Price alone isn’t enough—it tells you what happened but not how strong the move was.

Volume adds context by showing the intensity behind price changes, much like how order book volume indicates real buying or selling interest.

ROC ensures the indicator captures momentum, filtering out weak or random price moves and focusing on significant trends, similar to how aggressive order execution might appear in an order book.

Together, they create a balanced picture of market activity that’s more reliable than any single factor alone. The goal is to simulate the insights you’d get from an order book—where you’d see buy/sell imbalances—using data available in TradingView.

How to Use It

Setup:

Add the indicator to your chart via TradingView’s Pine Editor by copying and pasting the script.

Adjust the inputs to suit your trading style:

Lookback Period: Number of candlesticks (default 5) to sum buying/selling activity. Shorter = more responsive; longer = smoother.

Price Scale Factor: Scales the yellow price line (default 0.001). Increase for high-priced assets (e.g., 0.01 for indices like DAX) or decrease for low-priced ones (e.g., 0.0001 for crypto).

ROC Period: Candlesticks for momentum calculation (default 5). Shorter = faster response.

ROC Weight: How much momentum affects the signal (default 0.5). Higher = stronger momentum influence.

Volume Threshold: Minimum volume multiplier (default 1.5) to boost signals during high activity.

Reading the Oscillator:

Green Line Above Yellow: Strong buying pressure—price is rising with volume and momentum support. Consider this a bullish signal.

Red Line Above Yellow: Strong selling pressure—price is falling with volume and momentum support. Consider this a bearish signal.

Green/Red Crossovers: When the green line crosses above the red, it suggests buyers are taking control. When the red crosses above the green, sellers may be dominating.

Yellow Line Context: Compare green/red lines to the yellow price line to see if buying/selling strength aligns with price trends.

Trading Examples:

Bullish Setup: Green line spikes above yellow after a price breakout with high volume (e.g., DAX opening jump). Enter a long position if confirmed by other indicators.

Bearish Setup: Red line rises above yellow during a price drop with increasing volume. Look for a short opportunity.

Reversal Warning: If the green line stays high while price (yellow) flattens or drops, it could signal overbought conditions—be cautious.

What Makes It Unique?

Unlike traditional oscillators like RSI or MACD, which focus solely on price momentum or trends, this indicator blends price, volume, and momentum into a three-line system that mimics order book dynamics. Its low-latency design (short lookback and no heavy smoothing) makes it react quickly to market shifts, ideal for volatile markets like DAX or forex. The visual separation of buying (green) and selling (red) against price (yellow) offers a clear, intuitive way to spot imbalances without needing complex data.

Tips and Customization

Volatile Markets: Use a shorter lookback (e.g., 3) and ROC period (e.g., 3) for faster signals.

Stable Markets: Increase lookback (e.g., 10) for smoother, less noisy lines.

Scaling: If the green/red lines dwarf the yellow, adjust Price Scale Factor up (e.g., 0.01) to balance them.

Experiment: Test on your asset (stocks, crypto, indices) and tweak inputs to match its behavior.

MACD Crossover + AlertMACD Proximity & Crossover Alert Script

This script is designed to help traders stay ahead of MACD crossovers by providing:

Early alerts when the MACD and Signal lines are getting close (within a customizable threshold)

Instant alerts when a bullish or bearish crossover occurs

Whether you're swing trading or scalping, this tool gives you advanced notice to prepare — and a confirmation signal to act on. It works on any timeframe and helps avoid late entries by alerting you when momentum is shifting.

Features:

Customizable MACD settings (fast, slow, signal length)

Adjustable "proximity" threshold

Visual background highlight when lines are close

Built-in alert conditions for:

MACD crossing above Signal (bullish)

MACD crossing below Signal (bearish)

MACD and Signal getting close (early warning)

Perfect for traders who want a heads-up before momentum shifts — not just a reaction afterward.

Institutional Quantum Momentum Impulse [BullByte]## Overview

The Institutional Quantum Momentum Impulse (IQMI) is a sophisticated momentum oscillator designed to detect institutional-level trend strength, volatility conditions, and market regime shifts. It combines multiple advanced technical concepts, including:

- Quantum Momentum Engine (Hilbert Transform + MACD Divergence + Stochastic Energy)

- Fractal Volatility Scoring (GARCH + Keltner-based volatility)

- Dynamic Adaptive Bands (Self-adjusting thresholds based on efficiency)

- Market Phase Detection (Volume + Momentum alignment)

- Liquidity & Cumulative Delta Analysis

The indicator provides a Z-score normalized momentum reading, making it ideal for mean-reversion and trend-following strategies.

---

## Key Features

### 1. Quantum Momentum Core

- Combines Hilbert Transform, MACD divergence, and Stochastic Energy into a single composite momentum score.

- Normalized using a Z-score for statistical significance.

- Smoothed with EMA/WMA/HMA for cleaner signals.

### 2. Dynamic Adaptive Bands

- Upper/Lower bands adjust based on volatility and efficiency ratio .

- Acts as overbought/oversold zones when momentum reaches extremes.

### 3. Market Phase Detection

- Identifies bullish , bearish , or neutral phases using:

- Volume-Weighted MA alignment

- Fractal momentum extremes

### 4. Volatility & Liquidity Filters

- Fractal Volatility Score (0-100 scale) shows market instability.

- Liquidity Check ensures trades are taken in favorable spread conditions.

### 5. Dashboard & Visuals

- Real-time dashboard with key metrics:

- Momentum strength, volatility, efficiency, cumulative delta, and market regime.

- Gradient coloring for intuitive momentum visualization .

---

## Best Trade Setups

### 1. Trend-Following Entries

- Signal :

- QM crosses above zero + Market Phase = Bullish + ADX > 25

- Cumulative Delta rising (buying pressure)

- Confirmation :

- Efficiency > 0.5 (strong momentum quality)

- Liquidity = High (tight spreads)

### 2. Mean-Reversion Entries

- Signal :

- QM touches upper band + Volatility expanding

- Market Regime = Ranging (ADX < 25)

- Confirmation :

- Efficiency < 0.3 (weak momentum follow-through)

- Cumulative Delta divergence (price high but delta declining)

### 3. Breakout Confirmation

- Signal :

- QM holds above zero after a pullback

- Market Phase shifts to Bullish/Bearish

- Confirmation :

- Volatility rising (expansion phase)

- Liquidity remains high

---

## Recommended Timeframes

- Intraday (5M - 1H): Works well for scalping & swing trades.

- Swing Trading (4H - Daily): Best for trend-following setups.

- Position Trading (Weekly+): Useful for macro trend confirmation.

---

## Input Customization

- Resonance Factor (1.0 - 3.618 ): Adjusts MACD divergence sensitivity.

- Entropy Filter (0.382/0.50/0.618) : Controls stochastic damping.

- Smoothing Type (EMA/WMA/HMA) : Changes momentum responsiveness.

- Normalization Period : Adjusts Z-score lookback.

---

The IQMI is a professional-grade momentum indicator that combines institutional-level concepts into a single, easy-to-read oscillator. It works across all markets (stocks, forex, crypto) and is ideal for traders who want:

✅ Early trend detection

✅ Volatility-adjusted signals

✅ Institutional liquidity insights

✅ Clear dashboard for quick analysis

Try it on TradingView and enhance your trading edge! 🚀

Happy Trading!

- BullByte

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

Log Regression Oscillator Channel [BigBeluga]

This unique overlay tool blends logarithmic trend analysis with dynamic oscillator behavior. It projects RSI, MFI, or Stochastic lines directly into a log regression channel on the price chart — offering an intuitive way to detect overbought/oversold momentum within the broader price structure.

🔵Key Features:

Logarithmic Regression Channel:

➣ Draws a trend-based channel using logarithmic regression, adapting to price growth curvature over time.

➣ Features upper, lower, and optional midline boundaries to visualize trend flow and range extremes.

Oscillator Overlay (RSI / MFI / Stochastic):

➣ Projects your chosen oscillator inside the channel using dynamic polylines.

➣ Allows switching between RSI, Money Flow Index, or Stochastic for versatile momentum insight.

Threshold-Based Scaling:

➣ The top and bottom of the channel represent traditional oscillator thresholds (e.g., RSI 70/30).

➣ Users can modify the scale in settings to customize what "overbought" or "oversold" means visually.

Signal Line Integration:

➣ Adds a yellow moving average (signal line) for smoother confirmation of oscillator turns.

➣ Helps identify divergence, momentum shifts, and fakeouts with better clarity.

Live Oscillator Readout:

➣ Displays the real-time oscillator value at the right edge of the chart.

➣ Ensures traders stay aware of current momentum levels without switching panels.

🔵Usage:

Momentum Context:

➣ When the oscillator touches the upper regression band, it may signal local overbought pressure.

➣ Touching the lower band may indicate oversold conditions within the current log trend.

Divergence Detection:

➣ Use the oscillator’s behavior relative to the channel slope to spot divergence from price.

➣ For example, RSI rising inside a falling channel can flag early trend shifts.

Trend-Sensitive Entries:

➣ Combine oscillator signals with log channel direction to filter trades in trend alignment.

➣ Signal line crossovers inside the channel act as early warning for momentum turns.

The Log Regression Oscillator Channel transforms how traders view classic momentum tools. By embedding oscillators into a logarithmic trend structure, it offers unmatched clarity on momentum positioning relative to price expansion. Ideal for swing traders, mean-reverters, or trend followers looking to sharpen entries and exits with style.

Rolling ATR Momentum

Rolling ATR Momentum Indicator – User Manual

---

🔍 Overview

The Rolling ATR Momentum Indicator is a simple yet powerful tool designed to detect shifts in market volatility. It compares the current Average True Range (ATR) with the ATR from a previous point in time to measure how market volatility is changing.

This indicator is especially useful for:

- Spotting the beginning or fading of a momentum phase

- Filtering out low-volatility market conditions

- Enhancing timing for entries and exits in trending or breakout trades

---

📊 Key Components

✅ ATR Delta (Rolling)

- Definition: `ATR Delta = Current ATR - Past ATR`

- Inputs:

- ATR Period (default: 14): The base ATR calculation window

- Lookback Period (default: 5): How many bars ago to compare ATR

- Interpretation:

- Positive ATR Delta (Green Line): Market volatility is increasing

- Negative ATR Delta (Red Line): Market volatility is decreasing

📈 Zero Line

- A horizontal baseline at zero helps you easily see when ATR momentum shifts from negative to positive (or vice versa).

🟩/🟥 Background Color

- Green Background: ATR Delta is positive (rising volatility)

- Red Background: ATR Delta is negative (falling volatility)

🔵 Optional: ATR Reference Lines

- You can optionally display raw Current ATR and Past ATR by changing their visibility settings.

---

✅ How to Use It

Entry Timing (Futures/Options)

- Use ATR Delta as a filter:

- Only take trades when ATR Delta is positive → confirms momentum is building

- Avoid trades when ATR Delta is negative → market might be slow, sideways, or losing steam

Breakout Anticipation

- A rising ATR Delta after a tight range or consolidation can suggest that a breakout is underway

Stop-loss Strategy

- Use high ATR periods for wider stops (to avoid noise)

- Use low ATR periods for tighter stops or skip trading

---

🧠 Pro Tips

- This indicator doesn’t predict direction—combine with trend or price structure tools (like EMA, PPMA, candlesticks)

- Works best in trending or breakout environments

- Add it to multi-timeframe layouts to see volatility buildup on higher timeframes

---

⚙️ Settings

| Parameter | Description |

|----------|-------------|

| ATR Period | Length of the ATR calculation (default 14) |

| Lookback Period | How many bars back to compare ATR values |

---

🧭 Best For:

- Index futures (Nifty, BankNifty)

- Option buyers needing volatility confirmation

- Intraday & swing traders looking to trade momentum setups

---

Use the Rolling ATR Momentum indicator as your volatility radar—simple, clean, and highly effective for staying on the right side of market energy.

End of Manual

Rolling ATR Momentum - EnhancedATR Rolling Momentum Indicator – User Manual

---

🔍 Overview

The ATR Rolling Momentum Indicator is a dynamic volatility tool built on the Average True Range (ATR). It not only tracks increasing or decreasing momentum but also provides early warnings and confirmation signals for potential breakout moves. It’s especially powerful for futures and options traders looking to align with expanding price action.

---

📊 Core Components

✅ ATR Delta (Rolling ATR)

- Definition: Difference between current ATR and past ATR (user-defined lookback).

- Use: Tells whether volatility is expanding (positive delta) or contracting (negative delta).

- Visual: Green line for rising momentum, red for declining.

🟣 ATR Delta Slope

- Definition: Measures acceleration in momentum.

- Use: Helps identify early signs of breakout buildup.

- Visual: Purple line. Watch for slope turning up from below.

🟡 Volatility Squeeze (Yellow Dot)

- Definition: Current ATR is significantly lower than its 20-period average.

- Use: Indicates the market is coiling—possible breakout ahead.

🔼 Momentum Start (Green Triangle)

- Definition: ATR Delta slope turns from negative to positive.

- Use: Early warning to prepare for volatility expansion.

🔷 Breakout Confirmation (Blue Label Up)

- Definition: ATR Delta exceeds its high of the last 10 candles.

- Use: Confirms volatility breakout—trade opportunity if direction aligns.

🟩/🟥 Background Color

- Green Background: Momentum rising (positive ATR delta)

- Red Background: Momentum falling (negative ATR delta)

- Yellow Tint: Active squeeze zone

---

✅ How to Use It (Futures/Options Focus)

Step-by-Step:

1. Squeeze Detected (Yellow Dot) → Stay alert. Market is coiling.

2. Green Triangle Appears → Momentum is starting to rise.

3. Background Turns Green → Confirmed rising momentum.

4. Blue Label Appears → Confirmed breakout (enter trade if trend aligns).

Directional Bias:

- Use your main chart setup (price action, EMAs, trendlines, etc.) to decide direction (Call or Put, Long or Short).

- ATR Momentum only tells you how strong the move is—not which way.

---

⚙️ Inputs & Settings

- ATR Period: Default 14 (core volatility measure)

- Rolling Lookback: Used to calculate delta (default 5)

- Slope Length: Used to measure acceleration (default 3)

- Squeeze Factor: Default 0.8 — lower = more sensitive squeeze detection

- Breakout Lookback: Checks ATR delta against last X bars (default 10)

---

🧠 Pro Tips

- Works great when paired with EMA stacks, price structure, or breakout patterns.

- Avoid taking trades based only on squeeze or momentum—combine with chart confirmation.

- If background turns red after a breakout, it may be losing momentum—book partials or tighten stops.

---

🧭 Ideal For:

- Nifty/BankNifty Futures

- Option directional trades (call/put buying)

- Index scalping and momentum swing setups

---

Use this tool as your volatility compass—it won't tell you where to go, but it'll tell you when the wind is strong enough to move fast.

End of Manual