Historical Volatility based Standard DeviationThis Plots the Standard Deviation Price Band based on the Historical Volatility. SD 1, 2, 3. List of All my Indicators - www.tradingview.comИндикатор Pine Script®от UDAY_C_Santhakumar33290

Historical Volatility Strategy Strategy buy when HVol above BuyBand and close position when HVol below CloseBand. Markets oscillate from periods of low volatility to high volatility and back. The author`s research indicates that after periods of extremely low volatility, volatility tends to increase and price may move sharply. This increase in volatility tends to correlate with the beginning of short- to intermediate-term moves in price. They have found that we can identify which markets are about to make such a move by measuring the historical volatility and the application of pattern recognition. The indicator is calculating as the standard deviation of day-to-day logarithmic closing price changes expressed as an annualized percentage.Индикатор Pine Script®от HPotter1010 1 K

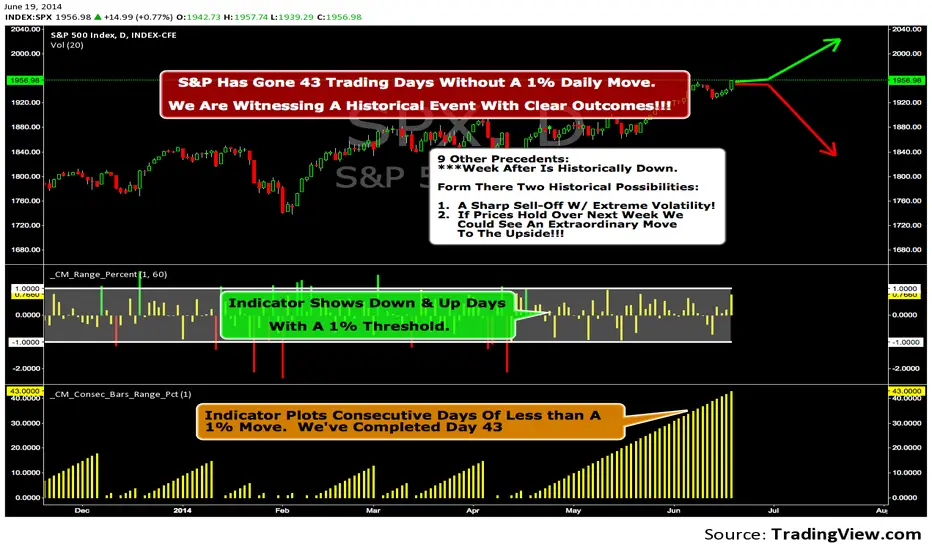

We Are Witnessing A Historical Event With A Clear Outcome!!!"Full Disclosure: I came across this information from www.SentimenTrader.com I have no financial affiliation…They provide incredible statistical facts on The General Market, Currencies, and Futures. They offer a two week free trial. I Highly Recommend. The S&P 500 has gone 43 trading days without a 1% daily move, up or down. which is the equivalent of two months and one day in trading days. During this stretch, the S&P has gained more than 4%, and it has notched a 52-week high recently as well. Since 1952, there were nine other precedents. All of these went 42 trading days without a 1% move, all of them saw the S&P gain at least 4% during their streaks, and all of them saw the S&P close at a 52-week highs. ***There was consistent weakness a week later, with only three gainers, and all below +0.5%. ***After that, stocks did better, often continuing an Extraordinary move higher. Charts can sometimes give us a better nuance than numbers from a table, and from the charts we can see a general pattern - ***if stocks held up well in the following weeks, then they tended to do extremely well in the months ahead. ***If stocks started to stumble after this two- month period of calm, however, then the following months tended to show a lot more volatility. We already know we're seeing an exceptional market environment at the moment, going against a large number of precedents that argued for weakness here, instead of the rally we've seen. If we continue to head higher in spite of everything, these precedents would suggest that we're in the midst of something that could be TRULY EXTRAORDINARY.Индикатор Pine Script®от ChrisMoody1212544

Statistical Volatility - Extreme Value Method This indicator used to calculate the statistical volatility, sometime called historical volatility, based on the Extreme Value Method. Please use this link to get more information about Volatility. Индикатор Pine Script®от HPotter330