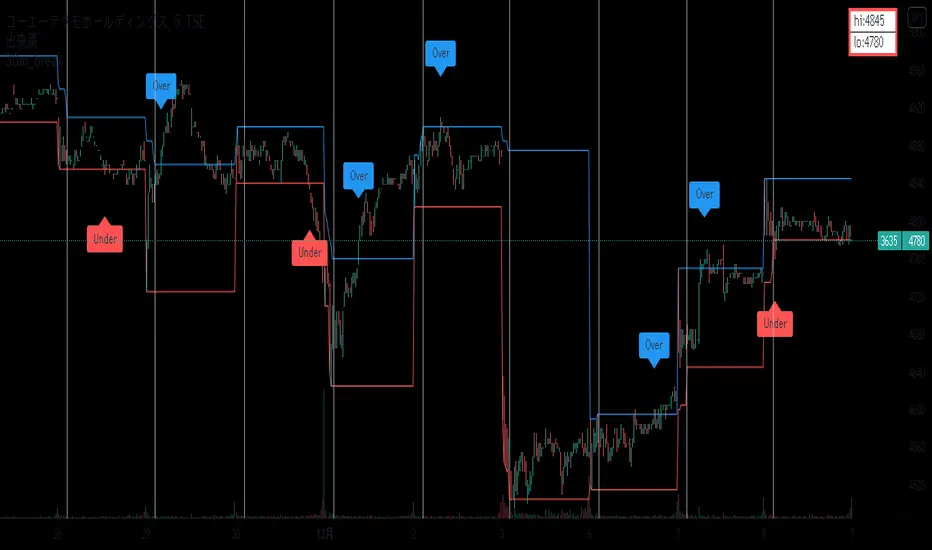

30min_breakEnglish:

It is an indicator that displays the high and low prices as of 30 minutes before the event,

and when you break it, you can see it with a balloon.

The high and low lines at 30 minutes before the front are shown as candidates for support lines and resistance lines.

Used in the minute chart

Japanese:

前場 30分時点の 高値・安値の線を表示し、そこをBreakしたら吹き出しでわかるようにしたインジケーターです

前場 30分時点の 高値安値の線を支持線・抵抗線の候補として図示します。

分足のチャートで利用します

Поиск скриптов по запросу "价格在30元内股票"

30min_breakEnglish:

It is an indicator that displays the high and low prices as of 30 minutes before the event,

and when you break it, you can see it with a balloon.

The high and low lines at 30 minutes before the front are shown as candidates for support lines and resistance lines.

Used in the minute chart

Japanese:

前場 30分時点の 高値・安値の線を表示し、そこをBreakしたら吹き出しでわかるようにしたインジケーターです

前場 30分時点の 高値安値の線を支持線・抵抗線の候補として図示します。

分足のチャートで利用します

Timeframe Time of Day Buying and Selling StrategyThis strategy allows you to back test longing or shorting or do nothing during time increments of 30 minutes. The price trends in one direction every 30 minutes and this strategy allows you to test various 30 minute time frames across a range of dates to capitalize on this.

Make sure you are in the 30 minute time frame while viewing the performance and trade history.

McClellan Oscillator for DAX (GER30) [aftabmk modified]About McClellan Oscillator

Developed by Sherman and Marian McClellan, the McClellan Oscillator is a breadth indicator derived from Net Advances, the number of advancing issues less the number of declining issues. Subtracting the 39-day exponential moving average of Net Advances from the 19-day exponential moving average of Net Advances forms the oscillator.

As the formula reveals, the McClellan Oscillator is a momentum indicator that works similar to MACD .

McClellan Oscillator signals can be generated with breadth thrusts, centerline crossovers, overall levels and divergences.

About my version

This version here is a modification, though:

- It can only be used on the DAX index (DAX 30 or GER 30)

- It only considers the DAX 30 stocks

- The data window will provide a summary about rising and declining stocks

- The data window will output the last change for each of the 30 stocks

BUG

I am only publishing this version because I am not sure if my current version is saved when I leave tradingview.com without publishing the script.

This version still contains a bug - the if/else clauses do not correctly recognize declining stocks. So the oscillator should not be used as it is.

Working on it these days. Feel free to provide feedback!

Stuff I am working on

- Coloring the area green/red according to the value

- Fixing this bug/making this script more efficient

DISCLAIMER

This script was mainly written for educational purposes (training myself how to write custom indicatotors).

As you can see, the code is really messy.

Credits

Based on the simple version of aftabmk

You can find the original version by searching for McClellan Oscillator for nifty 50.

Gann RetracementThe indicator is based on W. D. Gann's method of retracement studies. Gann looked at stock retracement action in terms of Halves (1/2), Thirds (1/3, 2/3), Fifths (1/5, 2/5, 3/5, and 4/5) and more importantly the Eighths (1/8, 2/8, 3/8, 4/8, 5/8, 6/8, and 7/8). Needless to say, {2, 3, 5, 8} are the only Fibonacci numbers between 1 to 10. These ratios can easily be visualized in the form of division of a Circle as follows :

Divide the circle in 12 equal parts of 30 degree each to produce the Thirds :

30 x 4 = 120 is 1/3 of 360

30 x 8 = 240 is 2/3 of 360

The 30 degree retracement captures fundamental geometric shapes like a regular Triangle (120-240-360), a Square (90-180-270-360), and a regular Hexagon (60-120-180-240-300-360) inscribed inside of the circle.

Now, divide the circle in 10 equal parts of 36 degree each to produce the Fifths :

36 x 2 = 72 is 1/5 of 360

36 x 4 = 144 is 2/5 of 360

36 x 6 = 216 is 3/5 of 360

36 x 8 = 288 is 4/5 of 360

where, (72-144-216-288-360) is a regular Pentagon.

Finally, divide the circle in 8 equal parts of 45 degree each to produce the Eighths :

45 x 1 = 45 is 1/8 of 360

45 x 2 = 90 is 2/8 of 360

45 x 3 = 135 is 3/8 of 360

45 x 4 = 180 is 4/8 of 360

45 x 5 = 225 is 5/8 of 360

45 x 6 = 270 is 6/8 of 360

45 x 7 = 315 is 7/8 of 360

where, (45-90-135-180-225-270-315-360) is a regular Octagon.

How to Use this indicator ?

The indicator generates Gann retracement levels between any two significant price points, such as a high and a low.

Input :

Swing High (significant high price point, such as a top)

Swing Low (significant low price point, such as a bottom)

Degree (degree of retracement)

Output :

Gann retracement levels (color coded as follows) :

Swing High and Swing Low (BLUE)

50% retracement (ORANGE)

Retracements between Swing Low and 50% level (RED)

Retracements between 50% level and Swing High (LIME)

Bollinger Bands %B + ATR This indicator is best suitable for the 30-minutes interval OIL charts, due to ATR accuracy.

BB%B is great for showing oversold/overbought market conditions and offers excellent entry/exit opportunities for Day Trading (30 minutes chart), as well as reliable convergence/divergence patterns. ATR is conveniently combined and shows potential market volatility levels for the day when used in 30-minutes charts, thus demarcating your day trade exit point.

To use the ATR on this indicator: Just read the ATR value of the lowest (for a new bull trend) or the highest (for a new bear trend) candlestick of the newly formed trend leg. Let's suppose the ATR reads 0.2891, then you project a move of 2.891 points towards the given trend direction using the ruler tool (30-minutes charts). That's all, and there you have your take profit target!

Good Luck!!!

ADX strategy (considering ADX and +DI only )I have been checking the strategies on ADX indicator.

I have found that +DI crossing above ADX line under threshold 30 and exit on crossdown when ADX above 30 has better results than just following crossovers of +DI and -DI , ADX crossing above 30 .

BUY Rule

========

fast ema is above slow ema (default 13 and 55 , you can change these values in settings)

+DI cross above ADX well beloe threshold level (default 30)

Exit reule

========

when +DI cross down ADX , well above on threshold level

Stop Loss

=========

Default is set to 8%

Take a look and let me know how your symbol works with this strategy

Note : Bar color changes to yellow when the BUY condition is met.

Bar color and Background color shows to blue --- if Long position is active

fast ema and long ema doesnt print on the chart -- please add manually to the chart

Warning : for the use of educational purposes only

EulerMethod: DeltaEN

Shows the Integral Volume Delta (IVD)

It is a detailed OBV. Each bar sums up the volume for bars of a shorter timeframe.

For example, inside a 1M bar, every 12h bar is added up, and inside a 1h bar, every 1min bar is added. Thus, a conditional volume delta inside the bar is obtained.

The indicator for each bar shows the volume of purchases (positive), sales (negative) and the difference — IVD

The delta histogram is thicker than the volume histograms

Settings detalisation

M — 6 hours, 12 hours and 1 day for the M timeframe (720 by default)

W — 4 hours, 6 hours and 12 hours for the W timeframe (240 by default)

D — 30 minutes, 1 hour and 2 hours for the D timeframe (60 by default)

H — 1 minute, 5 minutes and 15 minutes for timeframes [1h, D) (default is 1)

For timeframes of 15m and less, the calculation is carried out by minute bars

VSA mode

The classic OBV adds volume to the cumulative sum under the condition Сlose (n) > Close (n-1) and subtracts it under the condition Close (n) < Close (n-1)

When VSA mode is disabled, all volumes are summed up under these conditions.

When the VSA approximation is turned on, the volume per bar of detail is divided by the factor (Close - Low) / (High - Low)

That is, it takes into account the spread per bar and closing relative to the spread. VSA is enabled by default

A/D mode

Shows the cumulative Accumulation / Distribution Index

The delta of the detail bar is multiplied by (High + Low + Close) / 3 bars, the result is added to the cumulative sum

No additional price conversions required due to integral summation

Index line view is customizable

EM Delta does not receive intermediate values in real time.

To see the result, wait until the bar closes or switch to a smaller timeframe

RU

Показывает Интегральную Дельту Объёма (ИДО)

Представляет собой детализированный OBV. В каждом баре суммируется объём за бары меньшего таймфрейма.

Например, внутри 1М-бара суммируется каждый 12h-бар, а внутри 1h — каждый 1m-бар. Таким образом получается условная дельта объёма внутри бара

Индикатор на каждый бар показывает объём покупок (положительный), объём продаж (отрицательный) и разницу — ИДО

Гистограмма дельты толще гистограмм объёмов

Настройки детализации внутри бара

M — 6 часов, 12 часов и 1 день для таймфрейма M (по-умолчанию 720)

W — 4 часа, 6 часов и 12 часов для таймфрейма W (по-умолчанию 240)

D — 30 минут, 1 час и 2 часа для таймфрейма D (по-умолчанию 60)

H — 1 минута, 5 минут и 15 минут для таймфреймов [1h, D) (по-умолчанию 1)

Для таймфреймов 15m и меньше расчёт ведётся по минутным барам

Режим VSA

Классический OBV прибавляет объём к кумулятивной сумме при условии Сlose(n) > Close(n-1) и отнимает при условии Close(n) < Close(n-1)

При отключении режима VSA все объёмы суммируются по этим условиям

При включённой VSA-аппроксимации объём за бар детализации делится по фактору (Close - Low) / (High - Low)

То есть учитывает спред за бар и закрытие относительно спреда. По-умолчанию режим VSA включен

Режим A/D

Показывает кумулятивный индекс Накопления/Распределения

Дельта бара детализации умножается на (High + Low + Close) / 3 бара, результат прибавляется к кумулятивной сумме

Дополнительные преобразования цены не требуются ввиду интегрального суммирования

Вид линии индекса настраивается

EM Delta не получает промежуточные значения в реальном времени.

Чтобы увидеть результат, дождитесь закрытия бара или перейдите на меньший таймфрейм

Crypto Trading Hours UTC based on Berlin time (UTC +2)Although crypto markets trade 24/7, there are spikes in volume according to the general hours at which different parts of the world do the majority of their trading.

This Script highlights the US, European and Asian markets when they are most active. The normal market hours are always from 08:00 to 16:30 local time.

US market opens at 8:00 Silicon Valley local time, and closes at 16:30 New York local time.

European market opens at 8:00 London local time, and closes at 16:30 Frankfurt local time.

Asian market opens at 8:00 Hong Kong local time, and closes at 16:30 Sydney local time.

Supertrend MTF LAG ISSUEThis script based on

we all use Super trend but it main issue is the lag as it buy too late or sell too late

using Deavaet study of Heat map MTF we can do a little trick

if you look on his study you can see that major signal for example will happen in the time frame before it happen at larger time frame

so in this example if signal at MTF 30 min and signal at MTF 60 min happen at the same time at 2 hours or 4 hours candles then this signal are more likely to be true then random signal at each time frame specific.

since we use shorter time frame on larger time frame we can remove the lag issue that make supertrend not so effective

In this example I set the signal to be MTF 30 +60 om 2 hour TF , can be good also for 4 hour candles..

So you get the signal to close inside the larger candle

now if you want to make on even shorter TF then change the code to 15 and 30 MTF on candles on 1 hour

or 1 and 5 min on 30 min or 15 min

Panchang Time//This indicator is required in NimblrTA and can be used to define timeslots for the trend confirmation

study("Panchang Time", overlay=true)

timeinrange(res, sess) => time(res, sess) != 0

premarket = #C0C0C0

regular = #0000FF

regularslot2 = #00CCFF

postmarket = #5000FF

notrading = na

sessioncolor = timeinrange("30", "0915-0930") ? premarket : timeinrange("30", "0915-0930") ? regular : timeinrange("30", "0931-1200") ? regularslot2 : timeinrange("30", "1201-1305") ? postmarket : notrading

bgcolor(sessioncolor, transp=90)

extended session - Regular Opening-Range- JayyOpening Range and some other scripts updated to plot correctly (see comments below.) There are three variations of the fibonacci expansion beyond the opening range and retracements within the opening range of the US Market session - I have not put in the script for the other markets yet.

The three scripts have different uses and strengths:

The extended session script (with the script here below) will plot the opening range whether you are using the extended session or the regular session. (that is to say whether "ext" in the lower right hand corner is highlighted or not.). While in the extended session the opening range has some plotting issues with periods like 13 minutes or any period that is not divisible into 330 mins with a round number outcome (eg 330/60 =5.5. Therefore an hour long opening range has problems in the extended session.

The pre session script is only for the premarket. You can select any opening range period you like. I have set the opening range to be the full premarket session. If you select a different session you will have to unselect "pre open to 9:30 EST for Opening Range?" in the format section. The script defaults to 15 minutes in the "period Of Pre Opening Range?". To go back to the 4 am to 9:30 pre opening range select "pre open to 9:30 EST for Opening Range?" there is no automatic 330 minute selection.

The past days offset script only works in 5 min or 15 minute period. It will show the opening range from up to 20 days past over the current days price action. Use this for the regular session only. 0 shows the current day's opening range. Use the positive integers for number of days back ie 1, 2, 3 etc not -1, -2, -3 etc. The script is preprogrammed to use the current day (0).

Scripts updated to plot correctly: One thing they all have in common is a way of they deal with a somewhat random problem that shifts the plots 4 hours in one direction or the other ie the plot started at 9:30 EST or 1:30PM EST. This issue started to occur approximately June 22, 2015 and impacts any script that tried to use "session" times to manage a plot in my scripts. The issue now seems to have been resolved during this past week.

Just in case the problem reoccurs I have added a "Switch session plot?" to each script. If the plot looks funny check or uncheck the "Switch session plot?" and see the difference. Of course if a new issue crops up it will likely require a different fix.

I have updated all of the scripts shown on this chart. If you are using a script of mine that suffers from the compiler issue then you will find an update on this chart. You can get any and all of the scripts by clicking on the small sideways wishbone on the left middle of the chart. You will see a dialogue box. Then click "make it mine". This will import all of the scripts to your computer and you can play around with them all to decide what you want and what you don't want. This is the easiest way to get all of the scripts in one fell swoop. It is also the easiest way for me to make all of the scripts available. I do not have all of the plots visible since it is too messy and one of the scripts (pre OR) is only for the regular session. To view the scripts click on the blue eye to the right of the script title to show it on this script. If you can only use the regular session. The scripts will all (with the exception of the pre OR) work fine.

If for any reason this script seems flakey refresh the page r try a slightly different period. I have noticed that sometimes randomly the script loves to return to the 5 min OR. This is a very new issue transient issue. As always if you see an issue please let me know.

Cheers Jayy

Moving VWAP-KAMA CloudMoving VWAP-KAMA Cloud

Overview

The Moving VWAP-KAMA Cloud is a high-conviction trend filter designed to solve a major problem with standard indicators: Noise. By combining a smoothed Volume Weighted Average Price (MVWAP) with Kaufman’s Adaptive Moving Average (KAMA), this indicator creates a "Value Zone" that identifies the true structural trend while ignoring choppy price action.

Unlike brittle lines that break constantly, this cloud is "slow" by design—making it exceptionally powerful for spotting genuine trend reversals and filtering out fakeouts.

How It Works

This script uses a unique "Double Smoothing" architecture:

The Anchor (MVWAP): We take the standard VWAP and smooth it with a 30-period EMA. This represents the "Fair Value" baseline where volume has supported price over time.

The Filter (KAMA): We apply Kaufman's Adaptive Moving Average to the already smoothed MVWAP. KAMA is unique because it flattens out during low-volatility (choppy) periods and speeds up during high-momentum trends.

The Cloud:

Green/Teal Cloud: Bullish Structure (MVWAP > KAMA)

Purple Cloud: Bearish Structure (MVWAP < KAMA)

🔥 The "Reversal Slingshot" Strategy

Backtests reveal a powerful behavior during major trend changes, particularly after long bear markets:

The Resistance Phase: During a long-term downtrend, price will repeatedly rally into the Purple Cloud and get rejected. The flattened KAMA line acts as a "concrete ceiling," keeping the bearish trend intact.

The Breakout & Flip: When price finally breaks above the cloud with conviction, and the cloud flips Green, it signals a structural regime change.

The "Slingshot" Retest: Often, immediately after this flip, price will drop back into the top of the cloud. This is the "Slingshot" moment. The old resistance becomes new, hardened support.

The Rally: From this support bounce, stocks often launch into a sustained, multi-month bull run. This setup has been observed repeatedly at the bottom of major corrections.

How to Use This Indicator

1. Dynamic Support & Resistance

The KAMA Wall: When price retraces into the cloud, the KAMA line often flattens out, acting as a hard "floor" or "wall." A break of this wall usually signals a genuine trend change, not just a stop hunt.

2. Trend Confirmation (Regime Filter)

Bullish Regime: If price is holding above the cloud, only look for Long setups.

Bearish Regime: If price is holding below the cloud, only look for Short setups.

No-Trade Zone: If price is stuck inside the cloud, the market is traversing fair value. Stand aside until a clear winner emerges.

3. Multi-Timeframe Versatility

While designed for trend confirmation on higher timeframes (4H, Daily), this indicator adapts beautifully to lower timeframes (5m, 15m) for intraday scalping.

On Lower Timeframes: The cloud reacts much faster, acting as a dynamic "VWAP Band" that helps intraday traders stay on the right side of momentum during the session.

Settings

Moving VWAP Period (30): The lookback period for the base VWAP smoothing.

KAMA Settings (10, 10, 30): Controls the sensitivity of the adaptive filter.

Cloud Transparency: Adjust to keep your chart clean.

Alerts Included

Price Cross Over/Under MVWAP

Price Cross Over/Under KAMA

Cloud Flip (Bullish/Bearish Trend Change)

Tip for Traders

This is not a signal entry indicator. It is a Trend Conviction tool. Use it to filter your entries from faster indicators (like RSI or MACD). If your fast indicator signals "Buy" but the cloud is Purple, the probability is low. Wait for the Cloud Flip

Smart RSI MTF Matrix [DotGain]Summary

Are you tired of trading trend signals, only to miss the bigger picture because you are focused on a single timeframe?

The Smart RSI MTF Matrix is the ultimate "Cockpit View" for momentum traders. Unlike chart overlays that can sometimes clutter your price action, this indicator organizes RSI conditions across 10 different timeframes simultaneously into a clean, separate Heatmap pane.

It monitors everything from the 5-minute chart all the way up to the 12-Month view , giving you a complete X-ray vision of the market's momentum structure instantly.

⚙️ Core Components and Logic

The Smart RSI MTF Matrix relies on a sophisticated hierarchy to deliver clear, actionable context:

Multi-Timeframe Engine: The script runs 10 independent RSI calculations in the background, organized in rows from bottom (Short Term) to top (Long Term).

Classic RSI Thresholds:

Overbought (> 70): Indicates price may be extended to the upside.

Oversold (< 30): Indicates price may be extended to the downside.

Smart Visibility System (The "Secret Sauce"): Not all signals are equal. A 5-minute signal is "noise" compared to a Yearly signal. This indicator automatically applies Transparency to differentiate importance. The visibility increases by 10% for each higher timeframe slot (Row).

🚦 How to Read the Matrix

The indicator plots dots in 10 stacked rows. The position and opacity tell you the direction and significance:

🟥 RED DOTS (Overbought Condition)

Trigger: RSI is above 70 on that specific timeframe.

Meaning: Potential bearish reversal or pullback.

🟩 GREEN DOTS (Oversold Condition)

Trigger: RSI is below 30 on that specific timeframe.

Meaning: Potential bullish reversal or bounce.

⚪ GRAY DOTS (Neutral)

Trigger: RSI is between 30 and 70.

Meaning: No extreme momentum present.

👻 TRANSPARENCY (Signal Strength)

The visibility of the dot tells you exactly which Timeframe (Row) is triggered. The higher the row, the more solid the color:

Faint (10-30% Visibility): Rows 1-3 (5m, 15m, 1h). Used for scalping entries.

Medium (40-60% Visibility): Rows 4-6 (4h, 1D, 1W). Used for swing trading context.

Solid (70-100% Visibility): Rows 7-10 (1M, 3M, 6M, 12M). Used for identifying major macro cycles.

Visual Elements

Structure: Row 1 (Bottom) represents the 5-minute timeframe. Row 10 (Top) represents the 12-Month timeframe.

Vertical Alignment: If you see a vertical column of Red or Green dots, it indicates Multi-Timeframe Confluence —a highly probable reversal point.

Key Benefit

The goal of the Smart RSI MTF Matrix is to keep your main chart clean while providing maximum information. You can instantly see if a short-term pullback (Faint Green Dot) is happening within a long-term uptrend (Solid Gray/Red Dot), allowing for precision entries.

Have fun :)

Disclaimer

This "Smart RSI MTF Matrix" indicator is provided for informational and educational purposes only. It does not, and should not be construed as, financial, investment, or trading advice.

The signals generated by this tool (both "Buy" and "Sell" indications) are the result of a specific set of algorithmic conditions. They are not a direct recommendation to buy or sell any asset. All trading and investing in financial markets involves substantial risk of loss. You can lose all of your invested capital.

Past performance is not indicative of future results. The signals generated may produce false or losing trades. The creator (© DotGain) assumes no liability for any financial losses or damages you may incur as a result of using this indicator.

You are solely responsible for your own trading and investment decisions. Always conduct your own research (DYOR) and consider your personal risk tolerance before making any trades.

Patrice - GC M1 Bot (MACD EMA RSI)//@version=6

indicator("Patrice - GC M1 Bot (MACD EMA RSI)", overlay = true)

//----------------------

// Inputs (optimisés GC)

//----------------------

emaLenFast = input.int(9, "EMA rapide")

emaLenSlow = input.int(14, "EMA lente")

rsiLen = input.int(14, "RSI length")

atrLen = input.int(14, "ATR length")

volLen = input.int(20, "Volume moyenne")

slMult = input.float(0.4, "SL = ATR x", step = 0.1)

tpMult = input.float(0.7, "TP = ATR x", step = 0.1)

minAtr = input.float(0.7, "ATR minimum pour trader", step = 0.1)

maxDistEmaPct = input.float(0.3, "Distance max EMA9 (%)", step = 0.1)

//----------------------

// Indicateurs

//----------------------

ema9 = ta.ema(close, emaLenFast)

ema14 = ta.ema(close, emaLenSlow)

= ta.macd(close, 12, 26, 9)

hist = macdLine - signalLine

rsi = ta.rsi(close, rsiLen)

atr = ta.atr(atrLen)

volMa = ta.sma(volume, volLen)

//----------------------

// Session 9:30 - 11:00 (NY)

//----------------------

hourSession = hour(time, "America/New_York")

minuteSession = minute(time, "America/New_York")

inSession = (hourSession == 9 and minuteSession >= 30) or

(hourSession > 9 and hourSession < 11) or

(hourSession == 11 and minuteSession == 0)

//----------------------

// Filtres vol / ATR / distance EMA

//----------------------

volFilter = volume > volMa

atrFilter = atr > minAtr

distEmaPct = math.abs(close - ema9) / close * 100.0

distFilter = distEmaPct < maxDistEmaPct

//----------------------

// Tendance

//----------------------

bullTrend = close > ema9 and close > ema14 and ema9 > ema14

bearTrend = close < ema9 and close < ema14 and ema9 < ema14

//----------------------

// MACD : 2e barre

//----------------------

bullSecondBar = hist > 0 and hist > 0 and hist <= 0

bearSecondBar = hist < 0 and hist < 0 and hist >= 0

//----------------------

// Filtres RSI

//----------------------

rsiLongOk = rsi < 70 and rsi >= 45 and rsi <= 65

rsiShortOk = rsi > 30 and rsi >= 35 and rsi <= 55

//----------------------

// Gestion du risque (simple pour l'instant)

//----------------------

canTradeRisk = true

//----------------------

// Conditions d'entrée

//----------------------

longCond = bullTrend and bullSecondBar and rsiLongOk and inSession and volFilter and atrFilter and distFilter and canTradeRisk

shortCond = bearTrend and bearSecondBar and rsiShortOk and inSession and volFilter and atrFilter and distFilter and canTradeRisk

//----------------------

// SL / TP (info seulement, pas d'ordres)

//----------------------

slPoints = atr * slMult

tpPoints = atr * tpMult

longSL = close - slPoints

longTP = close + tpPoints

shortSL = close + slPoints

shortTP = close - tpPoints

//----------------------

// Visuels

//----------------------

plot(ema9, title = "EMA 9")

plot(ema14, title = "EMA 14")

plotshape(longCond, title = "Signal Long", style = shape.triangleup, location = location.belowbar, size = size.tiny, text = "L")

plotshape(shortCond, title = "Signal Short", style = shape.triangledown, location = location.abovebar, size = size.tiny, text = "S")

//----------------------

// Conditions d'ALERTE

//----------------------

alertcondition(longCond, title = "ALERTE LONG", message = "Signal LONG Patrice GC bot")

alertcondition(shortCond, title = "ALERTE SHORT", message = "Signal SHORT Patrice GC bot")

Smart Money Flow - Exchange & TVL Composite# Smart Money Flow - Exchange & TVL Composite Indicator

## Overview

The **Smart Money Flow (SMF)** indicator combines two powerful on-chain metrics - **Exchange Flows** and **Total Value Locked (TVL)** - to create a composite index that tracks institutional and "smart money" movement in the cryptocurrency market. This indicator helps traders identify accumulation and distribution phases by analyzing where capital is flowing.

## What It Does

This indicator normalizes and combines:

- **Exchange Net Flow** (from IntoTheBlock): Tracks Bitcoin/Ethereum movement to and from exchanges

- **Total Value Locked** (from DefiLlama): Measures capital locked in DeFi protocols

The composite index is displayed on a 0-100 scale with clear zones for overbought/oversold conditions.

## Core Concept

### Exchange Flows

- **Negative Flow (Outflows)** = Bullish Signal

- Coins moving OFF exchanges → Long-term holding/accumulation

- Indicates reduced selling pressure

- **Positive Flow (Inflows)** = Bearish Signal

- Coins moving TO exchanges → Preparation for selling

- Indicates potential distribution phase

### Total Value Locked (TVL)

- **Rising TVL** = Bullish Signal

- Capital flowing into DeFi protocols

- Increased ecosystem confidence

- **Falling TVL** = Bearish Signal

- Capital exiting DeFi protocols

- Decreased ecosystem confidence

### Combined Signals

**🟢 Strong Bullish (70-100):**

- Exchange outflows + Rising TVL

- Smart money accumulating and deploying capital

**🔴 Strong Bearish (0-30):**

- Exchange inflows + Falling TVL

- Smart money preparing to sell and exiting positions

**⚪ Neutral (40-60):**

- Mixed or balanced flows

## Key Features

### ✅ Auto-Detection

- Automatically detects chart symbol (BTC/ETH)

- Uses appropriate exchange flow data for each asset

### ✅ Weighted Composite

- Customizable weights for Exchange Flow and TVL components

- Default: 50/50 balance

### ✅ Normalized Scale

- 0-100 index scale

- Configurable lookback period for normalization (default: 90 days)

### ✅ Signal Zones

- **Overbought**: 70+ (Strong bullish pressure)

- **Oversold**: 30- (Strong bearish pressure)

- **Extreme**: 85+ / 15- (Very strong signals)

### ✅ Clean Interface

- Minimal visual clutter by default

- Only main index line and MA visible

- Optional elements can be enabled:

- Background color zones

- Divergence signals

- Trend change markers

- Info table with detailed metrics

### ✅ Divergence Detection

- Identifies when price diverges from smart money flows

- Potential reversal warning signals

### ✅ Alerts

- Extreme overbought/oversold conditions

- Trend changes (crossing 50 line)

- Bullish/bearish divergences

## How to Use

### 1. Trend Confirmation

- Index above 50 = Bullish trend

- Index below 50 = Bearish trend

- Use with price action for confirmation

### 2. Reversal Signals

- **Extreme readings** (>85 or <15) suggest potential reversal

- Look for divergences between price and indicator

### 3. Accumulation/Distribution

- **70+**: Accumulation phase - smart money buying/holding

- **30-**: Distribution phase - smart money selling

### 4. DeFi Health

- Monitor TVL component for DeFi ecosystem strength

- Combine with exchange flows for complete picture

## Settings

### Data Sources

- **Exchange Flow**: IntoTheBlock real-time data

- **TVL**: DefiLlama aggregated DeFi TVL

- **Manual Mode**: For testing or custom data

### Indicator Settings

- **Smoothing Period (MA)**: Default 14 periods

- **Normalization Lookback**: Default 90 days

- **Exchange Flow Weight**: Adjustable 0-100%

- **Overbought/Oversold Levels**: Customizable thresholds

### Visual Options

- Show/Hide Moving Average

- Show/Hide Zone Lines

- Show/Hide Background Colors

- Show/Hide Divergence Signals

- Show/Hide Trend Markers

- Show/Hide Info Table

## Data Requirements

⚠️ **Important Notes:**

- Uses **daily data** from IntoTheBlock and DefiLlama

- Works on any chart timeframe (data updates daily)

- Auto-switches between BTC and ETH based on chart

- All other crypto charts default to BTC exchange flow data

## Best Practices

1. **Use on Daily+ Timeframes**

- On-chain data is daily, most effective on D/W/M charts

2. **Combine with Price Action**

- Use as confirmation, not standalone signals

3. **Watch for Divergences**

- Price making new highs while indicator falling = warning

4. **Monitor Extreme Zones**

- Sustained readings >85 or <15 indicate strong conviction

5. **Context Matters**

- Consider broader market conditions and fundamentals

## Calculation

1. **Exchange Net Flow** = Inflows - Outflows (inverted for index)

2. **TVL Rate of Change** = % change over smoothing period

3. **Normalize** both metrics to 0-100 scale

4. **Composite Index** = (ExchangeFlow × Weight) + (TVL × Weight)

5. **Smooth** with moving average

## Disclaimer

This indicator uses on-chain data for analysis. While valuable, it should not be used as the sole basis for trading decisions. Always combine with other technical analysis tools, fundamental analysis, and proper risk management.

On-chain data reflects blockchain activity but may lag price action. Use this indicator as part of a comprehensive trading strategy.

---

## Credits

**Data Sources:**

- IntoTheBlock: Exchange flow metrics

- DefiLlama: Total Value Locked data

**Indicator by:** @iCD_creator

**Version:** 1.0

**Pine Script™ Version:** 6

---

## Updates & Support

For questions, suggestions, or bug reports, please comment below or message the author.

**Like this indicator? Leave a 👍 and share your feedback!**

Hash Supertrend [Hash Capital Research]Hash Supertrend Strategy by Hash Capital Research

Overview

Hash Supertrend is a professional-grade trend-following strategy that combines the proven Supertrend indicator with institutional visual design and flexible time filtering.

The strategy uses ATR-based volatility bands to identify trend direction and executes position reversals when the trend flips.This implementation features a distinctive fluorescent color system with customizable glow effects, making trend changes immediately visible while maintaining the clean, professional aesthetic expected in quantitative trading environments.

Entry Signals:

Long Entry: Price crosses above the Supertrend line (trend flips bullish)

Short Entry: Price crosses below the Supertrend line (trend flips bearish)

Controls the lookback period for volatility calculation

Lower values (7-10): More sensitive to price changes, generates more signals

Higher values (12-14): Smoother response, fewer signals but potentially delayed entries

Recommended range: 7-14 depending on market volatility

Factor (Default: 3.0)

Restricts trading to specific hours

Useful for avoiding low-liquidity sessions, overnight gaps, or known choppy periods

When disabled, strategy trades 24/7

Start Hour (Default: 9) & Start Minute (Default: 30)

Define when the trading session begins

Uses exchange timezone in 24-hour format

Example: 9:30 = 9:30 AM

End Hour (Default: 16) & End Minute (Default: 0)

Controls the vibrancy of the fluorescent color system

1-3: Subtle, muted colors

4-6: Balanced, moderate saturation

7-10: Bright, highly saturated fluorescent appearance

Affects both the Supertrend line and trend zones

Glow Effect (Default: On)

Adds luminous halo around the Supertrend line

Creates a multi-layered visual with depth

Particularly effective during strong trends

Glow Intensity (Default: 5.0)

Displays tiny fluorescent dots at entry points

Green dot below bar: Long entry

Red dot above bar: Short entry

Provides clear visual confirmation of executed trades

Show Trend Zone (Default: On)

Strong trending markets (2020-style bull runs, sustained bear markets)

Markets with clear directional bias

Instruments with consistent volatility patterns

Timeframes: 15m to Daily (optimal on 1H-4H)

Challenging Conditions:

Choppy, range-bound markets

Low volatility consolidation periods

Highly news-driven instruments with frequent gaps

Very low timeframes (1m-5m) prone to noise

Recommended AssetsCryptocurrency:

Steff- OBX- DTA OBX – US Open 15-Minute Zone Indicator

This indicator highlights the first 15 minutes of the U.S. stock market opening, also known as the OBX (Opening Balance Extension).

It is designed specifically for Nasdaq and S&P 500, which open at 09:30 New York time — corresponding to 15:30 Danish time.

What this indicator does:

• Marks the price range from 09:30–09:45 (U.S. time) as a zone on your chart

• Automatically adjusts to your local timezone, so the zone always aligns with Danish time

• Extends the zone to the right so you can track how price interacts with OBX throughout the day

• Draws all historical OBX zones so you can analyze previous reactions

• Rebuilds zones automatically when switching timeframes

• Detects breakouts from the zone

• Tracks balancing time only after a real breakout occurs

• Can automatically remove a zone if price spends a continuous amount of time inside it after the breakout (you set the minutes yourself)

• Allows full customization of OBX start time, duration, and behavior

• Individual zones can be manually deleted without being redrawn by the indicator

Why the OBX matters:

The OBX represents one of the most influential time windows in intraday trading because it reflects:

• The first injection of liquidity after the U.S. market opens

• Institutional positioning and algorithmic adjustments

• Early volatility and directional bias

• Common zones for reversals, breakouts, or mean reversion

• Key high-probability reaction levels used by professional traders

This indicator gives you a clear visual representation of when the market reacts to the U.S. open and how price interacts with the opening range throughout the session.

Kripto Fema ind/ This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © Femayakup

//@version=5

indicator(title = "Kripto Fema ind", shorttitle="Kripto Fema ind", overlay=true, format=format.price, precision=2,max_lines_count = 500, max_labels_count = 500, max_bars_back=500)

showEma200 = input(true, title="EMA 200")

showPmax = input(true, title="Pmax")

showLinreg = input(true, title="Linreg")

showMavilim = input(true, title="Mavilim")

showNadaray = input(true, title="Nadaraya Watson")

ma(source, length, type) =>

switch type

"SMA" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA (RMA)" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

//Ema200

timeFrame = input.timeframe(defval = '240',title= 'EMA200 TimeFrame',group = 'EMA200 Settings')

len200 = input.int(200, minval=1, title="Length",group = 'EMA200 Settings')

src200 = input(close, title="Source",group = 'EMA200 Settings')

offset200 = input.int(title="Offset", defval=0, minval=-500, maxval=500,group = 'EMA200 Settings')

out200 = ta.ema(src200, len200)

higherTimeFrame = request.security(syminfo.tickerid,timeFrame,out200 ,barmerge.gaps_on,barmerge.lookahead_on)

ema200Plot = showEma200 ? higherTimeFrame : na

plot(ema200Plot, title="EMA200", offset=offset200)

//Linreq

group1 = "Linreg Settings"

lengthInput = input.int(100, title="Length", minval = 1, maxval = 5000,group = group1)

sourceInput = input.source(close, title="Source")

useUpperDevInput = input.bool(true, title="Upper Deviation", inline = "Upper Deviation", group = group1)

upperMultInput = input.float(2.0, title="", inline = "Upper Deviation", group = group1)

useLowerDevInput = input.bool(true, title="Lower Deviation", inline = "Lower Deviation", group = group1)

lowerMultInput = input.float(2.0, title="", inline = "Lower Deviation", group = group1)

group2 = "Linreg Display Settings"

showPearsonInput = input.bool(true, "Show Pearson's R", group = group2)

extendLeftInput = input.bool(false, "Extend Lines Left", group = group2)

extendRightInput = input.bool(true, "Extend Lines Right", group = group2)

extendStyle = switch

extendLeftInput and extendRightInput => extend.both

extendLeftInput => extend.left

extendRightInput => extend.right

=> extend.none

group3 = "Linreg Color Settings"

colorUpper = input.color(color.new(color.blue, 85), "Linreg Renk", inline = group3, group = group3)

colorLower = input.color(color.new(color.red, 85), "", inline = group3, group = group3)

calcSlope(source, length) =>

max_bars_back(source, 5000)

if not barstate.islast or length <= 1

else

sumX = 0.0

sumY = 0.0

sumXSqr = 0.0

sumXY = 0.0

for i = 0 to length - 1 by 1

val = source

per = i + 1.0

sumX += per

sumY += val

sumXSqr += per * per

sumXY += val * per

slope = (length * sumXY - sumX * sumY) / (length * sumXSqr - sumX * sumX)

average = sumY / length

intercept = average - slope * sumX / length + slope

= calcSlope(sourceInput, lengthInput)

startPrice = i + s * (lengthInput - 1)

endPrice = i

var line baseLine = na

if na(baseLine) and not na(startPrice) and showLinreg

baseLine := line.new(bar_index - lengthInput + 1, startPrice, bar_index, endPrice, width=1, extend=extendStyle, color=color.new(colorLower, 0))

else

line.set_xy1(baseLine, bar_index - lengthInput + 1, startPrice)

line.set_xy2(baseLine, bar_index, endPrice)

na

calcDev(source, length, slope, average, intercept) =>

upDev = 0.0

dnDev = 0.0

stdDevAcc = 0.0

dsxx = 0.0

dsyy = 0.0

dsxy = 0.0

periods = length - 1

daY = intercept + slope * periods / 2

val = intercept

for j = 0 to periods by 1

price = high - val

if price > upDev

upDev := price

price := val - low

if price > dnDev

dnDev := price

price := source

dxt = price - average

dyt = val - daY

price -= val

stdDevAcc += price * price

dsxx += dxt * dxt

dsyy += dyt * dyt

dsxy += dxt * dyt

val += slope

stdDev = math.sqrt(stdDevAcc / (periods == 0 ? 1 : periods))

pearsonR = dsxx == 0 or dsyy == 0 ? 0 : dsxy / math.sqrt(dsxx * dsyy)

= calcDev(sourceInput, lengthInput, s, a, i)

upperStartPrice = startPrice + (useUpperDevInput ? upperMultInput * stdDev : upDev)

upperEndPrice = endPrice + (useUpperDevInput ? upperMultInput * stdDev : upDev)

var line upper = na

lowerStartPrice = startPrice + (useLowerDevInput ? -lowerMultInput * stdDev : -dnDev)

lowerEndPrice = endPrice + (useLowerDevInput ? -lowerMultInput * stdDev : -dnDev)

var line lower = na

if na(upper) and not na(upperStartPrice) and showLinreg

upper := line.new(bar_index - lengthInput + 1, upperStartPrice, bar_index, upperEndPrice, width=1, extend=extendStyle, color=color.new(colorUpper, 0))

else

line.set_xy1(upper, bar_index - lengthInput + 1, upperStartPrice)

line.set_xy2(upper, bar_index, upperEndPrice)

na

if na(lower) and not na(lowerStartPrice) and showLinreg

lower := line.new(bar_index - lengthInput + 1, lowerStartPrice, bar_index, lowerEndPrice, width=1, extend=extendStyle, color=color.new(colorUpper, 0))

else

line.set_xy1(lower, bar_index - lengthInput + 1, lowerStartPrice)

line.set_xy2(lower, bar_index, lowerEndPrice)

na

showLinregPlotUpper = showLinreg ? upper : na

showLinregPlotLower = showLinreg ? lower : na

showLinregPlotBaseLine = showLinreg ? baseLine : na

linefill.new(showLinregPlotUpper, showLinregPlotBaseLine, color = colorUpper)

linefill.new(showLinregPlotBaseLine, showLinregPlotLower, color = colorLower)

// Pearson's R

var label r = na

label.delete(r )

if showPearsonInput and not na(pearsonR) and showLinreg

r := label.new(bar_index - lengthInput + 1, lowerStartPrice, str.tostring(pearsonR, "#.################"), color = color.new(color.white, 100), textcolor=color.new(colorUpper, 0), size=size.normal, style=label.style_label_up)

//Mavilim

group4 = "Mavilim Settings"

mavilimold = input(false, title="Show Previous Version of MavilimW?",group=group4)

fmal=input(3,"First Moving Average length",group = group4)

smal=input(5,"Second Moving Average length",group = group4)

tmal=fmal+smal

Fmal=smal+tmal

Ftmal=tmal+Fmal

Smal=Fmal+Ftmal

M1= ta.wma(close, fmal)

M2= ta.wma(M1, smal)

M3= ta.wma(M2, tmal)

M4= ta.wma(M3, Fmal)

M5= ta.wma(M4, Ftmal)

MAVW= ta.wma(M5, Smal)

col1= MAVW>MAVW

col3= MAVWpmaxsrc ? pmaxsrc-pmaxsrc : 0

vdd1=pmaxsrc

ma = 0.0

if mav == "SMA"

ma := ta.sma(pmaxsrc, length)

ma

if mav == "EMA"

ma := ta.ema(pmaxsrc, length)

ma

if mav == "WMA"

ma := ta.wma(pmaxsrc, length)

ma

if mav == "TMA"

ma := ta.sma(ta.sma(pmaxsrc, math.ceil(length / 2)), math.floor(length / 2) + 1)

ma

if mav == "VAR"

ma := VAR

ma

if mav == "WWMA"

ma := WWMA

ma

if mav == "ZLEMA"

ma := ZLEMA

ma

if mav == "TSF"

ma := TSF

ma

ma

MAvg=getMA(pmaxsrc, length)

longStop = Normalize ? MAvg - Multiplier*atr/close : MAvg - Multiplier*atr

longStopPrev = nz(longStop , longStop)

longStop := MAvg > longStopPrev ? math.max(longStop, longStopPrev) : longStop

shortStop = Normalize ? MAvg + Multiplier*atr/close : MAvg + Multiplier*atr

shortStopPrev = nz(shortStop , shortStop)

shortStop := MAvg < shortStopPrev ? math.min(shortStop, shortStopPrev) : shortStop

dir = 1

dir := nz(dir , dir)

dir := dir == -1 and MAvg > shortStopPrev ? 1 : dir == 1 and MAvg < longStopPrev ? -1 : dir

PMax = dir==1 ? longStop: shortStop

plot(showsupport ? MAvg : na, color=#fbff04, linewidth=2, title="EMA9")

pALL=plot(PMax, color=color.new(color.red, transp = 0), linewidth=2, title="PMax")

alertcondition(ta.cross(MAvg, PMax), title="Cross Alert", message="PMax - Moving Avg Crossing!")

alertcondition(ta.crossover(MAvg, PMax), title="Crossover Alarm", message="Moving Avg BUY SIGNAL!")

alertcondition(ta.crossunder(MAvg, PMax), title="Crossunder Alarm", message="Moving Avg SELL SIGNAL!")

alertcondition(ta.cross(pmaxsrc, PMax), title="Price Cross Alert", message="PMax - Price Crossing!")

alertcondition(ta.crossover(pmaxsrc, PMax), title="Price Crossover Alarm", message="PRICE OVER PMax - BUY SIGNAL!")

alertcondition(ta.crossunder(pmaxsrc, PMax), title="Price Crossunder Alarm", message="PRICE UNDER PMax - SELL SIGNAL!")

buySignalk = ta.crossover(MAvg, PMax)

plotshape(buySignalk and showsignalsk ? PMax*0.995 : na, title="Buy", text="Buy", location=location.absolute, style=shape.labelup, size=size.tiny, color=color.new(color.green, transp = 0), textcolor=color.white)

sellSignallk = ta.crossunder(MAvg, PMax)

plotshape(sellSignallk and showsignalsk ? PMax*1.005 : na, title="Sell", text="Sell", location=location.absolute, style=shape.labeldown, size=size.tiny, color=color.new(color.red, transp = 0), textcolor=color.white)

// buySignalc = ta.crossover(pmaxsrc, PMax)

// plotshape(buySignalc and showsignalsc ? PMax*0.995 : na, title="Buy", text="Buy", location=location.absolute, style=shape.labelup, size=size.tiny, color=#0F18BF, textcolor=color.white)

// sellSignallc = ta.crossunder(pmaxsrc, PMax)

// plotshape(sellSignallc and showsignalsc ? PMax*1.005 : na, title="Sell", text="Sell", location=location.absolute, style=shape.labeldown, size=size.tiny, color=#0F18BF, textcolor=color.white)

// mPlot = plot(ohlc4, title="", style=plot.style_circles, linewidth=0,display=display.none)

longFillColor = highlighting ? (MAvg>PMax ? color.new(color.green, transp = 90) : na) : na

shortFillColor = highlighting ? (MAvg math.exp(-(math.pow(x, 2)/(h * h * 2)))

//-----------------------------------------------------------------------------}

//Append lines

//-----------------------------------------------------------------------------{

n = bar_index

var ln = array.new_line(0)

if barstate.isfirst and repaint

for i = 0 to 499

array.push(ln,line.new(na,na,na,na))

//-----------------------------------------------------------------------------}

//End point method

//-----------------------------------------------------------------------------{

var coefs = array.new_float(0)

var den = 0.

if barstate.isfirst and not repaint

for i = 0 to 499

w = gauss(i, h)

coefs.push(w)

den := coefs.sum()

out = 0.

if not repaint

for i = 0 to 499

out += src * coefs.get(i)

out /= den

mae = ta.sma(math.abs(src - out), 499) * mult

upperN = out + mae

lowerN = out - mae

//-----------------------------------------------------------------------------}

//Compute and display NWE

//-----------------------------------------------------------------------------{

float y2 = na

float y1 = na

nwe = array.new(0)

if barstate.islast and repaint

sae = 0.

//Compute and set NWE point

for i = 0 to math.min(499,n - 1)

sum = 0.

sumw = 0.

//Compute weighted mean

for j = 0 to math.min(499,n - 1)

w = gauss(i - j, h)

sum += src * w

sumw += w

y2 := sum / sumw

sae += math.abs(src - y2)

nwe.push(y2)

sae := sae / math.min(499,n - 1) * mult

for i = 0 to math.min(499,n - 1)

if i%2 and showNadaray

line.new(n-i+1, y1 + sae, n-i, nwe.get(i) + sae, color = upCss)

line.new(n-i+1, y1 - sae, n-i, nwe.get(i) - sae, color = dnCss)

if src > nwe.get(i) + sae and src < nwe.get(i) + sae and showNadaray

label.new(n-i, src , '▼', color = color(na), style = label.style_label_down, textcolor = dnCss, textalign = text.align_center)

if src < nwe.get(i) - sae and src > nwe.get(i) - sae and showNadaray

label.new(n-i, src , '▲', color = color(na), style = label.style_label_up, textcolor = upCss, textalign = text.align_center)

y1 := nwe.get(i)

//-----------------------------------------------------------------------------}

//Dashboard

//-----------------------------------------------------------------------------{

var tb = table.new(position.top_right, 1, 1

, bgcolor = #1e222d

, border_color = #373a46

, border_width = 1

, frame_color = #373a46

, frame_width = 1)

if repaint

tb.cell(0, 0, 'Repainting Mode Enabled', text_color = color.white, text_size = size.small)

//-----------------------------------------------------------------------------}

//Plot

//-----------------------------------------------------------------------------}

// plot(repaint ? na : out + mae, 'Upper', upCss)

// plot(repaint ? na : out - mae, 'Lower', dnCss)

//Crossing Arrows

// plotshape(ta.crossunder(close, out - mae) ? low : na, "Crossunder", shape.labelup, location.absolute, color(na), 0 , text = '▲', textcolor = upCss, size = size.tiny)

// plotshape(ta.crossover(close, out + mae) ? high : na, "Crossover", shape.labeldown, location.absolute, color(na), 0 , text = '▼', textcolor = dnCss, size = size.tiny)

//-----------------------------------------------------------------------------}

//////////////////////////////////////////////////////////////////////////////////

enableD = input (true, "DIVERGANCE ON/OFF" , group="INDICATORS ON/OFF")

//DIVERGANCE

prd1 = input.int (defval=5 , title='PIVOT PERIOD' , minval=1, maxval=50 , group="DIVERGANCE")

source = input.string(defval='HIGH/LOW' , title='SOURCE FOR PIVOT POINTS' , options= , group="DIVERGANCE")

searchdiv = input.string(defval='REGULAR/HIDDEN', title='DIVERGANCE TYPE' , options= , group="DIVERGANCE")

showindis = input.string(defval='FULL' , title='SHOW INDICATORS NAME' , options= , group="DIVERGANCE")

showlimit = input.int(1 , title='MINIMUM NUMBER OF DIVERGANCES', minval=1, maxval=11 , group="DIVERGANCE")

maxpp = input.int (defval=20 , title='MAXIMUM PIVOT POINTS TO CHECK', minval=1, maxval=20 , group="DIVERGANCE")

maxbars = input.int (defval=200 , title='MAXIMUM BARS TO CHECK' , minval=30, maxval=200 , group="DIVERGANCE")

showlast = input (defval=false , title='SHOW ONLY LAST DIVERGANCE' , group="DIVERGANCE")

dontconfirm = input (defval=false , title="DON'T WAIT FOR CONFORMATION" , group="DIVERGANCE")

showlines = input (defval=false , title='SHOW DIVERGANCE LINES' , group="DIVERGANCE")

showpivot = input (defval=false , title='SHOW PIVOT POINTS' , group="DIVERGANCE")

calcmacd = input (defval=true , title='MACD' , group="DIVERGANCE")

calcmacda = input (defval=true , title='MACD HISTOGRAM' , group="DIVERGANCE")

calcrsi = input (defval=true , title='RSI' , group="DIVERGANCE")

calcstoc = input (defval=true , title='STOCHASTIC' , group="DIVERGANCE")

calccci = input (defval=true , title='CCI' , group="DIVERGANCE")

calcmom = input (defval=true , title='MOMENTUM' , group="DIVERGANCE")

calcobv = input (defval=true , title='OBV' , group="DIVERGANCE")

calcvwmacd = input (true , title='VWMACD' , group="DIVERGANCE")

calccmf = input (true , title='CHAIKIN MONEY FLOW' , group="DIVERGANCE")

calcmfi = input (true , title='MONEY FLOW INDEX' , group="DIVERGANCE")

calcext = input (false , title='CHECK EXTERNAL INDICATOR' , group="DIVERGANCE")

externalindi = input (defval=close , title='EXTERNAL INDICATOR' , group="DIVERGANCE")

pos_reg_div_col = input (defval=#ffffff , title='POSITIVE REGULAR DIVERGANCE' , group="DIVERGANCE")

neg_reg_div_col = input (defval=#00def6 , title='NEGATIVE REGULAR DIVERGANCE' , group="DIVERGANCE")

pos_hid_div_col = input (defval=#00ff0a , title='POSITIVE HIDDEN DIVERGANCE' , group="DIVERGANCE")

neg_hid_div_col = input (defval=#ff0015 , title='NEGATIVE HIDDEN DIVERGANCE' , group="DIVERGANCE")

reg_div_l_style_ = input.string(defval='SOLID' , title='REGULAR DIVERGANCE LINESTYLE' , options= , group="DIVERGANCE")

hid_div_l_style_ = input.string(defval='SOLID' , title='HIDDEN DIVERGANCE LINESTYLE' , options= , group="DIVERGANCE")

reg_div_l_width = input.int (defval=2 , title='REGULAR DIVERGANCE LINEWIDTH' , minval=1, maxval=5 , group="DIVERGANCE")

hid_div_l_width = input.int (defval=2 , title='HIDDEN DIVERGANCE LINEWIDTH' , minval=1, maxval=5 , group="DIVERGANCE")

showmas = input.bool (defval=false , title='SHOW MOVING AVERAGES (50 & 200)', inline='MA' , group="DIVERGANCE")

cma1col = input.color (defval=#ffffff , title='' , inline='MA' , group="DIVERGANCE")

cma2col = input.color (defval=#00def6 , title='' , inline='MA' , group="DIVERGANCE")

//PLOTS

plot(showmas ? ta.sma(close, 50) : na, color=showmas ? cma1col : na)

plot(showmas ? ta.sma(close, 200) : na, color=showmas ? cma2col : na)

var reg_div_l_style = reg_div_l_style_ == 'SOLID' ? line.style_solid : reg_div_l_style_ == 'DASHED' ? line.style_dashed : line.style_dotted

var hid_div_l_style = hid_div_l_style_ == 'SOLID' ? line.style_solid : hid_div_l_style_ == 'DASHED' ? line.style_dashed : line.style_dotted

rsi = ta.rsi(close, 14)

= ta.macd(close, 12, 26, 9)

moment = ta.mom(close, 10)

cci = ta.cci(close, 10)

Obv = ta.obv

stk = ta.sma(ta.stoch(close, high, low, 14), 3)

maFast = ta.vwma(close, 12)

maSlow = ta.vwma(close, 26)

vwmacd = maFast - maSlow

Cmfm = (close - low - (high - close)) / (high - low)

Cmfv = Cmfm * volume

cmf = ta.sma(Cmfv, 21) / ta.sma(volume, 21)

Mfi = ta.mfi(close, 14)

var indicators_name = array.new_string(11)

var div_colors = array.new_color(4)

if barstate.isfirst and enableD

array.set(indicators_name, 0, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 1, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 2, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 3, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 4, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 5, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 6, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 7, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 8, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 9, showindis == "DON'T SHOW" ? '' : '')

array.set(indicators_name, 10, showindis == "DON'T SHOW" ? '' : '')

array.set(div_colors, 0, pos_reg_div_col)

array.set(div_colors, 1, neg_reg_div_col)

array.set(div_colors, 2, pos_hid_div_col)

array.set(div_colors, 3, neg_hid_div_col)

float ph1 = ta.pivothigh(source == 'CLOSE' ? close : high, prd1, prd1)

float pl1 = ta.pivotlow(source == 'CLOSE' ? close : low, prd1, prd1)

plotshape(ph1 and showpivot, text='H', style=shape.labeldown, color=color.new(color.white, 100), textcolor=#00def6, location=location.abovebar, offset=-prd1)

plotshape(pl1 and showpivot, text='L', style=shape.labelup, color=color.new(color.white, 100), textcolor=#ffffff, location=location.belowbar, offset=-prd1)

var int maxarraysize = 20

var ph_positions = array.new_int(maxarraysize, 0)

var pl_positions = array.new_int(maxarraysize, 0)

var ph_vals = array.new_float(maxarraysize, 0.)

var pl_vals = array.new_float(maxarraysize, 0.)

if ph1

array.unshift(ph_positions, bar_index)

array.unshift(ph_vals, ph1)

if array.size(ph_positions) > maxarraysize

array.pop(ph_positions)

array.pop(ph_vals)

if pl1

array.unshift(pl_positions, bar_index)

array.unshift(pl_vals, pl1)

if array.size(pl_positions) > maxarraysize

array.pop(pl_positions)

array.pop(pl_vals)

positive_regular_positive_hidden_divergence(src, cond) =>

divlen = 0

prsc = source == 'CLOSE' ? close : low

if dontconfirm or src > src or close > close

startpoint = dontconfirm ? 0 : 1

for x = 0 to maxpp - 1 by 1

len = bar_index - array.get(pl_positions, x) + prd1

if array.get(pl_positions, x) == 0 or len > maxbars

break

if len > 5 and (cond == 1 and src > src and prsc < nz(array.get(pl_vals, x)) or cond == 2 and src < src and prsc > nz(array.get(pl_vals, x)))

slope1 = (src - src ) / (len - startpoint)

virtual_line1 = src - slope1

slope2 = (close - close ) / (len - startpoint)

virtual_line2 = close - slope2

arrived = true

for y = 1 + startpoint to len - 1 by 1

if src < virtual_line1 or nz(close ) < virtual_line2

arrived := false

break

virtual_line1 -= slope1

virtual_line2 -= slope2

virtual_line2

if arrived

divlen := len

break

divlen

negative_regular_negative_hidden_divergence(src, cond) =>

divlen = 0

prsc = source == 'CLOSE' ? close : high

if dontconfirm or src < src or close < close

startpoint = dontconfirm ? 0 : 1

for x = 0 to maxpp - 1 by 1

len = bar_index - array.get(ph_positions, x) + prd1

if array.get(ph_positions, x) == 0 or len > maxbars

break

if len > 5 and (cond == 1 and src < src and prsc > nz(array.get(ph_vals, x)) or cond == 2 and src > src and prsc < nz(array.get(ph_vals, x)))

slope1 = (src - src ) / (len - startpoint)

virtual_line1 = src - slope1

slope2 = (close - nz(close )) / (len - startpoint)

virtual_line2 = close - slope2

arrived = true

for y = 1 + startpoint to len - 1 by 1

if src > virtual_line1 or nz(close ) > virtual_line2

arrived := false

break

virtual_line1 -= slope1

virtual_line2 -= slope2

virtual_line2

if arrived

divlen := len

break

divlen

//CALCULATIONS

calculate_divs(cond, indicator_1) =>

divs = array.new_int(4, 0)

array.set(divs, 0, cond and (searchdiv == 'REGULAR' or searchdiv == 'REGULAR/HIDDEN') ? positive_regular_positive_hidden_divergence(indicator_1, 1) : 0)

array.set(divs, 1, cond and (searchdiv == 'REGULAR' or searchdiv == 'REGULAR/HIDDEN') ? negative_regular_negative_hidden_divergence(indicator_1, 1) : 0)

array.set(divs, 2, cond and (searchdiv == 'HIDDEN' or searchdiv == 'REGULAR/HIDDEN') ? positive_regular_positive_hidden_divergence(indicator_1, 2) : 0)

array.set(divs, 3, cond and (searchdiv == 'HIDDEN' or searchdiv == 'REGULAR/HIDDEN') ? negative_regular_negative_hidden_divergence(indicator_1, 2) : 0)

divs

var all_divergences = array.new_int(44)

array_set_divs(div_pointer, index) =>

for x = 0 to 3 by 1

array.set(all_divergences, index * 4 + x, array.get(div_pointer, x))

array_set_divs(calculate_divs(calcmacd , macd) , 0)

array_set_divs(calculate_divs(calcmacda , deltamacd) , 1)

array_set_divs(calculate_divs(calcrsi , rsi) , 2)

array_set_divs(calculate_divs(calcstoc , stk) , 3)

array_set_divs(calculate_divs(calccci , cci) , 4)

array_set_divs(calculate_divs(calcmom , moment) , 5)

array_set_divs(calculate_divs(calcobv , Obv) , 6)

array_set_divs(calculate_divs(calcvwmacd, vwmacd) , 7)

array_set_divs(calculate_divs(calccmf , cmf) , 8)

array_set_divs(calculate_divs(calcmfi , Mfi) , 9)

array_set_divs(calculate_divs(calcext , externalindi), 10)

total_div = 0

for x = 0 to array.size(all_divergences) - 1 by 1

total_div += math.round(math.sign(array.get(all_divergences, x)))

total_div

if total_div < showlimit

array.fill(all_divergences, 0)

var pos_div_lines = array.new_line(0)

var neg_div_lines = array.new_line(0)

var pos_div_labels = array.new_label(0)

var neg_div_labels = array.new_label(0)

delete_old_pos_div_lines() =>

if array.size(pos_div_lines) > 0

for j = 0 to array.size(pos_div_lines) - 1 by 1

line.delete(array.get(pos_div_lines, j))

array.clear(pos_div_lines)

delete_old_neg_div_lines() =>

if array.size(neg_div_lines) > 0

for j = 0 to array.size(neg_div_lines) - 1 by 1

line.delete(array.get(neg_div_lines, j))

array.clear(neg_div_lines)

delete_old_pos_div_labels() =>

if array.size(pos_div_labels) > 0

for j = 0 to array.size(pos_div_labels) - 1 by 1

label.delete(array.get(pos_div_labels, j))

array.clear(pos_div_labels)

delete_old_neg_div_labels() =>

if array.size(neg_div_labels) > 0

for j = 0 to array.size(neg_div_labels) - 1 by 1

label.delete(array.get(neg_div_labels, j))

array.clear(neg_div_labels)

delete_last_pos_div_lines_label(n) =>

if n > 0 and array.size(pos_div_lines) >= n

asz = array.size(pos_div_lines)

for j = 1 to n by 1

line.delete(array.get(pos_div_lines, asz - j))

array.pop(pos_div_lines)

if array.size(pos_div_labels) > 0

label.delete(array.get(pos_div_labels, array.size(pos_div_labels) - 1))

array.pop(pos_div_labels)

delete_last_neg_div_lines_label(n) =>

if n > 0 and array.size(neg_div_lines) >= n

asz = array.size(neg_div_lines)

for j = 1 to n by 1

line.delete(array.get(neg_div_lines, asz - j))

array.pop(neg_div_lines)

if array.size(neg_div_labels) > 0

label.delete(array.get(neg_div_labels, array.size(neg_div_labels) - 1))

array.pop(neg_div_labels)

pos_reg_div_detected = false

neg_reg_div_detected = false

pos_hid_div_detected = false

neg_hid_div_detected = false

var last_pos_div_lines = 0

var last_neg_div_lines = 0

var remove_last_pos_divs = false

var remove_last_neg_divs = false

if pl1

remove_last_pos_divs := false

last_pos_div_lines := 0

last_pos_div_lines

if ph1

remove_last_neg_divs := false

last_neg_div_lines := 0

last_neg_div_lines

divergence_text_top = ''

divergence_text_bottom = ''

distances = array.new_int(0)

dnumdiv_top = 0

dnumdiv_bottom = 0

top_label_col = color.white

bottom_label_col = color.white

old_pos_divs_can_be_removed = true

old_neg_divs_can_be_removed = true

startpoint = dontconfirm ? 0 : 1

for x = 0 to 10 by 1

div_type = -1

for y = 0 to 3 by 1

if array.get(all_divergences, x * 4 + y) > 0

div_type := y

if y % 2 == 1

dnumdiv_top += 1

top_label_col := array.get(div_colors, y)

top_label_col

if y % 2 == 0

dnumdiv_bottom += 1

bottom_label_col := array.get(div_colors, y)

bottom_label_col

if not array.includes(distances, array.get(all_divergences, x * 4 + y))

array.push(distances, array.get(all_divergences, x * 4 + y))

new_line = showlines ? line.new(x1=bar_index - array.get(all_divergences, x * 4 + y), y1=source == 'CLOSE' ? close : y % 2 == 0 ? low : high , x2=bar_index - startpoint, y2=source == 'CLOSE' ? close : y % 2 == 0 ? low : high , color=array.get(div_colors, y), style=y < 2 ? reg_div_l_style : hid_div_l_style, width=y < 2 ? reg_div_l_width : hid_div_l_width) : na

if y % 2 == 0

if old_pos_divs_can_be_removed

old_pos_divs_can_be_removed := false

if not showlast and remove_last_pos_divs

delete_last_pos_div_lines_label(last_pos_div_lines)

last_pos_div_lines := 0

last_pos_div_lines

if showlast

delete_old_pos_div_lines()

array.push(pos_div_lines, new_line)

last_pos_div_lines += 1

remove_last_pos_divs := true

remove_last_pos_divs

if y % 2 == 1

if old_neg_divs_can_be_removed

old_neg_divs_can_be_removed := false

if not showlast and remove_last_neg_divs

delete_last_neg_div_lines_label(last_neg_div_lines)

last_neg_div_lines := 0

last_neg_div_lines

if showlast

delete_old_neg_div_lines()

array.push(neg_div_lines, new_line)

last_neg_div_lines += 1

remove_last_neg_divs := true

remove_last_neg_divs

if y == 0

pos_reg_div_detected := true

pos_reg_div_detected

if y == 1

neg_reg_div_detected := true

neg_reg_div_detected

if y == 2

pos_hid_div_detected := true

pos_hid_div_detected

if y == 3

neg_hid_div_detected := true

neg_hid_div_detected

if div_type >= 0

divergence_text_top += (div_type % 2 == 1 ? showindis != "DON'T SHOW" ? array.get(indicators_name, x) + '\n' : '' : '')

divergence_text_bottom += (div_type % 2 == 0 ? showindis != "DON'T SHOW" ? array.get(indicators_name, x) + '\n' : '' : '')

divergence_text_bottom

if showindis != "DON'T SHOW"

if dnumdiv_top > 0

divergence_text_top += str.tostring(dnumdiv_top)

divergence_text_top

if dnumdiv_bottom > 0

divergence_text_bottom += str.tostring(dnumdiv_bottom)

divergence_text_bottom

if divergence_text_top != ''

if showlast

delete_old_neg_div_labels()

array.push(neg_div_labels, label.new(x=bar_index, y=math.max(high, high ), color=top_label_col, style=label.style_diamond, size = size.auto))

if divergence_text_bottom != ''

if showlast

delete_old_pos_div_labels()

array.push(pos_div_labels, label.new(x=bar_index, y=math.min(low, low ), color=bottom_label_col, style=label.style_diamond, size = size.auto))

// POSITION AND SIZE

PosTable = input.string(defval="Bottom Right", title="Position", options= , group="Table Location & Size", inline="1")

SizTable = input.string(defval="Auto", title="Size", options= , group="Table Location & Size", inline="1")

Pos1Table = PosTable == "Top Right" ? position.top_right : PosTable == "Middle Right" ? position.middle_right : PosTable == "Bottom Right" ? position.bottom_right : PosTable == "Top Center" ? position.top_center : PosTable == "Middle Center" ? position.middle_center : PosTable == "Bottom Center" ? position.bottom_center : PosTable == "Top Left" ? position.top_left : PosTable == "Middle Left" ? position.middle_left : position.bottom_left

Siz1Table = SizTable == "Auto" ? size.auto : SizTable == "Huge" ? size.huge : SizTable == "Large" ? size.large : SizTable == "Normal" ? size.normal : SizTable == "Small" ? size.small : size.tiny

tbl = table.new(Pos1Table, 21, 16, border_width = 1, border_color = color.gray, frame_color = color.gray, frame_width = 1)

// Kullanıcı tarafından belirlenecek yeşil ve kırmızı zaman dilimi sayısı

greenThreshold = input.int(5, minval=1, maxval=10, title="Yeşil Zaman Dilimi Sayısı", group="Alarm Ayarları")

redThreshold = input.int(5, minval=1, maxval=10, title="Kırmızı Zaman Dilimi Sayısı", group="Alarm Ayarları")

// TIMEFRAMES OPTIONS

box01 = input.bool(true, "TF ", inline = "01", group="Select Timeframe")

tf01 = input.timeframe("1", "", inline = "01", group="Select Timeframe")

box02 = input.bool(false, "TF ", inline = "02", group="Select Timeframe")

tf02 = input.timeframe("3", "", inline = "02", group="Select Timeframe")

box03 = input.bool(true, "TF ", inline = "03", group="Select Timeframe")

tf03 = input.timeframe("5", "", inline = "03", group="Select Timeframe")

box04 = input.bool(true, "TF ", inline = "04", group="Select Timeframe")

tf04 = input.timeframe("15", "", inline = "04", group="Select Timeframe")

box05 = input.bool(false, "TF ", inline = "05", group="Select Timeframe")

tf05 = input.timeframe("30", "", inline = "05", group="Select Timeframe")

box06 = input.bool(true, "TF ", inline = "01", group="Select Timeframe")

tf06 = input.timeframe("60", "", inline = "01", group="Select Timeframe")

box07 = input.bool(false, "TF ", inline = "02", group="Select Timeframe")

tf07 = input.timeframe("120", "", inline = "02", group="Select Timeframe")

box08 = input.bool(false, "TF ", inline = "03", group="Select Timeframe")

tf08 = input.timeframe("180", "", inline = "03", group="Select Timeframe")

box09 = input.bool(true, "TF ", inline = "04", group="Select Timeframe")

tf09 = input.timeframe("240", "", inline = "04", group="Select Timeframe")

box10 = input.bool(false, "TF ", inline = "05", group="Select Timeframe")

tf10 = input.timeframe("D", "", inline = "05", group="Select Timeframe")

// indicator('Tillson FEMA', overlay=true)

length1 = input(1, 'FEMA Length')

a1 = input(0.7, 'Volume Factor')

e1 = ta.ema((high + low + 2 * close) / 4, length1)

e2 = ta.ema(e1, length1)

e3 = ta.ema(e2, length1)

e4 = ta.ema(e3, length1)

e5 = ta.ema(e4, length1)

e6 = ta.ema(e5, length1)

c1 = -a1 * a1 * a1

c2 = 3 * a1 * a1 + 3 * a1 * a1 * a1

c3 = -6 * a1 * a1 - 3 * a1 - 3 * a1 * a1 * a1

c4 = 1 + 3 * a1 + a1 * a1 * a1 + 3 * a1 * a1

FEMA = c1 * e6 + c2 * e5 + c3 * e4 + c4 * e3

tablocol1 = FEMA > FEMA

tablocol3 = FEMA < FEMA

color_1 = col1 ? color.rgb(149, 219, 35): col3 ? color.rgb(238, 11, 11) : color.yellow

plot(FEMA, color=color_1, linewidth=3, title='FEMA')

tilson1 = FEMA

tilson1a =FEMA

// DEFINITION OF VALUES

symbol = ticker.modify(syminfo.tickerid, syminfo.session)

tfArr = array.new(na)

tilson1Arr = array.new(na)

tilson1aArr = array.new(na)

// DEFINITIONS OF RSI & CCI FUNCTIONS APPENDED IN THE TIMEFRAME OPTIONS

cciNcciFun(tf, flg) =>

= request.security(symbol, tf, )

if flg and (barstate.isrealtime ? true : timeframe.in_seconds(timeframe.period) <= timeframe.in_seconds(tf))

array.push(tfArr, na(tf) ? timeframe.period : tf)

array.push(tilson1Arr, tilson_)

array.push(tilson1aArr, tilson1a_)

cciNcciFun(tf01, box01), cciNcciFun(tf02, box02), cciNcciFun(tf03, box03), cciNcciFun(tf04, box04),

cciNcciFun(tf05, box05), cciNcciFun(tf06, box06), cciNcciFun(tf07, box07), cciNcciFun(tf08, box08),

cciNcciFun(tf09, box09), cciNcciFun(tf10, box10)

// TABLE AND CELLS CONFIG

// Post Timeframe in format

tfTxt(x)=>

out = x

if not str.contains(x, "S") and not str.contains(x, "M") and

not str.contains(x, "W") and not str.contains(x, "D")

if str.tonumber(x)%60 == 0

out := str.tostring(str.tonumber(x)/60)+"H"

else

out := x + "m"

out

if barstate.islast

table.clear(tbl, 0, 0, 20, 15)

// TITLES

table.cell(tbl, 0, 0, "⏱", text_color=color.white, text_size=Siz1Table, bgcolor=#000000)

table.cell(tbl, 1, 0, "FEMA("+str.tostring(length1)+")", text_color=#FFFFFF, text_size=Siz1Table, bgcolor=#000000)

j = 1

greenCounter = 0 // Yeşil zaman dilimlerini saymak için bir sayaç

redCounter = 0

if array.size(tilson1Arr) > 0

for i = 0 to array.size(tilson1Arr) - 1

if not na(array.get(tilson1Arr, i))

//config values in the cells

TF_VALUE = array.get(tfArr,i)

tilson1VALUE = array.get(tilson1Arr, i)

tilson1aVALUE = array.get(tilson1aArr, i)

SIGNAL1 = tilson1VALUE >= tilson1aVALUE ? "▲" : tilson1VALUE <= tilson1aVALUE ? "▼" : na

// Yeşil oklar ve arka planı ayarla

greenArrowColor1 = SIGNAL1 == "▲" ? color.rgb(0, 255, 0) : color.rgb(255, 0, 0)

greenBgColor1 = SIGNAL1 == "▲" ? color.rgb(25, 70, 22) : color.rgb(93, 22, 22)

allGreen = tilson1VALUE >= tilson1aVALUE

allRed = tilson1VALUE <= tilson1aVALUE

// Determine background color for time text

timeBgColor = allGreen ? #194616 : (allRed ? #5D1616 : #000000)

txtColor = allGreen ? #00FF00 : (allRed ? #FF4500 : color.white)

if allGreen

greenCounter := greenCounter + 1

redCounter := 0

else if allRed

redCounter := redCounter + 1

greenCounter := 0

else

redCounter := 0

greenCounter := 0

// Dinamik pair değerini oluşturma

pair = "USDT_" + syminfo.basecurrency + "USDT"

// Bot ID için kullanıcı girişi

bot_id = input.int(12387976, title="Bot ID", minval=0,group ='3Comas Message', inline = '1') // Varsayılan değeri 12387976 olan bir tamsayı girişi alır

// E-posta tokenı için kullanıcı girişi

email_token = input("cd4111d4-549a-4759-a082-e8f45c91fa47", title="Email Token",group ='3Comas Message', inline = '1')

// USER INPUT FOR DELAY

delay_seconds = input.int(0, title="Delay Seconds", minval=0, maxval=86400,group ='3Comas Message', inline = '1')

// Dinamik mesajın oluşturulması

message = '{ "message_type": "bot", "bot_id": ' + str.tostring(bot_id) + ', "email_token": "' + email_token + '", "delay_seconds": ' + str.tostring(delay_seconds) + ', "pair": "' + pair + '"}'

// Kullanıcının belirlediği yeşil veya kırmızı zaman dilimi sayısına ulaşıldığında alarmı tetikle

if greenCounter >= greenThreshold

alert(message, alert.freq_once_per_bar_close)

// if redCounter >= redThreshold

// alert(message, alert.freq_once_per_bar_close)

// Kullanıcının belirlediği yeşil veya kırmızı zaman dilimi sayısına ulaşıldığında alarmı tetikle

// if greenCounter >= greenThreshold

// alert("Yeşil zaman dilimi sayısı " + str.tostring(greenThreshold) + " adede ulaştı", alert.freq_once_per_bar_close)

// if redCounter >= redThreshold

// alert("Kırmızı zaman dilimi sayısı " + str.tostring(redThreshold) + " adede ulaştı", alert.freq_once_per_bar_close)

table.cell(tbl, 0, j, tfTxt(TF_VALUE), text_color=txtColor, text_halign=text.align_left, text_size=Siz1Table, bgcolor=timeBgColor)

table.cell(tbl, 1, j, str.tostring(tilson1VALUE, "#.#######")+SIGNAL1, text_color=greenArrowColor1, text_halign=text.align_right, text_size=Siz1Table, bgcolor=greenBgColor1)

j += 1

prd = input.int(defval=10, title='Pivot Period', minval=4, maxval=30, group='Setup')

ppsrc = input.string(defval='High/Low', title='Source', options= , group='Setup')

maxnumpp = input.int(defval=20, title=' Maximum Number of Pivot', minval=5, maxval=100, group='Setup')

ChannelW = input.int(defval=10, title='Maximum Channel Width %', minval=1, group='Setup')

maxnumsr = input.int(defval=5, title=' Maximum Number of S/R', minval=1, maxval=10, group='Setup')

min_strength = input.int(defval=2, title=' Minimum Strength', minval=1, maxval=10, group='Setup')

labelloc = input.int(defval=20, title='Label Location', group='Colors', tooltip='Positive numbers reference future bars, negative numbers reference histical bars')

linestyle = input.string(defval='Dashed', title='Line Style', options= , group='Colors')

linewidth = input.int(defval=2, title='Line Width', minval=1, maxval=4, group='Colors')

resistancecolor = input.color(defval=color.red, title='Resistance Color', group='Colors')

supportcolor = input.color(defval=color.lime, title='Support Color', group='Colors')

showpp = input(false, title='Show Point Points')

float src1 = ppsrc == 'High/Low' ? high : math.max(close, open)

float src2 = ppsrc == 'High/Low' ? low : math.min(close, open)

float ph = ta.pivothigh(src1, prd, prd)

float pl = ta.pivotlow(src2, prd, prd)

plotshape(ph and showpp, text='H', style=shape.labeldown, color=na, textcolor=color.new(color.red, 0), location=location.abovebar, offset=-prd)

plotshape(pl and showpp, text='L', style=shape.labelup, color=na, textcolor=color.new(color.lime, 0), location=location.belowbar, offset=-prd)