mysourcetypesncsLibrary "mysourcetypes"

Libreria personale per sorgenti estese (Close, Open, High, Low, Median, Typical, Weighted, Average, Average Median Body, Trend Biased, Trend Biased Extreme, Volume Body, Momentum Biased, Volatility Adjusted, Body Dominance, Shadow Biased, Gap Aware, Rejection Biased, Range Position, Adaptive Trend, Pressure Balanced, Impulse Wave)

rclose()

Regular Close

Returns: Close price

ropen()

Regular Open

Returns: Open price

rhigh()

Regular High

Returns: High price

rlow()

Regular Low

Returns: Low price

rmedian()

Regular Median (HL2)

Returns: (High + Low) / 2

rtypical()

Regular Typical (HLC3)

Returns: (High + Low + Close) / 3

rweighted()

Regular Weighted (HLCC4)

Returns: (High + Low + Close + Close) / 4

raverage()

Regular Average (OHLC4)

Returns: (Open + High + Low + Close) / 4

ravemedbody()

Average Median Body

Returns: (Open + Close) / 2

rtrendb()

Trend Biased Regular

Returns: Trend-weighted price

rtrendbext()

Trend Biased Extreme

Returns: Extreme trend-weighted price

rvolbody()

Volume Weighted Body

Returns: Body midpoint weighted by volume intensity

rmomentum()

Momentum Biased

Returns: Price biased towards momentum direction

rvolatility()

Volatility Adjusted

Returns: Price adjusted by candle's volatility

rbodydominance()

Body Dominance

Returns: Emphasizes body over wicks

rshadowbias()

Shadow Biased

Returns: Price biased by shadow length

rgapaware()

Gap Aware

Returns: Considers gap between candles

rrejection()

Rejection Biased

Returns: Emphasizes price rejection levels

rrangeposition()

Range Position

Returns: Where close sits within the candle range (0-100%)

radaptivetrend()

Adaptive Trend

Returns: Adapts based on recent trend strength

rpressure()

Pressure Balanced

Returns: Balances buying/selling pressure within candle

rimpulse()

Impulse Wave

Returns: Detects impulsive moves vs corrections

Поиск скриптов по запросу "OHLC"

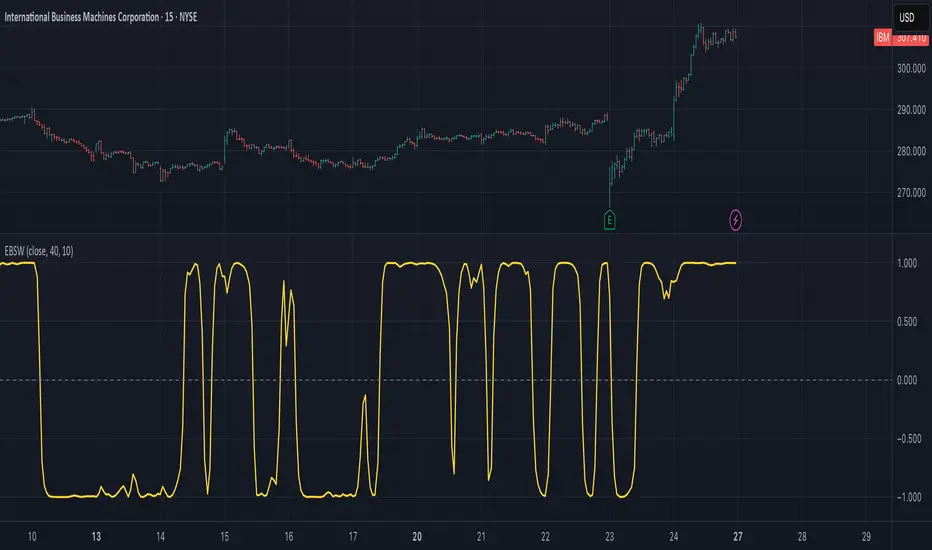

Ehlers Even Better Sinewave (EBSW)# EBSW: Ehlers Even Better Sinewave

## Overview and Purpose

The Ehlers Even Better Sinewave (EBSW) indicator, developed by John Ehlers, is an advanced cycle analysis tool. This implementation is based on a common interpretation that uses a cascade of filters: first, a High-Pass Filter (HPF) to detrend price data, followed by a Super Smoother Filter (SSF) to isolate the dominant cycle. The resulting filtered wave is then normalized using an Automatic Gain Control (AGC) mechanism, producing a bounded oscillator that fluctuates between approximately +1 and -1. It aims to provide a clear and responsive measure of market cycles.

## Core Concepts

* **Detrending (High-Pass Filter):** A 1-pole High-Pass Filter removes the longer-term trend component from the price data, allowing the indicator to focus on cyclical movements.

* **Cycle Smoothing (Super Smoother Filter):** Ehlers' Super Smoother Filter is applied to the detrended data to further refine the cycle component, offering effective smoothing with relatively low lag.

* **Wave Generation:** The output of the SSF is averaged over a short period (typically 3 bars) to create the primary "wave".

* **Automatic Gain Control (AGC):** The wave's amplitude is normalized by dividing it by the square root of its recent power (average of squared values). This keeps the oscillator bounded and responsive to changes in volatility.

* **Normalized Oscillator:** The final output is a single sinewave-like oscillator.

## Common Settings and Parameters

| Parameter | Default | Function | When to Adjust |

| ----------- | ------- | --------------------------------------------------------------------------------------------- | ----------------------------------------------------------------------------------------------------------------------------------------------- |

| Source | close | Price data used for calculation. | Typically `close`, but `hlc3` or `ohlc4` can be used for a more comprehensive price representation. |

| HP Length | 40 | Lookback period for the 1-pole High-Pass Filter used for detrending. | Shorter periods make the filter more responsive to shorter cycles; longer periods focus on longer-term cycles. Adjust based on observed cycle characteristics. |

| SSF Length | 10 | Lookback period for the Super Smoother Filter used for smoothing the detrended cycle component. | Shorter periods result in a more responsive (but potentially noisier) wave; longer periods provide more smoothing. |

**Pro Tip:** The `HP Length` and `SSF Length` parameters should be tuned based on the typical cycle lengths observed in the market and the desired responsiveness of the indicator.

## Calculation and Mathematical Foundation

**Simplified explanation:**

1. Remove the trend from the price data using a 1-pole High-Pass Filter.

2. Smooth the detrended data using a Super Smoother Filter to get a clean cycle component.

3. Average the output of the Super Smoother Filter over the last 3 bars to create a "Wave".

4. Calculate the average "Power" of the Super Smoother Filter output over the last 3 bars.

5. Normalize the "Wave" by dividing it by the square root of the "Power" to get the final EBSW value.

**Technical formula (conceptual):**

1. **High-Pass Filter (HPF - 1-pole):**

`angle_hp = 2 * PI / hpLength`

`alpha1_hp = (1 - sin(angle_hp)) / cos(angle_hp)`

`HP = (0.5 * (1 + alpha1_hp) * (src - src )) + alpha1_hp * HP `

2. **Super Smoother Filter (SSF):**

`angle_ssf = sqrt(2) * PI / ssfLength`

`alpha2_ssf = exp(-angle_ssf)`

`beta_ssf = 2 * alpha2_ssf * cos(angle_ssf)`

`c2 = beta_ssf`

`c3 = -alpha2_ssf^2`

`c1 = 1 - c2 - c3`

`Filt = c1 * (HP + HP )/2 + c2*Filt + c3*Filt `

3. **Wave Generation:**

`WaveVal = (Filt + Filt + Filt ) / 3`

4. **Power & Automatic Gain Control (AGC):**

`Pwr = (Filt^2 + Filt ^2 + Filt ^2) / 3`

`EBSW_SineWave = WaveVal / sqrt(Pwr)` (with check for Pwr == 0)

> 🔍 **Technical Note:** The combination of HPF and SSF creates a form of band-pass filter. The AGC mechanism ensures the output remains scaled, typically between -1 and +1, making it behave like a normalized oscillator.

## Interpretation Details

* **Cycle Identification:** The EBSW wave shows the current phase and strength of the dominant market cycle as filtered by the indicator. Peaks suggest cycle tops, and troughs suggest cycle bottoms.

* **Trend Reversals/Momentum Shifts:** When the EBSW wave crosses the zero line, it can indicate a potential shift in the short-term cyclical momentum.

* Crossing up through zero: Potential start of a bullish cyclical phase.

* Crossing down through zero: Potential start of a bearish cyclical phase.

* **Overbought/Oversold Levels:** While normalized, traders often establish subjective or statistically derived overbought/oversold levels (e.g., +0.85 and -0.85, or other values like +0.7, +0.9).

* Reaching above the overbought level and turning down may signal a potential cyclical peak.

* Falling below the oversold level and turning up may signal a potential cyclical trough.

## Limitations and Considerations

* **Parameter Sensitivity:** The indicator's performance depends on tuning `hpLength` and `ssfLength` to prevailing market conditions.

* **Non-Stationary Markets:** In strongly trending markets with weak cyclical components, or in very choppy non-cyclical conditions, the EBSW may produce less reliable signals.

* **Lag:** All filtering introduces some lag. The Super Smoother Filter is designed to minimize this for its degree of smoothing, but lag is still present.

* **Whipsaws:** Rapid oscillations around the zero line can occur in volatile or directionless markets.

* **Requires Confirmation:** Signals from EBSW are often best confirmed with other forms of technical analysis (e.g., price action, volume, other non-correlated indicators).

## References

* Ehlers, J. F. (2002). *Rocket Science for Traders: Digital Signal Processing Applications*. John Wiley & Sons.

* Ehlers, J. F. (2013). *Cycle Analytics for Traders: Advanced Technical Trading Concepts*. John Wiley & Sons.

Mayer Mutiple | QRMayer Multiple | QR — Publication Description

What it does

Mayer Multiple | QR is a cycle/valuation style oscillator that measures how far price sits above or below its longer-term average and normalizes that distance by current volatility. It helps you spot overheated extensions and deep discounts relative to trend, with adaptive bands that expand/contract as conditions change.

How it works (principle)

The script compares price to a long lookback moving average (default uses a 200-period average of ohlc4) and turns that gap into an oscillator.

It then computes a rolling standard deviation of that oscillator to build dynamic upper/lower bands (±1σ, ±2σ, ±3σ).

When the oscillator rises above the upper bands, the move is statistically stretched (potential distribution/risk). When it falls below the lower bands, it’s statistically depressed (potential accumulation/opportunity).

A small baseline band around zero (scaled from volatility) provides a quick trend-bias read without crowding the view.

Why this matters: Classic “Mayer Multiple” tools use a fixed threshold over a single moving average. This version is volatility-aware: its bands adapt to the market’s current dispersion, reducing false signals in quiet regimes and avoiding constant “overheat” flags in high-vol regimes.

What you see on the chart

White oscillator line: volatility-normalized deviation from the long-term average.

Adaptive bands:

Upper 1/2/3σ (shaded blue tones) = progressively more extended.

Lower 1/2/3σ (shaded green tones) = progressively more discounted.

Baseline ribbon: subtle band around zero for quick bias.

Background highlights: optional flashes when the oscillator exceeds the ±3σ extremes.

All visuals are generated by this script alone; no other indicator is required to understand usage.

How to use it

Context: Use on higher timeframes to gauge where price sits versus its long-term “fair value corridor.”

Signal reading:

Above +1σ/+2σ/+3σ: extension → consider de-risking, trailing stops, or waiting for mean reversion.

Below −1σ/−2σ/−3σ: discount → consider scaling in, watching for trend resumption cues.

Confluence: Treat it as a condition, not a trigger. Pair with structure (higher highs/lows), breadth, or momentum for entries/exits.

Regime awareness: As volatility rises, bands widen; prioritize trend context over single print extremes.

Inputs you can tune

Color mode: preset palettes for lines/fills/backgrounds.

Dynamic Threshold Length: lookback for the volatility (σ) calculation driving the adaptive bands.

Source: price input used for the long-term reference.

Band toggles: show/hide ±1σ / ±2σ / ±3σ envelopes to reduce clutter.

Originality & value

Adaptive, volatility-aware implementation of a Mayer-style concept: rather than one fixed threshold, it scales to current regime, keeping readings comparable across cycles.

Clear, clean presentation (oscillator + bands + optional background) designed for publication with a clean chart so the script’s output is immediately identifiable.

Offers actionable context (stretch/discount zones) while leaving trade execution to the user’s process.

Limitations & good practices

Best used for context and risk framing, not stand-alone entries.

Adaptive bands depend on the lookback you choose; very short windows can overfit, very long windows can lag.

Extremes can persist in strong trends—don’t fade momentum blindly.

Disclaimer

This tool is for research and education only and not investment advice. Markets involve risk. Past performance does not predict or guarantee future results. Use prudent risk management and test settings on your instruments/timeframes.

DynLenLibLibrary "DynLenLib"

sum_dyn(src, len)

Parameters:

src (float)

len (int)

lag_dyn(src, len)

Parameters:

src (float)

len (int)

highest_dyn(src, len)

Parameters:

src (float)

len (int)

lowest_dyn(src, len)

Parameters:

src (float)

len (int)

var_dyn(src, len)

Parameters:

src (float)

len (int)

stdev_dyn(src, len)

Parameters:

src (float)

len (int)

hl2()

hlc3()

ohlc4()

sma_dyn(src, len)

Parameters:

src (float)

len (int)

ema_dyn(src, len)

Parameters:

src (float)

len (int)

rma_dyn(src, len)

Parameters:

src (float)

len (int)

smma_dyn(src, len)

Parameters:

src (float)

len (int)

wma_dyn(src, len)

Parameters:

src (float)

len (int)

vwma_dyn(price, vol, len)

Parameters:

price (float)

vol (float)

len (int)

hma_dyn(src, len)

Parameters:

src (float)

len (int)

dema_dyn(src, len)

Parameters:

src (float)

len (int)

tema_dyn(src, len)

Parameters:

src (float)

len (int)

kama_dyn(src, erLen, fastLen, slowLen)

Parameters:

src (float)

erLen (int)

fastLen (int)

slowLen (int)

mcginley_dyn(src, len)

Parameters:

src (float)

len (int)

median_price()

true_range()

atr_dyn(len)

Parameters:

len (int)

bbands_dyn(src, len, mult)

Parameters:

src (float)

len (int)

mult (float)

bb_percent_b(src, len, mult)

Parameters:

src (float)

len (int)

mult (float)

bb_bandwidth(src, len, mult)

Parameters:

src (float)

len (int)

mult (float)

keltner_dyn(src, lenEMA, lenATR, multATR)

Parameters:

src (float)

lenEMA (int)

lenATR (int)

multATR (float)

donchian_dyn(len)

Parameters:

len (int)

choppiness_index(len)

Parameters:

len (int)

vol_stop(lenATR, mult)

Parameters:

lenATR (int)

mult (float)

roc_dyn(src, len)

Parameters:

src (float)

len (int)

rsi_dyn(src, len)

Parameters:

src (float)

len (int)

stoch_dyn(kLen, dLen, smoothK)

Parameters:

kLen (int)

dLen (int)

smoothK (int)

stoch_rsi_dyn(rsiLen, stochLen, kSmooth, dLen)

Parameters:

rsiLen (int)

stochLen (int)

kSmooth (int)

dLen (int)

cci_dyn(src, len)

Parameters:

src (float)

len (int)

cmo_dyn(src, len)

Parameters:

src (float)

len (int)

trix_dyn(len)

Parameters:

len (int)

tsi_dyn(shortLen, longLen)

Parameters:

shortLen (int)

longLen (int)

ultimate_osc(len1, len2, len3)

Parameters:

len1 (int)

len2 (int)

len3 (int)

dpo_dyn(src, len)

Parameters:

src (float)

len (int)

willr_dyn(len)

Parameters:

len (int)

macd_dyn(src, fastLen, slowLen, sigLen)

Parameters:

src (float)

fastLen (int)

slowLen (int)

sigLen (int)

ppo_dyn(src, fastLen, slowLen, sigLen)

Parameters:

src (float)

fastLen (int)

slowLen (int)

sigLen (int)

aroon_dyn(len)

Parameters:

len (int)

dmi_adx_dyn(diLen, adxLen)

Parameters:

diLen (int)

adxLen (int)

vortex_dyn(len)

Parameters:

len (int)

coppock_dyn(rocLen1, rocLen2, wmaLen)

Parameters:

rocLen1 (int)

rocLen2 (int)

wmaLen (int)

rvi_dyn(len)

Parameters:

len (int)

price_osc_dyn(src, fastLen, slowLen)

Parameters:

src (float)

fastLen (int)

slowLen (int)

rci_dyn(src, len)

Parameters:

src (float)

len (int)

obv()

pvt()

cmf_dyn(len)

Parameters:

len (int)

adl()

chaikin_osc_dyn(fastLen, slowLen)

Parameters:

fastLen (int)

slowLen (int)

mfi_dyn(len)

Parameters:

len (int)

volume_osc_dyn(fastLen, slowLen)

Parameters:

fastLen (int)

slowLen (int)

up_down_volume()

cvd()

supertrend_dyn(atrLen, mult)

Parameters:

atrLen (int)

mult (float)

envelopes_dyn(src, len, pct)

Parameters:

src (float)

len (int)

pct (float)

linreg_line_slope(src, len)

Parameters:

src (float)

len (int)

lsma_dyn(src, len)

Parameters:

src (float)

len (int)

corrcoef_dyn(a, b, len)

Parameters:

a (float)

b (float)

len (int)

psar(step, maxStep)

Parameters:

step (float)

maxStep (float)

pivots_standard()

williams_alligator(src, jawLen, teethLen, lipsLen)

Parameters:

src (float)

jawLen (int)

teethLen (int)

lipsLen (int)

twap_dyn(src, len)

Parameters:

src (float)

len (int)

vwap_anchored(price, volume, reset)

Parameters:

price (float)

volume (float)

reset (bool)

performance_pct(len)

Parameters:

len (int)

Keltner Channel Enhanced [DCAUT]█ Keltner Channel Enhanced

📊 ORIGINALITY & INNOVATION

The Keltner Channel Enhanced represents an important advancement over standard Keltner Channel implementations by introducing dual flexibility in moving average selection for both the middle band and ATR calculation. While traditional Keltner Channels typically use EMA for the middle band and RMA (Wilder's smoothing) for ATR, this enhanced version provides access to 25+ moving average algorithms for both components, enabling traders to fine-tune the indicator's behavior to match specific market characteristics and trading approaches.

Key Advancements:

Dual MA Algorithm Flexibility: Independent selection of moving average types for middle band (25+ options) and ATR smoothing (25+ options), allowing optimization of both trend identification and volatility measurement separately

Enhanced Trend Sensitivity: Ability to use faster algorithms (HMA, T3) for middle band while maintaining stable volatility measurement with traditional ATR smoothing, or vice versa for different trading strategies

Adaptive Volatility Measurement: Choice of ATR smoothing algorithm affects channel responsiveness to volatility changes, from highly reactive (SMA, EMA) to smoothly adaptive (RMA, TEMA)

Comprehensive Alert System: Five distinct alert conditions covering breakouts, trend changes, and volatility expansion, enabling automated monitoring without constant chart observation

Multi-Timeframe Compatibility: Works effectively across all timeframes from intraday scalping to long-term position trading, with independent optimization of trend and volatility components

This implementation addresses key limitations of standard Keltner Channels: fixed EMA/RMA combination may not suit all market conditions or trading styles. By decoupling the trend component from volatility measurement and allowing independent algorithm selection, traders can create highly customized configurations for specific instruments and market phases.

📐 MATHEMATICAL FOUNDATION

Keltner Channel Enhanced uses a three-component calculation system that combines a flexible moving average middle band with ATR-based (Average True Range) upper and lower channels, creating volatility-adjusted trend-following bands.

Core Calculation Process:

1. Middle Band (Basis) Calculation:

The basis line is calculated using the selected moving average algorithm applied to the price source over the specified period:

basis = ma(source, length, maType)

Supported algorithms include EMA (standard choice, trend-biased), SMA (balanced and symmetric), HMA (reduced lag), WMA, VWMA, TEMA, T3, KAMA, and 17+ others.

2. Average True Range (ATR) Calculation:

ATR measures market volatility by calculating the average of true ranges over the specified period:

trueRange = max(high - low, abs(high - close ), abs(low - close ))

atrValue = ma(trueRange, atrLength, atrMaType)

ATR smoothing algorithm significantly affects channel behavior, with options including RMA (standard, very smooth), SMA (moderate smoothness), EMA (fast adaptation), TEMA (smooth yet responsive), and others.

3. Channel Calculation:

Upper and lower channels are positioned at specified multiples of ATR from the basis:

upperChannel = basis + (multiplier × atrValue)

lowerChannel = basis - (multiplier × atrValue)

Standard multiplier is 2.0, providing channels that dynamically adjust width based on market volatility.

Keltner Channel vs. Bollinger Bands - Key Differences:

While both indicators create volatility-based channels, they use fundamentally different volatility measures:

Keltner Channel (ATR-based):

Uses Average True Range to measure actual price movement volatility

Incorporates gaps and limit moves through true range calculation

More stable in trending markets, less prone to extreme compression

Better reflects intraday volatility and trading range

Typically fewer band touches, making touches more significant

More suitable for trend-following strategies

Bollinger Bands (Standard Deviation-based):

Uses statistical standard deviation to measure price dispersion

Based on closing prices only, doesn't account for intraday range

Can compress significantly during consolidation (squeeze patterns)

More touches in ranging markets

Better suited for mean-reversion strategies

Provides statistical probability framework (95% within 2 standard deviations)

Algorithm Combination Effects:

The interaction between middle band MA type and ATR MA type creates different indicator characteristics:

Trend-Focused Configuration (Fast MA + Slow ATR): Middle band uses HMA/EMA/T3, ATR uses RMA/TEMA, quick trend changes with stable channel width, suitable for trend-following

Volatility-Focused Configuration (Slow MA + Fast ATR): Middle band uses SMA/WMA, ATR uses EMA/SMA, stable trend with dynamic channel width, suitable for volatility trading

Balanced Configuration (Standard EMA/RMA): Classic Keltner Channel behavior, time-tested combination, suitable for general-purpose trend following

Adaptive Configuration (KAMA + KAMA): Self-adjusting indicator responding to efficiency ratio, suitable for markets with varying trend strength and volatility regimes

📊 COMPREHENSIVE SIGNAL ANALYSIS

Keltner Channel Enhanced provides multiple signal categories optimized for trend-following and breakout strategies.

Channel Position Signals:

Upper Channel Interaction:

Price Touching Upper Channel: Strong bullish momentum, price moving more than typical volatility range suggests, potential continuation signal in established uptrends

Price Breaking Above Upper Channel: Exceptional strength, price exceeding normal volatility expectations, consider adding to long positions or tightening trailing stops

Price Riding Upper Channel: Sustained strong uptrend, characteristic of powerful bull moves, stay with trend and avoid premature profit-taking

Price Rejection at Upper Channel: Momentum exhaustion signal, consider profit-taking on longs or waiting for pullback to middle band for reentry

Lower Channel Interaction:

Price Touching Lower Channel: Strong bearish momentum, price moving more than typical volatility range suggests, potential continuation signal in established downtrends

Price Breaking Below Lower Channel: Exceptional weakness, price exceeding normal volatility expectations, consider adding to short positions or protecting against further downside

Price Riding Lower Channel: Sustained strong downtrend, characteristic of powerful bear moves, stay with trend and avoid premature covering

Price Rejection at Lower Channel: Momentum exhaustion signal, consider covering shorts or waiting for bounce to middle band for reentry

Middle Band (Basis) Signals:

Trend Direction Confirmation:

Price Above Basis: Bullish trend bias, middle band acts as dynamic support in uptrends, consider long positions or holding existing longs

Price Below Basis: Bearish trend bias, middle band acts as dynamic resistance in downtrends, consider short positions or avoiding longs

Price Crossing Above Basis: Potential trend change from bearish to bullish, early signal to establish long positions

Price Crossing Below Basis: Potential trend change from bullish to bearish, early signal to establish short positions or exit longs

Pullback Trading Strategy:

Uptrend Pullback: Price pulls back from upper channel to middle band, finds support, and resumes upward, ideal long entry point

Downtrend Bounce: Price bounces from lower channel to middle band, meets resistance, and resumes downward, ideal short entry point

Basis Test: Strong trends often show price respecting the middle band as support/resistance on pullbacks

Failed Test: Price breaking through middle band against trend direction signals potential reversal

Volatility-Based Signals:

Narrow Channels (Low Volatility):

Consolidation Phase: Channels contract during periods of reduced volatility and directionless price action

Breakout Preparation: Narrow channels often precede significant directional moves as volatility cycles

Trading Approach: Reduce position sizes, wait for breakout confirmation, avoid range-bound strategies within channels

Breakout Direction: Monitor for price breaking decisively outside channel range with expanding width

Wide Channels (High Volatility):

Trending Phase: Channels expand during strong directional moves and increased volatility

Momentum Confirmation: Wide channels confirm genuine trend with substantial volatility backing

Trading Approach: Trend-following strategies excel, wider stops necessary, mean-reversion strategies risky

Exhaustion Signs: Extreme channel width (historical highs) may signal approaching consolidation or reversal

Advanced Pattern Recognition:

Channel Walking Pattern:

Upper Channel Walk: Price consistently touches or exceeds upper channel while staying above basis, very strong uptrend signal, hold longs aggressively

Lower Channel Walk: Price consistently touches or exceeds lower channel while staying below basis, very strong downtrend signal, hold shorts aggressively

Basis Support/Resistance: During channel walks, price typically uses middle band as support/resistance on minor pullbacks

Pattern Break: Price crossing basis during channel walk signals potential trend exhaustion

Squeeze and Release Pattern:

Squeeze Phase: Channels narrow significantly, price consolidates near middle band, volatility contracts

Direction Clues: Watch for price positioning relative to basis during squeeze (above = bullish bias, below = bearish bias)

Release Trigger: Price breaking outside narrow channel range with expanding width confirms breakout

Follow-Through: Measure squeeze height and project from breakout point for initial profit targets

Channel Expansion Pattern:

Breakout Confirmation: Rapid channel widening confirms volatility increase and genuine trend establishment

Entry Timing: Enter positions early in expansion phase before trend becomes overextended

Risk Management: Use channel width to size stops appropriately, wider channels require wider stops

Basis Bounce Pattern:

Clean Bounce: Price touches middle band and immediately reverses, confirms trend strength and entry opportunity

Multiple Bounces: Repeated basis bounces indicate strong, sustainable trend

Bounce Failure: Price penetrating basis signals weakening trend and potential reversal

Divergence Analysis:

Price/Channel Divergence: Price makes new high/low while staying within channel (not reaching outer band), suggests momentum weakening

Width/Price Divergence: Price breaks to new extremes but channel width contracts, suggests move lacks conviction

Reversal Signal: Divergences often precede trend reversals or significant consolidation periods

Multi-Timeframe Analysis:

Keltner Channels work particularly well in multi-timeframe trend-following approaches:

Three-Timeframe Alignment:

Higher Timeframe (Weekly/Daily): Identify major trend direction, note price position relative to basis and channels

Intermediate Timeframe (Daily/4H): Identify pullback opportunities within higher timeframe trend

Lower Timeframe (4H/1H): Time precise entries when price touches middle band or lower channel (in uptrends) with rejection

Optimal Entry Conditions:

Best Long Entries: Higher timeframe in uptrend (price above basis), intermediate timeframe pulls back to basis, lower timeframe shows rejection at middle band or lower channel

Best Short Entries: Higher timeframe in downtrend (price below basis), intermediate timeframe bounces to basis, lower timeframe shows rejection at middle band or upper channel

Risk Management: Use higher timeframe channel width to set position sizing, stops below/above higher timeframe channels

🎯 STRATEGIC APPLICATIONS

Keltner Channel Enhanced excels in trend-following and breakout strategies across different market conditions.

Trend Following Strategy:

Setup Requirements:

Identify established trend with price consistently on one side of basis line

Wait for pullback to middle band (basis) or brief penetration through it

Confirm trend resumption with price rejection at basis and move back toward outer channel

Enter in trend direction with stop beyond basis line

Entry Rules:

Uptrend Entry:

Price pulls back from upper channel to middle band, shows support at basis (bullish candlestick, momentum divergence)

Enter long on rejection/bounce from basis with stop 1-2 ATR below basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Downtrend Entry:

Price bounces from lower channel to middle band, shows resistance at basis (bearish candlestick, momentum divergence)

Enter short on rejection/reversal from basis with stop 1-2 ATR above basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Trend Management:

Trailing Stop: Use basis line as dynamic trailing stop, exit if price closes beyond basis against position

Profit Taking: Take partial profits at opposite channel, move stops to basis

Position Additions: Add to winners on subsequent basis bounces if trend intact

Breakout Strategy:

Setup Requirements:

Identify consolidation period with contracting channel width

Monitor price action near middle band with reduced volatility

Wait for decisive breakout beyond channel range with expanding width

Enter in breakout direction after confirmation

Breakout Confirmation:

Price breaks clearly outside channel (upper for longs, lower for shorts), channel width begins expanding from contracted state

Volume increases significantly on breakout (if using volume analysis)

Price sustains outside channel for multiple bars without immediate reversal

Entry Approaches:

Aggressive: Enter on initial break with stop at opposite channel or basis, use smaller position size

Conservative: Wait for pullback to broken channel level, enter on rejection and resumption, tighter stop

Volatility-Based Position Sizing:

Adjust position sizing based on channel width (ATR-based volatility):

Wide Channels (High ATR): Reduce position size as stops must be wider, calculate position size using ATR-based risk calculation: Risk / (Stop Distance in ATR × ATR Value)

Narrow Channels (Low ATR): Increase position size as stops can be tighter, be cautious of impending volatility expansion

ATR-Based Risk Management: Use ATR-based risk calculations, position size = 0.01 × Capital / (2 × ATR), use multiples of ATR (1-2 ATR) for adaptive stops

Algorithm Selection Guidelines:

Different market conditions benefit from different algorithm combinations:

Strong Trending Markets: Middle band use EMA or HMA, ATR use RMA, capture trends quickly while maintaining stable channel width

Choppy/Ranging Markets: Middle band use SMA or WMA, ATR use SMA or WMA, avoid false trend signals while identifying genuine reversals

Volatile Markets: Middle band and ATR both use KAMA or FRAMA, self-adjusting to changing market conditions reduces manual optimization

Breakout Trading: Middle band use SMA, ATR use EMA or SMA, stable trend with dynamic channels highlights volatility expansion early

Scalping/Day Trading: Middle band use HMA or T3, ATR use EMA or TEMA, both components respond quickly

Position Trading: Middle band use EMA/TEMA/T3, ATR use RMA or TEMA, filter out noise for long-term trend-following

📋 DETAILED PARAMETER CONFIGURATION

Understanding and optimizing parameters is essential for adapting Keltner Channel Enhanced to specific trading approaches.

Source Parameter:

Close (Most Common): Uses closing price, reflects daily settlement, best for end-of-day analysis and position trading, standard choice

HL2 (Median Price): Smooths out closing bias, better represents full daily range in volatile markets, good for swing trading

HLC3 (Typical Price): Gives more weight to close while including full range, popular for intraday applications, slightly more responsive than HL2

OHLC4 (Average Price): Most comprehensive price representation, smoothest option, good for gap-prone markets or highly volatile instruments

Length Parameter:

Controls the lookback period for middle band (basis) calculation:

Short Periods (10-15): Very responsive to price changes, suitable for day trading and scalping, higher false signal rate

Standard Period (20 - Default): Represents approximately one month of trading, good balance between responsiveness and stability, suitable for swing and position trading

Medium Periods (30-50): Smoother trend identification, fewer false signals, better for position trading and longer holding periods

Long Periods (50+): Very smooth, identifies major trends only, minimal false signals but significant lag, suitable for long-term investment

Optimization by Timeframe: 1-15 minute charts use 10-20 period, 30-60 minute charts use 20-30 period, 4-hour to daily charts use 20-40 period, weekly charts use 20-30 weeks.

ATR Length Parameter:

Controls the lookback period for Average True Range calculation, affecting channel width:

Short ATR Periods (5-10): Very responsive to recent volatility changes, standard is 10 (Keltner's original specification), may be too reactive in whipsaw conditions

Standard ATR Period (10 - Default): Chester Keltner's original specification, good balance between responsiveness and stability, most widely used

Medium ATR Periods (14-20): Smoother channel width, ATR 14 aligns with Wilder's original ATR specification, good for position trading

Long ATR Periods (20+): Very smooth channel width, suitable for long-term trend-following

Length vs. ATR Length Relationship: Equal values (20/20) provide balanced responsiveness, longer ATR (20/14) gives more stable channel width, shorter ATR (20/10) is standard configuration, much shorter ATR (20/5) creates very dynamic channels.

Multiplier Parameter:

Controls channel width by setting ATR multiples:

Lower Values (1.0-1.5): Tighter channels with frequent price touches, more trading signals, higher false signal rate, better for range-bound and mean-reversion strategies

Standard Value (2.0 - Default): Chester Keltner's recommended setting, good balance between signal frequency and reliability, suitable for both trending and ranging strategies

Higher Values (2.5-3.0): Wider channels with less frequent touches, fewer but potentially higher-quality signals, better for strong trending markets

Market-Specific Optimization: High volatility markets (crypto, small-caps) use 2.5-3.0 multiplier, medium volatility markets (major forex, large-caps) use 2.0 multiplier, low volatility markets (bonds, utilities) use 1.5-2.0 multiplier.

MA Type Parameter (Middle Band):

Critical selection that determines trend identification characteristics:

EMA (Exponential Moving Average - Default): Standard Keltner Channel choice, Chester Keltner's original specification, emphasizes recent prices, faster response to trend changes, suitable for all timeframes

SMA (Simple Moving Average): Equal weighting of all data points, no directional bias, slower than EMA, better for ranging markets and mean-reversion

HMA (Hull Moving Average): Minimal lag with smooth output, excellent for fast trend identification, best for day trading and scalping

TEMA (Triple Exponential Moving Average): Advanced smoothing with reduced lag, responsive to trends while filtering noise, suitable for volatile markets

T3 (Tillson T3): Very smooth with minimal lag, excellent for established trend identification, suitable for position trading

KAMA (Kaufman Adaptive Moving Average): Automatically adjusts speed based on market efficiency, slow in ranging markets, fast in trends, suitable for markets with varying conditions

ATR MA Type Parameter:

Determines how Average True Range is smoothed, affecting channel width stability:

RMA (Wilder's Smoothing - Default): J. Welles Wilder's original ATR smoothing method, very smooth, slow to adapt to volatility changes, provides stable channel width

SMA (Simple Moving Average): Equal weighting, moderate smoothness, faster response to volatility changes than RMA, more dynamic channel width

EMA (Exponential Moving Average): Emphasizes recent volatility, quick adaptation to new volatility regimes, very responsive channel width changes

TEMA (Triple Exponential Moving Average): Smooth yet responsive, good balance for varying volatility, suitable for most trading styles

Parameter Combination Strategies:

Conservative Trend-Following: Length 30/ATR Length 20/Multiplier 2.5, MA Type EMA or TEMA/ATR MA Type RMA, smooth trend with stable wide channels, suitable for position trading

Standard Balanced Approach: Length 20/ATR Length 10/Multiplier 2.0, MA Type EMA/ATR MA Type RMA, classic Keltner Channel configuration, suitable for general purpose swing trading

Aggressive Day Trading: Length 10-15/ATR Length 5-7/Multiplier 1.5-2.0, MA Type HMA or EMA/ATR MA Type EMA or SMA, fast trend with dynamic channels, suitable for scalping and day trading

Breakout Specialist: Length 20-30/ATR Length 5-10/Multiplier 2.0, MA Type SMA or WMA/ATR MA Type EMA or SMA, stable trend with responsive channel width

Adaptive All-Conditions: Length 20/ATR Length 10/Multiplier 2.0, MA Type KAMA or FRAMA/ATR MA Type KAMA or TEMA, self-adjusting to market conditions

Offset Parameter:

Controls horizontal positioning of channels on chart. Positive values shift channels to the right (future) for visual projection, negative values shift left (past) for historical analysis, zero (default) aligns with current price bars for real-time signal analysis. Offset affects only visual display, not alert conditions or actual calculations.

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Keltner Channel Enhanced provides improvements over standard implementations while maintaining proven effectiveness.

Response Characteristics:

Standard EMA/RMA Configuration: Moderate trend lag (approximately 0.4 × length periods), smooth and stable channel width from RMA smoothing, good balance for most market conditions

Fast HMA/EMA Configuration: Approximately 60% reduction in trend lag compared to EMA, responsive channel width from EMA ATR smoothing, suitable for quick trend changes and breakouts

Adaptive KAMA/KAMA Configuration: Variable lag based on market efficiency, automatic adjustment to trending vs. ranging conditions, self-optimizing behavior reduces manual intervention

Comparison with Traditional Keltner Channels:

Enhanced Version Advantages:

Dual Algorithm Flexibility: Independent MA selection for trend and volatility vs. fixed EMA/RMA, separate tuning of trend responsiveness and channel stability

Market Adaptation: Choose configurations optimized for specific instruments and conditions, customize for scalping, swing, or position trading preferences

Comprehensive Alerts: Enhanced alert system including channel expansion detection

Traditional Version Advantages:

Simplicity: Fewer parameters, easier to understand and implement

Standardization: Fixed EMA/RMA combination ensures consistency across users

Research Base: Decades of backtesting and research on standard configuration

When to Use Enhanced Version: Trading multiple instruments with different characteristics, switching between trending and ranging markets, employing different strategies, algorithm-based trading systems requiring customization, seeking optimization for specific trading style and timeframe.

When to Use Standard Version: Beginning traders learning Keltner Channel concepts, following published research or trading systems, preferring simplicity and standardization, wanting to avoid optimization and curve-fitting risks.

Performance Across Market Conditions:

Strong Trending Markets: EMA or HMA basis with RMA or TEMA ATR smoothing provides quicker trend identification, pullbacks to basis offer excellent entry opportunities

Choppy/Ranging Markets: SMA or WMA basis with RMA ATR smoothing and lower multipliers, channel bounce strategies work well, avoid false breakouts

Volatile Markets: KAMA or FRAMA with EMA or TEMA, adaptive algorithms excel by automatic adjustment, wider multipliers (2.5-3.0) accommodate large price swings

Low Volatility/Consolidation: Channels narrow significantly indicating consolidation, algorithm choice less impactful, focus on detecting channel width contraction for breakout preparation

Keltner Channel vs. Bollinger Bands - Usage Comparison:

Favor Keltner Channels When: Trend-following is primary strategy, trading volatile instruments with gaps, want ATR-based volatility measurement, prefer fewer higher-quality channel touches, seeking stable channel width during trends.

Favor Bollinger Bands When: Mean-reversion is primary strategy, trading instruments with limited gaps, want statistical framework based on standard deviation, need squeeze patterns for breakout identification, prefer more frequent trading opportunities.

Use Both Together: Bollinger Band squeeze + Keltner Channel breakout is powerful combination, price outside Bollinger Bands but inside Keltner Channels indicates moderate signal, price outside both indicates very strong signal, Bollinger Bands for entries and Keltner Channels for trend confirmation.

Limitations and Considerations:

General Limitations:

Lagging Indicator: All moving averages lag price, even with reduced-lag algorithms

Trend-Dependent: Works best in trending markets, less effective in choppy conditions

No Direction Prediction: Indicates volatility and deviation, not future direction, requires confirmation

Enhanced Version Specific Considerations:

Optimization Risk: More parameters increase risk of curve-fitting historical data

Complexity: Additional choices may overwhelm beginning traders

Backtesting Challenges: Different algorithms produce different historical results

Mitigation Strategies:

Use Confirmation: Combine with momentum indicators (RSI, MACD), volume, or price action

Test Parameter Robustness: Ensure parameters work across range of values, not just optimized ones

Multi-Timeframe Analysis: Confirm signals across different timeframes

Proper Risk Management: Use appropriate position sizing and stops

Start Simple: Begin with standard EMA/RMA before exploring alternatives

Optimal Usage Recommendations:

For Maximum Effectiveness:

Start with standard EMA/RMA configuration to understand classic behavior

Experiment with alternatives on demo account or paper trading

Match algorithm combination to market condition and trading style

Use channel width analysis to identify market phases

Combine with complementary indicators for confirmation

Implement strict risk management using ATR-based position sizing

Focus on high-quality setups rather than trading every signal

Respect the trend: trade with basis direction for higher probability

Complementary Indicators:

RSI or Stochastic: Confirm momentum at channel extremes

MACD: Confirm trend direction and momentum shifts

Volume: Validate breakouts and trend strength

ADX: Measure trend strength, avoid Keltner signals in weak trends

Support/Resistance: Combine with traditional levels for high-probability setups

Bollinger Bands: Use together for enhanced breakout and volatility analysis

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Keltner Channel Enhanced has limitations and should not be used as the sole basis for trading decisions. While the flexible moving average selection for both trend and volatility components provides valuable adaptability across different market conditions, algorithm performance varies with market conditions, and past characteristics do not guarantee future results.

Key considerations:

Always use multiple forms of analysis and confirmation before entering trades

Backtest any parameter combination thoroughly before live trading

Be aware that optimization can lead to curve-fitting if not done carefully

Start with standard EMA/RMA settings and adjust only when specific conditions warrant

Understand that no moving average algorithm can eliminate lag entirely

Consider market regime (trending, ranging, volatile) when selecting parameters

Use ATR-based position sizing and risk management on every trade

Keltner Channels work best in trending markets, less effective in choppy conditions

Respect the trend direction indicated by price position relative to basis line

The enhanced flexibility of dual algorithm selection provides powerful tools for adaptation but requires responsible use, thorough understanding of how different algorithms behave under various market conditions, and disciplined risk management.

MACD Enhanced [DCAUT]█ MACD Enhanced

📊 ORIGINALITY & INNOVATION

The MACD Enhanced represents a significant improvement over traditional MACD implementations. While Gerald Appel's original MACD from the 1970s was limited to exponential moving averages (EMA), this enhanced version expands algorithmic options by supporting 21 different moving average calculations for both the main MACD line and signal line independently.

This improvement addresses an important limitation of traditional MACD: the inability to adapt the indicator's mathematical foundation to different market conditions. By allowing traders to select from algorithms ranging from simple moving averages (SMA) for stability to advanced adaptive filters like Kalman Filter for noise reduction, this implementation changes MACD from a fixed-algorithm tool into a flexible instrument that can be adjusted for specific market environments and trading strategies.

The enhanced histogram visualization system uses a four-color gradient that helps communicate momentum strength and direction more clearly than traditional single-color histograms.

📐 MATHEMATICAL FOUNDATION

The core calculation maintains the proven MACD formula: Fast MA(source, fastLength) - Slow MA(source, slowLength), but extends it with algorithmic flexibility. The signal line applies the selected smoothing algorithm to the MACD line over the specified signal period, while the histogram represents the difference between MACD and signal lines.

Available Algorithms:

The implementation supports a comprehensive spectrum of technical analysis algorithms:

Basic Averages: SMA (arithmetic mean), EMA (exponential weighting), RMA (Wilder's smoothing), WMA (linear weighting)

Advanced Averages: HMA (Hull's low-lag), VWMA (volume-weighted), ALMA (Arnaud Legoux adaptive)

Mathematical Filters: LSMA (least squares regression), DEMA (double exponential), TEMA (triple exponential), ZLEMA (zero-lag exponential)

Adaptive Systems: T3 (Tillson T3), FRAMA (fractal adaptive), KAMA (Kaufman adaptive), MCGINLEY_DYNAMIC (reactive to volatility)

Signal Processing: ULTIMATE_SMOOTHER (low-pass filter), LAGUERRE_FILTER (four-pole IIR), SUPER_SMOOTHER (two-pole Butterworth), KALMAN_FILTER (state-space estimation)

Specialized: TMA (triangular moving average), LAGUERRE_BINOMIAL_FILTER (binomial smoothing)

Each algorithm responds differently to price action, allowing traders to match the indicator's behavior to market characteristics: trending markets benefit from responsive algorithms like EMA or HMA, while ranging markets require stable algorithms like SMA or RMA.

📊 COMPREHENSIVE SIGNAL ANALYSIS

Histogram Interpretation:

Positive Values: Indicate bullish momentum when MACD line exceeds signal line, suggesting upward price pressure and potential buying opportunities

Negative Values: Reflect bearish momentum when MACD line falls below signal line, indicating downward pressure and potential selling opportunities

Zero Line Crosses: MACD crossing above zero suggests transition to bullish bias, while crossing below indicates bearish bias shift

Momentum Changes: Rising histogram (regardless of positive/negative) signals accelerating momentum in the current direction, while declining histogram warns of momentum deceleration

Advanced Signal Recognition:

Divergences: Price making new highs/lows while MACD fails to confirm often precedes trend reversals

Convergence Patterns: MACD line approaching signal line suggests impending crossover and potential trade setup

Histogram Peaks: Extreme histogram values often mark momentum exhaustion points and potential reversal zones

🎯 STRATEGIC APPLICATIONS

Comprehensive Trend Confirmation Strategies:

Primary Trend Validation Protocol:

Identify primary trend direction using higher timeframe (4H or Daily) MACD position relative to zero line

Confirm trend strength by analyzing histogram progression: consistent expansion indicates strong momentum, contraction suggests weakening

Use secondary confirmation from MACD line angle: steep angles (>45°) indicate strong trends, shallow angles suggest consolidation

Validate with price structure: trending markets show consistent higher highs/higher lows (uptrend) or lower highs/lower lows (downtrend)

Entry Timing Techniques:

Pullback Entries in Uptrends: Wait for MACD histogram to decline toward zero line without crossing, then enter on histogram expansion with MACD line still above zero

Breakout Confirmations: Use MACD line crossing above zero as confirmation of upward breakouts from consolidation patterns

Continuation Signals: Look for MACD line re-acceleration (steepening angle) after brief consolidation periods as trend continuation signals

Advanced Divergence Trading Systems:

Regular Divergence Recognition:

Bullish Regular Divergence: Price creates lower lows while MACD line forms higher lows. This pattern is traditionally considered a potential upward reversal signal, but should be combined with other confirmation signals

Bearish Regular Divergence: Price makes higher highs while MACD shows lower highs. This pattern is traditionally considered a potential downward reversal signal, but trading decisions should incorporate proper risk management

Hidden Divergence Strategies:

Bullish Hidden Divergence: Price shows higher lows while MACD displays lower lows, indicating trend continuation potential. Use for adding to existing long positions during pullbacks

Bearish Hidden Divergence: Price creates lower highs while MACD forms higher highs, suggesting downtrend continuation. Optimal for adding to short positions during bear market rallies

Multi-Timeframe Coordination Framework:

Three-Timeframe Analysis Structure:

Primary Timeframe (Daily): Determine overall market bias and major trend direction. Only trade in alignment with daily MACD direction

Secondary Timeframe (4H): Identify intermediate trend changes and major entry opportunities. Use for position sizing decisions

Execution Timeframe (1H): Precise entry and exit timing. Look for MACD line crossovers that align with higher timeframe bias

Timeframe Synchronization Rules:

Daily MACD above zero + 4H MACD rising = Strong uptrend context for long positions

Daily MACD below zero + 4H MACD declining = Strong downtrend context for short positions

Conflicting signals between timeframes = Wait for alignment or use smaller position sizes

1H MACD signals only valid when aligned with both higher timeframes

Algorithm Considerations by Market Type:

Trending Markets: Responsive algorithms like EMA, HMA may be considered, but effectiveness should be tested for specific market conditions

Volatile Markets: Noise-reducing algorithms like KALMAN_FILTER, SUPER_SMOOTHER may help reduce false signals, though results vary by market

Range-Bound Markets: Stability-focused algorithms like SMA, RMA may provide smoother signals, but individual testing is required

Short Timeframes: Low-lag algorithms like ZLEMA, T3 theoretically respond faster but may also increase noise

Important Note: All algorithm choices and parameter settings should be thoroughly backtested and validated based on specific trading strategies, market conditions, and individual risk tolerance. Different market environments and trading styles may require different configuration approaches.

📋 DETAILED PARAMETER CONFIGURATION

Comprehensive Source Selection Strategy:

Price Source Analysis and Optimization:

Close Price (Default): Most commonly used, reflects final market sentiment of each period. Best for end-of-day analysis, swing trading, daily/weekly timeframes. Advantages: widely accepted standard, good for backtesting comparisons. Disadvantages: ignores intraday price action, may miss important highs/lows

HL2 (High+Low)/2: Midpoint of the trading range, reduces impact of opening gaps and closing spikes. Best for volatile markets, gap-prone assets, forex markets. Calculation impact: smoother MACD signals, reduced noise from price spikes. Optimal when asset shows frequent gaps, high volatility during specific sessions

HLC3 (High+Low+Close)/3: Weighted average emphasizing the close while including range information. Best for balanced analysis, most asset classes, medium-term trading. Mathematical effect: 33% weight to high/low, 33% to close, provides compromise between close and HL2. Use when standard close is too noisy but HL2 is too smooth

OHLC4 (Open+High+Low+Close)/4: True average of all price points, most comprehensive view. Best for complete price representation, algorithmic trading, statistical analysis. Considerations: includes opening sentiment, smoothest of all options but potentially less responsive. Optimal for markets with significant opening moves, comprehensive trend analysis

Parameter Configuration Principles:

Important Note: Different moving average algorithms have distinct mathematical characteristics and response patterns. The same parameter settings may produce vastly different results when using different algorithms. When switching algorithms, parameter settings should be re-evaluated and tested for appropriateness.

Length Parameter Considerations:

Fast Length (Default 12): Shorter periods provide faster response but may increase noise and false signals, longer periods offer more stable signals but slower response, different algorithms respond differently to the same parameters and may require adjustment

Slow Length (Default 26): Should maintain a reasonable proportional relationship with fast length, different timeframes may require different parameter configurations, algorithm characteristics influence optimal length settings

Signal Length (Default 9): Shorter lengths produce more frequent crossovers but may increase false signals, longer lengths provide better signal confirmation but slower response, should be adjusted based on trading style and chosen algorithm characteristics

Comprehensive Algorithm Selection Framework:

MACD Line Algorithm Decision Matrix:

EMA (Standard Choice): Mathematical properties: exponential weighting, recent price emphasis. Best for general use, traditional MACD behavior, backtesting compatibility. Performance characteristics: good balance of speed and smoothness, widely understood behavior

SMA (Stability Focus): Equal weighting of all periods, maximum smoothness. Best for ranging markets, noise reduction, conservative trading. Trade-offs: slower signal generation, reduced sensitivity to recent price changes

HMA (Speed Optimized): Hull Moving Average, designed for reduced lag. Best for trending markets, quick reversals, active trading. Technical advantage: square root period weighting, faster trend detection. Caution: can be more sensitive to noise

KAMA (Adaptive): Kaufman Adaptive MA, adjusts smoothing based on market efficiency. Best for varying market conditions, algorithmic trading. Mechanism: fast smoothing in trends, slow smoothing in sideways markets. Complexity: requires understanding of efficiency ratio

Signal Line Algorithm Optimization Strategies:

Matching Strategy: Use same algorithm for both MACD and signal lines. Benefits: consistent mathematical properties, predictable behavior. Best when backtesting historical strategies, maintaining traditional MACD characteristics

Contrast Strategy: Use different algorithms for optimization. Common combinations: MACD=EMA, Signal=SMA for smoother crossovers, MACD=HMA, Signal=RMA for balanced speed/stability, Advanced: MACD=KAMA, Signal=T3 for adaptive behavior with smooth signals

Market Regime Adaptation: Trending markets: both fast algorithms (EMA/HMA), Volatile markets: MACD=KALMAN_FILTER, Signal=SUPER_SMOOTHER, Range-bound: both slow algorithms (SMA/RMA)

Parameter Sensitivity Considerations:

Impact of Parameter Changes:

Length Parameter Sensitivity: Small parameter adjustments can significantly affect signal timing, while larger adjustments may fundamentally change indicator behavior characteristics

Algorithm Sensitivity: Different algorithms produce different signal characteristics. Thoroughly test the impact on your trading strategy before switching algorithms

Combined Effects: Changing multiple parameters simultaneously can create unexpected effects. Recommendation: adjust parameters one at a time and thoroughly test each change

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Response Characteristics by Algorithm:

Fastest Response: ZLEMA, HMA, T3 - minimal lag but higher noise

Balanced Performance: EMA, DEMA, TEMA - good trade-off between speed and stability

Highest Stability: SMA, RMA, TMA - reduced noise but increased lag

Adaptive Behavior: KAMA, FRAMA, MCGINLEY_DYNAMIC - automatically adjust to market conditions

Noise Filtering Capabilities:

Advanced algorithms like KALMAN_FILTER and SUPER_SMOOTHER help reduce false signals compared to traditional EMA-based MACD. Noise-reducing algorithms can provide more stable signals in volatile market conditions, though results will vary based on market conditions and parameter settings.

Market Condition Adaptability:

Unlike fixed-algorithm MACD, this enhanced version allows real-time optimization. Trending markets benefit from responsive algorithms (EMA, HMA), while ranging markets perform better with stable algorithms (SMA, RMA). The ability to switch algorithms without changing indicators provides greater flexibility.

Comparative Performance vs Traditional MACD:

Algorithm Flexibility: 21 algorithms vs 1 fixed EMA

Signal Quality: Reduced false signals through noise filtering algorithms

Market Adaptability: Optimizable for any market condition vs fixed behavior

Customization Options: Independent algorithm selection for MACD and signal lines vs forced matching

Professional Features: Advanced color coding, multiple alert conditions, comprehensive parameter control

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Like all technical indicators, it has limitations and should not be used as the sole basis for trading decisions. Algorithm performance varies with market conditions, and past characteristics do not guarantee future results. Always combine with proper risk management and thorough strategy testing.

Multiple Smoothed Moving AveragesMultiple Smoothed Moving Averages (SMMAs)

This indicator displays up to 5 Smoothed Moving Averages (SMMAs) on your chart, providing a comprehensive view of multiple trend timeframes simultaneously.

═══════════════════════════════════════

WHAT IS A SMOOTHED MOVING AVERAGE?

═══════════════════════════════════════

The Smoothed Moving Average (SMMA), also known as the Running Moving Average (RMA), is a type of moving average that provides more smoothing than a Simple Moving Average (SMA).

Unlike SMA which gives equal weight to all values in the period, SMMA uses a recursive formula that gives more weight to previous SMMA values, resulting in:

- Smoother price action with less noise

- Slower response to recent price changes

- Better identification of longer-term trends

- Reduced false signals in choppy markets

CALCULATION METHOD:

- First value: Simple Moving Average of the initial period

- Subsequent values: (Previous SMMA × (Length - 1) + Current Price) / Length

This recursive nature makes SMMA particularly effective for identifying sustained trends while filtering out short-term volatility.

═══════════════════════════════════════

FEATURES

═══════════════════════════════════════

✓ 5 Independent SMMAs: Each with its own configurable period length

✓ Individual Toggles: Show/hide each SMMA independently

✓ Distinct Colors: Easy visual identification of each moving average

✓ Customizable Lengths: Adjust each period to match your trading strategy

✓ Shared Source: All SMMAs calculate from the same price source (default: close)

✓ Overlay Display: Plots directly on the price chart

═══════════════════════════════════════

DEFAULT SETTINGS

═══════════════════════════════════════

- SMMA 1: 30 periods (Blue)

- SMMA 2: 50 periods (Orange)

- SMMA 3: 100 periods (Green)

- SMMA 4: 200 periods (Purple)

- SMMA 5: 300 periods (Red)

All SMMAs are enabled by default.

═══════════════════════════════════════

HOW TO USE

═══════════════════════════════════════

TREND IDENTIFICATION:

- Price above all SMMAs = Strong uptrend

- Price below all SMMAs = Strong downtrend

- Price between SMMAs = Transitional phase or consolidation

SUPPORT & RESISTANCE:

- SMMAs often act as dynamic support in uptrends

- SMMAs often act as dynamic resistance in downtrends

- Longer-period SMMAs (200, 300) provide stronger S/R levels

CROSSOVER SIGNALS:

- Faster SMMA crossing above slower SMMA = Bullish signal

- Faster SMMA crossing below slower SMMA = Bearish signal

MULTIPLE TIMEFRAME ANALYSIS:

- Short-term trends: 30, 50 periods

- Medium-term trends: 100 periods

- Long-term trends: 200, 300 periods

═══════════════════════════════════════

CUSTOMIZATION

═══════════════════════════════════════

INPUTS TAB:

- Adjust each SMMA length to suit your trading timeframe

- Toggle individual SMMAs on/off using checkboxes

- Change the source (close, open, high, low, hl2, hlc3, ohlc4)

STYLE TAB:

- Modify line colors for each SMMA

- Adjust line thickness and style

- Change transparency levels

═══════════════════════════════════════

NOTES

═══════════════════════════════════════

- This indicator uses the mathematically correct SMMA calculation with the recursive formula

- All calculations are performed on every bar to ensure data consistency

- SMMAs respond more slowly than EMAs but faster than WMAs to price changes

- Best used in combination with other technical analysis tools

- Use on any timeframe

═══════════════════════════════════════

Perfect for traders who want a clear, multi-timeframe view of market trends using the smooth, reliable SMMA calculation method.

EMA Candle ColorEMA Candle Color - Visual EMA-Based Candle Coloring System

Overview:

This indicator provides a visual approach to trend identification by coloring candles based on their relationship with an Exponential Moving Average (EMA). The script dynamically colors both the candle bars and plots custom candles to give traders an immediate visual representation of price momentum relative to the EMA.

How It Works:

The indicator calculates an EMA based on your chosen source (default: open price) and length (default: 10 periods). It then applies a simple yet effective rule:

When the source price is ABOVE the EMA → Candles turn GREEN (bullish)

When the source price is BELOW the EMA → Candles turn RED (bearish)

This instant visual feedback helps traders quickly identify:

Current trend direction

Potential support/resistance levels (the EMA line itself)

Momentum shifts when candles change color

Key Features:

Customizable EMA Parameters: Adjust the EMA length (1-500) and source (open, close, high, low, hl2, hlc3, ohlc4)

Custom Color Selection: Choose your preferred bullish and bearish colors to match your chart theme

Dual Visualization: Both bar coloring and custom plotcandle for enhanced visibility

Offset Capability: Shift the EMA line forward or backward for advanced analysis

Clean Design: Minimal overlay that doesn't clutter your chart

How to Use:

1. Add the indicator to your chart

2. Adjust the EMA Length based on your trading timeframe:

- Shorter periods (5-20) for day trading and scalping

- Medium periods (20-50) for swing trading

- Longer periods (50-200) for position trading

3. Watch for candle color changes as potential entry/exit signals

4. Combine with other indicators for confirmation

Trading Applications:

Trend Following: Stay in trades while candles remain the same color

Reversal Signals: Watch for color changes as early reversal warnings

Filter System: Only take long positions during green candles, shorts during red

Visual Clarity: Quickly assess market sentiment at a glance

Settings:

Length: EMA calculation period (default: 10)

Source: Price data used for EMA calculation (default: open)

Offset: Shift EMA line on chart (default: 0)

Bullish Color: Color for candles above EMA (default: green)

Bearish Color: Color for candles below EMA (default: red)

Technical Details:

The script uses Pine Script v6 and employs the standard ta.ema() function for smooth, responsive EMA calculations. The candle coloring is achieved through both barcolor() and plotcandle() functions, ensuring visibility across different chart settings.

Note:

This indicator works on all timeframes and instruments. For best results, combine with proper risk management and additional confirmation indicators. The EMA Candle Color system is designed to simplify trend identification, not as a standalone trading system.

Tips:

Use on higher timeframes for more reliable signals

Combine with volume analysis for confirmation

Consider using multiple EMA periods for confluence

Disable default candles if using the plotcandle feature to avoid overlap

This script is open-source. Feel free to use it as a foundation for your own trading system or modify it to suit your specific trading style.

Oscillator CandlesticksI've always wondered why we don't use candlesticks for oscillators...then I stopped wondering and made an oscillator with candlesticks.

The following oscillators are available as a proof of concept:

* Consumer Channel Index (CCI)

* Rate of Change (ROC)

* Relative Strength Index (RSI)

* Trend Strength Index (TSI)

You can add a moving average to the ohlc4 value of the oscillator and choose the type of the moving average and whether it should be influenced by volume.

Kalman Filter [DCAUT]█ Kalman Filter

📊 ORIGINALITY & INNOVATION

The Kalman Filter represents an important adaptation of aerospace signal processing technology to financial market analysis. Originally developed by Rudolf E. Kalman in 1960 for navigation and guidance systems, this implementation brings the algorithm's noise reduction capabilities to price trend analysis.

This implementation addresses a common challenge in technical analysis: the trade-off between smoothness and responsiveness. Traditional moving averages must choose between being smooth (with increased lag) or responsive (with increased noise). The Kalman Filter improves upon this limitation through its recursive estimation approach, which continuously balances historical trend information with current price data based on configurable noise parameters.

The key advancement lies in the algorithm's adaptive weighting mechanism. Rather than applying fixed weights to historical data like conventional moving averages, the Kalman Filter dynamically adjusts its trust between the predicted trend and observed prices. This allows it to provide smoother signals during stable periods while maintaining responsiveness during genuine trend changes, helping to reduce whipsaws in ranging markets while not missing significant price movements.

📐 MATHEMATICAL FOUNDATION

The Kalman Filter operates through a two-phase recursive process:

Prediction Phase:

The algorithm first predicts the next state based on the previous estimate:

State Prediction: Estimates the next value based on current trend

Error Covariance Prediction: Calculates uncertainty in the prediction

Update Phase:

Then updates the prediction based on new price observations:

Kalman Gain Calculation: Determines the weight given to new measurements

State Update: Combines prediction with observation based on calculated gain

Error Covariance Update: Adjusts uncertainty estimate for next iteration

Core Parameters:

Process Noise (Q): Represents uncertainty in the trend model itself. Higher values indicate the trend can change more rapidly, making the filter more responsive to price changes.

Measurement Noise (R): Represents uncertainty in price observations. Higher values indicate less trust in individual price points, resulting in smoother output.

Kalman Gain Formula:

The Kalman Gain determines how much weight to give new observations versus predictions:

K = P(k|k-1) / (P(k|k-1) + R)

Where:

K is the Kalman Gain (0 to 1)

P(k|k-1) is the predicted error covariance

R is the measurement noise parameter

When K approaches 1, the filter trusts new measurements more (responsive).

When K approaches 0, the filter trusts its prediction more (smooth).

This dynamic adjustment mechanism allows the filter to adapt to changing market conditions automatically, providing an advantage over fixed-weight moving averages.

📊 COMPREHENSIVE SIGNAL ANALYSIS

Visual Trend Indication:

The Kalman Filter line provides color-coded trend information:

Green Line: Indicates the filter value is rising, suggesting upward price momentum

Red Line: Indicates the filter value is falling, suggesting downward price momentum

Gray Line: Indicates sideways movement with no clear directional bias

Crossover Signals:

Price-filter crossovers generate trading signals:

Golden Cross: Price crosses above the Kalman Filter line, suggests potential bullish momentum development, may indicate a favorable environment for long positions, filter will naturally turn green as it adapts to price moving higher

Death Cross: Price crosses below the Kalman Filter line, suggests potential bearish momentum development, may indicate consideration for position reduction or shorts, filter will naturally turn red as it adapts to price moving lower

Trend Confirmation:

The filter serves as a dynamic trend baseline:

Price Consistently Above Filter: Confirms established uptrend

Price Consistently Below Filter: Confirms established downtrend

Frequent Crossovers: Suggests ranging or choppy market conditions

Signal Reliability Factors:

Signal quality varies based on market conditions:

Higher reliability in trending markets with sustained directional moves

Lower reliability in choppy, range-bound conditions with frequent reversals

Parameter adjustment can help adapt to different market volatility levels

🎯 STRATEGIC APPLICATIONS

Trend Following Strategy:

Use the Kalman Filter as a dynamic trend baseline:

Enter long positions when price crosses above the filter

Enter short positions when price crosses below the filter

Exit when price crosses back through the filter in the opposite direction

Monitor filter slope (color) for trend strength confirmation

Dynamic Support/Resistance:

The filter can act as a moving support or resistance level:

In uptrends: Filter often provides dynamic support for pullbacks

In downtrends: Filter often provides dynamic resistance for bounces

Price rejections from the filter can offer entry opportunities in trend direction

Filter breaches may signal potential trend reversals

Multi-Timeframe Analysis:

Combine Kalman Filters across different timeframes:

Higher timeframe filter identifies primary trend direction

Lower timeframe filter provides precise entry and exit timing

Trade only in direction of higher timeframe trend for better probability

Use lower timeframe crossovers for position entry/exit within major trend

Volatility-Adjusted Configuration:

Adapt parameters to match market conditions:

Low Volatility Markets (Forex majors, stable stocks): Use lower process noise for stability, use lower measurement noise for sensitivity

Medium Volatility Markets (Most equities): Process noise default (0.05) provides balanced performance, measurement noise default (1.0) for general-purpose filtering

High Volatility Markets (Cryptocurrencies, volatile stocks): Use higher process noise for responsiveness, use higher measurement noise for noise reduction

Risk Management Integration:

Use filter as a trailing stop-loss level in trending markets

Tighten stops when price moves significantly away from filter (overextension)

Wider stops in early trend formation when filter is just establishing direction

Consider position sizing based on distance between price and filter

📋 DETAILED PARAMETER CONFIGURATION

Source Selection:

Determines which price data feeds the algorithm:

OHLC4 (default): Uses average of open, high, low, close for balanced representation

Close: Focuses purely on closing prices for end-of-period analysis

HL2: Uses midpoint of high and low for range-based analysis

HLC3: Typical price, gives more weight to closing price

HLCC4: Weighted close price, emphasizes closing values

Process Noise (Q) - Adaptation Speed Control:

This parameter controls how quickly the filter adapts to changes:

Technical Meaning:

Represents uncertainty in the underlying trend model

Higher values allow the estimated trend to change more rapidly

Lower values assume the trend is more stable and slow-changing

Practical Impact:

Lower Values: Produces very smooth output with minimal noise, slower to respond to genuine trend changes, best for long-term trend identification, reduces false signals in choppy markets

Medium Values: Balanced responsiveness and smoothness, suitable for swing trading applications, default (0.05) works well for most markets

Higher Values: More responsive to price changes, may produce more false signals in ranging markets, better for short-term trading and day trading, captures trend changes earlier, adjust freely based on market characteristics

Measurement Noise (R) - Smoothing Control:

This parameter controls how much the filter trusts individual price observations:

Technical Meaning:

Represents uncertainty in price measurements

Higher values indicate less trust in individual price points

Lower values make each price observation more influential

Practical Impact:

Lower Values: More reactive to each price change, less smoothing with more noise in output, may produce choppy signals

Medium Values: Balanced smoothing and responsiveness, default (1.0) provides general-purpose filtering

Higher Values: Heavy smoothing for very noisy markets, reduces whipsaws significantly but increases lag in trend change detection, best for cryptocurrency and highly volatile assets, can use larger values for extreme smoothing

Parameter Interaction:

The ratio between Process Noise and Measurement Noise determines overall behavior:

High Q / Low R: Very responsive, minimal smoothing

Low Q / High R: Very smooth, maximum lag reduction

Balanced Q and R: Middle ground for most applications

Optimization Guidelines:

Start with default values (Q=0.05, R=1.0)

If too many false signals: Increase R or decrease Q