Volume StatsDescription:

Volume Stats displays volume data and statistics for every day of the year, and is designed to work on "1D" timeframe. The data is displayed in a table with columns being months of the year, and rows being days of each month. By default, latest data is displayed, but you have an option to switch to data of the previous year as well.

The statistics displayed for each day is:

- volume

- % of total yearly volume

- % of total monthly volume

The statistics displayed for each column (month) is:

- monthly volume

- % of total yearly volume

- sentiment (was there more bullish or bearish volume?)

- min volume (on which day of the month was the min volume)

- max volume (on which day of the month was the max volume)

The cells change their colors depending on whether the volume is bullish or bearish, and what % of total volume the current cell has (either yearly or monthly). The header cells also change their color (based either on sentiment or what % of yearly volume the current month has).

This is the first (and free) version of the indicator, and I'm planning to create a "PRO" version of this indicator in future.

Parameters:

- Timezone

- Cell data -> which data to display in the cells (no data, volume or percentage)

- Highlight min and max volume -> if checked, cells with min and max volume (either monthly or yearly) will be highlighted with a dot or letter (depending on the "Cell data" input)

- Cell stats mode -> which data to use for color and % calculation (All data = yearly, Column = monthly)

- Display data from previous year -> if checked, the data from previous year will be used

- Header color is calculated from -> either sentiment or % of the yearly volume

- Reverse theme -> the table colors are automatically changed based on the "Dark mode" of Tradingview, this checkbox reverses the logic (so that darker colors will be used when "Dark mode" is off, and lighter colors when it's on)

- Hide logo -> hides the cat logo (PLEASE DO NOT HIDE THE CAT)

Conclusion:

Let me know what you think of the indicator. As I said, I'm planning to make a PRO version with more features, for which I already have some ideas, but if you have any suggestions, please let me know.

Поиск скриптов по запросу "Table"

Candle Body Percentages TableThis script is designed as an analysis tool to visually represent the relative strength of bullish and bearish market sentiments over a specified number of candles. It calculates and displays the percentages of bullish and bearish "candle bodies" as part of the total price range observed in the chosen period.

Here's a breakdown of its functionalities:

User-Defined Period Analysis: Users can specify the number of candles they wish to analyze, allowing for flexible and dynamic examination of market trends over different time frames.

Bullish Body Percentage: The script calculates the combined length of all bullish candle bodies (where the closing price is higher than the opening price) within the selected range and expresses this total as a percentage of the combined price range of all candles analyzed.

Bearish Body Percentage: Similarly, it computes the aggregate length of all bearish candle bodies (where the closing price is lower than the opening price) and presents this sum as a percentage of the total price range.

Visual Representation: The results are displayed in a table format on the chart, providing an immediate visual summary of the prevailing market dynamics. The table shows the percentages of price movement dominated by bullish or bearish sentiment.

Market Sentiment Indicator: This tool can be particularly useful for traders and analysts looking to gauge market sentiment. High bullish body percentages might indicate strong buying pressure, while high bearish body percentages could suggest significant selling pressure.

Strategic Decision Making: By providing a clearer picture of market sentiment over a user-defined period, the script aids in making informed trading decisions, potentially enhancing trading strategies that are sensitive to trends and market momentum.

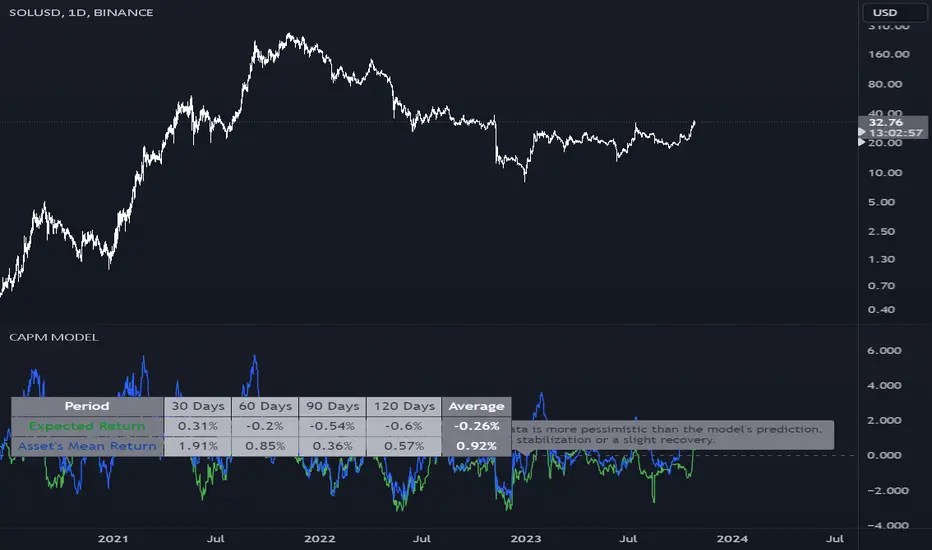

CAPM Model with Returns TableThe given Pine Script is designed to implement the Capital Asset Pricing Model (CAPM) to calculate the expected return for a specified asset over various user-defined periods and compare it with the asset's historical mean return. The core features and functionalities of the script include:

Inputs:

Benchmark Symbol: Defaulted to "CRYPTOCAP:TOTAL". This serves as a comparison metric.

Risk-free Rate: Represents the return on an investment that is considered risk-free.

Benchmark Period: Used for plotting purposes. It doesn't affect table calculations.

Period Settings: Allows users to specify four different time periods for calculations.

Functionalities:

Computes daily returns for the benchmark and asset.

Calculates beta, which represents the volatility of the asset as compared to the volatility of the benchmark.

Uses CAPM to estimate expected returns over user-defined periods.

Generates a table displaying the expected return and asset's mean return for each period.

Provides implications based on the comparison between the expected returns and the asset's historical returns. This is showcased through a mutable label that is updated with each bar.

Visualization:

Plots expected return and asset's mean return over the benchmark period.

Provides a horizontal line to represent zero return.

Use Case:

This script can be helpful for traders or analysts looking to gauge the potential return of an asset compared to its historical performance using the CAPM. The implications provided by the script can serve as useful insights for making investment decisions. It's especially beneficial for those trading or analyzing assets in the cryptocurrency market, given the default benchmark setting.

Note: Before relying on this script for trading decisions, ensure a thorough understanding of its methodology and validate its assumptions against your research.

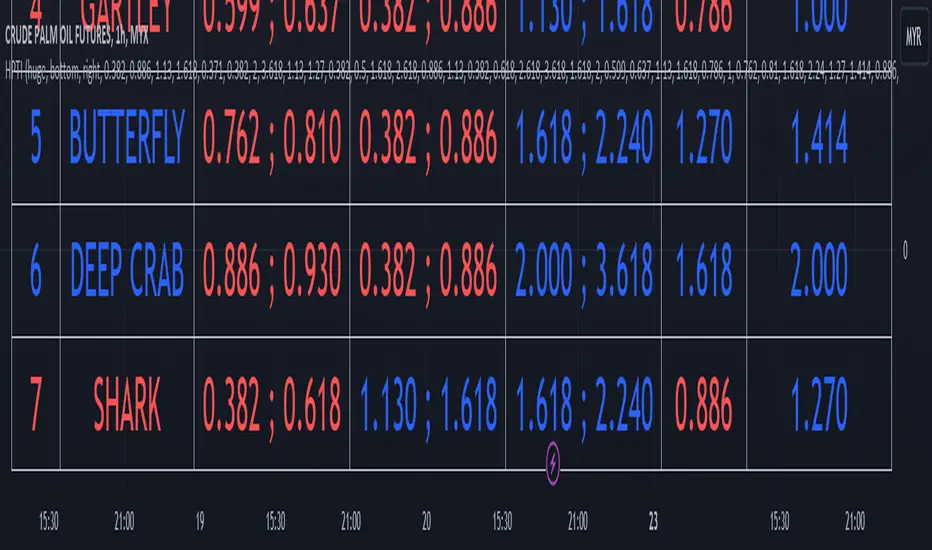

Harmonic Pattern Table Inputs█ OVERVIEW

This indicator was intended as educational purpose only based on Harmonic Pattern Table (Source Code) .

Some user have different ratios in mind, thus I add input to allow user to change those ratios.

█ CREDITS

Scott M Carney, Trading Volume 3: Reaction vs. Reversal

█ CREDITS

1. List Harmonic Patterns.

2. Font size small for mobile app and font size normal for desktop.

3. Font color does automatically change follow dark / light chart theme.

4. Inputs to change ratio values.

█ USAGE / EXAMPLES

TradersCheckListThe Traders Check List is a unique and innovative tool designed to assist traders in their decision-making process. Unlike traditional indicators that provide signals or visual representations of market data, the Traders Check List offers a structured and customizable checklist that traders can use to ensure they're adhering to their trading plan and strategy.

While there are countless indicators available for trend detection, momentum, volatility, and other market aspects, very few tools focus on the trader's process. The Traders Check List fills this gap by providing a visual reminder of key trading considerations directly on the chart.

Functionality:

Upon applying the Traders Check List to a chart, users will see a table displayed, typically in the top right corner. This table contains rows that represent different trading considerations, such as trend direction, risk management, and psychological factors. Each row can be customized by the user to fit their specific trading plan.

For instance, a trader might have a row labeled "Trending Lower" with a corresponding "Yes/No" column to confirm if the current instrument is indeed trending downward.

Underlying Concepts:

The Traders Check List is based on the principle that successful trading is not just about market analysis but also about discipline and consistency. By having a visual checklist on the chart, traders are constantly reminded of their strategy's key components, reducing the likelihood of impulsive or emotional decisions.

How to Use:

Apply the Traders Check List to your desired chart.

Customize the rows based on your trading strategy's key considerations.

As you analyze the market, update the checklist to reflect the current conditions and your analysis.

Before entering a trade, review the checklist to ensure all criteria are met.

Intraday Session Table Intraday Session Table indicator up dates the values as per session input. By default session input duration is for 15 minutes. It updates the Intraday Closing Price- Open Price (CL-OP) of session at the end of the session. The next column displays the increase / decrease in CL-OP

The third column displays various values viz ROC, Closing Price, RSI(14 bars), MA20, MA50,Momentum(10 bars),Closing Price-Open Price,Net number of bars (Intraday Red bars minus Green bars) and Net intraday volume in millions.The parameters can be selected from the dropdown list in Input Box.

User can CHECK OUT Table input Box and select from the list to see individual charts.

User can analyze the movement of values to ascertain the trend.It gives fair idea of the up and down movement based on the session wise movement of values. The access to individual charts of some of the values help the user to have a graphic picture of the situation.

DISCLAIMER: For educational and entertainment purpose only .Nothing in this content should be interpreted as financial advice or a recommendation to buy or sell any sort of security/ies or investment/s.

Multi-Timeframe Trend TableThis is the first publication of an indicator to show trend on the higher timeframes and is an English version of the "Mtf Supertrend Table" coded by FxTraderProAsistan. Credit goes to him for the genesis of this work. I updated the original code to Pinescript V.5 and modified it to suit my needs. Please enjoy.

This trend table indicator has the following features:

1. Trend Mode : Option to select the method of determining trend, using the Pinescript built-in ta.supertrend function or finding trend based on the cross of 20 and 50 EMA

2. 6 trend timeframes of your choosing, with show/hide

3. Optional feature to include the DXY (US dollar) trends, for the timeframes chosen. Useful for instruments that react to changes in the US dollar

4. ATR settings to adjust the Supertrend parameters. Default values are an ATR length of 10 and a Factor of 3

Strategy Template + Performance & Returns table + ExtrasA script I've been working on since summer 2022. A template for any strategy so you just have to write or paste the code and go straight into risk management settings

Features:

>Signal only Longs/only Shorts/Both

>Leverage system

>Proper fees calculation (even with leverage on)

>Different Stop Loss systems: Simple percentage, 4 different "move to Break Even" systems and Scaling SL after each TP order (read the disclaimer at the bottom regarding this and the TV % profitable metric)

>2 Take Profit systems: Simple percentages, or Risk/reward ratios based on SL level

>Additional option on TP so last one "rides free" until closure of position or Stoploss is hit (for more than 1 orders)

>Up to 5 TP orders

>Show or hide SL/TP levels on demand

>2 date filters. Manual filter is nothing new, enter two dates/hours and filter will turn on. BUT automatic filter is another thing (thanks to user @bfr_ for his help in codingthis feature)

>AUTOMATIC DATE FILTER. Allows you to split all historical data on the chart in X periods, then choose the range of periods used. Up to 10 but that can be changed, instructions included. Useful for WalkForward simulations, haven't seen a script in TradingView that allows you to do this and test your strategy on "unseen data" automatically

EXTRA SETTINGS

Besides, some additions I like to add to my codes:

>Returns table for monthly and weekly performance. Requires recalculation on every tick. This is a modified version of @QuantNomad's work. May add lower TF options later on

>Volume Based S/R system. Original work from @shtcoinr

>One feature that was made by me, the "portfolio table". Yields info and metrics of your strategy, current position and balance. You're able to turn it off and change its size

Should anyone find an error, or have any idea on how to improve this code, please contact me. Future updates could come, stay tuned

DISCLAIMER:

In order to have accurate StopLoss hit, I had to change the previous system, which was a "close position on candle close" instead at actual stoploss level. It was fixed, but resulted on inflation of the number of trading orders, thus reducing the percent profitable and making it strongly biased and unreal. Keep that in mind, that "real" profitability could be 2x or 3x the metric TradingView says. If your strategy has a really high trading frequency, resulting in 3000+ orders, might be a problem. Try to make use of the automatic/manual date filter as workaround, I have no means of changing this, seems it is not a bug but an intended design of the PineScript Code

Volume Price and FundamentalsVolume Price and Fundamentals indicators contains 4 exponential moving averages based upon Fibonnaci numbers as period (8, 21, 55 & 144) with crossovers and crossunders.

It also contain a table for volume and 50 Day Avg. Volume, Relative volume, Change in Volume, Volume Value, Up-Down Closing Basis days in last 50 days, Volume ratio (U/D Ratio) on last 50-day Up / Down days and along with fundamental analysis table with various Fundamental Analysis parameters and QoQ & YoY comparison basis for better investment decision making.

Risk Calculation Table - Amount BasedHello, this is my first script, and I believe that understanding the Risk and Reward is also the first essential step to become a successful trader.

Well maybe there are a lot of script like this but I think no one was suitable for me, so I learnt how to make one.

I think I need to explain some aspects about this script:

Input Section :

1. Entry = Entry Price.

2. SL = Stop Loss Price.

3. TP = Take Profit Price.

4. Amount = How much dollars you trade on this trade.

4. Ticker's Decimal = The number behind the decimal, to adjust this just type how much 0 you want behind the decimal.

Output Section :

1. You can adjust the lines plotted on the chart to automatically enter your entry, stop loss, and take profit price.

2. The table's appearance can be repositioned and resized.

3. The terms in the table, I think it's clear enough for everyone to understand.

If there are any critics or suggestions, I will appreciate it so much.

Greetings from Indonesia :)

Annual Returns % Comparison [By MUQWISHI]Overview

The Annual Returns % Comparison indicator aimed to compare the historical annual percentage change of any two symbols. The indicator output shows a column-plot that was developed by two using a pine script table, so each period has pair columns showing the yearly percentage change for entered symbols.

Features

- Enter date range.

- Fill up with any two symbols.

- Choose the output data whether adjusted or not.

- Change the location of the table plot

- Color columns by a symbol.

- Size the height and width of columns.

- Color background, border, and text.

- The tooltip of the column value appears once the cursor sets above the specific column. As it seen below.

Let me know if you have any questions.

Thanks.

Multi-timeframe Moving Average with Summary TableThis script aims to keep you orientated with regard to moving averages on higher time frames when working in the lower timeframe. It will show the given MA specification from you current timeframe and the timeframes above. In addition, it also shows a summary table of what the MAs on the other timeframes are doing (trending up/down, flat).

So if you are on the 15 minute timeframe looking at the 20SMA you will know where the 20SMA is on the 1hour, 4hour, 1D, 1W, 1M. You also know the direction of the upper timeframe mas (the 1 hour is trending up but the 4hour is flat etc).

Defining whether an MA is trending is a little subjective but the script making a reasonable job of it - it compares the current MA level to the MA level the defined bars back and compares that to the average true range. (That way it works the same across all currencies regardless of their natural volatility. There is a check feature so you can understand the results your settings are creating.

summary table

show mas

check feature

Gann Square 4 Cross Cardinal Table ConceptThis indicator was intended as educational purpose only for Gann Square 4, specifically to show Cross Cardinal.

This indicator was build upon The Tunnel Thru The Air Or Looking Back From 1940, written by WD Gann.

Gann Square 4 is similar to Gann Square 9 (Refer this build) but limited to Cross Cardinal only.

Indikator ini bertujuan sebagai pendidikan sahaja untuk Gann Square 4, khusus untuk menunjukkan Cross Cardinal.

Indikator ini dibina berdasarkan buku The Tunnel Thru The Air Or Looking Back From 1940, ditulis oleh WD Gann.

Gann Square 4 hampir sama dengan Gann Square 9 (Rujuk binaan ini) tetapi terhad kepada Cross Cardinal sahaja.

Indicator features :

1. Font size from tiny to huge.

2. For desktop display only, not for mobile.

3. All values can be selected individually.

Kemampuan indikator :

1. Saiz font dari paling kecil ke paling besar.

2. Untuk paparan desktop sahaja, bukan untuk mobile.

3. Semua nilai boleh dipilih secara individu.

FAQ

1. Credits / Kredit

WD Gann , The Tunnel Thru The Air Or Looking Back From 1940

Ganzilla

2. Page involved / Muka Surat terlibat

195 - 198

3. Code Usage / Penggunaan Kod

Free to use for personal usage.

Bebas untuk kegunaan peribadi.

Left : All values off / Kiri : Semua nilai off

Right : All values on / Kanan : Semua nilai on

Left : Random Usage / Kiri : Kegunaan Random

Right : Ideal Usage / Kanan : Kegunaan Ideal

Harmonic Trading Ratios Educational (Source Code)This table indicator was intended as educational purpose only for Harmonic Trading Ratios.

The ratios are used for Harmonic AB=CD and XAB=CD.

Ratio calculation are shown for Retracement and Projection based Primary, Primary Derived, Secondary Derived and Secondary Derived Extreme.

Primary Retracement : 0.618

Primary Projection : 1.618

Please take note that Secondary Derived Extreme is only available for Projection.

Indikator berjadual bertujuan sebagai pendidikan sahaja untuk Harmonic Trading Ratios.

Ratio digunakan untuk Harmonic AB=CD and XAB=CD.

Pengiraan ratio untuk Retracement and Projection adalah berdasarkan Primary, Primary Derived, Secondary Derived dan Secondary Derived Extreme.

Primary Retracement : 0.618

Primary Projection : 1.618

Sila ambil perhatian bahawa Secondary Derived Extreme adalah untuk Projection sahaja.

The values shown in table was based on Harmonic Trading: Volume One, Page 18 written by Scott M Carney.

Nilai yang ditunjukkan dalam jadual adalah berdasarkan buku Harmonic Trading: Volume One, Page 18 ditulis oleh Scott M Carney.

Indicator features :

1. List Harmonic Trading Ratios including calculation.

2. Show and draw individual Harmonic Trading Ratio.

3. For desktop display only, not for mobile.

Kemampuan indikator :

1. Senarai Harmonic Trading Ratios termasuk pengiraan.

2. Memapar dan melukis Harmonic Trading Ratio secara berasingan.

3. Untuk paparan desktop sahaja, bukan untuk mobile.

FAQ

1. Credits / Kredit

Scott M Carney,

Scott M Carney, Harmonic Trading: Volume One

2. Code Usage / Penggunaan Kod

Free to use for personal usage but credits are most welcomed especially for credits to Scott M Carney.

Bebas untuk kegunaan peribadi tetapi kredit adalah amat dialu-alukan terutamanya kredit kepada Scott M Carney.

Display for Bullish / Bearish Retracement

Paparan untuk Bullish / Bearish Retracement

Display for Primary Retracement and Primary Projection

Paparan untuk Primary Retracement and Primary Projection

Display for Secondary Derived Extreme Retracement and Secondary Derived Extreme Projection

Paparan untuk Secondary Derived Extreme Retracement and Secondary Derived Extreme Projection

Technical Ratings Colored CandlesFor those that want technical ratings but don't want waste valuable screen real estate. Candles are colored to the rating strength. It also plots the results for "total", "MA" and "other" in a table on right of screen. Table and candle coloring can be turned off in style settings. This script uses the built in Technical Ratings indicator. For more informations on Technical Ratings please refer to official documentation.

ADR% / ATR / LoD dist. TableDisplays the following values in a table in the upper right corner of the chart:

ADR%: Average daily range (in percent).

ATR: Average true range (hidden by default).

LoD dist.: Distance of current price to low of the day as a percentage of ATR.

All values are calculated based on daily bars, no matter what time frame you are currently viewing. Doesn't work for time frames >1D, which is why the table is not shown on weekly/monthly charts.

Credit to MikeC / TheScrutiniser and GlinckEastwoot for ADR% formula

ADR% / ATR / LoD dist. Table - V2ADR% / ATR / LoD Distance Table (V2) + ATR Range Lines is a simple “daily volatility dashboard” that helps you quickly judge how extended a stock is during the day and where “normal” daily movement zones sit relative to price.

It’s designed to help you answer:

“Has this stock already made most of its usual daily move?”

“Am I chasing too late?”

“Where are typical +ATR / −ATR stretch and pullback zones?”

What you’ll see

ADR% (Average Daily Range %)

Shows the stock’s typical daily travel (low → high) as a percentage.

Example: ADR% = 4% means the stock often swings ~4% in a normal day.

ATR (Average True Range)

Shows the stock’s typical daily movement in price units ($ / points).

Example: ATR = 2.50 means it often moves about $2.50 per day.

LoD dist. (Low of Day distance)

Shows how far price is from today’s Low of Day, measured relative to ATR (as a %).

Higher % = more extended away from the day’s low.

Optional: ATR Range Lines (added in this version)

You can enable two guide lines that extend to the right:

ATR Up Line = Price + ATR

ATR Down Line = Price − ATR

These act like volatility guardrails to visualize “typical daily stretch” and “typical pullback” zones.

ATR “Live vs Locked” option (important)

Lock ATR to last completed day (no intraday updates):

ON (Locked): Uses the last completed daily ATR (yesterday’s finished value).

✅ ATR stays constant all day while the market is live.

OFF (Live): ATR can update intraday as today’s daily candle expands.

✅ ATR may change during the session.

Either way, ATR is still based on your chosen ATR Length (lookback period). Locking simply prevents the ATR from drifting intraday.

How to use it (Kullamägi-style principle)

Kristjan Kullamägi’s momentum style emphasizes pressing strength when conditions are right, but also respecting extension and risk/reward. This tool helps you quantify that:

If ADR%/ATR suggests the stock already moved near its usual daily range, chasing can be lower reward.

The ATR lines help you visualize when price is in a “normal stretch zone” vs a better risk area.

Locking ATR gives you stable intraday reference levels for cleaner execution.

Tips

Use ADR% to understand whether there’s likely “room” left in today’s move.

Use LoD dist. to quickly gauge if price is already far from the day’s low (extended).

Use ATR Up/Down Lines as a simple volatility framework for entries, add-ons, and risk planning.

Keep Lock ATR ON if you prefer stable levels throughout the session.

Credits

Original indicator concept & script: ArmerSchlucker

ADR% formula credit: MikeC / TheScrutiniser and GlinckEastwoot

Modifications (V2): TradersPod

Added optional ATR Up/Down lines extending to the right

Added “Lock ATR to last completed day” option for stable intraday ATR reference

Kept the original logic and purpose intact

ATR Table (Top Right) - Multi Rangejust your friendly atr table to multiple ranges and for the sense of what is brewing

Hybrid ST/EMA Cloud + Trend TableSimilar to the hybrid supertrend with trend table, this version adds some EMA preferences

Ultimate Auto Trendlines Improved No lag, No Repaint with TableA major update - cleanest, most accurate non-repainting trendline tool.

What's new in this version:

• Connects MULTIPLE recent pivots (not just consecutive) → stronger, more reliable levels

• Solid lines extended far right → instant future S/R projection

• Built-in table (top-right): Price + EMA 10/20/50 (Above/Below) + MACD (Bull/Bear) + RSI (Bull/Bear) + ADX (Strong/Weak)

• Alerts for new trendlines — get notified the moment a fresh level forms

• Optional "R"/"S" pivot labels — clean visual swing confirmation

• Max 8 lines total → keeps your chart readable and focused

Why traders are adding this right now:

• 100% non-repainting – safe for live entries & alerts

• 80–85%+ touch/bounce rate in trending markets (SPY/QQQ/NASDAQ daily & 4H backtests)

• Angle filter kills flat/noise lines

• Works killer on stocks, indices, forex majors, crypto

Best settings to start:

Pivot Left/Right: 5/5

Min Angle: 12–15°

Max Trendlines: 8

Line Extension: 100–200 bars

Show Labels: On

Want the latest updates, settings tweaks, or new versions first?

Please Follow me on X → @TrendRiderPro1

Drop a like/favorite/comment if you add it – I read every one and reply to as many as I can.

Any feedback (bugs, ideas, your best settings) is super welcome!

Happy trading – let’s catch those clean bounces & big moves! 🚀📈

If you add it, drop a like/favorite/comment — I read every one and reply to as many as I can.

Any feedback (settings, bugs, ideas) is super welcome — helps me keep improving it.

Happy trading — let’s catch those clean bounces & big moves! 🚀

ETF-Futures Opening Ratio (Table)This indicator calculates the opening price ratio between an ETF and its corresponding futures contract using the 9:30 AM New York (RTH) opening price.

The ratio is locked at the official market open and remains fixed throughout the session, providing a stable reference for:

Translating ETF price levels into futures equivalents

Comparing relative value and premium/discount behavior

Maintaining consistent cross-instrument analysis during the trading day

The output is displayed in a simple on-chart table for quick reference and minimal chart clutter.