Trend Filter (2-pole) [BigBeluga]Trend Filter (2-pole)

The Trend Filter (2-pole) is an advanced trend-following indicator based on a two-pole filter, which smooths out market noise while effectively highlighting trends and their strength. It incorporates color gradients and support/resistance dots to enhance trend visualization and decision-making for traders.

SP500:

🔵What is a Two-Pole Filter?

A two-pole filter is a digital signal processing technique widely used in electronics, control systems, and time series data analysis to smooth data and reduce noise.

//@function Two-pole filter

//@param src (series float) Source data (e.g., price)

//@param length (float) Length of the filter (higher value means smoother output)

//@param damping (float) Damping factor for the filter

//@returns (series float) Filtered value

method two_pole_filter(float src, int length, float damping) =>

// Calculate filter coefficients

float omega = 2.0 * math.pi / length

float alpha = damping * omega

float beta = math.pow(omega, 2)

// Initialize the filter variables

var float f1 = na

var float f2 = na

// Update the filter

f1 := nz(f1 ) + alpha * (src - nz(f1 ))

f2 := nz(f2 ) + beta * (f1 - nz(f2 ))

f2

It operates using two cascaded smoothing stages (poles), allowing for a more refined and responsive output compared to simple moving averages or other basic filters.

Two-pole filters are particularly valued for their ability to maintain smooth transitions while reducing lag, making them ideal for applications where precision and responsiveness are critical.

In trading, this filter helps detect trends by smoothing price data while preserving significant directional changes.

🔵Key Features of the Indicator:

Gradient-Colored Trend Filter Line: The main filter line dynamically changes color based on trend strength and direction:

- Green: Strong uptrend.

- Red: Strong downtrend.

- Yellow: Indicates a transition phase, signaling potential trend shifts.

Support and Resistance Dots with Signals:

- Dots are plotted below the filter line during uptrends and above it during downtrends.

- These dots represent consecutive rising or falling conditions of the filter line, which traders can set in the settings (e.g., the number of consecutive rises or falls required).

- The dots often act as dynamic support or resistance levels, providing valuable guidance during trends.

- Trend Signals:

Customizable Sensitivity: The indicator allows traders to adjust the filter length, damping factor, and the threshold for rising/falling conditions, enabling it to adapt to different trading styles and timeframes.

Bar Color Option: The indicator can optionally color bars to match the gradient of the filter line, enhancing visual clarity of trends directly on the price chart.

🔵How It Works:

The Trend Filter (2-pole) smooths price data using a two-pole filter, which reduces noise and highlights the underlying trend.

The gradient coloring of the filter line helps traders visually assess the strength and direction of trends.

Rising and falling conditions of the filter line are tracked, and dots are plotted when consecutive conditions meet the threshold, acting as potential support or resistance levels during trends.

The yellow transition color signals periods of indecision, helping traders anticipate potential reversals or consolidations.

🔵Use Cases:

Identify and follow strong uptrends and downtrends with gradient-based visual cues.

Use the yellow transition color to anticipate trend shifts or consolidation zones.

Leverage the plotted dots as dynamic support and resistance levels to refine entry and exit strategies.

Combine with other indicators for confirmation of trends and reversals.

This indicator is perfect for traders who want a visually intuitive and highly customizable tool to spot trends, gauge their strength, and make informed trading decisions.

Поиск скриптов по запросу "VAR+计量模型+黄金期货"

MTF Countdown with Direction - AynetIndicator Definition and Inputs:

pineCopyindicator('MTF Countdown with Direction - Aynet', overlay = true)

This code creates a Multiple Time Frame (MTF) countdown indicator with direction

The overlay = true parameter places the indicator on top of the price chart

Timeframe Options:

Users can choose to show/hide the following timeframes:

1 minute

5 minutes

15 minutes

30 minutes

1 hour

4 hours

Daily

Time Calculations:

pineCopyget_current_time()

Calculates the current time

Converts Unix timestamp to seconds

Calculates time since midnight

Returns time broken down into hours, minutes, and seconds

Countdown Calculation:

pineCopyget_period_countdown(period_seconds)

Calculates remaining time for each timeframe

Computes elapsed time in current period

Returns remaining time in hours, minutes, and seconds

Direction and Closing Price Calculation:

Separate functions for each timeframe (get_direction_and_close_1m(), get_direction_and_close_5m(), etc.)

Each function:

Gets current closing price

Compares with previous closing price

Determines direction (up: 1, down: -1, sideways: 0)

Returns direction and closing price

Table Creation and Updates:

Creates a table in the top right corner

Table consists of 4 columns:

Period (Timeframe)

Time Left (Remaining time)

Direction (Shown with arrows)

Close (Closing price)

Each row has a different background color

Direction arrows:

Green up arrow (▲): Price rising

Red down arrow (▼): Price falling

Gray line (―): Price sideways

Dynamic Data Structures:

pineCopyvar timeframes = array.new_int()

var timeframe_names = array.new_string()

var show_array = array.new_bool()

Uses dynamic arrays for timeframes

Adds selected timeframes to arrays on first run

Key Features:

Shows remaining time until period close

Displays price direction for each timeframe

Shows current closing prices

All information in a single, easy-to-read table

This indicator helps traders by providing a comprehensive view of:

When each timeframe will close

The direction of price movement

Current closing prices

across multiple timeframes in a single table, making it easier to track market movements across different time periods.

The color-coding and arrow system makes it visually intuitive to understand market direction at a glance, while the countdown timer helps with timing decisions.

TrigWave Suite [InvestorUnknown]The TrigWave Suite combines Sine-weighted, Cosine-weighted, and Hyperbolic Tangent moving averages (HTMA) with a Directional Movement System (DMS) and a Relative Strength System (RSS).

Hyperbolic Tangent Moving Average (HTMA)

The HTMA smooths the price by applying a hyperbolic tangent transformation to the difference between the price and a simple moving average. It also adjusts this value by multiplying it by a standard deviation to create a more stable signal.

// Function to calculate Hyperbolic Tangent

tanh(x) =>

e_x = math.exp(x)

e_neg_x = math.exp(-x)

(e_x - e_neg_x) / (e_x + e_neg_x)

// Function to calculate Hyperbolic Tangent Moving Average

htma(src, len, mul) =>

tanh_src = tanh((src - ta.sma(src, len)) * mul) * ta.stdev(src, len) + ta.sma(src, len)

htma = ta.sma(tanh_src, len)

Sine-Weighted Moving Average (SWMA)

The SWMA applies sine-based weights to historical prices. This gives more weight to the central data points, making it responsive yet less prone to noise.

// Function to calculate the Sine-Weighted Moving Average

f_Sine_Weighted_MA(series float src, simple int length) =>

var float sine_weights = array.new_float(0)

array.clear(sine_weights) // Clear the array before recalculating weights

for i = 0 to length - 1

weight = math.sin((math.pi * (i + 1)) / length)

array.push(sine_weights, weight)

// Normalize the weights

sum_weights = array.sum(sine_weights)

for i = 0 to length - 1

norm_weight = array.get(sine_weights, i) / sum_weights

array.set(sine_weights, i, norm_weight)

// Calculate Sine-Weighted Moving Average

swma = 0.0

if bar_index >= length

for i = 0 to length - 1

swma := swma + array.get(sine_weights, i) * src

swma

Cosine-Weighted Moving Average (CWMA)

The CWMA uses cosine-based weights for data points, which produces a more stable trend-following behavior, especially in low-volatility markets.

f_Cosine_Weighted_MA(series float src, simple int length) =>

var float cosine_weights = array.new_float(0)

array.clear(cosine_weights) // Clear the array before recalculating weights

for i = 0 to length - 1

weight = math.cos((math.pi * (i + 1)) / length) + 1 // Shift by adding 1

array.push(cosine_weights, weight)

// Normalize the weights

sum_weights = array.sum(cosine_weights)

for i = 0 to length - 1

norm_weight = array.get(cosine_weights, i) / sum_weights

array.set(cosine_weights, i, norm_weight)

// Calculate Cosine-Weighted Moving Average

cwma = 0.0

if bar_index >= length

for i = 0 to length - 1

cwma := cwma + array.get(cosine_weights, i) * src

cwma

Directional Movement System (DMS)

DMS is used to identify trend direction and strength based on directional movement. It uses ADX to gauge trend strength and combines +DI and -DI for directional bias.

// Function to calculate Directional Movement System

f_DMS(simple int dmi_len, simple int adx_len) =>

up = ta.change(high)

down = -ta.change(low)

plusDM = na(up) ? na : (up > down and up > 0 ? up : 0)

minusDM = na(down) ? na : (down > up and down > 0 ? down : 0)

trur = ta.rma(ta.tr, dmi_len)

plus = fixnan(100 * ta.rma(plusDM, dmi_len) / trur)

minus = fixnan(100 * ta.rma(minusDM, dmi_len) / trur)

sum = plus + minus

adx = 100 * ta.rma(math.abs(plus - minus) / (sum == 0 ? 1 : sum), adx_len)

dms_up = plus > minus and adx > minus

dms_down = plus < minus and adx > plus

dms_neutral = not (dms_up or dms_down)

signal = dms_up ? 1 : dms_down ? -1 : 0

Relative Strength System (RSS)

RSS employs RSI and an adjustable moving average type (SMA, EMA, or HMA) to evaluate whether the market is in a bullish or bearish state.

// Function to calculate Relative Strength System

f_RSS(rsi_src, rsi_len, ma_type, ma_len) =>

rsi = ta.rsi(rsi_src, rsi_len)

ma = switch ma_type

"SMA" => ta.sma(rsi, ma_len)

"EMA" => ta.ema(rsi, ma_len)

"HMA" => ta.hma(rsi, ma_len)

signal = (rsi > ma and rsi > 50) ? 1 : (rsi < ma and rsi < 50) ? -1 : 0

ATR Adjustments

To minimize false signals, the HTMA, SWMA, and CWMA signals are adjusted with an Average True Range (ATR) filter:

// Calculate ATR adjusted components for HTMA, CWMA and SWMA

float atr = ta.atr(atr_len)

float htma_up = htma + (atr * atr_mult)

float htma_dn = htma - (atr * atr_mult)

float swma_up = swma + (atr * atr_mult)

float swma_dn = swma - (atr * atr_mult)

float cwma_up = cwma + (atr * atr_mult)

float cwma_dn = cwma - (atr * atr_mult)

This adjustment allows for better adaptation to varying market volatility, making the signal more reliable.

Signals and Trend Calculation

The indicator generates a Trend Signal by aggregating the output from each component. Each component provides a directional signal that is combined to form a unified trend reading. The trend value is then converted into a long (1), short (-1), or neutral (0) state.

Backtesting Mode and Performance Metrics

The Backtesting Mode includes a performance metrics table that compares the Buy and Hold strategy with the TrigWave Suite strategy. Key statistics like Sharpe Ratio, Sortino Ratio, and Omega Ratio are displayed to help users assess performance. Note that due to labels and plotchar use, automatic scaling may not function ideally in backtest mode.

Alerts and Visualization

Trend Direction Alerts: Set up alerts for long and short signals

Color Bars and Gradient Option: Bars are colored based on the trend direction, with an optional gradient for smoother visual feedback.

Important Notes

Customization: Default settings are experimental and not intended for trading/investing purposes. Users are encouraged to adjust and calibrate the settings to optimize results according to their trading style.

Backtest Results Disclaimer: Please note that backtest results are not indicative of future performance, and no strategy guarantees success.

FTMO Rules MonitorFTMO Rules Monitor: Stay on Track with Your FTMO Challenge Goals

TLDR; You can test with this template whether your strategy for one asset would pass the FTMO challenges step 1 then step 2, then with real money conditions.

Passing a prop firm challenge is ... challenging.

I believe a toolkit allowing to test in minutes whether a strategy would have passed a prop firm challenge in the past could be very powerful.

The FTMO Rules Monitor is designed to help you stay within FTMO’s strict risk management guidelines directly on your chart. Whether you’re aiming for the $10,000 or the $200,000 account challenge, this tool provides real-time tracking of your performance against FTMO’s rules to ensure you don’t accidentally breach any limits.

NOTES

The connected indicator for this post doesn't matter.

It's just a dummy double supertrends (see below)

The strategy results for this script post does not matter as I'm posting a FTMO rules template on which you can connect any indicator/strategy.

//@version=5

indicator("Supertrends", overlay=true)

// Supertrend 1 Parameters

var string ST1 = "Supertrend 1 Settings"

st1_atrPeriod = input.int(10, "ATR Period", minval=1, maxval=50, group=ST1)

st1_factor = input.float(2, "Factor", minval=0.5, maxval=10, step=0.5, group=ST1)

// Supertrend 2 Parameters

var string ST2 = "Supertrend 2 Settings"

st2_atrPeriod = input.int(14, "ATR Period", minval=1, maxval=50, group=ST2)

st2_factor = input.float(3, "Factor", minval=0.5, maxval=10, step=0.5, group=ST2)

// Calculate Supertrends

= ta.supertrend(st1_factor, st1_atrPeriod)

= ta.supertrend(st2_factor, st2_atrPeriod)

// Entry conditions

longCondition = direction1 == -1 and direction2 == -1 and direction1 == 1

shortCondition = direction1 == 1 and direction2 == 1 and direction1 == -1

// Optional: Plot Supertrends

plot(supertrend1, "Supertrend 1", color = direction1 == -1 ? color.green : color.red, linewidth=3)

plot(supertrend2, "Supertrend 2", color = direction2 == -1 ? color.lime : color.maroon, linewidth=3)

plotshape(series=longCondition, location=location.belowbar, color=color.green, style=shape.triangleup, title="Long")

plotshape(series=shortCondition, location=location.abovebar, color=color.red, style=shape.triangledown, title="Short")

signal = longCondition ? 1 : shortCondition ? -1 : na

plot(signal, "Signal", display = display.data_window)

To connect your indicator to this FTMO rules monitor template, please update it as follow

Create a signal variable to store 1 for the long/buy signal or -1 for the short/sell signal

Plot it in the display.data_window panel so that it doesn't clutter your chart

signal = longCondition ? 1 : shortCondition ? -1 : na

plot(signal, "Signal", display = display.data_window)

In the FTMO Rules Monitor template, I'm capturing this external signal with this input.source variable

entry_connector = input.source(close, "Entry Connector", group="Entry Connector")

longCondition = entry_connector == 1

shortCondition = entry_connector == -1

🔶 USAGE

This indicator displays essential FTMO Challenge rules and tracks your progress toward meeting each one. Here’s what’s monitored:

Max Daily Loss

• 10k Account: $500

• 25k Account: $1,250

• 50k Account: $2,500

• 100k Account: $5,000

• 200k Account: $10,000

Max Total Loss

• 10k Account: $1,000

• 25k Account: $2,500

• 50k Account: $5,000

• 100k Account: $10,000

• 200k Account: $20,000

Profit Target

• 10k Account: $1,000

• 25k Account: $2,500

• 50k Account: $5,000

• 100k Account: $10,000

• 200k Account: $20,000

Minimum Trading Days: 4 consecutive days for all account sizes

🔹 Key Features

1. Real-Time Compliance Check

The FTMO Rules Monitor keeps track of your daily and total losses, profit targets, and trading days. Each metric updates in real-time, giving you peace of mind that you’re within FTMO’s rules.

2. Color-Coded Visual Feedback

Each rule’s status is shown clearly with a ✓ for compliance or ✗ if the limit is breached. When a rule is broken, the indicator highlights it in red, so there’s no confusion.

3. Completion Notification

Once all FTMO requirements are met, the indicator closes all open positions and displays a celebratory message on your chart, letting you know you’ve successfully completed the challenge.

4. Easy-to-Read Table

A table on your chart provides an overview of each rule, your target, current performance, and whether you’re meeting each goal. The table adjusts its color scheme based on your chart settings for optimal visibility.

5. Dynamic Position Sizing

Integrated ATR-based position sizing helps you manage risk and avoid large drawdowns, ensuring each trade aligns with FTMO’s risk management principles.

Daveatt

Prometheus Fractal WaveThe Fractal Wave is an indicator that uses a fractal analysis to determine where reversals may happen. This is done through a Fractal process, making sure a price point is in a certain set and then getting a Distance metric.

Calculation:

A bullish Fractal is defined by the current bar’s high being less than the last bar’s high, and the last bar’s high being greater than the second to last bar’s high, and the last bar’s high being greater than the third to last bar’s high.

A bearish Fractal is defined by the current low being greater than the last bar’s low, and the last bar’s low being less than the second to last bar’s low, and the last bar’s low being less than the third to last bar’s low.

When there is that bullish or bearish fractal the value we store is either the last bar’s high or low respective to bullish or bearish fractal.

Once we have that value stored we either subtract the last bar’s low from the bullish Fractal value, and subtract the last bar’s high from the bearish Fractal value. Those are our Distances.

Code:

isBullishFractal() =>

high > high and high < high and high > high

isBearishFractal() =>

low < low and low > low and low < low

var float lastBullishFractal = na

var float lastBearishFractal = na

if isBullishFractal() and barstate.isconfirmed

lastBullishFractal := high

if isBearishFractal() and barstate.isconfirmed

lastBearishFractal := low

//------------------------------

//-------CACLULATION------------

//------------------------------

bullWaveDistance = na(lastBullishFractal) ? na : lastBullishFractal - low

bearWaveDistance = na(lastBearishFractal) ? na : high - lastBearishFractal

We then plot the bullish distance and the negative bearish distance.

The trade scenarios come from when one breaks the zero line and then goes back above or below. So if the last bullish distance was below 0 and is now above, or if the last negative bearish distance was above 0 and now below. We plot a green label below a candle for a bullish scenario, or a red label above a candle for a bearish one, you can turn them on or off.

Code:

plot(bullWaveDistance, color=color.green, title="Bull Wave Distance", linewidth=2)

plot(-bearWaveDistance, color=color.red, title="Bear Wave Distance", linewidth=2)

plot(0, "Zero Line", color=color.gray, display = display.pane)

bearish_reversal = plot_labels ? bullWaveDistance < 0 and bullWaveDistance > 0 : na

bullish_reversal = plot_labels ? -bearWaveDistance > 0 and -bearWaveDistance < 0 : na

plotshape(bullish_reversal, location=location.belowbar, color=color.green, style=shape.labelup, title="Bullish Fractal", text="↑", display = display.all - display.status_line, force_overlay = true)

plotshape(bearish_reversal, location=location.abovebar, color=color.red, style=shape.labeldown, title="Bearish Fractal", text="↓", display = display.all - display.status_line, force_overlay = true)

We can see in this daily NASDAQ:QQQ chart that the indicator gives us marks that can either be used as Reversal signals or as breathers in the trend.

Since it is designed to provide reversals, on something like Gold where the uptrend has been strong, the signals may be just short breathers, not full blown strong reversal signs.

The indicator works just as well intra day as it does on larger timeframes.

We encourage traders to not follow indicators blindly, none are 100% accurate. Please comment on any desired updates, all criticism is welcome!

PRINT_TYPELibrary "PRINT_TYPE"

Inputs

Inputs objects

Fields:

inbalance_percent (series int) : percentage coefficient to determine the Imbalance of price levels

stacked_input (series int) : minimum number of consecutive Imbalance levels required to draw extended lines

show_summary_footprint (series bool)

procent_volume_area (series int) : definition size Value area

new_imbalance_cond (series bool) : bool input for setup alert on new imbalance buy and sell

new_imbalance_line_cond (series bool) : bool input for setup alert on new imbalance line buy and sell

stop_past_imbalance_line_cond (series bool) : bool input for setup alert on stop past imbalance line buy and sell

Constants

Constants all Constants objects

Fields:

imbalance_high_char (series string) : char for printing buy imbalance

imbalance_low_char (series string) : char for printing sell imbalance

color_title_sell (series color) : color for footprint sell

color_title_buy (series color) : color for footprint buy

color_line_sell (series color) : color for sell line

color_line_buy (series color) : color for buy line

color_title_none (series color) : color None

Calculation_data

Calculation_data data for calculating

Fields:

detail_open (array) : array open from calculation timeframe

detail_high (array) : array high from calculation timeframe

detail_low (array) : array low from calculation timeframe

detail_close (array) : array close from calculation timeframe

detail_vol (array) : array volume from calculation timeframe

previos_detail_close (array) : array close from calculation timeframe

isBuyVolume (series bool) : attribute previosly bar buy or sell

Footprint_row

Footprint_row objects one footprint row

Fields:

price (series float) : row price

buy_vol (series float) : buy volume

sell_vol (series float) : sell volume

imbalance_buy (series bool) : attribute buy inbalance

imbalance_sell (series bool) : attribute sell imbalance

buy_vol_box (series box) : for ptinting buy volume

sell_vol_box (series box) : for printing sell volume

buy_vp_box (series box) : for ptinting volume profile buy

sell_vp_box (series box) : for ptinting volume profile sell

row_line (series label) : for ptinting row price

empty (series bool) : = true attribute row with zero volume buy and zero volume sell

Imbalance_line_var_object

Imbalance_line_var_object var objects printing and calculation imbalance line

Fields:

cum_buy_line (array) : line array for saving all history buy imbalance line

cum_sell_line (array) : line array for saving all history sell imbalance line

Imbalance_line

Imbalance_line objects printing and calculation imbalance line

Fields:

buy_price_line (array) : float array for saving buy imbalance price level

sell_price_line (array) : float array for saving sell imbalance price level

var_imba_line (Imbalance_line_var_object) : var objects this type

Footprint_bar

Footprint_bar all objects one bar with footprint

Fields:

foot_rows (array) : objects one row footprint

imba_line (Imbalance_line) : objects imbalance line

row_size (series float) : size rows

total_vol (series float) : total volume one footprint bar

foot_buy_vol (series float) : buy volume one footprint bar

foot_sell_vol (series float) : sell volume one footprint bar

foot_max_price_vol (map) : map with one value - price row with max volume buy + sell

calc_data (Calculation_data) : objects with detail data from calculation resolution

Support_objects

Support_objects support object for footprint calculation

Fields:

consts (Constants) : all consts objects

inp (Inputs) : all input objects

bar_index_show_condition (series bool) : calculation bool value for show all objects footprint

row_line_color (series color) : calculation value - color for row price

dop_info (series string)

show_table_cond (series bool)

Mean Reversion Cloud (Ornstein-Uhlenbeck) // AlgoFyreThe Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator detects mean-reversion opportunities by applying the Ornstein-Uhlenbeck process. It calculates a dynamic mean using an Exponential Weighted Moving Average, surrounded by volatility bands, signaling potential buy/sell points when prices deviate.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Adaptive Mean Calculation

🔸Volatility-Based Cloud

🔸Speed of Reversion (θ)

🔶 FUNCTIONALITY

🔸Dynamic Mean and Volatility Bands

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Visualization via Table and Plotshapes

🞘 Table Overview

🞘 Plotshapes Explanation

🞘 Code extract

🔶 INSTRUCTIONS

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

🞘 Understanding What to Look For on the Chart

🞘 Possible Entry Signals

🞘 Possible Take Profit Strategies

🞘 Possible Stop-Loss Levels

🞘 Additional Tips

🔸Customize settings

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) is a unique indicator that applies the Ornstein-Uhlenbeck stochastic process to identify mean-reverting behavior in asset prices. Unlike traditional moving average-based indicators, this model uses an Exponentially Weighted Moving Average (EWMA) to calculate the long-term mean, dynamically adjusting to recent price movements while still considering all historical data. It also incorporates volatility bands, providing a "cloud" that visually highlights overbought or oversold conditions. By calculating the speed of mean reversion (θ) through the autocorrelation of log returns, this indicator offers traders a more nuanced and mathematically robust tool for identifying mean-reversion opportunities. These innovations make it especially useful for markets that exhibit range-bound characteristics, offering timely buy and sell signals based on statistical deviations from the mean.

🔸Adaptive Mean Calculation Traditional MA indicators use fixed lengths, which can lead to lagging signals or over-sensitivity in volatile markets. The Mean Reversion Cloud uses an Exponentially Weighted Moving Average (EWMA), which adapts to price movements by dynamically adjusting its calculation, offering a more responsive mean.

🔸Volatility-Based Cloud Unlike simple moving averages that only plot a single line, the Mean Reversion Cloud surrounds the dynamic mean with volatility bands. These bands, based on standard deviations, provide traders with a visual cue of when prices are statistically likely to revert, highlighting potential reversal zones.

🔸Speed of Reversion (θ) The indicator goes beyond price averages by calculating the speed at which the price reverts to the mean (θ), using the autocorrelation of log returns. This gives traders an additional tool for estimating the likelihood and timing of mean reversion, making the signals more reliable in practice.

🔶 FUNCTIONALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator is designed to detect potential mean-reversion opportunities in asset prices by applying the Ornstein-Uhlenbeck stochastic process. It calculates a dynamic mean through the Exponentially Weighted Moving Average (EWMA) and plots volatility bands based on the standard deviation of the asset's price over a specified period. These bands create a "cloud" that represents expected price fluctuations, helping traders to identify overbought or oversold conditions. By calculating the speed of reversion (θ) from the autocorrelation of log returns, the indicator offers a more refined way of assessing how quickly prices may revert to the mean. Additionally, the inclusion of volatility provides a comprehensive view of market conditions, allowing for more accurate buy and sell signals.

Let's dive into the details:

🔸Dynamic Mean and Volatility Bands The dynamic mean (μ) is calculated using the EWMA, giving more weight to recent prices but considering all historical data. This process closely resembles the Ornstein-Uhlenbeck (OU) process, which models the tendency of a stochastic variable (such as price) to revert to its mean over time. Volatility bands are plotted around the mean using standard deviation, forming the "cloud" that signals overbought or oversold conditions. The cloud adapts dynamically to price fluctuations and market volatility, making it a versatile tool for mean-reversion strategies. 🞘 How it works Step one: Calculate the dynamic mean (μ) The Ornstein-Uhlenbeck process describes how a variable, such as an asset's price, tends to revert to a long-term mean while subject to random fluctuations. In this indicator, the EWMA is used to compute the dynamic mean (μ), mimicking the mean-reverting behavior of the OU process. Use the EWMA formula to compute a weighted mean that adjusts to recent price movements. Assign exponentially decreasing weights to older data while giving more emphasis to current prices. Step two: Plot volatility bands Calculate the standard deviation of the price over a user-defined period to determine market volatility. Position the upper and lower bands around the mean by adding and subtracting a multiple of the standard deviation. 🞘 How to calculate Exponential Weighted Moving Average (EWMA)

The EWMA dynamically adjusts to recent price movements:

mu_t = lambda * mu_{t-1} + (1 - lambda) * P_t

Where mu_t is the mean at time t, lambda is the decay factor, and P_t is the price at time t. The higher the decay factor, the more weight is given to recent data.

Autocorrelation (ρ) and Standard Deviation (σ)

To measure mean reversion speed and volatility: rho = correlation(log(close), log(close ), length) Where rho is the autocorrelation of log returns over a specified period.

To calculate volatility:

sigma = stdev(close, length)

Where sigma is the standard deviation of the asset's closing price over a specified length.

Upper and Lower Bands

The upper and lower bands are calculated as follows:

upper_band = mu + (threshold * sigma)

lower_band = mu - (threshold * sigma)

Where threshold is a multiplier for the standard deviation, usually set to 2. These bands represent the range within which the price is expected to fluctuate, based on current volatility and the mean.

🞘 Code extract // Calculate Returns

returns = math.log(close / close )

// Calculate Long-Term Mean (μ) using EWMA over the entire dataset

var float ewma_mu = na // Initialize ewma_mu as 'na'

ewma_mu := na(ewma_mu ) ? close : decay_factor * ewma_mu + (1 - decay_factor) * close

mu = ewma_mu

// Calculate Autocorrelation at Lag 1

rho1 = ta.correlation(returns, returns , corr_length)

// Ensure rho1 is within valid range to avoid errors

rho1 := na(rho1) or rho1 <= 0 ? 0.0001 : rho1

// Calculate Speed of Mean Reversion (θ)

theta = -math.log(rho1)

// Calculate Volatility (σ)

sigma = ta.stdev(close, corr_length)

// Calculate Upper and Lower Bands

upper_band = mu + threshold * sigma

lower_band = mu - threshold * sigma

🔸Visualization via Table and Plotshapes

The table shows key statistics such as the current value of the dynamic mean (μ), the number of times the price has crossed the upper or lower bands, and the consecutive number of bars that the price has remained in an overbought or oversold state.

Plotshapes (diamonds) are used to signal buy and sell opportunities. A green diamond below the price suggests a buy signal when the price crosses below the lower band, and a red diamond above the price indicates a sell signal when the price crosses above the upper band.

The table and plotshapes provide a comprehensive visualization, combining both statistical and actionable information to aid decision-making.

🞘 Code extract // Reset consecutive_bars when price crosses the mean

var consecutive_bars = 0

if (close < mu and close >= mu) or (close > mu and close <= mu)

consecutive_bars := 0

else if math.abs(deviation) > 0

consecutive_bars := math.min(consecutive_bars + 1, dev_length)

transparency = math.max(0, math.min(100, 100 - (consecutive_bars * 100 / dev_length)))

🔶 INSTRUCTIONS

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator can be set up by adding it to your TradingView chart and configuring parameters such as the decay factor, autocorrelation length, and volatility threshold to suit current market conditions. Look for price crossovers and deviations from the calculated mean for potential entry signals. Use the upper and lower bands as dynamic support/resistance levels for setting take profit and stop-loss orders. Combining this indicator with additional trend-following or momentum-based indicators can improve signal accuracy. Adjust settings for better mean-reversion detection and risk management.

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

Adding the Indicator to the Chart:

Go to your TradingView chart.

Click on the "Indicators" button at the top.

Search for "Mean Reversion Cloud (Ornstein-Uhlenbeck)" in the indicators list.

Click on the indicator to add it to your chart.

Configuring the Indicator:

Open the indicator settings by clicking on the gear icon next to its name on the chart.

Decay Factor: Adjust the decay factor (λ) to control the responsiveness of the mean calculation. A higher value prioritizes recent data.

Autocorrelation Length: Set the autocorrelation length (θ) for calculating the speed of mean reversion. Longer lengths consider more historical data.

Threshold: Define the number of standard deviations for the upper and lower bands to determine how far price must deviate to trigger a signal.

Chart Setup:

Select the appropriate timeframe (e.g., 1-hour, daily) based on your trading strategy.

Consider using other indicators such as RSI or MACD to confirm buy and sell signals.

🞘 Understanding What to Look For on the Chart

Indicator Behavior:

Observe how the price interacts with the dynamic mean and volatility bands. The price staying within the bands suggests mean-reverting behavior, while crossing the bands signals potential entry points.

The indicator calculates overbought/oversold conditions based on deviation from the mean, highlighted by color-coded cloud areas on the chart.

Crossovers and Deviation:

Look for crossovers between the price and the mean (μ) or the bands. A bullish crossover occurs when the price crosses below the lower band, signaling a potential buying opportunity.

A bearish crossover occurs when the price crosses above the upper band, suggesting a potential sell signal.

Deviations from the mean indicate market extremes. A large deviation indicates that the price is far from the mean, suggesting a potential reversal.

Slope and Direction:

Pay attention to the slope of the mean (μ). A rising slope suggests bullish market conditions, while a declining slope signals a bearish market.

The steepness of the slope can indicate the strength of the mean-reversion trend.

🞘 Possible Entry Signals

Bullish Entry:

Crossover Entry: Enter a long position when the price crosses below the lower band with a positive deviation from the mean.

Confirmation Entry: Use additional indicators like RSI (above 50) or increasing volume to confirm the bullish signal.

Bearish Entry:

Crossover Entry: Enter a short position when the price crosses above the upper band with a negative deviation from the mean.

Confirmation Entry: Look for RSI (below 50) or decreasing volume to confirm the bearish signal.

Deviation Confirmation:

Enter trades when the deviation from the mean is significant, indicating that the price has strayed far from its expected value and is likely to revert.

🞘 Possible Take Profit Strategies

Static Take Profit Levels:

Set predefined take profit levels based on historical volatility, using the upper and lower bands as guides.

Place take profit orders near recent support/resistance levels, ensuring you're capitalizing on the mean-reversion behavior.

Trailing Stop Loss:

Use a trailing stop based on a percentage of the price deviation from the mean to lock in profits as the trend progresses.

Adjust the trailing stop dynamically along the calculated bands to protect profits as the price returns to the mean.

Deviation-Based Exits:

Exit when the deviation from the mean starts to decrease, signaling that the price is returning to its equilibrium.

🞘 Possible Stop-Loss Levels

Initial Stop Loss:

Place an initial stop loss outside the lower band (for long positions) or above the upper band (for short positions) to protect against excessive deviations.

Use a volatility-based buffer to avoid getting stopped out during normal price fluctuations.

Dynamic Stop Loss:

Move the stop loss closer to the mean as the price converges back towards equilibrium, reducing risk.

Adjust the stop loss dynamically along the bands to account for sudden market movements.

🞘 Additional Tips

Combine with Other Indicators:

Enhance your strategy by combining the Mean Reversion Cloud with momentum indicators like MACD, RSI, or Bollinger Bands to confirm market conditions.

Backtesting and Practice:

Backtest the indicator on historical data to understand how it performs in various market environments.

Practice using the indicator on a demo account before implementing it in live trading.

Market Awareness:

Keep an eye on market news and events that might cause extreme price movements. The indicator reacts to price data and might not account for news-driven events that can cause large deviations.

🔸Customize settings 🞘 Decay Factor (λ): Defines the weight assigned to recent price data in the calculation of the mean. A value closer to 1 places more emphasis on recent prices, while lower values create a smoother, more lagging mean.

🞘 Autocorrelation Length (θ): Sets the period for calculating the speed of mean reversion and volatility. Longer lengths capture more historical data, providing smoother calculations, while shorter lengths make the indicator more responsive.

🞘 Threshold (σ): Specifies the number of standard deviations used to create the upper and lower bands. Higher thresholds widen the bands, producing fewer signals, while lower thresholds tighten the bands for more frequent signals.

🞘 Max Gradient Length (γ): Determines the maximum number of consecutive bars for calculating the deviation gradient. This setting impacts the transparency of the plotted bands based on the length of deviation from the mean.

🔶 CONCLUSION

The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator offers a sophisticated approach to identifying mean-reversion opportunities by applying the Ornstein-Uhlenbeck stochastic process. This dynamic indicator calculates a responsive mean using an Exponentially Weighted Moving Average (EWMA) and plots volatility-based bands to highlight overbought and oversold conditions. By incorporating advanced statistical measures like autocorrelation and standard deviation, traders can better assess market extremes and potential reversals. The indicator’s ability to adapt to price behavior makes it a versatile tool for traders focused on both short-term price deviations and longer-term mean-reversion strategies. With its unique blend of statistical rigor and visual clarity, the Mean Reversion Cloud provides an invaluable tool for understanding and capitalizing on market inefficiencies.

Realized Price Oscillator [InvestorUnknown]Overview

The Realized Price Oscillator is a fundamental analysis tool designed to assess Bitcoin's price dynamics relative to its realized price. The indicator calculates various metrics using data from the realized market capitalization and total supply. It applies normalization techniques to scale values within a specified range, helping investors identify overbought or oversold conditions over the long time horizon. The oscillator also features DCA-based signals to assist in strategic market entry and exit.

Key Features

1. Normalization and Scaling:

The indicator scales values using a limit that can be adjusted for decimal precision (Limit). It allows for both positive and negative values, providing flexibility in analysis.

Decay functionality is included to progressively reduce the extreme values over time, ensuring recent data impacts the oscillator more than older data.

f_rescale(float value, float min, float max, float limit, bool negatives) =>

((limit * (negatives ? 2 : 1)) * (value - min) / (max - min)) - (negatives ? limit : 0)

2. Realized Price Oscillator Calculation:

Realized Price Oscillator is computed using logarithmic differences between the open, high, low, and close prices and the realized price. This helps in identifying how the current market price compares with the average cost basis of the Bitcoin supply.

f_realized_price_oscillator(float realized_price) =>

rpo_o = math.log(open / realized_price)

rpo_h = math.log(high / realized_price)

rpo_l = math.log(low / realized_price)

rpo_c = math.log(close / realized_price)

3. Oscillator Normalization:

The normalized oscillator calculates the range between the maximum and minimum values over time. It adjusts the oscillator values based on these bounds, considering a decay factor. This normalized range assists in consistent signal generation.

normalized_oscillator(float x, float b) =>

float oscillator = b

var float min = na

var float max = na

if (oscillator > max or na(max)) and time >= normalization_start_date

max := oscillator

if (min > oscillator or na(min)) and time >= normalization_start_date

min := oscillator

if time >= normalization_start_date

max := max * decay

min := min * decay

normalized_oscillator = f_rescale(x, min, max, lim, neg)

4. Dollar-Cost Averaging (DCA) Signals:

DCA-based signals are generated using user-defined thresholds (DCA IN and DCA OUT). The oscillator triggers buy signals when the normalized low value falls below the DCA IN threshold and sell signals when the normalized high value exceeds the DCA OUT threshold.

5. Visual Representation:

The indicator plots candlestick representations of the normalized Realized Price Oscillator values (open, high, low, close) over time, starting from a specified date (plot_start_date).

Colors are dynamically adjusted using a gradient to represent the state of the oscillator, ranging from green (buy zone) to red (sell zone). Background and bar colors also change based on DCA conditions.

How It Works

Data Sourcing: Realized price data is sourced using Bitcoin’s realized market cap (BTC_MARKETCAPREAL) and total supply (BTC_SUPPLY).

Realized Price Oscillator Metrics: Logarithmic differences between price and realized price are computed to generate Realized Price Oscillator values for open, high, low, and close.

Normalization: The indicator rescales the oscillator values based on a defined limit, adjusting for negative values if allowed. It employs a decay factor to reduce the influence of historical extremes.

Conclusion

The Realized Price Oscillator is a sophisticated tool that combines market price analysis with realized price metrics to offer a robust framework for understanding Bitcoin's valuation. By leveraging normalization techniques and DCA thresholds, it provides actionable insights for long-term investing strategies.

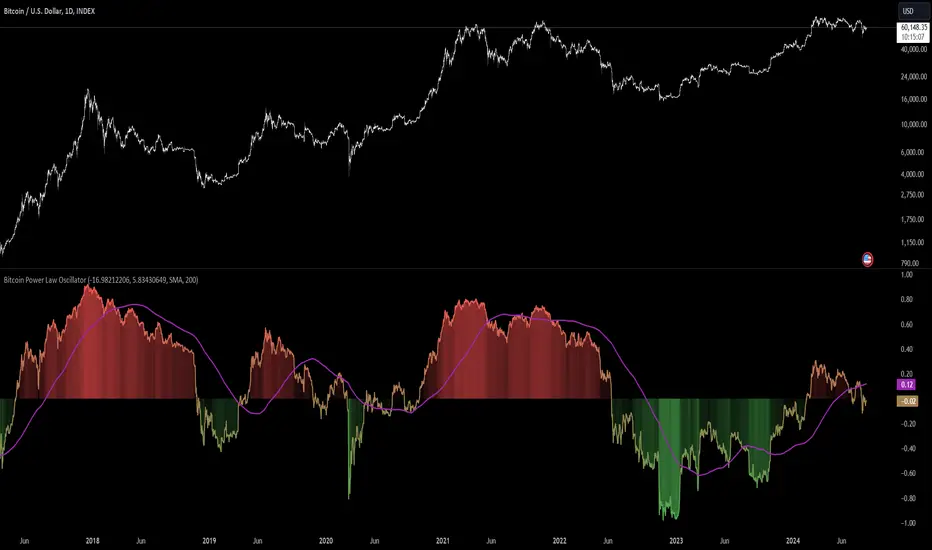

Bitcoin Power Law Oscillator [InvestorUnknown]The Bitcoin Power Law Oscillator is a specialized tool designed for long-term mean-reversion analysis of Bitcoin's price relative to a theoretical midline derived from the Bitcoin Power Law model (made by capriole_charles). This oscillator helps investors identify whether Bitcoin is currently overbought, oversold, or near its fair value according to this mathematical model.

Key Features:

Power Law Model Integration: The oscillator is based on the midline of the Bitcoin Power Law, which is calculated using regression coefficients (A and B) applied to the logarithm of the number of days since Bitcoin’s inception. This midline represents a theoretical fair value for Bitcoin over time.

Midline Distance Calculation: The distance between Bitcoin’s current price and the Power Law midline is computed as a percentage, indicating how far above or below the price is from this theoretical value.

float a = input.float (-16.98212206, 'Regression Coef. A', group = "Power Law Settings")

float b = input.float (5.83430649, 'Regression Coef. B', group = "Power Law Settings")

normalization_start_date = timestamp(2011,1,1)

calculation_start_date = time == timestamp(2010, 7, 19, 0, 0) // First BLX Bitcoin Date

int days_since = request.security('BNC:BLX', 'D', ta.barssince(calculation_start_date))

bar() =>

= request.security('BNC:BLX', 'D', bar())

int offset = 564 // days between 2009/1/1 and "calculation_start_date"

int days = days_since + offset

float e = a + b * math.log10(days)

float y = math.pow(10, e)

float midline_distance = math.round((y / btc_close - 1.0) * 100)

Oscillator Normalization: The raw distance is converted into a normalized oscillator, which fluctuates between -1 and 1. This normalization adjusts the oscillator to account for historical extremes, making it easier to compare current conditions with past market behavior.

float oscillator = -midline_distance

var float min = na

var float max = na

if (oscillator > max or na(max)) and time >= normalization_start_date

max := oscillator

if (min > oscillator or na(min)) and time >= normalization_start_date

min := oscillator

rescale(float value, float min, float max) =>

(2 * (value - min) / (max - min)) - 1

normalized_oscillator = rescale(oscillator, min, max)

Overbought/Oversold Identification: The oscillator provides a clear visual representation, where values near 1 suggest Bitcoin is overbought, and values near -1 indicate it is oversold. This can help identify potential reversal points or areas of significant market imbalance.

Optional Moving Average: Users can overlay a moving average (either SMA or EMA) on the oscillator to smooth out short-term fluctuations and focus on longer-term trends. This is particularly useful for confirming trend reversals or persistent overbought/oversold conditions.

This indicator is particularly useful for long-term Bitcoin investors who wish to gauge the market's mean-reversion tendencies based on a well-established theoretical model. By focusing on the Power Law’s midline, users can gain insights into whether Bitcoin’s current price deviates significantly from what historical trends would suggest as a fair value.

Adaptive Trend Classification: Moving Averages [InvestorUnknown]Adaptive Trend Classification: Moving Averages

Overview

The Adaptive Trend Classification (ATC) Moving Averages indicator is a robust and adaptable investing tool designed to provide dynamic signals based on various types of moving averages and their lengths. This indicator incorporates multiple layers of adaptability to enhance its effectiveness in various market conditions.

Key Features

Adaptability of Moving Average Types and Lengths: The indicator utilizes different types of moving averages (EMA, HMA, WMA, DEMA, LSMA, KAMA) with customizable lengths to adjust to market conditions.

Dynamic Weighting Based on Performance: ] Weights are assigned to each moving average based on the equity they generate, with considerations for a cutout period and decay rate to manage (reduce) the influence of past performances.

Exponential Growth Adjustment: The influence of recent performance is enhanced through an adjustable exponential growth factor, ensuring that more recent data has a greater impact on the signal.

Calibration Mode: Allows users to fine-tune the indicator settings for specific signal periods and backtesting, ensuring optimized performance.

Visualization Options: Multiple customization options for plotting moving averages, color bars, and signal arrows, enhancing the clarity of the visual output.

Alerts: Configurable alert settings to notify users based on specific moving average crossovers or the average signal.

User Inputs

Adaptability Settings

λ (Lambda): Specifies the growth rate for exponential growth calculations.

Decay (%): Determines the rate of depreciation applied to the equity over time.

CutOut Period: Sets the period after which equity calculations start, allowing for a focus on specific time ranges.

Robustness Lengths: Defines the range of robustness for equity calculation with options for Narrow, Medium, or Wide adjustments.

Long/Short Threshold: Sets thresholds for long and short signals.

Calculation Source: The data source used for calculations (e.g., close price).

Moving Averages Settings

Lengths and Weights: Allows customization of lengths and initial weights for each moving average type (EMA, HMA, WMA, DEMA, LSMA, KAMA).

Calibration Mode

Calibration Mode: Enables calibration for fine-tuning inputs.

Calibrate: Specifies which moving average type to calibrate.

Strategy View: Shifts entries and exits by one bar for non-repainting backtesting.

Calculation Logic

Rate of Change (R): Calculates the rate of change in the price.

Set of Moving Averages: Generates multiple moving averages with different lengths for each type.

diflen(length) =>

int L1 = na, int L_1 = na

int L2 = na, int L_2 = na

int L3 = na, int L_3 = na

int L4 = na, int L_4 = na

if robustness == "Narrow"

L1 := length + 1, L_1 := length - 1

L2 := length + 2, L_2 := length - 2

L3 := length + 3, L_3 := length - 3

L4 := length + 4, L_4 := length - 4

else if robustness == "Medium"

L1 := length + 1, L_1 := length - 1

L2 := length + 2, L_2 := length - 2

L3 := length + 4, L_3 := length - 4

L4 := length + 6, L_4 := length - 6

else

L1 := length + 1, L_1 := length - 1

L2 := length + 3, L_2 := length - 3

L3 := length + 5, L_3 := length - 5

L4 := length + 7, L_4 := length - 7

// Function to calculate different types of moving averages

ma_calculation(source, length, ma_type) =>

if ma_type == "EMA"

ta.ema(source, length)

else if ma_type == "HMA"

ta.sma(source, length)

else if ma_type == "WMA"

ta.wma(source, length)

else if ma_type == "DEMA"

ta.dema(source, length)

else if ma_type == "LSMA"

lsma(source,length)

else if ma_type == "KAMA"

kama(source, length)

else

na

// Function to create a set of moving averages with different lengths

SetOfMovingAverages(length, source, ma_type) =>

= diflen(length)

MA = ma_calculation(source, length, ma_type)

MA1 = ma_calculation(source, L1, ma_type)

MA2 = ma_calculation(source, L2, ma_type)

MA3 = ma_calculation(source, L3, ma_type)

MA4 = ma_calculation(source, L4, ma_type)

MA_1 = ma_calculation(source, L_1, ma_type)

MA_2 = ma_calculation(source, L_2, ma_type)

MA_3 = ma_calculation(source, L_3, ma_type)

MA_4 = ma_calculation(source, L_4, ma_type)

Exponential Growth Factor: Computes an exponential growth factor based on the current bar index and growth rate.

// The function `e(L)` calculates an exponential growth factor based on the current bar index and a given growth rate `L`.

e(L) =>

// Calculate the number of bars elapsed.

// If the `bar_index` is 0 (i.e., the very first bar), set `bars` to 1 to avoid division by zero.

bars = bar_index == 0 ? 1 : bar_index

// Define the cuttime time using the `cutout` parameter, which specifies how many bars will be cut out off the time series.

cuttime = time

// Initialize the exponential growth factor `x` to 1.0.

x = 1.0

// Check if `cuttime` is not `na` and the current time is greater than or equal to `cuttime`.

if not na(cuttime) and time >= cuttime

// Use the mathematical constant `e` raised to the power of `L * (bar_index - cutout)`.

// This represents exponential growth over the number of bars since the `cutout`.

x := math.pow(math.e, L * (bar_index - cutout))

x

Equity Calculation: Calculates the equity based on starting equity, signals, and the rate of change, incorporating a natural decay rate.

pine code

// This function calculates the equity based on the starting equity, signals, and rate of change (R).

eq(starting_equity, sig, R) =>

cuttime = time

if not na(cuttime) and time >= cuttime

// Calculate the rate of return `r` by multiplying the rate of change `R` with the exponential growth factor `e(La)`.

r = R * e(La)

// Calculate the depreciation factor `d` as 1 minus the depreciation rate `De`.

d = 1 - De

var float a = 0.0

// If the previous signal `sig ` is positive, set `a` to `r`.

if (sig > 0)

a := r

// If the previous signal `sig ` is negative, set `a` to `-r`.

else if (sig < 0)

a := -r

// Declare the variable `e` to store equity and initialize it to `na`.

var float e = na

// If `e ` (the previous equity value) is not available (first calculation):

if na(e )

e := starting_equity

else

// Update `e` based on the previous equity value, depreciation factor `d`, and adjustment factor `a`.

e := (e * d) * (1 + a)

// Ensure `e` does not drop below 0.25.

if (e < 0.25)

e := 0.25

e

else

na

Signal Generation: Generates signals based on crossovers and computes a weighted signal from multiple moving averages.

Main Calculations

The indicator calculates different moving averages (EMA, HMA, WMA, DEMA, LSMA, KAMA) and their respective signals, applies exponential growth and decay factors to compute equities, and then derives a final signal by averaging weighted signals from all moving averages.

Visualization and Alerts

The final signal, along with additional visual aids like color bars and arrows, is plotted on the chart. Users can also set up alerts based on specific conditions to receive notifications for potential trading opportunities.

Repainting

The indicator does support intra-bar changes of signal but will not repaint once the bar is closed, if you want to get alerts only for signals after bar close, turn on “Strategy View” while setting up the alert.

Conclusion

The Adaptive Trend Classification: Moving Averages Indicator is a sophisticated tool for investors, offering extensive customization and adaptability to changing market conditions. By integrating multiple moving averages and leveraging dynamic weighting based on performance, it aims to provide reliable and timely investing signals.

Cosine Kernel Regressions [QuantraSystems]Cosine Kernel Regressions

Introduction

The Cosine Kernel Regressions indicator (CKR) uses mathematical concepts to offer a unique approach to market analysis. This indicator employs Kernel Regressions using bespoke tunable Cosine functions in order to smoothly interpret a variety of market data, providing traders with incredibly clean insights into market trends.

The CKR is particularly useful for traders looking to understand underlying trends without the 'noise' typical in raw price movements. It can serve as a standalone trend analysis tool or be combined with other indicators for more robust trading strategies.

Legend

Fast Trend Signal Line - This is the foreground oscillator, it is colored upon the earliest confirmation of a change in trend direction.

Slow Trend Signal Line - This oscillator is calculated in a similar manner. However, it utilizes a lower frequency within the cosine tuning function, allowing it to capture longer and broader trends in one signal. This allows for tactical trading; the user can trade smaller moves without losing sight of the broader trend.

Case Study

In this case study, the CKR was used alongside the Triple Confirmation Kernel Regression Oscillator (KRO)

Initially, the KRO indicated an oversold condition, which could be interpreted as a signal to enter a long position in anticipation of a price rebound. However, the CKR’s fast trend signal line had not yet confirmed a positive trend direction - suggesting that entering a trade too early and without confirmation could be a mistake.

Waiting for a confirmed positive trend from the CKR proved beneficial for this trade. A few candles after the oversold signal, the CKR's fast trend signal line shifted upwards, indicating a strong upward momentum. This was the optimal entry point suggested by the CKR, occurring after the confirmation of the trend change, which significantly reduced the likelihood of entering during a false recovery or continuation of the downtrend.

This is one of the many uses of the CKR - by timing entries using the fast signal line , traders could avoid unnecessary losses by preventing premature entries.

Methodology

The methodology behind CKR is a multi-layered approach and utilizes many ‘base’ indicators.

Relative Strength Index

Stochastic Oscillator

Bollinger Band Percent

Chande Momentum Oscillator

Commodity Channel Index

Fisher Transform

Volume Zone Oscillator

The calculated output from each indicator is standardized and scaled before being averaged. This prevents any single indicator from overpowering the resulting signal.

// ╔════════════════════════════════╗ //

// ║ Scaling/Range Adjustment ║ //

// ╚════════════════════════════════╝ //

RSI_ReScale (_res ) => ( _res - 50 ) * 2.8

STOCH_ReScale (_stoch ) => ( _stoch - 50 ) * 2

BBPCT_ReScale (_bbpct ) => ( _bbpct - 0.5 ) * 120

CMO_ReScale (_chandeMO ) => ( _chandeMO * 1.15 )

CCI_ReScale (_cci ) => ( _cci / 2 )

FISH_ReScale (_fish1 ) => ( _fish1 * 30 )

VZO_ReScale (_VP, _TV ) => (_VP / _TV) * 110

These outputs are then fed into a customized cosine kernel regression function, which smooths the data, and combines all inputs into a single coherent output.

// ╔════════════════════════════════╗ //

// ║ COSINE KERNEL REGRESSIONS ║ //

// ╚════════════════════════════════╝ //

// Define a function to compute the cosine of an input scaled by a frequency tuner

cosine(x, z) =>

// Where x = source input

// y = function output

// z = frequency tuner

var y = 0.

y := math.cos(z * x)

Y

// Define a kernel that utilizes the cosine function

kernel(x, z) =>

var y = 0.

y := cosine(x, z)

math.abs(x) <= math.pi/(2 * z) ? math.abs(y) : 0. // cos(zx) = 0

// The above restricts the wave to positive values // when x = π / 2z

The tuning of the regression is adjustable, allowing users to fine-tune the sensitivity and responsiveness of the indicator to match specific trading strategies or market conditions. This robust methodology ensures that CKR provides a reliable and adaptable tool for market analysis.

Pine Script Chart ViewerDisplay your custom charts exported from anywhere in TradingView.

Put your candles on candles :

var Candle candles = array.from(...)

For instance:

var Candle candles = array.from(Candle.new(2.0, 4.0, 1.0, 3.0), Candle.new(3.0, 5.0, 2.0, 4.0))

Candle details:

Candle.new(open_1, high_1, low_1, close_1)

Price Cross Time Custom Range Interactive█ OVERVIEW

This indicator was a time-based indicator and intended as educational purpose only based on pine script v5 functions for ta.cross() , ta.crossover() and ta.crossunder() .

I realised that there is some overlap price with the cross functions, hence I integrate them into Custom Range Interactive with value variance and overlap displayed into table.

This was my submission for Pinefest #1 , I decided to share this as public, I may accidentally delete this as long as i keep as private.

█ INSPIRATION

Inspired by design, code and usage of CAGR. Basic usage of custom range / interactive, pretty much explained here . Credits to TradingView.

█ FEATURES

1. Custom Range Interactive

2. Label can be resize and change color.

3. Label show tooltip for price and time.

4. Label can be offset to improve readability.

5. Table can show price variance when any cross is true.

6. Table can show overlap if found crosss is overlap either with crossover and crossunder.

7. Table text color automatically change based on chart background (light / dark mode).

8. Source 2 is drawn as straight line, while Source 1 will draw as label either above line for crossover, below line for crossunder and marked 'X' if crossing with Source 2's line.

9. Cross 'X' label can be offset to improve readability.

10. Both Source 1 and Source 2 can select Open, Close, High and Low, which can be displayed into table.

█ LIMITATIONS

1. Table is limited to intraday timeframe only as time format is not accurate for daily timeframe and above. Example daily timeframe will give result less 1 day from actual date.

2. I did not include other sources such external source or any built in sources such as hl2, hlc3, ohlc4 and hlcc4.

█ CODE EXPLAINATION

I pretty much create custom function with method which returns tuple value.

method crossVariant(float price = na, chart.point ref = na) =>

cross = ta.cross( price, ref.price)

over = ta.crossover( price, ref.price)

under = ta.crossunder(price, ref.price)

Unfortunately, I unable make the labels into array which i plan to return string value by getting the text value from array label, hence i use label.all and add incremental int value as reference.

series label labelCross = na, labelCross.delete()

var int num = 0

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

I realised cross value can be overlap with crossover and crossunder, hence I add bool to enable force overlap and add additional bools.

series label labelCross = na, labelCross.delete()

var int num = 0

if forceOverlap

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

else

if cross and over

num += 1

labelCross := label.new()

if cross and under

num += 1

labelCross := label.new()

if cross and not over and not under

num += 1

labelCross := label.new()

█ USAGE / EXAMPLES

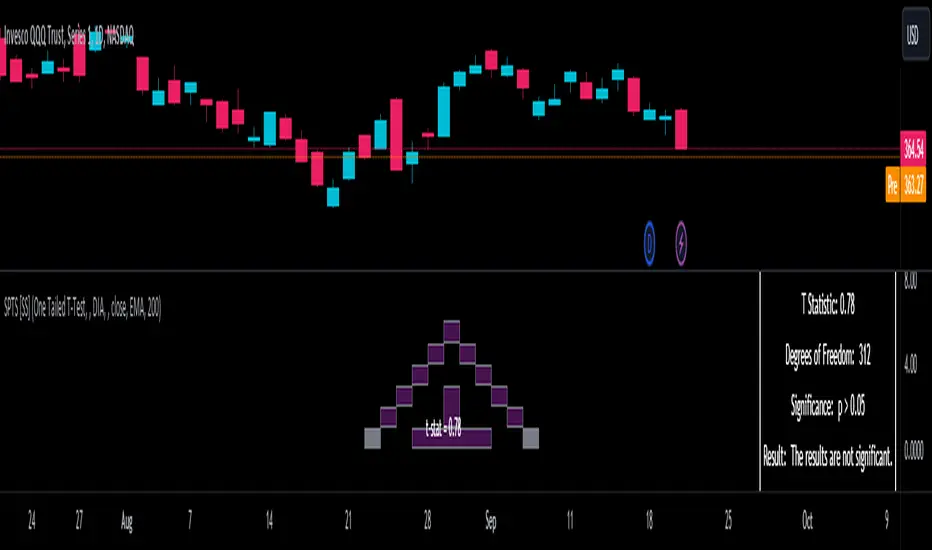

Statistical Package for the Trading Sciences [SS]

This is SPTS.

It stands for Statistical Package for the Trading Sciences.

Its a play on SPSS (Statistical Package for the Social Sciences) by IBM (software that, prior to Pinescript, I would use on a daily basis for trading).

Let's preface this indicator first:

This isn't so much an indicator as it is a project. A passion project really.

This has been in the works for months and I still feel like its incomplete. But the plan here is to continue to add functionality to it and actually have the Pinecoding and Tradingview community contribute to it.

As a math based trader, I relied on Excel, SPSS and R constantly to plan my trades. Since learning a functional amount of Pinescript and coding a lot of what I do and what I relied on SPSS, Excel and R for, I use it perhaps maybe a few times a week.

This indicator, or package, has some of the key things I used Excel and SPSS for on a daily and weekly basis. This also adds a lot of, I would say, fairly complex math functionality to Pinescript. Because this is adding functionality not necessarily native to Pinescript, I have placed most, if not all, of the functionality into actual exportable functions. I have also set it up as a kind of library, with explanations and tips on how other coders can take these functions and implement them into other scripts.

The hope here is that other coders will take it, build upon it, improve it and hopefully share additional functionality that can be added into this package. Hence why I call it a project. Okay, let's get into an overview:

Current Functions of SPTS:

SPTS currently has the following functionality (further explanations will be offered below):

Ability to Perform a One-Tailed, Two-Tailed and Paired Sample T-Test, with corresponding P value.

Standard Pearson Correlation (with functionality to be able to calculate the Pearson Correlation between 2 arrays).

Quadratic (or Curvlinear) correlation assessments.

R squared Assessments.

Standard Linear Regression.

Multiple Regression of 2 independent variables.

Tests of Normality (with Kurtosis and Skewness) and recognition of up to 7 Different Distributions.

ARIMA Modeller (Sort of, more details below)

Okay, so let's go over each of them!

T-Tests

So traditionally, most correlation assessments on Pinescript are done with a generic Pearson Correlation using the "ta.correlation" argument. However, this is not always the best test to be used for correlations and determine effects. One approach to correlation assessments used frequently in economics is the T-Test assessment.

The t-test is a statistical hypothesis test used to determine if there is a significant difference between the means of two groups. It assesses whether the sample means are likely to have come from populations with the same mean. The test produces a t-statistic, which is then compared to a critical value from the t-distribution to determine statistical significance. Lower p-values indicate stronger evidence against the null hypothesis of equal means.

A significant t-test result, indicating the rejection of the null hypothesis, suggests that there is statistical evidence to support that there is a significant difference between the means of the two groups being compared. In practical terms, it means that the observed difference in sample means is unlikely to have occurred by random chance alone. Researchers typically interpret this as evidence that there is a real, meaningful difference between the groups being studied.

Some uses of the T-Test in finance include:

Risk Assessment: The t-test can be used to compare the risk profiles of different financial assets or portfolios. It helps investors assess whether the differences in returns or volatility are statistically significant.

Pairs Trading: Traders often apply the t-test when engaging in pairs trading, a strategy that involves trading two correlated securities. It helps determine when the price spread between the two assets is statistically significant and may revert to the mean.

Volatility Analysis: Traders and risk managers use t-tests to compare the volatility of different assets or portfolios, assessing whether one is significantly more or less volatile than another.

Market Efficiency Tests: Financial researchers use t-tests to test the Efficient Market Hypothesis by assessing whether stock price movements follow a random walk or if there are statistically significant deviations from it.

Value at Risk (VaR) Calculation: Risk managers use t-tests to calculate VaR, a measure of potential losses in a portfolio. It helps assess whether a portfolio's value is likely to fall below a certain threshold.

There are many other applications, but these are a few of the highlights. SPTS permits 3 different types of T-Test analyses, these being the One Tailed T-Test (if you want to test a single direction), two tailed T-Test (if you are unsure of which direction is significant) and a paired sample t-test.

Which T is the Right T?

Generally, a one-tailed t-test is used to determine if a sample mean is significantly greater than or less than a specified population mean, whereas a two-tailed t-test assesses if the sample mean is significantly different (either greater or less) from the population mean. In contrast, a paired sample t-test compares two sets of paired observations (e.g., before and after treatment) to assess if there's a significant difference in their means, typically used when the data points in each pair are related or dependent.

So which do you use? Well, it depends on what you want to know. As a general rule a one tailed t-test is sufficient and will help you pinpoint directionality of the relationship (that one ticker or economic indicator has a significant affect on another in a linear way).

A two tailed is more broad and looks for significance in either direction.

A paired sample t-test usually looks at identical groups to see if one group has a statistically different outcome. This is usually used in clinical trials to compare treatment interventions in identical groups. It's use in finance is somewhat limited, but it is invaluable when you want to compare equities that track the same thing (for example SPX vs SPY vs ES1!) or you want to test a hypothesis about an index and a leveraged share (for example, the relationship between FNGU and, say, MSFT or NVDA).

Statistical Significance

In general, with a t-test you would need to reference a T-Table to determine the statistical significance of the degree of Freedom and the T-Statistic.

However, because I wanted Pinescript to full fledge replace SPSS and Excel, I went ahead and threw the T-Table into an array, so that Pinescript can make the determination itself of the actual P value for a t-test, no cross referencing required :-).

Left tail (Significant):

Both tails (Significant):

Distributed throughout (insignificant):

As you can see in the images above, the t-test will also display a bell-curve analysis of where the significance falls (left tail, both tails or insignificant, distributed throughout).

That said, I have not included this function for the paired sample t-test because that is a bit more nuanced. But for the one and two tailed assessments, the indicator will provide you the P value.

Pearson Correlation Assessment

I don't think I need to go into too much detail on this one.

I have put in functionality to quickly calculate the Pearson Correlation of two array's, which is not currently possible with the "ta.correlation" function.

Quadratic (Curvlinear) Correlation

Not everything in life is linear, sometimes things are curved!

The Pearson Correlation is great for linear assessments, but tends to under-estimate the degree of the relationship in curved relationships. There currently is no native function to t-test for quadratic/curvlinear relationships, so I went ahead and created one.

You can see an example of how Quadratic and Pearson Correlations vary when you look at CME_MINI:ES1! against AMEX:DIA for the past 10 ish months:

Pearson Correlation:

Quadratic Correlation:

One or the other is not always the best, so it is important to check both!

R-Squared Assessments:

The R-squared value, or the square of the Pearson correlation coefficient (r), is used to measure the proportion of variance in one variable that can be explained by the linear relationship with another variable. It represents the goodness-of-fit of a linear regression model with a single predictor variable.

R-Squared is offered in 3 separate forms within this indicator. First, there is the generic R squared which is taking the square root of a Pearson Correlation assessment to assess the variance.

The next is the R-Squared which is calculated from an actual linear regression model done within the indicator.

The first is the R-Squared which is calculated from a multiple regression model done within the indicator.

Regardless of which R-Squared value you are using, the meaning is the same. R-Square assesses the variance between the variables under assessment and can offer an insight into the goodness of fit and the ability of the model to account for the degree of variance.

Here is the R Squared assessment of the SPX against the US Money Supply:

Standard Linear Regression

The indicator contains the ability to do a standard linear regression model. You can convert one ticker or economic indicator into a stock, ticker or other economic indicator. The indicator will provide you with all of the expected information from a linear regression model, including the coefficients, intercept, error assessments, correlation and R2 value.

Here is AAPL and MSFT as an example:

Multiple Regression

Oh man, this was something I really wanted in Pinescript, and now we have it!

I have created a function for multiple regression, which, if you export the function, will permit you to perform multiple regression on any variables available in Pinescript!

Using this functionality in the indicator, you will need to select 2, dependent variables and a single independent variable.

Here is an example of multiple regression for NASDAQ:AAPL using NASDAQ:MSFT and NASDAQ:NVDA :

And an example of SPX using the US Money Supply (M2) and AMEX:GLD :

Tests of Normality:

Many indicators perform a lot of functions on the assumption of normality, yet there are no indicators that actually test that assumption!

So, I have inputted a function to assess for normality. It uses the Kurtosis and Skewness to determine up to 7 different distribution types and it will explain the implication of the distribution. Here is an example of SP:SPX on the Monthly Perspective since 2010:

And NYSE:BA since the 60s:

And NVDA since 2015:

ARIMA Modeller

Okay, so let me disclose, this isn't a full fledge ARIMA modeller. I took some shortcuts.

True ARIMA modelling would involve decomposing the seasonality from the trend. I omitted this step for simplicity sake. Instead, you can select between using an EMA or SMA based approach, and it will perform an autogressive type analysis on the EMA or SMA.

I have tested it on lookback with results provided by SPSS and this actually works better than SPSS' ARIMA function. So I am actually kind of impressed.

You will need to input your parameters for the ARIMA model, I usually would do a 14, 21 and 50 day EMA of the close price, and it will forecast out that range over the length of the EMA.

So for example, if you select the EMA 50 on the daily, it will plot out the forecast for the next 50 days based on an autoregressive model created on the EMA 50. Here is how it looks on AMEX:SPY :

You can also elect to plot the upper and lower confidence bands:

Closing Remarks

So that is the indicator/package.

I do hope to continue expanding its functionality, but as of now, it does already have quite a lot of functionality.

I really hope you enjoy it and find it helpful. This. Has. Taken. AGES! No joke. Between referencing my old statistics textbooks, trying to remember how to calculate some of these things, and wanting to throw my computer against the wall because of errors in the code, this was a task, that's for sure. So I really hope you find some usefulness in it all and enjoy the ability to be able to do functions that previously could really only be done in external software.

As always, leave your comments, suggestions and feedback below!

Take care!

libHTF[without request.security()]Library "libHTF"

libHTF: use HTF values without request.security()

This library enables to use HTF candles without request.security().

Basic data structure

Using to access values in the same manner as series variable.

The last member of HTF array is always latest current TF's data.

If new bar in HTF(same as last bar closes), new member is pushed to HTF array.

2nd from the last member of HTF array is latest fixed(closed) bar.

HTF: How to use

1. set TF

tf_higher() function selects higher TF. TF steps are ("1","5","15","60","240","D","W","M","3M","6M","Y").

example:

tfChart = timeframe.period

htf1 = tf_higher(tfChart)

2. set HTF matrix

htf_candle() function returns 1 bool and 1 matrix.

bool is a flag for start of new candle in HTF context.

matrix is HTF candle data(0:open,1:time_open,2:close,3:time_close,4:high,5:time:high,6:low,7:time_low).

example:

=htf_candle(htf1)

3. how to access HTF candle data

you can get values using .lastx() method.