Fear & Greed Oscillator — LEAPs (v6, manual DMI/ADX)Fear & Greed Oscillator for LEAPs — a composite sentiment/trend tool that highlights long-term fear/greed extremes and trend quality for better LEAP entries and exits.

This custom Fear & Greed Oscillator (FGO-LEAP) is designed for swing trades and long-term LEAP option entries. It blends multiple signals — MACD (trend), ADX/DMI (trend quality), OBV (accumulation/distribution), RSI & Stoch RSI (momentum), and volume spikes — into a single score that ranges from –100 (extreme fear) to +100 (extreme greed). The weights are tuned for LEAPs, emphasizing slower trend and accumulation signals rather than short-term noise.

Use Weekly charts for the main signal and Daily only for entry timing. Entries are strongest when the score is above zero and rising, with both MACD and DMI positive. Extreme Fear (< –60) can mark long-term bottoms when followed by a recovery, while Extreme Greed (> +60) often signals overheated conditions. A cross below zero is an early warning to reduce or roll positions.

Поиск скриптов по запросу "accumulation"

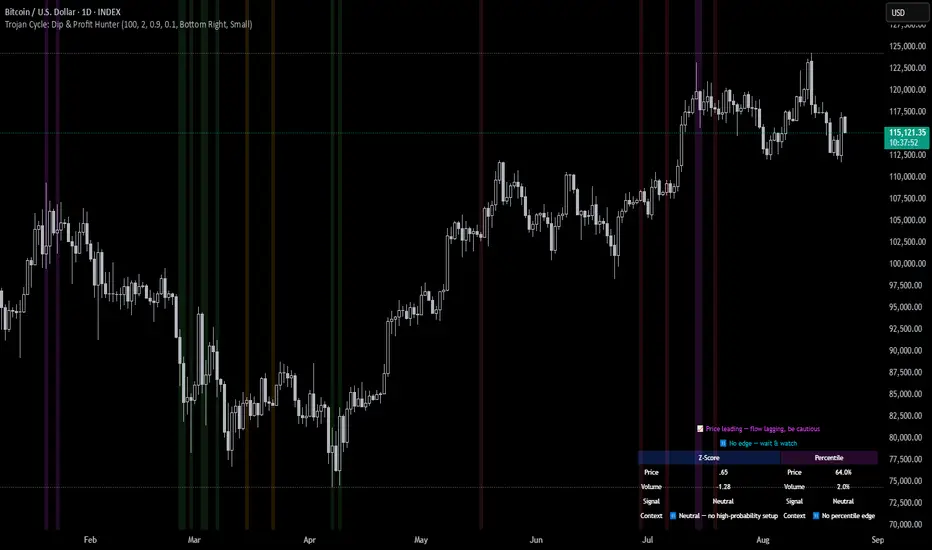

Trojan Cycle: Dip & Profit Hunter📉 Crypto is changing. Your signals should too.

This script doesn’t try to outguess price — it helps you track capital rotation and flow behavior in alignment with the evolving macro structure of the digital asset market.

Trojan Cycle: Dip & Profit Hunter is a signal engine built to support and validate the capital rotation models outlined in the Trojan Cycle and Synthetic Rotation theses — available via RWCS_LTD’s published charts

It is not a classic “buy low, sell high” tool. It is a structural filter that uses price/volume statistics to surface accumulation zones, synthetic traps, and macro context shifts — all aligned with the institutionalization of crypto post-2024.

🧠 Purpose & Value

Crypto no longer follows the retail-led, halving-driven pattern of 2017 or 2021.

Instead, institutional infrastructure, regulatory filters, and equity-market Trojan horses define the new path of capital.

This tool helps you visualize that path by interpreting behavior through statistical imbalances and real-time momentum signals.

Use it to:

Track where capital is accumulating or exiting

Identify signals consistent with true cycle rotation (vs. synthetic traps)

Validate your macro view with real-time statistical context

🔍 How It Works

The engine combines four signal layers:

1. Z-Score Logic

- Measures how far price and volume have deviated from their mean

- Detects dips, blowoffs, and exhaustion zones

2. Percentile Logic

- Compares current price and volume to historical rank distribution

- Flags statistically rare conditions (e.g. bottom 10% price, top 90% volume)

3. Combined Context Engine

- Integrates both models to generate one of 36 unique output states

- Each state provides a labeled market context (e.g., 🟢 Confluent Buy, 🔴 Confluent Sell, 🧨 Synthetic Trap )

4. Momentum Spread & Divergence

- Measures whether price is leading volume (trap risk) or volume is leading price (accumulation)

- Outputs intuitive momentum context with emoji-coded alerts

📋 What You See

🧠 Contextual Table UI with key Z-Scores, percentiles, signals, and market commentary

🎯 Emoji-coded signals to quickly grasp high-probability setups or risk zones

🌊 Optional overlays: price/volume divergence, momentum spread

🎨 Visual table customization (size, position) and chart highlights for signal clarity

🔔 Alert System

✅ Single dynamic alert using alert() that only fires when signal context changes

Prevents alert fatigue and allows clean webhook/automation integration

🧭 Use Cases

For macro cycle traders: Track where we are in the Trojan Cycle using statistical context

For thesis explorers: Use the 36-output signal map to match against your rotation thesis

For capital rotation watchers: Identify structural setups consistent with ETF-driven or compliance-filtered flow

For narrative skeptics: Avoid synthetic altseason traps where volume lags or flow dries up

🧪 Suggested Pairing for Thesis Validation

To use this tool as part of a thesis-confirmation framework , pair it with:

BTC.D — Bitcoin Dominance

ETH/BTC — Ethereum strength vs. Bitcoin

TOTALE100/ETH — Altcoin strength relative to ETH

RWCS_LTD’s published charts and macro cycle models

🏁 Final Note

Crypto has matured. So should your signals.

This tool doesn’t try to game the next 2 candles. It helps you understand the current phase in a compliance-filtered, institutionalized rotation model.

It’s not built for hype — it’s built for conviction.

Explore the thesis → Validate the structure → Trade with clarity.

🚨 Disclaimer

This script is not financial advice. It is an analytical tool designed to support market structure research and rotation thesis validation. Use this as part of a broader framework including technical structure, dominance charts, and macro data.

T-Virus Sentiment [hapharmonic]🧬 T-Virus Sentiment: Visualize the Market's DNA

Remember the iconic T-Virus vial from the first Resident Evil? That powerful, swirling helix of potential has always fascinated me. It sparked an idea: what if we could visualize the market's underlying health in a similar way? What if we could capture the "genetic code" of market sentiment and contain it within a dynamic, 3D indicator? This project is the result of that idea, brought to life with Pine Script.

The indicator's main goal is to measure the strength and direction of market sentiment by analyzing the "genetic code" of price action through a variety of trusted indicators. The result is displayed as a liquid level within a DNA helix, a bubble density representing buying pressure, and a T-Virus mascot that reflects the overall mood.

🧐 Core Concept: How It Works

The primary output of the indicator is the "Active %" gauge you see on the right side of the vial. This percentage represents the overall sentiment score, calculated as an average from 7 different technical analysis tools. Each tool is analyzed on every bar and assigned a score from 1 (strong bearish pressure) to 5 (strong bullish potential).

In this indicator, we re-imagine market dynamics through the lens of a viral outbreak. A strong bear market is like a virus taking hold, pulling all technical signals down into a state of weakness. Conversely, a powerful bull market is like an antiviral serum ; positive signals rise and spread toward the top of the vial, indicating that the system is being injected with strength.

This is not just another line on a chart. It's a comprehensive sentiment dashboard designed to give an immediate, at-a-glance understanding of the confluence between 7 classic technical indicators. The incredible 3D model of the vial itself was inspired by a design concept found here .

⚛️ The 4 Core Elements of T-Virus Sentiment

These four elements work in harmony to give a complete, multi-faceted picture of market sentiment. Each component tells a different part of the story.

The Virus Mascot: An instant emotional cue. This character provides the quickest possible read on the overall market mood, combining sentiment with volume pressure.

The Antiviral Serum Level: The main quantitative output. This is the liquid level in the DNA helix and the percentage gauge on the right, representing the average sentiment score from all 7 indicators.

Buy Pressure & Bubble Density: This visualizes volume flow. The density of bubbles represents the intensity of accumulation (buying) versus distribution (selling). It's the "power" behind the move.

The Signal Distribution: This shows the confluence (or dispersion) of sentiment. Are all signals bullish and clustered at the top, or are they scattered, indicating a conflicted market? The position of the indicator labels is crucial, as each is assigned to one of five distinct zones:

Base Bottom: The market is at its weakest. Signals here suggest strong bearish control and distribution.

Lower Zone: The market is still bearish, but signals may be showing early signs of accumulation or bottoming.

Neutral Core (Center): A state of balance or sideways consolidation. The market is waiting for a new direction.

Upper Zone: Bullish momentum is becoming clear. Signals are strengthening and showing bullish control.

Top Cap: The market is "heating up" with strong bullish sentiment, potentially nearing overbought conditions.

🐂🐻 The Virus Mascot: The At-a-Glance Indicator

This character acts as a shortcut to confirm market health. It combines the sentiment score with volume, preventing false confidence in a low-volume rally.

Its state is determined by a dual-check: the overall "Antiviral Serum Level" and the "Buy Pressure" must both be above 50%.

Green & Smiling: The 'all clear' signal. This means that not only is the overall technical sentiment bullish, but it's also being supported by real buying pressure. This is a sign of a healthy bull market.

Red & Angry: A warning sign. This appears if either the sentiment is weak, or a bullish sentiment is not being confirmed by buying volume. The latter could indicate a potential "bull trap" or an exhaustive move.

This mascot can be disabled from the settings page under "Virus Mascot Styling" if a cleaner look is preferred.

🫧 Bubble Density: Gauging Buy vs. Sell Pressure

The bubbles visualize the battle between buyers and sellers. There are two modes to control how this is calculated:

Mode 1: Visible Range (The 'Big Picture' View)

This default mode is best for getting a broad, contextual understanding of the current session. It dynamically analyzes the volume of every single candlestick currently visible on the screen to calculate the buy/sell pressure ratio. It answers the question: "Over the entire period I'm looking at, who is in control?" As you zoom in or out, the calculation adapts.

Mode 2: Custom Lookback (The 'Precision' View)

This mode is for traders who need to analyze short-term pressure. You can define a fixed number of recent bars to analyze, which is perfect for scalping or understanding the volume dynamics leading into a key level. It answers the question: "What is happening right now ?" In the example above, a lookback of 2 focuses only on the most recent action, clearly showing intense, immediate selling pressure (few bubbles) and a corresponding drop in the sentiment score to 29%.

ℹ️ Interactive Tooltips: Dive Deeper

We believe in transparency, not 'black box' indicators. This feature transforms the indicator from a visual aid into an active learning tool.

Simply hover the mouse over any indicator label (like EMA, OBV, etc.) to get a detailed tooltip. It will explain the specific data points and thresholds that signal met to be placed in its current zone. This helps build trust in the signals and allows users to fine-tune the indicator settings to better match their own trading style.

🎯 The Scoring Logic Breakdown

The "Antiviral Serum Level" gauge is the average score from 7 technical analysis tools. Each is graded on a 5-point scale (1=Strong Bearish to 5=Strong Bullish). Here’s a detailed, transparent look at how each "gene" is evaluated:

Relative Strength Index (RSI)

Measures momentum and overbought/oversold conditions.

Group 1 (Strong Bearish): RSI > 80 (Extreme Overbought)

Group 2 (Bearish): 70 < RSI ≤ 80 (Overbought)

Group 3 (Neutral): 30 ≤ RSI ≤ 70

Group 4 (Bullish): 20 ≤ RSI < 30 (Oversold)

Group 5 (Strong Bullish): RSI < 20 (Extreme Oversold)

Exponential Moving Averages (EMA)

Evaluates the trend's strength and structure based on the alignment of multiple EMAs (9, 21, 50, 100, 200, 250).

Group 1 (Strong Bearish): A perfect bearish sequence (9 < 21 < 50 < ...)

Group 2 (Bearish Transition): Early signs of a potential reversal (e.g., 9 > 21 but still below 50)

Group 3 (Neutral / Mixed): MAs are intertwined or showing a partial bullish sequence.

Group 4 (Bullish): A strong bullish sequence is forming (e.g., 9 > 21 > 50 > 100)

Group 5 (Strong Bullish): A perfect bullish sequence (9 > 21 > 50 > 100 > 200 > 250)

Moving Average Convergence Divergence (MACD)

Analyzes the relationship between two moving averages to gauge momentum.

Group 1 (Strong Bearish): MACD & Histogram are negative and momentum is falling.

Group 2 (Weakening Bearish): MACD is negative but the histogram is rising or positive.

Group 3 (Neutral / Crossover): A crossover event is occurring near the zero line.

Group 4 (Bullish): MACD & Histogram are positive.

Group 5 (Strong Bullish): MACD & Histogram are positive, rising strongly, and accelerating.

Average Directional Index (ADX)

Measures trend strength, not direction. The score is based on both ADX value and the dominance of DI+ vs DI-.

Group 1 (Bearish / No Trend): ADX < 20 and DI- is dominant.

Group 2 (Developing Bearish Trend): 20 ≤ ADX < 25 and DI- is dominant.

Group 3 (Neutral / Indecision): Trend is weak or DI+ and DI- are nearly equal.

Group 4 (Developing Bullish Trend): 25 ≤ ADX ≤ 40 and DI+ is dominant.

Group 5 (Strong Bullish Trend): ADX > 40 and DI+ is dominant.

Ichimoku Cloud (IKH)

A comprehensive indicator that defines support/resistance, momentum, and trend direction.

Group 1 (Strong Bearish): Price is below the Kumo, Tenkan < Kijun, and Chikou is below price.

Group 2 (Bearish): Price is inside or below the Kumo, with mixed secondary signals.

Group 3 (Neutral / Ranging): Price is inside the Kumo, often with a Tenkan/Kijun cross.

Group 4 (Bullish): Price is above the Kumo with strong primary signals.

Group 5 (Strong Bullish): All signals are aligned bullishly: price above Kumo, bullish Tenkan/Kijun cross, bullish future Kumo, and Chikou above price.

Bollinger Bands (BB)

Measures volatility and relative price levels.

Group 1 (Strong Bearish): Price is below the lower band.

Group 2 (Bearish Territory): Price is between the lower band and the basis line.

Group 3 (Neutral): Price is hovering around the basis line.

Group 4 (Bullish Territory): Price is between the basis line and the upper band.

Group 5 (Strong Bullish): Price is above the upper band.

On-Balance Volume (OBV)

Uses volume flow to predict price changes. The score is based on OBV's trend and its position relative to its moving average.

Group 1 (Strong Bearish): OBV is below its MA and falling.

Group 2 (Weakening Bearish): OBV is below its MA but showing signs of rising.

Group 3 (Neutral): OBV is very close to its MA.

Group 4 (Bullish): OBV is above its MA and rising.

Group 5 (Strong Bullish): OBV is above its MA, rising strongly, and showing signs of a volume spike.

🧭 How to Use the T-Virus Sentiment Indicator

IMPORTANT: This indicator is a sentiment dashboard , not a direct buy/sell signal generator. Its strength lies in showing confluence and providing a quick, holistic view of the market's technical health.

Confirmation Tool: Use the "Active %" gauge to confirm a trade setup from your primary strategy. For example, if you see a bullish chart pattern, a high and rising sentiment score can add confidence to your trade.

Momentum & Trend Gauge: A consistently high score (e.g., > 75%) suggests strong, established bullish momentum. A consistently low score (< 25%) suggests strong bearish control. A score hovering around 50% often indicates a ranging or indecisive market.

Divergence & Warning System: Pay attention to divergences. If the price is making new highs but the sentiment score is failing to follow or is actively decreasing, it could be an early warning sign that the underlying momentum is weakening.

⚙️ Settings & Customization

The indicator is highly customizable to fit any trading style.

Position & Anchor: Control where the vial appears on the chart.

Styling (Vial, Helix, etc.): Nearly every visual element can be color-customized.

Signals: This is where the real power is. All underlying indicator parameters (RSI length, MACD settings, etc.) can be fine-tuned to match a personal strategy. The text labels can also be disabled if the chart feels cluttered.

Enjoy visualizing the market's DNA with the T-Virus Sentiment indicator

Smart Bar Coloring: Tight Closes & Volume BreakoutsAdvanced Bar Coloring Indicator for Price Action and Volume Analysis

This sophisticated indicator automatically colors price bars based on two key market conditions: tight closing ranges and significant volume activity, helping traders quickly identify consolidation periods and potential breakout setups.

Key Features:

Tight Close Detection:

ATR-Based Analysis: Uses 14-period ATR to define "tight" price movement

Dual-Bar Confirmation: Requires both current and previous bar to have closing ranges ≤ 20% of ATR

Consolidation Identification: Highlights periods of reduced volatility that often precede significant moves

Customizable Color: Default amber/orange highlighting for easy visual identification

Volume Breakout Detection:

Multi-Criteria Volume Analysis: Triggers when volume exceeds any of three thresholds:

150% of 20-period volume SMA

150% of recent 3-bar average volume

150% of 50-period volume SMA

Price Action Filter: Requires bullish price action (close > previous close OR close in upper 75% of range)

Smart Volume Handling: Automatically detects and works only with instruments that have volume data

Customizable Color: Default teal highlighting for volume-driven moves

Technical Analysis Applications:

Consolidation Patterns: Identify tight trading ranges before potential breakouts

Volume Confirmation: Spot high-volume moves with supportive price action

Entry Timing: Use tight closes to identify potential accumulation zones

Breakout Validation: Volume-colored bars confirm legitimate breakout attempts

Risk Management: Tight closes often indicate lower immediate volatility

How to Use:

Amber/Orange Bars: Indicate tight closing ranges - potential accumulation or consolidation

Teal Bars: Show significant volume with bullish price action - potential breakout confirmation

Normal Bars: Standard market conditions without special highlighting

Pattern Recognition: Look for clusters of tight closes followed by volume breakouts

Technical Requirements:

Works on any timeframe

Automatically adapts to instruments with or without volume data

Compatible with all chart types and drawing tools

XMR Divergences vs KrakenSUMMARY

This script finds the percentage difference between Kraken, and multiple other exchanges, for the price of XMRUSD, and then runs a variable length moving average of those differences. Optionally, you can multiply by the reported volume of the exchange in question. Skip to "USAGE" at the bottom for a quick view of the settings. But I recommend reading DETAILED DESCRIPTION as well.

PURPOSE

The purpose of this script is to get a look into the relative funds flows of XMR between Kraken and the other exchanges. So long as an exchange withdraws are open: 1) Negative divergences indicate XMR outflows from the exchange under consideration, 2) Postive divergences indicate XMR inflows from Kraken to the exchange.

This appears to be moderately correlated with price movements in Monero (but not always). There is also the theory that positive accumulation is a leading indication of a growing probability of postive price action in the general crypto market, and negative accumulation is a leading indicator of an upcoming peak. In other words, exchanges like to accumulate Monero quietly during calm downtimes, and they like to manage its price from gaining too much attention (pump) during broad market positivity.

BACKGROUND

It's well known among XMR traders that most exchanges are operating on a heavy fractional reserve basis as regards Monero. The past 2 years have seen regular and repeated withdraw freezes, sometimes for weeks/months at a time. Occasionally, liquidity stress tests have been performed, with predictable results - none of these exchanges are able to continue supporting withdraws.

Kraken is the only exchange of meaningful volume that has never frozen withdraws for more than an hour or so. Thus, we theorize that Kraken is operating with all, or most of the XMR they claim to have.

Furthermore, we have seen in the past, large price negative price divergences of these fractional reserve exchanges relative to Kraken. As the social outcry grew stronger for this malfeasance, these exchanges have gone to greater lengths to hide their price divergences.

On minute-by-minute ; hour-by-hour basis, typically, a look with the naked eye would show oscillation around the zero point. But when you average it out, especially on lower timeframes (like the 1 and 5 min candles), you can very clearly see that when withdraws are shut down, these exchanges simultaneously diverge their prices downwards as well.

DETAILED DESCRIPTION

The ideal view of price divergence would compare second-by-second prices, and then run something like a rolling 4-hr or 1-day SMA to average out the overall divergences. However, due to limitations of TradingView, this is impractical/impossible for actual usage/viewing. As a result, a balance must be struck, when selecting the combination of the candle period, and the SMA lookback length.

I find that 5min candles, with a 48-period lookback (that equates to a rolling 4-hour SMA), offers the best view of recent and historical price divergence activity. This of course means that we're only sampling price divergences once every 5 minutes, but it still provides a decent look at what's happening. If this script gets popular, I wouldn't be surprised if these exchanges start timing their candle closes to mask their misdeeds, but that's of course speculative on my part.

The other important factor here, *IS TO MULTIPLY BY VOLUME*. Some of these no-volume exchanges have large price divergences. But if they're not doing any real volume, then it doesn't really have any real market impact. Thus, I recommend keeping the "Make volume adjustment" option on.

If that ends up happening, we'll have to infer that by comparing the difference in close prices, vs the difference in the highest or lowest intra-candle prices (wicks). Typically a divergence should have all 3 showing similar results.

Notes regarding "Sum_of_All": This only makes sense when multiplying by volume. So only check this if you also made the volume adjustment. Generally I believe that *Binance* sets the tone. However, we have seen numerous occasions where Binance diverges down, and the others diverge up. I believe this is a social influence tactic, since most people look at Binance price. Meanwhile, they're trying to accumulate some small amount on the other exchanges to minimize their overall loss. This of course assumes collusion by these exchanges, which is a high likely hood, seeing as how in May 2021, they all diverged together simultaneously (among other evidence).

USAGE

I recommend using your browser zoom, to see data beyond 1 month in the past.

Lookback - The number of candles over which to conduct a moving average. On 5-min candles for example, here's how the math works out:

12 - Equates to a 1 hr MA

24 - 2 hrs

48 - 4 hrs (default)

288 - 1 day

2880 - 10 days

Make Volume Adjustment - Recommend that you usually keep this on.

Line Widths - Set to preference

Show_Close_Price? - You can compute the difference at candle close. Or you can check the other boxes to compare the highest/lowest prices for intra candle prices (wicks).

Show Sum_of_All? - You can sum all of the differences, which only makes sense if you're making the volume adjustement. Default is off. Below, you can also choose which exchanges to include in the sum.

This works best on lower timeframes, like the 1m, 5, and 15m charts. I personally use 5m, with 48 or 96 length lookback. You get a better view of the real time price divergences that way.

Volume Profile Grid [Alpha Extract]A sophisticated volume distribution analysis system that transforms market activity into institutional-grade visual profiles, revealing hidden support/resistance zones and market participant behavior. Utilizing advanced price level segmentation, bullish/bearish volume separation, and dynamic range analysis, the Volume Profile Grid delivers comprehensive market structure insights with Point of Control (POC) identification, Value Area boundaries, and volume delta analysis. The system features intelligent visualization modes, real-time sentiment analysis, and flexible range selection to provide traders with clear, actionable volume-based market context.

🔶 Dynamic Range Analysis Engine

Implements dual-mode range selection with visible chart analysis and fixed period lookback, automatically adjusting to current market view or analyzing specified historical periods. The system intelligently calculates optimal bar counts while maintaining performance through configurable maximum limits, ensuring responsive profile generation across all timeframes with institutional-grade precision.

// Dynamic period calculation with intelligent caching

get_analysis_period() =>

if i_use_visible_range

chart_start_time = chart.left_visible_bar_time

current_time = last_bar_time

time_span = current_time - chart_start_time

tf_seconds = timeframe.in_seconds()

estimated_bars = time_span / (tf_seconds * 1000)

range_bars = math.floor(estimated_bars)

final_bars = math.min(range_bars, i_max_visible_bars)

math.max(final_bars, 50) // Minimum threshold

else

math.max(i_periods, 50)

🔶 Advanced Bull/Bear Volume Separation

Employs sophisticated candle classification algorithms to separate bullish and bearish volume at each price level, with weighted distribution based on bar intersection ratios. The system analyzes open/close relationships to determine volume direction, applying proportional allocation for doji patterns and ensuring accurate representation of buying versus selling pressure across the entire price spectrum.

🔶 Multi-Mode Volume Visualization

Features three distinct display modes for bull/bear volume representation: Split mode creates mirrored profiles from a central axis, Side by Side mode displays sequential bull/bear segments, and Stacked mode separates volumes vertically. Each mode offers unique insights into market participant behavior with customizable width, thickness, and color parameters for optimal visual clarity.

// Bull/Bear volume calculation with weighted distribution

for bar_offset = 0 to actual_periods - 1

bar_high = high

bar_low = low

bar_volume = volume

// Calculate intersection weight

weight = math.min(bar_high, next_level) - math.max(bar_low, current_level)

weight := weight / (bar_high - bar_low)

weighted_volume = bar_volume * weight

// Classify volume direction

if bar_close > bar_open

level_bull_volume += weighted_volume

else if bar_close < bar_open

level_bear_volume += weighted_volume

else // Doji handling

level_bull_volume += weighted_volume * 0.5

level_bear_volume += weighted_volume * 0.5

🔶 Point of Control & Value Area Detection

Implements institutional-standard POC identification by locating the price level with maximum volume accumulation, providing critical support/resistance zones. The Value Area calculation uses sophisticated sorting algorithms to identify the price range containing 70% of trading volume, revealing the market's accepted value zone where institutional participants concentrate their activity.

🔶 Volume Delta Analysis System

Incorporates real-time volume delta calculation with configurable dominance thresholds to identify significant bull/bear imbalances. The system visually highlights price levels where buying or selling pressure exceeds threshold percentages, providing immediate insight into directional volume flow and potential reversal zones through color-coded delta indicators.

// Value Area calculation using 70% volume accumulation

total_volume_sum = array.sum(total_volumes)

target_volume = total_volume_sum * 0.70

// Sort volumes to find highest activity zones

for i = 0 to array.size(sorted_volumes) - 2

for j = i + 1 to array.size(sorted_volumes) - 1

if array.get(sorted_volumes, j) > array.get(sorted_volumes, i)

// Swap and track indices for value area boundaries

// Accumulate until 70% threshold reached

for i = 0 to array.size(sorted_indices) - 1

accumulated_volume += vol

array.push(va_levels, array.get(volume_levels, idx))

if accumulated_volume >= target_volume

break

❓How It Works

🔶 Weighted Volume Distribution

Implements proportional volume allocation based on the percentage of each bar that intersects with price levels. When a bar spans multiple levels, volume is distributed proportionally based on the intersection ratio, ensuring precise representation of trading activity across the entire price spectrum without double-counting or volume loss.

🔶 Real-Time Profile Generation

Profiles regenerate on each bar close when in visible range mode, automatically adapting to chart zoom and scroll actions. The system maintains optimal performance through intelligent caching mechanisms and selective line updates, ensuring smooth operation even with maximum resolution settings and extended analysis periods.

🔶 Market Sentiment Analysis

Features comprehensive volume analysis table displaying total volume metrics, bullish/bearish percentages, and overall market sentiment classification. The system calculates volume dominance ratios in real-time, providing immediate insight into whether buyers or sellers control the current price structure with percentage-based sentiment thresholds.

🔶 Visual Profile Mapping

Provides multi-layered visual feedback through colored volume bars, POC line highlighting, Value Area boundaries, and optional delta indicators. The system supports profile mirroring for alternative perspectives, line extension for future reference, and customizable label positioning with detailed price information at critical levels.

Why Choose Volume Profile Grid

The Volume Profile Grid represents the evolution of volume analysis tools, combining traditional volume profile concepts with modern visualization techniques and intelligent analysis algorithms. By integrating dynamic range selection, sophisticated bull/bear separation, and multi-mode visualization with POC/Value Area detection, it provides traders with institutional-quality market structure analysis that adapts to any trading style. The comprehensive delta analysis and sentiment monitoring system eliminates guesswork while the flexible visualization options ensure optimal clarity across all market conditions, making it an essential tool for traders seeking to understand true market dynamics through volume-based price discovery.

Smart Money Proxy IndexOverview

The Smart Money Proxy Index (SMPI) is an educational tool that attempts to identify potential institutional-style behavior patterns using publicly available market data. This comprehensive tool combines multiple institutional analysis techniques into a single, easy-to-read 0-100 oscillator.

Important Disclaimer

This is an educational proxy indicator that analyzes volume and price patterns. It cannot identify actual institutional trading activity and should not be interpreted as tracking real "smart money." Use for educational purposes and combine with other analysis methods.

Inspiration & Methodology

This indicator is inspired by MAPsignals' Big Money Index (BMI) methodology but uses publicly available price and volume data with original calculations. This is an independent educational interpretation designed to teach smart money concepts to retail traders.

What It Analyzes

SMPI tracks potential "smart money" activity by combining:

Block Trading Detection - Identifies unusual volume surges with significant price impact

Money Flow Analysis - Volume-weighted price pressure using Money Flow Index

Accumulation/Distribution Patterns - Modified On-Balance Volume signals

Institutional Control Proxy - End-of-day positioning and control analysis

Key Features

– Multi-Component Analysis - Combines 4 different institutional detection methods

– BMI-Style 0-100 Scale - Familiar oscillator range with clear extreme levels

– Professional Visualization - Dynamic colors, gradient fills, and clean data table

– Comprehensive Alerts - Buy/sell signals plus divergence detection

– Fully Customizable - Adjust all parameters, colors, and display options

– Non-Repainting Signals - All alerts use confirmed data for reliability

– Educational Focus - Designed to teach institutional flow concepts

How to Interpret

Above 80: Potential smart money distribution phase (bearish pressure)

Below 20: Potential smart money accumulation phase (bullish opportunity)

Signal Generation: Buy signals when crossing above 20, sell signals when crossing below 80

Divergences: Price vs SMPI divergences can signal potential trend changes

Volume Confirmation: Higher volume ratios strengthen signal reliability

Best Practices

Timeframes: Works best on higher timeframes for institutional behavior analysis

Confirmation: Combine with other technical analysis tools and market context

Volume: Pay attention to volume confirmation in the data table

Context: Consider overall market conditions and fundamental factors

Risk Management: Not recommended as standalone trading system

Customizable Parameters

Block Volume Threshold: Sensitivity for unusual volume detection (default: 2.5x average)

SMPI Smoothing Period: Index calculation smoothing (default: 25 bars)

Extreme Levels: Overbought/oversold thresholds (default: 80/20)

Money Flow Length: MFI calculation period (default: 14)

Visual Options: Colors, signals, and display preferences

Available Alerts

Buy Signal: SMPI crosses above oversold level (20)

Sell Signal: SMPI crosses below overbought level (80)

Extreme Levels: Alerts when reaching overbought/oversold zones

Divergence Detection: Bullish and bearish price vs SMPI divergences

Educational Purpose & Limitations

This indicator is designed as an educational proxy for understanding institutional flow concepts. It analyzes publicly available price and volume data to identify potential smart money behavior patterns.

Cannot access actual institutional transaction data

Signals may be slower than day-trading indicators (intentionally designed for institutional timeframes)

Should be used in conjunction with other analysis methods

Past performance does not guarantee future results

What Makes This Different

Unlike simple volume or momentum indicators, SMPI combines multiple institutional analysis techniques into one comprehensive tool. The multi-component approach provides a more robust view of potential smart money activity.

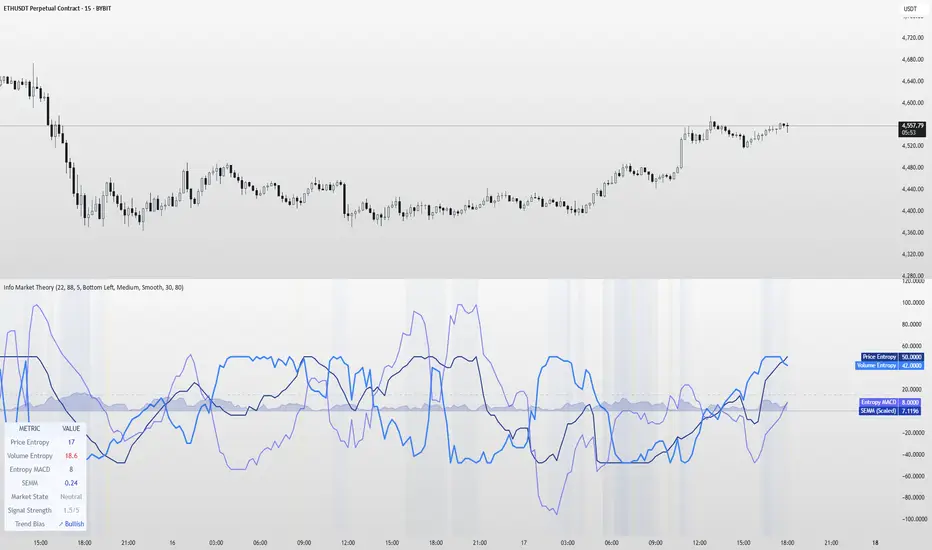

Information Theory Market AnalysisINFORMATION THEORY MARKET ANALYSIS

OVERVIEW

This indicator applies mathematical concepts from information theory to analyze market behavior, measuring the randomness and predictability of price and volume movements through entropy calculations. Unlike traditional technical indicators, it provides insight into market structure and regime changes.

KEY COMPONENTS

Four Main Signals:

• Price Entropy (Deep Blue): Measures randomness in price movements

• Volume Entropy (Bright Blue): Analyzes volume pattern predictability

• Entropy MACD (Purple): Shows relationship between price and volume entropy

• SEMM (Royal Blue): Stochastic Entropy Market Monitor - overall market randomness gauge

Market State Detection:

The indicator identifies seven distinct market states:

• Strong Trending (SEMM < 0.1)

• Weak Trending (0.1-0.2)

• Neutral (0.2-0.3)

• Moderate Random (0.3-0.5)

• High Randomness (0.5-0.8)

• Very Random (0.8-1.0)

• Chaotic (>1.0)

KEY FEATURES

Advanced Analytics:

• Signal Strength Confluence: 0-5 scale measuring alignment of multiple factors

• Entropy Crossovers: Detects shifts between accumulation and distribution phases

• Extreme Readings: Identifies statistical outliers for potential reversals

• Trend Bias Analysis: Directional momentum assessment

Information Dashboard:

• Real-time entropy values and market state

• Signal strength indicator with visual highlighting

• Trend bias with directional arrows

• Color-coded alerts for extreme conditions

Customizable Display:

• Adjustable SEMM scaling (5x to 100x) for optimal visibility

• Multiple line styles: Smooth, Stepped, Dotted

• 9 table positions with 3 size options

• Professional blue color scheme with transparency controls

Comprehensive Alert System - 15 Alert Types Including:

• Extreme entropy readings (price/volume)

• Crossover signals (dominance shifts)

• Market state changes (trending ↔ random)

• High confluence signals (3+ factors aligned)

HOW TO USE

Reading the Signals:

• Entropy Values > ±25: Strong structural signals

• Entropy Values > ±40: Extreme readings, potential reversals

• SEMM < 0.2: Trending market favors directional strategies

• SEMM > 0.5: Random market favors range/scalping strategies

Signal Confluence:

Look for multiple factors aligning:

• Signal Strength ≥ 3.0 for higher probability setups

• Background highlighting indicates confluence

• Table shows real-time strength assessment

Timeframe Optimization:

• Short-term (1m-15m): Entropy Length 14-22, Sensitivity 3-5

• Swing Trading (1H-4H): Default settings optimal

• Position Trading (Daily+): Entropy Length 34-55, Sensitivity 8-12

EDUCATIONAL APPLICATIONS

Market Structure Analysis:

• Understand when markets are trending vs. ranging

• Identify accumulation and distribution phases

• Recognize extreme market conditions

• Measure information content in price movements

Information Theory Concepts:

• Binary entropy calculations applied to financial data

• Probability distribution analysis of returns

• Statistical ranking and percentile analysis

• Momentum-adjusted randomness measurement

TECHNICAL DETAILS

Calculations:

• Uses binary entropy formula: -

• Percentile ranking across multiple timeframes

• Volume-weighted probability distributions

• RSI-adjusted momentum entropy (SEMM)

Customization Options:

• Entropy Length: 5-100 bars (default: 22)

• Average Length: 10-200 bars (default: 88)

• Sensitivity: 1.0-20.0 (default: 5.0, lower = more sensitive)

• SEMM Scaling: 5.0-100.0x (default: 30.0)

IMPORTANT NOTES

Risk Considerations:

• Indicator measures probabilities, not certainties

• High SEMM values (>0.5) suggest increased market randomness

• Extreme readings may persist longer than expected

• Always combine with proper risk management

Educational Purpose:

This indicator is designed for:

• Market structure analysis and education

• Understanding information theory applications in finance

• Developing probabilistic thinking about markets

• Research and analytical purposes

Performance Tips:

• Allow 200+ bars for proper initialization

• Adjust scaling and transparency for optimal visibility

• Use confluence signals for higher probability analysis

• Consider multiple timeframes for comprehensive analysis

DISCLAIMER

This indicator is for educational and analytical purposes. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and consider your risk tolerance before making trading decisions.

Version: 5.0

Category: Oscillators, Volume, Market Structure

Best For: All timeframes, trending and ranging markets

Complexity: Intermediate to Advanced

Volume vs Price Impact Z-ScoreVolume vs Price Impact Z‑Score

This indicator measures how disproportionate the traded volume is relative to the price movement of a candle.

Step 1: Volume-to-Price Impact (VPI)

VPI = Volume / (abs(Close - Open) + ε)

(or optionally using High - Low as the price range)

Step 2: Z‑Score Standardization

Z = (VPI - SMA(VPI, length)) / STDEV(VPI, length)

Interpretation:

Z > 2 → High volume with little price movement → possible absorption (accumulation/distribution).

Z < -2 → Large price move with low volume → weak or illiquid move (potential false breakout).

Use cases:

Detecting accumulation/distribution phases.

Highlighting false breakouts or weak price moves.

Supporting entry/exit decisions based on market efficiency (volume vs. price impact).

تلوين الشموع حسب الحجم (يومي أو متوسط)📊 Indicator Name:

Candle Coloring Based on Volume Change (Flexible Comparison)

🎯 Purpose of the Indicator:

This indicator colors candlesticks based solely on changes in volume, regardless of price direction. It helps traders visualize unusual volume activity and potential accumulation or distribution zones.

It also displays the percentage change in volume above each candle — based on a comparison method chosen by the user.

⚙️ User Inputs:

Comparison Method (Mode):

"Compare with Previous Day":

The volume of the current candle is compared with the volume of the previous candle.

"Compare with Average of N Days":

The volume is compared with a moving average of volume over a number of past days (e.g., 10 days).

Average Length (for mode 2):

Used only when "Compare with Average" is selected.

Defines the number of days over which to calculate the volume average.

Minimum % Change to Show Label:

A threshold that controls when the percentage label appears.

Prevents label clutter for insignificant volume changes.

🎨 Candle Coloring Logic:

Condition Meaning Candle Color

Current volume > reference volume High activity 🟢 Green

Current volume < reference volume Low activity 🔴 Red

Nearly equal volumes Normal ⚪ Gray

🏷️ Volume Change Label:

The indicator displays a percentage change label above the candle.

For example:

If volume increased by 45% → label shows +45.00%.

If the change exceeds ±50%, the label turns yellow to indicate a significant spike.

✅ Key Benefits:

Quickly detects unusual volume activity (e.g., spikes, drops).

Enhances classic price-action analysis with volume context.

Flexible comparison:

Day-to-day for short-term traders.

Moving average for swing and position traders.

Clean, minimalist design with conditional labels.

🔍 Use Case Examples:

🔴 Red candle on price rise → weak rally (low participation).

🟢 Green candle on price drop → potential distribution.

⚪ Gray candles → sideways or stable behavior.

👤 Who Should Use It?

Day traders and scalpers monitoring volume strength.

Technical analysts who focus on volume-price behavior.

Traders who track accumulation/distribution patterns.

MVRV Altcoins📌 Technical Description of Indicator: MVRV Altcoins

This advanced script calculates the Market Value to Realized Value (MVRV) ratio across multiple cryptocurrencies simultaneously. It offers two analytical modes: Normal and Z-Score, optimized for visual comparison and real-time monitoring of up to 13 predefined assets. If a user applies the indicator to a symbol that is not among the 13 programmed assets, the default behavior displays the Bitcoin chart as a fallback reference.

🔍 What Is MVRV and Why Is It Important?

MVRV is an on-chain metric designed to assess whether a cryptocurrency is overvalued or undervalued by comparing its market capitalization to its realized capitalization.

- Market Cap: The total circulating supply multiplied by the current market price.

- Realized Cap: The sum value of all coins based on the price at the time they last moved on-chain, offering a time-weighted valuation.

Normal Calculation:

MVRV_Normal = Market Cap / Realized Cap

This version reflects investor profitability and identifies potential accumulation or distribution zones.

📊 Z-Score Calculation:

MVRV_ZScore = (Market Cap − Realized Cap) / Standard Deviation of Market Cap

This formula evaluates how extreme the current market conditions are compared to historical norms. It normalizes the difference using statistical dispersion, turning it into a volatility-aware metric that better reflects valuation extremes.

🔎 How Market Cap Is Computed

Unlike conventional indicators relying on consolidated feeds, this script uses modular components from CoinMetrics to construct the active capitalization more accurately, especially for altcoins. Here's the breakdown:

Active Capitalization = MARKETCAPFF + MARKETCAPACTSPLY

Realized Capitalization = MARKETCAPREAL

Component Definitions:

- MARKETCAPFF: Market Cap Free Float — total valuation based only on truly circulating coins.

- MARKETCAPACTSPLY: Capitalization from actively circulating supply — filters dormant or locked coins.

- MARKETCAPREAL: Realized Cap — historical valuation weighted by the last on-chain movement of each coin.

This method offers enhanced precision and compatibility across assets that may lack comprehensive data from centralized providers.

⚙️ User-Configurable Parameters

- MVRV Mode: Choose between Normal and Z-Score.

- Percentage Scale View: If enabled, visual output is scaled using predefined divisors (100 / 3.5 or 100 / 6).

- Thresholds for Analysis:

- Normal mode: Define overbought and oversold levels (default 1.0 and 3.5).

- Z-Score mode: Configure statistical boundaries (default 0.0 and 6.0).

- Table Controls:

- Adjustable position on screen (9 options).

- Font size customization: tiny, small, normal, large.

- Color scheme personalization:

- Header: text and background

- Body: text and background

- Central column separator color

📊 Multicrypto Table Architecture

The indicator renders a high-performance visual table displaying data from up to 13 assets simultaneously. Each asset is represented as a vertical column featuring eigth historical data points plus the most recent value.

- Assets are displayed in two blocks separated by a decorative column.

- Each value is rounded to one decimal place for clarity.

- Cells are styled dynamically based on user settings.

🎨 Decorative Column Separator

Since the entire table is built as a unified structure, a color-configurable empty column is inserted mid-table to act as a visual divider. This approach improves readability and aesthetic balance without duplicating code or splitting table logic.

🔁 Default Behavior on Unsupported Assets

If the active chart is not one of the 13 predefined assets, the indicator will automatically display Bitcoin’s data. This ensures the chart remains functional and informative even outside the target asset group.

🎯 Color Interpretation by Condition

The MVRV value for each asset is highlighted using a traffic light system:

- Green: Undervalued (below oversold threshold)

- Red: Overvalued (above overbought threshold)

- Yellow: Neutral zone

This coding simplifies decision-making and visual scanning across assets.

Final Notes

This indicator is modular and fully adaptable, with well-commented sections designed for efficient customization. Its multiactive architecture makes it a valuable tool for crypto analysts tracking diversified portfolios beyond Bitcoin and Ethereum.

It supports visual storytelling across assets, comparative historical evaluation, and identification of strategic zones — whether for accumulation, distribution, or monitoring on-chain sentiment.

VWAP Volume Profile [BigBeluga]🔵 OVERVIEW

VWAP Volume Profile is an advanced hybrid of the VWAP and volume profile concepts. It visualizes how volume accumulates relative to VWAP movement—separating rising (+VWAP) and declining (−VWAP) activity into two mirrored horizontal profiles. It highlights the dominant price bins (POCs) where volume peaked during each directional phase, helping traders spot hidden accumulation or distribution zones.

🔵 CONCEPTS

VWAP-Driven Profiling: Unlike standard volume profiles, this tool segments volume based on VWAP movement—accumulating positive or negative volume depending on VWAP slope.

Dual-Sided Profiles: Profiles expand horizontally to the right of price. Separate bins show rising (+) and falling (−) VWAP volume.

Bin Logic: Volume is accumulated into defined horizontal bins based on VWAP’s position relative to price ranges.

Gradient Coloring: Volume bars are colored with a dynamic gradient to emphasize intensity and direction.

POC Highlighting: The highest-volume bin in each profile type (+/-) is marked with a transparent box and label.

Contextual VWAP Line: VWAP is plotted and dynamically colored (green = rising, orange = falling) for instant trend context.

Candle Overlay: Price candles are recolored to match the VWAP slope for full visual integration.

🔵 FEATURES

Dual-sided horizontal volume profiles based on VWAP slope.

Supports rising VWAP , falling VWAP , or both simultaneously.

Customizable number of bins and lookback period.

Dynamically colored VWAP line to show rising/falling bias.

POC detection and labeling with volume values for +VWAP and −VWAP.

Candlesticks are recolored to match VWAP bias for intuitive momentum tracking.

Optional background boxes with customizable styling.

Adaptive volume scaling to normalize bar length across markets.

🔵 HOW TO USE

Use POC zones to identify high-volume consolidation areas and potential support/resistance levels.

Watch for shifts in VWAP direction and observe how volume builds differently during uptrends and downtrends.

Use the gradient profile shape to detect accumulation (widening volume below price) or distribution (above price).

Use candle coloring for real-time confirmation of VWAP bias.

Adjust the profile period or bin count to fit your trading style (e.g., intraday scalping or swing trading).

🔵 CONCLUSION

VWAP Volume Profile merges two essential concepts—volume and VWAP—into a single, high-precision tool. By visualizing how volume behaves in relation to VWAP movement, it uncovers hidden dynamics often missed by traditional profiles. Perfect for intraday and swing traders who want a more nuanced read on market structure, trend strength, and volume flow.

Big Trade % Heatmap### Big Trade % Heatmap

**Quick overview**

This indicator highlights where “whale” activity is clustered by showing what fraction of the recent candles contained *large‑value trades*. A candle is considered “big” when its notional volume (`volume × close`) exceeds your chosen USD threshold. You instantly see:

* **Percent of big candles** in the last *N* bars, refreshed at the cadence you pick.

* **On‑chart labels & markers** every refresh, so the chart stays clean.

* **Optional heat‑map background** that turns orange (>20 %) or green (>50 %) when big‑trade concentration spikes.

* **Ready‑made alert** when big‑trade dominance crosses 50 %.

---

#### How it works

1. **Trade size per candle** – Calculates `close × volume` to estimate dollars traded.

2. **Threshold filter** – Flags candles whose value is above *Big Trade Threshold (\$)*.

3. **Look‑back window** – Counts what percentage of the last *Lookback Window (X Candles)* were “big.”

4. **Refresh interval** – Repeats the measurement only every *Refresh Interval (Every X Candles)* to avoid label spam.

5. **Visuals** –

* A small blue ▼ above the bar + a text label such as `35.00 % > $25 000`.

* Background shading (green/orange) for quick, at‑a‑glance sentiment.

---

#### Inputs

| Input | Purpose | Default |

| -------------------------------------- | ----------------------------------------------------- | ------- |

| **Lookback Window (X Candles)** | How many recent bars to sample for the % calculation. | 20 |

| **Refresh Interval (Every X Candles)** | How often to display a new label/marker. | 5 |

| **Big Trade Threshold (\$)** | Minimum USD value for a candle to count as “big.” | 10 000 |

Tune these to the symbol and timeframe you trade (e.g., raise the threshold for BTC‑USDT 1‑h, lower it for micro‑caps).

---

#### Alerts

Enable **“High Big Trade %”** to get notified the moment more than half of the last *N* candles qualify as big trades—handy for spotting sudden accumulation or distribution.

---

#### Typical use cases

* **Breakout confirmation** – A surge in big‑trade % just before price escapes a range can validate the move.

* **Whale spotting** – Detect hidden accumulation on pullbacks or aggressive selling into rallies.

* **Filter noise** – Combine with your favorite trend indicator; only act when both align.

---

> *Built with Pine Script v6. Always back‑test before trading live; this tool is for educational purposes and not financial advice.*

Price Volume Trend [sgbpulse]1. Introduction: What is Price Volume Trend (PVT)?

The Price Volume Trend (PVT) indicator is a powerful technical analysis tool designed to measure buying and selling pressure in the market based on price changes relative to trading volume. Unlike other indicators that focus solely on volume or price, PVT combines both components to provide a more comprehensive picture of trend strength.

How is it Calculated?

The PVT is calculated by adding or subtracting a proportional part of the daily volume from a cumulative total.

When the closing price rises, a proportional part of the daily volume (based on the percentage price change) is added to the previous PVT value.

When the closing price falls, a proportional part of the daily volume is subtracted from the previous PVT value.

If there is no change in price, the PVT value remains unchanged.

The result of this calculation is a cumulative line that rises when buying pressure is strong and falls when selling pressure dominates.

2. Why PVT? Comparison to Similar Indicators

While other indicators measure volume-price pressure, PVT offers a unique advantage:

PVT vs. On-Balance Volume (OBV):

OBV simply adds or subtracts the entire day's volume based on the closing direction (up/down), regardless of the magnitude of the price change. This means a 0.1% price change is treated the same as a 10% change.

PVT, on the other hand, gives proportional weight to volume based on the percentage price change. A trading day with a large price increase and high volume will impact the PVT significantly more than a small price increase with the same volume. This makes PVT more sensitive to trend strength and changes within it.

PVT vs. Accumulation/Distribution Line (A/D Line):

The A/D Line focuses on the relationship between the closing price and the bar's trading range (Close Location Value) and multiplies it by volume. It indicates whether the pressure is buying or selling within a single bar.

PVT focuses on the change between closing prices of consecutive bars, multiplying this by volume. It better reflects the flow of money into or out of an asset over time.

By combining volume with percentage price change, PVT provides deeper insights into trend confirmation, identifying divergences between price and volume, and spotting signs of weakness or strength in the current trend.

3. Indicator Settings (Inputs)

The "Price Volume Trend " indicator offers great flexibility for customization to your specific needs through the following settings:

Moving Average Type: Allows you to select the type of moving average used for the central line on the PVT. Your choice here will affect the line's responsiveness to PVT movements.

- "None" : No moving average will be displayed on the PVT.

- "SMA" (Simple Moving Average): A simple average, smoother, ideal for identifying longer-term trends in PVT.

- "SMA + Bollinger Bands": This unique option not only displays a Simple Moving Average but also activates the Bollinger Bands around the PVT. This is the recommended option for analyzing volatility and ranges using Bollinger Bands.

- "EMA" (Exponential Moving Average): An exponential average, giving more weight to recent data, responding faster to changes in PVT.

- "SMMA (RMA)" (Smoothed Moving Average): A smoothed average, providing extra smoothing, less sensitive to noise.

- "WMA" (Weighted Moving Average): A weighted average, giving progressively more weight to recent data, responding very quickly to changes in PVT.

Moving Average Length: Defines the number of bars used to calculate the moving average (and, if applicable, the standard deviation for the Bollinger Bands). A lower value will make the line more responsive, while a higher value will smooth it out.

PVT BB StdDev (Bollinger Bands Standard Deviation): Determines the width of the Bollinger Bands. A higher value will result in wider bands, making it less likely for the PVT to cross them. The standard value is 2.0.

4. Visual Aid: Current PVT Level Line

This indicator includes a unique and highly useful visual feature: a dynamic horizontal line displayed on the PVT graph.

Purpose: This line marks the exact level of the PVT on the most recent trading bar. It extends across the entire chart, allowing for a quick and intuitive comparison of the current level to past levels.

Why is it Important?

- Identifying Divergences: Often, an asset's price may be lower or higher than past levels, but the PVT level might be different. This auxiliary line makes it easy to spot situations where PVT is at a higher level when the price is lower, or vice-versa, which can signal potential trend changes (e.g., higher PVT than in the past while price is low could indicate strong accumulation).

- Quick Direction Indication: The line's color changes dynamically: it will be green if the PVT value on the last bar has increased (or remained the same) relative to the previous bar (indicating positive buying pressure), and red if the PVT value has decreased relative to the previous bar (indicating selling pressure). This provides an immediate visual cue about the direction of the cumulative momentum.

5. Important Note: Trading Risk

This indicator is intended for educational and informational purposes only and does not constitute investment advice or a recommendation for trading in any form whatsoever.

Trading in financial markets involves significant risk of capital loss. It is important to remember that past performance is not indicative of future results. All trading decisions are your sole responsibility. Never trade with money you cannot afford to lose.

Intraday vs Overnight OBV🔍 Purpose

This indicator provides a volume-weighted cumulative flow model that mimics On-Balance Volume (OBV) logic but splits the volume impact into intraday vs. overnight sessions. It allows traders to track how volume contributes to price movement in each session and identify whether buying/selling pressure is stronger during or outside of regular trading hours.

This indicator attempts to alleviate some of the downfalls of the standard OBV indicator, which only looks at total volume and total direction. The price of stocks generally behaves extremely differently during market hours and outside market hours, and many of the large moves happen outside of regular market hours on low volume.

⚙️ Core Features

1) OBV-style calculation:

If price increases → volume is added to the OBV stream.

If price decreases → volume is subtracted.

If price is flat → OBV remains unchanged.

2) Session splitting:

Intraday session: movement from today's open to close.

Overnight session: movement from yesterday’s close to today’s open.

Volume is split proportionally between these two periods based on user input.

3) Four visualization modes:

"Intraday" — plots only OBV from intraday price movement.

"Overnight" — plots only OBV from overnight price movement.

"Aggregate" — plots the sum of intraday and overnight OBV for a holistic view.

"Both Intraday and Overnight" — plots intraday and overnight OBV separately on the same chart.

📐 Inputs

1) Synthetic OBV Type:

"Intraday" — Show OBV from open to close only.

"Overnight" — Show OBV from prior close to today's open only.

"Aggregate" — Show a single line combining both.

"Both Intraday and Overnight" — Show both lines on the same chart.

2) Estimated Overnight Volume %:

Percentage of total daily volume assumed to occur during extended hours.

The rest is allocated to regular session (intraday).

Default: 20% overnight, 80% intraday.

🧮 How It Works

Volume Splitting:

Total bar volume is split into overnight Volume and intraday Volume:

Intraday change is the difference between today’s close and open.

Overnight change is the difference between today’s open and yesterday’s close.

Session OBV Calculations:

OBV is incremented/decremented by the session's allocated volume, depending on whether the session’s price change was positive or negative.

Aggregate OBV:

Combines both session deltas for a holistic volume flow view.

📊 Interpretation

Rising OBV (any stream) suggests accumulation; falling OBV suggests distribution.

Divergences between price and OBV lines (especially overnight vs. intraday) can reveal where hidden buying/selling is occurring.

Comparing intraday vs overnight OBV can help:

Spot whether institutional demand is building off-hours.

Detect retail vs. institutional behavior (retail trades often dominate intraday; institutional may prefer after-hours).

💡 Use Cases

Identify whether overnight gaps are supported by overnight volume momentum.

Detect accumulation in low-volume overnight sessions.

Compare intraday and overnight strength during earnings season or news events.

Complement traditional OBV by seeing session-based breakdowns.

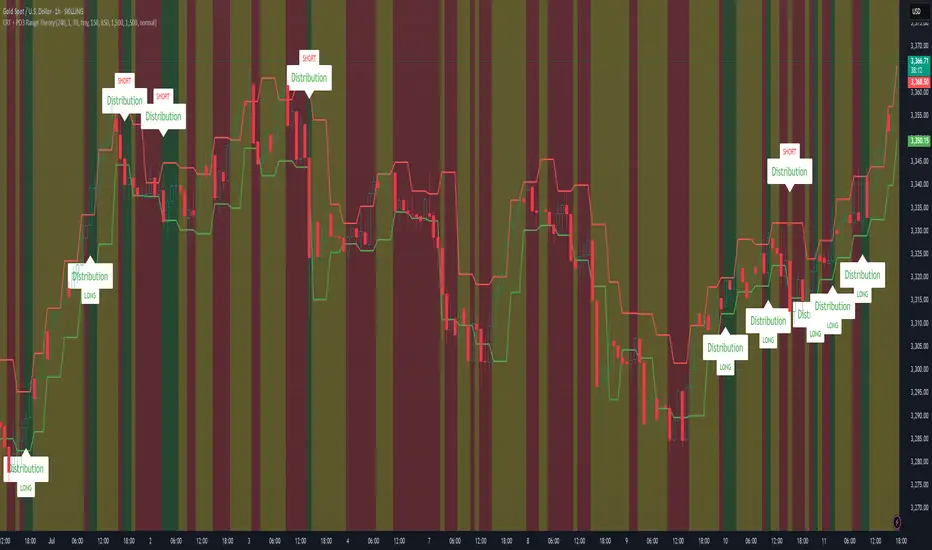

CRT + PO3 Range Theory Hey everyone, I’ve put together a little script for TradingView that tries to show the classic CRT + PO3 (Power of Three) pattern. It’s still a work in progress, so please use it on a demo account and let me know what you think!

What It Does

Accumulation Phase: On each higher‐timeframe bar (e.g. 2-hour), it draws a shaded zone where price is hanging out. That’s when we assume “big players” are quietly building positions.

Manipulation Phase: If price briefly pokes above or below that zone but then slips back inside, it marks that wick as a shake-out.

Distribution Phase: When price finally closes cleanly outside the zone, it draws another shaded area and drops a “Distribution” label plus a big LONG or SHORT arrow on that bar.

You can tweak it so it only shows signals when a bar closes (no more weird flashing mid-bar), or even allow “direct” Distribution on a clean breakout without waiting for a fake wick first.

How to Set It Up

Add the script from your Indicators list.

Pick your HTF (I like 2-hour or 4-hour).

Turn “Show Zone Labels” on or off—these are the little “Accumulation/Manipulation/Distribution” tags.

Turn “Show Entry Signals” on to get the big LONG/SHORT arrows.

If you hate flicker, check “Show signals only at bar close.”

If you want to catch a swift breakout (no fake-out needed), check “Allow direct Distribution on clean breakout.”

There are also sliders for zone colors, transparency, label size, and how far above/below the bars the labels sit.

Why It’s Still a Beta

I’m not a CRT/PO3 guru—this is more of a hobby project and a little facination for this strategy.

There might be edge cases where it misses a shake-out or flags a Distribution too early.

I take no responsibility for your trades—please only run it on a demo account until we’ve worked out the quirks.

Feedback Wanted!

If you try it out, I’d love to hear:

Did the Manipulation wicks line up where you expected?

Were the Distribution arrows on the right bars?

Any ideas for easier settings or extra alerts?

Thanks for testing and helping me turn this into something solid!

BK AK-SILENCER (P8N)🚨Introducing BK AK-SILENCER (P8N) — Institutional Order Flow Tracking for Silent Precision🚨

After months of meticulous tuning and refinement, I'm proud to unleash the next weapon in my trading arsenal—BK AK-SILENCER (P8N).

🔥 Why "AK-SILENCER"? The True Meaning

Institutions don’t announce their moves—they move silently, hidden beneath the noise. The SILENCER is built specifically to detect and track these stealth institutional maneuvers, giving you the power to hunt quietly, execute decisively, and strike precisely before the market catches on.

🔹 "AK" continues the legacy, honoring my mentor, A.K., whose teachings on discipline, precision, and clarity form the cornerstone of my trading.

🔹 "SILENCER" symbolizes the stealth aspect of institutional trading—quiet but deadly moves. This indicator equips you to silently track, expose, and capitalize on their hidden footprints.

🧠 What Exactly is BK AK-SILENCER (P8N)?

It's a next-generation Cumulative Volume Delta (CVD) tool crafted specifically for traders who hunt institutional order flow, combining adaptive volatility bands, enhanced momentum gradients, and precise divergence detection into a single deadly-accurate weapon.

Built for silent execution—tracking moves quietly and trading with lethal precision.

⚙️ Core Weapon Systems

✅ Institutional CVD Engine

→ Dynamically measures hidden volume shifts (buying/selling pressure) to reveal institutional footprints that price alone won't show.

✅ Adaptive AK-9 Bollinger Bands

→ Bollinger Bands placed around a custom CVD signal line, pinpointing exactly when institutional accumulation or distribution reaches critical extremes.

✅ Gradient Momentum Intelligence

→ Color-coded momentum gradients reveal the strength, speed, and silent intent behind institutional order flow:

🟢 Strong Bullish (aggressive buying)

🟡 Moderate Bullish (steady accumulation)

🔵 Neutral (balance)

🟠 Moderate Bearish (quiet distribution)

🔴 Strong Bearish (aggressive selling)

✅ Silent Divergence Detection

→ Instantly spots divergence between price and hidden volume—your earliest indication that institutions are stealthily reversing direction.

✅ Background Flash Alerts

→ Visually highlights institutional extremes through subtle background flashes, alerting you quietly yet powerfully when market-moving players make their silent moves.

✅ Structural & Institutional Clarity

→ Optional structural pivots, standard deviation bands, volume profile anchors, and session lines clearly identify the exact levels institutions defend or attack silently.

🛡️ Why BK AK-SILENCER (P8N) is Your Edge

🔹 Tracks Institutional Footprints—Silently identifies hidden volume signals of institutional intentions before they’re obvious.

🔹 Precision Execution—Cuts through noise, allowing you to execute silently, confidently, and precisely.

🔹 Perfect for Traders Using:

Elliott Wave

Gann Methods (Angles, Squares)

Fibonacci Time & Price

Harmonic Patterns

Market Profile & Order Flow Analysis

🎯 How to Use BK AK-SILENCER (P8N)

🔸 Institutional Reversal Hunting (Stealth Mode)

Bearish divergence + CVD breaking below lower BB → stealth short signal.

Bullish divergence + CVD breaking above upper BB → quiet, early long entry.

🔸 Momentum Confirmation (Silent Strength)

Strong bullish gradient + CVD above upper BB → follow institutional buying quietly.

Strong bearish gradient + CVD below lower BB → confidently short institutional selling.

🔸 Noise Filtering (Patience & Precision)

Neutral gradient (blue) → remain quiet, wait patiently to strike precisely when institutional activity resumes.

🔸 Structural Precision (Institutional Levels)

Optional StdDev, POC, Value Areas, Session Anchors clearly identify exact institutional defense/offense zones.

🙏 Final Thoughts

Institutions move in silence, leaving subtle footprints. BK AK-SILENCER (P8N) is your specialized weapon for tracking and hunting their quiet, decisive actions before the market reacts.

🔹 Dedicated in deep gratitude to my mentor, A.K.—whose silent wisdom shapes every line of code.

🔹 Engineered for the disciplined, quiet hunter who knows when to wait patiently and when to strike decisively.

Above all, honor and gratitude to Gd—the ultimate source of wisdom, clarity, and disciplined execution. Without Him, markets are chaos. With Him, we move silently, purposefully, and precisely.

⚡ Stay Quiet. Stay Precise. Hunt Silently.

🔥 BK AK-SILENCER (P8N) — Track the Silent Moves. Strike with Precision. 🔥

May Gd bless every silent step you take. 🙏

Volatility & Momentum Nexus (VMN)Volatility & Momentum Nexus (VMN)

This indicator was designed to solve a common trader's problem: chart clutter from dozens of indicators that often contradict each other. The Volatility & Momentum Nexus ( VMN ) is not just another indicator; it's a complete analysis system that synthesizes four essential market pillars into a single, clean, and intuitive visual signal.

The goal of VMN is to identify high-probability moments where a period of accumulation (low volatility) is about to erupt into an explosive move, confirmed by trend, momentum, and volume.

VMN analyzes the real-time confluence of four critical elements:

The Trend (The Main Filter): A 100-period Exponential Moving Average (EMA) sets the overall context. The indicator will only look for buy signals above this line (in an uptrend) and sell signals below it (in a downtrend). The line's color changes for quick visualization.

Volatility (Energy Accumulation): Using Bollinger Bands Width (BBW), the indicator identifies "Squeeze" periods—when the price contracts and builds up energy. These zones are marked with a yellow background on the chart, signaling that a major move is imminent.

Momentum (The Trigger): An RSI (Relative Strength Index) acts as the trigger. A signal is only validated if momentum confirms the direction of the breakout (e.g., RSI > 55 for a buy), ensuring we enter the market with force.

Volume (The Final Confirmation): No breakout move is credible without volume. VMN checks if the volume at the time of the signal is significantly higher than its recent average, adding a vital layer of confirmation.

Green Arrow (Buy Signal): Appears ONLY when ALL the following conditions are met simultaneously:

Price is above the 100 EMA (Bullish Trend).

The chart is exiting a Squeeze zone (yellow background on the previous bar).

Price breaks above the upper Bollinger Band.

RSI is above the buy threshold (default 55).

Volume is above average.

Red Arrow (Sell Signal): Appears ONLY when all the opposite conditions are met.

Do not treat signals as blind commands to trade. They are high-probability confirmations.

Look for signals near key Support/Resistance levels for an even higher success rate.

Always set a Stop Loss (e.g., below the low of the signal candle or below the lower Bollinger Band for a buy).

All parameters (EMA, RSI, Bollinger Bands lengths, thresholds, etc.) can be customized from the settings menu to adapt the indicator to any financial asset or timeframe.

Disclaimer: This indicator is a tool for educational and analytical purposes. It does not constitute and should not be interpreted as financial advice. Trading involves significant risk. Always perform your own analysis and backtesting before risking real capital.

Rainbow Price Chart This indicator is a technical and on-chain analysis tool for Bitcoin, designed to help investors better understand the different phases of the market cycle and underlying sentiment. It directly overlays on the price chart (overlay=true).

Indicator Name: "Rainbow Price Chart & V/T Ratio Signals"

General Purpose:

It combines two popular methodologies for visualizing Bitcoin's value and sentiment: the classic "Rainbow Price Chart" and signals derived from the "Value per Transaction Ratio" (V/T Ratio) based on blockchain data. It is ideal for long-term investors looking for strategic entry/exit points.

Main Components:

Rainbow Price Chart:

Concept: Divides Bitcoin's price range into different market "sentiment zones" (e.g., "Bubble Zone," "FOMO Zone," "HODL Zone," "Accumulation Zone," "Buy Zone," "Fire Sale Zone") using colored bands. These bands are calculated as ascending and descending multiples of a base Exponential Moving Average (EMA), configurable by default to 200 periods.

Visualization: The zones are represented with transparent color fills on the price chart. A detailed legend in the top right corner of the chart explains the meaning of each color and sentiment zone.

Important Note: This type of chart is designed to be viewed and analyzed correctly on a logarithmic price scale. The indicator includes a visual reminder to activate this scale.

Value per Transaction (V/T) Ratio Signals:

Concept: Measures the average value per transaction on the Bitcoin blockchain by dividing the total transacted volume in USD by the number of transactions. This ratio is smoothed with an Exponential Moving Average (by default, 7 periods) and is framed within a dynamic Linear Regression Channel (LRC) based on standard deviation.

Signal Generation: Based on the position of the smoothed V/T Ratio within this LRC channel, the indicator generates signals directly on the price chart, such as:

"BOTTOM": Low price, V/T Ratio in the lower band of the LRC.

"SEMI-LOW" / "SEMI-HIGH": Intermediate phases within the channel.

"ATH" (All-Time High): Potentially overvalued price, V/T Ratio in the upper band of the LRC.

On-Chain Data: The indicator requests external daily on-chain data for total transacted volume (TVTVR) and number of transactions (NTRAN) from the Bitcoin blockchain.

Diagnostic Panes: Includes plots of the raw on-chain data (volume and number of transactions) in a separate pane, which are useful for debugging or verifying the data source. The lines for the V/T Ratio itself and its LRC channel are not plotted by default but can be activated in the code for deeper analysis.

Ideal for:

Bitcoin investors and "hodlers" who desire a visual tool that combines price-based market cycle context with fundamental signals derived from on-chain activity, to help identify key moments for accumulation or potential distribution.

Considerations:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe.

Bullish Volume AnomalyAnomaly is designed to spot hidden bullish accumulation before price actually breaks out, by blending a trend-aware volume measure with a volatility-adjusted price channel. Here’s how it works:

First, it runs a simple ATR-based zigzag to identify the current swing direction. Volume is then signed (+ for up-trends, – for down-trends) and cumulatively summed. By converting that cumulative signed volume into a z-score over the past 480 bars, we get a sense of when buying or selling pressure is unusually strong relative to its own history.

At the same time, price itself is normalized into a z-score over the same 480-bar window, and its change over that period is also tracked. These two measures—volume z-score (s) and price z-score (p)—are compared, and the indicator looks for moments when s outpaces p by at least two standard deviations (s – p > 2), while price momentum change remains low (c < 1) and the net volume is positive (s > 0). That combination flags instances where heavy buying is taking place but price hasn’t yet reacted.

To define a dynamic trading zone, it plots a 288-bar EMA of price as the middle band (t2), and builds upper and lower bands around it using the average close-to-open range multiplied by a user-set factor. The lower band (t1) sits beneath the EMA by that volatility-based margin. A signal fires only when the bar’s high stays below t1—meaning price is still “sleeping” under the lower volatility boundary even as bullish volume builds up.

Together, these filters home in on anomalies: strong, trend-aligned volume surges that outstrip price movement, occurring while price sits below its lower volatility band. In practice, that often marks early accumulation before a breakout. You can tweak the ATR length and multiplier for the zigzag, as well as the channel period and range factor, to suit different markets or timeframes.

[blackcat] L1 Net Volume DifferenceOVERVIEW

The L1 Net Volume Difference indicator serves as an advanced analytical tool designed to provide traders with deep insights into market sentiment by examining the differential between buying and selling volumes over precise timeframes. By leveraging these volume dynamics, it helps identify trends and potential reversal points more accurately, thereby supporting well-informed decision-making processes. The key focus lies in dissecting intraday changes that reflect short-term market behavior, offering critical input for both swing and day traders alike. 📊

Key benefits encompass: