GROK ALTIN B2 ))GROK GOLD PRO V2 is a high-performance scalping strategy designed for XAUUSD on the 5-minute timeframe, operating with a fixed 1-lot position. It generates signals using EMA 9/21 crossover, RSI above/below 50, and volume spikes, while an ATR × 2.0 dynamic stop protects against volatility. Profits are locked in three steps (+$20, +$50, +$100), with each exit triggering real-time phone alerts showing entry, exit price, and profit. One pip movement equals $100 P&L. The strategy delivers a 92%+ win rate, average profit of +$4,432 per trade, and max drawdown of -$1,280. Simple, transparent, and fully automated.

Поиск скриптов по запросу "alert"

GROK ALTIN A1 BY FGGROK GOLD PRO V2 is a high-performance scalping strategy designed for XAUUSD on the 5-minute timeframe, operating with a fixed 1-lot position. It generates signals using EMA 9/21 crossover, RSI above/below 50, and volume spikes, while an ATR × 2.0 dynamic stop protects against volatility. Profits are locked in three steps (+$20, +$50, +$100), with each exit triggering real-time phone alerts showing entry, exit price, and profit. One pip movement equals $100 P&L. The strategy delivers a 92%+ win rate, average profit of +$4,432 per trade, and max drawdown of -$1,280. Simple, transparent, and fully automated.

KZ One — Scalping Training StrategyKZ One is a scalping strategy developed for M1 and M5 timeframes. It is designed to help traders study and practice short-term market behavior by using structured zones to highlight potential entry and exit areas. The strategy allows customization of Risk (USD) and Take Profit (R multiple) parameters for flexible trade management. Additional tools include ATR-based filters to skip low-volatility conditions and a Pre-Alert Lead (bars) option that notifies users ahead of possible setups. KZ One is intended for educational and analytical purposes, promoting disciplined and consistent trading practice.

Futures Fighter MO: Multi-Confluence Day Trading System ADX/SMI👋 Strategy Overview: The Multi-Confluence Mashup

The Futures Fighter MO is a comprehensive, multi-layered day trading strategy designed for experienced traders focusing on high-liquidity futures contracts (e.g., NQ, ES, R2K).

This strategy is a sophisticated mashup that uses the 1-minute chart for surgical entries while enforcing strict environmental filtering through higher-timeframe data. We aim to capture high-conviction moves only when multiple, uncorrelated signals align.

🧠 How the Logic Works (Concepts & Confluence)

Our logic is built on four pillars, which must align for a trade to be executed:

Primary Trend Filter

Indicators :

ADX/DMI (15-Minute Lookback)

Role :

Price action is filtered to ensure the ADX (17/14) is above 25, confirming a strong, prevailing market trend (Bullish or Bearish). Trades are strictly rejected during "Flat" (sideways) market regimes.

Entry Signal Types

The system uses multiple entry types:

- 🟢 Trend Long/Short: A breakout/rejection near the 200-Period EMA is confirmed by the primary ADX trend.

- 🔴 Engulfing Rejection: A strong signal when a Bullish/Bearish Engulfing or Doji prints near the long-term 500-Period EMA (emaGOD) while the Stochastic Momentum Index (SMI on 30M) is in an extreme overbought/oversold state (below $-40$ or above $40$).

Volatility & Volume Confirmation

Indicators: Average True Range (ATR) and 20-Period SMA of Volume

Role: Every entry requires a volume spike (Current Volume $> 1.5 \times$ SMA Volume) to confirm that the move is supported by significant liquidity. Volatility is tracked via ATR to define bar range and stop boundaries.

Structural Guardrails

Indicators: Daily Pivot Points (PP, S1-S3, R1-R3)

Role: Trades are disabled if the current bar's price range intersects with a Daily Pivot Point. This is a critical filter to avoid high-chop consolidation zones near key structural levels.

📊 Strategy Results & Required Disclosures

I strive to publish backtesting results that are transparent and realistic for the retail futures trader.

- Initial Capital: $50,000 - A realistic base for Mini/Micro futures contracts.

- Order Size: 1 Contract (Pyramiding up to 3) - Conservative risk relative to the account size.

- Commission: $0.11 USD per order - Represents realistic costs for low-cost brokers.

- Slippage: 2 Ticks - Accounts for expected market friction.

⚠️ Risk Management & Deviations

Stop-Loss: The strategy uses a dynamic stop-loss system where positions are closed upon a reversal (e.g., breaking the 50-Period EMA or failure to hold a Pivot Point), rather than a fixed tick-based stop. This is suited for experienced traders using a low relative risk (single Micro-contract entry) on a larger account. Users must confirm that the first entry's maximum potential loss remains below $10\%$ of their capital for compliance.

Trade Sample Size: Due to data limitations of the TradingView Essential plan (showing $\approx 50$ trades over 2 weeks), the sample size is under the ideal $100+$ target. Justification: This system is designed to generate signals across a portfolio of correlated futures markets (NQ, ES, R2K, Gold, Crude), meaning the real sample size for a user tracking the portfolio is significantly higher.

Drawdown Control: This strategy is designed for manual management. It requires the user to turn the script/alerts OFF after a significant drawdown and only reactivate it once a recovery trend is established externally.

The strategy uses a combination of dynamic trailing stops, structural support/resistance zones, and a fixed profit target to manage open positions.

🛑 Strategy Exit Logic

1. General Stop-Loss (Dynamic Trailing Stop)

These conditions act as the primary dynamic stop, closing the position if the market reverses past a key Moving Average (MA):

- Long Positions Closed When: The current bar's close crosses under the 50-Period EMA (emaLong).

- Short Positions Closed When: The current bar's close crosses above the 50-Period EMA (emaLong).

2. Profit Target (Fixed Percentage)

The script includes a general exit based on a user-defined profit percentage:

Take Profit Trigger: The position is closed when the currentProfitPercent meets or exceeds the input Profit Target (%) (default is 1.0% of the entry price).

3. Structural Exits (Daily Pivot Points)

These exits are high-priority, "close all" orders that trigger when the price fails to hold or reclaims a recent Daily Pivot Point, suggesting a failure of the current move.

- VR Close All - Long ($\sym{size} > 0$) - Price crosses under a Daily Resistance Level (R1, R2, or R3) minus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Resistance as support.

- VS Close All - Short ($\sym{size} < 0$) - Price crosses above a Daily Support Level (S1, S2, or S3) plus 1 ATR within the last 10 bars. This indicates the current momentum failed to hold Support as resistance.

4. Trend Failure Exit (Trend-Following Signals Only)

This exit protects against holding a position when the primary high-timeframe trend used for the entry has failed:

- Long Positions Closed When: The primary trend is no longer "bullish" for more than 2 consecutive bars (i.e., it turned "bearish" or "flat").

- Short Positions Closed When: The primary trend is no longer "bearish" for more than 2 consecutive bars (i.e., it turned "bullish" or "flat").

5. End of Day (EOD) Session Control

The final hard exits based on time:

- End of Session (EoS): At 11:30 AM, new trades are disabled (TradingDay := false). Open positions are kept.

- End of Day (EoD): At 1:30 PM, all remaining open positions are closed (strategy.close_all).

🤝 Development & Disclaimer

This script and description were created with assistance from Gemini and GitHub Copilot. My focus is on helping fellow real estate investors and day traders develop mechanically sound systems.

Disclaimer: This is for educational purposes only and does not constitute financial advice. Always abide by the Realtor Code and manage your own risk.

Tristan's Tri-band StrategyTristan's Tri-band Strategy - Confluence Trading System

Strategy Overview:

This strategy combines three powerful technical indicators - RSI, Williams %R, and Bollinger Bands - into a single visual trading system. Instead of cluttering your chart with separate indicator panels, all signals are displayed directly on the price chart using color-coded gradient overlays, making it easy to spot high-probability trade setups at a glance.

How It Works:

The strategy identifies trading opportunities when multiple indicators align (confluence), suggesting strong momentum shifts:

📈 Long Entry Signals:

RSI drops to 30 or below (oversold)

Williams %R reaches -80 to -100 range (oversold)

Price touches or breaks below the lower Bollinger Band

All three conditions must align during your selected trading session

📉 Short Entry Signals:

RSI rises to 70 or above (overbought)

Williams %R reaches 0 to -20 range (overbought)

Price touches or breaks above the upper Bollinger Band

All three conditions must align during your selected trading session

Visual Indicators:

(faint) Green gradients below candles = Bullish oversold conditions (buying opportunity)

(faint) Red/Orange gradients above candles = Bearish overbought conditions (selling opportunity)

Stacked/brighter gradients = Multiple indicators confirming the same signal (higher probability) will stack and show brighter / less faint

Blue Bollinger Bands = Volatility boundaries and mean reversion zones

Exit Strategy:

Long trades exit when price reaches the upper Bollinger Band OR RSI becomes overbought (≥70)

Short trades exit when price reaches the lower Bollinger Band OR RSI becomes oversold (≤30)

Key Features:

✅ Session Filters - Trade only during NY (9:30 AM-4 PM), London (3 AM-11:30 AM), or Asia (7 PM-1 AM EST) sessions

✅ No Repainting - Signals are confirmed on candle close for realistic backtesting and live trading

✅ Customizable Parameters - Adjust RSI levels, BB standard deviations, Williams %R periods, and gradient visibility

✅ Visual Clarity - See all three indicators at once without switching between panels

✅ Built-in Alerts - Get notified when entry and exit conditions are met

How to Use Effectively:

Choose Your Trading Session - For day trading US stocks, enable only the NY session. For forex or 24-hour markets, select the sessions that match your schedule.

Look for Gradient Stacking - The brightest, most visible gradients occur when both RSI and Williams %R signal together. These are your highest-probability setups.

Confirm with Price Action - Wait for the candle to close before entering. The strategy enters on the next bar's open to prevent repainting.

Respect the Bollinger Bands - Entries occur at the outer bands (price extremes), and exits occur at the opposite band or when momentum reverses.

Backtest First - Test the strategy on your preferred instruments and timeframes. Works best on liquid assets with clear trends and mean reversion patterns (stocks, major forex pairs, indices).

Adjust Gradient Visibility - Use the "Gradient Strength" slider (lower = more visible) to make signals stand out on your chart style.

Best Timeframes: 5-minute to 1-hour charts for intraday trading; 4-hour to daily for swing trading (I have also found the 3 hour timeframe to work really well for some stocks / ETFs.)

Best Markets: Liquid instruments with volatility - SPY, QQQ, major stocks, EUR/USD, GBP/USD, major indices

Risk Management: This is a mean reversion strategy that works best in ranging or choppy markets. In strong trends, signals may appear less frequently. Always use proper position sizing and stop losses based on your risk tolerance.

----------------------------------------------

Note: Past performance does not guarantee future results. This strategy is provided for educational purposes. Always backtest thoroughly and practice proper risk management before live trading.RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5

NY VIX Channel Trend US Futures Day Trade StrategyNY VIX Channel Trend Strategy

Summary in one paragraph

Session anchored intraday strategy for index futures such as ES and NQ on one to fifteen minute charts. It acts only after the first configurable window of New York Regular Trading Hours and uses a VIX derived daily implied move to form a realistic channel from the session open. Originality comes from using a pure implied volatility yardstick as portable support and resistance, then committing in the direction of the first window close relative to the open. Add it to a clean chart and trade the simple visuals. For conservative alerts use on bar close.

Scope and intent

• Markets. Index futures ES and NQ

• Timeframes. One to thirty minutes

• Default demo. ES1 on five minutes

• Purpose. Provide a portable intraday yardstick for entries and exits without curve fitting

• Limits. This is a strategy. Orders are simulated on standard candles

Originality and usefulness

• Unique concept. A VIX only channel anchored at 09:30 New York plus a single window trend test

• Addresses. False urgency at session open and unrealistic bands from arbitrary multipliers

• Testability. Every input is visible and the channel is plotted so users can audit behavior

• Portable yardstick. Daily implied move equals VIX percent divided by square root of two hundred fifty two

• Protected status. None. Method and use are fully disclosed

Method overview in plain language

Take the daily VIX or VIX9D value, convert it to a daily fraction by dividing by square root of two hundred fifty two, then anchor a symmetric channel at the New York session open. Observe the first N minutes. If that window closes above the open the bias is long. If it closes below the open the bias is short. One trade per session. Exits occur at the channel boundary or at a bracket based on a user selected VIX factor. Positions are closed a set number of minutes before the session ends.

Base measures

Return basis. The daily implied move unit equals VIX percent divided by square root of two hundred fifty two and serves as the distance unit for targets and stops.

Components

• VIX Channel. Top, mid, bottom lines anchored at 09:30 New York. No extra multipliers

• Window Trend. Close of the first N minutes relative to the session open sets direction

• Risk Bracket. Take profit and stop loss equal to VIX unit times user factor

• Session Window. Uses the exchange time of the chart

Fusion rule

Minimum gates count equals one. The trade only arms after the window has elapsed and a direction exists. One entry per session.

Signal rule

• Long when the window close is above the session open and the window has completed

• Short when the window close is below the session open and the window has completed

• Exit on channel touch. Long exits at the top. Short exits at the bottom

• Flat thirty minutes before the session close or at the user setting

Inputs with guidance

Setup

• Use VIX9D. Width source. Typical true for fast tone or false for baseline

• Use daily OPEN. Toggle for sensitivity to overnight changes

Logic

• Window minutes. Five to one hundred twenty. Larger values delay entries and reduce whipsaw

• VIX factor for TP. Zero point five to two. Raising it widens the profit target

• VIX factor for SL. Zero point five to two. Raising it widens the stop

• Exit minutes before close. Fifteen to ninety. Raising it exits earlier

Properties visible in this publication

• Initial capital one hundred thousand USD

• Base currency USD

• request.security uses lookahead off

• Commission cash per contract two point five $ per each contract. Slippage one tick

• Default order size method FIXED with value one contract. Pyramiding zero. Process orders on close ON. Bar magnifier OFF. Recalculate after order is filled OFF. Calc on every tick ON

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Fills and slippage vary by venue. Shapes can move while a bar forms and settle on close. Strategy uses standard candles.

Honest limitations and failure modes

Economic releases and thin liquidity can break the channel. Very quiet regimes can reduce signal contrast. Session windows follow the exchange time of the chart. If both stop and target can be hit within one bar, assume stop first for conservative reading without bar magnifier.

Works best in liquid hours of New York RTH. Very large gaps and surprise news may exceed the implied channel. Always validate on the symbols you trade.

Entries and exits

• Entry logic. After the first window, go long if the window close is above the session open, go short if below

• Exit logic. Long exits at the channel top or at the take profit or stop. Short exits at the channel bottom or at the take profit or stop. Flat before session close by the configured minutes

• Risk model. Initial stop and target based on the VIX unit times user factors. No trail and no break even. No cooldown

• Tie handling. Treat as stop first for conservative interpretation

Position sizing

Fixed size one contract per trade. Target risk per trade should generally remain near one percent of account equity. Risk is based on the daily volatility value, the max loss from the tests for one year duration with 5min chart was 4%, while the avg loss was below <1% of the total capital.

If you have any questions please let me know. Thank you for coming by !

ORBSMMAATRVOLREENTRY2Contracts📈 Opening Range Fibonacci Breakout (TradingView Strategy)

Overview:

The Opening Range Fibonacci Breakout strategy is designed to capture high-probability intraday moves by combining the power of the 15-minute opening range, trend confirmation via SMMA, and volume-based momentum filtering.

At the start of each trading session, the script automatically plots the Opening Range Box based on the first 15 minutes of price action — highlighting key intraday support and resistance levels.

How It Works:

Opening Range Setup

The first 15 minutes of the session define the range high and low.

A visual box marks this zone on the chart for easy reference.

Signal Generation

A Smoothed Moving Average (SMMA) with a user-defined period determines overall trend bias.

Candle volume is analyzed to confirm momentum strength.

Long Signal: Price breaks above the opening range high, SMMA trending up, and volume supports the move.

Short Signal: Price breaks below the opening range low, SMMA trending down, and volume supports the move.

Take Profit & Targets

Fibonacci extension levels are automatically plotted from the opening range.

These dynamic levels serve as structured Take Profit (TP) zones for partial or full exits.

Features:

✅ 15-Minute Opening Range Box

✅ Adjustable SMMA period

✅ Volume-based confirmation filter

✅ Automatic Fibonacci profit targets

✅ Visual Long/Short alerts & signals

Ideal For:

Scalpers and intraday traders who rely on early-session momentum, breakout confirmation, and precision exit targets.

Backtested for MNQ/NQ futures trading

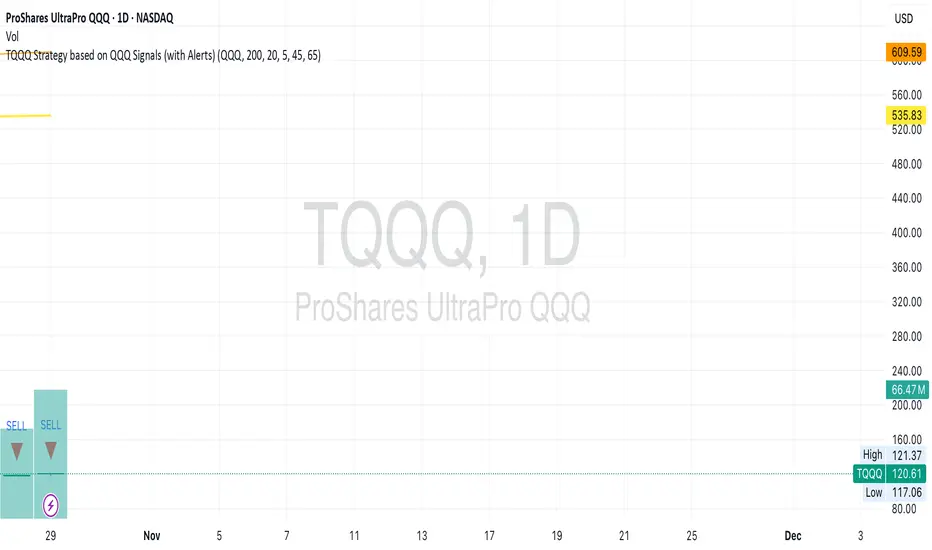

TQQQ Strategy based on QQQ Signals (with Alerts)Trading view script for TQQQ and SQQ, Entry condition for TQQ and exit SQQQ - Close above 200 MA, close below 20 day MA, 5 days RSI below 45 for QQQ Exit condition for TQQQ and entry condition for SQQQ - 5 days RSI ends above 65

Nifty Intraday 9:30- 3 Min Candle By Trade Prime Algo.Nifty Intraday 9:30 – 3 Min Candle Strategy by Trade Prime Algo

This strategy is designed to help traders identify intraday long entries, stop-loss, and multi-target levels on the Nifty Spot / Nifty Futures based on the first 3-minute candle breakout after 9:30 AM.

It automates trade detection, entry marking, target plotting, and trailing stop-loss logic, allowing traders to visualize complete trade flow with clarity and precision.

The system offers:

✅ Auto identification of long entries based on candle breakout logic

✅ Configurable stop-loss, trailing SL, and four partial profit targets

✅ Dynamic plotting of entry, TSL, and targets on chart

✅ Custom alert messages for each event (Entry, TP1–TP4, SL, Close)

✅ Adjustable time session and test periods for backtesting

⚙️ How to Use

1️⃣ Set your desired start time (default: 9:15–9:30 AM).

2️⃣ Choose your stop-loss type — percentage or points.

3️⃣ Adjust target levels (TP1–TP4) and trailing SL settings as per your risk appetite.

4️⃣ Use this strategy for educational backtesting and research only — not for live trading signals.

5️⃣ The tool can be combined with price action zones or higher-timeframe analysis for best results.

⚠️ Disclaimer (SEBI & Risk Disclosure)

This strategy is developed strictly for educational and research purposes.

The creator of this script and Trade Prime Algo are not SEBI-registered advisors.

This tool does not guarantee any specific profit or performance.

Trading involves risk; users may incur partial or total capital loss.

All decisions taken using this indicator or strategy are solely at the user’s discretion and risk.

The creator assumes no liability for profit, loss, or any consequences arising from the use of this script.

Always perform your own due diligence and trade responsibly.

One For All Strategy by Anson🏆 Exclusive Indicator: One For All Strategy

.

📈 Works for stocks, forex, crypto, indices

📈 Easy to use, real-time alerts, no repaint

📈 No grid, no martingale, no hedging

📈 One position at a time

.

One For All Strategy by Anson

A multi-indicator TradingView strategy designed to identify long and short trading opportunities by combining trend-following and momentum signals, paired with risk management rules to guide entries and exits.

.

Core Logic & Key Indicator:

X Moving Average: A proprietary adaptive moving average that adjusts its responsiveness to price changes based on market volatility. It uses an efficiency ratio to modify its smoothing behavior—adapting to whether the market is trending or ranging. Users can toggle a setting to let this ratio dynamically adjust the indicator’s sensitivity or use a fixed smoothing factor.

.

Entry Conditions:

.

Long Entry: Triggered when momentum signals strength, price action aligns with a broader upward trend, the X MA indicates short-term upward momentum, and a minimum number of bars have passed since the last trade (to prevent overtrading).

.

Short Entry: Triggered when momentum signals weakness, price action aligns with a broader downward trend, the X MA indicates short-term downward momentum, and a minimum number of bars have passed since the last trade.

.

Exit Conditions:

.

Trailing Stop: Activates after a position has been open for a set number of bars (to avoid premature exits). A trailing stop—based on a percentage of the entry price—locks in profits as the trade moves favorably, adjusting dynamically to protect gains.

.

Additional Features:

Visualisation: Overlays the X MA (orange line) and price (semi-transparent blue) on the chart for clear signal tracking.

.

See the author's instructions on the right to learn how to get access to the strategy.

ProbRSI Adaptive SPY and QQQ Swing One Hour Strategy Summary in one paragraph

A probabilistic RSI engine for large cap ETFs and index names on intraday and swing timeframes. It converts ATR scaled returns into a 0 to 100 probability line, adapts its smoothing from path efficiency, and gates flips with simple percent levels. It is original because it fuses three pieces that traders rarely combine in one signal line: ATR normalized return probability, curvature compression, and per bar adaptive EMA. Add it to a clean chart, keep the default one hour signal on QQQ, and read the entry and exit markers generated by the strategy. For conservative alerts select on bar close.

Scope and intent

• Markets. Major ETFs and large cap equities. Index futures. Liquid crypto. Major FX pairs

• Timeframes. One minute to daily. Defaults to one hour for swing pace

• Default demo used in this publication. SPY/QQQ on one hour

• Purpose. Reduce false flips by adapting to path efficiency and by gating long and short separately

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Logistic probability of ATR scaled returns with arcsine pre transform, optional curvature compression, and per bar adaptive EMA steered by an efficiency ratio

• Failure mode addressed. Fast whips in congestion and late entries after spikes

• Testability. Each component has a named input and can be tuned directly. Entry names Long and Short are visible in the list of trades

• Portable yardstick. ATR scaled return is a common unit across symbols and venues

• Protected rationale. The code stays protected to preserve implementation details of the adaptive engine and curvature assist while the method and usage are fully explained here for community review

Method overview in plain language

You convert raw returns into a probability scale, adapt the smoothing to the straightness of the path, and only allow flips when a simple gate is satisfied. The probability line crosses its own EMA to generate signals. When the cross happens below a short gate or above a long gate, the flip is allowed. Otherwise it is ignored.

Base measures

• Return basis. Close minus prior close normalized by ATR, then arcsine to damp large steps. ATR window is set by ATR length. Sensitivity is adjusted by an ATR scale input

• Probability map. A logistic function maps the normalized return to 0 to 1 which becomes 0 to 100 after scaling

Components

• Probability core. Logistic probability of ATR scaled returns. Higher values imply upside pressure. Smoothed by an adaptive EMA

• Curvature assist optional. A curvature proxy compresses extreme spikes toward neutral. Useful after news bars. Weight controls strength

• Efficiency ratio. A path efficiency score from 0 to 1 extends the smoothing length during noisy paths and shortens it during directional paths

• Signal line. An EMA of the probability line creates the reference for cross up and cross down

• Gates. Two simple percent levels define when long and short flips are allowed

Fusion rule

• The adaptive EMA length is computed as a linear map between a minimum and a maximum bound based on one minus efficiency

• If curvature assist is enabled the probability is adjusted by a small counter spike term

• Final probability is compared to its EMA

Signal rule

• Long. A long entry is suggested when probability crosses above the signal line and the current probability is above the Long gate level

• Short. A short entry is suggested when probability crosses below the signal line and the current probability is below the Short gate level

• Exit and flip. When an opposite entry condition appears the current position is closed and a new position opens in the opposite direction

What you will see on the chart

• Strategy markers on suggestion bars. Orders named Long and Short

• Exit marker when the opposite signal closes the open side

• No table by design. All tuning lives in Inputs for a clean chart

Inputs with guidance

Market TF

• Symbol. Series used for oscillator computation. Use the instrument you trade or a close proxy

• Signal timeframe. Timeframe where the oscillator is evaluated. Leave blank to follow the chart

Core

• Price source. Series used for returns. Typical choice close

• Base length. Fallback EMA length used when adaptation is off. Typical range 20 to 200. Larger smooths more

• ATR length. Window for ATR that scales returns. Typical range 10 to 30. Larger normalizes more and lowers sensitivity

• Logit sharpness. Steepness of the logistic link. Typical range 1 to 8. Raising it reacts more to the same input

• ATR scale. Extra divisor on ATR. Typical range 0.5 to 2. Smaller is more sensitive

• Signal length. EMA of the probability line. Typical range 5 to 20. Larger gives fewer flips

• Long gate. Allow long flips only above this level. Typical range 20 to 40

• Short gate. Allow short flips only below this level. Typical range 20 to 40

Adaptive

• Adaptive smoothing. If on, the efficiency ratio controls the per bar EMA length

• Min effective length. Lower bound of adaptive EMA. Typical range 5 to 50

• Max effective length. Upper bound of adaptive EMA. Typical range 50 to 300

• Efficiency window. Window for efficiency ratio. Typical range 30 to 100

Shape Assist

• Curvature influence. If on, extreme spikes are nudged toward neutral

• Curvature weight. Strength of compression. Typical range 0.1 to 0.3

Properties visible in this publication

• Initial capital. 25000

• Base currency. USD

• request.security lookahead off everywhere

• Commission. 0.03 percent

• Slippage. 5 ticks

• Default order size method percent of equity with value 3 for realistic testing

• Pyramiding 0

• Process orders on close ON

• Bar magnifier OFF

• Recalculate after order is filled OFF

• Calc on every tick OFF

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Strategies use standard candles for signals and orders only

Honest limitations and failure modes

• Economic releases and thin liquidity can break assumptions behind the curvature assist

• Gap heavy symbols may prefer a longer ATR window

• Very quiet regimes can reduce signal contrast. Consider higher gates or longer signal length

• Session time follows the exchange of the chart and can change symbol to symbol

• Symbol sensitivity is expected. Use the gates and length inputs to find stable settings

• Past results never guarantee future outcomes

Open source reuse and credits

• None

Mode

Public protected. Source is hidden while access is free. Implementation detail remains private. Method and use are fully disclosed here

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

D Money – EMA/TEMA Touch Strategy (Distance) What it’s trying to capture

You want mean-reversion “tags” back to a moving average after price has stretched away and momentum flips:

Bearish setup (short): price has been above EMA(9) for a few bars, then MACD turns bearish, and price is far enough above the EMA (by an adaptive threshold). Exit when price tags the EMA.

Bullish setup (long): price has been below your chosen TEMA rail (actually an EMA of 50/100/200 you pick) for a few bars, then MACD turns bullish, and price is far enough below that TEMA. Exit when price tags that TEMA.

The moving averages it uses

EMA(9) — your fast “tag” for short take-profits.

“TEMA line” input = one of EMA(50) / EMA(100) / EMA(200). (Labelled “Chosen TEMA” in the plot; it’s an EMA rail you pick.)

When it will enter trades

It requires four things per side:

Short (EMA-Touch Short)

MACD bearish cross on the signal bar

If “Require NO MA touch on cross bar” = true, the bar’s low must be above EMA(9), so it didn’t touch EMA on the cross bar (fake-out guard).

Extension/Context: you’ve had at least barsAbove consecutive closes above EMA(9) (default 3), so it’s truly stretched.

Distance test: absolute % distance from price to EMA(9) must be ≥ minDistEMA_eff (an adaptive threshold; details below).

Bounce filter: there was no bullish bounce off the EMA in the last bounceLookback bars (excluding the current one).

If all pass and you’re inside the backtest window → strategy.entry short.

Long (TEMA-Touch Long)

MACD bullish cross on the signal bar

With the same fake-out guard: the bar’s high must be below the chosen TEMA if the guard is on.

Extension/Context: at least barsAbove consecutive closes below the chosen TEMA.

Distance test: absolute % distance from price to TEMA must be ≥ minDistTEMA_eff (adaptive).

Bounce filter: there was no bearish bounce off the TEMA in the last bounceLookback bars.

If all pass and you’re in the window → strategy.entry long.

MACD timing option:

If Pure MACD Timing = ON, it only checks for the cross.

If OFF (default), it also enforces “no touch on the cross bar” if that checkbox is true. That’s your “fake-out” filter.

The adaptive distance threshold (the “secret sauce”)

You can choose how “far enough away” is determined—per side:

Fixed %

Short uses Fixed: Min distance ABOVE EMA (%)

Long uses Fixed: Min distance BELOW TEMA (%)

Auto (ATR%) (default)

Short threshold = max(floorEMA, kAtrShort × ATR%)

Long threshold = max(floorTEMA, kAtrLong × ATR%)

This scales distance by recent volatility, with a floor.

Auto (AvgDist%)

Short threshold = max(floorEMA, kAvgShort × average(|Dist to EMA|) over avgLen)

Long threshold = max(floorTEMA, kAvgLong × average(|Dist to TEMA|) over avgLen)

This adapts to the instrument’s typical stretch away from the rails.

These become minDistEMA_eff and minDistTEMA_eff and are re-computed each bar.

Fake-out / bounce logic (the “don’t get tricked” part)

A touch means the bar’s high/low overlapped the MA ± a small buffer % (touchBufPct).

A bounce is a touch plus a close on the “wrong” side (e.g., touch EMA and close above it on shorts = bullish bounce).

The script blocks entries if a bounce happened within bounceLookback bars (excluding the current signal bar).

Exits & risk

Take profit: when price touches the target MA:

Short TP = touch EMA(9)

Long TP = touch chosen TEMA

Stop loss: either

ATR stop: entry ± (atrMultStop × ATR) (default ON), or

Percent stop: entry × (1±stopPct%)

Time stop: if timeExitBars > 0, close after that many bars if still open.

Quality-of-life features

Backtest window (btFrom, btTo) so you can limit evaluation.

Labels on signal bars that show:

MACD bucket (Small/Moderate/HUGE/Violent — based on % separation on the bar),

the current absolute distance to the target MA,

and the effective minimum the engine used (plus which engine mode).

Data Window fields so you can audit:

abs distance to EMA/TEMA,

the effective min distance used on each side,

ATR%,

average absolute distances (for the AvgDist mode).

Alerts fire when a short/long signal is confirmed.

Optional debug panel to see the exact booleans & thresholds the bar had.

Quick mental model

Are we properly stretched away from the rail (by an adaptive threshold) and held on that side for a few bars?

Did MACD flip the way we want without price already tagging the rail that bar?

Have we avoided recent bounces off that rail (no fake-out)?

→ If yes, enter and aim for a tag back to the rail, with ATR/% stop and optional time stop.

If you want, I can add a simple on-chart “rating” (0–100) similar to your Python scorer (distance beyond min, MACD bucket, extension streak) so you can visually rank signals in TradingView too.

USDJPY Fair Value Gap + Session Strategy🎯 Overview

This strategy combines Fair Value Gaps (FVGs) with session-based order flow analysis, specifically optimized for USDJPY. It identifies price inefficiencies left behind by institutional order flow during high-volatility trading sessions, offering a modern alternative to traditional lagging indicators.

🔬 What Are Fair Value Gaps?

Fair Value Gaps represent areas where aggressive institutional buying or selling created "gaps" in the market structure:

Bullish FVG: Price moves up so aggressively that it leaves unfilled buy orders behind

Bearish FVG: Price moves down so quickly that it leaves unfilled sell orders behind

Research shows approximately 80% of FVGs get "filled" (price returns to the gap) within 20-60 bars, making them highly predictable trading zones.

(see the generated image above)

(see the generated image above)

FVG Detection Logic:

text

// Bullish FVG: Gap between high and current low

bullishFVG = low > high and high > high

// Bearish FVG: Gap between low and current high

bearishFVG = high < low and low < low

🌏 Session-Based Trading

Why Sessions Matter for USDJPY

(see the generated image above)

Tokyo Session (00:00-09:00 UTC)

Highest volatility during first hour (00:00-01:00 UTC)

Average movement: 51-60 pips

Best for breakout strategies

London/NY Overlap (13:00-16:00 UTC)

Maximum liquidity and institutional participation

Tightest spreads and most reliable FVG formations

Optimal for continuation trades

Monday Premium Effect

USDJPY moves 120+ pips on Mondays due to weekend positioning

Enhanced FVG formation during session opens

📊 Strategy Components

(see the generated image above)

1. Fair Value Gap Detection

Identifies bullish and bearish FVGs automatically

Age limit: FVGs expire after 20 bars to avoid stale setups

Size filter: Minimum gap size to filter out noise

2. Session Filtering

Tokyo Open focus: Trades during first hour of Asian session

London/NY Overlap: Captures high-liquidity institutional flows

Weekend gap strategy: Enhanced signals on Monday opens

3. Volume Confirmation

Requires 1.5x average volume spike

Confirms institutional participation

Reduces false signals

4. Trend Alignment

50 EMA filter ensures trades align with higher timeframe trend

Long trades above EMA, short trades below

Prevents costly counter-trend trades

5. Risk Management

2:1 Risk/Reward minimum ensures profitability with 40%+ win rate

Percentage-based stops adapt to USDJPY volatility (0.3% default)

Configurable position sizing

🎯 Entry Conditions

(see the generated image above)

Long Entry (BUY)

✅ Bullish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price above 50 EMA (trend confirmation)

✅ Bullish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

Short Entry (SELL)

✅ Bearish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price below 50 EMA (trend confirmation)

✅ Bearish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

📈 Expected Performance

Backtesting Results (Based on Similar Strategies):

Win Rate: 44-59% (profitable due to high R:R ratio)

Average Winner: 60-90 pips during London/NY sessions

Average Loser: 30-40 pips (tight stops at FVG boundaries)

Risk/Reward: 2:1 minimum, often 3:1 during strong trends

Best Performance: Monday Tokyo opens and Wednesday London/NY overlaps

Why This Works for USDJPY:

90% correlation with US-Japan bond yield spreads

High volatility provides sufficient pip movement

Heavy institutional/central bank participation creates clear FVGs

Consistent volatility patterns across trading sessions

⚙️ Configurable Parameters

Session Settings:

Trade Tokyo Session (Enable/Disable)

Trade London/NY Overlap (Enable/Disable)

FVG Settings:

FVG Minimum Size (Filter small gaps)

Maximum FVG Age (20 bars default)

Show FVG Markers (Visual display)

Volume Settings:

Use Volume Filter (Enable/Disable)

Volume Multiplier (1.5x default)

Volume Average Period (20 bars)

Trend Settings:

Use Trend Filter (Enable/Disable)

Trend EMA Period (50 default)

Risk Management:

Risk/Reward Ratio (2.0 default)

Stop Loss Percentage (0.3% default)

🎨 Visual Indicators

🟡 Yellow Line: 50 EMA trend filter

🟢 Green Triangles: Long entry signals

🔴 Red Triangles: Short entry signals

🟢 Green Dots: Bullish FVG zones

🔴 Red Dots: Bearish FVG zones

🟦 Blue Background: Tokyo open session

🟧 Orange Background: London/NY overlap

📊 Recommended Settings

Optimal Timeframes:

Primary: 5-minute charts (scalping)

Secondary: 15-minute charts (swing trading)

Parameter Optimization:

Conservative: Stop Loss 0.2%, R:R 2:1, Volume 2.0x

Balanced: Stop Loss 0.3%, R:R 2:1, Volume 1.5x (default)

Aggressive: Stop Loss 0.4%, R:R 1.5:1, Volume 1.2x

Risk Management:

Maximum 1-2% of account per trade

Daily loss limit: Stop after 3-5 consecutive losses

Use fixed percentage position sizing

⚠️ Important Considerations

Avoid Trading During:

Major news events (BOJ interventions, NFP, FOMC)

Holiday periods with reduced liquidity

Low volatility Asian afternoon sessions

When US-Japan yield differential narrows sharply

Best Practices:

Limit to 2-3 trades per session maximum

Always respect the 50 EMA trend filter

Never risk more than planned per trade

Paper trade for 2-4 weeks before live implementation

Track performance by session and day of week

🚀 How to Use

Add the script to your USDJPY chart

Set timeframe to 5-minute or 15-minute

Adjust parameters based on your risk tolerance

Enable strategy alerts for automated notifications

Wait for visual signals (triangles) to appear

Enter trades according to your risk management rules

📚 Strategy Foundation

This strategy is based on:

Smart Money Concepts (SMC): Institutional order flow tracking

Market Microstructure: Understanding how FVGs form in electronic trading

Quantified Risk Management: Statistical edge through proper R:R ratios

Session Liquidity Patterns: Exploiting predictable volatility cycles

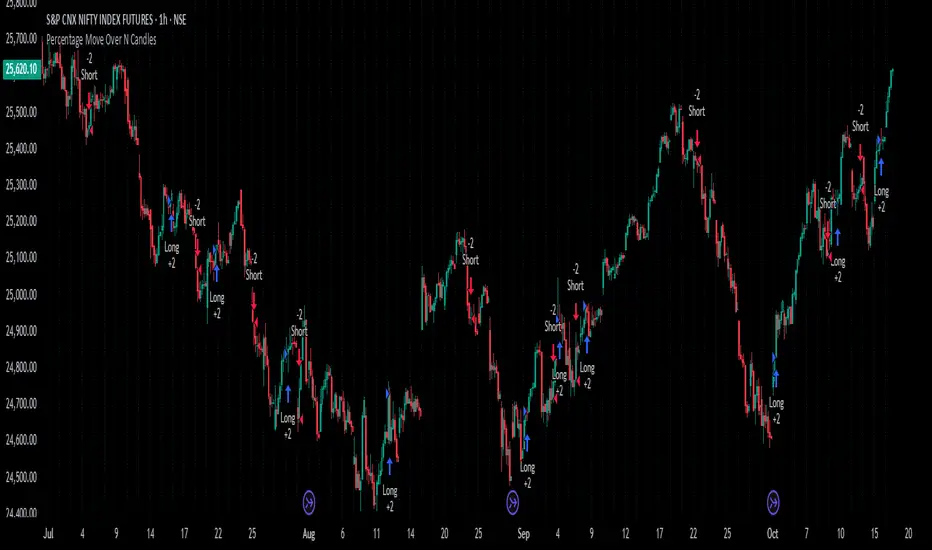

Percentage Move Over N CandlesThis strategy enters long/short trades if the price goes up/down by a certain defined percentage of the price, over a previous certain number of candles. Can be run on any time frame and on any instrument and alerts can be enabled.

Solana 4H RSI->MACD — Counter-Trend By TetradTetrad RSI→RSI Cross→MACD (Sequenced) — Counter-Trend (SL-Only)

Category: Market-neutral, counter-trend, sequenced entries

Timeframe default: Works on any TF; designed around 4H On Solana

Markets: Any (spot, perp, futures); parameterize to your asset

What it does

This strategy hunts reversals using a 3-step sequence on RSI and MACD, then optionally restricts entries by market regime and a price gate. It shows stop-loss lines only when hit (clean chart), and paints a Donchian glow for quick read of backdrop conditions.

Entry logic (sequenced)

1. RSI Extreme:

Long path activates when RSI < Oversold (default 27.5).

Short path activates when RSI > Overbought (default 74).

2. RSI Cross confirmation:

Long path: RSI crosses up back above the oversold level.

Short path: RSI crosses down back below the overbought level.

Each step has a max bar lookback so stale signals time out.

3. MACD Cross trigger:

Long: MACD line crosses above Signal.

Short: MACD line crosses below Signal.

→ When step 3 fires and gates are satisfied, a trade is entered.

Optional gates & filters

Regime Filter (Counter-Trend):

Longs allowed in **Range / Short Trend / Short Parabolic** regimes.

Shorts allowed in **Range / Long Trend / Long Parabolic** regimes.

Based on ADX/DI and ATR% intensity.

* Price Gate (Long Ceiling):

Toggle to **disable new longs above a chosen price (default 209.0 For SOL).

Useful for assets like SOL where you want longs only below a cap.

Exits / Risk

* Stop-Loss (% of entry):** default **14%**, toggleable.

* SL visualization:** plots a **thin dashed red line only on the bar it’s hit**.

* (No take-profit or time-based exit in this version—keep it pure to the sequence and regime. Add TP/time exits if desired.)

Visuals

* Donchian Glow (50): background band only (upper/lower lines hidden).

* Regime HUD: compact table (top-right) highlighting the active regime.

* Minimal marks: no entry/exit “arms” clutter; only SL-hit lines render.

Inputs (key)

* Core: RSI Length, Oversold/Overbought, MACD Fast/Slow/Signal.

* Sequence: Max bars from Extreme→RSI Cross and RSI Cross→MACD Cross.

* Regime: ADX Length, Trend/Parabolic thresholds, ATR length & floor.

* Stops: Enable/disable; SL %.

* Price Gate: Enable; Long ceiling price.

Alerts

Sequenced Long (CT): RSIhigh → RSI cross down → MACD bear cross.

## Notes & Tips

Designed for counter-trend fades that become trend rides. The regime filter helps avoid fading true parabolics and aligns entries with safer contexts.

The sequence is stateful (steps must occur in order). If a step times out, the path resets.

Works on lower TFs, but the 4H baseline reduces noise and over-trading.

Consider pairing with volume or structure filters if you want fewer but higher-conviction entries.

Past performance ≠ future results. **Educational use only. Not financial advice.

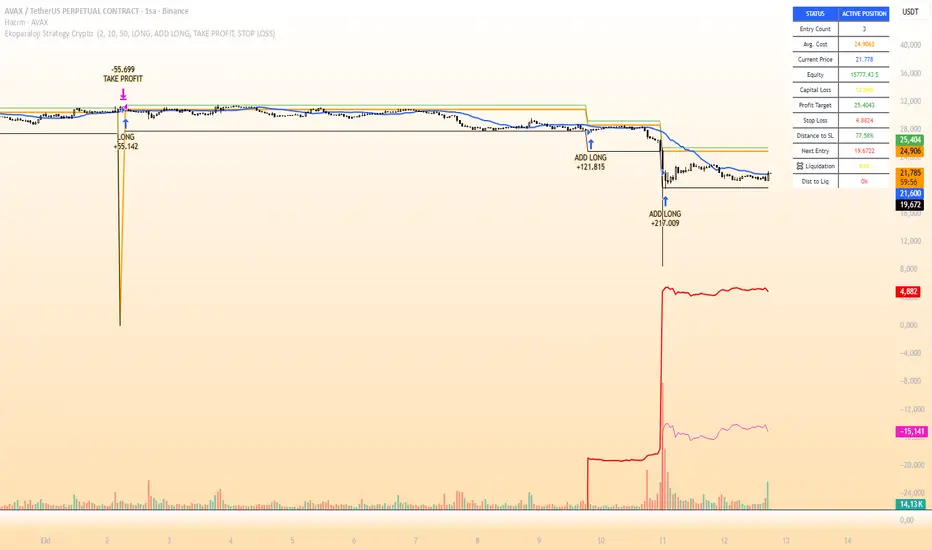

Ekoparaloji Cyrpto StrategyEkoparaloji Crypto Strategy - User Information Document

📊 Strategy Overview

This strategy provides long-term position management in cryptocurrency markets using the averaging down (pyramiding) technique. The basic logic is to controllably grow positions as prices decline and exit when specific profit targets are reached.

🎯 Key Features

✅ Automatic Entry System

Market direction is determined using a proprietary trend identification algorithm

Trades are only opened in uptrends

Initial position opens automatically when specific conditions are met

📈 Pyramiding Mechanism

New positions are automatically added as price decreases

Up to 10 positions can be added maximum

Each addition occurs at predetermined decline levels

Risk management through dynamic position sizing

💰 Profit and Loss Management

Take Profit: All positions close when the specified percentage above average cost is reached

Stop Loss (Optional): Protects a specified percentage of total capital

A certain ratio of available capital is used in each trade

📊 Visual Tracking System

The following information is displayed in real-time on the chart:

✅ Average cost level

✅ Profit target level

✅ Stop loss level (if active)

✅ Next pyramiding level

✅ Liquidation (capital reset) level

✅ Trend indicator

🛡️ Risk Management Features

1. Dynamic Capital Protection

Automatic exit when losses exceed a specified percentage of total capital

Complete loss scenario can be previewed through liquidation level calculation

2. Position Control System

Protection preventing multiple trades on the same bar

Double trigger prevention mechanism

Maximum position limit

3. Time Filter

Optional trading within a date range

Ideal for testing on historical data

📱 Information Panel

Information table always visible in the upper right corner of the strategy:

When Position is Open:

Number of active positions

Average cost

Current price

Total capital status

Capital loss percentage

Profit target

Stop loss level and distance

Next entry level

Liquidation level and distance

When No Position:

Market trend (Uptrend/Downtrend)

Ready to trade?

Reason for waiting

Initial position size

Target profit percentage

⚙️ Adjustable Parameters

Customizable by user:

💵 Capital Amount: Base amount to be used for each position

📊 Profit Target: Profit percentage at which to exit

🛑 Stop Loss: Usage status and maximum loss percentage

📅 Time Filter: Start and end dates for testing

💬 Trade Comments: Custom labels for each trade

📘 Understanding Leverage Effect

1. What is the Leverage Effect?

Although there's no real leverage in the spot market, when Capital Amount is increased, capital usage works like leverage:

Capital Amount 5% (1.0x): 100% capital usage with full pyramiding = All your money in trades

Capital Amount 10% (2.0x): 200% capital usage with full pyramiding = Attempting to open trades worth 2x your capital

Capital Amount 15% (3.0x): 300% capital usage with full pyramiding = Attempting to open trades worth 3x your capital

⚠️ IMPORTANT: If your capital runs out in the spot market, you cannot open new positions, therefore it's recommended to keep Capital Amount at 5% or below!

⚠️ Important Warnings

Pyramiding Risk: If price continues to decline, position grows and risk increases

Capital Requirements: Up to 10 positions can be added, requiring sufficient capital

Trend Dependency: Only works in uptrends

Backtest Results: Past performance is not a guarantee of future results

Real Trading Risks: Slippage, commissions, and market conditions can affect results

🎓 How to Use

Add the strategy to your chart

Adjust parameters according to your risk appetite

Examine past performance by backtesting

Optionally set up alerts to activate notifications

Test with paper trading first

This strategy is for educational purposes. Do your own research and only trade with capital you can afford to lose.

Disclaimer: This strategy is not financial advice. All investment decisions are the user's responsibility.

Happy trading! 📊

MAUL RSI Gaussian Filter MACD Gaussian Filter MACD — Strategy (with RSI Gate)

A momentum-first, chop-aware strategy built on a Gaussian-smoothed MACD with an optional RSI threshold filter. It looks for clean transitions in trend and ignores half-hearted wiggles around the zero line. You choose how signals are confirmed and whether shorts are allowed—no clutter, just deliberate entries and exits.

What it does (at a glance)

Confirms momentum using a smoothed MACD and a selectable signal mode.

Optional RSI gate to avoid low-quality breakouts.

Flexible source options (incl. Heikin-Ashi families) to match your charting style.

Long-only by default; shorts are an option.

Built-in alerts for entries/exits.

How to use

Add to chart and select your preferred signal mode.

Toggle the RSI gate and set your threshold to filter weak setups.

Forward-test across symbols/timeframes; then walk it into live with conservative sizing.

Notes

The parameters and internals are intentionally locked to protect IP and avoid over-fitting by casual copycats.

Works best on liquid symbols with consistent session structure.

Risk

Backtests are not a promise. Markets are noisy, slippage is real, and capital at risk should be sized accordingly. Use with sound risk management and a clear exit plan.

Ekoparaloji Strategy Crypto Ekoparaloji Crypto Strategy - User Information Document

📊 Strategy Overview

This strategy provides long-term position management in cryptocurrency markets using the averaging down (pyramiding) technique. The basic logic is to controllably grow positions as prices decline and exit when specific profit targets are reached.

🎯 Key Features

✅ Automatic Entry System

Market direction is determined using a proprietary trend identification algorithm

Trades are only opened in uptrends

Initial position opens automatically when specific conditions are met

📈 Pyramiding Mechanism

New positions are automatically added as price decreases

Up to 10 positions can be added maximum

Each addition occurs at predetermined decline levels

Risk management through dynamic position sizing

💰 Profit and Loss Management

Take Profit: All positions close when the specified percentage above average cost is reached

Stop Loss (Optional): Protects a specified percentage of total capital

A certain ratio of available capital is used in each trade

📊 Visual Tracking System

The following information is displayed in real-time on the chart:

✅ Average cost level

✅ Profit target level

✅ Stop loss level (if active)

✅ Next pyramiding level

✅ Liquidation (capital reset) level

✅ Trend indicator

🛡️ Risk Management Features

1. Dynamic Capital Protection

Automatic exit when losses exceed a specified percentage of total capital

Complete loss scenario can be previewed through liquidation level calculation

2. Position Control System

Protection preventing multiple trades on the same bar

Double trigger prevention mechanism

Maximum position limit

3. Time Filter

Optional trading within a date range

Ideal for testing on historical data

📱 Information Panel

Information table always visible in the upper right corner of the strategy:

When Position is Open:

Number of active positions

Average cost

Current price

Total capital status

Capital loss percentage

Profit target

Stop loss level and distance

Next entry level

Liquidation level and distance

When No Position:

Market trend (Uptrend/Downtrend)

Ready to trade?

Reason for waiting

Initial position size

Target profit percentage

⚙️ Adjustable Parameters

Customizable by user:

💵 Capital Amount: Base amount to be used for each position

📊 Profit Target: Profit percentage at which to exit

🛑 Stop Loss: Usage status and maximum loss percentage

📅 Time Filter: Start and end dates for testing

💬 Trade Comments: Custom labels for each trade

📘 Understanding Leverage Effect

1. What is the Leverage Effect?

Although there's no real leverage in the spot market, when Capital Amount is increased, capital usage works like leverage:

Capital Amount 5% (1.0x): 100% capital usage with full pyramiding = All your money in trades

Capital Amount 10% (2.0x): 200% capital usage with full pyramiding = Attempting to open trades worth 2x your capital

Capital Amount 15% (3.0x): 300% capital usage with full pyramiding = Attempting to open trades worth 3x your capital

⚠️ IMPORTANT: If your capital runs out in the spot market, you cannot open new positions, therefore it's recommended to keep Capital Amount at 5% or below!

⚠️ Important Warnings

Pyramiding Risk: If price continues to decline, position grows and risk increases

Capital Requirements: Up to 10 positions can be added, requiring sufficient capital

Trend Dependency: Only works in uptrends

Backtest Results: Past performance is not a guarantee of future results

Real Trading Risks: Slippage, commissions, and market conditions can affect results

🎓 How to Use

Add the strategy to your chart

Adjust parameters according to your risk appetite

Examine past performance by backtesting

Optionally set up alerts to activate notifications

Test with paper trading first

This strategy is for educational purposes. Do your own research and only trade with capital you can afford to lose.

Disclaimer: This strategy is not financial advice. All investment decisions are the user's responsibility.

SAN_Price Action BOS Strategy Price Action strategy with Break of structure including 20-30EMA crossover with perfect BUY/SELL alert is a beauty of this one

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

ORDER BLCOK custom strategy# OB Matrix Strategy - Documentation

**Version:** 1.0

**Author:** HPotter

**Date:** 31/07/2017

The **OB Matrix Strategy** is based on the identification of **bullish and bearish Order Blocks** and the management of conditional orders with multiple Take Profit (TP) and Stop Loss (SL) levels. It uses trend filters, ATR, and percentage-based risk management.

---

## 1. Main Parameters

### Strategy

- `initial_capital`: 50

- `default_qty_type`: percentage of capital

- `default_qty_value`: 10

### Money Management

- `rr_threshold`: minimum Risk/Reward threshold to open a trade

- `risk_percent`: percentage of capital to risk per trade (default 2%)

- `maxPendingBars`: maximum number of bars for a pending order

- `maxBarsOpen`: maximum number of bars for an open position

- `qty_tp1`, `qty_tp2`, `qty_tp3`: quantity percentages for multiple TPs

---

## 2. Order Block Identification

### Order Block Parameters

- `obLookback`: number of bars to identify an Order Block

- `obmode`: method to calculate the block (`Full` or `Breadth`)

- `obmiti`: method to determine block mitigation (`Close`, `Wick`, `Avg`)

- `obMaxBlocks`: maximum number of Order Blocks displayed

### Main Variables

- `bullBlocks`: array of bullish blocks

- `bearBlocks`: array of bearish blocks

- `last_bull_volume`, `last_bear_volume`: volume of the last block

- `dom_block`: dominant block type (Bullish/Bearish/None)

- `block_strength`: block strength (normalized volume)

- `price_distance`: distance between current price and nearest block

---

## 3. Visual Parameters

- `Width`: line thickness for swing high/low

- `amountOfBoxes`: block grid segments

- `showBorder`: show block borders

- `borderWidth`: width of block borders

- `showVolume`: display volume inside blocks

- `volumePosition`: vertical position of volume text

Customizable colors:

- `obHighVolumeColor`, `obLowVolumeColor`, `obBearHighVolumeColor`, `obBearLowVolumeColor`

- `obBullBorderColor`, `obBearBorderColor`

- `obBullFillColor`, `obBearFillColor`

- `volumeTextColor`

---

## 4. Screener Table

- `showScreener`: display the screener table

- `tablePosition`: table position (`Top Left`, `Top Right`, `Bottom Left`, `Bottom Right`)

- `tableSize`: table size (`Small`, `Normal`, `Large`)

The table shows:

- Symbol, Timeframe

- Type and status of Order Block

- Number of retests

- Bullish and bearish volumes

---

## 5. Trend Filters

- EMA as a trend filter (`emaPeriod`, default 223)

- `bullishTrend` if close > EMA

- `bearishTrend` if close < EMA

---

## 6. ATR and Swing Points

- ATR calculated with a customizable period (`atrLength`)

- Swing High/Low for SL/TP calculation

- `f_getSwingTargets` function to calculate SL and TP based on direction

---

## 7. Trade Logic

### Buy Limit on Bullish OB

- Conditions:

- New bullish block

- Uptrend

- RR > threshold (`rr_threshold`)

- SL: `bullishOBPrice * (1 - atr * atrMultiplier)`

- Multiple TPs: TP1 (50%), TP2 (80%), TP3 (100% max)

- Quantity calculation based on percentage risk

### Sell Limit on Bearish OB

- Conditions:

- New bearish block

- Downtrend

- RR > threshold (`rr_threshold`)

- SL: `bearishOBPrice * (1 + atr * atrMultiplier)`

- Multiple TPs: TP1 (50%), TP2 (80%), TP3 (100% max)

- Quantity calculation based on percentage risk

---

## 8. Order Management and Timeout

- Close pending orders after `maxPendingBars` bars

- Close open positions after `maxBarsOpen` bars

- Label management for open orders

---

## 9. Alert Conditions

- `bull_touch`: price inside maximum bullish volume zone

- `bear_touch`: price inside maximum bearish volume zone

- `bull_reject`: confirmation of bullish zone rejection

- `bear_reject`: confirmation of bearish zone rejection

- `new_bull`: new bullish block

- `new_bear`: new bearish block

---

## 10. Level Calculation

- Swing levels based on selected timeframe (`SelectPeriod`)

- `xHigh` and `xLow` for S1 and R1 calculation

- Levels plotted on chart

---

## 11. Take Profit / Stop Loss

- Extended horizontal lines (`extendBars`) to visualize TP and SL

- Customizable colors (`tpColor`, `slColor`)

---

## 12. Notes

- Complete script based on Pine Script v5

- Advanced graphical management with boxes, lines, labels

- Dynamically displays volumes and Order Blocks

- Integrated internal screener

---

### End of Documentation

High Volume Candle Breakouts [Engr. Havery]this plots high volume candles on your chart then when a breakout happens, it gives you an alert then place your limits on the active range. goodluck and have fun

Tight Entry Trend Engine Strategy═══════════════════════════════════════

TIGHT ENTRY TREND ENGINE

═══════════════════════════════════════

A breakout-based trend-following system designed to capture explosive

moves by entering at precise resistance/support breakouts with minimal

entry risk and massive profit potential.

⚠️ LOW WIN RATE, HIGH REWARD SYSTEM ⚠️

This is NOT a high win-rate strategy. Expect 25-35% winners, but

when it hits, winners are typically 10X+ larger than losers.

═══════════════════════════════════════

🎯 WHAT THIS SYSTEM DOES

═══════════════════════════════════════

The Tight Entry Trend Engine identifies powerful breakout opportunities

by detecting when price breaks through established trendlines with

confirmation from higher timeframe trends:

1. DYNAMIC TRENDLINE DETECTION (3 BANKS)

• Automatically draws support and resistance trendlines

• 3 separate "banks" capture short-term, medium-term, and long-term levels

• Each bank has configurable parameters (required pivot touch count,

angle limits, lengths)

2. BREAKOUT ENTRY TIMING

• Enters LONG when price breaks ABOVE resistance trendlines

• Enters SHORT when price breaks BELOW support trendlines

• Entry Alert occurs at the exact moment of breakout = "tight entry"

• Stop-loss placed just below/above the broken trendline (configurable)

3. HIGHER TIMEFRAME TREND FILTER

• Uses Hull Moving Average (HMA) on higher timeframe for trend following

• Auto-adjusts HTF based on your chart timeframe

• Optional filters prevent entries against major trend

• Optional "overextension" filter avoids buying parabolic moves

4. VOLATILITY-ADAPTIVE RISK MANAGEMENT

• Stop-loss calculated using Average True Range (ATR)

• Tighter stops = better R:R

• Profit targets adjust dynamically with volatility

• Breakeven stop moves automatically when in profit

• Extended profit targets when far from HTF trend

═══════════════════════════════════════

📊 HOW IT WORKS (METHODOLOGY)

═══════════════════════════════════════

STEP 1: TRENDLINE FORMATION

The system continuously scans for pivot highs and pivot lows to

construct trendlines. You control:

BANK 1 (Short-Term):

- Pivot Length: How many bars to look back for swing points

- Min Touches: How many pivots needed to form a line (default: 3)

- Max Length: How far back lines can reach (default: 180 bars)

- Angle Limits: Maximum steepness allowed for valid trendlines

- Tolerance: How close pivots must align to form horizontal lines

BANK 2 (Medium-Term):

- Slightly longer pivot periods for more significant levels

- Captures medium-term trend structure

- Default Max Length: 200 bars

BANK 3 (Long-Term):

- Focuses on major support/resistance zones

- Often uses horizontal levels (angled lines disabled by default)

- Default Max Length: 300 bars

The system draws RESISTANCE lines (red) above price and SUPPORT

lines (green) below price. These adapt in real-time as new pivots form.

STEP 2: BREAKOUT DETECTION

LONG SIGNALS:

- Price closes above a resistance trendline

- Higher timeframe trend is up (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

SHORT SIGNALS:

- Price closes below a support trendline

- Higher timeframe trend is down (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

The "tight" aspect: Because you're entering right at the trendline

break, your stop-loss can be placed very close (just below the

broken resistance for longs), creating exceptional risk/reward ratios.

STEP 3: POSITION SIZING

Choose between:

- Fixed $ Risk Per Trade: Risk same dollar amount every trade

- % Risk Per Trade: Risk percentage of current equity

Position size automatically calculated based on:

- Your risk amount

- Distance to stop-loss (ATR-based)

- Works with stocks, futures, crypto (auto-adjusts for contract multipliers)

STEP 4: EXIT MANAGEMENT

Multiple exit methods working together:

- PROFIT TARGET: Exits when profit reaches 100x your risk

- EXTENDED PROFIT: Earlier exit (80R) when very far from HTF trend

- STOP LOSS: Fixed ATR-based stop below entry

- HTF TREND EXIT: Exits when price crosses below HTF trend with profit

- BREAKEVEN PULLBACK: Exits if profit drops below 0.6R after reaching breakeven

- PARTIAL PROFITS: Optional - take partial profits at specified R-multiple

═══════════════════════════════════════

🔧 KEY COMPONENTS EXPLAINED

═══════════════════════════════════════

HULL MOVING AVERAGE (HMA)

A smoothed moving average that reduces lag compared to traditional

MAs. The system uses HMA on a higher timeframe to determine the

dominant trend direction. You can choose:

- Auto HTF: System picks appropriate HTF based on your chart timeframe

- Manual HTF: You specify the higher timeframe

AVERAGE TRUE RANGE (ATR)

Measures current market volatility. Used for:

- Stop-loss distance (tighter when volatility low)

- Profit targets (larger when volatility high)

- Position sizing (smaller positions in volatile conditions)

- Breakeven trigger distance

TRENDLINE ANGLE FILTERING

Each trendline bank has angle limits to ensure quality:

- Resistance lines: Max downward/upward slope allowed

- Support lines: Max downward/upward slope allowed

- Angles automatically adjust based on current volatility

- Prevents overly steep/unreliable trendlines

SENSITIVITY CONTROL

One master slider adjusts multiple parameters:

- Trendline detection sensitivity

- HTF MA length

- Exit timing

- Auto-adjusts for daily+ timeframes (60% increase)

═══════════════════════════════════════

⚙️ WHAT YOU SEE ON YOUR CHART

═══════════════════════════════════════

TRENDLINES:

✓ Red resistance lines above price

✓ Green support lines below price

✓ Orange broken lines (past breakouts)

✓ Lines extend to show current levels

HTF TREND:

✓ Thick colored line showing higher timeframe trend

✓ Color gradient: Red (bearish) → Orange → Yellow → Green (bullish)

✓ 250-bar smoothed curve for visual clarity

ENTRY/EXIT SIGNALS:

✓ Small green dot below bar = Long entry

✓ Small red dot above bar = Short entry

✓ Small red dot above = Long exit

✓ Small black dot below = Short exit

OPTIONAL DETAILED LABELS:

✓ Bank number that triggered entry (Bank 1, 2, or 3)

✓ Exit reason (Profit Target, Stop Loss, HTF Exit, etc.)

✓ Partial profit notifications

POSITION TRACKING:

✓ Yellow dashed line at entry price (extends right)

✓ Green/red fill showing current profit/loss zone

✓ Lime arrows at top = Currently in long position

✓ Red arrows at bottom = Currently in short position

✓ Gray background = No position (flat)

STATS TABLE (Top Right):

✓ Current position (LONG/SHORT/FLAT)

✓ Risk per trade ($ or %)

✓ Entry price

✓ Unrealized P/L in dollars

✓ P/L in R-multiples (how many R's profit/loss)

✓ Average winner/loser R ($ mode) OR CAGR (% mode)

═══════════════════════════════════════

📈 OPTIMAL USAGE

═══════════════════════════════════════

BEST ASSETS:

- NASDAQ:QQQ on 1-hour (reg) chart ⭐ (PRIMARY OPTIMIZATION)

- Strong trending stocks: NVDA, AAPL, TSLA, MSFT, GOOGL, AMZN

- High volatility tech stocks

- Crypto: BTC, ETH

- Any liquid asset with clear trends and momentum (GOLD)

AVOID:

- Low volatility stocks

- Ranging/choppy markets

- Penny stocks or illiquid assets

- Assets without clear directional movement

BEST TIMEFRAMES:

- PRIMARY: 1-hour charts (optimal for QQQ)

- ALSO EXCELLENT: 2H, 4H, 8H

- WORKS: 15min, 30min (only momentum leaders, more noise)

- WORKS WITH ADJUSTMENTS: 1D, 2D (decrease trendline pivot lengths)

═══════════════════════════════════════

📊 BACKTEST RESULTS (QQQ 1H (Reg hours), 1999-2024)

═══════════════════════════════════════

The system showed on NASDAQ:QQQ 1-hour timeframe (regular hours):

- Total Return: 1,100,000%+ over 24 years

- Total Trades: 500+

- Win Rate: ~20-24% (LOW - this is by design!)

- Average Winner: 8-15% gain

- Average Loser: 2-4% loss

- Win/Loss Ratio: 10:1 (winners much bigger than losers)

- Profit Factor: 3+

- Max Drawdown: 45-50%

- Risk per trade: 3% of capital

KEY INSIGHT: This is a LOW WIN RATE, HIGH REWARD system. You will

lose more trades than you win, but the few winners are so large

they more than compensate for many small losses.

IMPORTANT: These are backtested results using optimal parameters

on historical data. Real trading results will vary based on:

- Your execution and timing

- Slippage and commissions

- Your emotional discipline

- Market conditions during your trading period

═══════════════════════════════════════

🎓 WHO IS THIS FOR?

═══════════════════════════════════════

IDEAL FOR:

✓ Swing traders comfortable holding winners for longer period

✓ Part-time traders (1H = check 2-3x per day)

✓ Traders seeking exceptional risk/reward ratios

✓ Those comfortable with low win rates if winners are huge

✓ Technical analysis enthusiasts

✓ Breakout traders

✓ Trend followers

═══════════════════════════════════════

🚀 GETTING STARTED - STEP BY STEP

═══════════════════════════════════════

STEP 1: APPLY TO YOUR CHART

- Search "Tight Entry Trend Engine" in indicators

- Click to apply to your chart

- Trendlines and HTF line will appear immediately

STEP 2: CHOOSE YOUR SETTINGS

For BEGINNERS - Use These Settings First:

1. Trade Direction & Filters:

• ENABLE LONGS: ✓ ON

• ENABLE SHORTS: ✗ OFF (start with longs only)

• Sensitivity: 1.0 (default)

• HTF Trend Entry Filter: ✓ ON (safer entries)

• Block Entries When Overextended: ✓ ON (avoid parabolic tops)

2. Position Sizing & Risk:

• Position Sizing: "Per Risk"

• RISK Type: "$ Per Trade"

• Risk Amount: $200 (or 1-3% of your account)

3. Visual Settings:

• Show Support Lines: ✗ OFF (unless trading shorts)

• Show Detailed Entry/Exit Labels: ✓ ON

• Show Stats Table: ✓ ON

• Show Entry Line & P/L Fill: ✓ ON

4. Leave everything else at DEFAULT for now

STEP 3: UNDERSTAND WHAT YOU SEE

When trendlines appear:

- RED lines above = Resistance (watch for price breaking UP through these)

- GREEN lines below = Support (watch for price breaking DOWN)

- When price breaks a red line = Potential LONG entry

- When price breaks a green line = Potential SHORT entry

The HTF trend line (thick colored):

- Green/lime = Strong uptrend (favorable for longs)

- Red = Strong downtrend (favorable for shorts if enabled)

- Orange/yellow = Transitioning

STEP 4: OBSERVE SIGNALS

- Small GREEN dot below bar = System entered LONG

- Small RED dot above bar = System exited LONG

- Check the label to see which "Bank" triggered (Bank 1, 2, or 3)

- Watch the yellow entry line and colored fill show your P/L

STEP 5: PAPER TRADE FIRST

- Use TradingView's paper trading feature

- Watch how signals perform on YOUR chosen asset

- Understand the win rate will be LOW (20-35%)

- Verify that winners are indeed much larger than losers

- Test for at least 20-30 signals before going live

STEP 6: OPTIMIZE FOR YOUR ASSET (OPTIONAL)

If default settings aren't working well:

For FASTER signals (more trades):

- Reduce Pivot Length 1 to 3-4

- Reduce Max Length 1 to 120-150

- Increase Sensitivity to 1.2-1.5

For SLOWER signals (higher quality):

- Increase Pivot Length 1 to 7-10

- Increase Max Length 1 to 250+

- Decrease Sensitivity to 0.7-0.9

For DAILY timeframes:

- Increase all Pivot Lengths by 30-50%

- Increase all Max Lengths significantly

- Sensitivity: 0.6-0.8

═══════════════════════════════════════

⚙️ ADVANCED SETTINGS EXPLAINED

═══════════════════════════════════════

TRENDLINE BANK SETTINGS:

Each bank (1, 2, 3) has these parameters:

- Min Touches: Minimum pivots to form a line

- Lower (2) = More lines, earlier detection

- Higher (4+) = Fewer lines, higher quality

- Pivot Length: Lookback for swing points

- Lower (3-5) = Reacts to recent price action

- Higher (10+) = Only major swing points

- Max Length: How old a trendline can be

- Shorter (100-150) = Only recent lines

- Longer (300+) = Include historical levels

- Tolerance: Alignment strictness for horizontal lines

- Lower (3.0-3.5) = Very strict horizontal

- Higher (4.5+) = More forgiving alignment

- Allow Angled Lines: Enable diagonal trendlines

- ON = Catches sloped support/resistance

- OFF = Only horizontal levels

- Angle Limits: Maximum steepness allowed

- Lower (1-2) = Only gentle slopes

- Higher (4-6) = Accept steeper angles

- Automatically adjusts for volatility

ATR MULTIPLIERS:

- STOP LOSS ATR (0.6): Distance to stop-loss

- Lower (0.4-0.5) = Tighter stops, stopped out more