Hierarchical + K-Means Clustering Strategy===== USER GUIDE =====

Hierarchical + K-Means Clustering Strategy

OVERVIEW:

This strategy combines hierarchical clustering and K-means algorithms to analyze market volatility patterns

and generate trading signals. It uses a modified SuperTrend indicator with ATR-based volatility clustering

to identify potential trend changes and market conditions.

KEY FEATURES:

- Advanced volatility analysis using hierarchical clustering and K-means algorithms

- Modified SuperTrend indicator for trend identification

- Multiple filter options including moving average and ADX trend strength

- Volume-based exit mechanism to protect profits

- Customizable appearance settings

SETTINGS EXPLANATION:

1. SuperTrend Settings:

- ATR Length: Period for ATR calculation (default: 11)

- SuperTrend Factor: Multiplier for ATR to determine trend bands (default: 3)

2. Hierarchical Clustering Settings:

- Training Data Length: Number of bars used for clustering analysis (default: 200)

3. Appearance Settings:

- Transparency 1 & 2: Control the opacity of trend lines and fills

- Bullish/Bearish Color: Colors for uptrend and downtrend visualization

4. Time Settings:

- Start Year/Month: Define when the strategy should start executing trades

5. Filter Settings:

- Moving Average Filter: Uses SMA to filter trades (only enter when price is on correct side of MA)

- Trend Strength Filter: Uses ADX to ensure trades are taken in strong trend conditions

6. Volume Stop Loss Settings:

- Volume Ratio Threshold: Controls sensitivity of volume-based exits

- Monitoring Delay Bars: Number of bars to wait before monitoring volume for exit signals

HOW TO USE:

1. Apply the indicator to your chart

2. Adjust settings according to your trading preferences and timeframe

3. Long signals appear when price crosses above the SuperTrend line (▲k marker)

4. Short signals appear when price crosses below the SuperTrend line (▼k marker)

5. The strategy automatically manages exits based on volume balance conditions

INTERPRETATION:

- Green line/area: Bullish trend - consider long positions

- Red line/area: Bearish trend - consider short positions

- Yellow line: Moving average for additional trend confirmation

- Volume balance exits occur when buying/selling pressure equalizes

RECOMMENDED TIMEFRAMES:

This strategy works best on 1H, 4H, and daily charts for most markets.

For highly volatile assets, shorter timeframes may also be effective.

RISK MANAGEMENT:

Always use proper position sizing and consider setting additional stop losses

beyond the strategy's built-in exit mechanisms.

===== END OF USER GUIDE =====

Поиск скриптов по запросу "algo"

Profit Hunter @DaviddTechProfit Hunter @DaviddTech is an advanced multi-strategy indicator designed to give traders a significant edge in identifying high-probability trading opportunities across all market conditions. By combining the power of T3 adaptive moving averages, ADX-based trend strength analysis, SuperTrend trailing stops, and dynamic support/resistance detection, this indicator delivers a complete trading system in one powerful package.

## 📊 Recommended Usage

Timeframes: Most effective on 1H, 4H, and Daily charts for swing trading; 5M and 15M for day trading

Markets: Works across all markets including Forex, Crypto, Indices, and Stocks

Setup Guidelines: Look for T3 crossovers with strong ADX readings (>25) coinciding with breakout signals (yellow dots/red crosses) near key support/resistance levels for highest probability entries

## 🔥 Key Features:

### T3 Adaptive Trend Detection:

Utilizes premium T3 adaptive indicators instead of standard EMAs for superior smoothing and accuracy

Dynamic color-shifting cloud formation between fast and slow T3 lines reveals immediate trend direction

Proprietary transparency algorithm intensifies cloud colors during strong trends based on real-time ADX readings

### Advanced Support & Resistance Mapping:

Automatically identifies and marks key market structure levels during T3 crossovers

Dynamic horizontal level plotting with optional extension for monitoring future price interactions

Intelligent level validation - converts to dotted lines when price breaks through, maintaining visual clarity

### SuperTrend Trailing Stoploss System:

Professional-grade white trailing stop indicator adapts to market volatility using ATR calculations

Generates precise entry and exit signals with optional buy/sell labels at critical reversal points

Visual trend state highlighting for immediate assessment of current market position

### Breakout Detection & Confirmation:

Sophisticated dual-algorithm breakout system combining Bollinger Bands and Keltner Channels

Visual breakout alerts with yellow dots (bullish) and red crosses (bearish) for instant pattern recognition

Validates breakouts against T3 trend direction to minimize false signals

### Alpha Edge Color System:

Utilizes DaviddTech's signature color scheme with bullish green and bearish pink

Revolutionary transparency algorithm translates ADX readings into precise visual intensity

Higher ADX values produce more vivid colors, instantly communicating trend strength without additional indicators

## 💰 Trading Applications:

Alpha Discovery: Identify emerging trends before the majority of market participants

Precision Entry/Exit: Use SuperTrend signals combined with support/resistance levels for optimal trade execution

Risk Management: Set stops based on the white trailing stoploss line for mathematically-optimized protection

Trend Confirmation: Validate setups using the T3 cloud direction and ADX-based intensity

Breakout Trading: Capture explosive moves with confirmed Bollinger/Keltner breakout signals

Swing Position Management: Monitor extended support/resistance levels for multi-day positioning

## ✨ Strategy Example

As shown in the chart image, ideal entries occur when:

The T3 cloud turns bullish (green) or bearish (pink) with strong color intensity

A yellow dot (bullish) or red cross (bearish) breakout signal appears

Price respects the white SuperTrend line as support/resistance

The trade aligns with key horizontal support/resistance levels identified by the indicator

## 📝 Attribution

This indicator builds upon and enhances concepts from:

Market Trend Levels Detector by BigBeluga (support/resistance detection framework)

T3 indicator implementation by DaviddTech (adaptive moving average system)

Average Directional Index (ADX) methodology for trend strength measurement

Profit Hunter @DaviddTech represents the culmination of advanced technical analysis methodologies in one seamless system.

Boilerplate Configurable Strategy [Yosiet]This is a Boilerplate Code!

Hello! First of all, let me introduce myself a little bit. I don't come from the world of finance, but from the world of information and communication technologies (ICT) where we specialize in data processing with the aim of automating it and eliminating all human factors and actors in the processes. You could say that I am an algotrader.

That said, in my journey through trading in recent years I have understood that this world is often shown to be incomplete. All those who want to learn about trading only end up learning a small part of what it really entails, they only seek to learn how to read candlesticks. Therefore, I want to share with the entire community a fraction of what I have really understood it to be.

As a computer scientist, the most important thing is the data, it is the raw material of our work and without data you simply cannot do anything. Entropy is simple: Data in -> Data is transformed -> Data out.

The quality of the outgoing data will directly depend on the incoming data, there is no greater mystery or magic in the process. In trading it is no different, because at the end of the day it is nothing more than data. As we often say, if garbage comes in, garbage comes out.

Most people focus on the results only, on the outgoing data, because in the end we all want the same thing, to make easy money. Very few pay attention to the input data, much less to the process.

Now, I am not here to delude you, because there is no bigger lie than easy money, but I am here to give you a boilerplate code that will help you create strategies where you only have to concentrate on the quality of the incoming data.

To the Point

The code is a strategy boilerplate that applies the technique that you decide to customize for the criteria for opening a position. It already has the other factors involved in trading programmed and automated.

1. The Entry

This section of the boilerplate is the one that each individual must customize according to their needs and knowledge. The code is offered with two simple, well-known strategies to exemplify how the code can be reused for your own benefits.

For the purposes of this post on tradingview, I am going to use the simplest of the known strategies in trading for entries: SMA Crossing

// SMA Cross Settings

maFast = ta.sma(close, length)

maSlow = ta.sma(open, length)

The Strategy Properties for all cases published here:

For Stock TSLA H1 From 01/01/2025 To 02/15/2025

For Crypto XMR-USDT 30m From 01/01/2025 To 02/15/2025

For Forex EUR-USD 5m From 01/01/2025 To 02/15/2025

But the goal of this post is not to sell you a dream, else to show you that the same Entry decision works very well for some and does not for others and with this boilerplate code you only have to think of entries, not exits.

2. Schedules, Days, Sessions

As you know, there are an infinite number of markets that are susceptible to the sessions of each country and the news that they announce during those sessions, so the code already offers parameters so that you can condition the days and hours of operation, filter the best time parameters for a specific market and time frame.

3. Data Filtering

The data offered in trading are numerical series presented in vectors on a time axis where an endless number of mathematical equations can be applied to process them, with matrix calculation and non-linear regressions being the best, in my humble opinion.

4. Read Fundamental Macroeconomic Events, News

The boilerplate has integration with the tradingview SDK to detect when news will occur and offers parameters so that you can enable an exclusion time margin to not operate anything during that time window.

5. Direction and Sense

In my experience I have found the peculiarity that the same algorithm works very well for a market in a time frame, but for the same market in another time frame it is only a waste of time and money. So now you can easily decide if you only want to open LONG, SHORT or both side positions and know how effective your strategy really is.

6. Reading the money, THE PURPOSE OF EVERYTHING

The most important section in trading and the reason why many clients usually hire me as a financial programmer, is reading and controlling the money, because in the end everyone wants to win and no one wants to lose. Now they can easily parameterize how the money should flow and this is the genius of this boilerplate, because it is what will really decide if an algorithm (Indicator: A bunch of math equations) for entries will really leave you good money over time.

7. Managing the Risk, The Ego Destroyer

Many trades, little money. Most traders focus on making money and none of them know about statistics and the few who do know something about it, only focus on the winrate. Well, with this code you can unlock what really matters, the true success criteria to be able to live off of trading: Profit Factor, Sortino Ratio, Sharpe Ratio and most importantly, will you really make money?

8. Managing Emotions

Finally, the main reason why many lose money is because they are very bad at managing their emotions, because with this they will no longer need to do so because the boilerplate has already programmed criteria to chase the price in a position, cut losses and maximize profits.

In short, this is a boilerplate code that already has the data processing and data output ready, you only have to worry about the data input.

“And so the trader learned: the greatest edge was not in predicting the storm, but in building a boat that could not sink.”

DISCLAIMER

This post is intended for programmers and quantitative traders who already have a certain level of knowledge and experience. It is not intended to be financial advice or to sell you any money-making script, if you use it, you do so at your own risk.

Midnight Opening Ranges[TDL]Midnight Opening Range Indicator for TradingView

Description:

The Midnight Opening Range Indicator as taught by Micheal J. Huddleston is a powerful tool designed for traders who want to analyze price action during the critical midnight to 00:30 timeframe. This indicator highlights the opening range for both the current day and previous days, providing valuable insights into market behavior during this specific period. It also calculates and displays deviations from the opening range, as well as allows for custom opening prices to be set, making it highly adaptable to your trading strategy.

Key Features:

Today's Opening Range (00:00 - 00:30):

The indicator plots the high and low of the price range between 00:00 and 00:30 for the current day.

This range is highlighted on the chart, making it easy to identify the initial market movement and potential support/resistance levels.

Previous Days' Opening Ranges:

The indicator also displays the opening ranges for previous days, allowing you to how price reacts off of previous days ranges not just todays.

This feature helps in identifying patterns or recurring behaviors in the market in which price uses this range and previous days ranges throughout the trading day.

Deviations from the Opening Range:

The indicator calculates and plots deviations from the opening range, both above and below the high and low of the range.

These deviations can be used to identify potential breakout or reversal points, giving you an edge in anticipating market moves.

Custom Opening Prices:

The indicator allows you to set custom opening prices, which can be useful if you want to analyze the market based on a specific reference point rather than the default midnight opening.

This feature is particularly useful for traders who follow alternative trading sessions or have specific entry criteria.

Customizable Visuals:

The indicator offers customizable colors and styles for the opening range, deviations, and custom opening prices, allowing you to tailor the visual representation to your preferences.

How to Use:

Identify Key Levels: Use the highlighted opening range to identify key support and resistance levels for the day.

Monitor Deviations: Watch for price movements beyond the opening range deviations to spot potential breakouts or reversals.

Previous Range Data: Use previous days to identify areas of potential AMD.

Set Custom Prices: Adjust the custom opening price to align with your trading strategy or session preferences.

Ideal For:

Day Traders: Perfect for traders who focus on the early hours of the market to capture initial momentum.

Swing Traders: Useful for identifying key levels that could influence price action over several days.

Algorithmic Traders: Can be integrated into automated trading systems to trigger trades based on the opening range and deviations.

Conclusion:

The Midnight Opening Range Indicator is an essential tool for any trader looking to gain an edge in the market by focusing on the critical midnight to 00:30 timeframe. With its ability to highlight opening ranges, calculate deviations, and accommodate custom opening prices, this indicator provides a comprehensive view of market behavior during this pivotal period. Whether you're a day trader, swing trader, or algorithmic trader, this indicator will help you make more informed trading decisions.

Naive Bayes Candlestick Pattern Classifier v1.1 BETAAn intermezzo on why i made this script publication..

A : Candlestick Pattern took hours to backtest, why not using Machine Learning techniques?

B : Machine Learning, no that's gonna be really heavy bro!

A : Not really, because we use Naive Bayes.

B : The simplest, yet powerful machine learning algorithm to separate (a.k.a classify) multivariate data.

----------------------------------------------------------------------------------------------------------------------

Hello, everyone!

After deep research in extracting meaningful information from the market, I ended up building this powerful machine learning indicator based on the evolution of Bayesian Statistics. This indicator not only leverages the simplicity of Naive Bayes but also extends its application to candlestick pattern analysis, making it an invaluable tool for traders who are looking to enhance their technical analysis without spending countless hours manually backtesting each pattern on each market!.

What most interesting part is actually after learning all of likely useless methods like fibonacci, supply and demand, volume profile, etc. We always ended up back to basic like support and resistance and candlestick patterns, but with a slight twist on strategy algorithm design and statistical approach. Thus, the only reason why i made this, because i exactly know that you guys will ended up in this position as time goes by.

The essence of this indicator lies in its ability to automate the recognition and statistical evaluation of various candlestick patterns. Traditionally, traders have relied on visual inspection and manual backtesting to determine the effectiveness of patterns like Bullish Engulfing, Bearish Engulfing, Harami variations, Hammer formations, and even more complex multi-candle patterns such as Three White Soldiers, Three Black Crows, Dark Cloud Cover, and Piercing Pattern. However, these conventional methods are both time-consuming and prone to subjective bias.

To address these challenges, I employed Naive Bayes—a probabilistic classifier that, despite its simplicity, offers robust performance in various domains. Naive Bayes assumes that each feature is independent of the others given the class label, which, although a strong assumption, works remarkably well in practice, especially when the dataset is large like market data and the feature space is high-dimensional. In our case, each candlestick pattern acts as a feature that can be statistically evaluated based on its historical performance. The indicator calculates a probability that a given pattern will lead to a price reversal, by comparing the pattern’s close price to the highest or lowest price achieved in a lookahead window.

One of the standout features of this script is its flexibility. Each candlestick pattern is not only coded into the system but also comes with individual toggles to enable or disable them based on your trading strategy. This means you can choose to focus on single-candle patterns like Bullish Engulfing or more complex multi-candle formations such as Three White Soldiers, without modifying the core code. The built-in customization options allow you to adjust colors and labels for each pattern, giving you the freedom to tailor the visual output to your preference. This level of customization ensures that the indicator integrates seamlessly into your existing TradingView setup.

Moreover, the indicator isn’t just about pattern recognition—it also incorporates outcome-based learning. Every time a pattern is detected, it looks ahead a predefined number of bars to evaluate if the expected reversal actually materialized. This outcome is then stored in arrays, and over time, the script dynamically calculates the probability of success for each pattern. These probabilities are presented in a real-time updating table on your chart, which shows not only the percentage probability but also the count of historical occurrences. With this information at your fingertips, you can quickly gauge the reliability of each pattern in your chosen market and timeframe.

Another significant advantage of this approach is its speed and efficiency. While more complex machine learning models like neural networks might require heavy computational resources and longer training times, the Naive Bayes classifier in this script is lightweight, instantaneous and can be updated on the fly with each new bar. This real-time capability is essential for modern traders who need to make quick decisions in fast-paced markets.

Furthermore, by automating the process of backtesting, the indicator frees up your time to focus on other aspects of trading strategy development. Instead of manually analyzing hundreds or even thousands of candles, you can rely on the statistical power of Naive Bayes to provide you with insights on which patterns are most likely to result in profitable moves. This not only enhances your efficiency but also helps to eliminate the cognitive biases that often plague manual analysis.

In summary, this indicator represents a fusion of traditional candlestick analysis with modern machine learning techniques. It harnesses the simplicity and effectiveness of Naive Bayes to deliver a dynamic, real-time evaluation of various candlestick patterns. Whether you are a seasoned trader looking to refine your technical analysis or a beginner eager to understand market dynamics, this tool offers a powerful, customizable, and efficient solution. Welcome to a new era where advanced statistical methods meet practical trading insights—happy trading and may your patterns always be in your favor!

Note : On this current released beta version, you must manually adjust reversal percentage move based on each market. Further updates may include automated best range detection and probability.

permutation█ OVERVIEW

This library provides functions for generating permutations of string or float arrays, using an iterative approach where pine has no recursion. It supports allowing/limiting duplicate elements and handles large result sets by segmenting them into manageable chunks within custom Data types. The most combinations will vary, but the highest is around 250,000 unique combinations. depending on input array values and output length. it will return nothing if the input count is too low.

█ CONCEPTS

This library addresses two key challenges in Pine Script:

• Recursion Depth Limits: Pine has limitations on recursion depth. This library uses an iterative, stack-based algorithm to generate permutations, avoiding recursive function calls that could exceed these limits.

• Array Size Limits: Pine arrays have size restrictions. This library manages large permutation sets by dividing them into smaller segments stored within a custom Data or DataFloat type, using maps for efficient access.

█ HOW TO USE

1 — Include the Library: Add this library to your script using:

import kaigouthro/permutation/1 as permute

2 — Call the generatePermutations Function:

stringPermutations = permute.generatePermutations(array.from("a", "b", "c"), 2, 1)

floatPermutations = permute.generatePermutations(array.from(1.0, 2.0, 3.0), 2, 1)

• set : The input array of strings or floats.

• size : The desired length of each permutation.

• maxDuplicates (optional): The maximum allowed repetitions of an element within a single permutation. Defaults to 1.

3 — Access the Results: The function returns a Data (for strings) or DataFloat (for floats) object. These objects contain:

• data : An array indicating which segments are present (useful for iterating).

• segments : A map where keys represent segment indices and values are the actual permutation data within that segment.

Example: Accessing Permutations

for in stringPermutations.segments

for in currentSegment.segments

// Access individual permutations within the segment.

permutation = segmennt.data

for item in permutation

// Use the permutation elements...

█ TYPES

• PermutationState / PermutationStateFloat : Internal types used by the iterative algorithm to track the state of permutation generation.

• Data / DataFloat : Custom types to store and manage the generated permutations in segments.

█ NOTES

* The library prioritizes handling potentially large permutation sets. 250,000 i about the highest achievable.

* The segmentation logic ensures that results are accessible even when the total number of permutations exceeds Pine's array size limits.

----

Library "permutation"

This library provides functions for generating permutations of user input arrays containing either strings or floats. It uses an iterative, stack-based approach to handle potentially large sets and avoid recursion limitation. The library supports limiting the number of duplicate elements allowed in each permutation. Results are stored in a custom Data or DataFloat type that uses maps to segment large permutation sets into manageable chunks, addressing Pine Script's array size limitations.

generatePermutations(set, size, maxDuplicates)

> Generates permutations of a given size from a set of strings or floats.

Parameters:

set (array) : (array or array) The set of strings or floats to generate permutations from.

size (int) : (int) The size of the permutations to generate.

maxDuplicates (int) : (int) The maximum number of times an element can be repeated in a permutation.

Returns: (Data or DataFloat) A Data object for strings or a DataFloat object for floats, containing the generated permutations.

stringPermutations = generatePermutations(array.from("a", "b", "c"), 2, 1)

floatPermutations = generatePermutations(array.from(1.0, 2.0, 3.0), 2, 1)

generatePermutations(set, size, maxDuplicates)

Parameters:

set (array)

size (int)

maxDuplicates (int)

PermutationState

PermutationState

Fields:

data (array) : (array) The current permutation being built.

index (series int) : (int) The current index being considered in the set.

depth (series int) : (int) The current depth of the permutation (number of elements).

counts (map) : (map) Map to track the count of each element in the current permutation (for duplicates).

PermutationStateFloat

PermutationStateFloat

Fields:

data (array) : (array) The current permutation being built.

index (series int) : (int) The current index being considered in the set.

depth (series int) : (int) The current depth of the permutation (number of elements).

counts (map) : (map) Map to track the count of each element in the current permutation (for duplicates).

Data

Data

Fields:

data (array) : (array) Array to indicate which segments are present.

segments (map) : (map) Map to store permutation segments. Each segment contains a subset of the generated permutations.

DataFloat

DataFloat

Fields:

data (array) : (array) Array to indicate which segments are present.

segments (map) : (map) Map to store permutation segments. Each segment contains a subset of the generated permutations.

Shannon Entropy Volatility AnalyzerThis algorithm aims to measure market uncertainty or volatility using a Shannon entropy-based approach. 🔄📊

Entropy is a measure of disorder or unpredictability, and here we use it to evaluate the structure of price returns within a defined range of periods (window length). 🧩⏳ Thus, the goal is to detect changes to identify conditions of high or low volatility. 🔍⚡

What we seek with Shannon's formula in this algorithm is to measure market uncertainty or volatility through dynamic entropy. This measure helps us understand how unpredictable price behavior is over a given period, which is key to making informed decisions. 📈🧠

Through this formula, we calculate the level of disorder or dispersion in price returns based on their probability of occurrence, enabling us to identify moments of high or low volatility. 💡💥

Shannon Entropy Calculation 📏

• Uses probabilities to measure uncertainty in returns. 🎲

• Entropy is normalized on a scale of 0 to 100, where:

o High Entropy: Unpredictable movements (high uncertainty). ⚠️💥

•

o Low Entropy: Structured movements (low uncertainty). 📉🔒

•

• With probabilities, we measure the level of dispersion or unpredictability of returns using Shannon's entropy formula. 📊🔍

________________________________________

Indicator Usefulness 🛠️

• Identify High Volatility: When the market is unpredictable, the indicator signals "High Uncertainty." ⚡🔮

• Detect Market Stability: When the market is more predictable and structured, the indicator highlights "Low Uncertainty." 🔒🧘♂️

• Neutral Zones: Helps monitor markets without extreme conditions, enabling safer entry or exit opportunities. ⚖️🚶♂️

________________________________________

Uncertainty Zones 🌀

1. High Uncertainty: When entropy exceeds the upper threshold. 🚨🔺

2. Low Uncertainty: When entropy is below the lower threshold. 🔻💡

3. Neutral: When entropy lies between both thresholds. ⚖️🔄

________________________________________

What We Aim to Achieve with the Formula in Practice 🎯

1. Detection of Volatile Moments: Shannon’s formula helps us identify when the market is unpredictable. This is a good moment to take additional precautions, such as reducing position size or avoiding trading during high volatility phases. ⚠️📉

2. Trading Opportunities in Stable Markets: With low entropy, we can identify when the market is more predictable, favoring trend or momentum strategies with a higher chance of success. 🚀📈

3. Optimization of Risk Management: By measuring market volatility in real-time, we can adjust entry and exit strategies, tailoring risk based on the level of uncertainty detected. 🔄⚖️

________________________________________

We hope this makes it easy to interpret and use. If you have any questions or comments, please feel free to reach out to us! 📬😊

MultiLayer Acceleration/Deceleration Strategy [Skyrexio]Overview

MultiLayer Acceleration/Deceleration Strategy leverages the combination of Acceleration/Deceleration Indicator(AC), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Acceleration/Deceleration Indicator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Acceleration/Deceleration shall create one of two types of long signals (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created long signal.

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one long signal, another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. We'll begin with the simplest: the EMA.

The Exponential Moving Average (EMA) is a type of moving average that assigns greater weight to recent price data, making it more responsive to current market changes compared to the Simple Moving Average (SMA). This tool is widely used in technical analysis to identify trends and generate buy or sell signals. The EMA is calculated as follows:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy, the EMA acts as a long-term trend filter. For instance, long trades are considered only when the price closes above the EMA (default: 100-period). This increases the likelihood of entering trades aligned with the prevailing trend.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

In this strategy if the most recent up fractal breakout occurs above the Alligator's teeth and follows the last down fractal breakout below the teeth, the algorithm identifies an uptrend. Long trades can be opened during this phase if a signal aligns. If the price breaks a down fractal below the teeth line during an uptrend, the strategy assumes the uptrend has ended and closes all open long trades.

By combining the EMA as a long-term trend filter with the Alligator and fractals as short-term filters, this approach increases the likelihood of opening profitable trades while staying aligned with market dynamics.

Now let's talk about Acceleration/Deceleration signals. AC indicator is calculated using the Awesome Oscillator, so let's first of all briefly explain what is Awesome Oscillator and how it can be calculated. The Awesome Oscillator (AO), developed by Bill Williams, is a momentum indicator designed to measure market momentum by contrasting recent price movements with a longer-term historical perspective. It helps traders detect potential trend reversals and assess the strength of ongoing trends.

The formula for AO is as follows:

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

The Acceleration/Deceleration (AC) Indicator, introduced by Bill Williams, measures the rate of change in market momentum. It highlights shifts in the driving force of price movements and helps traders spot early signs of trend changes. The AC Indicator is particularly useful for identifying whether the current momentum is accelerating or decelerating, which can indicate potential reversals or continuations. For AC calculation we shall use the AO calculated above is the following formula:

AC = AO − SMA5(AO), where SMA5(AO)is the 5-period Simple Moving Average of the Awesome Oscillator

When the AC is above the zero line and rising, it suggests accelerating upward momentum.

When the AC is below the zero line and falling, it indicates accelerating downward momentum.

When the AC is below zero line and rising it suggests the decelerating the downtrend momentum. When AC is above the zero line and falling, it suggests the decelerating the uptrend momentum.

Now we can explain which AC signal types are used in this strategy. The first type of long signal is when AC value is below zero line. In this cases we need to see three rising bars on the histogram in a row after the falling one. The second type of signals occurs above the zero line. There we need only two rising AC bars in a row after the falling one to create the signal. The signal bar is the last green bar in this sequence. The strategy places the buy stop order one tick above the candle's high, which corresponds to the signal bar on AC indicator.

After that we can have the following scenarios:

Price hit the order on the next candle in this case strategy opened long with this price.

Price doesn't hit the order price, the next candle set lower high. If current AC bar is increasing buy stop order changes by the script to the high of this new bar plus one tick. This procedure repeats until price finally hit buy order or current AC bar become decreasing. In the second case buy order cancelled and strategy wait for the next AC signal.

If long trades are initiated, the strategy continues utilizing subsequent signals until the total number of trades reaches a maximum of 5. All open trades are closed when the trend shifts to a downtrend, as determined by the combination of the Alligator and Fractals described earlier.

Why we use AC signals? If currently strategy algorithm considers the high probability of the short-term uptrend with the Alligator and Fractals combination pointed out above and the long-term trend is also suggested by the EMA filter as bullish. Rising AC bars after period of falling AC bars indicates the high probability of local pull back end and there is a high chance to open long trade in the direction of the most likely main uptrend. The numbers of rising bars are different for the different AC values (below or above zero line). This is needed because if AC below zero line the local downtrend is likely to be stronger and needs more rising bars to confirm that it has been changed than if AC is above zero.

Why strategy use only 10% per signal? Sometimes we can see the false signals which appears on sideways. Not risking that much script use only 10% per signal. If the first long trade has been open and price continue going up and our trend approximation by Alligator and Fractals is uptrend, strategy add another one 10% of capital to every next AC signal while number of active trades no more than 5. This capital allocation allows to take part in long trades when current uptrend is likely to be strong and use only 10% of capital when there is a high probability of sideways.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.11.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 10%

Maximum Single Position Loss: -5.15%

Maximum Single Profit: +24.57%

Net Profit: +2108.85 USDT (+21.09%)

Total Trades: 111 (36.94% win rate)

Profit Factor: 2.391

Maximum Accumulated Loss: 367.61 USDT (-2.97%)

Average Profit per Trade: 19.00 USDT (+1.78%)

Average Trade Duration: 75 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 3h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

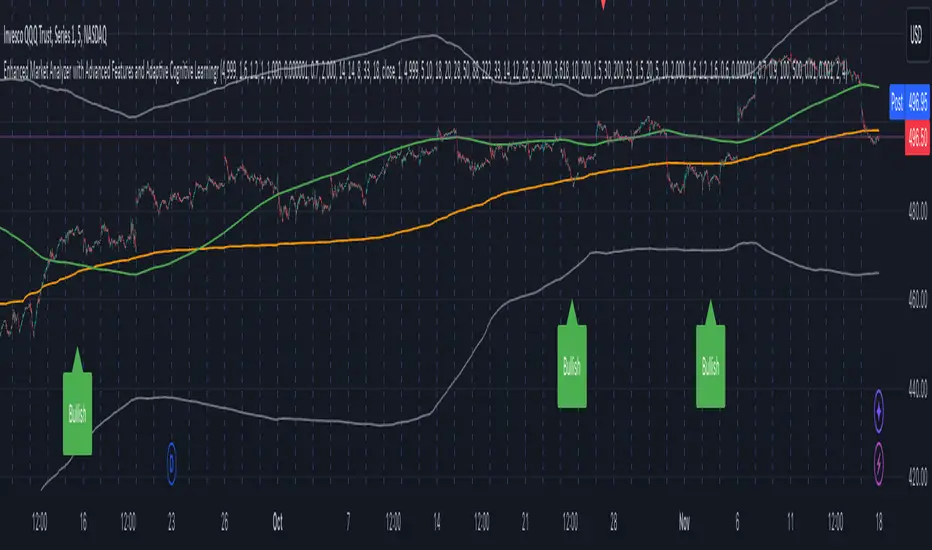

Enhanced Market Analyzer with Adaptive Cognitive LearningThe "Enhanced Market Analyzer with Advanced Features and Adaptive Cognitive Learning" is an advanced, multi-dimensional trading indicator that leverages sophisticated algorithms to analyze market trends and generate predictive trading signals. This indicator is designed to merge traditional technical analysis with modern machine learning techniques, incorporating features such as adaptive learning, Monte Carlo simulations, and probabilistic modeling. It is ideal for traders who seek deeper market insights, adaptive strategies, and reliable buy/sell signals.

Key Features:

Adaptive Cognitive Learning:

Utilizes Monte Carlo simulations, reinforcement learning, and memory feedback to adapt to changing market conditions.

Adjusts the weighting and learning rate of signals dynamically to optimize predictions based on historical and real-time data.

Hybrid Technical Indicators:

Custom RSI Calculation: An RSI that adapts its length based on recursive learning and error adjustments, making it responsive to varying market conditions.

VIDYA with CMO Smoothing: An advanced moving average that incorporates Chander Momentum Oscillator for adaptive smoothing.

Hamming Windowed VWMA: A volume-weighted moving average that applies a Hamming window for smoother calculations.

FRAMA: A fractal adaptive moving average that responds dynamically to price movements.

Advanced Statistical Analysis:

Skewness and Kurtosis: Provides insights into the distribution and potential risk of market trends.

Z-Score Calculations: Identifies extreme market conditions and adjusts trading thresholds dynamically.

Probabilistic Monte Carlo Simulation:

Runs thousands of simulations to assess potential price movements based on momentum, volatility, and volume factors.

Integrates the results into a probabilistic signal that informs trading decisions.

Feature Extraction:

Calculates a variety of market metrics, including price change, momentum, volatility, volume change, and ATR.

Normalizes and adapts these features for use in machine learning algorithms, enhancing signal accuracy.

Ensemble Learning:

Combines signals from different technical indicators, such as RSI, MACD, Bollinger Bands, Stochastic Oscillator, and statistical features.

Weights each signal based on cumulative performance and learning feedback to create a robust ensemble signal.

Recursive Memory and Feedback:

Stores and averages past RSI calculations in a memory array to provide historical context and improve future predictions.

Adaptive memory factor adjusts the influence of past data based on current market conditions.

Multi-Factor Dynamic Length Calculation:

Determines the length of moving averages based on volume, volatility, momentum, and rate of change (ROC).

Adapts to various market conditions, ensuring that the indicator is responsive to both high and low volatility environments.

Adaptive Learning Rate:

The learning rate can be adjusted based on market volatility, allowing the system to adapt its speed of learning and sensitivity to changes.

Enhances the system's ability to react to different market regimes.

Monte Carlo Simulation Engine:

Simulates thousands of random outcomes to model potential future price movements.

Weights and aggregates these simulations to produce a final probabilistic signal, providing a comprehensive risk assessment.

RSI with Dynamic Adjustments:

The initial RSI length is adjusted recursively based on calculated errors between true RSI and predicted RSI.

The adaptive RSI calculation ensures that the indicator remains effective across various market phases.

Hybrid Moving Averages:

Short-Term and Long-Term Averages: Combines FRAMA, VIDYA, and Hamming VWMA with specific weights for a unique hybrid moving average.

Weighted Gradient: Applies a color gradient to indicate trend strength and direction, improving visual clarity.

Signal Generation:

Generates buy and sell signals based on the ensemble model and multi-factor analysis.

Uses percentile-based thresholds to determine overbought and oversold conditions, factoring in historical data for context.

Optional settings to enable adaptation to volume and volatility, ensuring the indicator remains effective under different market conditions.

Monte Carlo and Learning Parameters:

Users can customize the number of Monte Carlo simulations, learning rate, memory factor, and reward decay for tailored performance.

Applications:

Scalping and Day Trading:

The fast response of the adaptive RSI and ensemble learning model makes this indicator suitable for short-term trading strategies.

Swing Trading:

The combination of long-term moving averages and probabilistic models provides reliable signals for medium-term trends.

Volatility Analysis:

The ATR, Bollinger Bands, and adaptive moving averages offer insights into market volatility, helping traders adjust their strategies accordingly.

Bollinger Bands Mean Reversion by Kevin Davey Bollinger Bands Mean Reversion Strategy Description

The Bollinger Bands Mean Reversion Strategy is a popular trading approach based on the concept of volatility and market overreaction. The strategy leverages Bollinger Bands, which consist of an upper and lower band plotted around a central moving average, typically using standard deviations to measure volatility. When the price moves beyond these bands, it signals potential overbought or oversold conditions, and the strategy seeks to exploit a reversion back to the mean (the central band).

Strategy Components:

1. Bollinger Bands:

The bands are calculated using a 20-period Simple Moving Average (SMA) and a multiple (usually 2.0) of the standard deviation of the asset’s price over the same period. The upper band represents the SMA plus two standard deviations, while the lower band is the SMA minus two standard deviations. The distance between the bands increases with higher volatility and decreases with lower volatility.

2. Mean Reversion:

Mean reversion theory suggests that, over time, prices tend to move back toward their historical average. In this strategy, a buy signal is triggered when the price falls below the lower Bollinger Band, indicating a potential oversold condition. Conversely, the position is closed when the price rises back above the upper Bollinger Band, signaling an overbought condition.

Entry and Exit Logic:

Buy Condition: The strategy enters a long position when the price closes below the lower Bollinger Band, anticipating a mean reversion to the central band (SMA).

Sell Condition: The long position is exited when the price closes above the upper Bollinger Band, implying that the market is likely overbought and a reversal could occur.

This approach uses mean reversion principles, aiming to capitalize on short-term price extremes and volatility compression, often seen in sideways or non-trending markets. Scientific studies have shown that mean reversion strategies, particularly those based on volatility indicators like Bollinger Bands, can be effective in capturing small but frequent price reversals  .

Scientific Basis for Bollinger Bands:

Bollinger Bands, developed by John Bollinger, are widely regarded in both academic literature and practical trading as an essential tool for volatility analysis and mean reversion strategies. Research has shown that Bollinger Bands effectively identify relative price highs and lows, and can be used to forecast price volatility and detect potential breakouts . Studies in financial markets, such as those by Fernández-Rodríguez et al. (2003), highlight the efficacy of Bollinger Bands in detecting overbought or oversold conditions in various assets .

Who is Kevin Davey?

Kevin Davey is an award-winning algorithmic trader and highly regarded expert in developing and optimizing systematic trading strategies. With over 25 years of experience, Davey gained significant recognition after winning the prestigious World Cup Trading Championships multiple times, where he achieved triple-digit returns with minimal drawdown. His success has made him a key figure in algorithmic trading education, with a focus on disciplined and rule-based trading systems.

ICT Judas Swing | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Judas Swing Indicator! This indicator is built around the ICT's "Judas Swing" strategy. The strategy looks for a liquidity grab around NY 9:30 session and a Fair Value Gap for entry confirmation. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Judas Swing :

Implementation of ICT's Judas Swing Strategy

2 Different TP / SL Methods

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The strategy begins by identifying the New York session from 9:30 to 9:45 and marking recent liquidity zones. These liquidity zones are determined by locating high and low pivot points: buyside liquidity zones are identified using high pivots that haven't been invalidated, while sellside liquidity zones are found using low pivots. A break of either buyside or sellside liquidity must occur during the 9:30-9:45 session, which is interpreted as a liquidity grab by smart money. The strategy assumes that after this liquidity grab, the price will reverse and move in the opposite direction. For entry confirmation, a fair value gap (FVG) in the opposite direction of the liquidity grab is required. A buyside liquidity grab calls for a bearish FVG, while a sellside grab requires a bullish FVG. Based on the type of FVG—bullish for buys and bearish for sells—the indicator will then generate a Buy or Sell signal.

After the Buy or Sell signal, the indicator immediately draws the take-profit (TP) and stop-loss (SL) targets. The indicator has three different TP & SL modes, explained in the "Settings" section of this write-up.

You can set up alerts for entry and TP & SL signals, and also check the current performance of the indicator and adjust the settings accordingly to the current ticker using the backtesting dashboard.

🚩 UNIQUENESS

This indicator is an all-in-one suit for the ICT's Judas Swing concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. Different and customizable algorithm modes will help the trader fine-tune the indicator for the asset they are currently trading. Three different TP / SL modes are available to suit your needs. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️ SETTINGS

1. General Configuration

Swing Length -> The swing length for pivot detection. Higher settings will result in

FVG Detection Sensitivity -> You may select between Low, Normal, High or Extreme FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivies resulting in spotting bigger FVGs, and higher sensitivies resulting in spotting all sizes of FVGs.

2. TP / SL

TP / SL Method ->

a) Dynamic: The TP / SL zones will be auto-determined by the algorithm based on the Average True Range (ATR) of the current ticker.

b) Fixed : You can adjust the exact TP / SL ratios from the settings below.

Dynamic Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

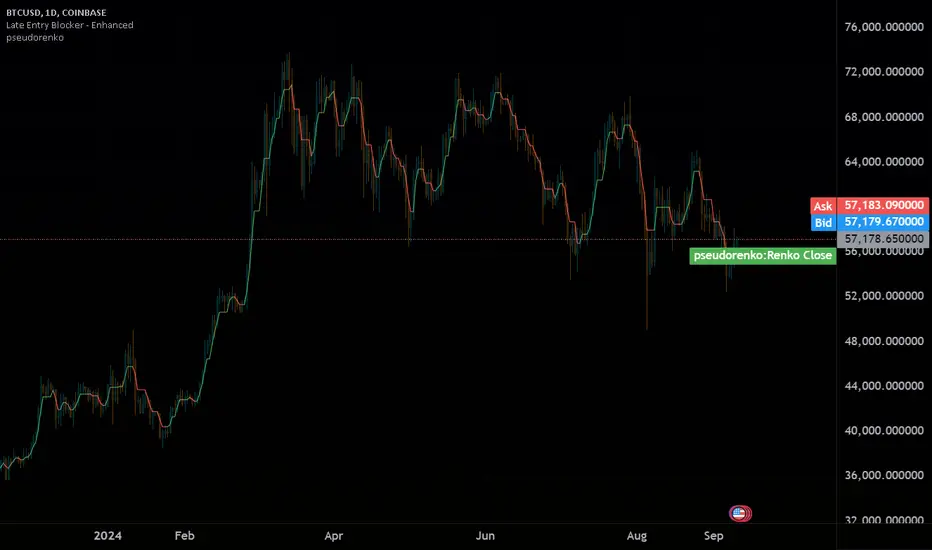

pseudorenko█ CALCULATE PSEUDO-RENKO VALUE

Calculates and returns the Pseudo-Renko Stabilized value (or close price) based on a given input value, along with the direction of the current Renko brick. This function adapts the traditional Renko brick size dynamically based on the volatility of the input value using a combination of SMA and EMA calculations. The calculated price represents the closing price of the most recent Pseudo-Renko brick, while the direction indicates the trend ( 1 for uptrend, -1 for downtrend).

Parameters:

* `val` :

* Type: ` float `

* Description: The input value upon which the Pseudo-Renko calculations are performed. You can use any price series or custom value as input.

* `sensitivity` :

* Type: ` float `

* Default Value: ` 1.0 `

* Description: Controls the sensitivity of the brick size to the volatility of the `val`. Higher values lead to larger bricks, resulting in a smoother Renko chart. Lower values produce smaller bricks, leading to a more reactive chart.

* Possible Values: Any positive float.

* `length` :

* Type: ` int `

* Default Value: ` 7 `

* Description: The length used for calculating the EMA and SMA in the dynamic brick size calculation. It influences how quickly the brick size adapts to changing volatility of the `val`.

* Possible Values: Any positive integer.

Return Values:

* `lastRenkoClose` :

* Type: ` float `

* Description: The closing price of the last completed Pseudo-Renko brick based on the `val`.

* `renkoDirection` :

* Type: ` int `

* Description: The direction of the current Pseudo-Renko brick based on the `val`:

* ` 1 `: Uptrend

* ` -1 `: Downtrend

* ` 0 `: No change (initially, or no brick change since the previous bar)

Example Usage:

//@version=5

indicator("Pseudo-Renko Stabilized (Val)", overlay=true)

// Get user inputs

sensitivityInput = input.float(0.1, "Sensitivity",0.01,step=0.01)

lengthInput = input.int(5, "Length",2)

// Example usage with the 'close' price as the input value

= pseudo_renko(math.avg(close,open), sensitivityInput, lengthInput)

// Plot the Renko close price

plot(renkoClose, "Renko Close", renkoDirection>0?color.aqua:color.orange,2)

// You can also use other values as input, such as:

// = pseudo_renko(high, sensitivityInput, lengthInput)

// = pseudo_renko(low, sensitivityInput, lengthInput)

This example demonstrates how to use the `pseudo_renko` function within an indicator. It takes user inputs for `sensitivity` and `length`, then calculates the Pseudo-Renko values using the average of the `close` and `open` prices as the `val`. The resulting `renkoClose` price is plotted on the chart, with a color change based on the `renkoDirection`. It also illustrates how you can use other values, like `high` and `low`, as input to the function.

Note: The Pseudo-Renko algorithm is based on adapting the Renko brick size dynamically based on the input `val`. This provides more flexibility compared to the normal, but is experimental. The `sensitivity` and `length` parameters, along with the choice of the `val`, offer further customization to tune the algorithm's behavior to your preference and trading style.

Pseudo-Renko Stabilized (Val)█ CALCULATE PSEUDO-RENKO VALUE

Calculates and returns the Pseudo-Renko Stabilized value (or close price) based on a given input value, along with the direction of the current Renko brick. This function adapts the traditional Renko brick size dynamically based on the volatility of the input value using a combination of SMA and EMA calculations. The calculated price represents the closing price of the most recent Pseudo-Renko brick, while the direction indicates the trend ( 1 for uptrend, -1 for downtrend).

Parameters:

* `val` :

* Type: ` float `

* Description: The input value upon which the Pseudo-Renko calculations are performed. You can use any price series or custom value as input.

* `sensitivity` :

* Type: ` float `

* Default Value: ` 1.0 `

* Description: Controls the sensitivity of the brick size to the volatility of the `val`. Higher values lead to larger bricks, resulting in a smoother Renko chart. Lower values produce smaller bricks, leading to a more reactive chart.

* Possible Values: Any positive float.

* `length` :

* Type: ` int `

* Default Value: ` 7 `

* Description: The length used for calculating the EMA and SMA in the dynamic brick size calculation. It influences how quickly the brick size adapts to changing volatility of the `val`.

* Possible Values: Any positive integer.

Return Values:

* `lastRenkoClose` :

* Type: ` float `

* Description: The closing price of the last completed Pseudo-Renko brick based on the `val`.

* `renkoDirection` :

* Type: ` int `

* Description: The direction of the current Pseudo-Renko brick based on the `val`:

* ` 1 `: Uptrend

* ` -1 `: Downtrend

* ` 0 `: No change (initially, or no brick change since the previous bar)

Example Usage:

//@version=5

indicator("Pseudo-Renko Stabilized (Val)", overlay=true)

// Get user inputs

sensitivityInput = input.float(0.1, "Sensitivity",0.01,step=0.01)

lengthInput = input.int(5, "Length",2)

// Example usage with the 'close' price as the input value

= pseudo_renko(math.avg(close,open), sensitivityInput, lengthInput)

// Plot the Renko close price

plot(renkoClose, "Renko Close", renkoDirection>0?color.aqua:color.orange,2)

// You can also use other values as input, such as:

// = pseudo_renko(high, sensitivityInput, lengthInput)

// = pseudo_renko(low, sensitivityInput, lengthInput)

This example demonstrates how to use the `pseudo_renko` function within an indicator. It takes user inputs for `sensitivity` and `length`, then calculates the Pseudo-Renko values using the average of the `close` and `open` prices as the `val`. The resulting `renkoClose` price is plotted on the chart, with a color change based on the `renkoDirection`. It also illustrates how you can use other values, like `high` and `low`, as input to the function.

Note: The Pseudo-Renko algorithm is based on adapting the Renko brick size dynamically based on the input `val`. This provides more flexibility compared to the normal, but is experimental. The `sensitivity` and `length` parameters, along with the choice of the `val`, offer further customization to tune the algorithm's behavior to your preference and trading style.

ICT Unicorn | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Unicorn Indicator! This indicator is built around the ICT's "Unicorn" strategy. The strategy uses Breaker Blocks and Fair Value Gaps for entry confirmation. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Unicorn Indicator :

Implementation of ICT's Unicorn Strategy

Toggleable Retracement Entry Method

3 Different TP / SL Methods

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The ICT Unicorn entry model merges the concepts of Breaker Blocks and Fair Value Gaps (FVGs), offering a distinct method for identifying trade opportunities. By integrating these two elements, we can have a position entry with stop-loss and take-profit targets on the potential support & resistance zones. This model is particularly reliable for trade entry, as it combines two powerful entry techniques.

An ICT Unicorn Model consists of a FVG which is overlapping with a Breaker Block of the same type. Here is an example :

When a FVG overlaps with a Breaker Block of the same type, the indicator gives a Buy or Sell signal depending on the FVG type (Bullish & Bearish). If the "Require Retracement" option is enabled in the settings, the signals are not given immediately. Instead, the current price of the ticker will need to touch the FVG once more before the signals are given.

After the Buy or Sell signal, the indicator immediately draws the take-profit (TP) and stop-loss (SL) targets. The indicator has three different TP & SL modes, explained in the "Settings" section of this write-up.

You can set up alerts for entry and TP & SL signals, and also check the current performance of the indicator and adjust the settings accordingly to the current ticker using the backtesting dashboard.

🚩 UNIQUENESS

This indicator is an all-in-one suit for the ICT's Unicorn concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. Different and customizable algorithm modes will help the trader fine-tune the indicator for the asset they are currently trading. Three different TP / SL modes are available to suit your needs. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️ SETTINGS

1. General Configuration

FVG Detection Sensitivity -> You may select between Low, Normal, High or Extreme FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivies resulting in spotting bigger FVGs, and higher sensitivies resulting in spotting all sizes of FVGs.

Swing Length -> Swing length is used when finding order block formations. Smaller values will result in finding smaller order & breaker blocks.

Require Retracement ->

a) Disabled : The entry signal is given immediately once a FVG overlaps with a Breaker Block of the same type.

b) Enabled : The current price of the ticker will need to touch the FVG once more before the entry signal is given.

2. TP / SL

TP / SL Method ->

a) Unicorn : This is the default option. The SL will be set to the lowest low of the last 100 bars with an extra offset in a Buy signal. For Sell signals, the SL will be set to the highest high of the last 100 bars with an extra offset. The TP is then set to a value using the SL value and maintaining a risk-reward ratio.

b) Dynamic: The TP / SL zones will be auto-determined by the algorithm based on the Average True Range (ATR) of the current ticker.

c) Fixed : You can adjust the exact TP / SL ratios from the settings below.

Dynamic Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

ICT 9:30am First FVGThis indicator is designed based on ICT (Inner Circle Trader)'s algorithmic price action theory, specifically targeting the first fair value gap (FVG) that forms immediately after the New York Stock Exchange opens at 9:30am. The FVG represents an imbalance in the price delivery where a significant price action gap occurs, which can play a crucial role in future price movements.

Features:

Identification of First FVG: Automatically identifies and plots the first fair value gap that forms post the 9:30am NY open.

Customizable Visualization: Choose between block or line styles for visual representation, with customizable colors and border styles.

Date Labeling: Optionally displays date labels for each identified gap to track patterns over time.

Imbalance Extension: Options to extend the imbalances to the current bar, helping to visualize their influence on ongoing price action.

Purpose:

The first fair value gap formed after the market opens is an important algorithmic price range in ICT's price action theory. This indicator simplifies the identification of these critical gaps and helps in understanding their impact on future price action.

Uptrick: Trend SMA Oscillator### In-Depth Analysis of the "Uptrick: Trend SMA Oscillator" Indicator

---

#### Introduction to the Indicator

The "Uptrick: Trend SMA Oscillator" is an advanced yet user-friendly technical analysis tool designed to help traders across all levels of experience identify and follow market trends with precision. This indicator builds upon the fundamental principles of the Simple Moving Average (SMA), a cornerstone of technical analysis, to deliver a clear, visually intuitive overlay on the price chart. Through its strategic use of color-coding and customizable parameters, the Uptrick: Trend SMA Oscillator provides traders with actionable insights into market dynamics, enhancing their ability to make informed trading decisions.

#### Core Concepts and Methodology

1. **Foundational Principle – Simple Moving Average (SMA):**

- The Simple Moving Average (SMA) is the heart of the Uptrick: Trend SMA Oscillator. The SMA is a widely-used technical indicator that calculates the average price of an asset over a specified number of periods. By smoothing out price data, the SMA helps to reduce the noise from short-term fluctuations, providing a clearer picture of the overall trend.

- In the Uptrick: Trend SMA Oscillator, two SMAs are employed:

- **Primary SMA (oscValue):** This is applied to the closing price of the asset over a user-defined period (default is 14 periods). This SMA tracks the price closely and is sensitive to changes in market direction.

- **Smoothing SMA (oscV):** This second SMA is applied to the primary SMA, further smoothing the data and helping to filter out minor price movements that might otherwise be mistaken for trend reversals. The default period for this smoothing is 50, but it can be adjusted to suit the trader's preference.

2. **Color-Coding for Trend Visualization:**

- One of the most distinctive features of this indicator is its use of color to represent market trends. The indicator’s line changes color based on the relationship between the primary SMA and the smoothing SMA:

- **Bullish (Green):** The line turns green when the primary SMA is equal to or greater than the smoothing SMA, indicating that the market is in an upward trend.

- **Bearish (Red):** Conversely, the line turns red when the primary SMA falls below the smoothing SMA, signaling a downward trend.

- This color-coded system provides traders with an immediate, easy-to-interpret visual cue about the market’s direction, allowing for quick decision-making.

#### Detailed Explanation of Inputs

1. **Bullish Color (Default: Green #00ff00):**

- This input allows traders to customize the color that represents bullish trends on the chart. The default setting is green, a color commonly associated with upward market movement. However, traders can adjust this to any color that suits their visual preferences or matches their overall chart theme.

2. **Bearish Color (Default: Red RGB: 245, 0, 0):**

- The bearish color input determines the color of the line when the market is trending downwards. The default setting is a vivid red, signaling caution or selling opportunities. Like the bullish color, this can be customized to fit the trader’s needs.

3. **Line Thickness (Default: 5):**

- This setting controls the thickness of the line plotted by the indicator. The default thickness of 5 makes the line prominent on the chart, ensuring that the trend is easily visible even in complex or crowded chart setups. Traders can adjust the thickness to make the line thinner or thicker, depending on their visual preferences.

4. **Primary SMA Period (Value 1 - Default: 14):**

- The primary SMA period defines how many periods (e.g., days, hours) are used to calculate the moving average based on the asset’s closing prices. The default period of 14 is a balanced setting that offers a good mix of responsiveness and stability, but traders can adjust this depending on their trading style:

- **Shorter Periods (e.g., 5-10):** These make the indicator more sensitive, capturing trends more quickly but also increasing the likelihood of reacting to short-term price fluctuations or "noise."

- **Longer Periods (e.g., 20-50):** These smooth the data more, providing a more stable trend line that is less prone to whipsaws but may be slower to respond to trend changes.

5. **Smoothing SMA Period (Value 2 - Default: 50):**

- The smoothing SMA period determines how much the primary SMA is smoothed. A longer smoothing period results in a more gradual, stable line that focuses on the broader trend. The default of 50 is designed to smooth out most of the short-term fluctuations while still being responsive enough to detect significant trend shifts.

- **Customization:**

- **Shorter Smoothing Periods (e.g., 20-30):** Make the indicator more responsive, better for fast-moving markets or for traders who want to capture quick trends.

- **Longer Smoothing Periods (e.g., 70-100):** Enhance stability, ideal for long-term traders looking to avoid reacting to minor price movements.

#### Unique Characteristics and Advantages

1. **Simplicity and Clarity:**

- The Uptrick: Trend SMA Oscillator’s design prioritizes simplicity without sacrificing effectiveness. By relying on the widely understood SMA, it avoids the complexity of more esoteric indicators while still providing reliable trend signals. This simplicity makes it accessible to traders of all levels, from novices who are just learning about technical analysis to experienced traders looking for a straightforward, dependable tool.

2. **Visual Feedback Mechanism:**

- The indicator’s use of color to signify market trends is a particularly powerful feature. This visual feedback mechanism allows traders to assess market conditions at a glance. The clarity of the green and red color scheme reduces the mental effort required to interpret the indicator, freeing the trader to focus on strategy execution.

3. **Adaptability Across Markets and Timeframes:**

- One of the strengths of the Uptrick: Trend SMA Oscillator is its versatility. The basic principles of moving averages apply equally well across different asset classes and timeframes. Whether trading stocks, forex, commodities, or cryptocurrencies, traders can use this indicator to gain insights into market trends.

- **Intraday Trading:** For day traders who operate on short timeframes (e.g., 1-minute, 5-minute charts), the oscillator can be adjusted to be more responsive, capturing quick shifts in momentum.

- **Swing Trading:** Swing traders, who typically hold positions for several days to weeks, will find the default settings or slightly adjusted periods ideal for identifying and riding medium-term trends.

- **Long-Term Trading:** Position traders and investors can adjust the indicator to focus on long-term trends by increasing the periods for both the primary and smoothing SMAs, filtering out minor fluctuations and highlighting sustained market movements.

4. **Minimal Lag:**

- One of the challenges with moving averages is lag—the delay between when the price changes and when the indicator reflects this change. The Uptrick: Trend SMA Oscillator addresses this by allowing traders to adjust the periods to find a balance between responsiveness and stability. While all SMAs inherently have some lag, the customizable nature of this indicator helps traders mitigate this effect to align with their specific trading goals.

5. **Customizable and Intuitive:**

- While many technical indicators come with a fixed set of parameters, the Uptrick: Trend SMA Oscillator is fully customizable, allowing traders to tailor it to their trading style, market conditions, and personal preferences. This makes it a highly flexible tool that can be adjusted as markets evolve or as a trader’s strategy changes over time.

#### Practical Applications for Different Trader Profiles

1. **Day Traders:**

- **Use Case:** Day traders can customize the SMA periods to create a faster, more responsive indicator. This allows them to capture short-term trends and make quick decisions. For example, reducing the primary SMA to 5 and the smoothing SMA to 20 can help day traders react promptly to intraday price movements.

- **Strategy Integration:** Day traders might use the Uptrick: Trend SMA Oscillator in conjunction with volume-based indicators to confirm the strength of a trend before entering or exiting trades.

2. **Swing Traders:**

- **Use Case:** Swing traders can use the default settings or slightly adjust them to smooth out minor price fluctuations while still capturing medium-term trends. This approach helps in identifying the optimal points to enter or exit trades based on the broader market direction.

- **Strategy Integration:** Swing traders can combine this indicator with oscillators like the Relative Strength Index (RSI) to confirm overbought or oversold conditions, thereby refining their entry and exit strategies.

3. **Position Traders:**

- **Use Case:** Position traders, who hold trades for extended periods, can extend the SMA periods to focus on long-term trends. By doing so, they minimize the impact of short-term market noise and focus on the underlying trend.

- **Strategy Integration:** Position traders might use the Uptrick: Trend SMA Oscillator in combination with fundamental analysis. The indicator can help confirm the timing of entries and exits based on broader economic or corporate developments.

4. **Algorithmic and Quantitative Traders:**

- **Use Case:** The simplicity and clear logic of the Uptrick: Trend SMA Oscillator make it an excellent candidate for algorithmic trading strategies. Its binary output—bullish or bearish—can be easily coded into automated trading systems.

- **Strategy Integration:** Quant traders might use the indicator as part of a larger trading system that incorporates multiple indicators and rules, optimizing the SMA periods based on historical backtesting to achieve the best results.

5. **Novice Traders:**

- **Use Case:** Beginners can use the Uptrick: Trend SMA Oscillator to learn the basics of trend-following strategies.

The visual simplicity of the color-coded line helps novice traders quickly understand market direction without the need to interpret complex data.

- **Educational Value:** The indicator serves as an excellent starting point for those new to technical analysis, providing a practical example of how moving averages work in a real-world trading environment.

#### Combining the Indicator with Other Tools

1. **Relative Strength Index (RSI):**