PriceAction & Economic StrategyThis indicator combines price-action logic with macroeconomic data to generate trading signals.

Features:

- Price-action signals: A bullish signal occurs when a candle closes above its open; a bearish signal occurs when a candle closes below its open.

- Signal gap: The indicator includes an input called "Signal Gap (bars)" that defines the minimum number of bars between signals. By default the gap is set to 3, but you can adjust this between 1 and 10 to control signal frequency.

- Alerts: The script defines alert conditions for long and short signals, allowing you to create TradingView alerts that notify you when a new signal occurs.

- Economic data: The script uses TradingView's built-in `request.economic()` function to request U.S. GDP data. The GDP series is plotted in the Data Window for additional macroeconomic context.

How to use:

1. Add the indicator to a chart.

2. Open the indicator's settings and adjust the "Signal Gap (bars)" input to set the minimum bar gap between signals.

3. Look for green triangles plotted below the bars (bullish signals) and red triangles plotted above the bars (bearish signals). These appear only when the gap criterion is met.

4. If you want alerts, click the Alert button in TradingView, select this indicator, and choose either the Long or Short alert conditions.

5. To view the GDP data, open the Data Window; the GDP value will be shown alongside other series for each bar.

6. Use these signals in combination with your own analysis; this indicator is for educational purposes and does not constitute financial advice.

Поиск скриптов по запросу "bear"

Iriza4 -DAX EMA+HULL+ADX TP40 SL205 MIN SKALP. Additional filters improve accuracy: the strategy blocks trades after too many consecutive bullish or bearish candles (streak filter) and ignores signals when price is too far from the EMA (measured by ATR distance).

Each position uses a fixed risk-to-reward ratio of 1 : 2 with clear stop-loss and take-profit targets, without partial exits or breakevens. The goal is to identify clean pullbacks inside strong trends and filter out late or exhausted entries

XAUUSD 5m — CET 13:00→01:00 Supertrend + RSI (1:2 RR) — $240KThis strategy is designed for XAUUSD (Gold) on the 5-minute chart, optimized for trading during the most active hours (13:00–01:00 CET).

It combines a Supertrend direction filter with RSI crossovers for precise entries, and applies a 1:2 risk–reward ratio for consistent risk management.

🧠 Logic Overview:

Buy Signal: RSI crosses above 55 while Supertrend is bullish

Sell Signal: RSI crosses below 45 while Supertrend is bearish

Trading Hours: 13:00 → 01:00 CET (corresponding to 07:00 → 19:00 New York time)

Risk Management: Fixed 1:2 RR (TP = 2× SL distance from Supertrend line)

Session Management: Automatically closes all trades after 01:00 CET

Order Size: $240,000 notional exposure per position

💡 Best used for:

Scalping or intraday trading on XAUUSD during high-volatility hours.

The setup works best when combined with strong price action or volume confirmation.

⚠️ Disclaimer:

This script is for educational and testing purposes only.

Past performance does not guarantee future results.

Always test on demo before using live funds.

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.

The modular design allows traders to start with basic trend-following and progressively add complexity through ZLEMA confirmation, multiple stop-loss methods, and advanced exit strategies. Comprehensive performance tracking and export capabilities make this strategy an excellent tool for systematic testing and optimization.

Note: This strategy is provided for educational and backtesting purposes. All trading involves risk. Past performance does not guarantee future results. Always test thoroughly with paper trading before risking real capital, and adjust position sizing and risk parameters according to your risk tolerance and account size.

================================================================================

TAGS:

================================================================================

trend following, ZLEMA, zero lag, volatility bands, ATR stops, risk management, swing trading, momentum, trend confirmation, backtesting

================================================================================

CATEGORY:

================================================================================

Strategies

================================================================================

CHART SETUP RECOMMENDATIONS:

================================================================================

For optimal visualization when publishing:

Use a clean chart with no other indicators overlaid

Select a timeframe that shows multiple trade signals (4H or Daily recommended)

Choose a trending asset (crypto, forex major pairs, or trending stocks work well)

Show at least 6-12 months of data to demonstrate strategy across different market conditions

Enable the floating stats table to display key performance metrics

Ensure all indicator lines (ZLEMA, bands, stops) are clearly visible

Use the default chart type (candlesticks) - avoid Heikin Ashi, Renko, etc.

Make sure symbol information and timeframe are clearly visible

================================================================================

COMPLIANCE NOTES:

================================================================================

✅ Open-source publication with complete code visibility

✅ English-only title and description

✅ Detailed explanation of methodology and calculations

✅ Realistic commission (0.1%) and slippage (3 ticks) included

✅ All default parameters clearly documented

✅ Performance limitations and risks disclosed

✅ No unrealistic claims about performance

✅ No guaranteed results promised

✅ Appropriate for public library (original trend-following implementation with ZLEMA)

✅ Educational disclaimers included

✅ All features explained in detail

================================================================================

Mario vr SIT MC Utilizar en el gráfico

4

1

55

🧠 Market Structure Pro System – MVR

Market Structure Pro System – MVR is an advanced trading strategy designed to detect key reversal and trend-break zones with high precision.

It combines multiple professional tools within a single algorithm — integrating market structure, dynamic channels, volatility filters, and trend confirmations — making it ideal for scalping and swing trading across different markets (Forex, indices, cryptocurrencies, or stocks).

⚙️ How it works

The algorithm performs a complete structural analysis of the market through several technical layers:

🔹 1. Price Structure (BOS, Supply & Demand)

The system automatically detects:

Order Blocks

Supply and Demand Zones

Break of Structure (BOS) to identify market structure shifts

This allows traders to recognize where price is likely to react or break a trend, anticipating major market movements.

🔹 2. Keltner Channels and Linear Regression

The strategy uses multiple Keltner Channels with different settings to measure volatility expansion and contraction.

In combination, a dynamic linear regression line shows the overall market direction, helping confirm whether price is trending or ranging.

🔹 3. Volatility and Trend Filters

It integrates several complementary systems:

ATR (Average True Range): measures the strength and volatility of price movement.

PSAR (Parabolic SAR): identifies potential trend reversals.

Supertrend: acts as the main trend filter and confirmation tool.

These filters work together to avoid false signals in ranging or low-volatility conditions.

🔹 4. Swing Highs / Lows and Dynamic Lines

The indicator also marks swing high and low points, helping visualize dynamic support and resistance levels and potential price reversal areas.

📈 Signal Interpretation

BUY signals:

Occur when price breaks a demand zone or bearish structure, while trend filters (Supertrend / PSAR) confirm bullish direction.

SELL signals:

Trigger when price breaks a supply zone or bullish structure, with bearish confirmation from the trend filters.

These conditions can be further validated by visual confirmations from the Keltner Channel or a color change in the linear regression.

Script protegido

Este script se publica como código cerrado. Sin embargo, puede utilizarlo libremente y sin limitaciones: obtenga más información aquí.

mariovr_usd

Exención de responsabilidad

La información y las publicaciones que ofrecemos, no implican ni constituyen un asesoramiento financiero, ni de inversión, trading o cualquier otro tipo de consejo o recomendación emitida o respaldada por TradingView. Puede obtener información adicional en las Condiciones de uso.

1 comentario

Enhanced OB Retest Strategy v7.0The OB Retest Strategy is a full Order Block retest trading system that detects, plots, and trades OB zones across multiple timeframes. It uses structure breaks, retrace depth, and ATR filters to identify strong reversal or continuation setups.

⸻

⚙️ Core Features

• Multi-timeframe OB detection using break-of-structure (BOS) logic

• Automatic zone creation for bullish and bearish order blocks

• Smart merging of overlapping OB zones

• Dynamic flip-zone logic that turns invalidated OBs into new zones

• Wick zone detection for high-precision entries

• ATR-based trailing stop and optional breakeven

• Adjustable retrace depth, breakout %, and ATR filters

• Built-in performance table showing PnL, win rate, and total trades

• Fully backtestable with date range and commission control

⸻

🧠 Logic Summary

1. Detects a BOS on the higher timeframe.

2. Identifies the last opposing candle as the valid OB.

3. Validates the OB based on ATR size and breakout strength.

4. Waits for price to retest the zone to a set depth.

5. Executes trades and manages exits using trailing stop or breakeven.

6. Flips invalidated zones automatically.

⸻

💡 Usage Tips

• Best used on 1H to 4H charts for swing setups.

• Tune ATR and breakout thresholds for your market’s volatility.

• Combine with higher-timeframe bias or liquidity levels for better accuracy.

⸻

⚠️ Notes

• For educational and testing purposes only.

• Backtested results do not predict future performance.

• Always test before live use.

ICT Liquidity Sweep Asia/London 1 Trade per High & Low🧠 ICT Liquidity Sweep Asia/London — 1 Trade per High & Low

This strategy is inspired by the ICT (Inner Circle Trader) concepts of liquidity sweeps and market structure, focusing on the Asia and London sessions.

It automatically identifies liquidity grabs (sweeps) above or below key session highs/lows and enters trades with a fixed risk/reward ratio (RR).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚙️ Core Logic

-Asia Session: 8:00 PM – 11:59 PM (New York time)

-London Session: 2:00 AM – 5:00 AM (New York time)

-The script marks the Asia High/Low and London High/Low ranges for each day.

-When the market sweeps above a session high → potential Short setup

-When the market sweeps below a session low → potential Long setup

-A trade is triggered when the confirmation candle closes in the opposite direction of the sweep (bearish after a high sweep, bullish after a low sweep).

-Only one trade per sweep type (1 per High, 1 per Low) is allowed per session.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

📈 Risk Management

-Configurable Risk/Reward Target (default = 2:1)

-Configurable Position Size (number of contracts)

-Each trade uses a fixed Stop Loss (beyond the wick of the sweep) and a Take Profit calculated from the RR setting.

-All trades are automatically logged in the Strategy Tester with performance metrics.

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

💡 Features

✅ Visual session highlighting (Asia = Aqua, London = Orange)

✅ Automatic liquidity line plotting (session highs/lows)

✅ Entry & exit labels (optional visual display)

✅ Customizable RR and contract size

✅ Works on any instrument (ideal for indices, futures, or forex)

✅ Compatible with all timeframes (optimized for 1M–15M)

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

⚠️ Notes

-Best used on New York time-based charts.

-Designed for educational and backtesting purposes — not financial advice.

-Use as a foundation for further optimization (e.g., SMT confirmation, FVG filter, or time-based restrictions).

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

🧩 Recommended Use

Pair this with:

-ICT’s concepts like CISD (Change in State of Delivery) and FVGs (Fair Value Gaps)

-Higher timeframe liquidity maps

-Session bias or daily narrative filters

----------------------------------------------------------------------------------

----------------------------------------------------------------------------------

Author: jygirouard

Strategy Version: 1.3

Type: ICT Liquidity Sweep Automation

Timezone: America/New_York

Aurum DCX AVE Gold and Silver StrategySummary in one paragraph

Aurum DCX AVE is a volatility break strategy for gold and silver on intraday and swing timeframes. It aligns a new Directional Convexity Index with an Adaptive Volatility Envelope and an optional USD/DXY bias so trades appear only when direction quality and expansion agree. It is original because it fuses three pieces rarely combined in one model for metals: a convexity aware trend strength score, a percentile based envelope that widens with regime heat, and an intermarket DXY filter.

Scope and intent

• Markets. Gold and silver futures or spot, other liquid commodities, major indices

• Timeframes. Five minutes to one day. Defaults to 30min for swing pace

• Default demo used in this publication. TVC:GOLD on 30m

• Purpose. Enter confirmed volatility breaks while muting chop using regime heat and USD bias

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. DCX combines DI strength with path efficiency and curvature. AVE blends ATR with a high TR percentile and widens with DCX heat. DXY adds an intermarket bias

• Failure mode addressed. False starts inside compression and unconfirmed breakouts during USD swings

• Testability. Each component has a named input. Entry names L and S are visible in the list of trades

• Portable yardstick. Weekly ATR for stops and R multiples for targets

• Open source. Method and implementation are disclosed for community review

Method overview in plain language

You score direction quality with DCX, size an adaptive envelope with a blend of ATR and a high TR percentile, and only allow breaks that clear the band while DCX is above a heat threshold in the same direction. An optional DXY filter favors long when USD weakens and short when USD strengthens. Orders are bracketed with a Weekly ATR stop and an R multiple target, with optional trailing to the envelope.

Base measures

• Range basis. True Range and ATR over user windows. A high TR percentile captures expansion tails used by AVE

• Return basis. Not required

Components

• Directional Convexity Index DCX. Measures directional strength with DX, multiplies by path efficiency, blends a curvature term from acceleration, scales to 0 to 100, and uses a rise window

• Adaptive Volatility Envelope AVE. Midline ALMA or HMA or EMA plus bands sized by a blend of ATR and a high TR percentile. The blend weight follows volatility of volatility. Band width widens with DCX heat

• DXY Bias optional. Daily EMA trend of DXY. Long bias when USD weakens. Short bias when USD strengthens

• Risk block. Initial stop equals Weekly ATR times a multiplier. Target equals an R multiple of the initial risk. Optional trailing to AVE band

Fusion rule

• All gates must pass. DCX above threshold and rising. Directional lead agrees. Price breaks the AVE band in the same direction. DXY bias agrees when enabled

Signal rule

• Long. Close above AVE upper and DCX above threshold and DCX rising and plus DI leads and DXY bias is bearish

• Short. Close below AVE lower and DCX above threshold and DCX falling and minus DI leads and DXY bias is bullish

• Exit and flip. Bracket exit at stop or target. Optional trailing to AVE band

Inputs with guidance

Setup

• Symbol. Default TVC:GOLD (Correlation Asset for internal logic)

• Signal timeframe. Blank follows the chart

• Confirm timeframe. Default 1 day used by the bias block

Directional Convexity Index

• DCX window. Typical 10 to 21. Higher filters more. Lower reacts earlier

• DCX rise bars. Typical 3 to 6. Higher demands continuation

• DCX entry threshold. Typical 15 to 35. Higher avoids soft moves

• Efficiency floor. Typical 0.02 to 0.06. Stability in quiet tape

• Convexity weight 0..1. Typical 0.25 to 0.50. Higher gives curvature more influence

Adaptive Volatility Envelope

• AVE window. Typical 24 to 48. Higher smooths more

• Midline type. ALMA or HMA or EMA per preference

• TR percentile 0..100. Typical 75 to 90. Higher favors only strong expansions

• Vol of vol reference. Typical 0.05 to 0.30. Controls how much the percentile term weighs against ATR

• Base envelope mult. Typical 1.4 to 2.2. Width of bands

• Regime adapt 0..1. Typical 0.6 to 0.95. How much DCX heat widens or narrows the bands

Intermarket Bias

• Use DXY bias. Default ON

• DXY timeframe. Default 1 day

• DXY trend window. Typical 10 to 50

Risk

• Risk percent per trade. Reporting field. Keep live risk near one to two percent

• Weekly ATR. Default 14. Basis for stops

• Stop ATR weekly mult. Typical 1.5 to 3.0

• Take profit R multiple. Typical 1.5 to 3.0

• Trail with AVE band. Optional. OFF by default

Properties visible in this publication

• Initial capital. 20000

• Base currency. USD

• request.security lookahead off everywhere

• Commission. 0.03 percent

• Slippage. 5 ticks

• Default order size method percent of equity with value 3% of the total capital available

• Pyramiding 0

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Strategies use standard candles for signals and orders only

Honest limitations and failure modes

• Economic releases and thin liquidity can break assumptions behind the expansion logic

• Gap heavy symbols may prefer a longer ATR window

• Very quiet regimes can reduce signal contrast. Consider higher DCX thresholds or wider bands

• Session time follows the exchange of the chart and can change symbol to symbol

• Symbol sensitivity is expected. Use the gates and length inputs to find stable settings

Open source reuse and credits

• None

Mode

Public open source. Source is visible and free to reuse within TradingView House Rules

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

HermesHERMES STRATEGY - TRADINGVIEW DESCRIPTION

OVERVIEW

Hermes is an adaptive trend-following strategy that uses dual ALMA (Arnaud Legoux Moving Average) filters to identify high-quality entry and exit points. It's designed for swing and position traders who want smooth, low-lag signals with minimal whipsaws.

Unlike traditional moving averages that operate on price, Hermes analyzes price returns (percentage changes) to create signals that work consistently across any asset class and price range.

HOW IT WORKS

DUAL ALMA SYSTEM

The strategy uses two ALMA lines applied to price returns:

• Fast ALMA (Blue Line): Short-term trend signal (default: 80 periods)

• Slow ALMA (Black Line): Long-term baseline trend (default: 250 periods)

ALMA is superior to simple or exponential moving averages because it provides:

• Smoother curves with less noise

• Significantly reduced lag

• Natural resistance to outliers and flash crashes

TRADING LOGIC

BUY SIGNAL:

• Fast ALMA crosses above Slow ALMA (bullish regime)

• Price makes new N-bar high (momentum confirmation)

• Optional: Price above 200 EMA (macro trend filter)

• Optional: ALMA lines sufficiently separated (strength filter)

SELL SIGNAL:

• Fast ALMA crosses below Slow ALMA (bearish regime)

• Optional: Price makes new N-bar low (momentum confirmation)

The strategy stays in position during the entire bullish regime, allowing you to ride trends for weeks or months.

VISUAL INDICATORS

LINES:

• Blue Line: Fast ALMA (short-term signal)

• Black Line: Slow ALMA (long-term baseline)

TRADE MARKERS:

• Green Triangle Up: Buy executed

• Red Triangle Down: Sell executed

• Orange "M": Buy blocked by momentum filter

• Purple "W": Buy blocked by weak crossover strength

KEY PARAMETERS

ALMA SETTINGS:

• Short Period (default: 30) - Fast signal responsiveness

• Long Period (default: 250) - Baseline stability

• ALMA Offset (default: 0.90) - Balance between lag and smoothness

• ALMA Sigma (default: 7.5) - Gaussian curve width

ENTRY/EXIT FILTERS:

• Buy Lookback (default: 7) - Bars for momentum confirmation (required)

• Sell Lookback (default: 0) - Exit momentum bars (0 = disabled for faster exits)

• Min Crossover Strength (default: 0.0) - Required ALMA separation (0 = disabled)

• Use Macro Filter (default: true) - Only enter above 200 EMA

BEST PRACTICES

RECOMMENDED ASSETS - Works well on:

• Cryptocurrencies (Bitcoin, Ethereum, etc.)

• Major indices (S&P 500, Nasdaq)

• Large-cap stocks

• Commodities (Gold, Oil)

RECOMMENDED TIMEFRAMES:

• Daily: Primary timeframe for swing trading

• 4-Hour: More active trading (increase trade frequency)

• Weekly: Long-term position trading

PARAMETER TUNING:

• More trades: Lower Short Period (60-80)

• Fewer trades: Raise Short Period (100-120)

• Faster exits: Set Sell Lookback = 0

• Safer entries: Enable Macro Filter (Use Macro Filter = true)

STRATEGY ADVANTAGES

1. Low Lag - ALMA provides faster signals than traditional moving averages

2. Smooth Signals - Minimal whipsaws compared to crossover strategies

3. Asset Agnostic - Same parameters work across different markets

4. Trend Capture - Stays positioned during entire bullish regimes

5. Risk Management - Multiple filters prevent poor entries

6. Visual Clarity - Easy to interpret regime and filter states

WHEN TO USE HERMES

BEST FOR:

• Trending markets (crypto bull runs, equity uptrends)

• Swing trading (hold days to weeks)

• Position trading (hold weeks to months)

• Clear trend identification

• Risk-managed exposure

NOT SUITABLE FOR:

• Ranging/sideways markets

• Scalping or day trading

• High-frequency trading

• Mean reversion strategies

RISK DISCLAIMER

This indicator is for educational purposes only. Past performance does not guarantee future results. Always use proper position sizing and risk management. Test thoroughly on historical data before live trading.

CREDITS

Inspired by Giovanni Santostasi's Power Law Volatility Indicator, generalized for universal application across all assets using adaptive ALMA filtering.

Strategy by Hermes Trading Systems

QUICK START

1. Add indicator to chart

2. Use on daily timeframe for best results

3. Look for green buy signals when blue line crosses above black line

4. Exit on red sell signals when blue line crosses below black line

5. Adjust parameters based on your trading style:

• Conservative: Enable Macro Filter, increase Buy Lookback to 10

• Aggressive: Disable Macro Filter, lower Short Period to 60

• Default settings work well for most assets

XqKtPvRwSd-StrategyTradingView Pine Script Suite (v4.0) — General Overview

Purpose

A modular indicator and strategy suite designed for crypto markets, focusing on trend detection, momentum, range visualization, and signal generation. The suite supports popular symbols (BTC, ETH, BNB, SOL, DOGE) and offers flexible visualization and alert options.

Main Components

- v4.0-indicator: Multi-signal display for monitoring market conditions and trend bias.

- v4.0-watch-15m: Watchlist-style indicator with symbol-aware auto-tuning and optional chart timeframe adaptation.

- v4.0-strategy: Backtestable strategy using a unified, SuperTrend-based trend determination for entries/exits.

- v4.0-range: Range and structure visualization with dynamic lines, zones, and basic breakout cues.

- Two Poles.pinescript and fengzi/Two Poles Trend: Low-lag trend and smoothing filters for stability.

- supertrend.pinescript: SuperTrend variations used across the suite for direction and stops.

- fengzi utilities:

- Hann Window FIR Filter: Denoising and smoothing to reduce noise without excessive lag.

- Heatmap + Hann Resonance: Visual heat/energy mapping for momentum and resonance cues.

- Heatmap Trailing Stop with Breakouts: Trailing stop framework with breakout detection.

- Additional modules: super Z, AI JX, v3.2, and 4.0.pinescript (combined or experimental entries).

Key Features

- Unified Trend Logic: Strategy and visual components rely on a consistent SuperTrend-based direction model, improving clarity and consistency.

- Adaptive Timeframe: Option to use the chart’s timeframe; parameters scale from a 15m baseline to maintain relative behavior.

- Symbol Auto-Tuning: Default parameter sets are tailored for common crypto symbols; manual overrides are available.

- RSI Top/Bottom Hints: Optional dynamic cues for potential peaks in uptrends and troughs in downtrends; can contribute to scoring and alerts.

- Visual Customization: Configurable markers (arrows, dots, crosses), colors, line widths, and subtle background highlighting.

- Scoring and Clustering: Combines checks into a simplified score and clusters signals to reduce noise.

- Alerts: Supports TradingView alerts for entries, exits, and RSI hints.

- Compatibility: Designed to compile across common Pine versions and avoid local-scope plotting issues.

Basic Usage

- Add the indicator or strategy to your chart depending on your goal (monitoring vs. backtesting).

- Choose to follow the chart’s timeframe or set a working timeframe manually.

- Keep symbol auto-tuning enabled for a balanced default, or adjust parameters to match your preferences.

- Toggle optional modules (RSI hints, scoring contribution, visualization) based on your needs.

- For strategies, run backtests across your target period and review performance metrics (win rate, drawdown, and trade frequency).

Configuration Guidelines

- For earlier entries: lower SuperTrend period or multiplier; relax RSI thresholds.

- For more conservative behavior: increase SuperTrend period or multiplier; tighten thresholds; use stricter RSI logic.

- For cleaner signals: rely on the unified trend and consider limiting trades during extreme volatility or illiquid sessions.

Outputs

- Trend markers and lines indicating bullish/bearish bias and reversals.

- Range drawings with dynamic line coordinates, zones, and visual cues for consolidations and breakouts.

- Optional multi-timeframe dashboard-style summaries where applicable.

Extensibility

- Parameters and defaults can be extended for additional symbols and styles.

- Optional weighting or neutrality rules can be added to trend logic if you prefer stricter confirmation.

- Additional filters (volatility, session, volume) can be integrated to refine entries and exits.

Notes

- Not financial advice; backtest thoroughly before using any strategy live.

- Performance and signal quality vary by symbol, timeframe, and market conditions; adjust parameters as needed.

- Pine version differences may require minor adjustments; keep your environment up to date.

MACD + Supertrend + DEMA StrategySTRATEGY 📊 STRATEGY LOGIC:

Long Entry: When ALL of these occur simultaneously:

MACD histogram crosses above 0

Supertrend is bullish (green)

Short DEMA > Long DEMA

Short Entry: When ALL of these occur simultaneously:

MACD histogram crosses below 0

Supertrend is bearish (red)

Short DEMA < Long DEMA

Exits: Based on your TP/SL percentages from entry price

This follows the same clean structure as your MACD strategy but adds the alignment concept and proper risk management!

Fincandle ATR Direction TrackerOverview

The Fincandle ATR Direction Tracker is a strategy designed to capture momentum moves in the market using a dynamic ATR-based trailing stop. It identifies strong momentum candles and filters signals using trend alignment with moving averages.

Partial exits allow users to take a portion of profit at a predefined ATR multiple while keeping the remaining position open until the opposite signal occurs.

How It Works

Momentum Detection:

Measures candle body size relative to the Average True Range (ATR).

A candle is considered momentum if its body size exceeds ATR × Multiplier.

Trend Filter:

Uses two moving averages (Fast MA and Slow MA) to determine the market trend.

Bullish trend: Fast MA > Slow MA → long trades allowed

Bearish trend: Fast MA < Slow MA → short trades allowed

Trend filter can be toggled on or off.

ATR Trailing Stop:

A dynamic trailing stop adapts to price volatility.

Crossing above the trail triggers a buy signal, crossing below triggers a sell signal.

Partial Exit / Take Profit:

Step 1: Exit 50% of the position when price moves a configurable multiple of ATR in your favor.

Step 2: Close the remaining position when the opposite signal occurs (e.g., price crosses below/above the ATR trail).

How to Use

Add the strategy to any chart (stocks, indices, forex, crypto).

Configure ATR period, sensitivity, take profit multiple, and moving average lengths to suit the timeframe and asset.

Monitor buy/sell markers and dynamic ATR trail on the chart.

Optional: Set alerts for real-time notifications when signals trigger.

Adjust partial exit multiplier to control risk/reward.

Example Settings

ATR Period: 10

ATR Sensitivity: 3 × ATR

Take Profit: 2 × ATR

Fast MA: 50

Slow MA: 200

Partial Exit: 50% of position at take profit, remaining exits on opposite signal

Key Features

Adaptive ATR trailing stop for volatility-based entries/exits.

Trend alignment filter with Fast/Slow MA.

Partial exit logic for better risk management.

Visual BUY/SELL markers and alerts.

Fully Pine Script v6 compatible.

Disclaimer

This strategy is for educational and analytical purposes only.

It does not guarantee profits. Traders should always use proper risk management.

TEMA 20/34/55 Strategie mit Buy & SellThis indicator uses three Triple Exponential Moving Averages (TEMA) with periods 20 (green), 34 (blue), and 55 (red) to identify trend direction.

A buy signal is generated when TEMA20 crosses above TEMA34 and TEMA34 crosses above TEMA55 (bullish trend start).

A sell signal is generated when TEMA20 crosses below TEMA34 and TEMA34 crosses below TEMA55 (bearish trend start).

The strategy enters long and short positions with configurable stop loss and take profit levels.

Ideal for trend following and suitable for intraday or swing trading.

nadia

Gold ramon strategy based on 50 candles and atr of 12

You enter the maximum of 50 candles once the most bearish starts to rise, we expect 10 candles, if you don't go up in 10 candles, you don't enter, if you go up before 10 candles, you enter.

When is TP? Enough with 5 candles

The temporality is 1 hour. It can be adjusted to 1 minute temporality for scalping.

It is never lost, because it always exceeds the previous maximums.

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

Tight Entry Trend Engine Strategy═══════════════════════════════════════

TIGHT ENTRY TREND ENGINE

═══════════════════════════════════════

A breakout-based trend-following system designed to capture explosive

moves by entering at precise resistance/support breakouts with minimal

entry risk and massive profit potential.

⚠️ LOW WIN RATE, HIGH REWARD SYSTEM ⚠️

This is NOT a high win-rate strategy. Expect 25-35% winners, but

when it hits, winners are typically 10X+ larger than losers.

═══════════════════════════════════════

🎯 WHAT THIS SYSTEM DOES

═══════════════════════════════════════

The Tight Entry Trend Engine identifies powerful breakout opportunities

by detecting when price breaks through established trendlines with

confirmation from higher timeframe trends:

1. DYNAMIC TRENDLINE DETECTION (3 BANKS)

• Automatically draws support and resistance trendlines

• 3 separate "banks" capture short-term, medium-term, and long-term levels

• Each bank has configurable parameters (required pivot touch count,

angle limits, lengths)

2. BREAKOUT ENTRY TIMING

• Enters LONG when price breaks ABOVE resistance trendlines

• Enters SHORT when price breaks BELOW support trendlines

• Entry Alert occurs at the exact moment of breakout = "tight entry"

• Stop-loss placed just below/above the broken trendline (configurable)

3. HIGHER TIMEFRAME TREND FILTER

• Uses Hull Moving Average (HMA) on higher timeframe for trend following

• Auto-adjusts HTF based on your chart timeframe

• Optional filters prevent entries against major trend

• Optional "overextension" filter avoids buying parabolic moves

4. VOLATILITY-ADAPTIVE RISK MANAGEMENT

• Stop-loss calculated using Average True Range (ATR)

• Tighter stops = better R:R

• Profit targets adjust dynamically with volatility

• Breakeven stop moves automatically when in profit

• Extended profit targets when far from HTF trend

═══════════════════════════════════════

📊 HOW IT WORKS (METHODOLOGY)

═══════════════════════════════════════

STEP 1: TRENDLINE FORMATION

The system continuously scans for pivot highs and pivot lows to

construct trendlines. You control:

BANK 1 (Short-Term):

- Pivot Length: How many bars to look back for swing points

- Min Touches: How many pivots needed to form a line (default: 3)

- Max Length: How far back lines can reach (default: 180 bars)

- Angle Limits: Maximum steepness allowed for valid trendlines

- Tolerance: How close pivots must align to form horizontal lines

BANK 2 (Medium-Term):

- Slightly longer pivot periods for more significant levels

- Captures medium-term trend structure

- Default Max Length: 200 bars

BANK 3 (Long-Term):

- Focuses on major support/resistance zones

- Often uses horizontal levels (angled lines disabled by default)

- Default Max Length: 300 bars

The system draws RESISTANCE lines (red) above price and SUPPORT

lines (green) below price. These adapt in real-time as new pivots form.

STEP 2: BREAKOUT DETECTION

LONG SIGNALS:

- Price closes above a resistance trendline

- Higher timeframe trend is up (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

SHORT SIGNALS:

- Price closes below a support trendline

- Higher timeframe trend is down (optional filter)

- Price not overextended from HTF trend (optional filter)

- No position currently open

The "tight" aspect: Because you're entering right at the trendline

break, your stop-loss can be placed very close (just below the

broken resistance for longs), creating exceptional risk/reward ratios.

STEP 3: POSITION SIZING

Choose between:

- Fixed $ Risk Per Trade: Risk same dollar amount every trade

- % Risk Per Trade: Risk percentage of current equity

Position size automatically calculated based on:

- Your risk amount

- Distance to stop-loss (ATR-based)

- Works with stocks, futures, crypto (auto-adjusts for contract multipliers)

STEP 4: EXIT MANAGEMENT

Multiple exit methods working together:

- PROFIT TARGET: Exits when profit reaches 100x your risk

- EXTENDED PROFIT: Earlier exit (80R) when very far from HTF trend

- STOP LOSS: Fixed ATR-based stop below entry

- HTF TREND EXIT: Exits when price crosses below HTF trend with profit

- BREAKEVEN PULLBACK: Exits if profit drops below 0.6R after reaching breakeven

- PARTIAL PROFITS: Optional - take partial profits at specified R-multiple

═══════════════════════════════════════

🔧 KEY COMPONENTS EXPLAINED

═══════════════════════════════════════

HULL MOVING AVERAGE (HMA)

A smoothed moving average that reduces lag compared to traditional

MAs. The system uses HMA on a higher timeframe to determine the

dominant trend direction. You can choose:

- Auto HTF: System picks appropriate HTF based on your chart timeframe

- Manual HTF: You specify the higher timeframe

AVERAGE TRUE RANGE (ATR)

Measures current market volatility. Used for:

- Stop-loss distance (tighter when volatility low)

- Profit targets (larger when volatility high)

- Position sizing (smaller positions in volatile conditions)

- Breakeven trigger distance

TRENDLINE ANGLE FILTERING

Each trendline bank has angle limits to ensure quality:

- Resistance lines: Max downward/upward slope allowed

- Support lines: Max downward/upward slope allowed

- Angles automatically adjust based on current volatility

- Prevents overly steep/unreliable trendlines

SENSITIVITY CONTROL

One master slider adjusts multiple parameters:

- Trendline detection sensitivity

- HTF MA length

- Exit timing

- Auto-adjusts for daily+ timeframes (60% increase)

═══════════════════════════════════════

⚙️ WHAT YOU SEE ON YOUR CHART

═══════════════════════════════════════

TRENDLINES:

✓ Red resistance lines above price

✓ Green support lines below price

✓ Orange broken lines (past breakouts)

✓ Lines extend to show current levels

HTF TREND:

✓ Thick colored line showing higher timeframe trend

✓ Color gradient: Red (bearish) → Orange → Yellow → Green (bullish)

✓ 250-bar smoothed curve for visual clarity

ENTRY/EXIT SIGNALS:

✓ Small green dot below bar = Long entry

✓ Small red dot above bar = Short entry

✓ Small red dot above = Long exit

✓ Small black dot below = Short exit

OPTIONAL DETAILED LABELS:

✓ Bank number that triggered entry (Bank 1, 2, or 3)

✓ Exit reason (Profit Target, Stop Loss, HTF Exit, etc.)

✓ Partial profit notifications

POSITION TRACKING:

✓ Yellow dashed line at entry price (extends right)

✓ Green/red fill showing current profit/loss zone

✓ Lime arrows at top = Currently in long position

✓ Red arrows at bottom = Currently in short position

✓ Gray background = No position (flat)

STATS TABLE (Top Right):

✓ Current position (LONG/SHORT/FLAT)

✓ Risk per trade ($ or %)

✓ Entry price

✓ Unrealized P/L in dollars

✓ P/L in R-multiples (how many R's profit/loss)

✓ Average winner/loser R ($ mode) OR CAGR (% mode)

═══════════════════════════════════════

📈 OPTIMAL USAGE

═══════════════════════════════════════

BEST ASSETS:

- NASDAQ:QQQ on 1-hour (reg) chart ⭐ (PRIMARY OPTIMIZATION)

- Strong trending stocks: NVDA, AAPL, TSLA, MSFT, GOOGL, AMZN

- High volatility tech stocks

- Crypto: BTC, ETH

- Any liquid asset with clear trends and momentum (GOLD)

AVOID:

- Low volatility stocks

- Ranging/choppy markets

- Penny stocks or illiquid assets

- Assets without clear directional movement

BEST TIMEFRAMES:

- PRIMARY: 1-hour charts (optimal for QQQ)

- ALSO EXCELLENT: 2H, 4H, 8H

- WORKS: 15min, 30min (only momentum leaders, more noise)

- WORKS WITH ADJUSTMENTS: 1D, 2D (decrease trendline pivot lengths)

═══════════════════════════════════════

📊 BACKTEST RESULTS (QQQ 1H (Reg hours), 1999-2024)

═══════════════════════════════════════

The system showed on NASDAQ:QQQ 1-hour timeframe (regular hours):

- Total Return: 1,100,000%+ over 24 years

- Total Trades: 500+

- Win Rate: ~20-24% (LOW - this is by design!)

- Average Winner: 8-15% gain

- Average Loser: 2-4% loss

- Win/Loss Ratio: 10:1 (winners much bigger than losers)

- Profit Factor: 3+

- Max Drawdown: 45-50%

- Risk per trade: 3% of capital

KEY INSIGHT: This is a LOW WIN RATE, HIGH REWARD system. You will

lose more trades than you win, but the few winners are so large

they more than compensate for many small losses.

IMPORTANT: These are backtested results using optimal parameters

on historical data. Real trading results will vary based on:

- Your execution and timing

- Slippage and commissions

- Your emotional discipline

- Market conditions during your trading period

═══════════════════════════════════════

🎓 WHO IS THIS FOR?

═══════════════════════════════════════

IDEAL FOR:

✓ Swing traders comfortable holding winners for longer period

✓ Part-time traders (1H = check 2-3x per day)

✓ Traders seeking exceptional risk/reward ratios

✓ Those comfortable with low win rates if winners are huge

✓ Technical analysis enthusiasts

✓ Breakout traders

✓ Trend followers

═══════════════════════════════════════

🚀 GETTING STARTED - STEP BY STEP

═══════════════════════════════════════

STEP 1: APPLY TO YOUR CHART

- Search "Tight Entry Trend Engine" in indicators

- Click to apply to your chart

- Trendlines and HTF line will appear immediately

STEP 2: CHOOSE YOUR SETTINGS

For BEGINNERS - Use These Settings First:

1. Trade Direction & Filters:

• ENABLE LONGS: ✓ ON

• ENABLE SHORTS: ✗ OFF (start with longs only)

• Sensitivity: 1.0 (default)

• HTF Trend Entry Filter: ✓ ON (safer entries)

• Block Entries When Overextended: ✓ ON (avoid parabolic tops)

2. Position Sizing & Risk:

• Position Sizing: "Per Risk"

• RISK Type: "$ Per Trade"

• Risk Amount: $200 (or 1-3% of your account)

3. Visual Settings:

• Show Support Lines: ✗ OFF (unless trading shorts)

• Show Detailed Entry/Exit Labels: ✓ ON

• Show Stats Table: ✓ ON

• Show Entry Line & P/L Fill: ✓ ON

4. Leave everything else at DEFAULT for now

STEP 3: UNDERSTAND WHAT YOU SEE

When trendlines appear:

- RED lines above = Resistance (watch for price breaking UP through these)

- GREEN lines below = Support (watch for price breaking DOWN)

- When price breaks a red line = Potential LONG entry

- When price breaks a green line = Potential SHORT entry

The HTF trend line (thick colored):

- Green/lime = Strong uptrend (favorable for longs)

- Red = Strong downtrend (favorable for shorts if enabled)

- Orange/yellow = Transitioning

STEP 4: OBSERVE SIGNALS

- Small GREEN dot below bar = System entered LONG

- Small RED dot above bar = System exited LONG

- Check the label to see which "Bank" triggered (Bank 1, 2, or 3)

- Watch the yellow entry line and colored fill show your P/L

STEP 5: PAPER TRADE FIRST

- Use TradingView's paper trading feature

- Watch how signals perform on YOUR chosen asset

- Understand the win rate will be LOW (20-35%)

- Verify that winners are indeed much larger than losers

- Test for at least 20-30 signals before going live

STEP 6: OPTIMIZE FOR YOUR ASSET (OPTIONAL)

If default settings aren't working well:

For FASTER signals (more trades):

- Reduce Pivot Length 1 to 3-4

- Reduce Max Length 1 to 120-150

- Increase Sensitivity to 1.2-1.5

For SLOWER signals (higher quality):

- Increase Pivot Length 1 to 7-10

- Increase Max Length 1 to 250+

- Decrease Sensitivity to 0.7-0.9

For DAILY timeframes:

- Increase all Pivot Lengths by 30-50%

- Increase all Max Lengths significantly

- Sensitivity: 0.6-0.8

═══════════════════════════════════════

⚙️ ADVANCED SETTINGS EXPLAINED

═══════════════════════════════════════

TRENDLINE BANK SETTINGS:

Each bank (1, 2, 3) has these parameters:

- Min Touches: Minimum pivots to form a line

- Lower (2) = More lines, earlier detection

- Higher (4+) = Fewer lines, higher quality

- Pivot Length: Lookback for swing points

- Lower (3-5) = Reacts to recent price action

- Higher (10+) = Only major swing points

- Max Length: How old a trendline can be

- Shorter (100-150) = Only recent lines

- Longer (300+) = Include historical levels

- Tolerance: Alignment strictness for horizontal lines

- Lower (3.0-3.5) = Very strict horizontal

- Higher (4.5+) = More forgiving alignment

- Allow Angled Lines: Enable diagonal trendlines

- ON = Catches sloped support/resistance

- OFF = Only horizontal levels

- Angle Limits: Maximum steepness allowed

- Lower (1-2) = Only gentle slopes

- Higher (4-6) = Accept steeper angles

- Automatically adjusts for volatility

ATR MULTIPLIERS:

- STOP LOSS ATR (0.6): Distance to stop-loss

- Lower (0.4-0.5) = Tighter stops, stopped out more

- Higher (0.8-1.0) = Wider stops, more room

- PROFIT TARGET ATR (100): Main profit target

- This is 100x your risk = 10,000% R:R

- Lower (50-80) = Take profits sooner

- Higher (120+) = Let winners run longer

- BREAKEVEN ATR (40): When to move stop to breakeven

- Lower (20-30) = Protect profits earlier

- Higher (60+) = Give more room before protecting

HIGHER TIMEFRAME:

- Auto HTF: Automatically selects appropriate HTF

- 5min chart → uses 2H

- 15-30min → uses 6H

- 1-4H → uses 2D

- Daily → uses 4D

- HTF MA Length (300): HMA period for trend

- Lower (150-250) = More responsive

- Higher (400-500) = Smoother, less whipsaw

- HTF Trend Following Exit: Exits when crossing HTF

- ON = Additional exit method

- OFF = Rely only on profit targets/stops

- HTF Trend Entry Filter: Only trade with HTF trend

- ON = Safer, fewer signals

- OFF = More aggressive, more signals

- Block Entries When Overextended: Prevents chasing

- ON = Avoids parabolic tops/bottoms

- OFF = Enter all breakouts regardless

═══════════════════════════════════════

💡 TRADING PHILOSOPHY & EXPECTATIONS

═══════════════════════════════════════

This system is built on one core principle:

"ACCEPT SMALL, FREQUENT LOSSES TO CAPTURE RARE, MASSIVE WINS"

What this means:

- You WILL lose 65%-75% of your trades

- Most losses will be small (1-2R)

- Some winners hit 80R+

- Over time, math works in your favour

Twisted Forex's Doji + Area StrategyTitle

Twisted Forex’s Doji + Area Strategy

Description

What this strategy does

This strategy looks for doji candles forming inside or near supply/demand areas . Areas are built from swing pivots and sized with ATR, then tracked for retests (“confirmations”). When a doji prints close to an area and quality checks pass, the strategy places a trade with the stop beyond the doji and a configurable R:R target.

How areas (zones) are built

• Swings are detected with a user-set pivot length.

• Each swing spawns a horizontal area centered at the pivot price with half-height = zoneHalfATR × ATR .

• Duplicates are de-duplicated by center distance (ATR-scaled).

• Areas fade when broken beyond a buffer or after an optional age (expiry).

• Retests are recorded when price touches and then bounces away from the area; repeated reactions increase the zone’s “strength”.

Signal logic (summary)

Doji detection: strict or loose body criteria with optional minimum wick fractions and ATR-scaled minimum range.

Proximity: price must be inside/near a supply or demand area (proxATR × ATR).

Side resolution: overlap is resolved by (a) which side price penetrates more, (b) fast/slow EMA trend, or (c) nearest distance. Optional “previous candle flip” can bias long after a bearish candle and short after a bullish one.

Optional 1-bar confirmation: the bar after the doji must close away from the area by confirmATR × ATR .

Quality filter (Off/Soft/Strict): four checks—(i) wick rejection past the edge, (ii) doji closes in an edge “band” of the area, (iii) fresh touch (cooldown), (iv) approach impulse over a short lookback. In Strict , thresholds auto-tighten.

Orders & exits

• Long: stop below doji low minus buffer; Short: above doji high plus buffer.

• Target = rrMultiple × risk distance .

• Pyramiding is off by default.

Position sizing

You can size from the script or from Strategy Properties:

• Script-driven (default): set Position sizing = “Risk % of equity” and choose riskPercent (e.g., 1.0%). The script applies safe floors/rounding (FX micro-lots by default) so quantity never rounds to zero.

• Properties-driven : toggle Use TV Properties → Order size ON, then pick “Percent of equity” in Properties (e.g., 1%). The header includes safe defaults so trades still place.

Key inputs to explore

• Zone building : pivotLen, zoneHalfATR, minDepartureATR, expiryBars, breakATR, leftBars, dedupeATR.

• Doji & proximity : strictDoji, dojiBodyFrac, minWickFrac, minRangeATR, proxATR, minBarsBetween.

• Overlap resolution : usePenetration, useTrend (EMA 21/55), “previous candle flip”, needNextBarConf & confirmATR.

• Quality : qualityMode (Off/Soft/Strict), minQualPass/kStrict, wickPenATR, edgeBandFrac, approachLookback, approachMinATR, freshTouchBars.

• Zone strength gating : minStrengthSoft / minStrengthStrict.

• HTF confluence (optional) : useHTFTrend (HTF EMA 34/89) and/or useHTFZoneProx (HTF swing bands).

Tips to make it cleaner / higher quality

• Turn needNextBarConf ON and use confirmATR = 0.10–0.15 .

• Increase approachMinATR (e.g., 0.35–0.45) to require a stronger pre-touch impulse.

• Raise minStrengthSoft/Strict (e.g., 4–6) so only well-reacted zones can signal.

• Use signalsOnlyConfirmed ON if you prefer trades only from zones with retests (the script falls back gracefully when none exist yet).

• Nudge proxATR to 0.5–0.6 to demand tighter proximity to the level.

• Optional: enable useHTFTrend to filter counter-trend setups.

Default settings used in this publication

• Initial capital: 100,000 (illustrative).

• Slippage: 1 tick; Commission: 0% (you can raise commission if you prefer—spread is partly modeled by slippage).

• Sizing: Risk % of equity via inputs; riskPercent = 1.0% ; FX uses micro-lot floors by default.

• Quality: Off by default (Soft/Strict available).

• HTF trend gate: Off by default.

Backtesting notes

For a meaningful sample size, test on liquid symbols/timeframes that yield 100+ trades (e.g., majors on 5–15m over 1–2 years). Backtests are modelled and broker costs/spread vary—validate on your feed and forward-test.

How to read the chart

Shaded bands are supply (above) and demand (below). Brighter bands are the nearest K per side (visual aid). BUY/SELL labels mark entries; colored dots show entry/SL/TP levels. You can hide zones or unconfirmed zones for a cleaner view.

Disclaimer

This is educational material, not financial advice. Trading involves risk. Always test and size responsibly.

PG DMean & Price Sync ver 9.4 - ConsolidatedPG DMean & Price Sync Strategy (SD Filter)

This strategy combines the momentum-oscillator properties of the Detrended Mean (DMean) with a Standard Deviation (SD) Price Filter for confirming trend direction, aiming to isolate high-conviction trades while actively managing risk.

🔑 Core Logic

DMean Momentum Signal: The strategy's primary engine is the DMean, which measures the percentage difference between the current closing price and a longer-term Moving Average (price_ma). It is then smoothed by a DMean Signal line (MA of the DMean).

Entry Signal: A trade is triggered when the DMean line crosses above (for Long) or below (for Short) its Signal Line, but it must clear a user-defined Dead Zone Threshold to confirm momentum commitment.

SD Filter Confirmation (Price Sync): A Standard Deviation Channel, based on a separate user-defined price source and period, is used to filter trades.

Long Filter: Allows Long entries only when the price is trading above the lower SD band, suggesting the current price action is stronger than the recent average volatility to the downside.

Short Filter: Allows Short entries only when the price is currently below the Filter Basis (SMA), confirming a bearish stance within the SD channel.

🛡️ Risk & Exit Management

Primary Exit: All trades are exited by reverse DMean Crossover/Crossunder, meaning the position is closed when the DMean momentum reverses against the open trade (e.g., DMean crosses under the Signal to exit a Long).

Hard Stop Loss (Short Trades): A mandatory percentage-based Hard Stop Loss is implemented only for short positions to protect against sudden upward price spikes, closing the trade if the loss exceeds the set percentage. (Note: This version does not include a Hard SL for Long trades).

📊 Performance Dashboard

A custom Performance Dashboard Table is displayed at the bottom right of the chart to provide real-time, at-a-glance comparison of the strategy's equity performance versus a simple Buy & Hold over the selected backtesting date range.

SMC Strategy with RSI/OB at Market PriceTakes trade using smc with rsi confirmation

Buy Signal Triggers When:

Scenario 1 (Immediate Touch): Price touches/enters bullish OB boundaries AND previous candle closed with RSI ≤ 35

Scenario 2 (Close Inside): Current candle closes inside bullish OB AND current RSI ≤ 35

Sell Signal Triggers When:

Scenario 1 (Immediate Touch): Price touches/enters bearish OB boundaries AND previous candle closed with RSI ≥ 65

Scenario 2 (Close Inside): Current candle closes inside bearish OB AND current RSI ≥ 65

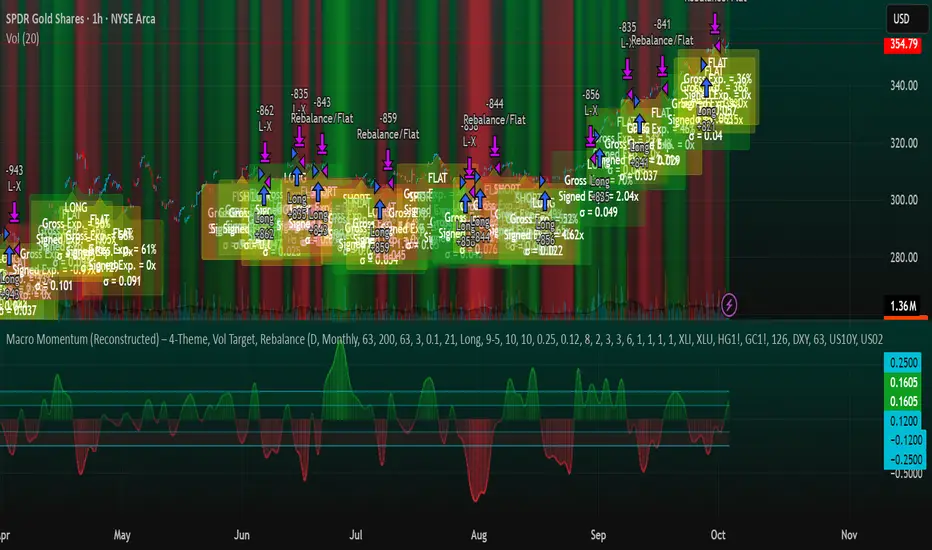

Macro Momentum – 4-Theme, Vol Target, RebalanceMacro Momentum — 4-Theme, Vol Target, Rebalance

Purpose. A macro-aware strategy that blends four economic “themes”—Business Cycle, Trade/USD, Monetary Policy, and Risk Sentiment—into a single, smoothed Composite signal. It then:

gates entries/exits with hysteresis bands,

enforces optional regime filters (200-day bias), and

sizes the position via volatility targeting with caps for long/short exposure.

It’s designed to run on any chart (index, ETF, futures, single stocks) while reading external macro proxies on a chosen Signal Timeframe.

How it works (high level)

Build four theme signals from robust macro proxies:

Business Cycle: XLI/XLU and Copper/Gold momentum, confirmed by the chart’s price vs a long SMA (default 200D).

Trade / USD: DXY momentum (sign-flipped so a rising USD is bearish for risk assets).

Monetary Policy: 10Y–2Y curve slope momentum and 10Y yield trend (steepening & falling 10Y = risk-on; rising 10Y = risk-off).

Risk Sentiment: VIX momentum (bearish if higher) and HYG/IEF momentum (bullish if credit outperforms duration).

Normalize & de-noise.

Optional Winsorization (MAD or stdev) clamps outliers over a lookback window.

Optional Z-score → tanh mapping compresses to ~ for stable weighting.

Theme lines are SMA-smoothed; the final Composite is LSMA-smoothed (linreg).

Decide direction with hysteresis.

Enter/hold long when Composite ≥ Entry Band; enter/hold short when Composite ≤ −Entry Band.

Exit bands are tighter than entry bands to avoid whipsaws.

Apply regime & direction constraints.

Optional Long-only above 200MA (chart symbol) and/or Short-only below 200MA.

Global Direction control (Long / Short / Both) and Invert switch.

Size via volatility targeting.

Realized close-to-close vol is annualized (choose 9-5 or 24/7 market profile).

Target exposure = TargetVol / RealizedVol, capped by Max Long/Max Short multipliers.

Quantity is computed from equity; futures are rounded to whole contracts.

Rebalance cadence & execution.

Trades are placed on Weekly / Monthly / Quarterly rebalance bars or when the sign of exposure flips.

Optional ATR stop/TP for single-stock style risk management.

Inputs you’ll actually tweak

General

Signal Timeframe: Where macro is sampled (e.g., D/W).

Rebalance Frequency: Weekly / Monthly / Quarterly.

ROC & SMA lengths: Defaults for theme momentum and the 200D regime filter.

Normalization: Z-score (tanh) on/off.

Winsorization

Toggle, lookback, multiplier, MAD vs Stdev.

Risk / Sizing

Target Annualized Vol & Realized Vol Lookback.

Direction (Long/Short/Both) and Invert.

Max long/short exposure caps.

Advanced Thresholds

Theme/Composite smoothing lengths.

Entry/Exit bands (hysteresis).

Regime / Execution

Long-only above 200MA, Short-only below 200MA.

Stops/TP (optional)

ATR length and SL/TP multiples.

Theme Weights

Per-theme scalars so you can push/pull emphasis (e.g., overweight Policy during rate cycles).

Macro Proxies

Symbols for each theme (XLI, XLU, HG1!, GC1!, DXY, US10Y, US02Y, VIX, HYG, IEF). Swap to alternatives as needed (e.g., UUP for DXY).

Signals & logic (under the hood)

Business Cycle = ½ ROC(XLI/XLU) + ½ ROC(Copper/Gold), then confirmed by (price > 200SMA ? +1 : −1).

Trade / USD = −ROC(DXY).

Monetary Policy = 0.6·ROC(10Y–2Y) − 0.4·ROC(10Y).

Risk Sentiment = −0.6·ROC(VIX) + 0.4·ROC(HYG/IEF).

Each theme → (optional Winsor) → (robust z or scaled ROC) → tanh → SMA smoothing.

Composite = weighted average → LSMA smoothing → compare to bands → dir ∈ {−1,0,+1}.

Rebalance & flips. Orders fire on your chosen cadence or when the sign of exposure changes.

Position size. exposure = clamp(TargetVol / realizedVol, maxLong/Short) × dir.

Note: The script also exposes Gross Exposure (% equity) and Signed Exposure (× equity) as diagnostics. These can help you audit how vol-targeting and caps translate into sizing over time.

Visuals & alerts

Composite line + columns (color/intensity reflect direction & strength).

Entry/Exit bands with green/red fills for quick polarity reads.

Hidden plots for each Theme if you want to show them.

Optional rebalance labels (direction, gross & signed exposure, σ).

Background heatmap keyed to Composite.

Alerts

Enter/Inc LONG when Composite crosses up (and on rebalance bars).

Enter/Inc SHORT when Composite crosses down (and on rebalance bars).

Exit to FLAT when Composite returns toward neutral (and on rebalance bars).

Practical tips

Start higher timeframes. Daily signals with Monthly rebalance are a good baseline; weekly signals with quarterly rebalances are even cleaner.

Tune Entry/Exit bands before anything else. Wider bands = fewer trades and less noise.

Weights reflect regime. If policy dominates markets, raise Monetary Policy weight; if credit stress drives moves, raise Risk Sentiment.

Proxies are swappable. Use UUP for USD, or futures-continuous symbols that match your data plan.

Futures vs ETFs. Quantity auto-rounds for futures; ETFs accept fractional shares. Check contract multipliers when interpreting exposure.

Caveats

Macro proxies can repaint at the selected signal timeframe as higher-TF bars form; that’s intentional for macro sampling, but test live.

Vol targeting assumes reasonably stationary realized vol over the lookback; if markets regime-shift, revisit volLook and targetVol.

If you disable normalization/winsorization, themes can become spikier; expect more hysteresis band crossings.

What to change first (quick start)

Set Signal Timeframe = D, Rebalance = Monthly, Z-score on, Winsor on (MAD).

Entry/Exit bands: 0.25 / 0.12 (defaults), then nudge until trade count and turnover feel right.

TargetVol: try 10% for diversified indices; lower for single stocks, higher for vol-sell strategies.

Leave weights = 1.0 until you’ve inspected the four theme lines; then tilt deliberately.

高频策略优化版-空头Open Condition Reversal: Change the condition of the TEMA fast line above the slow line to the condition of the fast line below the slow line RSI condition from " buy above the threshold " to " short below the threshold ", and adjust the default threshold from 30 to 70 (more suitable for shorting overbought area) moving average direction judgment from up to down stop-loss direction adjustment: Short stop-loss Settings above the entry price (entry price * (1 + i _ sl) ) Short stop-loss set below the entry price (entry price * (1-tp) Tracking stop-loss level adjusted to below the entry price MACD logic adjustment: Preferred use of the bearish pattern as a short signal bullish pattern for closing risk management: Maintained a dynamic stop-loss mechanism, adjusted to protect the market from the bottom of the visual stop-loss strategy: The visual marking of the ACD energy column is convenient for monitoring signals to be fully tested before use, especially for adjusting RSI thresholds and stop-loss parameters to suit the characteristics of specific trading varieties.

三均線中頻策略 v3.0 - R=2.5 + 進場點點標記📌 Core Strategy Concept

This is a medium-frequency trend-following model that utilizes three Simple Moving Averages to determine bullish or bearish alignment. It then enters trades in the direction of the trend when price confirms a breakout and applies a fixed risk-to-reward ratio (R). Stop loss and take profit levels are dynamically calculated based on moving averages, ensuring clear risk control and systematic execution.

✅ Strategy Advantages

📏 Clear Rules Trade conditions based on triple SMA alignment and price breakout; easy to replicate.

🛡 Defined Risk Stop loss and take profit are calculated based on moving averages with a fixed R ratio, ensuring disciplined risk management.

⚖️ Balanced Frequency Medium trade frequency avoids overtrading while still capturing sufficient opportunities.

👁 Visual Markers Entry points are visually marked on the chart for easy backtesting and live tracking.

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.