Alpha Trigger CoreAlpha Trigger Core — Trend Momentum Strategy with Dual Take Profit System

Alpha Trigger Core is a precision-engineered trend-following strategy developed for crypto and altcoin markets. Unlike simple indicator mashups, this system was built from the ground up with a specific logic framework that integrates trend, momentum, volatility, and structure validation into a single unified strategy.

It is not a random combination of indicators, but rather a coordinated system of filters that work together to increase signal quality and minimize false positives. This makes it especially effective on trending assets like BTC, ETH, AVAX, and SOL on the 1-hour chart.

🔍 How It Works

This strategy fuses multiple advanced filters into a cohesive signal engine:

🔹 Trend Identification

A hybrid model combining:

Kalman Filter — Smooths price noise with predictive tracking.

SuperTrend Overlay — Confirms directional bias using ATR.

ZLEMA Envelope — Defines dynamic upper/lower bounds based on price velocity.

🔹 Momentum Filter

Uses a ZLEMA-smoothed CCI to identify accelerating moves.

Long entries require a rising 3-bar CCI sequence.

Short entries require a falling 3-bar CCI sequence.

🔹 Volatility Strength Filter (Vortex Indicator)

Validates entries only when Vortex Diff exceeds a customizable threshold.

Prevents low-volatility "chop zone" trades.

🔹 Wick Trap Filter

Filters out false breakouts driven by liquidity wicks.

Validates that body structure supports the breakout.

📈 Entry & Exit Logic

Long Entry: All trend, momentum, volatility filters must align bullishly and wick traps must be absent.

Short Entry: All filters must align bearishly, with no wick rejection.

Early Exit: Uses ZLEMA slope crossover to exit before a full trend reversal is confirmed.

🎯 Take Profit System

TP1: Takes 50% profit at a user-defined % target.

TP2: Closes remaining 100% at second target.

Cooldown: Prevents immediate reentry and ensures clean position transitions.

📊 Real-Time Strategy Dashboard

Tracks and displays:

Position status (Long, Short, Flat)

Entry Price

TP1/TP2 Hit status

Win Rate (%)

Profit Factor

Bars Since Entry

Fully customizable position & font size

🤖 Bot-Ready Multi-Exchange Alerts

Compatible with WonderTrading, 3Commas, Binance, Bybit, and more.

Customizable comment= tags for entry, exit, TP1, and TP2.

Fully alert-compatible for webhook integrations.

📌 Suggested Use

Best used on trending crypto pairs with moderate-to-high volatility. Recommended on the 1H timeframe for altcoins and majors. Can be used for manual confirmation or automated trading.

🔒 Script Transparency

This is a closed-source script. However, the description above provides a transparent breakdown of the strategy’s core logic, filters, and execution model — ensuring compliance with TradingView’s publishing guidelines.

⚠️ Trading Disclaimer

This script is for educational purposes only and is not financial advice. Always conduct your own analysis before making investment decisions. Past performance does not guarantee future results. Use this strategy at your own risk.

Поиск скриптов по запросу "bear"

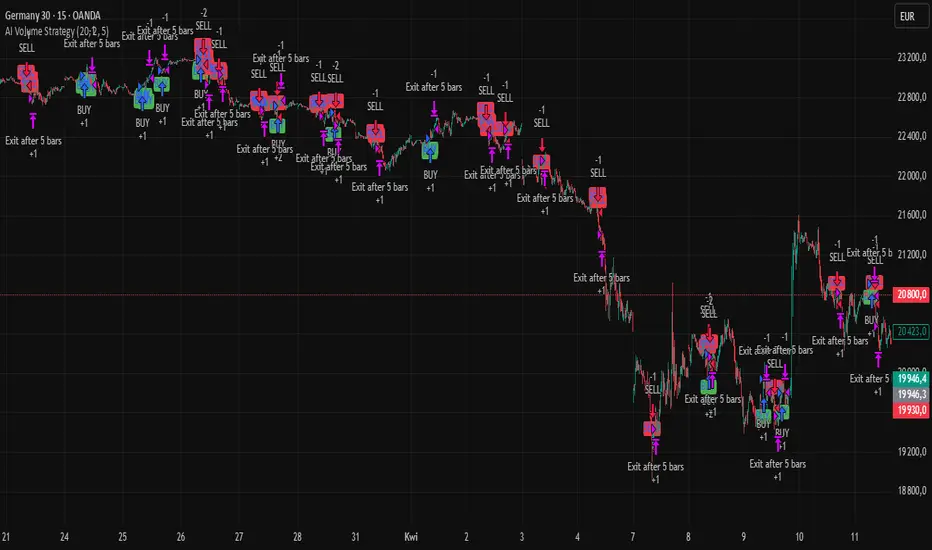

AI Volume StrategyAI Volume Strategy detects significant volume spikes and combines them with trend direction and candlestick color to generate buy and sell signals. The strategy uses an Exponential Moving Average (EMA) of volume to identify abnormal volume spikes that may indicate strong market activity. Additionally, it uses a 50-period EMA of price to filter the trend and decide on entry direction.

Key Features:

Volume Spike Detection: The strategy detects when the current volume exceeds the EMA of volume by a user-defined multiplier, signaling abnormal increases in market activity.

Trend Direction Filter: The strategy uses a 50-period EMA of price to determine the market trend. Buy signals are generated when the price is above the EMA (uptrend), and sell signals are generated when the price is below the EMA (downtrend).

Candle Color Filter: The strategy generates a buy signal only when the current candle is bullish (green) and a sell signal only when the current candle is bearish (red).

Exit after X Bars: The strategy automatically closes the position after a specified number of bars (default is 5 bars), but the exit condition can be adjusted based on user preference, timeframe, and backtesting results. The default exit is after 5 bars, but users can set it to 1 bar or any other number depending on their preferences and strategy.

Signals:

Buy Signal: Generated when a volume spike occurs, the trend is upward, and the current candle is bullish.

Sell Signal: Generated when a volume spike occurs, the trend is downward, and the current candle is bearish.

Alerts:

Buy Alert: Alerts the user when a buy signal is triggered.

Sell Alert: Alerts the user when a sell signal is triggered.

Visualization:

Buy Signal: A green label appears below the bar when the buy conditions are met.

Sell Signal: A red label appears above the bar when the sell conditions are met.

Volume EMA: Optionally, the Volume EMA line can be plotted on the chart to visualize volume trends.

This strategy helps traders identify potential entry points based on increased volume activity while considering trend direction and candlestick patterns. With the ability to adjust the exit condition, users can fine-tune the strategy to their specific needs and backtest results.

02 SMC + BB Breakout (Improved)This strategy combines Smart Money Concepts (SMC) with Bollinger Band breakouts to identify potential trading opportunities. SMC focuses on identifying key price levels and market structure shifts, while Bollinger Bands help pinpoint overbought/oversold conditions and potential breakout points. The strategy also incorporates higher timeframe trend confirmation to filter out trades that go against the prevailing trend.

Key Components:

Bollinger Bands:

Calculated using a Simple Moving Average (SMA) of the closing price and a standard deviation multiplier.

The strategy uses the upper and lower bands to identify potential breakout points.

The SMA (basis) acts as a centerline and potential support/resistance level.

The fill between the upper and lower bands can be toggled by the user.

Higher Timeframe Trend Confirmation:

The strategy allows for optional confirmation of the current trend using a higher timeframe (e.g., daily).

It calculates the SMA of the higher timeframe's closing prices.

A bullish trend is confirmed if the higher timeframe's closing price is above its SMA.

This helps filter out trades that go against the prevailing long-term trend.

Smart Money Concepts (SMC):

Order Blocks:

Simplified as recent price clusters, identified by the highest high and lowest low over a specified lookback period.

These levels are considered potential areas of support or resistance.

Liquidity Zones (Swing Highs/Lows):

Identified by recent swing highs and lows, indicating areas where liquidity may be present.

The Swing highs and lows are calculated based on user defined lookback periods.

Market Structure Shift (MSS):

Identifies potential changes in market structure.

A bullish MSS occurs when the closing price breaks above a previous swing high.

A bearish MSS occurs when the closing price breaks below a previous swing low.

The swing high and low values used for the MSS are calculated based on the user defined swing length.

Entry Conditions:

Long Entry:

The closing price crosses above the upper Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bullish.

A bullish MSS must have occurred.

Short Entry:

The closing price crosses below the lower Bollinger Band.

If higher timeframe confirmation is enabled, the higher timeframe trend must be bearish.

A bearish MSS must have occurred.

Exit Conditions:

Long Exit:

The closing price crosses below the Bollinger Band basis.

Or the Closing price falls below 99% of the order block low.

Short Exit:

The closing price crosses above the Bollinger Band basis.

Or the closing price rises above 101% of the order block high.

Position Sizing:

The strategy calculates the position size based on a fixed percentage (5%) of the strategy's equity.

This helps manage risk by limiting the potential loss per trade.

Visualizations:

Bollinger Bands (upper, lower, and basis) are plotted on the chart.

SMC elements (order blocks, swing highs/lows) are plotted as lines, with user-adjustable visibility.

Entry and exit signals are plotted as shapes on the chart.

The Bollinger band fill opacity is adjustable by the user.

Trading Logic:

The strategy aims to capitalize on Bollinger Band breakouts that are confirmed by SMC signals and higher timeframe trend. It looks for breakouts that align with potential market structure shifts and key price levels (order blocks, swing highs/lows). The higher timeframe filter helps avoid trades that go against the overall trend.

In essence, the strategy attempts to identify high-probability breakout trades by combining momentum (Bollinger Bands) with structural analysis (SMC) and trend confirmation.

Key User-Adjustable Parameters:

Bollinger Bands Length

Standard Deviation Multiplier

Higher Timeframe

Higher Timeframe Confirmation (on/off)

SMC Elements Visibility (on/off)

Order block lookback length.

Swing lookback length.

Bollinger band fill opacity.

This detailed description should provide a comprehensive understanding of the strategy's logic and components.

***DISCLAIMER: This strategy is for educational purposes only. It is not financial advice. Past performance is not indicative of future results. Use at your own risk. Always perform thorough backtesting and forward testing before using any strategy in live trading.***

Advanced Adaptive Grid Trading StrategyThis strategy employs an advanced grid trading approach that dynamically adapts to market conditions, including trend, volatility, and risk management considerations. The strategy aims to capitalize on price fluctuations in both rising (long) and falling (short) markets, as well as during sideways movements. It combines multiple indicators to determine the trend and automatically adjusts grid parameters for more efficient trading.

How it Works:

Trend Analysis:

Short, long, and super long Moving Averages (MA) to determine the trend direction.

RSI (Relative Strength Index) to identify overbought and oversold levels, and to confirm the trend.

MACD (Moving Average Convergence Divergence) to confirm momentum and trend direction.

Momentum indicator.

The strategy uses a weighted scoring system to assess trend strength (strong bullish, moderate bullish, strong bearish, moderate bearish, sideways).

Grid System:

The grid size (the distance between buy and sell levels) changes dynamically based on market volatility, using the ATR (Average True Range) indicator.

Grid density also adapts to the trend: in a strong trend, the grid is denser in the direction of the trend.

Grid levels are shifted depending on the trend direction (upwards in a bear market, downwards in a bull market).

Trading Logic:

The strategy opens long positions if the trend is bullish and the price reaches one of the lower grid levels.

It opens short positions if the trend is bearish and the price reaches one of the upper grid levels.

In a sideways market, it can open positions in both directions.

Risk Management:

Stop Loss for every position.

Take Profit for every position.

Trailing Stop Loss to protect profits.

Maximum daily loss limit.

Maximum number of positions limit.

Time-based exit (if the position is open for too long).

Risk-based position sizing (optional).

Input Options:

The strategy offers numerous settings that allow users to customize its operation:

Timeframe: The chart's timeframe (e.g., 1 minute, 5 minutes, 1 hour, 4 hours, 1 day, 1 week).

Base Grid Size (%): The base size of the grid, expressed as a percentage.

Max Positions: The maximum number of open positions allowed.

Use Volatility Grid: If enabled, the grid size changes dynamically based on the ATR indicator.

ATR Length: The period of the ATR indicator.

ATR Multiplier: The multiplier for the ATR to fine-tune the grid size.

RSI Length: The period of the RSI indicator.

RSI Overbought: The overbought level for the RSI.

RSI Oversold: The oversold level for the RSI.

Short MA Length: The period of the short moving average.

Long MA Length: The period of the long moving average.

Super Long MA Length: The period of the super long moving average.

MACD Fast Length: The fast period of the MACD.

MACD Slow Length: The slow period of the MACD.

MACD Signal Length: The period of the MACD signal line.

Stop Loss (%): The stop loss level, expressed as a percentage.

Take Profit (%): The take profit level, expressed as a percentage.

Use Trailing Stop: If enabled, the strategy uses a trailing stop loss.

Trailing Stop (%): The trailing stop loss level, expressed as a percentage.

Max Loss Per Day (%): The maximum daily loss, expressed as a percentage.

Time Based Exit: If enabled, the strategy exits the position after a certain amount of time.

Max Holding Period (hours): The maximum holding time in hours.

Use Risk Based Position: If enabled, the strategy calculates position size based on risk.

Risk Per Trade (%): The risk per trade, expressed as a percentage.

Max Leverage: The maximum leverage.

Important Notes:

This strategy does not guarantee profits. Cryptocurrency markets are volatile, and trading involves risk.

The strategy's effectiveness depends on market conditions and settings.

It is recommended to thoroughly backtest the strategy under various market conditions before using it live.

Past performance is not indicative of future results.

3Commas Multicoin Scalper PRO [SwissAlgo]Introduction

Are you tired of tracking dozens of cryptocurrency charts and placing orders manually on your Exchange?

The 3Commas Multicoin Scalper PRO is an automated trading system designed to simultaneously identify and execute potential trading setups on multiple cryptocurrencies on your preferred Exchange (Binance, Bybit, OKX, Gate.io, Bitget) via 3Commas integration.

It analyzes price action, volume, momentum, volatility, and trend patterns across 180+ USDT Perpetual coins divided into 17 crypto categories , providing real-time signals directly to your 3Commas bots for automated trade execution. This indicator aims to identify potential trend-following and contrarian setups in both bull and bear markets.

-------------------------------------

What it Does

The 3Commas Multicoin Scalper PRO is a technical analysis tool that monitors multiple cryptocurrency pairs simultaneously and connects with 3Commas for signal delivery and execution.

Here's how the strategy works:

🔶 Technical Analysis : Analyzes price action, volume, momentum, volatility, and trend patterns across multiple USDT Perpetual Futures contracts simultaneously.

🔶 Pattern Detection : Identifies specific candle patterns and technical confluences that suggest potential trading setups across all USDT.P contracts of the selected categories

🔶 Signal Generation : When technical criteria are met at bar close, the indicator creates deal-start signals for the relevant pairs.

🔶 3Commas Integration : Packages these signals and delivers them to 3Commas through TradingView alerts, allowing 3Commas bots to receive specific pair information ('Deal-Start' signals).

🔶 Category Management : Each TradingView alert monitors an entire category (approximately 11 pairs), allowing selective activation of different crypto categories.

🔶 Visual Feedback : Provides color-coded candles and backgrounds to visualize technical conditions, with optional pivot points and trend visualization.

Candle types:

Signals:

-------------------------------------

Quick Start Guide

1. Setup 3Commas Bots : Configure two DCA bots in 3Commas (All USDT pairs) - one for LONG positions and one for SHORT positions.

2. Define Trading Parameters : Set your budget for each trade and adjust your preferred sensitivity within the indicator settings.

3. Create Category Alerts : Set up one TradingView alert for each crypto category you want to trade.

That's it! Once configured, the system automatically sends signals to your 3Commas bots when predefined trading setups are detected across coins in your selected/activated categories. The indicator scans all coins at bar close (for example, every hour on the 1H timeframe) and triggers trade execution only for those showing technical confluences.

Important : The more categories you activate by setting TradingView alerts, the more signals your 3Commas bots will receive. Consider your total capital when enabling multiple categories. More details about the setup process are provided below (see paragraph "Detailed Setup & Configuration")

-------------------------------------

Built-in Backtesting

The 3Commas Multicoin Scalper PRO includes backtesting visualization for each coin. When viewing any USDT Perpetual pair on your chart, you can visualize how the strategy would have performed historically on that specific asset.

Color-coded candles and signal markers show past trading setups, helping you evaluate which coins responded best to the strategy. This built-in backtesting capability can support your selection of assets/categories to trade before deploying real capital.

As backtesting results are hypothetical and do not guarantee future performance, your research and analysis are essential for selecting the crypto categories/coins to trade.

The default strategy settings are: Start Capital 1.000$, leverage 25X, Commissions 0.1% (average Taker Fee on Exchanges for average users), Order Amount 200$ for Longs/150$ for Shorts, Slippage 4

-------------------------------------

Key Features

🔶 Multi-Exchange Support : Compatible with BINANCE, BYBIT, BITGET, GATEIO, and OKX USDT Perpetual markets (USDT.P)

🔶 Wide Asset Coverage : Simultaneously analyzes 180+ cryptocurrencies across 17 specialized crypto categories

🔶 Custom Category Option : Create your watchlist with up to 10 custom USDT Perpetual pairs

🔶 3Commas Integration : Seamlessly connects with 3Commas bots to automate trade entries and exits

🔶 Dual Strategy Approach : Identifies both "trend following" and "contrarian" potential setups

🔶 Confluence-Based Signals : Uses a combination of multiple technical factors - price spikes, price momentum, volume spikes, volume momentum, trend analysis, and volatility spikes - to generate potential trading setups

🔶 Risk Management : Adjustable sensitivity/risk levels, leverage settings, and budget allocation for each trade

🔶 Visual Indicators : Color-coded candles and trading signals provide visual feedback on market conditions

🔶 Trend Indication : Background colors showing ongoing uptrends/downtrends

🔶 Pivot Points & Daily Open : Optional display of pivot points and daily open price for additional context

🔶 Liquidity Analysis : Optional display of high/low liquidity timeframes throughout the trading week

🔶 Trade Control : Configurable limit for the maximum number of signals sent to 3Commas for execution (per bar close and category)

Available Exchanges

Categories

Custom Category

Trend following/contrarian signals

-------------------------------------

Methodology

The 3Commas Multicoin Scalper PRO utilizes a multi-faceted approach to identify potential trading setups:

1. Price Action Analysis : Detects abnormal price movements by comparing the current candle's range to historical averages and standard deviations, helping identify potential "pump and dump" scenarios or new-trends start

2. Price Momentum : Evaluates the relative strength of bullish vs. bearish price movements over time, indicating the build-up of buying or selling pressure.

3. Volume Analysis: Identifies unusual volume spikes by comparing current volume to historical averages, signaling strong market interest in a particular direction.

4. Volume Momentum : Measures the ratio of bullish to bearish volume, revealing the dominance of buyers or sellers over time.

5. Trend Analysis : Combines EMA slopes, RSI, and Stochastic RSI to determine overall trend direction and strength.

6. Volatility : Monitors the ATR (Average True Range) to detect periods of increased market volatility, which may indicate potential breakouts or reversals

7. Candle Wick Analysis : Evaluates upper and lower wick percentages to detect potential rejection patterns and reversals.

8. Pivot Point Analysis : Uses pivot points (PP, R1-R3, S1-S3) for identifying key support/resistance areas and potential breakout/breakdown levels.

9. Daily Open Reference: Analyzes price action relative to the daily open for potential setups related to price movement vs. the opening price

10. Market Timing/Liquidity : Evaluates high/low liquidity periods, specific days/times of heightened risk, and potential market manipulation timeframes.

11. Boost Factors : Applies additional weight to certain confluence patterns to adjust global scores

These factors are combined into a "Global Score" ranging from -1 to +1 , applied at bar close to the newly formed candles.

Scores above predefined thresholds (configurable via the Sensitivity Settings) indicate strong bullish or bearish conditions and trigger signals based on predefined patterns. The indicator then applies additional filters to generate specific "Trend Following" and "Contrarian" trading signals. The identified signals are packaged and sent to 3Commas for execution.

Pivot Points

Daily open

Market Trend

Liquidity patterns by weekday

-------------------------------------

Who This Strategy Is For?

The 3Commas Multicoin Scalper PRO may benefit:

Crypto Traders seeking to automate their trading across multiple coins simultaneously

3Commas Users looking to enhance their bot performance with advanced technical signals

Busy Traders who want to monitor many market opportunities without constant chart-watching

Multi-strategy traders interested in both trend-following and reversal trading approaches

Traders of Various Experience Levels from intermediate traders wanting to save time to advanced traders seeking to scale their operations

Perpetual Futures Traders on major exchanges (Binance, Bybit, OKX, Gate.io, Bitget)

Swing and Scalp Traders seeking to identify short to medium-term profit opportunities

-------------------------------------

Visual Indicators

The indicator provides visual feedback through:

1. Candlestick Colors :

* Lime: Strong bullish candle (High positive score)

* Blue: Moderate bullish candle (Medium positive score)

* Red: Strong bearish candle (High negative score)

* Purple: Moderate bearish candle (Medium negative score)

* Pale Green/Red: Mild bullish/bearish candle

2. Signal Markers :

* ↗: Trend Following Long signal

* ↘: Trend Following Short signal

* ⤴: Contrarian Long signal

* ⤵: Contrarian Short signal

3. Optional Elements :

* Pivot Points: Daily support/resistance levels (R1-R3, S1-S3, PP)

* Daily Open: Reference price level for the current trading day

* Trend Background: Color-coded background suggesting potential ongoing uptrend/downtrend

* Liquidity Highlighting: Background colors indicating typical high/low market liquidity periods

4. TradingView Strategy Plots and Backtesting Data : Standard performance metrics showing entry/exit points, equity curves, and trade statistics, based on the signals generated by the script.

-------------------------------------

Detailed Setup & Configuration

The indicator features a user-friendly input panel organized in sequential steps to guide you through the complete setup process. Tooltips for each step provide additional information to help you understand the actions required to get the strategy running.

Informative tables provide additional details and instructions for critical setup steps such as 3Commas bot configuration and TradingView alert creation (to activate trading on specific categories).

1. Choose Exchange, Crypto Category & Sensitivity

* Select your USDT Perpetual Exchange (BINANCE, BYBIT, BITGET, GATEIO, or OKX) - i.e. the same Exchange connected in your 3Commas account

* Browse and choose your preferred crypto category, or define your watchlist

* Choose from three sensitivity levels: Default, Aggressive, or Test Mode (test mode is designed to generate way more signals, a potentially helpful feature when you are testing the indicator and alerts)

2. Setup 3Commas Bots and integrate them with the algo

* Create both LONG and SHORT DCA Bots in 3Commas

* Configure bots to accept signals for 'All USDT Pairs' with "TradingView Custom Signal" as deal start condition

* Enter your Bot IDs and Email Token in the indicator settings

* Set a maximum budget for LONG and SHORT trades

* Choose whether to allow LONG trades, SHORT trades, or both, according to your preference and market analysis

* Set maximum trades per bar/category (i.e. the max. number of simultaneous signals that the algo may send to your 3Commas bots for execution at every bar close - every hour if you set the 1H timeframe)

* Access the detailed setup guide table for step-by-step 3Commas configuration instructions

3Commas integration

3. Choose Visuals

* Toggle various optional visual elements to add to the chart: category metrics, fired alerts, coin metrics, daily open, pivot points

* Select a color theme: Dark or Light

4. Activate Trading via Alerts

* Create TradingView alerts for each category you want to trade

* Set alert condition to "3Commas Multicoin Scalper" with "Any alert() function call"

* Set the content of the message filed to: {{Message}}, deleting the default content shown in this text field, to enable proper 3Commas integration (any other text than {{Message}}, would break the delivery trading signals from Tradingview to 3Commas)

* View the alerts setup instruction table for visual guidance on this critical step

Alerts

Fired Alerts

Important Configuration Notes

Ensure that the TradingView chart's exchange matches your selected exchange in the indicator settings and your 3Commas bot settings.

You must configure the same leverage in both the script and your 3Commas bots

Your 3Commas bots must be configured for All USDT pairs

You must enter the exact Bot IDs and Email Token from 3Commas (these remain confidential - no one, including us, has access to them)

If you activate multiple categories without sufficient capital, 3Commas will display " insufficient funds " errors - align your available capital with the number of categories you activate (each deal will use the budget amount specified in user inputs)

You are free to set your Take Profit % / trailing on 3Commas

We recommend not to use DCA orders (i.e. set the number of DCA orders at zero)

Legend of symbols

-------------------------------------

FAQs

General Questions

❓ Q: What is Global Score? A: The Global Score serves as a foundation for signal generation. When a candle's score exceeds certain thresholds (defined by your Risk Level setting), it becomes a candidate for signal generation. However, not all high-scoring candles generate trading signals - the indicator applies additional pattern recognition and contextual filters. For example, a strongly positive score (lime candle) in an established uptrend may trigger a "Trend Following" signal, while a strongly negative score (red candle) in a downtrend might generate a "Trend Following Short" signal. Similarly, contrarian signals are generated when specific reversal patterns occur alongside appropriate Global Score values, often involving wick analysis and pivot point interactions. This multi-layer approach helps filter out false positives and identify higher-probability trading setups.

❓ Q: What's the difference between "Trend following" and "Contrarian" signals in the script? A: "Trend Following" signals follow the identified trends while "Contrarian" signals anticipate potential trend reversals.

❓ Q: Why can't I configure all the parameters? A: We've designed the solution to be plug-and-play to prevent users from getting lost in endless configurations. The preset values have been tested against their trade-offs in terms of financial performance, average trade duration, and risk levels.

❓ Q: Why don't I see any signals on my chart? A: Make sure you're viewing a USDT Perpetual pair from your selected exchange that belongs to the crypto category you've chosen to analyze. For example, if you've selected the "Top Major Coins" category with Binance as your exchange, you need to view a chart of one of those specific pairs (like BINANCE:BTCUSDT.P) to see signals. If you switch exchanges, for example from Binance to Bybit, you need to pull a Bybit pair on the chart to see backtesting data and signals.

❓ Q: Does this indicator guarantee profits? A: No. Trading cryptocurrencies involves significant risk, and past performance is not indicative of future results. This indicator is a tool to help you identify potential trading setups, but it does not and cannot guarantee profits.

❓ Q: Does this indicator repaint or use lookahead bias? A: No. All trading signals generated by this indicator are based only on completed price data and do not repaint. The system is designed to ensure that backtesting results reflect as closely as possible what you should experience in live trading.

While reference levels like pivot points are kept stable throughout the day using lookahead on, the actual buy and sell signals are calculated using only historical data (lookahead off) that would have been available at that moment in time. This ensures reliability and consistency between backtesting and real-time trading performance.

Technical Setup

❓ Q: What exchanges are supported? A: The strategy supports BINANCE, BYBIT, BITGET, GATEIO, and OKX USDT Perpetual markets (i.e. all the Exchanges you can connect to your 3Commas account for USDT Perpetual trading, excluding Coinbase Perpetual that offers UDSC pairs, instead of USDT).

❓ Q: What timeframe should I use? A: The indicator is optimized for the 1-hour (1H) timeframe but may run on any timeframe.

❓ Q: How many coins can I trade at once? A: You can trade all coins within each selected category (up to 11 coins per category in standard categories). You can activate multiple categories by setting up multiple alerts.

❓ Q: How many alerts do I need to set up? A: You need to set up one alert for each crypto category you want to trade. For example, if you want to trade both the "Top Major Coins" and the "DeFi" categories, you'll need to create two separate alerts, one for each category. We recommend starting with one category, testing the results carefully, monitoring performance daily, and perhaps activating additional categories in a second stage.

❓ Q: Are there any specific risk management features built into the indicator? A: Yes, the indicator includes risk management features: adjustable maximum trades per hour/category, the ability to enable/disable long or short signals depending on market conditions, customizable trade size for both long and short positions, and different sensitivity/risk level settings.

❓ Q: What happens if 3Commas can't execute a signal? A: If 3Commas cannot execute a signal (due to insufficient funds, bot offline, etc.), the trade will be skipped. The indicator will continue sending signals for other valid setups, but it doesn't retry failed signals.

❓ Q: Can I run this indicator on multiple charts at once? A: Yes, but it's not necessary. The indicator analyzes all coins in your selected categories regardless of which chart you apply it to. For optimal resource usage, apply it to a single chart of a USDT Perpetual pair from your selected exchange. To stop trading a category delete the alert created for that category.

❓ Q: How frequently does the indicator scan for new signals? A: The indicator scans all coins in your selected categories at the close of each bar (every hour if you selected the 1H timeframe).

3Commas Integration

❓ Q: Do I need a 3Commas account? A: Yes, a 3Commas account with active DCA bots (both LONG and SHORT) is required for automated trade execution. A paid subscription is needed, as multipair Bots and multiple simultaneous deals are involved.

❓ Q: How do I set the leverage? A: Set the leverage identically in both the indicator settings and your 3Commas DCA bots (the max supported leverage is 50x). Always be careful about leverage, as it amplifies both profits and losses.

❓ Q: Where do I find my 3Commas Bot IDs and Email Token? A: Open your 3Commas DCA bot and scroll to the "Messages" section. You'll find the Bot ID and Email Token within any message (e.g., "Start Deal").

Display Settings

❓ Q: What does the Sensitivity setting do? A: It adjusts the sensitivity of signal generation. "Default" provides a balanced approach with moderate signal frequency. "Aggressive" lowers the thresholds for signal generation, potentially increasing trade frequency but may include more noise. "Test Mode" is the most sensitive setting, useful for testing alert configurations but not recommended for live trading. Higher risk levels may generate more signals but with potentially lower average quality, while lower risk levels produce fewer but potentially better signals.

❓ Q: What does "Show fired alerts" do? A: The "Show fired alerts" option displays a label on your chart showing which signals have been fired and sent to 3Commas during the most recent candle closes. This visual indicator helps you confirm that your alerts are working properly and shows which coins from your selected category have triggered signals. It's useful when setting up and testing the system, allowing you to verify that signals are being sent to 3Commas as expected and their frequency over time.

❓ Q: What does "Show coin/token metrics" do? A: This toggle displays detailed technical metrics for the specific coin/token currently shown on your chart. When enabled, it shows statistics for the last closed candle for that coin.

❓ Q: What does "Show most liquid days/times" do? A: This toggle displays color-coded background highlighting to indicate periods of varying market liquidity throughout the trading week. Green backgrounds show generally higher liquidity periods (typically weekday trading hours), yellow highlights potentially manipulative periods (often Sunday/Monday overnight), and gray indicates low liquidity periods (when major markets are closed or during late hours).

⚠️ Disclaimer

This indicator is for informational and educational purposes only and does not constitute financial advice. Trading cryptocurrencies involves significant risk, including the potential loss of all invested capital, and past performance is not indicative of future results.

Always conduct your own thorough research (DYOR) and understand the risks involved before making any trading decisions. Trading with leverage significantly amplifies both potential profits and losses - exercise extreme caution when using leverage and never risk more than you can afford to lose.

The Bot ID and Email Token information are transmitted directly from TradingView to 3Commas via secure connections. No third party or entity will ever have access to this data (including the Author). Do not share your 3Commas credentials with anyone.

This indicator is not affiliated with, endorsed by, or sponsored by TradingView or 3Commas.

Strategy SuperTrend SDI WebhookThis Pine Script™ strategy is designed for automated trading in TradingView. It combines the SuperTrend indicator and Smoothed Directional Indicator (SDI) to generate buy and sell signals, with additional risk management features like stop loss, take profit, and trailing stop. The script also includes settings for leverage trading, equity-based position sizing, and webhook integration.

Key Features

1. Date-based Trade Execution

The strategy is active only between the start and end dates set by the user.

times ensures that trades occur only within this predefined time range.

2. Position Sizing and Leverage

Uses leverage trading to adjust position size dynamically based on initial equity.

The user can set leverage (leverage) and percentage of equity (usdprcnt).

The position size is calculated dynamically (initial_capital) based on account performance.

3. Take Profit, Stop Loss, and Trailing Stop

Take Profit (tp): Defines the target profit percentage.

Stop Loss (sl): Defines the maximum allowable loss per trade.

Trailing Stop (tr): Adjusts dynamically based on trade performance to lock in profits.

4. SuperTrend Indicator

SuperTrend (ta.supertrend) is used to determine the market trend.

If the price is above the SuperTrend line, it indicates an uptrend (bullish).

If the price is below the SuperTrend line, it signals a downtrend (bearish).

Plots visual indicators (green/red lines and circles) to show trend changes.

5. Smoothed Directional Indicator (SDI)

SDI helps to identify trend strength and momentum.

It calculates +DI (bullish strength) and -DI (bearish strength).

If +DI is higher than -DI, the market is considered bullish.

If -DI is higher than +DI, the market is considered bearish.

The background color changes based on the SDI signal.

6. Buy & Sell Conditions

Long Entry (Buy) Conditions:

SDI confirms an uptrend (+DI > -DI).

SuperTrend confirms an uptrend (price crosses above the SuperTrend line).

Short Entry (Sell) Conditions:

SDI confirms a downtrend (+DI < -DI).

SuperTrend confirms a downtrend (price crosses below the SuperTrend line).

Optionally, trades can be filtered using crossovers (occrs option).

7. Trade Execution and Exits

Market entries:

Long (strategy.entry("Long")) when conditions match.

Short (strategy.entry("Short")) when bearish conditions are met.

Trade exits:

Uses predefined take profit, stop loss, and trailing stop levels.

Positions are closed if the strategy is out of the valid time range.

Usage

Automated Trading Strategy:

Can be integrated with webhooks for automated execution on supported trading platforms.

Trend-Following Strategy:

Uses SuperTrend & SDI to identify trend direction and strength.

Risk-Managed Leverage Trading:

Supports position sizing, stop losses, and trailing stops.

Backtesting & Optimization:

Can be used for historical performance analysis before deploying live.

Conclusion

This strategy is suitable for traders who want to automate their trading using SuperTrend and SDI indicators. It incorporates risk management tools like stop loss, take profit, and trailing stop, making it adaptable for leverage trading. Traders can customize settings, conduct backtests, and integrate it with webhooks for real-time trade execution. 🚀

Important Note:

This script is provided for educational and template purposes and does not constitute financial advice. Traders and investors should conduct their research and analysis before making any trading decisions.

FVG Breakout Lite by tradingbauhausExplanation of "FVG Breakout Lite by tradingbauhaus"

This script is a trading strategy built for TradingView that helps you spot and trade "Fair Value Gaps" (FVGs)—price areas where the market moved quickly, leaving a gap that might act as support or resistance later. It’s designed to catch breakout opportunities when the price moves strongly in one direction, with extra filters to make trades more reliable. Here’s how it works and how you can use it:

What It Does

1. Finds Fair Value Gaps (FVGs):

A "Bullish FVG" happens when the price jumps up quickly, leaving a gap below where it didn’t trade much (e.g., today’s low is higher than the high from two bars ago).

A "Bearish FVG" is the opposite: the price drops fast, leaving a gap above (e.g., today’s high is lower than the low from two bars ago).

The script draws colored boxes on your chart to show these gaps: green for bullish, red for bearish.

2. Spots Breakouts:

It looks for "strong" FVGs by comparing them to a trend (based on the highest highs and lowest lows over a set period).

If a bullish gap forms above the recent highs, or a bearish gap below the recent lows, it’s marked as a breakout opportunity.

3. Adds a Volume Check:

Trades only happen if the market’s volume is higher than usual (e.g., 1.2x the average volume over the last 20 bars). This helps ensure the breakout has real momentum behind it.

4. Trades Automatically:

Long Trades (Buy): If a bullish breakout FVG forms and volume is high, it buys at the current price.

Short Trades (Sell): If a bearish breakout FVG forms with high volume, it sells short.

Each trade comes with a stop loss (to limit losses) and a take profit (to lock in gains), both adjustable by you.

5. Shows Mitigation Lines (Optional):

If you turn on "Display Mitigation Zones," it draws lines at the edge of each breakout FVG. These lines show where the price might return to "fill" the gap later, helping you see key levels.

6. Includes Webull Costs:

The script factors in real trading fees from Webull, like tiny SEC and FINRA fees for selling, and a daily margin cost if you’re borrowing money to trade. These don’t show up on the chart but affect the strategy’s performance in backtesting.

How to Use It

1. Add to Your Chart:

Copy the script into TradingView’s Pine Editor, click "Add to Chart," and it’ll start drawing FVGs and running the strategy.

2. Customize Settings:

Trend Period (Default: 25): How many bars it looks back to define the trend. Longer periods mean fewer but stronger signals.

Volume Lookback (Default: 20) & Volume Threshold (Default: 1.2): Adjust how it measures "high volume." Increase the threshold for stricter trades.

Stop Loss % (Default: 1.5%) & Take Profit % (Default: 3%): Set how much you’re willing to lose or aim to gain per trade.

Margin Rate % (Default: 8.74%): Webull’s rate for borrowing money—lower it if your account qualifies for a better rate.

Display Mitigation Zones (Default: On): Toggle this to see or hide the gap lines.

Colors: Change the green (bullish) and red (bearish) shades to suit your chart.

3. Backtest It:

Go to the "Strategy Tester" tab in TradingView to see how it performs on past data. It’ll show trades, profits, losses, and Webull fees included.

4. Watch It Work:

Green boxes mean bullish FVGs; red boxes mean bearish FVGs. If volume spikes and the price breaks out, you’ll see trades happen automatically.

What to Expect

Visuals: You’ll see colored boxes for FVGs and optional lines showing where they start. These help you spot key price zones even if you’re not trading.

Trades: It’s selective—only trades when FVGs align with a breakout and volume confirms it. Expect fewer trades but with higher potential.

Risk: The stop loss keeps losses in check, while the take profit aims for a 2:1 reward-to-risk ratio by default (3% gain vs. 1.5% loss).

Costs: Webull’s fees are small but baked into the results, so you’re seeing a realistic picture of profits.

Tips for Users

Test it on a small timeframe (like 5-minute charts) for day trading or a larger one (like daily) for swing trading.

Play with the volume threshold—if you get too few trades, lower it (e.g., 1.1); if too many, raise it (e.g., 1.5).

Watch how price reacts to the mitigation lines—they’re often support or resistance zones traders target.

This strategy is lightweight, focused, and built for traders who like breakouts with a bit of confirmation. It’s not foolproof (no strategy is!), but it gives you a clear way to trade FVGs with some smart filters.

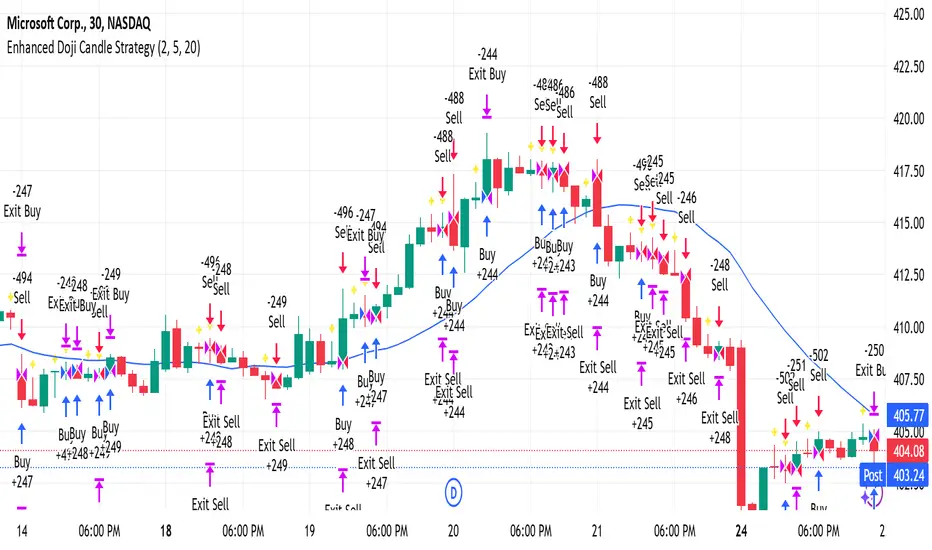

Enhanced Doji Candle StrategyYour trading strategy is a Doji Candlestick Reversal Strategy designed to identify potential market reversals using Doji candlestick patterns. These candles indicate indecision in the market, and when detected, your strategy uses a Simple Moving Average (SMA) with a short period of 20 to confirm the overall market trend. If the price is above the SMA, the trend is considered bullish; if it's below, the trend is bearish.

Once a Doji is detected, the strategy waits for one or two consecutive confirmation candles that align with the market trend. For a bullish confirmation, the candles must close higher than their opening price without significant bottom wicks. Conversely, for a bearish confirmation, the candles must close lower without noticeable top wicks. When these conditions are met, a trade is entered at the market price.

The risk management aspect of your strategy is clearly defined. A stop loss is automatically placed at the nearest recent swing high or low, with a tighter distance of 5 pips to allow for more trading opportunities. A take-profit level is set using a 2:1 reward-to-risk ratio, meaning the potential reward is twice the size of the risk on each trade.

Additionally, the strategy incorporates an early exit mechanism. If a reversal Doji forms in the opposite direction of your trade, the position is closed immediately to minimize losses. This strategy has been optimized to increase trade frequency by loosening the strictness of Doji detection and confirmation conditions while still maintaining sound risk management principles.

The strategy is coded in Pine Script for use on TradingView and uses built-in indicators like the SMA for trend detection. You also have flexible parameters to adjust risk levels, take-profit targets, and stop-loss placements, allowing you to tailor the strategy to different market conditions.

SuperTrend AI Oscillator StrategySuperTrend AI Oscillator Strategy

Overview

This strategy is a trend-following approach that combines the SuperTrend indicator with oscillator-based filtering.

By identifying market trends while utilizing oscillator-based momentum analysis, it aims to improve entry precision.

Additionally, it incorporates a trailing stop to strengthen risk management while maximizing profits.

This strategy can be applied to various markets, including Forex, Crypto, and Stocks, as well as different timeframes. However, its effectiveness varies depending on market conditions, so thorough testing is required.

Features

1️⃣ Trend Identification Using SuperTrend

The SuperTrend indicator (a volatility-adjusted trend indicator based on ATR) is used to determine trend direction.

A long entry is considered when SuperTrend turns bullish.

A short entry is considered when SuperTrend turns bearish.

The goal is to capture clear trend reversals and avoid unnecessary trades in ranging markets.

2️⃣ Entry Filtering with an Oscillator

The Super Oscillator is used to filter entry signals.

If the oscillator exceeds 50, it strengthens long entries (indicating strong bullish momentum).

If the oscillator drops below 50, it strengthens short entries (indicating strong bearish momentum).

This filter helps reduce trades in uncertain market conditions and improves entry accuracy.

3️⃣ Risk Management with a Trailing Stop

Instead of a fixed stop loss, a SuperTrend-based trailing stop is implemented.

The stop level adjusts automatically based on market volatility.

This allows profits to run while managing downside risk effectively.

4️⃣ Adjustable Risk-Reward Ratio

The default risk-reward ratio is set at 1:2.

Example: A 1% stop loss corresponds to a 2% take profit target.

The ratio can be customized according to the trader’s risk tolerance.

5️⃣ Clear Trade Signals & Visual Support

Green "BUY" labels indicate long entry signals.

Red "SELL" labels indicate short entry signals.

The Super Oscillator is plotted in a separate subwindow to visually assess trend strength.

A real-time trailing stop is displayed to support exit strategies.

These visual aids make it easier to identify entry and exit points.

Trading Parameters & Considerations

Initial Account Balance: Default is $7,000 (adjustable).

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 1,032

Visual Aids for Clarity

This strategy includes clear visual trade signals to enhance decision-making:

Green "BUY" labels for long entries

Red "SELL" labels for short entries

Super Oscillator plotted in a subwindow with a 50 midline

Dynamic trailing stop displayed for real-time trend tracking

These visual aids allow traders to quickly identify trade setups and manage positions with greater confidence.

Summary

The SuperTrend AI Oscillator Strategy is developed based on indicators from Black Cat and LuxAlgo.

By integrating high-precision trend analysis with AI-based oscillator filtering, it provides a strong risk-managed trading approach.

Important Notes

This strategy does not guarantee profits—performance varies based on market conditions.

Past performance does not guarantee future results. Markets are constantly changing.

Always test extensively with backtesting and demo trading before using it in live markets.

Risk management, position sizing, and market conditions should always be considered when trading.

Conclusion

This strategy combines trend analysis with momentum filtering, enhancing risk management in trading.

By following market trends carefully, making precise entries, and using trailing stops, it seeks to reduce risk while maximizing potential profits.

Before using this strategy, be sure to test it thoroughly via backtesting and demo trading, and adjust the settings to match your trading style.

AO/AC Trading Zones Strategy [Skyrexio] Overview

AO/AC Trading Zones Strategy leverages the combination of Awesome Oscillator (AO), Acceleration/Deceleration Indicator (AC), Williams Fractals, Williams Alligator and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Combination of AO and AC is used for creating so-called trading zones to create the signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over. In some special cases strategy uses AO and AC combination to trail profit (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Both AC and AO shall print two consecutive increasing values. At the price candle close which corresponds to this condition algorithm opens the first long trade with 10% of capital.

4. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

5. If AO and AC both continue printing the rising values strategy opens the long trade on each candle close with 10% of capital while number of opened trades reaches 5.

6. If AO and AC both has printed 5 rising values in a row algorithm close all trades if candle's low below the low of the 5-th candle with rising AO and AC values in a row.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting:

EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation).

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. We'll begin with the simplest: the EMA.

The Exponential Moving Average (EMA) is a type of moving average that assigns greater weight to recent price data, making it more responsive to current market changes compared to the Simple Moving Average (SMA). This tool is widely used in technical analysis to identify trends and generate buy or sell signals. The EMA is calculated as follows:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy, the EMA acts as a long-term trend filter. For instance, long trades are considered only when the price closes above the EMA (default: 100-period). This increases the likelihood of entering trades aligned with the prevailing trend.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

In this strategy if the most recent up fractal breakout occurs above the Alligator's teeth and follows the last down fractal breakout below the teeth, the algorithm identifies an uptrend. Long trades can be opened during this phase if a signal aligns. If the price breaks a down fractal below the teeth line during an uptrend, the strategy assumes the uptrend has ended and closes all open long trades.

By combining the EMA as a long-term trend filter with the Alligator and fractals as short-term filters, this approach increases the likelihood of opening profitable trades while staying aligned with market dynamics.

Now let's talk about the trading zones concept and its signals. To understand this we need to briefly introduce what is AO and AC. The Awesome Oscillator (AO), developed by Bill Williams, is a momentum indicator designed to measure market momentum by contrasting recent price movements with a longer-term historical perspective. It helps traders detect potential trend reversals and assess the strength of ongoing trends.

The formula for AO is as follows:

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

The Acceleration/Deceleration (AC) Indicator, introduced by Bill Williams, measures the rate of change in market momentum. It highlights shifts in the driving force of price movements and helps traders spot early signs of trend changes. The AC Indicator is particularly useful for identifying whether the current momentum is accelerating or decelerating, which can indicate potential reversals or continuations. For AC calculation we shall use the AO calculated above is the following formula:

AC = AO − SMA5(AO) , where SMA5(AO)is the 5-period Simple Moving Average of the Awesome Oscillator

When the AC is above the zero line and rising, it suggests accelerating upward momentum.

When the AC is below the zero line and falling, it indicates accelerating downward momentum.

When the AC is below zero line and rising it suggests the decelerating the downtrend momentum. When AC is above the zero line and falling, it suggests the decelerating the uptrend momentum.

Now let's discuss the trading zones concept and how it can create the signal. Zones are created by the combination of AO and AC. We can divide three zone types:

Greed zone: when the AO and AC both are rising

Red zone: when the AO and AC both are decreasing

Gray zone: when one of AO or AC is rising, the other is falling

Gray zone is considered as uncertainty. AC and AO are moving in the opposite direction. Strategy skip such price action to decrease the chance to stuck in the losing trade during potential sideways. Red zone is also not interesting for the algorithm because both indicators consider the trend as bearish, but strategy opens only long trades. It is waiting for the green zone to increase the chance to open trade in the direction of the potential uptrend. When we have 2 candles in a row in the green zone script executes a long trade with 10% of capital.

Two green zone candles in a row is considered by algorithm as a bullish trend, but now so strong, that's the reason why trade is going to be closed when the combination of Alligator and Fractals will consider the the trend change from bullish to bearish. If id did not happens, algorithm starts to count the green zone candles in a row. When we have 5 in a row script change the trade closing condition. Such situation is considered is a high probability strong bull market and all trades will be closed if candle's low will be lower than fifth green zone candle's low. This is used to increase probability to secure the profit. If long trades are initiated, the strategy continues utilizing subsequent signals until the total number of trades reaches a maximum of 5. Each trade uses 10% of capital.

Why we use trading zones signals? If currently strategy algorithm considers the high probability of the short-term uptrend with the Alligator and Fractals combination pointed out above and the long-term trend is also suggested by the EMA filter as bullish. Rising AC and AO values in the direction of the most likely main trend signaling that we have the high probability of the fastest bullish phase on the market. The main idea is to take part in such rapid moves and add trades if this move continues its acceleration according to indicators.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.12.31. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 10%

Maximum Single Position Loss: -9.49%

Maximum Single Profit: +24.33%

Net Profit: +4374.70 USDT (+43.75%)

Total Trades: 278 (39.57% win rate)

Profit Factor: 2.203

Maximum Accumulated Loss: 668.16 USDT (-5.43%)

Average Profit per Trade: 15.74 USDT (+1.37%)

Average Trade Duration: 60 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

ATR SuperTrend - IonJauregui-ActivTradesEste script en Pine Script utiliza el indicador SuperTrend basado en el ATR para identificar tendencias y generar señales de compra y venta.

¿Cómo funciona?

Detecta la volatilidad con el ATR para calcular niveles dinámicos de soporte y resistencia.

Dibuja la tendencia:

Línea verde: Tendencia alcista.

Línea roja: Tendencia bajista.

Genera señales de trading:

Compra cuando la tendencia pasa de bajista a alcista.

Venta cuando cambia de alcista a bajista.

Opera de forma automática:

Abre posiciones según las señales.

Establece stop loss y take profit para gestionar el riesgo.

Este indicador ayuda a seguir la tendencia y automatizar operaciones, filtrando el ruido del mercado.

**********************************************************

This Pine Script uses the SuperTrend indicator based on ATR to identify trends and generate buy and sell signals.

How it works:

Detects volatility with ATR to calculate dynamic support and resistance levels.

Plots the trend:

Green line: Bullish trend.

Red line: Bearish trend.

Generates trading signals:

Buy when the trend switches from bearish to bullish.

Sell when it switches from bullish to bearish.

Trades automatically:

Opens positions based on the signals.

Sets stop loss and take profit to manage risk.

This indicator helps follow the trend and automate trades, filtering out market noise.

Liquidity Trading Algorithm (LTA)

The Liquidity Trading Algorithm is an algorithm designed to provide trade signals based on

liquidity conditions in the market. The underlying algorithm is based on the Liquidity

Dependent Price Movement (LDPM) metric and the Liquidity Dependent Price Stability (LDPS)

algorithm.

Together, LDPM and LDPS demonstrate statistically significant forecasting capabilities for price-

action on equities, cryptocurrencies, and futures. LTA takes these liquidity measurements and

translates them into actionable insights by way of entering or exiting a position based

on the future outlooks, as measured by the current liquidity status.

The benefit of LTA is that it can incorporate these powerful liquidity measurements into

actionable insights with several features designed to help you tailor LTA's behavior and

measurements to your desired vantage point. These customizable features come by the way of determining LTA's assessment style, and additional monitoring systems for avoiding bear and bull traps, along with various other quality of life features, discussed in more detail below.

First, a few quick facts:

- LTA is compatible on a wide array of instruments, including Equities, Futures, Cryptocurrencies, and Forex.

- LTA is compatible on most intervals in so long as the data can be calculated appropriately,

(be sure to do a backtest on timescales less than 1-minue to ensure the data can be computed).

- LTA only measures liquidity at the end of the interval of the chart chosen, and does not respond to conditions during the candle interval, unless specified (such as with `Stops`).

- LTA is interval-dependent, this means it will measure and behave differently on different

intervals as the underlying algorithms are dependent on the interval chosen.

- LTA can utilize fractional share sizing for cryptocurrencies.

- LTA can be restricted to either bullish or bearish indications.

- Additional Monitoring Systems are available for additional risk mitigation.

In short, LTA is a widely applicable, unique algorithm designed to translate liquidity measurements into liquidity insights.

Before getting more into the details, here is a quick list of the main features and settings

available for customization:

- Backtesting Start Date: Manual selection of the start date for the algorithm during backtesting.

- Assessment Style: adjust how LDPM and LDPS measure and respond to changes in liquidity.

- Impose Wait: force LTA to wait before entering or exiting a position to ensure conditions have remained conducive.

- Trade Direction Allowance: Restrict LTA to only long or only short, if desired.

- Position Sizing Method: determine how LTA calculates position sizing.

- Fractional Share Sizing: allow LTA to calculate fractional share sizes for cryptocurrencies

- Max Size Limit: Impose a maximum size on LTA's positions.

- Initial Capital: Indicate how much capital LTA should stat with.

- Portfolio Allotment: Indicate to LTA how much (in percentages) of the available balance should be considered when calculating position size.

- Enact Additional Monitoring Systems: Indicate if LTA should impose additional safety criteria when monitoring liquidity.

- Configure Take Profit, Stop-Loss, Trailing Stop Loss

- Display Information tables on the current position, overall strategy performance, along

with a text output showing LTA's processes.

- Real-time text output and updates on LTA's inner workings.

Let's get into some more of the details.

LTA's Assessment Style

LTA's assessment style determines how LTA collects and responds to changing data. In traditional terms, this is akin to (but not quite exactly the same as) the sensitivity versus specificity spectrum, whereby on one end (the sensitive end), an algorithm responds to changes in data in a reactive manner (which tends to lower its specificity, or how often it is correct in its indications), and on the other end, the opposite one, the algorithm foresakes quick changes for longevity of outlook.

While this is in part true, it is not a full view of the underlying mechanisms that changing the assessment style augments. A better analogy would be that the sensitive end of the spectrum (`Aggressive`) is in a state such that the algorithm wants to changing its outlooks, and as such, with changes in data, the algorithm has to be convinced as to why that is not a good idea to change outlooks, whereas the the more specific states (`Conservative`, `Diamond`) must be convinced that their view is no longer valid and that it needs to be changed.

This means the `Aggressive` and the `Diamond` settings fundamentally differ not just in their

data collection, but also in the data processing such that the `Aggressive` decision tree has to

be convinced that the data is the same (as its defualt is that it has changed),

and the `Diamond` decision tree has to be convinced that the data is not the same, and as such, the outlook need changed.

From there, the algorithm cooks through the data and determines to what the outlook should be changed to, given the current state of liquidity.

`Balanced` lies in the middle of this balance, attempting to balance being open to new ideas while not removing the wisdom of the past, as it were.

On a scale of most `sensitive` to most `specific`, it is as follows: `Aggressive`, `Balanced`,

`Conservative`, `Diamond`.

Functionally, these different modes can help in different liquidity environments, as certain

environments are more conducive to an eager approach (such as found near `Aggressive`) or are more conducive to a more conservative approach, where sudden changes in liquidity are known to be short-lived and unremarkable (such as many previously identified bull or bear traps).

For instance, on low interval views, it can often-times be beneficial to keep the algorithm towards the `Sensitive` end, since on the lower-timeframes, the crosswinds can change quite dramatically; whereas on the longer intervals, it may be useful to maintain a more `Specific` algorithm (such as found near `Diamond` mode) setting since longer intervals typically lend themselves to longer time-horizons, which themselves typically lend themselves to "weathering the storm", as it were.

LTA's Assessment Style is also supported by the Additional Monitoring Systems which works

to add sensitivity without sacrificing specificity by enacting a separate monitoring system, as described below.

Additional Monitoring Systems

The Additional Monitoring System (AMS) attempts to add more context to any changes in liquidity conditions as measured, such that LTA as a whole will have an expanded view into any rapidly changing liquidity conditions before these changes manifest in the traditional data streams. The ideal is that this allows for early exits or early entrances to positions "a head of time".

The traditional use of this system is to indicate when liquidity is suggestive of the end of a particular run (be it a bear run or a bull run), so an early exit can be initiated (and thus,

downside averted) even before the data officially showcase such changes. In such cases (when AMS becomes activated), the algorithm will signal to exit any open positions, and will restrict the opening of any new positions.

When a position is exited because of AMS, it is denoted as an `Early Exit` and if a position is prevented from being entered, the text output will display `AM prevented entry...` to indicate that conditions are not meeting AMS' additional standards.

The algorithm will wait to make any actions while `AMS` is `active` and will only enter into a new position once `AMS` has been `deactivated` and overall liquidity conditions are appropriate.

Functionally, the benefits of AMS translate to:

- Toggeling AMS on will typically see a net reduction in overall profitability, but

- AMS will typically (almost always) reduce max drawdown,

an increases in max runup, and increase return-over-maxdrawdown, and

- AMS can provide benefit for equities that experience a lot of "traps" by navigating early

entrance and early exits.

So in short, AMS is way of adding an additional level of liquidity monitoring that attempts to

exit positions if conditions look to be deteriorating, and to enter conditions if they look to be

improving. The cost of this additional monitoring, however, is a greater number of trades indicated, and a lower overall profitability.

Impose Wait

Note: `Impose Wait` will not force Take Profit, Stop Loss, or Trailing Stop Loss to

wait.

LTA can be indicated to `wait` before entering or exiting a position if desired. This means that if conditions change, whereas without a `wait` imposed, the algorithm would immediately indicate this change via a signal to alter the strategy's position, with a `wait` imposed, the algorithm will `wait` the indicated number of bars, and then re-check conditions before proceeding.

If, while waiting, conditions change to a state that is no longer compatible with the "order-in-

waiting", then the order-in-waiting is removed, and the counts reset (i.e.: conditions must remain favorable to the intended positional change throughout the wait period).

Since LTA works at the end-of-intervals, there is an inherently "built-in" wait of 1 bar when

switching directly from long to short (i.e.: if a full switch is indicated, then it is indicated as

conditions change -> exit new position -> wait until -> check conditions ->

enter new position as indicated). Thus, to impose a wait of `1 bar` would be to effectively have a total of two candles' ends prior to the entrance of the new position).

There are two main styles of `Impose Wait` that you can utilize:

- `Wait` : this mode will cause LTA to `wait` when both entering and exiting a position (in so long as it is not an exit signaled via a Take Profit, Stop Loss or Trailing Stop Loss).

- `Exit-Wait` : This mode will >not< cause LTA to `wait` if conditions require the closing of a position, but will force LTA to wait before entering into a position.

Position:

In addition to the availability to restrict LTA to either a long-only or short-only strategy, LTA

also comprises additional flexibility when deciding on how it should navigate the markets with

regards to sizing. Notably, this flexibility benefits several aspects of LTA's existence, namely the ability to determine the `Sizing Method`, or if `Fractional Share Sizing` should be employed, and more, as discussed below.

Position Sizing Method

There are two main ways LTA can determine the size of a position. Either via the `Fixed-Share` choice, or the `Fixed-Percentage` choice.

- `Fixed-Share` will use the amount indicated in the `Max Sizing Limit` field as the position size, always.

Note: With `Fixed-Share` sizing, LTA will >not< check if the balance is sufficient

prior to signaling an entrance.

- `Fixed-Percentage` will use the percentage amount indicated in the `Portfolio Allotment` field as the percentage of available funds to use when calculating the position size. Additionally, with the `Fixed-Percentage` choice, you can set the `Max Sizing Limit` if desired, which will ensure that no position will be entered greater than the amount indicated in the field.

Fractional Share Sizing

If the underlying instrument supports it (typically only cryptocurrencies), share sizing can be

fractionalized. If this is done, the resulting positin size is rounded to `4 digits`. This means any

position with a size less than `0.00005` will be rounded to `0.0000`

Note: Ensure that the underlying instrument supports fractional share sizing prior

to initiating.

Max Sizing Limit

As discussed above, the `Max Sizing Limit` will determine:

- The position size for every position, if `Sizing Method : Fixed-Share` is utilized, or

- The maximum allowed size, regardless of available capital, if `Sizing Method : Fixed-Percentage` is utilized.

Note: There is an internal maximum of 100,000 units.

Initial Capital

Note: There are 2 `Initial Capital` settings; one in LTA's settings and one in the

`Properties` tab. Ensure these two are the same when doing backtesting.

The initial capital field will be used to determine the starting balanace of the strategy, and

is used to calculate the internal data reporting (the data tables).

Portfolio Allotment

You can specify how much of the total available balance should be used when calculating the share size. The default is 100%.

Stops

Note: Stops over-ride `AMS` and `Impose Wait`, and are not restricted to only the

end-of-candle and will occur instantaneously upon their activation. Neither `AMS` nor `Impose Wait` can over-ride a signal from a `Take-Profit`, `Stop-Loss`, or a `Trailing-Stop Loss`.

LTA enhouses three stops that can be configured, a `Take-Profit`, a `Stop-Loss` and a `Trailing-Stop Loss`. The configurations can be set in the settings in percent terms. These exit signals will always over-ride AMS or any other restrictions on position exit.