3D Surface Modeling [PhenLabs]📊 3D Surface Modeling

Version: PineScript™ v6

📌 Description

The 3D Surface Modeling indicator revolutionizes technical analysis by generating three-dimensional visualizations of multiple technical indicators across various timeframes. This advanced analytical tool processes and renders complex indicator data through a sophisticated matrix-based calculation system, creating an intuitive 3D surface representation of market dynamics.

The indicator employs array-based computations to simultaneously analyze multiple instances of selected technical indicators, mapping their behavior patterns across different temporal dimensions. This unique approach enables traders to identify complex market patterns and relationships that may be invisible in traditional 2D charts.

🚀 Points of Innovation

Matrix-Based Computation Engine: Processes up to 500 concurrent indicator calculations in real-time

Dynamic 3D Rendering System: Creates depth perception through sophisticated line arrays and color gradients

Multi-Indicator Integration: Seamlessly combines VWAP, Hurst, RSI, Stochastic, CCI, MFI, and Fractal Dimension analyses

Adaptive Scaling Algorithm: Automatically adjusts visualization parameters based on indicator type and market conditions

🔧 Core Components

Indicator Processing Module: Handles real-time calculation of multiple technical indicators using array-based mathematics

3D Visualization Engine: Converts indicator data into three-dimensional surfaces using line arrays and color mapping

Dynamic Scaling System: Implements custom normalization algorithms for different indicator types

Color Gradient Generator: Creates depth perception through programmatic color transitions

🔥 Key Features

Multi-Indicator Support: Comprehensive analysis across seven different technical indicators

Customizable Visualization: User-defined color schemes and line width parameters

Real-time Processing: Continuous calculation and rendering of 3D surfaces

Cross-Timeframe Analysis: Simultaneous visualization of indicator behavior across multiple periods

🎨 Visualization

Surface Plot: Three-dimensional representation using up to 500 lines with dynamic color gradients

Depth Indicators: Color intensity variations showing indicator value magnitude

Pattern Recognition: Visual identification of market structures across multiple timeframes

📖 Usage Guidelines

Indicator Selection

Type: VWAP, Hurst, RSI, Stochastic, CCI, MFI, Fractal Dimension

Default: VWAP

Starting Length: Minimum 5 periods

Default: 10

Step Size: Interval between calculations

Range: 1-10

Visualization Parameters

Color Scheme: Green, Red, Blue options

Line Width: 1-5 pixels

Surface Resolution: Up to 500 lines

✅ Best Use Cases

Multi-timeframe market analysis

Pattern recognition across different technical indicators

Trend strength assessment through 3D visualization

Market behavior study across multiple periods

⚠️ Limitations

High computational resource requirements

Maximum 500 line restriction

Requires substantial historical data

Complex visualization learning curve

🔬 How It Works

1. Data Processing:

Calculates selected indicator values across multiple timeframes

Stores results in multi-dimensional arrays

Applies custom scaling algorithms

2. Visualization Generation:

Creates line arrays for 3D surface representation

Applies color gradients based on value magnitude

Renders real-time updates to surface plot

3. Display Integration:

Synchronizes with chart timeframe

Updates surface plot dynamically

Maintains visual consistency across updates

🌟 Credits:

Inspired by LonesomeTheBlue (modified for multiple indicator types with scaling fixes and additional unique mappings)

💡 Note:

Optimal performance requires sufficient computing resources and historical data. Users should start with default settings and gradually adjust parameters based on their analysis requirements and system capabilities.

Поиск скриптов по запросу "curve"

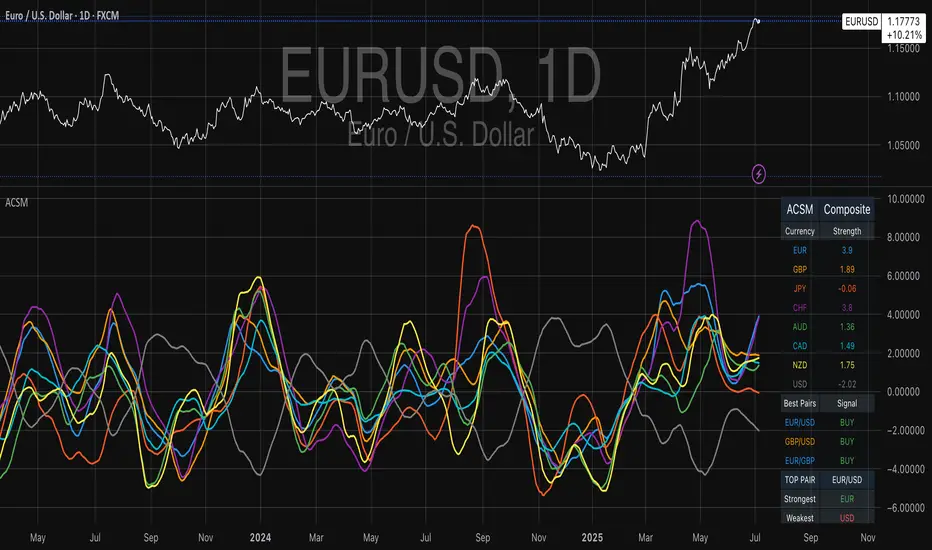

Advanced Currency Strength Meter# Advanced Currency Strength Meter (ACSM)

The Advanced Currency Strength Meter (ACSM) is a scientifically-based indicator that measures relative currency strength using established academic methodologies from international finance and behavioral economics. This indicator provides traders with a comprehensive view of currency market dynamics through multiple analytical frameworks.

### Theoretical Foundation

#### 1. Purchasing Power Parity (PPP) Theory

Based on Cassel's (1918) seminal work and refined by Froot & Rogoff (1995), PPP suggests that exchange rates should reflect relative price levels between countries. The ACSM momentum component captures deviations from long-term equilibrium relationships, providing insights into currency misalignments.

#### 2. Uncovered Interest Rate Parity (UIP) and Carry Trade Theory

Building on Fama (1984) and Lustig et al. (2007), the indicator incorporates volatility-adjusted momentum to capture carry trade flows and interest rate differentials that drive currency strength. This approach helps identify currencies benefiting from interest rate differentials.

#### 3. Behavioral Finance and Currency Momentum

Following Burnside et al. (2011) and Menkhoff et al. (2012), the model recognizes that currency markets exhibit persistent momentum effects due to behavioral biases and institutional flows. The indicator captures these momentum patterns for trading opportunities.

#### 4. Portfolio Balance Theory

Based on Branson & Henderson (1985), the relative strength matrix captures how portfolio rebalancing affects currency cross-rates and creates trading opportunities between different currency pairs.

### Technical Implementation

#### Core Methodologies:

- **Z-Score Normalization**: Following Sharpe (1994), provides statistical significance testing without arbitrary scaling

- **Momentum Analysis**: Uses return-based metrics (Jegadeesh & Titman, 1993) for trend identification

- **Volatility Adjustment**: Implements Average True Range methodology (Wilder, 1978) for risk-adjusted strength

- **Composite Scoring**: Equal-weight methodology to avoid overfitting and maintain robustness

- **Correlation Analysis**: Risk management framework based on Markowitz (1952) portfolio theory

#### Key Features:

- **Multi-Source Data Integration**: Supports OANDA, Futures, and CFD data sources

- **Scientific Methodology**: No arbitrary scaling or curve-fitting; all calculations based on established statistical methods

- **Comprehensive Dashboard**: Clean, professional table showing currency strengths and best trading pairs

- **Alert System**: Automated notifications for strong/weak currency conditions and extreme values

- **Best Pair Identification**: Algorithmic detection of highest-potential trading opportunities

### Practical Applications

#### For Swing Traders:

- Identify currencies in strong uptrends or downtrends

- Select optimal currency pairs based on relative strength divergence

- Time entries based on momentum convergence/divergence

#### For Day Traders:

- Use with real-time futures data for intraday opportunities

- Monitor currency correlations for risk management

- Detect early reversal signals through extreme value alerts

#### For Portfolio Managers:

- Multi-currency exposure analysis

- Risk management through correlation monitoring

- Strategic currency allocation decisions

### Visual Design

The indicator features a clean, professional dashboard that displays:

- **Currency Strength Values**: Each major currency (EUR, GBP, JPY, CHF, AUD, CAD, NZD, USD) with color-coded strength values

- **Best Trading Pairs**: Filtered list of highest-potential currency pairs with BUY/SELL signals

- **Market Analysis**: Real-time identification of strongest and weakest currencies

- **Potential Score**: Quantitative measure of trading opportunity strength

### Data Sources and Latency

The indicator supports multiple data sources to accommodate different trading needs:

- **OANDA (Delayed)**: Free data with 15-20 minute delay, suitable for swing trading

- **Futures (Real-time)**: CME currency futures for real-time analysis

- **CFDs**: Alternative real-time data source option

### Mathematical Framework

#### Strength Calculation:

Momentum = (Price - Price ) / Price * 100

Z-Score = (Price - Mean) / Standard Deviation

Volatility-Adjusted = Momentum / ATR-based Volatility

Composite = 0.5 * Momentum + 0.3 * Z-Score + 0.2 * Volatility-Adjusted

#### USD Strength Derivation:

USD strength is calculated as the weighted average of all USD-based pairs, providing a true baseline for relative strength comparison.

### Performance Considerations

The indicator is optimized for:

- **Computational Efficiency**: Uses Pine Script v6 best practices

- **Memory Management**: Appropriate lookback periods and array handling

- **Visual Clarity**: Clean table design optimized for both light and dark themes

- **Alert Reliability**: Robust signal generation with statistical significance testing

### Limitations and Risk Disclosure

- Model performance may vary during extreme market stress (Black Swan events)

- Requires stable data feeds for accurate calculations

- Not optimized for high-frequency scalping strategies

- Central bank interventions may temporarily distort signals

- Performance assumes normal market conditions with behavioral adjustments

### Academic References

- Branson, W. H., & Henderson, D. W. (1985). "The Specification and Influence of Asset Markets"

- Burnside, C., Eichenbaum, M., & Rebelo, S. (2011). "Carry Trade and Momentum in Currency Markets"

- Cassel, G. (1918). "Abnormal Deviations in International Exchanges"

- Fama, E. F. (1984). "Forward and Spot Exchange Rates"

- Froot, K. A., & Rogoff, K. (1995). "Perspectives on PPP and Long-Run Real Exchange Rates"

- Jegadeesh, N., & Titman, S. (1993). "Returns to Buying Winners and Selling Losers"

- Lustig, H., Roussanov, N., & Verdelhan, A. (2007). "Common Risk Factors in Currency Markets"

- Markowitz, H. (1952). "Portfolio Selection"

- Menkhoff, L., Sarno, L., Schmeling, M., & Schrimpf, A. (2012). "Carry Trades and Global FX Volatility"

- Sharpe, W. F. (1994). "The Sharpe Ratio"

- Wilder, J. W. (1978). "New Concepts in Technical Trading Systems"

### Usage Instructions

1. **Setup**: Add the indicator to your chart and select your preferred data source

2. **Currency Selection**: Choose which currencies to analyze (default: all major currencies)

3. **Methodology**: Select calculation method (Composite recommended for most users)

4. **Monitoring**: Watch the dashboard for strength changes and best pair opportunities

5. **Alerts**: Set up notifications for strong/weak currency conditions

Normalized Open InterestNormalized Open Interest (nOI) — Indicator Overview

What it does

Normalized Open Interest (nOI) transforms raw futures open-interest data into a 0-to-100 oscillator, so you can see at a glance whether participation is unusually high or low—similar in spirit to an RSI but applied to open interest. The script positions today’s OI inside a rolling high–low range and paints it with contextual colours.

Core logic

Data source – Loads the built-in “_OI” symbol that TradingView provides for the current market.

Rolling range – Looks back a user-defined number of bars (default 500) to find the highest and lowest OI in that window.

Normalization – Calculates

nOI = (OI – lowest) / (highest – lowest) × 100

so 0 equals the minimum of the window and 100 equals the maximum.

Visual cues – Plots the oscillator plus fixed horizontal levels at 70 % and 30 % (or your own numbers). The line turns teal above the upper level, red below the lower, and neutral grey in between.

User inputs

Window Length (bars) – How many candles the indicator scans for the high–low range; larger numbers smooth the curve, smaller numbers make it more reactive.

Upper Threshold (%) – Default 70. Anything above this marks potentially crowded or overheated interest.

Lower Threshold (%) – Default 30. Anything below this marks low or capitulating interest.

Practical uses

Spot extremes – Values above the upper line can warn that the long side is crowded; values below the lower line suggest disinterest or short-side crowding.

Confirm breakouts – A price breakout backed by a sharp rise in nOI signals genuine engagement.

Look for divergences – If price makes a new high but nOI does not, participation might be fading.

Combine with volume or RSI – Layer nOI with other studies to filter false signals.

Tips

On intraday charts for non-crypto symbols the script automatically fetches daily OI data to avoid gaps.

Adjust the thresholds to 80/20 or 60/40 to fit your market and risk preferences.

Alerts, shading, or additional signal logic can be added easily because the oscillator is already normalised.

Yield Curve Regime Shading with LegendTakes two symbols (e.g. two futures contracts, two FX pairs, etc.) as inputs.

Calculates the “regime” as the sign of the change in their difference over an n‑period lookback.

Lets you choose whether you want to color the bars themselves or shade the background.

How it works

Inputs

symbolA, symbolB: the two tickers you’re comparing.

n: lookback in bars to measure the change in the spread.

mode: pick between “Shading” or “Candle Color”.

Data fetching

We use request.security() to pull each series at the chart’s timeframe.

Regime calculation

spread = priceA – priceB

spreadPrev = ta.valuewhen(not na(spread), spread , 0) (i.e. the spread n bars ago)

If spread > spreadPrev → bullish regime

If spread < spreadPrev → bearish regime

Plotting

Shading: apply bgcolor() in green/red.

Candle Color: use barcolor() to override the bar color.

Tensor Market Analysis Engine (TMAE)# Tensor Market Analysis Engine (TMAE)

## Advanced Multi-Dimensional Mathematical Analysis System

*Where Quantum Mathematics Meets Market Structure*

---

## 🎓 THEORETICAL FOUNDATION

The Tensor Market Analysis Engine represents a revolutionary synthesis of three cutting-edge mathematical frameworks that have never before been combined for comprehensive market analysis. This indicator transcends traditional technical analysis by implementing advanced mathematical concepts from quantum mechanics, information theory, and fractal geometry.

### 🌊 Multi-Dimensional Volatility with Jump Detection

**Hawkes Process Implementation:**

The TMAE employs a sophisticated Hawkes process approximation for detecting self-exciting market jumps. Unlike traditional volatility measures that treat price movements as independent events, the Hawkes process recognizes that market shocks cluster and exhibit memory effects.

**Mathematical Foundation:**

```

Intensity λ(t) = μ + Σ α(t - Tᵢ)

```

Where market jumps at times Tᵢ increase the probability of future jumps through the decay function α, controlled by the Hawkes Decay parameter (0.5-0.99).

**Mahalanobis Distance Calculation:**

The engine calculates volatility jumps using multi-dimensional Mahalanobis distance across up to 5 volatility dimensions:

- **Dimension 1:** Price volatility (standard deviation of returns)

- **Dimension 2:** Volume volatility (normalized volume fluctuations)

- **Dimension 3:** Range volatility (high-low spread variations)

- **Dimension 4:** Correlation volatility (price-volume relationship changes)

- **Dimension 5:** Microstructure volatility (intrabar positioning analysis)

This creates a volatility state vector that captures market behavior impossible to detect with traditional single-dimensional approaches.

### 📐 Hurst Exponent Regime Detection

**Fractal Market Hypothesis Integration:**

The TMAE implements advanced Rescaled Range (R/S) analysis to calculate the Hurst exponent in real-time, providing dynamic regime classification:

- **H > 0.6:** Trending (persistent) markets - momentum strategies optimal

- **H < 0.4:** Mean-reverting (anti-persistent) markets - contrarian strategies optimal

- **H ≈ 0.5:** Random walk markets - breakout strategies preferred

**Adaptive R/S Analysis:**

Unlike static implementations, the TMAE uses adaptive windowing that adjusts to market conditions:

```

H = log(R/S) / log(n)

```

Where R is the range of cumulative deviations and S is the standard deviation over period n.

**Dynamic Regime Classification:**

The system employs hysteresis to prevent regime flipping, requiring sustained Hurst values before regime changes are confirmed. This prevents false signals during transitional periods.

### 🔄 Transfer Entropy Analysis

**Information Flow Quantification:**

Transfer entropy measures the directional flow of information between price and volume, revealing lead-lag relationships that indicate future price movements:

```

TE(X→Y) = Σ p(yₜ₊₁, yₜ, xₜ) log

```

**Causality Detection:**

- **Volume → Price:** Indicates accumulation/distribution phases

- **Price → Volume:** Suggests retail participation or momentum chasing

- **Balanced Flow:** Market equilibrium or transition periods

The system analyzes multiple lag periods (2-20 bars) to capture both immediate and structural information flows.

---

## 🔧 COMPREHENSIVE INPUT SYSTEM

### Core Parameters Group

**Primary Analysis Window (10-100, Default: 50)**

The fundamental lookback period affecting all calculations. Optimization by timeframe:

- **1-5 minute charts:** 20-30 (rapid adaptation to micro-movements)

- **15 minute-1 hour:** 30-50 (balanced responsiveness and stability)

- **4 hour-daily:** 50-100 (smooth signals, reduced noise)

- **Asset-specific:** Cryptocurrency 20-35, Stocks 35-50, Forex 40-60

**Signal Sensitivity (0.1-2.0, Default: 0.7)**

Master control affecting all threshold calculations:

- **Conservative (0.3-0.6):** High-quality signals only, fewer false positives

- **Balanced (0.7-1.0):** Optimal risk-reward ratio for most trading styles

- **Aggressive (1.1-2.0):** Maximum signal frequency, requires careful filtering

**Signal Generation Mode:**

- **Aggressive:** Any component signals (highest frequency)

- **Confluence:** 2+ components agree (balanced approach)

- **Conservative:** All 3 components align (highest quality)

### Volatility Jump Detection Group

**Volatility Dimensions (2-5, Default: 3)**

Determines the mathematical space complexity:

- **2D:** Price + Volume volatility (suitable for clean markets)

- **3D:** + Range volatility (optimal for most conditions)

- **4D:** + Correlation volatility (advanced multi-asset analysis)

- **5D:** + Microstructure volatility (maximum sensitivity)

**Jump Detection Threshold (1.5-4.0σ, Default: 3.0σ)**

Standard deviations required for volatility jump classification:

- **Cryptocurrency:** 2.0-2.5σ (naturally volatile)

- **Stock Indices:** 2.5-3.0σ (moderate volatility)

- **Forex Major Pairs:** 3.0-3.5σ (typically stable)

- **Commodities:** 2.0-3.0σ (varies by commodity)

**Jump Clustering Decay (0.5-0.99, Default: 0.85)**

Hawkes process memory parameter:

- **0.5-0.7:** Fast decay (jumps treated as independent)

- **0.8-0.9:** Moderate clustering (realistic market behavior)

- **0.95-0.99:** Strong clustering (crisis/event-driven markets)

### Hurst Exponent Analysis Group

**Calculation Method Options:**

- **Classic R/S:** Original Rescaled Range (fast, simple)

- **Adaptive R/S:** Dynamic windowing (recommended for trading)

- **DFA:** Detrended Fluctuation Analysis (best for noisy data)

**Trending Threshold (0.55-0.8, Default: 0.60)**

Hurst value defining persistent market behavior:

- **0.55-0.60:** Weak trend persistence

- **0.65-0.70:** Clear trending behavior

- **0.75-0.80:** Strong momentum regimes

**Mean Reversion Threshold (0.2-0.45, Default: 0.40)**

Hurst value defining anti-persistent behavior:

- **0.35-0.45:** Weak mean reversion

- **0.25-0.35:** Clear ranging behavior

- **0.15-0.25:** Strong reversion tendency

### Transfer Entropy Parameters Group

**Information Flow Analysis:**

- **Price-Volume:** Classic flow analysis for accumulation/distribution

- **Price-Volatility:** Risk flow analysis for sentiment shifts

- **Multi-Timeframe:** Cross-timeframe causality detection

**Maximum Lag (2-20, Default: 5)**

Causality detection window:

- **2-5 bars:** Immediate causality (scalping)

- **5-10 bars:** Short-term flow (day trading)

- **10-20 bars:** Structural flow (swing trading)

**Significance Threshold (0.05-0.3, Default: 0.15)**

Minimum entropy for signal generation:

- **0.05-0.10:** Detect subtle information flows

- **0.10-0.20:** Clear causality only

- **0.20-0.30:** Very strong flows only

---

## 🎨 ADVANCED VISUAL SYSTEM

### Tensor Volatility Field Visualization

**Five-Layer Resonance Bands:**

The tensor field creates dynamic support/resistance zones that expand and contract based on mathematical field strength:

- **Core Layer (Purple):** Primary tensor field with highest intensity

- **Layer 2 (Neutral):** Secondary mathematical resonance

- **Layer 3 (Info Blue):** Tertiary harmonic frequencies

- **Layer 4 (Warning Gold):** Outer field boundaries

- **Layer 5 (Success Green):** Maximum field extension

**Field Strength Calculation:**

```

Field Strength = min(3.0, Mahalanobis Distance × Tensor Intensity)

```

The field amplitude adjusts to ATR and mathematical distance, creating dynamic zones that respond to market volatility.

**Radiation Line Network:**

During active tensor states, the system projects directional radiation lines showing field energy distribution:

- **8 Directional Rays:** Complete angular coverage

- **Tapering Segments:** Progressive transparency for natural visual flow

- **Pulse Effects:** Enhanced visualization during volatility jumps

### Dimensional Portal System

**Portal Mathematics:**

Dimensional portals visualize regime transitions using category theory principles:

- **Green Portals (◉):** Trending regime detection (appear below price for support)

- **Red Portals (◎):** Mean-reverting regime (appear above price for resistance)

- **Yellow Portals (○):** Random walk regime (neutral positioning)

**Tensor Trail Effects:**

Each portal generates 8 trailing particles showing mathematical momentum:

- **Large Particles (●):** Strong mathematical signal

- **Medium Particles (◦):** Moderate signal strength

- **Small Particles (·):** Weak signal continuation

- **Micro Particles (˙):** Signal dissipation

### Information Flow Streams

**Particle Stream Visualization:**

Transfer entropy creates flowing particle streams indicating information direction:

- **Upward Streams:** Volume leading price (accumulation phases)

- **Downward Streams:** Price leading volume (distribution phases)

- **Stream Density:** Proportional to information flow strength

**15-Particle Evolution:**

Each stream contains 15 particles with progressive sizing and transparency, creating natural flow visualization that makes information transfer immediately apparent.

### Fractal Matrix Grid System

**Multi-Timeframe Fractal Levels:**

The system calculates and displays fractal highs/lows across five Fibonacci periods:

- **8-Period:** Short-term fractal structure

- **13-Period:** Intermediate-term patterns

- **21-Period:** Primary swing levels

- **34-Period:** Major structural levels

- **55-Period:** Long-term fractal boundaries

**Triple-Layer Visualization:**

Each fractal level uses three-layer rendering:

- **Shadow Layer:** Widest, darkest foundation (width 5)

- **Glow Layer:** Medium white core line (width 3)

- **Tensor Layer:** Dotted mathematical overlay (width 1)

**Intelligent Labeling System:**

Smart spacing prevents label overlap using ATR-based minimum distances. Labels include:

- **Fractal Period:** Time-based identification

- **Topological Class:** Mathematical complexity rating (0, I, II, III)

- **Price Level:** Exact fractal price

- **Mahalanobis Distance:** Current mathematical field strength

- **Hurst Exponent:** Current regime classification

- **Anomaly Indicators:** Visual strength representations (○ ◐ ● ⚡)

### Wick Pressure Analysis

**Rejection Level Mathematics:**

The system analyzes candle wick patterns to project future pressure zones:

- **Upper Wick Analysis:** Identifies selling pressure and resistance zones

- **Lower Wick Analysis:** Identifies buying pressure and support zones

- **Pressure Projection:** Extends lines forward based on mathematical probability

**Multi-Layer Glow Effects:**

Wick pressure lines use progressive transparency (1-8 layers) creating natural glow effects that make pressure zones immediately visible without cluttering the chart.

### Enhanced Regime Background

**Dynamic Intensity Mapping:**

Background colors reflect mathematical regime strength:

- **Deep Transparency (98% alpha):** Subtle regime indication

- **Pulse Intensity:** Based on regime strength calculation

- **Color Coding:** Green (trending), Red (mean-reverting), Neutral (random)

**Smoothing Integration:**

Regime changes incorporate 10-bar smoothing to prevent background flicker while maintaining responsiveness to genuine regime shifts.

### Color Scheme System

**Six Professional Themes:**

- **Dark (Default):** Professional trading environment optimization

- **Light:** High ambient light conditions

- **Classic:** Traditional technical analysis appearance

- **Neon:** High-contrast visibility for active trading

- **Neutral:** Minimal distraction focus

- **Bright:** Maximum visibility for complex setups

Each theme maintains mathematical accuracy while optimizing visual clarity for different trading environments and personal preferences.

---

## 📊 INSTITUTIONAL-GRADE DASHBOARD

### Tensor Field Status Section

**Field Strength Display:**

Real-time Mahalanobis distance calculation with dynamic emoji indicators:

- **⚡ (Lightning):** Extreme field strength (>1.5× threshold)

- **● (Solid Circle):** Strong field activity (>1.0× threshold)

- **○ (Open Circle):** Normal field state

**Signal Quality Rating:**

Democratic algorithm assessment:

- **ELITE:** All 3 components aligned (highest probability)

- **STRONG:** 2 components aligned (good probability)

- **GOOD:** 1 component active (moderate probability)

- **WEAK:** No clear component signals

**Threshold and Anomaly Monitoring:**

- **Threshold Display:** Current mathematical threshold setting

- **Anomaly Level (0-100%):** Combined volatility and volume spike measurement

- **>70%:** High anomaly (red warning)

- **30-70%:** Moderate anomaly (orange caution)

- **<30%:** Normal conditions (green confirmation)

### Tensor State Analysis Section

**Mathematical State Classification:**

- **↑ BULL (Tensor State +1):** Trending regime with bullish bias

- **↓ BEAR (Tensor State -1):** Mean-reverting regime with bearish bias

- **◈ SUPER (Tensor State 0):** Random walk regime (neutral)

**Visual State Gauge:**

Five-circle progression showing tensor field polarity:

- **🟢🟢🟢⚪⚪:** Strong bullish mathematical alignment

- **⚪⚪🟡⚪⚪:** Neutral/transitional state

- **⚪⚪🔴🔴🔴:** Strong bearish mathematical alignment

**Trend Direction and Phase Analysis:**

- **📈 BULL / 📉 BEAR / ➡️ NEUTRAL:** Primary trend classification

- **🌪️ CHAOS:** Extreme information flow (>2.0 flow strength)

- **⚡ ACTIVE:** Strong information flow (1.0-2.0 flow strength)

- **😴 CALM:** Low information flow (<1.0 flow strength)

### Trading Signals Section

**Real-Time Signal Status:**

- **🟢 ACTIVE / ⚪ INACTIVE:** Long signal availability

- **🔴 ACTIVE / ⚪ INACTIVE:** Short signal availability

- **Components (X/3):** Active algorithmic components

- **Mode Display:** Current signal generation mode

**Signal Strength Visualization:**

Color-coded component count:

- **Green:** 3/3 components (maximum confidence)

- **Aqua:** 2/3 components (good confidence)

- **Orange:** 1/3 components (moderate confidence)

- **Gray:** 0/3 components (no signals)

### Performance Metrics Section

**Win Rate Monitoring:**

Estimated win rates based on signal quality with emoji indicators:

- **🔥 (Fire):** ≥60% estimated win rate

- **👍 (Thumbs Up):** 45-59% estimated win rate

- **⚠️ (Warning):** <45% estimated win rate

**Mathematical Metrics:**

- **Hurst Exponent:** Real-time fractal dimension (0.000-1.000)

- **Information Flow:** Volume/price leading indicators

- **📊 VOL:** Volume leading price (accumulation/distribution)

- **💰 PRICE:** Price leading volume (momentum/speculation)

- **➖ NONE:** Balanced information flow

- **Volatility Classification:**

- **🔥 HIGH:** Above 1.5× jump threshold

- **📊 NORM:** Normal volatility range

- **😴 LOW:** Below 0.5× jump threshold

### Market Structure Section (Large Dashboard)

**Regime Classification:**

- **📈 TREND:** Hurst >0.6, momentum strategies optimal

- **🔄 REVERT:** Hurst <0.4, contrarian strategies optimal

- **🎲 RANDOM:** Hurst ≈0.5, breakout strategies preferred

**Mathematical Field Analysis:**

- **Dimensions:** Current volatility space complexity (2D-5D)

- **Hawkes λ (Lambda):** Self-exciting jump intensity (0.00-1.00)

- **Jump Status:** 🚨 JUMP (active) / ✅ NORM (normal)

### Settings Summary Section (Large Dashboard)

**Active Configuration Display:**

- **Sensitivity:** Current master sensitivity setting

- **Lookback:** Primary analysis window

- **Theme:** Active color scheme

- **Method:** Hurst calculation method (Classic R/S, Adaptive R/S, DFA)

**Dashboard Sizing Options:**

- **Small:** Essential metrics only (mobile/small screens)

- **Normal:** Balanced information density (standard desktop)

- **Large:** Maximum detail (multi-monitor setups)

**Position Options:**

- **Top Right:** Standard placement (avoids price action)

- **Top Left:** Wide chart optimization

- **Bottom Right:** Recent price focus (scalping)

- **Bottom Left:** Maximum price visibility (swing trading)

---

## 🎯 SIGNAL GENERATION LOGIC

### Multi-Component Convergence System

**Component Signal Architecture:**

The TMAE generates signals through sophisticated component analysis rather than simple threshold crossing:

**Volatility Component:**

- **Jump Detection:** Mahalanobis distance threshold breach

- **Hawkes Intensity:** Self-exciting process activation (>0.2)

- **Multi-dimensional:** Considers all volatility dimensions simultaneously

**Hurst Regime Component:**

- **Trending Markets:** Price above SMA-20 with positive momentum

- **Mean-Reverting Markets:** Price at Bollinger Band extremes

- **Random Markets:** Bollinger squeeze breakouts with directional confirmation

**Transfer Entropy Component:**

- **Volume Leadership:** Information flow from volume to price

- **Volume Spike:** Volume 110%+ above 20-period average

- **Flow Significance:** Above entropy threshold with directional bias

### Democratic Signal Weighting

**Signal Mode Implementation:**

- **Aggressive Mode:** Any single component triggers signal

- **Confluence Mode:** Minimum 2 components must agree

- **Conservative Mode:** All 3 components must align

**Momentum Confirmation:**

All signals require momentum confirmation:

- **Long Signals:** RSI >50 AND price >EMA-9

- **Short Signals:** RSI <50 AND price 0.6):**

- **Increase Sensitivity:** Catch momentum continuation

- **Lower Mean Reversion Threshold:** Avoid counter-trend signals

- **Emphasize Volume Leadership:** Institutional accumulation/distribution

- **Tensor Field Focus:** Use expansion for trend continuation

- **Signal Mode:** Aggressive or Confluence for trend following

**Range-Bound Markets (Hurst <0.4):**

- **Decrease Sensitivity:** Avoid false breakouts

- **Lower Trending Threshold:** Quick regime recognition

- **Focus on Price Leadership:** Retail sentiment extremes

- **Fractal Grid Emphasis:** Support/resistance trading

- **Signal Mode:** Conservative for high-probability reversals

**Volatile Markets (High Jump Frequency):**

- **Increase Hawkes Decay:** Recognize event clustering

- **Higher Jump Threshold:** Avoid noise signals

- **Maximum Dimensions:** Capture full volatility complexity

- **Reduce Position Sizing:** Risk management adaptation

- **Enhanced Visuals:** Maximum information for rapid decisions

**Low Volatility Markets (Low Jump Frequency):**

- **Decrease Jump Threshold:** Capture subtle movements

- **Lower Hawkes Decay:** Treat moves as independent

- **Reduce Dimensions:** Simplify analysis

- **Increase Position Sizing:** Capitalize on compressed volatility

- **Minimal Visuals:** Reduce distraction in quiet markets

---

## 🚀 ADVANCED TRADING STRATEGIES

### The Mathematical Convergence Method

**Entry Protocol:**

1. **Fractal Grid Approach:** Monitor price approaching significant fractal levels

2. **Tensor Field Confirmation:** Verify field expansion supporting direction

3. **Portal Signal:** Wait for dimensional portal appearance

4. **ELITE/STRONG Quality:** Only trade highest quality mathematical signals

5. **Component Consensus:** Confirm 2+ components agree in Confluence mode

**Example Implementation:**

- Price approaching 21-period fractal high

- Tensor field expanding upward (bullish mathematical alignment)

- Green portal appears below price (trending regime confirmation)

- ELITE quality signal with 3/3 components active

- Enter long position with stop below fractal level

**Risk Management:**

- **Stop Placement:** Below/above fractal level that generated signal

- **Position Sizing:** Based on Mahalanobis distance (higher distance = smaller size)

- **Profit Targets:** Next fractal level or tensor field resistance

### The Regime Transition Strategy

**Regime Change Detection:**

1. **Monitor Hurst Exponent:** Watch for persistent moves above/below thresholds

2. **Portal Color Change:** Regime transitions show different portal colors

3. **Background Intensity:** Increasing regime background intensity

4. **Mathematical Confirmation:** Wait for regime confirmation (hysteresis)

**Trading Implementation:**

- **Trending Transitions:** Trade momentum breakouts, follow trend

- **Mean Reversion Transitions:** Trade range boundaries, fade extremes

- **Random Transitions:** Trade breakouts with tight stops

**Advanced Techniques:**

- **Multi-Timeframe:** Confirm regime on higher timeframe

- **Early Entry:** Enter on regime transition rather than confirmation

- **Regime Strength:** Larger positions during strong regime signals

### The Information Flow Momentum Strategy

**Flow Detection Protocol:**

1. **Monitor Transfer Entropy:** Watch for significant information flow shifts

2. **Volume Leadership:** Strong edge when volume leads price

3. **Flow Acceleration:** Increasing flow strength indicates momentum

4. **Directional Confirmation:** Ensure flow aligns with intended trade direction

**Entry Signals:**

- **Volume → Price Flow:** Enter during accumulation/distribution phases

- **Price → Volume Flow:** Enter on momentum confirmation breaks

- **Flow Reversal:** Counter-trend entries when flow reverses

**Optimization:**

- **Scalping:** Use immediate flow detection (2-5 bar lag)

- **Swing Trading:** Use structural flow (10-20 bar lag)

- **Multi-Asset:** Compare flow between correlated assets

### The Tensor Field Expansion Strategy

**Field Mathematics:**

The tensor field expansion indicates mathematical pressure building in market structure:

**Expansion Phases:**

1. **Compression:** Field contracts, volatility decreases

2. **Tension Building:** Mathematical pressure accumulates

3. **Expansion:** Field expands rapidly with directional movement

4. **Resolution:** Field stabilizes at new equilibrium

**Trading Applications:**

- **Compression Trading:** Prepare for breakout during field contraction

- **Expansion Following:** Trade direction of field expansion

- **Reversion Trading:** Fade extreme field expansion

- **Multi-Dimensional:** Consider all field layers for confirmation

### The Hawkes Process Event Strategy

**Self-Exciting Jump Trading:**

Understanding that market shocks cluster and create follow-on opportunities:

**Jump Sequence Analysis:**

1. **Initial Jump:** First volatility jump detected

2. **Clustering Phase:** Hawkes intensity remains elevated

3. **Follow-On Opportunities:** Additional jumps more likely

4. **Decay Period:** Intensity gradually decreases

**Implementation:**

- **Jump Confirmation:** Wait for mathematical jump confirmation

- **Direction Assessment:** Use other components for direction

- **Clustering Trades:** Trade subsequent moves during high intensity

- **Decay Exit:** Exit positions as Hawkes intensity decays

### The Fractal Confluence System

**Multi-Timeframe Fractal Analysis:**

Combining fractal levels across different periods for high-probability zones:

**Confluence Zones:**

- **Double Confluence:** 2 fractal levels align

- **Triple Confluence:** 3+ fractal levels cluster

- **Mathematical Confirmation:** Tensor field supports the level

- **Information Flow:** Transfer entropy confirms direction

**Trading Protocol:**

1. **Identify Confluence:** Find 2+ fractal levels within 1 ATR

2. **Mathematical Support:** Verify tensor field alignment

3. **Signal Quality:** Wait for STRONG or ELITE signal

4. **Risk Definition:** Use fractal level for stop placement

5. **Profit Targeting:** Next major fractal confluence zone

---

## ⚠️ COMPREHENSIVE RISK MANAGEMENT

### Mathematical Position Sizing

**Mahalanobis Distance Integration:**

Position size should inversely correlate with mathematical field strength:

```

Position Size = Base Size × (Threshold / Mahalanobis Distance)

```

**Risk Scaling Matrix:**

- **Low Field Strength (<2.0):** Standard position sizing

- **Moderate Field Strength (2.0-3.0):** 75% position sizing

- **High Field Strength (3.0-4.0):** 50% position sizing

- **Extreme Field Strength (>4.0):** 25% position sizing or no trade

### Signal Quality Risk Adjustment

**Quality-Based Position Sizing:**

- **ELITE Signals:** 100% of planned position size

- **STRONG Signals:** 75% of planned position size

- **GOOD Signals:** 50% of planned position size

- **WEAK Signals:** No position or paper trading only

**Component Agreement Scaling:**

- **3/3 Components:** Full position size

- **2/3 Components:** 75% position size

- **1/3 Components:** 50% position size or skip trade

### Regime-Adaptive Risk Management

**Trending Market Risk:**

- **Wider Stops:** Allow for trend continuation

- **Trend Following:** Trade with regime direction

- **Higher Position Size:** Trend probability advantage

- **Momentum Stops:** Trail stops based on momentum indicators

**Mean-Reverting Market Risk:**

- **Tighter Stops:** Quick exits on trend continuation

- **Contrarian Positioning:** Trade against extremes

- **Smaller Position Size:** Higher reversal failure rate

- **Level-Based Stops:** Use fractal levels for stops

**Random Market Risk:**

- **Breakout Focus:** Trade only clear breakouts

- **Tight Initial Stops:** Quick exit if breakout fails

- **Reduced Frequency:** Skip marginal setups

- **Range-Based Targets:** Profit targets at range boundaries

### Volatility-Adaptive Risk Controls

**High Volatility Periods:**

- **Reduced Position Size:** Account for wider price swings

- **Wider Stops:** Avoid noise-based exits

- **Lower Frequency:** Skip marginal setups

- **Faster Exits:** Take profits more quickly

**Low Volatility Periods:**

- **Standard Position Size:** Normal risk parameters

- **Tighter Stops:** Take advantage of compressed ranges

- **Higher Frequency:** Trade more setups

- **Extended Targets:** Allow for compressed volatility expansion

### Multi-Timeframe Risk Alignment

**Higher Timeframe Trend:**

- **With Trend:** Standard or increased position size

- **Against Trend:** Reduced position size or skip

- **Neutral Trend:** Standard position size with tight management

**Risk Hierarchy:**

1. **Primary:** Current timeframe signal quality

2. **Secondary:** Higher timeframe trend alignment

3. **Tertiary:** Mathematical field strength

4. **Quaternary:** Market regime classification

---

## 📚 EDUCATIONAL VALUE AND MATHEMATICAL CONCEPTS

### Advanced Mathematical Concepts

**Tensor Analysis in Markets:**

The TMAE introduces traders to tensor analysis, a branch of mathematics typically reserved for physics and advanced engineering. Tensors provide a framework for understanding multi-dimensional market relationships that scalar and vector analysis cannot capture.

**Information Theory Applications:**

Transfer entropy implementation teaches traders about information flow in markets, a concept from information theory that quantifies directional causality between variables. This provides intuition about market microstructure and participant behavior.

**Fractal Geometry in Trading:**

The Hurst exponent calculation exposes traders to fractal geometry concepts, helping understand that markets exhibit self-similar patterns across multiple timeframes. This mathematical insight transforms how traders view market structure.

**Stochastic Process Theory:**

The Hawkes process implementation introduces concepts from stochastic process theory, specifically self-exciting point processes. This provides mathematical framework for understanding why market events cluster and exhibit memory effects.

### Learning Progressive Complexity

**Beginner Mathematical Concepts:**

- **Volatility Dimensions:** Understanding multi-dimensional analysis

- **Regime Classification:** Learning market personality types

- **Signal Democracy:** Algorithmic consensus building

- **Visual Mathematics:** Interpreting mathematical concepts visually

**Intermediate Mathematical Applications:**

- **Mahalanobis Distance:** Statistical distance in multi-dimensional space

- **Rescaled Range Analysis:** Fractal dimension measurement

- **Information Entropy:** Quantifying uncertainty and causality

- **Field Theory:** Understanding mathematical fields in market context

**Advanced Mathematical Integration:**

- **Tensor Field Dynamics:** Multi-dimensional market force analysis

- **Stochastic Self-Excitation:** Event clustering and memory effects

- **Categorical Composition:** Mathematical signal combination theory

- **Topological Market Analysis:** Understanding market shape and connectivity

### Practical Mathematical Intuition

**Developing Market Mathematics Intuition:**

The TMAE serves as a bridge between abstract mathematical concepts and practical trading applications. Traders develop intuitive understanding of:

- **How markets exhibit mathematical structure beneath apparent randomness**

- **Why multi-dimensional analysis reveals patterns invisible to single-variable approaches**

- **How information flows through markets in measurable, predictable ways**

- **Why mathematical models provide probabilistic edges rather than certainties**

---

## 🔬 IMPLEMENTATION AND OPTIMIZATION

### Getting Started Protocol

**Phase 1: Observation (Week 1)**

1. **Apply with defaults:** Use standard settings on your primary trading timeframe

2. **Study visual elements:** Learn to interpret tensor fields, portals, and streams

3. **Monitor dashboard:** Observe how metrics change with market conditions

4. **No trading:** Focus entirely on pattern recognition and understanding

**Phase 2: Pattern Recognition (Week 2-3)**

1. **Identify signal patterns:** Note what market conditions produce different signal qualities

2. **Regime correlation:** Observe how Hurst regimes affect signal performance

3. **Visual confirmation:** Learn to read tensor field expansion and portal signals

4. **Component analysis:** Understand which components drive signals in different markets

**Phase 3: Parameter Optimization (Week 4-5)**

1. **Asset-specific tuning:** Adjust parameters for your specific trading instrument

2. **Timeframe optimization:** Fine-tune for your preferred trading timeframe

3. **Sensitivity adjustment:** Balance signal frequency with quality

4. **Visual customization:** Optimize colors and intensity for your trading environment

**Phase 4: Live Implementation (Week 6+)**

1. **Paper trading:** Test signals with hypothetical trades

2. **Small position sizing:** Begin with minimal risk during learning phase

3. **Performance tracking:** Monitor actual vs. expected signal performance

4. **Continuous optimization:** Refine settings based on real performance data

### Performance Monitoring System

**Signal Quality Tracking:**

- **ELITE Signal Win Rate:** Track highest quality signals separately

- **Component Performance:** Monitor which components provide best signals

- **Regime Performance:** Analyze performance across different market regimes

- **Timeframe Analysis:** Compare performance across different session times

**Mathematical Metric Correlation:**

- **Field Strength vs. Performance:** Higher field strength should correlate with better performance

- **Component Agreement vs. Win Rate:** More component agreement should improve win rates

- **Regime Alignment vs. Success:** Trading with mathematical regime should outperform

### Continuous Optimization Process

**Monthly Review Protocol:**

1. **Performance Analysis:** Review win rates, profit factors, and maximum drawdown

2. **Parameter Assessment:** Evaluate if current settings remain optimal

3. **Market Adaptation:** Adjust for changes in market character or volatility

4. **Component Weighting:** Consider if certain components should receive more/less emphasis

**Quarterly Deep Analysis:**

1. **Mathematical Model Validation:** Verify that mathematical relationships remain valid

2. **Regime Distribution:** Analyze time spent in different market regimes

3. **Signal Evolution:** Track how signal characteristics change over time

4. **Correlation Analysis:** Monitor correlations between different mathematical components

---

## 🌟 UNIQUE INNOVATIONS AND CONTRIBUTIONS

### Revolutionary Mathematical Integration

**First-Ever Implementations:**

1. **Multi-Dimensional Volatility Tensor:** First indicator to implement true tensor analysis for market volatility

2. **Real-Time Hawkes Process:** First trading implementation of self-exciting point processes

3. **Transfer Entropy Trading Signals:** First practical application of information theory for trade generation

4. **Democratic Component Voting:** First algorithmic consensus system for signal generation

5. **Fractal-Projected Signal Quality:** First system to predict signal quality at future price levels

### Advanced Visualization Innovations

**Mathematical Visualization Breakthroughs:**

- **Tensor Field Radiation:** Visual representation of mathematical field energy

- **Dimensional Portal System:** Category theory visualization for regime transitions

- **Information Flow Streams:** Real-time visual display of market information transfer

- **Multi-Layer Fractal Grid:** Intelligent spacing and projection system

- **Regime Intensity Mapping:** Dynamic background showing mathematical regime strength

### Practical Trading Innovations

**Trading System Advances:**

- **Quality-Weighted Signal Generation:** Signals rated by mathematical confidence

- **Regime-Adaptive Strategy Selection:** Automatic strategy optimization based on market personality

- **Anti-Spam Signal Protection:** Mathematical prevention of signal clustering

- **Component Performance Tracking:** Real-time monitoring of algorithmic component success

- **Field-Strength Position Sizing:** Mathematical volatility integration for risk management

---

## ⚖️ RESPONSIBLE USAGE AND LIMITATIONS

### Mathematical Model Limitations

**Understanding Model Boundaries:**

While the TMAE implements sophisticated mathematical concepts, traders must understand fundamental limitations:

- **Markets Are Not Purely Mathematical:** Human psychology, news events, and fundamental factors create unpredictable elements

- **Past Performance Limitations:** Mathematical relationships that worked historically may not persist indefinitely

- **Model Risk:** Complex models can fail during unprecedented market conditions

- **Overfitting Potential:** Highly optimized parameters may not generalize to future market conditions

### Proper Implementation Guidelines

**Risk Management Requirements:**

- **Never Risk More Than 2% Per Trade:** Regardless of signal quality

- **Diversification Mandatory:** Don't rely solely on mathematical signals

- **Position Sizing Discipline:** Use mathematical field strength for sizing, not confidence

- **Stop Loss Non-Negotiable:** Every trade must have predefined risk parameters

**Realistic Expectations:**

- **Mathematical Edge, Not Certainty:** The indicator provides probabilistic advantages, not guaranteed outcomes

- **Learning Curve Required:** Complex mathematical concepts require time to master

- **Market Adaptation Necessary:** Parameters must evolve with changing market conditions

- **Continuous Education Important:** Understanding underlying mathematics improves application

### Ethical Trading Considerations

**Market Impact Awareness:**

- **Information Asymmetry:** Advanced mathematical analysis may provide advantages over other market participants

- **Position Size Responsibility:** Large positions based on mathematical signals can impact market structure

- **Sharing Knowledge:** Consider educational contributions to trading community

- **Fair Market Participation:** Use mathematical advantages responsibly within market framework

### Professional Development Path

**Skill Development Sequence:**

1. **Basic Mathematical Literacy:** Understand fundamental concepts before advanced application

2. **Risk Management Mastery:** Develop disciplined risk control before relying on complex signals

3. **Market Psychology Understanding:** Combine mathematical analysis with behavioral market insights

4. **Continuous Learning:** Stay updated on mathematical finance developments and market evolution

---

## 🔮 CONCLUSION

The Tensor Market Analysis Engine represents a quantum leap forward in technical analysis, successfully bridging the gap between advanced pure mathematics and practical trading applications. By integrating multi-dimensional volatility analysis, fractal market theory, and information flow dynamics, the TMAE reveals market structure invisible to conventional analysis while maintaining visual clarity and practical usability.

### Mathematical Innovation Legacy

This indicator establishes new paradigms in technical analysis:

- **Tensor analysis for market volatility understanding**

- **Stochastic self-excitation for event clustering prediction**

- **Information theory for causality-based trade generation**

- **Democratic algorithmic consensus for signal quality enhancement**

- **Mathematical field visualization for intuitive market understanding**

### Practical Trading Revolution

Beyond mathematical innovation, the TMAE transforms practical trading:

- **Quality-rated signals replace binary buy/sell decisions**

- **Regime-adaptive strategies automatically optimize for market personality**

- **Multi-dimensional risk management integrates mathematical volatility measures**

- **Visual mathematical concepts make complex analysis immediately interpretable**

- **Educational value creates lasting improvement in trading understanding**

### Future-Proof Design

The mathematical foundations ensure lasting relevance:

- **Universal mathematical principles transcend market evolution**

- **Multi-dimensional analysis adapts to new market structures**

- **Regime detection automatically adjusts to changing market personalities**

- **Component democracy allows for future algorithmic additions**

- **Mathematical visualization scales with increasing market complexity**

### Commitment to Excellence

The TMAE represents more than an indicator—it embodies a philosophy of bringing rigorous mathematical analysis to trading while maintaining practical utility and visual elegance. Every component, from the multi-dimensional tensor fields to the democratic signal generation, reflects a commitment to mathematical accuracy, trading practicality, and educational value.

### Trading with Mathematical Precision

In an era where markets grow increasingly complex and computational, the TMAE provides traders with mathematical tools previously available only to institutional quantitative research teams. Yet unlike academic mathematical models, the TMAE translates complex concepts into intuitive visual representations and practical trading signals.

By combining the mathematical rigor of tensor analysis, the statistical power of multi-dimensional volatility modeling, and the information-theoretic insights of transfer entropy, traders gain unprecedented insight into market structure and dynamics.

### Final Perspective

Markets, like nature, exhibit profound mathematical beauty beneath apparent chaos. The Tensor Market Analysis Engine serves as a mathematical lens that reveals this hidden order, transforming how traders perceive and interact with market structure.

Through mathematical precision, visual elegance, and practical utility, the TMAE empowers traders to see beyond the noise and trade with the confidence that comes from understanding the mathematical principles governing market behavior.

Trade with mathematical insight. Trade with the power of tensors. Trade with the TMAE.

*"In mathematics, you don't understand things. You just get used to them." - John von Neumann*

*With the TMAE, mathematical market understanding becomes not just possible, but intuitive.*

— Dskyz, Trade with insight. Trade with anticipation.

Open Interest-RSI + Funding + Fractal DivergencesIndicator — “Open Interest-RSI + Funding + Fractal Divergences”

A multi-factor oscillator that fuses Open-Interest RSI, real-time Funding-Rate data and price/OI fractal divergences.

It paints BUY/SELL arrows in its own pane and directly on the price chart, helping you spot spots where crowd positioning, leverage costs and price action contradict each other.

1 Purpose

OI-RSI – measures conviction behind position changes instead of price momentum.

Funding Rate – shows who pays to hold positions (longs → bull bias, shorts → bear bias).

Fractal Divergences – detects HH/LL in price that are not confirmed by OI-RSI.

Optional Funding filter – hides signals when funding is already extreme.

Together these elements highlight exhaustion points and potential mean-reversion trades.

2 Inputs

RSI / Divergence

RSI length – default 14.

High-OI level / Low-OI level – default 70 / 30.

Fractal period n – default 2 (swing width).

Fractals to compare – how many past swings to scan, default 3.

Max visible arrows – keeps last 50 BUY/SELL arrows for speed.

Funding Rate

mode – choose FR, Avg Premium, Premium Index, Avg Prem + PI or FR-candle.

Visual scale (×) – multiplies raw funding to fit 0-100 oscillator scale (default 10).

specify symbol – enable only if funding symbol differs from chart.

use lower tf – averages 1-min premiums for smoother intraday view.

show table – tiny two-row widget at chart edge.

Signal Filter

Use Funding filter – ON hides long signals when funding > Buy-threshold and short signals when funding < Sell-threshold.

BUY threshold (%) – default 0.00 (raw %).

SELL threshold (%) – default 0.00 (raw %).

(Enter funding thresholds as raw percentages, e.g. 0.01 = +0.01 %).

3 Visual Outputs

Sub-pane

Aqua OI-RSI curve with 70 / 50 / 30 reference lines.

Funding visualised according to selected mode (green above 0, red below 0, or other).

BUY / SELL arrows at oscillator extremes.

Price chart

Identical BUY / SELL arrows plotted with force_overlay = true above/below candles that formed qualifying fractals.

Optional table

Shows current asset ticker and latest funding value of the chosen mode.

4 Signal Logic (Summary)

Load _OI series and compute RSI.

Retrieve Funding-Rate + Premium Index (optionally from lower TF).

Find fractal swings (n bars left & right).

Check divergence:

Bearish – price HH + OI-RSI LH.

Bullish – price LL + OI-RSI HL.

If Funding-filter enabled, require funding < Buy-thr (long) or > Sell-thr (short).

Plot arrows and trigger two built-in alerts (Bearish OI-RSI divergence, Bullish OI-RSI divergence).

Signals are fixed once the fractal bar closes; they do not repaint afterwards.

5 How to Use

Attach to a liquid perpetual-futures chart (BTC, ETH, major Binance contracts).

If _OI or funding series is missing you’ll see an error.

Choose timeframe:

15 m – 4 h for intraday;

1 D+ for swing trades.

Lower TFs → more signals; raise Fractals to compare or use Funding filter to trim noise.

Trade checklist

Funding positive and rising → longs overcrowded.

Price makes higher high; OI-RSI makes lower high; Funding above Sell-threshold → consider short.

Reverse logic for longs.

Combine with trend filter (EMA ribbon, SuperTrend, etc.) so you fade only when price is stretched.

Automation – set TradingView alerts on the two alertconditions and send to webhooks/bots.

Performance tips

Keep Max visible arrows ≤ 50.

Disable lower-TF premium aggregation if script feels heavy.

6 Limitations

Some symbols lack _OI or funding history → script stops with a console message.

Binance Premium Index begins mid-2020; older dates show na.

Divergences confirm only after n bars (no forward repaint).

7 Changelog

v1.0 – 10 Jun 2025

Initial public release.

Added price-chart arrows via force_overlay.

Donchian x WMA Crossover (2025 Only, Adjustable TP, Real OHLC)Short Description:

Long-only breakout system that goes long when the Donchian Low crosses up through a Weighted Moving Average, and closes when it crosses back down (with an optional take-profit), restricted to calendar year 2025. All signals use the instrument’s true OHLC data (even on Heikin-Ashi charts), start with 1 000 AUD of capital, and deploy 100 % equity per trade.

Ideal parameters configured for Temple & Webster on ASX 30 minute candles. Adjust parameter to suit however best to download candle interval data and have GPT test the pine script for optimum parameters for your trading symbol.

Detailed Description

1. Strategy Concept

This strategy captures trend-driven breakouts off the bottom of a Donchian channel. By combining the Donchian Low with a WMA filter, it aims to:

Enter when volatility compresses and price breaks above the recent Donchian Low while the longer‐term WMA confirms upward momentum.

Exit when price falls back below that same WMA (i.e. when the Donchian Low crosses back down through WMA), but only if the WMA itself has stopped rising.

Optional Take-Profit: you can specify a profit target in decimal form (e.g. 0.01 = 1 %).

2. Timeframe & Universe

In-sample period: only bars stamped between Jan 1 2025 00:00 UTC and Dec 31 2025 23:59 UTC are considered.

Any resolution (e.g. 30 m, 1 h, D, etc.) is supported—just set your preferred timeframe in the TradingView UI.

3. True-Price Execution

All indicator calculations (Donchian Low, WMA, crossover checks, take-profit) are sourced from the chart’s underlying OHLC via request.security(). This guarantees that:

You can view Heikin-Ashi or other styled candles, but your strategy will execute on the real OHLC bars.

Chart styling never suppresses or distorts your backtest results.

4. Position Sizing & Equity

Initial capital: 1 000 AUD

Size per trade: 100 % of available equity

No pyramiding: one open position at a time

5. Inputs (all exposed in the “Inputs” tab):

Input Default Description

Donchian Length 7 Number of bars to calculate the Donchian channel low

WMA Length 62 Period of the Weighted Moving Average filter

Take Profit (decimal) 0.01 Exit when price ≥ entry × (1 + take_profit_perc)

6. How It Works

Donchian Low: ta.lowest(low, DonchianLength) over the specified look-back.

WMA: ta.wma(close, WMALength) applied to true closes.

Entry: ta.crossover(DonchianLow, WMA) AND barTime ∈ 2025.

Exit:

Cross-down exit: ta.crossunder(DonchianLow, WMA) and WMA is not rising (i.e. momentum has stalled).

Take-profit exit: price ≥ entry × (1 + take_profit_perc).

Calendar exit: barTime falls outside 2025.

7. Usage Notes

After adding to your chart, open the Strategy Tester tab to review performance metrics, list of trades, equity curve, etc.

You can toggle your chart to Heikin-Ashi for visual clarity without affecting execution, thanks to the real-OHLC calls.

Categorical Market Morphisms (CMM)Categorical Market Morphisms (CMM) - Where Abstract Algebra Transcends Reality

A Revolutionary Application of Category Theory and Homotopy Type Theory to Financial Markets

Bridging Pure Mathematics and Market Analysis Through Functorial Dynamics

Theoretical Foundation: The Mathematical Revolution

Traditional technical analysis operates on Euclidean geometry and classical statistics. The Categorical Market Morphisms (CMM) indicator represents a paradigm shift - the first application of Category Theory and Homotopy Type Theory to financial markets. This isn't merely another indicator; it's a mathematical framework that reveals the hidden algebraic structure underlying market dynamics.

Category Theory in Markets

Category theory, often called "the mathematics of mathematics," studies structures and the relationships between them. In market terms:

Objects = Market states (price levels, volume conditions, volatility regimes)

Morphisms = State transitions (price movements, volume changes, volatility shifts)

Functors = Structure-preserving mappings between timeframes

Natural Transformations = Coherent changes across multiple market dimensions

The Morphism Detection Engine

The core innovation lies in detecting morphisms - the categorical arrows representing market state transitions:

Morphism Strength = exp(-normalized_change × (3.0 / sensitivity))

Threshold = 0.3 - (sensitivity - 1.0) × 0.15

This exponential decay function captures how market transitions lose coherence over distance, while the dynamic threshold adapts to market sensitivity.

Functorial Analysis Framework

Markets must preserve structure across timeframes to maintain coherence. Our functorial analysis verifies this through composition laws:

Composition Error = |f(BC) × f(AB) - f(AC)| / |f(AC)|

Functorial Integrity = max(0, 1.0 - average_error)

When functorial integrity breaks down, market structure becomes unstable - a powerful early warning system.

Homotopy Type Theory: Path Equivalence in Markets

The Revolutionary Path Analysis

Homotopy Type Theory studies when different paths can be continuously deformed into each other. In markets, this reveals arbitrage opportunities and equivalent trading paths:

Path Distance = Σ(weight × |normalized_path1 - normalized_path2|)

Homotopy Score = (correlation + 1) / 2 × (1 - average_distance)

Equivalence Threshold = 1 / (threshold × √univalence_strength)

The Univalence Axiom in Trading

The univalence axiom states that equivalent structures can be treated as identical. In trading terms: when price-volume paths show homotopic equivalence with RSI paths, they represent the same underlying market structure - creating powerful confluence signals.

Universal Properties: The Four Pillars of Market Structure

Category theory's universal properties reveal fundamental market patterns:

Initial Objects (Market Bottoms)

Mathematical Definition = Unique morphisms exist FROM all other objects TO the initial object

Market Translation = All selling pressure naturally flows toward the bottom

Detection Algorithm:

Strength = local_low(0.3) + oversold(0.2) + volume_surge(0.2) + momentum_reversal(0.2) + morphism_flow(0.1)

Signal = strength > 0.4 AND morphism_exists

Terminal Objects (Market Tops)

Mathematical Definition = Unique morphisms exist FROM the terminal object TO all others

Market Translation = All buying pressure naturally flows away from the top

Product Objects (Market Equilibrium)

Mathematical Definition = Universal property combining multiple objects into balanced state

Market Translation = Price, volume, and volatility achieve multi-dimensional balance

Coproduct Objects (Market Divergence)

Mathematical Definition = Universal property representing branching possibilities

Market Translation = Market bifurcation points where multiple scenarios become possible

Consciousness Detection: Emergent Market Intelligence

The most groundbreaking feature detects market consciousness - when markets exhibit self-awareness through fractal correlations:

Consciousness Level = Σ(correlation_levels × weights) × fractal_dimension

Fractal Score = log(range_ratio) / log(memory_period)

Multi-Scale Awareness:

Micro = Short-term price-SMA correlations

Meso = Medium-term structural relationships

Macro = Long-term pattern coherence

Volume Sync = Price-volume consciousness

Volatility Awareness = ATR-change correlations

When consciousness_level > threshold , markets display emergent intelligence - self-organizing behavior that transcends simple mechanical responses.

Advanced Input System: Precision Configuration

Categorical Universe Parameters

Universe Level (Type_n) = Controls categorical complexity depth

Type 1 = Price only (pure price action)

Type 2 = Price + Volume (market participation)

Type 3 = + Volatility (risk dynamics)

Type 4 = + Momentum (directional force)

Type 5 = + RSI (momentum oscillation)

Sector Optimization:

Crypto = 4-5 (high complexity, volume crucial)

Stocks = 3-4 (moderate complexity, fundamental-driven)

Forex = 2-3 (low complexity, macro-driven)

Morphism Detection Threshold = Golden ratio optimized (φ = 0.618)

Lower values = More morphisms detected, higher sensitivity

Higher values = Only major transformations, noise reduction

Crypto = 0.382-0.618 (high volatility accommodation)

Stocks = 0.618-1.0 (balanced detection)

Forex = 1.0-1.618 (macro-focused)

Functoriality Tolerance = φ⁻² = 0.146 (mathematically optimal)

Controls = composition error tolerance

Trending markets = 0.1-0.2 (strict structure preservation)

Ranging markets = 0.2-0.5 (flexible adaptation)

Categorical Memory = Fibonacci sequence optimized

Scalping = 21-34 bars (short-term patterns)

Swing = 55-89 bars (intermediate cycles)

Position = 144-233 bars (long-term structure)

Homotopy Type Theory Parameters

Path Equivalence Threshold = Golden ratio φ = 1.618

Volatile markets = 2.0-2.618 (accommodate noise)

Normal conditions = 1.618 (balanced)

Stable markets = 0.786-1.382 (sensitive detection)

Deformation Complexity = Fibonacci-optimized path smoothing

3,5,8,13,21 = Each number provides different granularity

Higher values = smoother paths but slower computation

Univalence Axiom Strength = φ² = 2.618 (golden ratio squared)

Controls = how readily equivalent structures are identified

Higher values = find more equivalences

Visual System: Mathematical Elegance Meets Practical Clarity

The Morphism Energy Fields (Red/Green Boxes)

Purpose = Visualize categorical transformations in real-time

Algorithm:

Energy Range = ATR × flow_strength × 1.5

Transparency = max(10, base_transparency - 15)

Interpretation:

Green fields = Bullish morphism energy (buying transformations)

Red fields = Bearish morphism energy (selling transformations)

Size = Proportional to transformation strength

Intensity = Reflects morphism confidence

Consciousness Grid (Purple Pattern)

Purpose = Display market self-awareness emergence

Algorithm:

Grid_size = adaptive(lookback_period / 8)

Consciousness_range = ATR × consciousness_level × 1.2

Interpretation:

Density = Higher consciousness = denser grid

Extension = Cloud lookback controls historical depth

Intensity = Transparency reflects awareness level

Homotopy Paths (Blue Gradient Boxes)

Purpose = Show path equivalence opportunities

Algorithm:

Path_range = ATR × homotopy_score × 1.2

Gradient_layers = 3 (increasing transparency)

Interpretation:

Blue boxes = Equivalent path opportunities

Gradient effect = Confidence visualization

Multiple layers = Different probability levels

Functorial Lines (Green Horizontal)

Purpose = Multi-timeframe structure preservation levels

Innovation = Smart spacing prevents overcrowding

Min_separation = price × 0.001 (0.1% minimum)

Max_lines = 3 (clarity preservation)

Features:

Glow effect = Background + foreground lines

Adaptive labels = Only show meaningful separations

Color coding = Green (preserved), Orange (stressed), Red (broken)

Signal System: Bull/Bear Precision

🐂 Initial Objects = Bottom formations with strength percentages

🐻 Terminal Objects = Top formations with confidence levels

⚪ Product/Coproduct = Equilibrium circles with glow effects

Professional Dashboard System

Main Analytics Dashboard (Top-Right)

Market State = Real-time categorical classification

INITIAL OBJECT = Bottom formation active

TERMINAL OBJECT = Top formation active

PRODUCT STATE = Market equilibrium

COPRODUCT STATE = Divergence/bifurcation

ANALYZING = Processing market structure

Universe Type = Current complexity level and components

Morphisms:

ACTIVE (X%) = Transformations detected, percentage shows strength

DORMANT = No significant categorical changes

Functoriality:

PRESERVED (X%) = Structure maintained across timeframes

VIOLATED (X%) = Structure breakdown, instability warning

Homotopy:

DETECTED (X%) = Path equivalences found, arbitrage opportunities

NONE = No equivalent paths currently available

Consciousness:

ACTIVE (X%) = Market self-awareness emerging, major moves possible

EMERGING (X%) = Consciousness building

DORMANT = Mechanical trading only

Signal Monitor & Performance Metrics (Left Panel)

Active Signals Tracking:

INITIAL = Count and current strength of bottom signals

TERMINAL = Count and current strength of top signals

PRODUCT = Equilibrium state occurrences

COPRODUCT = Divergence event tracking

Advanced Performance Metrics:

CCI (Categorical Coherence Index):

CCI = functorial_integrity × (morphism_exists ? 1.0 : 0.5)

STRONG (>0.7) = High structural coherence

MODERATE (0.4-0.7) = Adequate coherence

WEAK (<0.4) = Structural instability

HPA (Homotopy Path Alignment):

HPA = max_homotopy_score × functorial_integrity

ALIGNED (>0.6) = Strong path equivalences

PARTIAL (0.3-0.6) = Some equivalences

WEAK (<0.3) = Limited path coherence

UPRR (Universal Property Recognition Rate):

UPRR = (active_objects / 4) × 100%

Percentage of universal properties currently active

TEPF (Transcendence Emergence Probability Factor):

TEPF = homotopy_score × consciousness_level × φ

Probability of consciousness emergence (golden ratio weighted)

MSI (Morphological Stability Index):

MSI = (universe_depth / 5) × functorial_integrity × consciousness_level

Overall system stability assessment

Overall Score = Composite rating (EXCELLENT/GOOD/POOR)

Theory Guide (Bottom-Right)

Educational reference panel explaining:

Objects & Morphisms = Core categorical concepts

Universal Properties = The four fundamental patterns

Dynamic Advice = Context-sensitive trading suggestions based on current market state

Trading Applications: From Theory to Practice

Trend Following with Categorical Structure

Monitor functorial integrity = only trade when structure preserved (>80%)

Wait for morphism energy fields = red/green boxes confirm direction

Use consciousness emergence = purple grids signal major move potential

Exit on functorial breakdown = structure loss indicates trend end

Mean Reversion via Universal Properties

Identify Initial/Terminal objects = 🐂/🐻 signals mark extremes

Confirm with Product states = equilibrium circles show balance points

Watch Coproduct divergence = bifurcation warnings

Scale out at Functorial levels = green lines provide targets

Arbitrage through Homotopy Detection

Blue gradient boxes = indicate path equivalence opportunities

HPA metric >0.6 = confirms strong equivalences

Multiple timeframe convergence = strengthens signal

Consciousness active = amplifies arbitrage potential

Risk Management via Categorical Metrics

Position sizing = Based on MSI (Morphological Stability Index)

Stop placement = Tighter when functorial integrity low

Leverage adjustment = Reduce when consciousness dormant

Portfolio allocation = Increase when CCI strong

Sector-Specific Optimization Strategies

Cryptocurrency Markets

Universe Level = 4-5 (full complexity needed)

Morphism Sensitivity = 0.382-0.618 (accommodate volatility)

Categorical Memory = 55-89 (rapid cycles)

Field Transparency = 1-5 (high visibility needed)

Focus Metrics = TEPF, consciousness emergence

Stock Indices

Universe Level = 3-4 (moderate complexity)

Morphism Sensitivity = 0.618-1.0 (balanced)

Categorical Memory = 89-144 (institutional cycles)

Field Transparency = 5-10 (moderate visibility)

Focus Metrics = CCI, functorial integrity

Forex Markets

Universe Level = 2-3 (macro-driven)

Morphism Sensitivity = 1.0-1.618 (noise reduction)

Categorical Memory = 144-233 (long cycles)

Field Transparency = 10-15 (subtle signals)

Focus Metrics = HPA, universal properties

Commodities

Universe Level = 3-4 (supply/demand dynamics) [/b

Morphism Sensitivity = 0.618-1.0 (seasonal adaptation)

Categorical Memory = 89-144 (seasonal cycles)

Field Transparency = 5-10 (clear visualization)

Focus Metrics = MSI, morphism strength

Development Journey: Mathematical Innovation

The Challenge

Traditional indicators operate on classical mathematics - moving averages, oscillators, and pattern recognition. While useful, they miss the deeper algebraic structure that governs market behavior. Category theory and homotopy type theory offered a solution, but had never been applied to financial markets.

The Breakthrough

The key insight came from recognizing that market states form a category where:

Price levels, volume conditions, and volatility regimes are objects

Market movements between these states are morphisms

The composition of movements must satisfy categorical laws