Custom Buy/Sell Pattern BuilderAre you tired of using trading indicators that only let you follow fixed, pre-designed rules? Do you wish you could build your own “Buy” or “Sell” signals, experiment with your own ideas, or see instantly if your unique pattern works—without learning coding or hiring a developer?

The Custom Buy/Sell Pattern Builder is designed for YOU.

This TradingView indicator lets ANY trader—even a complete beginner—define exactly what kind of price and volume conditions should create a BUY or SELL label on any chart, in any market, at any timeframe.

You don’t need to know programming. You don’t need to know the definition of a hammer, doji, volume spike, or Engulfing pattern.

With a few clicks and easy dropdown choices, you can:

Make your own rules for buying or selling

Choose how many candles your pattern should look at

Decide if you want the biggest body, the lowest volume, the biggest movement, or any combination you can imagine

The result?

You’ll see clear “BUY” or “SELL” labels automatically show up on your chart whenever the exact rule YOU built matches current price action.

No more guessing. No more forced strategies. Just pure control and visual feedback!

Why Is This Powerful?

Traditional indicators (like MACD, RSI, or even classic candlestick scanners) work the same for everyone—and only as their inventors defined.

But every trader, and every market, is unique.

What if you could say:

“Show me a ‘SELL’ every time the newest candle is bigger than the one before, but with LESS volume, while the bar before that had an even smaller body—but more volume than all others?”

With this tool, it’s EASY!

You simply pick which candle you want to compare (most recent, previous, etc), what to compare (body or volume—body means the candle’s “thickness”, from open to close), choose “greater than”, “less than”, or “equal to”, and set a multiplier if you want (like “half as much”, “twice as big”, etc).

After this, if any bar on the chart fits all your rules, it will mark it as a BUY or SELL, depending on your selection.

This means—

Beginners can start experimenting with their intuition or small ideas, without tech hurdles

Experienced traders can visualize and fine-tune any possible logic, before they commit to backtesting or automating a real strategy

Every “what if” or “I wonder” setup is just 2–3 clicks away

How Does It Work? Simple Steps

1. Choose Your Signal Type

“Buy” or “Sell”

This tells the indicator whether to mark the qualifying bars with a green “BUY” or red “SELL” label

2. Pick How Many Candles To Use

“Pattern Candle Count” input (2, 3, or 4)

Example: If you use 4, the pattern will be applied to the most recent 4 candles at every step

3. Define Your Pattern With Inputs

For each candle (from newest “0” to oldest “3”), you can set:

Body Condition (example: “is this candle’s body bigger/smaller/equal to another?”)

Pick which candle to compare against

Pick “>”, “<”, “>=”, “<=”, or “=”

Set a multiplier if needed (like “0.5” to mean “half as big as” or “2” for “twice as big as”)

Volume Condition (exact same choices, but based on trading volume—not the candle’s price body)

For example:

“Candle0 Body > Candle2 Body”

means “the latest candle’s real-body (open–close) is bigger than the one two bars ago.”

“Candle1 Volume <= Candle2 Volume”

means “the previous candle’s volume is less than or equal to the volume of the bar two periods ago.”

You can leave a comparison blank if you don’t want to use it for a particular candle.

What Happens After You Set Your Rules?

Every bar on your chart is checked for your logic:

If ALL body AND volume conditions are true (for each candle you specified),

AND

The signal side (“Buy” or “Sell”) matches your dropdown,

Then a green “BUY” or red “SELL” label will show right on the bar, so you can visually spot exactly where your logic works!

Practical Example:

Suppose you want an entry setup that is:

“Sell whenever the newest candle’s body is bigger than two bars ago, body before that is bigger than three bars ago, AND the newest candle’s volume is less than or equal to two bars ago, AND the candle three bars ago’s volume is less than or equal to half the candle two bars ago’s volume.”

You’d set:

Pattern Candle Count: 4

Side: Sell

Candle0 Body Ref#: 2, Op: >, Mult: 1

Candle1 Body Ref#: 3, Op: >, Mult: 1

Candle0 Vol Ref#: 2, Op: <=, Mult: 1

Candle3 Vol Ref#: 2, Op: <=, Mult: 0.5

And the script will find all “SELL” bars on your chart matching these conditions.

Inputs Section: What Does Each Setting Do?

Let’s break down each input in the indicator’s Settings one by one, so even if you’re new, you’ll understand exactly how to use it!

1. Pattern Candle Count (2–4)

What is it?

This sets how many candles in a row you want your rule to look at.

Example:

“4” means your rules are based on the most recent candle and the 3 before it.

“2” means you are only comparing the current and previous candles.

Tip:

Beginners often use 4 to spot stronger patterns, but you can experiment!

2. Signal Side

What is it?

Choose “Buy” or “Sell”. The word you pick here decides which colored label (green for Buy, red for Sell) appears if your pattern matches.

Example:

Want to spot where “Sell” is likely? Pick “Sell”.

Change to “Buy” if you want bullish signals instead.

3. Body & Volume Comparison Settings (per Candle)

For each candle (#0 is newest/current, #3 is oldest in your pattern window):

Body Comparison

Candle# Body Ref#

Choose which other candle you want to compare this one’s body to.

“0” = newest, “1” = previous, “2” = two bars ago, “3” = three bars ago

Candle# Body Op (Operator; >, <, >=, <=, =)

How do you want to compare?

“>” means “greater than” (is bigger than)

“<” means “less than” (is smaller than)

“=” means “equal to”

Candle# Body Mult (Multiplier)

If you want relative comparisons. For example, with Mult=1:

“Candle0 body > Candle2 body x 1” means just “0 is larger than 2.”

“Candle0 body > Candle2 body x 2” means “0 is more than double 2.”

Volume Comparison

Candle# Vol Ref# / Op / Mult

Exact same logic as body, but works on the “Volume” of each candle (how much was traded during that bar).

How to Set Up a Rule (Step by Step Example)

Say you want to mark a Sell every time:

The most recent candle’s real body is BIGGER than the candle 2 bars ago;

The previous candle’s body is also BIGGER than the candle 3 bars ago;

The current candle’s volume is LESS than or equal to the volume of candle 2;

The previous candle’s volume is LESS than or equal to candle 2’s volume;

The candle 3 bars ago’s volume is LESS than or equal to HALF candle 2’s volume.

You’d set:

Pattern Candle Count: 4

Side: "Sell"

Candle0 Body Ref#: 2, Op: “>”, Mult: 1

Candle1 Body Ref#: 3, Op: “>”, Mult: 1

Candle0 Vol Ref#: 2, Op: “<=”, Mult: 1

Candle1 Vol Ref#: 2, Op: “<=”, Mult: 1

Candle3 Vol Ref#: 2, Op: “<=”, Mult: 0.5

All other comparisons (operators) can be left blank if you don’t want to use them!

When these rules are met, a bright red “SELL” label will appear right above the bar matching all your conditions.

Practical Tips & FAQ for Beginners

What does “body” mean?

It’s the “true range” of the candle: the difference between open and close. This ignores wicks for simple setups.

What does “volume” mean?

This is the total trading activity during that candle/bar. Many traders believe that patterns with different volume “meaning” (such as low-volume up bars, or high-volume down bars) signal a meaningful change.

What if nothing shows on chart?

It just means your current rules are rarely or never matched! Try making your comparisons simpler (maybe just 2-body and 2-volume conditions to start).

You can always hit “Reset Settings” to go back to default.

Can I use this for both buying and selling?

YES! You can detect both bullish (Buy) and bearish (Sell) custom conditions; just switch “Signal Side.”

Do I need to know coding?

Not at all! Everything is in simple input panels.

Creative Use Cases, Example Recipes & Troubleshooting

Creative Ways to Use

Spotting Reversals

Example:

Buy when: the newest candle body is LARGER than the previous 3 bars, but ALL volumes are lower than their neighbors.

Why? Sometimes, a big candle with surprisingly low volume after a sequence of small bars can signal a reversal.

Finding Exhaustion Moves

Example:

Sell when: the current bar body is twice as big as two bars ago, but volume is half.

Why? A very big candle with very little volume compared to similar bars may show the move is “running out of steam.”

Custom “Breakout + Confirmation” Patterns

Example:

Buy when:

Candle 0’s body is greater than Candle 2’s by at least 1.5x,

Candle 0’s volume is greater than Candle 1 and Candle 2,

Candle 1’s volume is less than Candle 0.

Why? This could catch strong breakouts but filter out noisy moves.

Multi-bar Bias/Squeeze Filter

Use “Pattern Candle Count: 4”

Set all 4 volume conditions to “<” and each reference to the previous candle.

Now, a BUY or SELL only marks when each bar is “dryer”/less active than the last — a classic squeeze or low-volatility buildup.

Troubleshooting Guide

“I don’t see any Buy/Sell label; is something broken?”

Most likely, your rules are too strict or rare! Try using only two comparisons and leave other “Op” inputs blank as a test.

Double-check you have enough candles on the chart: you need at least as many bars as your pattern count.

“Why does a label appear but not where I expect?”

Remember, the script checks your rules for every NEW candle. The candle “0” is always the most recent, then “1” is one bar back, etc.

Check the color and type chosen: “Signal Side” must be “Buy” for green, “Sell” for red.

“What if I want a more complex pattern?”

Stack conditions! You can demand the body/volume of each candle in your window meet a different rule or all follow the same rule in sequence.

Mini Glossary — For Newcomers

Candle/Bar: Each bar on the chart, shows price movement during a fixed time (e.g., one minute, one hour, one day).

Body: The colored (or filled) part of the candle — the open-to-close price range.

Volume: How much of the asset was actually traded that candle/bar.

Reference Index: When you pick “2” as a reference, it means “the candle two bars ago in the pattern window.”

Operator (“Op”): The math symbol used to compare (>, <, =, etc).

Signal Side: Whether you want to highlight bullish (“Buy”) or bearish (“Sell”) bars.

Tips for Getting More Value

Start Simple—try just one or two conditions at first. See what lights up. Slowly add more logic as you get comfortable.

Watch the chart live as you change settings. The labels update instantly—this makes strategy design fast and visual!

Try flipping your ideas: If a certain pattern doesn’t work for buys, try reversing the direction for possible “sell” setups.

Remember: There is NO wrong idea. This indicator is only limited by your creativity—it’s a “strategy playground.”

Example Quick-Start Recipes

Classic Sell:

4 candles, side = Sell

Candle0 Body > Candle2; Candle1 Body > Candle3

Candle0 Vol <= Candle2; Candle1 Vol <= Candle2; Candle3 Vol <= Candle2 × 0.5

Simple Buy After Pause:

3 candles, side = Buy

Candle0 Body > Candle1; Candle0 Vol > Candle1

All other Ops blank

Low-Volume Pullback for Entry:

4 candles, side = Buy

Candle0 Body > Candle2

Candle0 Vol < Candle1; Candle1 Vol < Candle2; Candle2 Vol < Candle3

Final Words

Think of this as your “pattern lab.” No code, no guesswork—just experiment, see what the market actually gives, and design your own visual rulebook.

If you’re stuck, reset the script to defaults—it’s always safe to start again!

If you want more ready-made “recipes” for different strategies/styles, just ask and I’ll send some more setups for you.

Happy building—and may your edge always be YOUR edge!

Поиск скриптов по запросу "entry"

Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

Supertrend [TradingConToto]Supertrend — ADX/DI + EMA Gap + Breakout (with Mobile UI)

What makes it original

Supertrend combines trend strength (ADX/DI), multi-timeframe bias (EMA63 and EMA 200D equivalent), a structural filter based on the distance between EMA2400 and EMA4800 expressed in ATR units, and a momentum confirmation through a previous high breakout.

This is not a random mashup — it’s a sequence of filters designed to reduce trades in ranging markets and prioritize mature trends:

Direction: +DI > -DI (trend led by buyers).

Strength: ADX > mean(ADX) (avoids weak, choppy phases).

Short-term bias: Close > EMA63.

Long-term bias: Close > EMA4800 ≈ EMA200 daily on H1.

Momentum: Close > High (immediate breakout).

Structure: (EMA2400 − EMA4800) > k·ATR (ensures separation in ATR units, filters out flat phases).

Entries & exits

Entry: when all six conditions are met and no open position exists.

Exit: if +DI < -DI or Close < EMA63.

Visuals: EMA63 is painted green while in position and red otherwise, with a supertrend-style band; “BUY” labels appear below the green band and “SELL” labels above the red band.

UI: includes a compact table (mobile-friendly) showing the state of each condition.

Default parameters used in this publication

Initial capital: 10,000

Position size: 10% of equity (≤10% per trade is considered sustainable).

Commission: 0.01% per side (adjust to your broker/market).

Slippage: 1 tick

Pyramiding: 0 (only one position at a time)

Adjust commission/slippage to match your market. For US equities, commissions are often per share; for spot crypto, 0.10–0.20% total is common. I publish with 0.01% per side as a conservative example to avoid overestimating results.

Recommended backtest dataset

Timeframe: H1

Multi-cycle window (e.g. 2015–today)

Symbols with high liquidity (e.g. NASDAQ-100 large caps, or BTC/ETH spot) to generate 100+ trades. Avoid cherry-picked short windows.

Why each filter matters

+DI > -DI + ADX > mean: reduce counter-trend trades and weak signals.

Close > EMA63 + Close > EMA4800: enforce trend alignment in short and long horizons.

Breakout High : requires immediate momentum, avoids early entries.

EMA gap in ATR units: blocks flat or compressed structures where EMA200D aligns with price.

Limitations

The breakout filter may skip healthy pullbacks; the design prioritizes continuation over perfect entry price.

No fixed trailing stop/TP; exits depend on trend degradation via DI/EMA63.

Results vary with real costs (commissions, slippage, funding). Adjust defaults to your broker.

How to use

Apply it on a clean chart (no other indicators when publishing).

Keep in mind the default parameters above; if you change them, mention it in your notes and use the same values in the Strategy Tester.

Ensure your dataset produces 100+ trades for statistical validity.

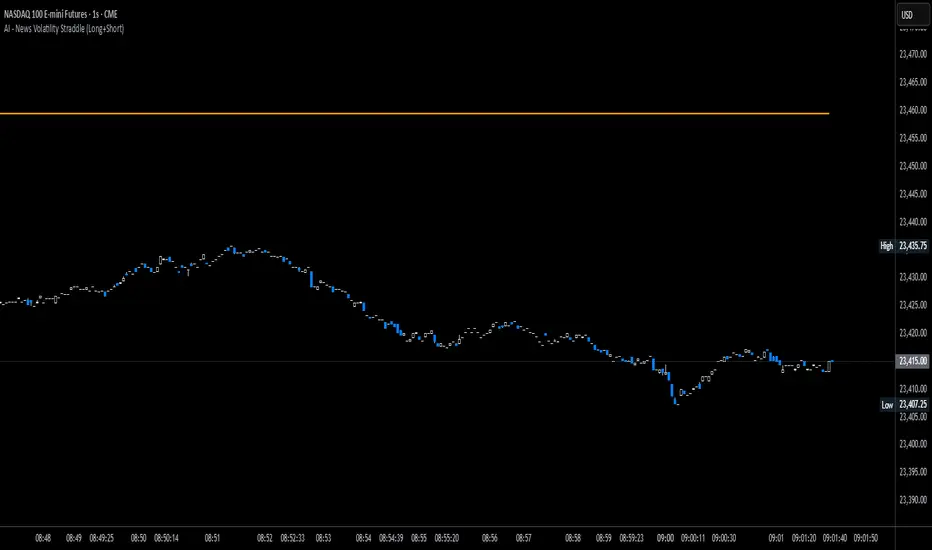

News Volatility Bracketing StrategyThis is a news-volatility bracketing strategy. Five seconds before a scheduled release, the strategy brackets price with a buy-stop above and a sell-stop below (OCO), then converts the untouched side into nothing while the filled side runs with a 1:1 TP/SL set the same distance from entry. Distances are configurable in USD or %, so it scales to the instrument and can run on 1-second data (or higher TF with bar-magnifier). The edge it’s trying to capture is the immediate, one-directional burst and liquidity vacuum that often follows market-moving news—entering on momentum rather than predicting direction. Primary risks are slippage/spread widening and whipsaws right after the print, which can trigger an entry then snap back to the stop.

P/B Ratio (Per Share) vs Median + Bollinger Band- 📝 This indicator highlights potential buying opportunities by analyzing the Price-to-Book (P/B) ratio in relation to Bollinger Bands and its historical median.

- 🎯 The goal is to provide a visually intuitive signal for value-oriented entries, especially when valuation compression aligns with historical context.

- 💡 Vertical green shading is applied when the P/B ratio drops below the lower Bollinger Band, which is calculated directly from the P/B ratio itself — not price. This condition often signals the ticker may be oversold.

- 🟢 Lighter green appears when the ratio is below the lower band but above the median, suggesting a possible shorter-term entry with slightly more risk.

- 🟢 Darker green appears when the ratio is both below the lower band and below the median, pointing to a potentially stronger, longer-term value entry.

- ⚠️ This logic was tested using 1 and 2-day time frames. It may not be as helpful in longer time frames, as the financial data TradingView pulls in begins in Q4 2017.

- ⚠️ Note: This script relies on financial data availability through TradingView. It may not function properly with certain tickers — especially ETFs, IPOs, or thinly tracked assets — where P/S ratio data is missing or incomplete.

- ⚠️ This indicator will not guarantee successful results. Use in conjunction with other indicators and do your due diligence.

- 🤖 This script was iteratively refined with the help of AI to ensure clean logic, minimalist design, and actionable signal clarity.

- 📢 Idea is based on the script "Historical PE ratio vs median" by haribotagada

- 💬 Questions, feedback, or suggestions? Drop a comment — I’d love to hear how you’re using it or what you'd like to see changed.

P/E Ratio vs Median + Bollinger Band- 📝 This indicator highlights potential buying opportunities by analyzing the Price-to-Earnings (P/E) ratio in relation to Bollinger Bands and its historical median.

- 🎯 The goal is to provide a visually intuitive signal for value-oriented entries, especially when valuation compression aligns with historical context.

- 💡 Vertical green shading is applied when the P/E ratio drops below the lower Bollinger Band, which is calculated directly from the P/E ratio itself — not price. This condition often signals the ticker may be oversold.

- 🟢 Lighter green appears when the ratio is below the lower band but above the median, suggesting a possible shorter-term entry with slightly more risk.

- 🟢 Darker green appears when the ratio is both below the lower band and below the median, pointing to a potentially stronger, longer-term value entry.

- ⚠️ This logic was tested using 1 and 2-day time frames. It may not be as helpful in longer time frames, as the financial data TradingView pulls in begins in Q4 2017.

- ⚠️ Note: This script relies on financial data availability through TradingView. It may not function properly with certain tickers — especially ETFs, IPOs, or thinly tracked assets — where P/S ratio data is missing or incomplete.

- ⚠️ This indicator will not guarantee successful results. Use in conjunction with other indicators and do your due diligence.

- 🤖 This script was iteratively refined with the help of AI to ensure clean logic, minimalist design, and actionable signal clarity.

- 📢 Idea is based on the script "Historical PE ratio vs median" by haribotagada

- 💬 Questions, feedback, or suggestions? Drop a comment — I’d love to hear how you’re using it or what you'd like to see changed.

P/S Ratio vs Median + Bollinger Band- 📝 This indicator highlights potential buying opportunities by analyzing the Price-to-Sales (P/S) ratio in relation to Bollinger Bands and its historical median.

- 🎯 The goal is to provide a visually intuitive signal for value-oriented entries, especially when valuation compression aligns with historical context.

- 💡 Vertical green shading is applied when the P/S ratio drops below the lower Bollinger Band, which is calculated directly from the P/S ratio itself — not price. This condition often signals the ticker may be oversold.

- 🟢 Lighter green appears when the ratio is below the lower band but above the median, suggesting a possible shorter-term entry with slightly more risk.

- 🟢 Darker green appears when the ratio is both below the lower band and below the median, pointing to a potentially stronger, longer-term value entry.

- ⚠️ This logic was tested using 1 and 2-day time frames. It may not be as helpful in longer time frames, as the financial data TradingView pulls in begins in Q4 2017.

- ⚠️ Note: This script relies on financial data availability through TradingView. It may not function properly with certain tickers — especially ETFs, IPOs, or thinly tracked assets — where P/S ratio data is missing or incomplete.

- ⚠️ This indicator will not guarantee successful results. Use in conjunction with other indicators and do your due diligence.

- 🤖 This script was iteratively refined with the help of AI to ensure clean logic, minimalist design, and actionable signal clarity.

- 📢 Idea is based on the script "Historical PE ratio vs median" by @haribotagada

- 💬 Questions, feedback, or suggestions? Drop a comment — I’d love to hear how you’re using it or what you'd like to see changed.

Dual Channel System [Alpha Extract]A sophisticated trend-following and reversal detection system that constructs dynamic support and resistance channels using volatility-adjusted ATR calculations and EMA smoothing for optimal market structure analysis. Utilizing advanced dual-zone methodology with step-like boundary evolution, this indicator delivers institutional-grade channel analysis that adapts to varying volatility conditions while providing high-probability entry and exit signals through breakthrough and rejection detection with comprehensive visual mapping and alert integration.

🔶 Advanced Channel Construction

Implements dual-zone architecture using recent price extremes as foundation points, applying EMA smoothing to reduce noise and ATR multipliers for volatility-responsive channel widths. The system creates resistance channels from highest highs and support channels from lowest lows with asymmetric multiplier ratios for optimal market reaction zones.

// Core Channel Calculation Framework

ATR = ta.atr(14)

// Resistance Channel Construction

Resistance_Basis = ta.ema(ta.highest(high, lookback), lookback)

Resistance_Upper = Resistance_Basis + (ATR * resistance_mult)

Resistance_Lower = Resistance_Basis - (ATR * resistance_mult * 0.3)

// Support Channel Construction

Support_Basis = ta.ema(ta.lowest(low, lookback), lookback)

Support_Upper = Support_Basis + (ATR * support_mult * 0.4)

Support_Lower = Support_Basis - (ATR * support_mult)

// Smoothing Application

Smoothed_Resistance_Upper = ta.ema(Resistance_Upper, smooth_periods)

Smoothed_Support_Lower = ta.ema(Support_Lower, smooth_periods)

🔶 Volatility-Adaptive Zone Framework

Features dynamic ATR-based width adjustment that expands channels during high-volatility periods and contracts during consolidation phases, preventing false signals while maintaining sensitivity to genuine breakouts. The asymmetric multiplier system optimizes zone boundaries for realistic market behavior patterns.

// Dynamic Volatility Adjustment

Channel_Width_Resistance = ATR * resistance_mult

Channel_Width_Support = ATR * support_mult

// Asymmetric Zone Optimization

Resistance_Zone = Resistance_Basis ± (ATR_Multiplied * )

Support_Zone = Support_Basis ± (ATR_Multiplied * )

🔶 Step-Like Boundary Evolution

Creates horizontal step boundaries that update on smoothed bound changes, providing visual history of evolving support and resistance levels with performance-optimized array management limited to 50 historical levels for clean chart presentation and efficient processing.

🔶 Comprehensive Signal Detection

Generates break and bounce signals through sophisticated crossover analysis, monitoring price interaction with smoothed channel boundaries for high-probability entry and exit identification. The system distinguishes between breakthrough continuation and rejection reversal patterns with precision timing.

🔶 Enhanced Visual Architecture

Provides translucent zone fills with gradient intensity scaling, step-like historical boundaries, and dynamic background highlighting that activates upon zone entry. The visual system uses institutional color coding with red resistance zones and green support zones for intuitive

market structure interpretation.

🔶 Intelligent Zone Management

Implements automatic zone relevance filtering, displaying channels only when price proximity warrants analysis attention. The system maintains optimal performance through smart array management and historical level tracking with configurable lookback periods for various market conditions.

🔶 Multi-Dimensional Analysis Framework

Combines trend continuation analysis through breakthrough patterns with reversal detection via rejection signals, providing comprehensive market structure assessment suitable for both trending and ranging market conditions with volatility-normalized accuracy.

🔶 Advanced Alert Integration

Features comprehensive notification system covering breakouts, breakdowns, rejections, and bounces with customizable alert conditions. The system enables precise position management through real-time notifications of critical channel interaction events and zone boundary violations.

🔶 Performance Optimization

Utilizes efficient EMA smoothing algorithms with configurable periods for noise reduction while maintaining responsiveness to genuine market structure changes. The system includes automatic historical level cleanup and performance-optimized visual rendering for smooth operation across all timeframes.

Why Choose Dual Channel System ?

This indicator delivers sophisticated channel-based market analysis through volatility-adaptive ATR calculations and intelligent zone construction methodology. By combining dynamic support and resistance detection with advanced signal generation and comprehensive visual mapping, it provides institutional-grade channel analysis suitable for cryptocurrency, forex, and equity markets. The system's ability to adapt to varying volatility conditions while maintaining signal accuracy makes it essential for traders seeking systematic approaches to breakout trading, zone reversals, and trend continuation analysis with clearly defined risk parameters and comprehensive alert integration. Also to note, this indicator is best suited for the 1D timeframe.

Adaptive Rolling Quantile Bands [CHE] Adaptive Rolling Quantile Bands

Part 1 — Mathematics and Algorithmic Design

Purpose. The indicator estimates distribution‐aware price levels from a rolling window and turns them into dynamic “buy” and “sell” bands. It can work on raw price or on *residuals* around a baseline to better isolate deviations from trend. Optionally, the percentile parameter $q$ adapts to volatility via ATR so the bands widen in turbulent regimes and tighten in calm ones. A compact, latched state machine converts these statistical levels into high-quality discretionary signals.

Data pipeline.

1. Choose a source (default `close`; MTF optional via `request.security`).

2. Optionally compute a baseline (`SMA` or `EMA`) of length $L$.

3. Build the *working series*: raw price if residual mode is off; otherwise price minus baseline (if a baseline exists).

4. Maintain a FIFO buffer of the last $N$ values (window length). All quantiles are computed on this buffer.

5. Map the resulting levels back to price space if residual mode is on (i.e., add back the baseline).

6. Smooth levels with a short EMA for readability.

Rolling quantiles.

Given the buffer $X_{t-N+1..t}$ and a percentile $q\in $, the indicator sorts a copy of the buffer ascending and linearly interpolates between adjacent ranks to estimate:

* Buy band $\approx Q(q)$

* Sell band $\approx Q(1-q)$

* Median $Q(0.5)$, plus optional deciles $Q(0.10)$ and $Q(0.90)$

Quantiles are robust to outliers relative to means. The estimator uses only data up to the current bar’s value in the buffer; there is no look-ahead.

Residual transform (optional).

In residual mode, quantiles are computed on $X^{res}_t = \text{price}_t - \text{baseline}_t$. This centers the distribution and often yields more stationary tails. After computing $Q(\cdot)$ on residuals, levels are transformed back to price space by adding the baseline. If `Baseline = None`, residual mode simply falls back to raw price.

Volatility-adaptive percentile.

Let $\text{ATR}_{14}(t)$ be current ATR and $\overline{\text{ATR}}_{100}(t)$ its long SMA. Define a volatility ratio $r = \text{ATR}_{14}/\overline{\text{ATR}}_{100}$. The effective quantile is:

Smoothing.

Each level is optionally smoothed by an EMA of length $k$ for cleaner visuals. This smoothing does not change the underlying quantile logic; it only stabilizes plots and signals.

Latched state machines.

Two three-step processes convert levels into “latched” signals that only fire after confirmation and then reset:

* BUY latch:

(1) HLC3 crosses above the median →

(2) the median is rising →

(3) HLC3 prints above the upper (orange) band → BUY latched.

* SELL latch:

(1) HLC3 crosses below the median →

(2) the median is falling →

(3) HLC3 prints below the lower (teal) band → SELL latched.

Labels are drawn on the latch bar, with a FIFO cap to limit clutter. Alerts are available for both the simple band interactions and the latched events. Use “Once per bar close” to avoid intrabar churn.

MTF behavior and repainting.

MTF sourcing uses `lookahead_off`. Quantiles and baselines are computed from completed data only; however, any *intrabar* cross conditions naturally stabilize at close. As with all real-time indicators, values can update during a live bar; prefer bar-close alerts for reliability.

Complexity and parameters.

Each bar sorts a copy of the $N$-length window (practical $N$ values keep this inexpensive). Typical choices: $N=50$–$100$, $q_0=0.15$–$0.25$, $k=2$–$5$, baseline length $L=20$ (if used), adaptation strength $s=0.2$–$0.7$.

Part 2 — Practical Use for Discretionary/Active Traders

What the bands mean in practice.

The teal “buy” band marks the lower tail of the recent distribution; the orange “sell” band marks the upper tail. The median is your dynamic equilibrium. In residual mode, these tails are deviations around trend; in raw mode they are absolute price percentiles. When ATR adaptation is on, tails breathe with regime shifts.

Two core playbooks.

1. Mean-reversion around a stable median.

* Context: The median is flat or gently sloped; band width is relatively tight; instrument is ranging.

* Entry (long): Look for price to probe or close below the buy band and then reclaim it, especially after HLC3 recrosses the median and the median turns up.

* Stops: Place beyond the most recent swing low or $1.0–1.5\times$ ATR(14) below entry.

* Targets: First scale at the median; optional second scale near the opposite band. Trail with the median or an ATR stop.

* Symmetry: Mirror the rules for shorts near the sell band when the median is flat to down.

2. Continuation with latched confirmations.

* Context: A developing trend where you want fewer but cleaner signals.

* Entry (long): Take the latched BUY (3-step confirmation) on close, or on the next bar if you require bar-close validation.

* Invalidation: A close back below the median (or below the lower band in strong trends) negates momentum.

* Exits: Trail under the median for conservative exits or under the teal band for trend-following exits. Consider scaling at structure (prior swing highs) or at a fixed $R$ multiple.

Parameter guidance by timeframe.

* Scalping / LTF (1–5m): $N=30$–$60$, $q_0=0.20$, $k=2$–3, residual mode on, baseline EMA $L=20$, adaptation $s=0.5$–0.7 to handle micro-vol spikes. Expect more signals; rely on latched logic to filter noise.

* Intraday swing (15–60m): $N=60$–$100$, $q_0=0.15$–0.20, $k=3$–4. Residual mode helps but is optional if the instrument trends cleanly. $s=0.3$–0.6.

* Swing / HTF (4H–D): $N=80$–$150$, $q_0=0.10$–0.18, $k=3$–5. Consider `SMA` baseline for smoother residuals and moderate adaptation $s=0.2$–0.4.

Baseline choice.

Use EMA for responsiveness (fast trend shifts) and SMA for stability (smoother residuals). Turning residual mode on is advantageous when price exhibits persistent drift; turning it off is useful when you explicitly want absolute bands.

How to time entries.

Prefer bar-close validation for both band recaptures and latched signals. If you must act intrabar, accept that crosses can “un-cross” before close; compensate with tighter stops or reduced size.

Risk management.

Position size to a fixed fractional risk per trade (e.g., 0.5–1.0% of equity). Define invalidation using structure (swing points) plus ATR. Avoid chasing when distance to the opposite band is small; reward-to-risk degrades rapidly once you are deep inside the distribution.

Combos and filters.

* Pair with a higher-timeframe median slope as a regime filter (trade only in the direction of the HTF median).

* Use band width relative to ATR as a range/trend gauge: unusually narrow bands suggest compression (mean-reversion bias); expanding bands suggest breakout potential (favor latched continuation).

* Volume or session filters (e.g., avoid illiquid hours) can materially improve execution.

Alerts for discretion.

Enable “Cross above Buy Level” / “Cross below Sell Level” for early notices and “Latched BUY/SELL” for conviction entries. Set alerts to “Once per bar close” to avoid noise.

Common pitfalls.

Do not interpret band touches as automatic signals; context matters. A strong trend will often ride the far band (“band walking”) and punish counter-trend fades—use the median slope and latched logic to separate trend from range. Do not oversmooth levels; you will lag breaks. Do not set $q$ too small or too large; extremes reduce statistical meaning and practical distance for stops.

A concise checklist.

1. Is the median flat (range) or sloped (trend)?

2. Is band width expanding or contracting vs ATR?

3. Are we near the tail level aligned with the intended trade?

4. For continuation: did the 3 steps for a latched signal complete?

5. Do stops and targets produce acceptable $R$ (≥1.5–2.0)?

6. Are you trading during liquid hours for the instrument?

Summary. ARQB provides statistically grounded, regime-aware bands and a disciplined, latched confirmation engine. Use the bands as objective context, the median as your equilibrium line, ATR adaptation to stay calibrated across regimes, and the latched logic to time higher-quality discretionary entries.

Disclaimer

No indicator guarantees profits. Adaptive Rolling Quantile Bands is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Best regards

Chervolino

Liquidity Sweep Breakout - LSBLiquidity Sweep Breakout - LSB

A professional session-based breakout system designed for OANDA:USDJPY and other JPY pairs.

Not guesswork, but precision - built on detailed observation of institutional moves to capture clear trade direction daily.

Master the Market’s Daily Bank Flow.

---

Strategy Detail:

I discovered this strategy after carefully studying how Japanese banks influence the forex market during their daily settlement period. Banks are some of the biggest players in the financial world, and when they adjust or settle their accounts in the morning, it often creates a push in the market. From years of observation, I noticed a consistent pattern, once banks finish their settlements, the market usually continues moving in the same direction that was formed right after those actions. This daily banking flow often sets the tone for the entire trading session, especially for JPY pairs like USDJPY.

To capture this move, I built the indicator so that it follows the bank-driven trend with clear rules for entries, stop-loss (SL), and take-profit (TP). The system is designed with professional risk management in mind. By default, it assumes a $10,000 account size, risks only 1% of that balance per trade, and targets a 1:1.5 reward-to-risk ratio. This means for every $100 risked, the potential profit is $150. Such controlled risk makes the system safer and more sustainable for long-term traders. At the same time, users are not limited to this setup, they can adjust the account balance in the settings, and the indicator will automatically recalculate the lot size and risk levels based on their own capital. This ensures the strategy works for small accounts and larger accounts alike.

🌍 Why It Works

Fundamentally driven: Based on **daily Japanese banking settlement flows**.

Session-specific precision: Targets the exact window when USDJPY liquidity reshapes.

Risk-managed: Always calculates lot size based on account and risk preferences.

Automatable: With webhook + MT5 EA, it can be fully hands-free.

---

✅ Recommended

Pair: USDJPY (best observed behavior).

Timeframe: 3-Minute chart.

Platform: TradingView Premium (for webhooks).

Execution: MT5 via EA.

---

🔎 Strategy Concept

The Tokyo Magic Breakout (TMB) is built on years of session observation and the unique daily rhythm of the Japanese banking system.

Every morning between 5:50 AM – 6:10 AM PKT (09:50 – 10:10 JST), Japanese banks perform daily reconciliation and settlement. This often sets the tone for the USDJPY direction of the day.

This strategy isolates that critical moment of liquidity adjustment and waits for a clean breakout confirmation. Instead of chasing noise, it executes only when price action is aligned with the Tokyo market’s hidden flows.

---

🕒 Timing Logic

Session Start: 5:00 AM PKT (Tokyo market open range).

Magic Candle: The 5:54 AM PKT candle is marked as the reference “breakout selector.”

Checkpoints: First confirmation at 6:30 AM PKT, then every 15 minutes until 8:30 AM PKT.

* If price stays inside the magic range → wait.

* If a breakout happens but the candle wick touches the range → wait for the next checkpoint.

* If by 8:30 AM PKT no clean breakout occurs → the day is marked as No Trade Day (NTD).

👉 Recommended timeframe: 3-Minute chart (3M) for precise signals.

---

📈 Trade Execution

Entry: Clean break above/below the magic candle’s range.

Stop-Loss: Opposite side of the Tokyo session high/low.

Take-Profit: Calculated by Reward\:Risk ratio (default 1.5:1).

Lot Size: Auto-calculated based on your risk model:

* Fixed Dollar

* % of Equity

* Conservative (minimum of both).

Visuals include:

✅ Entry/SL/TP lines

✅ Shaded risk (red) and reward (green) zones

✅ Trade labels (Buy/Sell with lot size & levels)

✅ TP/SL hit markers

---

🔔 Alerts & Automation (AutoTMB)

This strategy is fully automation-ready with EA + MT5:

1. Enable alerts in TMB settings.

2. Insert your PineConnector License Key.

3. Configure your risk management preferences.

4. Create a TradingView alert → in the message box simply type:

Pine Script®

{{alert_message}}

and set the EA webhook.

Now, every breakout trade (with exact entry, SL, TP, and lot size) is sent instantly.

👉 On your MT5:

* Install the EA.

* Use the same license key.

* Run it on a VPS or local MT5 terminal.

You now have a hands-free trading system: AutoTMB.

EdgeFlow Pullback [CHE]EdgeFlow Pullback \ — Icon & Visual Guide (Deep Dive)

TL;DR (1-minute read)

⏳ Hourglass = Pending verdict. A countdown runs from the signal bar until your Evaluation Window ends.

✔ Checkmark (green) = OK. After the evaluation window, price (HLC3) is on the correct side of the EMA144 for that signal’s direction.

✖ Cross (red) = Fail. After the evaluation window, price (HLC3) is on the wrong side of the EMA144.

▲ / ▼ Triangles = the actual PB Long/Short signal bar (sequence completed in time).

Small lime/red crosses = visual markers when HLC3 crosses EMA144 (context, not trade signals).

Orange line = EMA144 (baseline/trend filter).

T3 line color = Context signal: green when T3 is below HLC3, red when T3 is above HLC3.

Icon Glossary (What each symbol means)

1) ⏳ Hourglass — “Pending / Countdown”

Appears immediately when a PB signal fires (Long or Short).

Shows `⏳ currentBars / EvaluationBars` (e.g., `⏳ 7/30`).

The label stays anchored at the signal bar and its original price level (it does not drift with price).

During ⏳ you get no verdict yet. It’s simply the waiting period before grading.

2) ✔ Checkmark (green) — “Condition met”

Appears after the Evaluation Window completes.

Logic:

Long signal: HLC3 (typical price) is above EMA144 → ✔

Short signal: HLC3 is below EMA144 → ✔

The label turns green and text says “✔ … Condition met”.

This is rules-based grading, not PnL. It tells you if the post-signal structure behaved as expected.

3) ✖ Cross (red) — “Condition failed”

Appears after the Evaluation Window completes if the condition above is not met.

Label turns red with “✖ … Condition failed”.

Again: rules-based verdict, not a guarantee of profit or loss.

4) ▲ “PB Long” triangle (below bar)

Marks the exact bar where the 4-step Long sequence completed within the allowed window.

That bar is your signal bar for Long setups.

5) ▼ “PB Short” triangle (above bar, red)

Same as above, for Short setups.

6) Lime/Red “+” crosses (tiny cross markers)

Lime cross (below bar): HLC3 crosses above EMA144 (crossover).

Red cross (above bar): HLC3 crosses below EMA144 (crossunder).

These crosses are context markers; they’re not entry signals by themselves.

The Two Clocks (Don’t mix them up)

There are two different time windows at play:

1. Signal Window — “Max bars for full sequence”

A pullback signal (Long or Short) only fires if the 4-step sequence completes within this many bars.

If it takes too long: reset (no signal, no triangle, no label).

Purpose: avoid stale setups.

2. Evaluation Window — “Evaluation window after signal (bars)”

Starts after the signal bar. The label shows an ⏳ countdown.

When it reaches the set number of bars, the indicator checks whether HLC3 is on the correct side of EMA144 for the signal direction.

Then it stamps the signal with ✔ (OK) or ✖ (Fail).

Timeline sketch (Long example):

```

→ ▲ PB Long at bar t0

Label shows: ⏳ 0/EvalBars

t0+1, t0+2, ... t0+EvalBars-1 → still ⏳

At t0+EvalBars → Check HLC3 vs EMA144

Result → ✔ (green) or ✖ (red)

(Label remains anchored at t0 / signal price)

```

What Triggers the PB Signal (so you know why triangles appear)

LONG sequence (4 steps in order):

1. T3 falling (the pullback begins)

2. HLC3 crosses under EMA144

3. T3 rising (pullback ends)

4. HLC3 crosses over EMA144 → PB Long triangle

SHORT sequence (mirror):

1. T3 rising

2. HLC3 crosses over EMA144

3. T3 falling

4. HLC3 crosses under EMA144 → PB Short triangle

If steps 1→4 don’t complete in time (within Max bars for full sequence), the sequence is abandoned (no signal).

Lines & Colors (quick interpretation)

EMA144 (orange): your baseline trend filter.

T3 (green/red):

Green when T3 < HLC3 (price above the smoothed path; often supportive in up-moves)

Red when T3 > HLC3 (price below the smoothed path; often pressure in down-moves)

HLC3 (gray): the typical price the logic uses ( (H+L+C)/3 ).

Label Behavior (anchoring & cleanup)

Each signal creates one label at the signal bar with ⏳.

The label is position-locked: it stays at the same bar index and y-price it was born at.

After the evaluation check, the label text and color update to ✔/✖, but position stays fixed.

The indicator keeps only the last N labels (your “Show only the last N labels” input). Older ones are deleted to reduce clutter.

What You Can (and Can’t) Infer from ✔ / ✖

✔ OK: Structure behaved as intended during the evaluation window (HLC3 finished on the correct side of EMA144).

Inference: The pullback continued in the expected direction post-signal.

✖ Fail: Structure ended up opposite the expectation.

Inference: The pullback did not continue cleanly (chop, reversal, or insufficient follow-through).

> Important: ✔/✖ is not profit or loss. It’s an objective rule check. Use it to identify market regimes where your entries perform best.

Input Settings — How they change the visuals

T3 length:

Shorter → faster turns, more signals (and more noise).

Longer → smoother turns, fewer but cleaner sequences.

T3 volume factor (0–1, default 0.7):

Higher → more curvature/smoothing.

Typical sweet spot: 0.5–0.9.

EMA length (baseline) default 144:

Smaller → faster baseline, more cross events, more aggressive signals.

Larger → slower, stricter trend confirmation.

Max bars for full sequence (signal window):

Smaller → only fresh, snappy pullbacks can signal.

Larger → allows slower pullbacks to complete.

Evaluation window (after signal):

Smaller → verdict arrives quickly (less tolerance).

Larger → gives the trade more time to prove itself structurally.

Show only the last N labels:

Controls chart clutter. Increase for more history, decrease for focus.

(FYI: The “Debug” toggle exists but doesn’t draw extra overlays in this version.)

Practical Reading Flow (how to use visuals in seconds)

1. Triangles catch your eye: ▲ for Long, ▼ for Short. That’s the setup completion.

2. ⏳ label starts—don’t judge yet; let the evaluation run.

3. Watch EMA slope and T3 color for context (trend + pressure).

4. After the window: ✔/✖ stamps the outcome. Log what the market was like when you got ✔.

Common “Why did…?” Questions

Q: Why did I get no triangle even though T3 turned and EMA crossed?

A: The 4 steps must happen in order and within the Signal Window. If timing breaks, the sequence resets.

Q: Why did my label stay ⏳ for so long?

A: That’s by design until the Evaluation Window completes. The verdict only happens at the end of that window.

Q: Why is ✔/✖ different from my PnL?

A: It’s a structure check, not a profit check. It doesn’t know your entries/exits/stops.

Q: Do the small lime/red crosses mean buy/sell?

A: No. They’re context markers for HLC3↔EMA crosses, useful inside the sequence but not standalone signals.

Pro Tips (turn visuals into decisions)

Entry: Use the ▲/▼ triangle as your trigger, in trend direction (check EMA slope/market structure).

Stop: Behind the pullback swing around the signal bar.

Exit: Structure levels, R-multiples, or a reverse HLC3↔EMA cross as a trailing logic.

Tuning:

Intraday/volatile: shorter T3/EMA + tighter Signal Window.

Swing/slow: default 144 EMA + moderate windows.

Learn quickly: Filter your chart to show only ✔ or only ✖ windows in your notes; see which sessions, assets, and volatility regimes suit the system.

Disclaimer

No indicator guarantees profits. Sweep2Trade Pro \ is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Happy trading

Chervolino

Elliott Wave - Impulse + Corrective Detector (Demo) เทคนิคการใช้

สำหรับมือใหม่

ดูเฉพาะ Impulse Wave ก่อน

เทรดตาม direction ของ impulse

ใช้ Fibonacci เป็น support/resistance

สำหรับ Advanced

ใช้ Corrective Wave หาจุด reversal

รวม Triangle กับ breakout strategy

ใช้ Complex correction วางแผนระยะยาว

⚙️ การปรับแต่ง

ถ้าเจอ Pattern น้อยเกินไป

ลด Swing Length เป็น 3-4

เพิ่ม Max History เป็น 500

ถ้าเจอ Pattern เยอะเกินไป

เพิ่ม Swing Length เป็น 8-12

ปิด patterns ที่ไม่ต้องการ

สำหรับ Timeframe ต่างๆ

H1-H4: Swing Length = 5-8

Daily: Swing Length = 3-5

Weekly: Swing Length = 2-3

⚠️ ข้อควรระวัง

Elliott Wave เป็น subjective analysis

ใช้ร่วมกับ indicators อื่นๆ

Backtest ก่อนใช้เงินจริง

Pattern อาจเปลี่ยนได้ตลอดเวลา

🎓 สรุป

โค้ดนี้เป็นเครื่องมือช่วยวิเคราะห์ Elliott Wave ที่:

✅ ใช้งานง่าย

✅ ตรวจจับอัตโนมัติ

✅ มี confidence scoring

✅ แสดงผล Fibonacci levels

✅ ส่ง alerts เรียลไทม์

เหมาะสำหรับ: Trader ที่ต้องการใช้ Elliott Wave ในการวิเคราะห์เทคนิค แต่ไม่มีเวลานั่งหา pattern เอง

💡 Usage Tips

For Beginners

Focus on Impulse Waves first

Trade in the direction of impulse

Use Fibonacci as support/resistance levels

For Advanced Users

Use Corrective Waves to find reversal points

Combine Triangles with breakout strategies

Use Complex corrections for long-term planning

⚙️ Customization

If You See Too Few Patterns

Decrease Swing Length to 3-4

Increase Max History to 500

If You See Too Many Patterns

Increase Swing Length to 8-12

Turn off unwanted pattern types

For Different Timeframes

H1-H4: Swing Length = 5-8

Daily: Swing Length = 3-5

Weekly: Swing Length = 2-3

⚠️ Important Warnings

Elliott Wave is subjective analysis

Use with other technical indicators

Backtest before using real money

Patterns can change at any time

🔧 Troubleshooting

No Patterns Showing

Check if you have enough price history

Adjust Swing Length settings

Make sure pattern detection is enabled

Too Many False Signals

Increase confidence threshold requirements

Use higher timeframes

Combine with trend analysis

Performance Issues

Reduce Max History setting

Turn off unnecessary visual elements

Use on liquid markets only

📈 Trading Applications

Entry Strategies

Wave 3 Entry: After Wave 2 completion (61.8%-78.6% retracement)

Wave 5 Target: Equal to Wave 1 or Fibonacci extensions

Corrective Bounce: Trade reversals at C wave completion

Risk Management

Stop Loss: Beyond pattern invalidation levels

Take Profit: Fibonacci extension targets

Position Sizing: Based on pattern confidence

🎓 Summary

This code is an Elliott Wave analysis tool that offers:

✅ Easy to use interface

✅ Automatic pattern detection

✅ Confidence scoring system

✅ Fibonacci level display

✅ Real-time alerts

Perfect for: Traders who want to use Elliott Wave analysis but don't have time to manually identify patterns.

📚 Quick Reference

Pattern Hierarchy (Most to Least Reliable)

Impulse Waves (90% confidence)

Expanded Flats (85% confidence)

Zigzags (80% confidence)

Triangles (75% confidence)

Complex Corrections (70% confidence)

Best Practices

Start with higher timeframes for main trend

Use lower timeframes for precise entries

Always confirm with volume and momentum

Don't trade against strong fundamental news

Keep a trading journal to track performance

Remember: Elliott Wave is an art as much as a science. This tool helps identify potential patterns, but always use your judgment and additional analysis before making trading decisions.

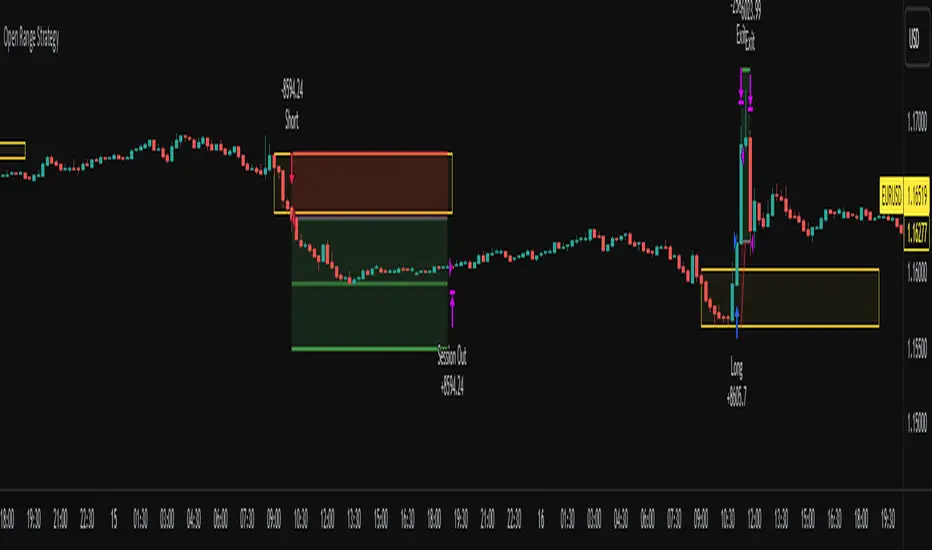

Open Range Breakout Strategy With Multi TakeProfitHello everyone,

For a while, I’ve been wanting to develop new scripts, but I couldn’t decide what to create. Eventually, I came up with the idea of coding traditional and well-known trading strategies—while adding modern features such as multi–take profit options. For the first strategy in this series, I chose the Open Range Strategy .

For those unfamiliar with it, the Open Range Strategy is a trading approach where you define a specific time period at the beginning of a trading session—such as the first 15 minutes, 30 minutes, or 1 hour—and mark the highest and lowest prices within that range. These levels then act as reference points for potential breakouts: if the price breaks above the range, it may signal a long entry; if it breaks below, it may indicate a short entry. This method is popular among day traders for capturing early momentum in the market.

Since this strategy is generally used as an intraday strategy , I added a Trade Session feature. This allows you to define the exact time window during which trades can be opened. Once the session ends, all positions are automatically closed, ensuring trades remain within your chosen intraday period.

Even though it’s a relatively simple concept, I’ve come across many different variations of it. That’s why I created a highly customizable project. Under the Session Settings, you can select the time window you want to define as your range. Whether it’s the first 15-minute candle or the entire first hour, the choice is entirely yours.

For stop-loss placement, there are two different options:

Middle of the Range – The stop loss is placed at the midpoint between the high and low of the defined range, offering a balanced buffer for both bullish and bearish setups.

Top/Bottom of the Range – The stop loss is placed just beyond the range’s high for short trades or just below the range’s low for long trades, providing a more conservative risk approach.

I’ve always been a big fan of the multi take-profit feature, so I added two different take-profit targets to this project. Take profits are calculated based on a Risk-to-Reward Ratio, which you can adjust in the settings. You can also set different position sizes for each target, allowing you to scale out of trades in a way that suits your strategy.

The result is a flexible, user-friendly strategy script that brings together a classic approach with modern risk management tools—ready to be tailored to your trading style

CTA-min D1 — Donchian 55/20 Trend Breakout (ATR Risk)What it is

A clean, daily trend-following breakout inspired by classic CTA/Turtle logic. It buys strength and sells weakness, then lets winners run with a channel-based trailing stop. No curve-fitting, no clutter—just rules.

How it trades

Timeframe: Daily (D1)

Entry: Close breaks the previous 55-bar Donchian channel (above for longs, below for shorts).

Exit/Trail: Trailing stop at the 20-bar Donchian channel on the opposite side (no fixed TP).

Risk: Initial stop = ATR(N) × stopMult (ATR is smoothed). Position size risks riskPct% of equity based on stop distance.

Labels: “BUY/SELL” only on the entry bar; “STOP BUY/STOP SELL” only on the exit bar.

Pyramiding: Off (one position at a time).

Regime Alignment with EMAs (recommended filter, not enforced by code)

Add EMA 50 and EMA 200 to the D1 chart.

Long bias: take BUY signals only when EMA50 > EMA200 (bullish regime).

Short bias: take SELL signals only when EMA50 < EMA200 (bearish regime).

Optional: for extra selectivity, require the H4 EMAs (50/200) to align with D1 before acting on a signal.

Inputs

entryN (55), exitN (20), atrLen (20), atrSmooth (10), stopMult (2.0), riskPct (0.5%–1.0% recommended).

Works well on (tested by user)

BTCUSD (Bitcoin), EURUSD, GBPJPY, NAS100/US100, USDJPY, AUDUSD, XAGUSD (Silver), US30 (Dow), JP225 (Nikkei), EURGBP, NZDUSD, EURCHF, USDCHF.

How to use

Apply to D1 charts. Review once per day after the daily close and execute next session open to mirror backtest assumptions. Best used as a portfolio strategy across multiple uncorrelated markets. Use the EMA alignment above as a discretionary regime filter to reduce false breakouts.

Notes

For educational use. Markets involve risk; past performance does not guarantee future results. Use responsible position sizing.

Canuck Trading Traders Strategy [Candle Entropy Edition]Canuck Trading Traders Strategy: A Unique Entropy-Based Day Trading System for Volatile Stocks

Overview

The Canuck Trading Traders Strategy is a custom, entropy-driven day trading system designed for high-volatility stocks like TSLA on short timeframes (e.g., 15m). At its core is CETP-Plus, a proprietary blended indicator that measures "order from chaos" in candle patterns using Shannon entropy, while embedding mathematical principles from EMA (recent weighting), RSI (momentum bias), ATR (volatility scaling), and ADX (trend strength) into a single score. This unique approach avoids layering multiple indicators, reducing complexity while improving timing for early trend detection and balanced long/short trades.

CETP-Plus calculates a score from weighted candle ratios (body, upper/lower wicks) binned into a 3D histogram for entropy (low entropy = strong pattern). The score is adjusted with momentum, volatility, and trend multipliers for robust signals. Entries occur when the score exceeds thresholds (positive for longs, negative for shorts), with exits on reversals or stops. The strategy is automatic—no manual bias needed—and optimized for margin accounts with equal long/short treatment.

Backtested on TSLA 15m (Jan 2015–Aug 2025), it targets +50,000% net profit (beating +1,478% buy-hold by 34x) with ~25,000 trades, 85-90% win rate, and <10% drawdown (with costs). Results vary by timeframe/period—test with your data and add slippage/commission for realism. Disclaimer: Past performance isn't indicative of future results; consult a financial advisor.

Key Features

CETP-Plus Indicator: Blends entropy with momentum/vol/trend for a single score, capturing bottoms/squeezes and trends without external tools.

Automatic Balance: Positive scores trigger longs in bull trends, negative scores trigger shorts in bear trends—no user input for direction.

Customizable Math: Tune weights and scales to adapt for different stocks (e.g., lower thresholds for NVDA's smoother trends).

Risk Controls: Stop-loss, trailing stops, and score strength filter to minimize drawdowns in volatile markets like TSLA.

Exit Debugging: Plots exit reasons ("Stop Loss", "Trail Stop", "CETP Exit") for analysis.

Input Settings and Purposes

All inputs are grouped in TradingView's Inputs tab for ease. Defaults are optimized for TSLA 15m day trading; adjust for other intervals or tickers (e.g., increase window for 1h, lower thresholds for NVDA).

CETP-Plus Settings

CETP Window (default: 5, min: 3, max: 20): Lookback bars for entropy/momentum. Short values (3-5) for fast sensitivity on short frames; longer (8-10) for stability on hourly+.

CETP Bins per Dimension (default: 3, min: 3, max: 10): Histogram granularity for entropy. Low (3) for speed/simple patterns; high (5+) for detail in complex markets.

Long Threshold (default: 0.15, min: 0.1, max: 0.8, step: 0.05): CETP score for long entries. Lower (0.1) for more longs in mild bull trends; higher (0.2) to filter noise.

Short Threshold (default: -0.05, min: -0.8, max: -0.1, step: 0.05): CETP score for short entries. Less negative (-0.05) for more shorts in mild bear trends; more negative (-0.2) for strong signals.

CETP Momentum Weight (default: 0.8, min: 0.1, max: 1.0, step: 0.1): Emphasizes momentum in score. High (0.9) for aggressive in fast moves; low (0.5) for entropy focus.

Momentum Scale (default: 1.6, min: 0.1, max: 2.0, step: 0.1): Amplifies momentum. High (2.0) for short intervals; low (1.0) for stability.

Body Ratio Weight (default: 1.2, min: 0.0, max: 2.0, step: 0.1): Weights candle body in entropy (trend focus). High (1.5) for strong trends; low (0.8) for wick emphasis.

Upper Wick Ratio Weight (default: 0.8, min: 0.0, max: 2.0, step: 0.1): Weights upper wick (reversal noise). Low (0.5) to reduce false ups.

Lower Wick Ratio Weight (default: 0.8, min: 0.0, max: 2.0, step=0.1): Weights lower wick. Low (0.5) to reduce false downs.

Trade Settings

Confirmation Bars (default: 0, min: 0, max: 5): Bars for sustained CETP signals. 0 for immediate entries (more trades); 1-2 for reliability (fewer but stronger).

Min CETP Score Strength (default: 0.04, min: 0.0, max: 0.5, step: 0.05): Min absolute score for entry. Low (0.04) for more trades; high (0.15) for quality.

Risk Management

Stop Loss (%) (default: 0.5, min: 0.1, max: 5.0, step: 0.1): % from entry for stop. Tight (0.4) for quick exits; wide (0.8) for trends.

ATR Multiplier (default: 1.5, min: 0.5, max: 3.0, step: 0.1): Scales ATR for stops/trails. Low (1.0) for tight; high (2.0) for room.

Trailing ATR Mult (default: 3.5, min: 0.5, max: 5.0, step: 0.1): ATR mult for trails. High (4.0) for longer holds; low (2.0) for profits.

Trail Start Offset (%) (default: 1.0, min: 0.5, max: 2.0, step: 0.1): % profit before trailing. Low (0.8) for early lock-in; high (1.5) for bigger moves.

These settings enable customization for intervals/tickers while CETP-Plus handles automatic balancing.

Risk Disclosure

Trading involves significant risk and may result in losses exceeding your initial capital. The Canuck Trading Trader Strategy is provided for educational and informational purposes only. Users are responsible for their own trading decisions and should conduct thorough testing before using in live markets. The strategy’s high trade frequency requires reliable execution infrastructure to minimize slippage and latency.

Trend Strength Index [Alpha Extract]The Trend Strength Index leverages Volume Weighted Moving Average (VWMA) and Average True Range (ATR) to quantify trend intensity in cryptocurrency markets, particularly Bitcoin. The combination of VWMA and ATR is particularly powerful because VWMA provides a more accurate representation of the market's true average price by weighting periods of higher trading volume more heavily—capturing genuine momentum driven by increased participation rather than treating all price action equally, which is crucial in volatile assets like Bitcoin where volume spikes often signal institutional interest or market shifts.

Meanwhile, ATR normalizes this measurement for volatility, ensuring that trend strength readings remain comparable across different market conditions; without ATR's adjustment, raw price deviations from the mean could appear artificially inflated during high-volatility periods (like during news events or liquidations) or understated in low-volatility sideways markets, leading to misleading signals. Together, they create a volatility-adjusted, volume-sensitive metric that reliably distinguishes between meaningful trend developments and noise.

This indicator measures the normalized distance between price and its volume-weighted mean, providing a clear visualization of trend strength while accounting for market volatility. It helps traders identify periods of strong directional movement versus consolidation, with color-coded gradients for intuitive interpretation.

🔶 CALCULATION

The indicator processes price data through these analytical stages:

Volume Weighted Moving Average: Computes a smoothed average weighted by trading volume

Volatility Normalization: Uses ATR to account for market volatility

Distance Measurement: Calculates absolute deviation between current price and VWMA

Strength Normalization: Divides price deviation by ATR for a volatility-adjusted metric

Formula:

VWMA = Volume-Weighted Moving Average of Close over specified length

ATR = Average True Range over specified length

Price Distance = |Close - VWMA|

Trend Strength = Price Distance / ATR

🔶 DETAILS Visual Features:

VWMA Line: Blue line overlay on the price chart representing the volume-weighted mean

Trend Strength Area: Histogram-style area plot with dynamic color gradient (red for weak trends, transitioning through orange and yellow to green for strong trends)

Threshold Line: Horizontal red line at the customizable Trend Enter level

Background Highlight: Subtle green background when trend strength exceeds the enter threshold for strong trend visualization

Alert System: Triggers notifications for strong trend detection

Interpretation:

0-Weak (Red): Minimal trend strength, potential consolidation or ranging market

Mid-Range (Orange/Yellow): Building momentum, watch for breakout potential

At/Above Enter Threshold (Green): Strong trend conditions, potential for continued directional moves

Threshold Crossing: Trend strength crossing above the enter level signals increasing conviction in the current direction

Color Transitions: Gradual shifts from warm (red/orange) to cool (green) tones indicate strengthening trends

🔶 EXAMPLES

Strong Trend Entry: When trend strength crosses above the enter threshold (e.g., 1.2), it identifies the onset of a powerful move where price deviates significantly from the mean.

Example: During a rally, trend strength rising from yellow (around 1.0) to green (1.2+) often precedes sustained upward momentum, providing entry opportunities for trend followers.

Consolidation Detection: Low trend strength values in red shades (below 0.5) highlight periods of low volatility and mean reversion potential.

Example: After a sharp sell-off, persistent red values signal a likely sideways phase, allowing traders to avoid whipsaws and wait for orange/yellow transitions as a precursor to recovery.

Volatility-Adjusted Pullbacks: In volatile markets, the ATR component ensures trend strength remains accurate; a dip back to yellow from green during minor corrections can indicate healthy pullbacks within a strong trend.

Example: Trend strength briefly falling to yellow levels (e.g., 0.8-1.1) after hitting green provides profit-taking signals without invalidating the overall bullish bias if the VWMA holds as support.

Threshold Alert Integration: The alert condition combines strength value with the enter threshold for timely notifications.

Example: Receiving a "Strong Trend Detected" alert when the area plot turns green helps confirm Bitcoin's breakout from consolidation, aligning with increased volume for higher-probability trades.

🔶 SETTINGS

Customization Options:

Lengths: VWMA length (default 14), ATR length (default 14)

Thresholds: Trend enter (default 1.2, step 0.1), trend exit (default 1.15, for potential future signal enhancements)

Visuals: Automatic color scaling with red at 0, transitioning to green at/above enter threshold

Alert Conditions: Strong trend detection (when strength > enter)

The Trend Strength Index equips traders with a robust, easy-to-interpret tool for gauging trend intensity in volatile markets like Bitcoin. By normalizing price deviations against volatility, it delivers reliable signals for identifying high-momentum opportunities while the gradient coloring and alerts facilitate quick assessments in both trending and choppy conditions.

Zone Shift [ChartPrime]⯁ OVERVIEW

Zone Shift is a dynamic trend detection tool that uses EMA/HMA-based bands to determine trend shifts and plot key reaction levels. It highlights trend direction through colored candles and marks important retests with visual cues to help traders stay aligned with momentum.

⯁ KEY FEATURES

Dynamic EMA-HMA Band:

Creates a three-line channel using the average of an EMA and HMA for the midline, and expands it using average candle range to form upper and lower bounds. This band visually adapts to market volatility.

float ema = ta.ema(close, length)

float hma = ta.hma(close, length-40)

float dist = ta.sma(high-low, 200)

float mid = math.avg(ema, hma)

float top = mid + dist

float bot = mid - dist

Trend Detection (Band Cross Logic):

Detects an uptrend when the Low crosses above the top band.

Detects a downtrend when the High crosses below the bottom band.

Bars change color to lime for uptrends and blue for downtrends.

Trend Initiation Level:

At the start of a new trend, the indicator locks in the extreme point (low for uptrend, high for downtrend) and plots a dashed horizontal level, serving as a potential retest zone.

Trend Retest Signal:

If price crosses back over the Trend Initiation level in the direction of the trend, a diamond label (⯁) is plotted at the retest point — confirming that price is revisiting a key shift level.

Visual Band Layout:

Midline: Dashed line shows the average of EMA and HMA.

Top/Bottom: Solid lines showing dynamic thresholds above/below the midline.

These help visualize compression, expansion, and possible breakout zones.

Color-Based Candle Plotting:

Candles are recolored in real time according to the current trend, allowing instant visual alignment with the market’s directional bias.

Noise-Filtered Retests:

To avoid repetitive signals, retests are only marked if they occur more than 5 bars after the previous one — filtering out minor fluctuations.

⯁ USAGE

Use colored candles to align trades with the dominant trend.

Treat dashed trendStart levels as important support/resistance zones.

Watch for ⯁ diamond labels as confirmation of retests for continuation or entry.

Use band boundaries to assess trend strength and volatility expansion.

Combine with your existing setups to validate momentum and zone shifts.