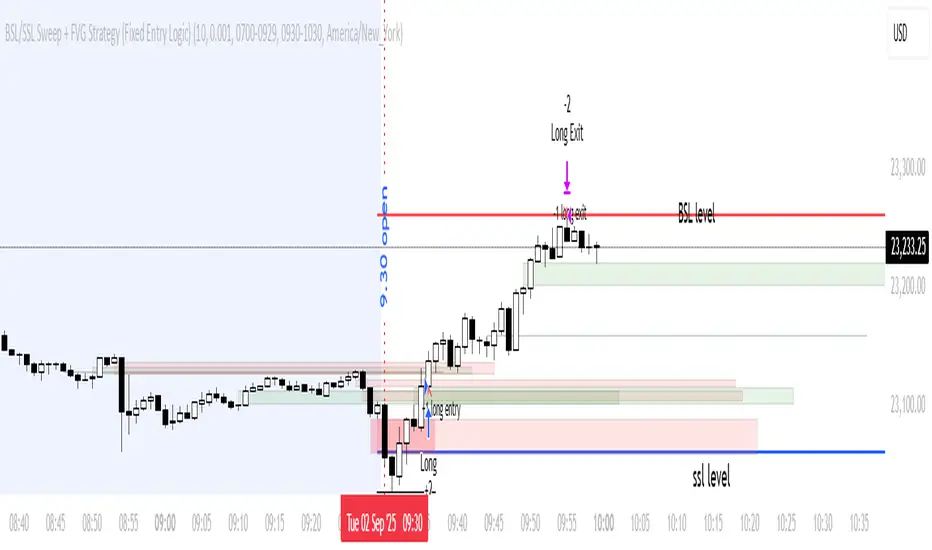

BSL/SSL Sweep + FVG Strategy Jobin (c) The New York ATM Model is a structured intraday strategy designed to capture algorithmic stop-hunts and reversals during the New York session open. It focuses on liquidity sweeps—either Buy-Side or Sell-Side—followed by a confirmation using Fair Value Gaps (FVGs).

Поиск скриптов по запросу "gaps"

FiniteStateMachine🟩 OVERVIEW

A flexible framework for creating, testing and implementing a Finite State Machine (FSM) in your script. FSMs use rules to control how states change in response to events.

This is the first Finite State Machine library on TradingView and it's quite a different way to think about your script's logic. Advantages of using this vs hardcoding all your logic include:

• Explicit logic : You can see all rules easily side-by-side.

• Validation : Tables show your rules and validation results right on the chart.

• Dual approach : Simple matrix for straightforward transitions; map implementation for concurrent scenarios. You can combine them for complex needs.

• Type safety : Shows how to use enums for robustness while maintaining string compatibility.

• Real-world examples : Includes both conceptual (traffic lights) and practical (trading strategy) demonstrations.

• Priority control : Explicit control over which rules take precedence when multiple conditions are met.

• Wildcard system : Flexible pattern matching for states and events.

The library seems complex, but it's not really. Your conditions, events, and their potential interactions are complex. The FSM makes them all explicit, which is some work. However, like all "good" pain in life, this is front-loaded, and *saves* pain later, in the form of unintended interactions and bugs that are very hard to find and fix.

🟩 SIMPLE FSM (MATRIX-BASED)

The simple FSM uses a matrix to define transition rules with the structure: state > event > state. We look up the current state, check if the event in that row matches, and if it does, output the resulting state.

Each row in the matrix defines one rule, and the first matching row, counting from the top down, is applied.

A limitation of this method is that you can supply only ONE event.

You can design layered rules using widlcards. Use an empty string "" or the special string "ANY" for any state or event wildcard.

The matrix FSM is foruse where you have clear, sequential state transitions triggered by single events. Think traffic lights, or any logic where only one thing can happen at a time.

The demo for this FSM is of traffic lights.

🟩 CONCURRENT FSM (MAP-BASED)

The map FSM uses a more complex structure where each state is a key in the map, and its value is an array of event rules. Each rule maps a named condition to an output (event or next state).

This FSM can handle multiple conditions simultaneously. Rules added first have higher priority.

Adding more rules to existing states combines the entries in the map (if you use the supplied helper function) rather than overwriting them.

This FSM is for more complex scenarios where multiple conditions can be true simultaneously, and you need to control which takes precedence. Like trading strategies, or any system with concurrent conditions.

The demo for this FSM is a trading strategy.

🟩 HOW TO USE

Pine Script libraries contain reusable code for importing into indicators. You do not need to copy any code out of here. Just import the library and call the function you want.

For example, for version 1 of this library, import it like this:

import SimpleCryptoLife/FiniteStateMachine/1

See the EXAMPLE USAGE sections within the library for examples of calling the functions.

For more information on libraries and incorporating them into your scripts, see the Libraries section of the Pine Script User Manual.

🟩 TECHNICAL IMPLEMENTATION

Both FSM implementations support wildcards using blank strings "" or the special string "ANY". Wildcards match in this priority order:

• Exact state + exact event match

• Exact state + empty event (event wildcard)

• Empty state + exact event (state wildcard)

• Empty state + empty event (full wildcard)

When multiple rules match the same state + event combination, the FIRST rule encountered takes priority. In the matrix FSM, this means row order determines priority. In the map FSM, it's the order you add rules to each state.

The library uses user-defined types for the map FSM:

• o_eventRule : Maps a condition name to an output

• o_eventRuleWrapper : Wraps an array of rules (since maps can't contain arrays directly)

Everything uses strings for maximum library compatibility, though the examples show how to use enums for type safety by converting them to strings.

Unlike normal maps where adding a duplicate key overwrites the value, this library's `m_addRuleToEventMap()` method *combines* rules, making it intuitive to build rule sets without breaking them.

🟩 VALIDATION & ERROR HANDLING

The library includes comprehensive validation functions that catch common FSM design errors:

Error detection:

• Empty next states

• Invalid states not in the states array

• Duplicate rules

• Conflicting transitions

• Unreachable states (no entry/exit rules)

Warning detection:

• Redundant wildcards

• Empty states/events (potential unintended wildcards)

• Duplicate conditions within states

You can display validation results in tables on the chart, with tooltips providing detailed explanations. The helper functions to display the tables are exported so you can call them from your own script.

🟩 PRACTICAL EXAMPLES

The library includes four comprehensive demos:

Traffic Light Demo (Simple FSM) : Uses the matrix FSM to cycle through traffic light states (red → red+amber → green → amber → red) with timer events. Includes pseudo-random "break" events and repair logic to demonstrate wildcards and priority handling.

Trading Strategy Demo (Concurrent FSM) : Implements a realistic long-only trading strategy using BOTH FSM types:

• Map FSM converts multiple technical conditions (EMA crosses, gaps, fractals, RSI) into prioritised events

• Matrix FSM handles state transitions (idle → setup → entry → position → exit → re-entry)

• Includes position management, stop losses, and re-entry logic

Error Demonstrations : Both FSM types include error demos with intentionally malformed rules to showcase the validation system's capabilities.

🟩 BRING ON THE FUNCTIONS

f_printFSMMatrix(_mat_rules, _a_states, _tablePosition)

Prints a table of states and rules to the specified position on the chart. Works only with the matrix-based FSM.

Parameters:

_mat_rules (matrix)

_a_states (array)

_tablePosition (simple string)

Returns: The table of states and rules.

method m_loadMatrixRulesFromText(_mat_rules, _rulesText)

Loads rules into a rules matrix from a multiline string where each line is of the form "current state | event | next state" (ignores empty lines and trims whitespace).

This is the most human-readable way to define rules because it's a visually aligned, table-like format.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_rulesText (string)

Returns: No explicit return. The matrix is modified as a side-effect.

method m_addRuleToMatrix(_mat_rules, _currentState, _event, _nextState)

Adds a single rule to the rules matrix. This can also be quite readble if you use short variable names and careful spacing.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_currentState (string)

_event (string)

_nextState (string)

Returns: No explicit return. The matrix is modified as a side-effect.

method m_validateRulesMatrix(_mat_rules, _a_states, _showTable, _tablePosition)

Validates a rules matrix and a states array to check that they are well formed. Works only with the matrix-based FSM.

Checks: matrix has exactly 3 columns; no empty next states; all states defined in array; no duplicate states; no duplicate rules; all states have entry/exit rules; no conflicting transitions; no redundant wildcards. To avoid slowing down the script unnecessarily, call this method once (perhaps using `barstate.isfirst`), when the rules and states are ready.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_a_states (array)

_showTable (bool)

_tablePosition (simple string)

Returns: `true` if the rules and states are valid; `false` if errors or warnings exist.

method m_getStateFromMatrix(_mat_rules, _currentState, _event, _strictInput, _strictTransitions)

Returns the next state based on the current state and event, or `na` if no matching transition is found. Empty (not na) entries are treated as wildcards if `strictInput` is false.

Priority: exact match > event wildcard > state wildcard > full wildcard.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_currentState (string)

_event (string)

_strictInput (bool)

_strictTransitions (bool)

Returns: The next state or `na`.

method m_addRuleToEventMap(_map_eventRules, _state, _condName, _output)

Adds a single event rule to the event rules map. If the state key already exists, appends the new rule to the existing array (if different). If the state key doesn't exist, creates a new entry.

Namespace types: map

Parameters:

_map_eventRules (map)

_state (string)

_condName (string)

_output (string)

Returns: No explicit return. The map is modified as a side-effect.

method m_addEventRulesToMapFromText(_map_eventRules, _configText)

Loads event rules from a multiline text string into a map structure.

Format: "state | condName > output | condName > output | ..." . Pairs are ordered by priority. You can have multiple rules on the same line for one state.

Supports wildcards: Use an empty string ("") or the special string "ANY" for state or condName to create wildcard rules.

Examples: " | condName > output" (state wildcard), "state | > output" (condition wildcard), " | > output" (full wildcard).

Splits lines by \n, extracts state as key, creates/appends to array with new o_eventRule(condName, output).

Call once, e.g., on barstate.isfirst for best performance.

Namespace types: map

Parameters:

_map_eventRules (map)

_configText (string)

Returns: No explicit return. The map is modified as a side-effect.

f_printFSMMap(_map_eventRules, _a_states, _tablePosition)

Prints a table of map-based event rules to the specified position on the chart.

Parameters:

_map_eventRules (map)

_a_states (array)

_tablePosition (simple string)

Returns: The table of map-based event rules.

method m_validateEventRulesMap(_map_eventRules, _a_states, _a_validEvents, _showTable, _tablePosition)

Validates an event rules map to check that it's well formed.

Checks: map is not empty; wrappers contain non-empty arrays; no duplicate condition names per state; no empty fields in o_eventRule objects; optionally validates outputs against matrix events.

NOTE: Both "" and "ANY" are treated identically as wildcards for both states and conditions.

To avoid slowing down the script unnecessarily, call this method once (perhaps using `barstate.isfirst`), when the map is ready.

Namespace types: map

Parameters:

_map_eventRules (map)

_a_states (array)

_a_validEvents (array)

_showTable (bool)

_tablePosition (simple string)

Returns: `true` if the event rules map is valid; `false` if errors or warnings exist.

method m_getEventFromConditionsMap(_currentState, _a_activeConditions, _map_eventRules)

Returns a single event or state string based on the current state and active conditions.

Uses a map of event rules where rules are pre-sorted by implicit priority via load order.

Supports wildcards using empty string ("") or "ANY" for flexible rule matching.

Priority: exact match > condition wildcard > state wildcard > full wildcard.

Namespace types: series string, simple string, input string, const string

Parameters:

_currentState (string)

_a_activeConditions (array)

_map_eventRules (map)

Returns: The output string (event or state) for the first matching condition, or na if no match found.

o_eventRule

o_eventRule defines a condition-to-output mapping for the concurrent FSM.

Fields:

condName (series string) : The name of the condition to check.

output (series string) : The output (event or state) when the condition is true.

o_eventRuleWrapper

o_eventRuleWrapper wraps an array of o_eventRule for use as map values (maps cannot contain collections directly).

Fields:

a_rules (array) : Array of o_eventRule objects for a specific state.

NX - ICT PD ArraysThis Pine Script indicator identifies and visualizes Fair Value Gaps (FVGs) and Order Blocks (OBs) based on refined price action logic.

FVGs are highlighted when price leaves an imbalance between candles, while Order Blocks are detected using ICT methodology—marking the last opposing candle before a displacement move.

The script dynamically tracks and updates these zones, halting box extension once price interacts with them. Customizable colors and lookback settings allow traders to tailor the display to their strategy.

Adaptive Gap Bands - DolphinTradeBot1️⃣ Overview

Adaptive Gap Bands is a momentum indicator that measures the percentage difference between fast and slow moving averages. This helps identify potential overbought or oversold zones.

The goal is to analyze “gap” behaviors within a trend and generate clearer entry–exit signals.

Since the bands are anchored to the slow moving average, they are more sensitive to the trend direction, making signals stronger in line with the prevailing trend.

📌 Signals do not repaint — once confirmed, they remain fixed on the chart.

2️⃣ How It Works ?

The indicator tracks the distance between fast and slow MAs.

The indicator measures the percentage gap between the fast and slow moving averages, relative to the slow MA.

Each time the gap reaches a new extreme during a swing, that value is stored.

When the averages cross, the stored values from the last N swings (defined by Swing Count) are collected.

These gap values are then averaged to create a smoother and more adaptive reference.

The bands are built by multiplying this average gap with the % Multiplier and projecting it around the slow MA.

3️⃣ How to Use It ?

Add the script to your chart.

Green label → potential Long signal.

Red label → potential Short signal.

Signals often appear when price moves outside the adaptive bands, showing extreme momentum.

Can also be used as a reference tool in manual trades to set profit/loss expectations.

By comparing upward vs. downward gaps, it can help analyze and confirm the dominant trend direction.

4️⃣⚙️ Settings

Swing Count → Number of past swings considered.

% Multiplier → Adjusts band width (narrower or wider).

MA Lengths & Types → Choose fast and slow moving averages (EMA, SMA, RMA, etc.).

TPO Levels [VAH/POC/VAL] with Poor H/L, Single Prints & NPOCs### 🎯 Advanced Market Profile & Key Level Analysis

This script is a unique and comprehensive technical analysis tool designed to help traders understand market structure, value, and key liquidity levels using the principles of **Auction Market Theory** and **Market Profile**.

This script is unique (and shouldn't be censored) because :

It allows large history of levels to be displayed

Accurate as possible tick size

Doesn't draw a profile but only the actual levels

Supports multi-timeframe levels even on the daily mode giving macro context

There is no indicator out there that does it

While these concepts are universal, this indicator was built primarily for the dynamic, 24/7 nature of the **cryptocurrency market**. It helps you move beyond simple price action to understand *why* the market is moving, which is especially crucial in the volatile crypto space.

### ## 📊 The Concepts Behind the Calculations

To use this script effectively, it's important to understand the core concepts it is built upon. The entire script is self-contained and does not require other indicators.

* **What is Market Profile?**

Market Profile is a unique charting technique that organizes price and time data to reveal market structure. It's built from **Time Price Opportunities (TPOs)**, which are 30-minute periods of market activity. By stacking these TPOs, the script builds a distribution, showing which price levels were most accepted (heavily traded) and which were rejected (lightly traded) during a session.

* **What is the Value Area (VA)?**

The Value Area is the heart of the profile. It represents the price range where **70%** of the session's trading volume occurred. This is considered the "fair value" zone where both buyers and sellers were in general agreement.

* **Point of Control (POC):** The single price level with the most TPOs. This was the most accepted or "fairest" price of the session and acts as a gravitational line for price.

* **Value Area High (VAH):** The upper boundary of the 70% value zone.

* **Value Area Low (VAL):** The lower boundary of the 70% value zone.

VAH and VAL are dynamic support and resistance levels. Trading outside the previous session's value area can signal the start of a new trend.

***

### ## 📈 Key Features Explained

This script automatically calculates and displays the following critical market-generated information:

* **Multi-Timeframe Market Profile**

Automatically draws Daily, Weekly, and Monthly profiles, allowing you to analyze market structure across different time horizons. The script preserves up to 20 historical sessions to provide deep market context.

* **Naked Point of Control (nPOC)**

A "Naked" POC is a Point of Control from a previous session that has **not** been revisited by price. These levels often act as powerful magnets for price, representing areas of unfinished business that the market may seek to retest. The script tracks and displays Daily, Weekly, and Monthly nPOCs until they are touched.

* **Single Prints (Imbalance Zones)**

A Single Print is a price level where only one TPO traded during the session's development. This signifies a rapid, aggressive price move and an imbalanced market. These areas, like gaps in a traditional chart, are frequently revisited as the market seeks to "fill in" these thin parts of the profile.

* **Poor Structure (Unfinished Auctions)**

A **Poor High** or **Poor Low** occurs when the top or bottom of a profile is flat, with two or more TPOs at the extreme price. This suggests that the auction in that direction was weak and inconclusive. These weak structures often signal a high probability that price will eventually break that high or low.

***

### ## 💡 How to Use This Indicator

This tool is not a signal generator but an analytical framework to improve your trading decisions.

1. **Determine Market Context:** Start by asking: Is the current price trading *inside* or *outside* the previous session's Value Area?

* **Inside VA:** The market is in a state of balance or range-bound. Look for trades between the VAH and VAL.

* **Outside VA:** The market is in a state of imbalance and may be starting a trend. Look for continuation or acceptance of prices outside the prior value.

2. **Identify Key Levels:**

* Use historical **nPOCs** as potential profit targets or areas to watch for a price reaction.

* Treat historical **VAH** and **VAL** levels as significant support and resistance zones.

* Note where **Single Prints** are. These are often price magnets that may get "filled" in the future.

3. **Spot Weakness:**

* A **Poor High** suggests weak resistance that may be easily broken.

* A **Poor Low** suggests weak support, signaling a potential for a continued move lower if broken.

***

### ## ⚙️ Customization & Crypto Presets

The indicator is highly customizable, allowing you to change colors, transparency, the number of historical sessions, and more.

To help traders get started quickly, the indicator includes **built-in layout presets** specifically calibrated for major cryptocurrencies: ** BINANCE:BTCUSDT.P , BINANCE:ETHUSDT.P , and BINANCE:SOLUSDT.P **. These presets automatically adjust key visual parameters to better suit the unique price characteristics and volatility of each asset, providing an optimized view right out of the box.

***

### ## ⚠️ Disclaimer

This indicator is a tool for market analysis and should not be interpreted as direct buy or sell signals. It provides information based on historical price action, which does not guarantee future results. Trading involves significant risk, and you should always use proper risk management. This script is designed for use on standard chart types (e.g., Candlesticks, Bar) and may produce misleading information on non-standard charts.

Chimera [theUltimator5]In myth, the chimera is an “impossible” hybrid—lion, goat, and serpent fused into one—striking to look at and formidable in presence. The word has come to mean a beautiful, improbable union of parts that shouldn’t work together, yet do.

Chimera is a dual-mode market context tool that blends a multi-input oscillator with classic ADX/DI trend strength, plus optional multi-timeframe “gap-line” tracking. Use it to visualize regime (trend vs. range), momentum swings around an adaptive midline, and higher timeframe (HTF) reference levels that auto-terminate on touch/cross.

Modes

1) Oscillator view

A smoothed composite of five common inputs—RSI, MACD (oscillator), Bollinger position, Stochastic, and an ATR/DI-weighted bias. Each is normalized to a comparable 0–100 style scale, averaged, and plotted as a candle-style oscillator (short vs. long smoothing, wickless for clarity). A dynamic midline with standard-deviation bands frames neutral → bearish/bullish zones. Colors ramp from neutral to your chosen Oversold/Overbought endpoints; consolidation can override to white.

Here is a description of the (5) signals used to calculate the sentiment oscillator:

RSI (14): Measures recent momentum by comparing average gains vs. losses. High = strength after advances; low = weakness after declines. (Z-score normalized to 0–100.)

MACD oscillator (12/26/9): Uses the difference between MACD and its signal (histogram) to gauge momentum shifts. Positive = bullish tilt; negative = bearish. (Z-score normalized.)

Bollinger Bands position (20, 2): Locates price within the bands (0–100 from lower → upper). Near upper suggests strength/expansion; near lower suggests weakness/contraction. (Then normalized.)

Stochastic (14, 3, 3): Shows where the close sits within the recent high-low range, smoothed via %D. Higher values = closes near highs; lower = near lows. (Scaled 0–100.)

ATR/DI composite (14): Volatility-weighted directional bias: (+DI − −DI) amplified by ATR as a % of price and its relative average. Positive = bullish pressure with volatility; negative = bearish. (Rank/scale normalized.)

All five are normalized and averaged into one composite, then smoothed (short/long) and compared to an adaptive midline with bands.

2) ADX view

Shows ADX, +DI, –DI with user-defined High Threshold. Transparency and color shift with regime. When ADX is strong, a directional “fire/ice” gradient fills the area between ADX and the high threshold, biased toward the dominant DI; when ADX is weak, a soft white fade highlights low-trend conditions.

HTF gap-line tracking (optional; both modes)

Detects “gap-like” reference levels after weak-trend consolidation flips into a sudden DI jump.

Anchors a line at the event bar’s open and auto-terminates upon first touch/cross (tick-size tolerance).

Auto-selects up to three higher timeframes suited to your chart resolution and prints non-overlapping lines with labels like 1H / 4H / 1D. Lower-priority duplicates are suppressed to reduce clutter.

Confirmation / repaint notes

Signals and lines finalize on bar close of the relevant timeframe.

HTF elements update only on the HTF bar close. During a forming bar they may appear transiently.

Line removal finalizes after the bar that produced the touch/cross closes.

Visual cues & effects

Oscillator candles: Open/High = long smoothing; Low/Close = short smoothing (no wicks).

Adaptive bands: Midline ± StdDev Multiplier × stdev of the blended series.

Consolidation tint: Optional white backdrop/candles when the consolidation condition is true (balance + low ADX).

Breakout VFX (optional): With strong DI/ADX and Bollinger breaks, renders a subtle “fire” flare above upper-band thrusts or “ice” shelf below lower-band thrusts.

Inputs (high-level)

Visual Style: Oscillator or ADX.

General (Oscillator): Lookback Period, Short/Long Smoothing, Standard Deviation Multiplier.

Color (Oscillator): Oversold/Overbought colors for gradient endpoints.

Plot (Oscillator): Show Candles, Show Slow MA Line, Show Individual Component (RSI/MACD/BB/Stoch/ATR).

Table (Oscillator): Show Information Table & position (compact dashboard of component values + status).

ADX / Gaps / VFX (both modes): ADX High Threshold, Highlight Backgrounds, Show Gap Labels, Visual Overlay Effects, and color choices for current-TF & HTF lines.

HTF selection: Automatic ladder (3 tiers) based on your chart timeframe.

Alerts (built-in)

Buy Signal – Primary: Oscillator exits oversold.

Sell Signal – Primary: Oscillator exits overbought.

Gap Fill Line Created (Any TF)

Gap Fill Line Terminated (Any TF)

ADX Crossed ABOVE/BELOW Low Threshold

ADX Crossed ABOVE/BELOW High Threshold

Consolidation Started

Alerts evaluate on the close of the relevant timeframe.

How to read it (quick guide)

Pick your lens: Oscillator for blended momentum around an adaptive midline; ADX for trend strength and DI skew.

Watch extremes & mean re-entries (Oscillator): Approaches to the top/bottom band show persistent momentum; returns toward the midline show normalization.

Check regime (ADX): Below Low = low-trend; above High = strong trend, with “fire/ice” bias toward +DI/–DI.

Track gap lines: Fresh labels mark new reference levels; lines auto-remove on first interaction. HTF lines add context but finalize only on HTF close.

The uniqueness from this indicator comes from multiple areas:

1. A unique multi-timeframe algorithm detects gap fill zones and plots them on the chart.

2. Visual effects for both visual modes were hand crafted to provide a visually stunning and intuitive interface.

3. The algorithm to determine sentiment uses a unique blend of weight and sensitivity adjustment to create a plot with elastic upper and lower bounds based off historical volatility and price action.

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).

- These are hardcoded but based on standard trading calendar assumptions.

5. **Compute Base Projections**:

- Base projection = Daily ATR × Days in period.

- This gives the total expected movement (range) without direction: e.g., for 3 months, $1 daily ATR × 63 = $63 total range.

6. **Analyze Candle Momentum (Win Rate)**:

- Counts green candles (close > open) and red candles (close < open) over the last 50 bars (ignores dojis where close == open).

- Total colored candles = green + red.

- Win rate = green / total colored (as a fraction, e.g., 0.7 for 70%). Defaults to 0.5 if no colored candles.

- This acts as a simple momentum proxy: higher win rate implies bullish bias.

7. **Adjust Projections Asymmetrically**:

- Upside projection = Base projection × Win rate.

- Downside projection = Base projection × (1 - Win rate).

- This skews the range: e.g., 70% win rate means 70% of the total range allocated to upside, 30% to downside.

8. **Calculate Projected Prices**:

- High = Current close + Upside projection.

- Low = Current close - Downside projection.

- Done separately for 1M and 3M.

9. **Plot Lines**:

- 3M High: Solid green line.

- 3M Low: Solid red line.

- 1M High: Dashed lime line.

- 1M Low: Dashed orange line.

- Lines extend horizontally from the current bar onward.

10. **Display Table**:

- A 3-column table (Projection, Price, % Change) in the top-right.

- Rows for 1M High/Low and 3M High/Low, color-coded.

- % Change = ((Projected price - Close) / Close) × 100.

- Updates dynamically with new data.

The entire process repeats on each new bar, so projections evolve as volatility and momentum change.

### Examples

Here are two hypothetical examples using the indicator on a daily chart. Assume it's applied to a stock like AAPL, but with made-up data for illustration. (In TradingView, you'd add the script to see real outputs.)

#### Example 1: Bullish Scenario (High Win Rate)

- Current Close: $150.

- Weekly ATR (50 periods): $10 → Daily ATR: $10 / 5 = $2.

- Last 50 Candles: 35 green, 15 red → Total colored: 50 → Win Rate: 35/50 = 0.7 (70%).

- Base Projections:

- 1M: $2 × 21 = $42.

- 3M: $2 × 63 = $126.

- Adjusted Projections:

- 1M Upside: $42 × 0.7 = $29.4 → High: $150 + $29.4 = $179.4 (+19.6%).

- 1M Downside: $42 × 0.3 = $12.6 → Low: $150 - $12.6 = $137.4 (-8.4%).

- 3M Upside: $126 × 0.7 = $88.2 → High: $150 + $88.2 = $238.2 (+58.8%).

- 3M Downside: $126 × 0.3 = $37.8 → Low: $150 - $37.8 = $112.2 (-25.2%).

- On the Chart: Green/lime lines skewed higher; table shows bullish % changes (e.g., +58.8% for 3M high).

- Interpretation: Suggests stronger potential upside due to recent bullish momentum; useful for call options or long positions.

#### Example 2: Bearish Scenario (Low Win Rate)

- Current Close: $50.

- Weekly ATR (50 periods): $3 → Daily ATR: $3 / 5 = $0.6.

- Last 50 Candles: 20 green, 30 red → Total colored: 50 → Win Rate: 20/50 = 0.4 (40%).

- Base Projections:

- 1M: $0.6 × 21 = $12.6.

- 3M: $0.6 × 63 = $37.8.

- Adjusted Projections:

- 1M Upside: $12.6 × 0.4 = $5.04 → High: $50 + $5.04 = $55.04 (+10.1%).

- 1M Downside: $12.6 × 0.6 = $7.56 → Low: $50 - $7.56 = $42.44 (-15.1%).

- 3M Upside: $37.8 × 0.4 = $15.12 → High: $50 + $15.12 = $65.12 (+30.2%).

- 3M Downside: $37.8 × 0.6 = $22.68 → Low: $50 - $22.68 = $27.32 (-45.4%).

- On the Chart: Red/orange lines skewed lower; table highlights larger downside % (e.g., -45.4% for 3M low).

- Interpretation: Indicates bearish risk; might prompt protective puts or short strategies.

#### Example 3: Neutral Scenario (Balanced Win Rate)

- Current Close: $100.

- Weekly ATR: $5 → Daily ATR: $1.

- Last 50 Candles: 25 green, 25 red → Win Rate: 0.5 (50%).

- Projections become symmetric:

- 1M: Base $21 → Upside/Downside $10.5 each → High $110.5 (+10.5%), Low $89.5 (-10.5%).

- 3M: Base $63 → Upside/Downside $31.5 each → High $131.5 (+31.5%), Low $68.5 (-31.5%).

- Interpretation: Pure volatility-based range, no directional bias—ideal for straddle options or range trading.

In real use, test on historical data: e.g., if past projections captured actual moves ~68% of the time (1 standard deviation for ATR), it validates the volatility assumption. Adjust the lookback for different assets (shorter for volatile cryptos, longer for stable blue-chips).

Key Levels: Daily, Weekly, Monthly [BackQuant]Key Levels: Daily, Weekly, Monthly

Map the market’s “memory” in one glance—yesterday’s range, this week’s chosen day high/low, and D/W/M opens—then auto-clean levels once they break.

What it does

This tool plots three families of high-signal reference lines and keeps them tidy as price evolves:

Chosen Day High/Low (per week) — Pick a weekday (e.g., Monday). For each past week, the script records that day’s session high and low and projects them forward for a configurable number of bars. These act like “memory levels” that price often revisits.

Daily / Weekly / Monthly Opens — Plots the opening price of each new day, week, and month with separate styling. These opens frequently behave like magnets/flip lines intraday and anchors for regime on higher timeframes.

Auto-pruning — When price breaks a stored level, the script can automatically remove it to reduce clutter and refocus you on still-active lines. See: (broken levels removed).

Why these levels matter

Liquidity pockets — Prior day’s high/low and the daily open concentrate stops and pending orders. Mapping them quickly reveals likely sweep or fade zones. Example: previous day highs + daily open highlighting liquidity:

Context & regime — Monthly opens frame macro bias; trading above a rising cluster of monthly opens vs. below gives a clean top-down read. Example: monthly-only “macro outlook” view:

Cleaner charts — Auto-remove broken lines so you focus on what still matters right now.

What it plots (at a glance)

Past Chosen Day High/Low for up to N prior weeks (your choice), extended right.

Current Daily Open , Weekly Open , and Monthly Open , each with its own color, label, and forward extension.

Optional short labels (e.g., “Mon High”) or full labels (with week/month info).

How breaks are detected & cleaned

You control both the evidence and the timing of a “break”:

Break uses — Choose Close (more conservative) or Wick (more sensitive).

Inclusive? — If enabled, equality counts (≥ high or ≤ low). If disabled, you need a strict cross.

Allow intraday breaks? — If on, a level can break during the tracked day; if off, the script only counts breaks after the session completes.

Remove Broken Levels — When a break is confirmed, the line/label is deleted automatically. (See the demo: )

Quick start

Pick a Day of Week to Track (e.g., Monday).

Set how many weeks back to show (e.g., 8–10).

Choose how far to extend each family (bars to the right for chosen-day H/L and D/W/M opens).

Decide if a break uses Close or Wick , and whether equality counts.

Toggle Remove Broken Levels to keep the chart clean automatically.

Tips by use-case

Intraday bias — Watch the Daily Open as a magnet/flip. If price gaps above and holds, pullbacks to the daily open often decide direction. Pair with last day’s high/low for sweep→reversal or true breakout cues. See:

Weekly structure — Track the week’s chosen day (e.g., Monday) high/low across prior weeks. If price stalls near a cluster of old “Monday Highs,” look for sweep/reject patterns or continuation on reclaim.

Macro regime — Hide daily/weekly lines and keep only Monthly Opens to read bigger cycles at a glance (BTC/crypto especially). Example:

Customization

Use wicks or bodies for highs/lows (wicks capture extremes; bodies are stricter).

Line style & thickness — solid/dashed/dotted, width 1–5, plus global transparency.

Labels — Abbreviated (“Mon High”, “D Open”) or full (month/week/day info).

Color scheme — Separate colors for highs, lows, and each of D/W/M opens.

Capacity controls — Set how many daily/weekly/monthly opens and how many weeks of chosen-day H/L to keep visible.

What’s under the hood

On your selected weekday, the script records that session’s true high and true low (using wicks or body-based extremes—your choice), then projects a horizontal line forward for the next bars.

At each new day/week/month , it records the opening price and projects that line forward as well.

Each bar, the script checks your “break” rules; once broken, lines/labels are removed if auto-cleaning is on.

Everything updates in real time; past levels don’t repaint after the session finishes.

Recommended presets

Day trading — Weeks back: 6–10; extend D/W opens: 50–100 bars; Break uses: Close ; Inclusive: off; Auto-remove: on.

Swing — Fewer daily opens, more weekly opens (2–6), and 8–12 weeks of chosen-day H/L.

Macro — Show only Monthly Opens (1–6 months), dashed style, thicker lines for clarity.

Reading the examples

Broken lines disappear — decluttering in action:

Macro outlook — monthly opens as cycle rails:

Liquidity map — previous day highs + daily open:

Final note

These are not “signals”—they’re reference points that many participants watch. By standardising how you draw them and automatically clearing the ones that no longer matter, you turn a noisy chart into a focused map: where liquidity likely sits, where price memory lives, and which lines are still in play.

Quantile Regression Bands [BackQuant]Quantile Regression Bands

Tail-aware trend channeling built from quantiles of real errors, not just standard deviations.

What it does

This indicator fits a simple linear trend over a rolling lookback and then measures how price has actually deviated from that trend during the window. It then places two pairs of bands at user-chosen quantiles of those deviations (inner and outer). Because bands are based on empirical quantiles rather than a symmetric standard deviation, they adapt to skewed and fat-tailed behaviour and often hug price better in trending or asymmetric markets.

Why “quantile” bands instead of Bollinger-style bands?

Bollinger Bands assume a (roughly) symmetric spread around the mean; quantiles don’t—upper and lower bands can sit at different distances if the error distribution is skewed.

Quantiles are robust to outliers; a single shock won’t inflate the bands for many bars.

You can choose tails precisely (e.g., 1%/99% or 5%/95%) to match your risk appetite.

How it works (intuitive)

Center line — a rolling linear regression approximates the local trend.

Residuals — for each bar in the lookback, the indicator looks at the gap between actual price and where the line “expected” price to be.

Quantiles — those gaps are sorted; you select which percentiles become your inner/outer offsets.

Bands — the chosen quantile offsets are added to the current end of the regression line to draw parallel support/resistance rails.

Smoothing — a light EMA can be applied to reduce jitter in the line and bands.

What you see

Center (linear regression) line (optional).

Inner quantile bands (e.g., 25th/75th) with optional translucent fill.

Outer quantile bands (e.g., 1st/99th) with a multi-step gradient to visualise “tail zones.”

Optional bar coloring: bars trend-colored by whether price is rising above or falling below the center line.

Alerts when price crosses the outer bands (upper or lower).

How to read it

Trend & drift — the slope of the center line is your local trend. Persistent closes on the same side of the center line indicate directional drift.

Pullbacks — tags of the inner band often mark routine pullbacks within trend. Reaction back to the center line can be used for continuation entries/partials.

Tails & squeezes — outer-band touches highlight statistically rare excursions for the chosen window. Frequent outer-band activity can signal regime change or volatility expansion.

Asymmetry — if the upper band sits much further from the center than the lower (or vice versa), recent behaviour has been skewed. Trade management can be adjusted accordingly (e.g., wider take-profit upslope than downslope).

A simple trend interpretation can be derived from the bar colouring

Good use-cases

Volatility-aware mean reversion — fade moves into outer bands back toward the center when trend is flat.

Trend participation — buy pullbacks to the inner band above a rising center; flip logic for shorts below a falling center.

Risk framing — set dynamic stops/targets at quantile rails so position sizing respects recent tail behaviour rather than fixed ticks.

Inputs (quick guide)

Source — price input used for the fit (default: close).

Lookback Length — bars in the regression window and residual sample. Longer = smoother, slower bands; shorter = tighter, more reactive.

Inner/Outer Quantiles (τ) — choose your “typical” vs “tail” levels (e.g., 0.25/0.75 inner, 0.01/0.99 outer).

Show toggles — independently toggle center line, inner bands, outer bands, and their fills.

Colors & transparency — customize band and fill appearance; gradient shading highlights the tail zone.

Band Smoothing Length — small EMA on lines to reduce stair-step artefacts without meaningfully changing levels.

Bar Coloring — optional trend tint from the center line’s momentum.

Practical settings

Swing trading — Length 75–150; inner τ = 0.25/0.75, outer τ = 0.05/0.95.

Intraday — Length 50–100 for liquid futures/FX; consider 0.20/0.80 inner and 0.02/0.98 outer in high-vol assets.

Crypto — Because of fat tails, try slightly wider outers (0.01/0.99) and keep smoothing at 2–4 to tame weekend jumps.

Signal ideas

Continuation — in an uptrend, look for pullback into the lower inner band with a close back above the center as a timing cue.

Exhaustion probe — in ranges, first touch of an outer band followed by a rejection candle back inside the inner band often precedes mean-reversion swings.

Regime shift — repeated closes beyond an outer band or a sharp re-tilt in the center line can mark a new trend phase; adjust tactics (stop-following along the opposite inner band).

Alerts included

“Price Crosses Upper Outer Band” — potential overextension or breakout risk.

“Price Crosses Lower Outer Band” — potential capitulation or breakdown risk.

Notes

The fit and quantiles are computed on a fixed rolling window and do not repaint; bands update as the window moves forward.

Quantiles are based on the recent distribution; if conditions change abruptly, expect band widths and skew to adapt over the next few bars.

Parameter choices directly shape behaviour: longer windows favour stability, tighter inner quantiles increase touch frequency, and extreme outer quantiles highlight only the rarest moves.

Final thought

Quantile bands answer a simple question: “How unusual is this move given the current trend and the way price has been missing it lately?” By scoring that question with real, distribution-aware limits rather than one-size-fits-all volatility you get cleaner pullback zones in trends, more honest “extreme” tags in ranges, and a framework for risk that matches the market’s recent personality.

DNSE VN301!, ADX Momentum StrategyDiscover the tailored Pine Script for trading VN30F1M Futures Contracts intraday.

This strategy applies the Statistical Method (IQR) to break down the components of the ADX, calculating the threshold of "normal" momentum fluctuations in price to identify potential breakouts for entry and exit signals. The script automatically closes all positions by 14:30 to avoid overnight holdings.

www.tradingview.com

Settings & Backtest Results:

- Chart: 30-minute timeframe

- Initial capital: VND 100 million

- Position size: 4 contracts per trade (includes trading fees, excludes tax)

- Backtest period: Sep-2021 to Sep-2025

- Return: over 270% (with 5 ticks slippage)

- Trades executed: 1,000+

- Win rate: ~40%

- Profit factor: 1.2

Default Script Settings:

Calculates the acceleration of changes in the +DI and -DI components of the ADX, using IQR to define "normal" momentum fluctuations (adjustable via Lookback period).

Calculates the difference between each bar’s Open and Close prices, using IQR to define "normal" gaps (adjustable via Lookback period).

Entry & Exit Conditions:

Entry Long: Change in +DI or -DI > Avg IQR Value AND Close Price > Previous Close

Exit Long: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI < Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price < Previous Close

Entry Short: Change in +DI or -DI > Avg IQR Value AND Close Price < Previous Close

Exit Short: (all 4 conditions must be met)

- Change in +DI or -DI > Avg IQR Value

- RSI > Previous RSI

- Close–Open Gap > Avg IQR Gap

- Close Price > Previous Close

Disclaimers:

Trading futures contracts carries a high degree of risk, and price movements can be highly volatile. This script is intended as a reference tool only. It should be used by individuals who fully understand futures trading, have assessed their own risk tolerance, and are knowledgeable about the strategy’s logic.

All investment decisions are the sole responsibility of the user. DNSE bears no liability for any potential losses incurred from applying this strategy in real trading. Past performance does not guarantee future results. Please contact us directly if you have specific questions about this script.

20 MA ReversionA mean reversion tactic with the 20 SMA:

the indicator is chcking specific parameters, such as the volume related to the last day's volume, distance from 20 SMA, CCI values and changes, trends, and recent gaps that will act as a magnet.

enjoy!

Technical Summary VWAP | RSI | VolatilityTechnical Summary VWAP | RSI | Volatility

The Quantum Trading Matrix is a multi-dimensional market-analysis dashboard designed as an educational and idea-generation tool to help traders read price structure, participation, momentum and volatility in one compact view. It is not an automated execution system; rather, it aggregates lightweight “quantum” signals — VWAP position, momentum oscillator behaviour, multi-EMA trend scoring, volume flow and institutional activity heuristics, market microstructure pivots and volatility measures — and synthesizes them into a single, transparent score and signal recommendation. The primary goal is to make explicit why a given market looks favourable or unfavourable by showing the individual ingredients and how they combine, enabling traders to learn, test and form rules based on observable market mechanics.

Each module of the matrix answers a distinct market question. VWAP and its percentage distance indicate whether the current price is trading above or below the intraday volume-weighted average — a proxy for intraday institutional control and value. The quantum momentum oscillator (fast and slow EMA difference scaled to percent) captures short-to-intermediate momentum shifts, providing a quickly responsive view of directional pressure. Multi-EMA trend scoring (8/21/50) produces a simple, transparent trend score by counting conditions such as price above EMAs and cross-EMAs ordering; this score is used to categorize market trend into descriptive buckets (e.g., STRONG UP, WEAK UP, NEUTRAL, DOWN). Volume analysis compares current volume to a recent moving average and computes a Z-score to detect spikes and unusual participation; additional buy/sell pressure heuristics (buyingPressure, sellingPressure, flowRatio) estimate whether upside or downside participation dominates the bar. Institutional activity is approximated by flagging large orders relative to volume baseline (e.g., volume > 2.5× MA) and estimating a dark pool proxy; this is a heuristic to highlight bars that likely had large players involved.

The dashboard also performs market-structure detection with small pivot windows to identify recent local support/resistance areas and computes price position relative to the daily high/low (dailyMid, pricePosition). Volatility is measured via ATR divided by price and bucketed into LOW/NORMAL/HIGH/EXTREME categories to help you adapt stop sizing and expectational horizons. Finally, all these pieces feed an interpretable scoring function that rewards alignment: VWAP above, strong flow ratio, bullish trend score, bullish momentum, and favorable RSI zone add to the overall score which is presented as a 0–100 metric and a colored emoji indicator for at-a-glance assessment.

The mashup is purposeful: each indicator covers a failure mode of the other. For example, momentum readings can be misleading during volatility spikes; VWAP informs whether institutions are on the bid or offer; volume Z-score detects abnormal participation that can validate a breakout; multi-EMA score mitigates single-EMA whipsaws by requiring a combination of price/EMA conditions. Combining these signals increases information content while keeping each component explainable — a key compliance requirement. The script intentionally emphasizes transparency: when it shows a BUY/SELL/HOLD recommendation, the dashboard shows the underlying sub-components so a trader can see whether VWAP, momentum, volume, trend or structure primarily drove the score.

For practical use, adopt a clear workflow: (1) check the matrix score and read the component tiles (VWAP position, momentum, trend and volume) to understand the drivers; (2) confirm market-structure support/resistance and pricePosition relative to the daily range; (3) require at least two corroborating components (for example, VWAP ABOVE + Momentum BULLISH or Volume spike + Trend STRONG UP) before considering entries; (4) use ATR-based stops or daily pivot distance for stop placement and size positions such that the trade risks a small, pre-defined percent of capital; (5) for intraday scalps shorten holding time and tighten stops, for swing trades increase lookback lengths and require multi-timeframe (higher TF) agreement. Treat the matrix as an idea filter and replay lab: when an alert triggers, replay the bars and observe which components anticipated the move and which lagged.

Parameter tuning matters. Shortening the momentum length makes the oscillator more sensitive (useful for scalping), while lengthening it reduces noise for swing contexts. Volume profile bars and MA length should match the instrument’s liquidity — increase the MA for low-liquidity stocks to reduce false institutional flags. The trend multiplier and signal sensitivity parameters let you calibrate how aggressively the matrix counts micro evidence into the score. Always backtest parameter sets across multiple periods and instruments; run walk-forward tests and keep a simple out-of-sample validation window to reduce overfitting risk.

Limitations and failure modes are explicit: institutional flags and dark-pool estimates are heuristics and cannot substitute for true tape or broker-level order flow; volume split by price range is an approximation and will not perfectly reflect signed volume; pivot detection with small windows may miss larger structural swings; VWAP is typically intraday-centric and less meaningful across multi-day swing contexts; the score is additive and may not capture non-linear relationships between features in extreme market regimes (e.g., flash crashes, circuit breaker events, or overnight gaps). The matrix is also susceptible to false signals during major news releases when price and volume behavior dislocate from typical patterns. Users should explicitly test behavior around earnings, macro data and low-liquidity periods.

To learn with the matrix, perform these experiments: (A) collect all BUY/SELL alerts over a 6-month period and measure median outcome at 5, 20 and 60 bars; (B) require additional gating conditions (e.g., only accept BUY when flowRatio>60 and trendScore≥4) and compare expectancy; (C) vary the institutional threshold (2×, 2.5×, 3× volumeMA) to see how many true positive spikes remain; (D) perform multi-instrument tests to ensure parameters are not tuned to a single ticker. Document every test and prefer robust, slightly lower returns with clearer logic rather than tuned “optimal” results that fail out of sample.

Originality statement: This script’s originality lies in the curated combination of intraday value (VWAP), multi-EMA trend scoring, momentum percent oscillator, volume Z-score plus buy/sell flow heuristics and a compact, interpretable scoring system. The script is not a simple indicator mashup; it is a didactic ensemble specifically designed to make internal rationale visible so traders can learn how each market characteristic contributes to actionable probability. The tool’s novelty is its emphasis on interpretability — showing the exact contributing signals behind a composite score — enabling reproducible testing and educational value.

Finally, for TradingView publication, include a clear description listing the modules, a short non-technical summary of how they interact, the tunable inputs, limitations and a risk disclaimer. Remove any promotional content or external contact links. If you used trademark symbols, either provide registration details or remove them. This transparent documentation satisfies TradingView’s requirement that mashups justify their composition and teach users how to use them.

Quantum Trading Matrix — multi-factor intraday dashboard (educational use only).

Purpose: Combines intraday VWAP position, a fast/slow EMA momentum percent oscillator, multi-EMA trend scoring (8/21/50), volume Z-score and buy/sell flow heuristics, pivot-based microstructure detection, and ATR-based volatility buckets to produce a transparent, componentized market score and trade-idea indicator. The mashup is intentional: VWAP identifies intraday value, momentum detects short bursts, EMAs provide structural trend bias, and volume/flow confirm participation. Signals require alignment of at least two components (for example, VWAP ABOVE + Momentum BULLISH + positive flow) for higher confidence.

Inputs: momentum period, volume MA/profile length, EMA configuration (8/21/50), trend multiplier, signal sensitivity, color and display options. Use shorter momentum lengths for scalps and longer for swing analysis. Increase volume MA for thinly traded instruments.

Limitations: Institutional/dark-pool estimates and flow heuristics are approximations, not actual exchange tape. VWAP is intraday-focused. Expect false signals during major news or low-liquidity sessions. Backtest and paper-trade before applying real capital.

Risk Disclaimer: For education and analysis only. Not financial advice. Use proper risk management. The author is not responsible for trading losses.

________________________________________

Risk & Misuse Disclaimer

This indicator is provided for education, analysis and idea generation only. It is not investment or financial advice and does not guarantee profits. Institutional activity flags, dark-pool estimates and flow heuristics are approximations and should not be treated as exchange tape. Backtest thoroughly and use demo/paper accounts before trading real capital. Always apply appropriate position sizing and stop-loss rules. The author is not responsible for any trading losses resulting from the use or misuse of this tool.

________________________________________

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Back test thoroughly and use proper risk management.

Pattern ScannerUltimate Pattern Scanner — multi-timeframe candlestick discovery tool (educational use only).

Purpose: This script scans user-selected timeframes for classical candlestick patterns (for example: engulfing, morning/evening stars, hammers, dojis, tasuki gaps, three soldiers/crows, tweezers, marubozu, and others) and reports pattern name, detection price, directional signal (Bull / Bear / Neutral), and a simple volume participation metric. It is intended as an idea-generation and training tool to help traders learn pattern mechanics, not as an automated trading system.

Main modules and rationale: 1) Pattern engine — applies classical candle structure rules to detect formations; 2) SMA trend filter (configurable length) — provides a directional bias to favor trade-with-trend setups; 3) Volume heuristic — approximates participation by separating candles into buy-like and sell-like volume and comparing total volume to a moving average; 4) Multi-timeframe aggregator — collects and presents pattern results from multiple timeframes; 5) Alerts — optional alerts list detected patterns and TFs. Combining these modules is intentional: patterns provide structure, SMA provides context, and volume supplies participation confirmation. Together they improve the educational value and practical relevance of each detected pattern.

How to use: Choose timeframes and SMA length that match your trading horizon. Use the scanner to locate pattern candidates, then confirm with higher-timeframe agreement and volume ratio before considering trade entry. Use structural stops (recent swing highs/lows or ATR-based stops) and define risk:reward rules. For learning, replay alerted bars and record outcomes over fixed horizons to build empirical statistics.

Limitations: Volume classification (close>open) is a heuristic and not a true bid/ask tape. SMA is a lagging trend proxy. Multi-timeframe agreement reduces but does not eliminate false signals, especially around news or in low-liquidity instruments. Use demo accounts and backtesting before live trading.

Inputs you can adjust: timeframe list, SMA length, volume MA length, which patterns to enable/disable, display options.

Compliance notes: This description explains why modules are combined and what the script does without exposing source code logic; it is non-promotional and contains no contact links. Remove any trademark symbols unless registration details are provided.

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Backtest thoroughly and use proper risk management.

Multi-RSI with Stochastic Oscillator - flack0xA sophisticated momentum analysis tool combining 4 customizable RSI oscillators with an innovative Close/Close Stochastic implementation. Designed for traders seeking comprehensive momentum insights across multiple timeframes in a single, organized indicator.

Key Features:

4 Independent RSI Oscillators with default periods: 2, 3, 9, 27

Innovative Close/Close Stochastic - Compares closing prices to closing price ranges (not high/low)

Complete Customization - Individual control over periods, colors, line widths, and visibility

Reference Levels - Customizable overbought (70), oversold (30), and midline (50) levels

Smart Alert System - Crossover notifications for key momentum shifts

Unique Close/Close Stochastic Methodology:

Unlike traditional Stochastic oscillators that use high/low ranges.

Benefits of Close/Close Approach:

Eliminates Gap Noise - Ignores overnight gaps and intraday wicks

Smoother Signals - Reduces whipsaws common in traditional Stochastic

Position-Relevant - Focuses on actual settlement prices traders care about

Cleaner Momentum Reading - Pure closing price momentum without intraday volatility

ICT Sweep + FVG Entry (v6) • Pro Pack 📌 ICT Sweep + FVG Entry Pro Pack

This indicator combines key ICT price action concepts with practical execution tools to help traders spot high-probability setups faster and more objectively. It’s designed for scalpers and intraday traders who want to keep their chart clean but never miss critical market structure events.

🔑 Features

Liquidity Pools (HTF)

• Auto-detects recent swing highs/lows from higher timeframes (5m/15m).

• Draws both lines and optional rectangles/zones for clear liquidity areas.

Liquidity Sweeps (BSL/SSL)

• Identifies when price sweeps above/below liquidity pools and rejects back.

• Optional Grade-A sweep filter (wick size + strong re-entry).

Fair Value Gaps (FVGs)

• Highlights bullish/bearish imbalances.

• Optional midline (50%) entry for precision.

• Auto-invalidation when price fully closes inside the gap.

Killzones (New York)

• Highlights AM (9:30–11:30) and PM (14:00–15:30) killzones.

• Option to block signals outside killzones for higher strike rate.

Bias Badge (DR50)

• Displays if price is trading in a Bull, Bear, or Range context based on displacement range midpoint.

SMT Assist (NQ vs ES)

• Detects simple divergences between indices:

Bearish SMT → NQ makes HH while ES doesn’t.

Bullish SMT → NQ makes LL while ES doesn’t.

SL/TP Helper & R:R Label

• Automatically draws stop loss (at sweep extreme) and target (opposite pool or recent swing).

• Displays expected Risk:Reward ratio and blocks entries if below your chosen minimum.

Filters

• ATR filter ensures signals only appear in sufficient volatility.

• Sweep quality filter avoids weak wicks and fake-outs.

🎯 How to Use

Start on HTF (5m/15m) → Identify liquidity zones and bias.

Drop to LTF (1m) → Wait for a liquidity sweep confirmation.

Check for FVG in the sweep’s direction → Look for retest entry.

Use the SL/TP helper to validate your risk/reward before taking the trade.

Focus entries during NY Killzones for maximum effectiveness.

✅ Why this helps

This tool reduces screen time and hesitation by automating repetitive ICT concepts:

Liquidity pools, sweeps, and FVGs are marked automatically.

Killzone timing and SMT divergence are simplified.

Clear visual signals for entries with built-in RR filter help keep your trading mechanical.

⚠️ Disclaimer: This script is for educational purposes only. It does not provide financial advice or guarantee results. Always use proper risk management.

ICT Sweep + FVG Entry (v6) • Antoine📌 ICT Sweep + FVG Entry (Antoine)

This indicator is designed for price action traders who follow ICT concepts and want a mechanical tool to spot liquidity sweeps, fair value gaps (FVGs), and precise entry signals.

🔎 Key Features

Liquidity Pools (HTF)

• Automatically plots recent swing highs/lows from a higher timeframe (5m/15m).

• These act as Buy Side Liquidity (BSL) and Sell Side Liquidity (SSL) levels where stop orders accumulate.

Sweep Detection

• Identifies when price breaks a pool (BSL/SSL) but closes back inside → a classic liquidity grab.

• Plots a triangle on the chart when a sweep is confirmed.

Fair Value Gap (FVG) Highlighting

• Detects bullish and bearish FVGs on the execution timeframe (ideal for 1m).

• Option to display active FVG zones with shaded boxes.

Entry Signals

• A signal (cross) appears when:

A liquidity sweep occurs.

An FVG forms in the direction of the rejection.

Price retests the FVG (entry at the 50% mid-level or edge).

Alerts Ready

• Get alerted for sweeps (bullish/bearish) and for entry confirmations (long/short FVG retests).

🎯 How to Use

Choose your HTF (5m or 15m) → The indicator maps major liquidity pools.

Drop to LTF (1m) → Wait for a sweep signal at one of the pools.

Confirm with FVG → If an FVG appears in the sweep’s direction, the indicator waits for a retest.

Entry → Enter on the retest of the FVG (edge or 50%).

Risk Management

Stop loss: just beyond the sweep’s wick.

Target: opposite liquidity pool.

Minimum recommended R:R: 1:2.

✅ Why this helps

This tool makes it easier to trade ICT-style setups without missing opportunities:

No need to manually draw every swing high/low.

Automatic FVG detection saves time.

Clear sweep + FVG + retest logic keeps your entries mechanical and disciplined.

⚠️ Disclaimer: This script is for educational purposes only. It does not guarantee profits. Always use proper risk management.

Swing Guardrail — 30-sec Midterm Check (EBITDA Margin & EV/EBITDWhat it does

Before a short-term swing entry, this indicator right-sizes positions by a quick midterm (3–12m) durability screen using two fundamentals:

EBITDA Margin (TTM) → earning power / operational resilience

EV/EBITDA (TTM) → price tag vs earning capacity (payback feel)

A high-contrast table (top-right) shows both metrics and a verdict:

PASS — both meet thresholds → normal size

HALF — only one meets → reduce size

FAIL — neither meets → avoid

Why check “midterm” for a short-term trade?

Short swings still face earnings/news gaps, failed breakouts, and regime shifts. Names with weak margins or stretched valuation tend to break faster and deeper. A 30-sec durability check helps you:

Filter fragile setups (avoid expensive + weakening names)

Stabilize drawdowns (size down when quality/price don’t align)

Keep timing unchanged while improving risk-adjusted returns

Inputs (defaults)

Min EBITDA Margin % (TTM): 8%

Max EV/EBITDA (TTM): 12

Dark chart? High-contrast colors

How to use with a swing system

Get your entry from price/volume (e.g., Ichimoku cloud break, Kijun reclaim, Tenkan>Kijun; or your A/B/C rules).

Run this check only to set size (not timing).

Optional alerts: Once per bar close for PASS / HALF / FAIL.

Size mapping & event guard

PASS → 100% of your planned size

HALF → ~50% size / tighter stops

FAIL → watchlist only

If earnings < ~10 JP business days, drop one tier; ≤3 days → avoid.

Sector guides (tweak as needed)

Software/Internet: Margin ≥ 15%, EV/EBITDA ≤ 18

Industrials/Consumer: Margin ≥ 8%, EV/EBITDA ≤ 12

Retail: Margin ≥ 5–7%, EV/EBITDA ≤ 10–12

Edge cases / substitutions

Banks/Insurers/REITs or net-cash/negative EBITDA: EV/EBITDA may mislead → consider Net Debt/EBITDA or sector metrics (CET1/LTV/DSCR).

Sparse data / fresh listings: numbers may be NA until updates.

Notes & limitations

Data via request.financial() (TTM/most-recent). Some tickers/regions can show NA until fundamentals refresh.

This is a risk-screen / sizing tool, not a buy/sell signal.

Disclaimer

Educational use only. Not investment advice.

日本語

タイトル

スイング用ガードレール―中期“壊れにくさ”30秒チェック(EBITDAマージン & EV/EBITDA, TTM)

概要

短期スイングのエントリー前に、中期(3〜12か月)の耐久性を2指標で素早く確認し、ポジションサイズを決めるためのツールです。

EBITDAマージン(TTM):事業の稼ぐ力・体力

EV/EBITDA(TTM):その体力に対する“値札”(回収年数の感覚)

右上の高コントラスト表に数値と判定を表示:

PASS:両方クリア → 通常サイズ

HALF:片方のみ → サイズ半分

FAIL:両方NG → 見送り

なぜ短期でも“中期”を確認?

短期でも決算・ニュースのギャップ、ブレイク失敗、地合い転換は起きます。マージンが弱い/割高すぎる銘柄は崩れやすく、戻りも鈍い傾向。30秒の耐久性チェックで

脆いセットアップを回避

ドローダウンを平準化(サイズで吸収)

タイミングは変えずに、リスク調整後リターンの改善を狙えます。

入力(既定)

最低EBITDAマージン:8%

最大EV/EBITDA:12

黒背景向け:高コントラスト表示

使い方(スイング手法と併用)

まずは価格シグナル(一目の雲上抜け/基準線回復/転換線>基準線、またはA/B/Cルール)。

本インジの判定でサイズのみ決定(エントリーのタイミングは出しません)。

任意でバー確定アラート(PASS/HALF/FAIL)を設定。

サイズ目安 & イベント抑制

PASS:計画サイズ100%

HALF:約50%(ストップもタイトに)

FAIL:見送り

決算まで≦10営業日なら1段階サイズダウン、≦3営業日は原則見送り。

セクター目安(調整推奨)

ソフト/ネット:マージン 15%以上、EV/EBITDA 18以下

工業/一般消費:マージン 8%以上、EV/EBITDA 12以下

小売:マージン 5〜7%以上、EV/EBITDA 10〜12以下

例外・代替

銀行・保険・REIT/ネットキャッシュ・EBITDAマイナス:EV/EBITDAは適さない場合 → Net Debt/EBITDAやCET1/LTV/DSCR等で補助。

新規上場・データ薄:更新までNAのことあり。

注意

データは request.financial() を使用。更新前はNAの可能性。

本ツールはリスク確認/サイズ調整用で、売買シグナルではありません。

免責

情報提供のみ。投資判断は自己責任で。

STOCK SCHOOL | FVGThe Stock School FVG Indicator is designed to help traders identify and trade Fair Value Gaps (FVGs) and Inverse FVGs (IFVGs) with precision.

Built for both intraday and swing traders, this tool highlights high-probability trading zones where institutions leave imbalances in the market.

✨ Key Features:

Auto-detects FVGs & IFVGs in real-time

Works on all timeframes and instruments (Nifty, BankNifty, Stocks, Forex, Crypto)

Non-repainting logic for reliable signals

Clean and easy-to-use interface with Stock School styling

Perfect for Smart Money Concept (SMC) traders

🚀 With this indicator, you can:

Spot institutional footprints quickly

Combine with BOS, CHoCH, Order Blocks for high accuracy

Trade liquidity sweeps + FVG collisions with confidence

💡 Disclaimer:

This indicator is for educational purposes only. Trading involves risk. Always use proper risk management.

Trading Sessions with Holidays & Timer🌍 Trading Sessions Matter

Markets breathe in cycles. When Tokyo, London, or New York steps in, liquidity shifts and price often reacts fast.

Example: New York closed BTC at $110K, and when traders woke up, the price was already $113K. That gap says everything about overnight pressure and the next move.

⚡ Indicator Features

✅ Session boxes (Tokyo, London, NY) with custom colors & time zones

✅ Open/close lines → spot gaps & momentum

✅ Average price per session → see where pressure builds

✅ Tick range → quick volatility check

✅ 🏖 Holiday markers → avoid false quiet markets

✅ Live status table → session OPEN / CLOSED + countdown timer

🚀 How to Use

Works on intraday timeframes (1m–4h)

Watch session opens/closes → liquidity shift points

Compare ranges & averages between Tokyo, London, NY

Use the timer to prep before the next wave

This tool helps you visualize the heartbeat of global markets session by session.

🔖 #BTCUSDT #Forex #TradingSessions #Crypto #DayTrading

ICT FVG Buy/Sell SignalsThis bot is built on ICT (Inner Circle Trader) concepts such as:

Fair Value Gaps (FVGs) – imbalance zones between candles.

Consequent Encroachment (CE) – the midpoint of a gap.

Premium / Discount Arrays – dealing ranges split into premium (sell-side) and discount (buy-side) zones.

Displacement candles – strong impulsive moves that confirm intent.

The bot scans for FVGs, marks CE levels, and waits for price to return to these levels.

When price revisits a valid FVG zone with displacement confirmation and in the correct PD array, the bot generates a BUY or SELL signal.

✅ Signal Rules

Buy Signal

Price trades back into a Bullish FVG.

Current bar shows bullish displacement (large bullish body relative to ATR).

Price is in discount territory of the current dealing range (if PD filter is enabled).

Close is above the CE line of the FVG.

Sell Signal

Price trades back into a Bearish FVG.

Current bar shows bearish displacement.

Price is in premium territory of the current dealing range.

Close is below the CE line of the FVG.

🎯 What You’ll See on the Chart

Green “BUY” labels below candles when long signals trigger.

Red “SELL” labels above candles when short signals trigger.

Shaded background:

Red = Premium zone (sell side).

Teal = Discount zone (buy side).

Yellow line = dealing range midpoint (equilibrium).

Dots on CE lines = midpoints of the latest bullish/bearish FVG.

🔔 Alerts

ICT Buy → Triggers when a bullish setup confirms.

ICT Sell → Triggers when a bearish setup confirms.

You can connect these alerts to:

TradingView notifications.

Webhooks (for brokers or bots like MetaTrader, NinjaTrader, or Discord).

⚙️ Settings

Swing length – how many bars to use when detecting swing highs/lows for the dealing range.

Use PD filter – toggle ON/OFF for requiring discount/premium alignment.

Displacement ATR multiple – how strong the candle body must be compared to ATR to count as a displacement.

ATR length – used for displacement filter.

📈 Supported Markets

Works on all symbols and timeframes.

Commonly applied to:

NASDAQ (NQ, QQQ)

S&P500 (ES, SPX, SPY)

Forex pairs

Crypto (BTC, ETH, etc.)

⚠️ Disclaimer

This bot is for educational purposes only. It does not guarantee profits and should be tested on demo accounts first.

Always apply proper risk management before trading live.

MTF FVG Confluence v6 — JSON Alerts via alert()This strategy combines multi-timeframe confluence with candlestick analysis and fair value gaps (FVGs) to generate structured long/short entries. It aligns Daily and 4H EMA trends with 1H MACD momentum, then confirms with engulfing candles and FVG zones for precision entries. Risk management is built-in, featuring stop-loss, 3R take-profit targets, and optional break-even logic, with dynamic JSON alerts for webhook automation.

Categories:

Candlestick analysis

Chart patterns

Cycles

FlowScope [Hapharmonic]FlowScope: Uncover the Market's True Intent 🔬

Ever wished you could look inside the candles and see where the real action is happening? FlowScope is your microscope for the market's flow, designed to give you a powerful edge by revealing the volume distribution that price action alone can't show you.

Instead of just looking at the open, high, low, and close, FlowScope lets you dive deeper into the market's auction process. It groups candles together and builds a detailed Volume Profile for that period, showing you exactly where the trading happened and revealing the story behind the price action.

Let's explore how you can use it to gain a powerful new edge.

🧐 Core Concept: How It Works

At its heart, FlowScope does three key things:

It Groups Candles: You decide how many candles to group together. For example, setting " Group Candles " to 4 on a 5-minute chart effectively gives you a detailed 20-minute candle and profile. This helps you see the bigger picture and filter out market noise.

It Builds a Volume Profile: For each group, FlowScope analyzes the volume at every single price level. It then displays this as a horizontal histogram (we call this a "footprint" or profile). Longer bars mean more volume was traded at that price, indicating a "fair" price or an area of acceptance. Shorter bars mean price moved through quickly, indicating rejection.

It Creates a Custom "Grouped Candle": To summarize the group's overall price action, FlowScope draws a single, custom candle representing the entire group's:

Open: The open of the first candle in the group.

High: The absolute highest price reached within the group.

Low: The absolute lowest price reached within the group.

Close: The close of the last candle in the group.

This gives you a crystal-clear view of the group's net result, free from the back-and-forth noise of the individual candles inside it.

Below are some of the stunning preset color palettes you can choose from to customize your view:

🚀 How to Use: Practical Applications

FlowScope isn't just for looking pretty; it's a powerful analysis tool. Here are a few ways to integrate it into your trading:

Identify High-Volume Nodes (HVNs): Look for the longest bars in the profile. These are price levels where the market spent the most time and traded the most volume. HVNs often act as powerful "magnets" for price, becoming key areas of support and resistance.

Spot Low-Volume Nodes (LVNs): These are areas with very short bars or gaps in the profile. They represent price levels that the market moved through quickly and inefficiently. If price returns to an LVN, it's likely to move through it quickly again.