Moving Average Rainbow (Stormer)This strategy is based and shown by trader and investor Alexandre Wolwacz "Stormer".

Overview

The strategy uses 12 moving averages (default EMA) to identify trends and generate trading signals opening positions.

Allowing to select the type of moving average and length to be used.

The conditions includes relationship between moving averages, the position of the current price relative to the moving averages, and the occurrence of certain price patterns.

Calculation

The mean moving averages is calculated by adding all the 12 moving averages and dividing by 12, the value is used to help to identify trend and possible condition to open position.

The 12 moving averages is spliced by 3 ranges, initial range (moving average lines 1 to 4), middle range (moving average lines 5 to 8) and end range (moving average lines 9 to 12). These ranges helps to identify potential trend and market turn over.

The moving average touch price is a relationship between the low price (uptrend) or high price (downtrend) with the moving average lines, it identifies where the price (low/high) has reached the the moving average line. Fetching the value to help for opening position, set stop loss and take profit.

Since the stop loss is based and set from the previous moving average touch price value, when position is about to be open and setting the stop loss value, there is a verification to check both current and previous moving average touch price to recalculate the stop loss value.

The turnover trend checks for a possible market turnover event, setting up a new profit target, this setting when enabled is to be helpful when a turnover occurs against the position to exit position with some profit based on highest high price if long or lowest low price if short.

The turnover signal is similar to turnover trend. The difference is that when this setting is enabled and it triggers, it simply exit the current position and opens up a reverse position, long goes short and short goes long. And there is an complement optional that checks current price exit profitable.

Entry Position

Long Position:

Price is higher than the mean moving averages. Meaning possible uptrend.

The lines of the middle range from the moving averages are in increasing order. Meaning possible uptrend.

The current high pierced up previous high.

Fetch the previous value of the moving average touch price. Meaning the low price has touched one of the moving average lines, which that value is conditioning to open position.

Short Position:

Price is lower than the mean moving averages. Meaning possible downtrend.

The lines of the middle range from the moving averages are in decreasing order. Meaning possible downtrend.

The current low pierced down previous low.

Fetch the previous value of the moving average touch price. Meaning the high price has touched one of the moving average lines, which that value is conditioning to open position.

Risk Management

Stop Loss:

The stop loss is based from the previous moving average touch price value, high price for short and low price for long or occurs an verification to check for both current and previous moving average touch price value and a recalculation is done to set the stop loss.

Take Profit:

According to the author, the profit target should be at least 1:1.6 the risk, so to have the strategy mathematically positive.

The profit target is configured input, can be increased or decreased.

It calculates the take profit based on the price of the stop loss with the profit target input.

Turnover Trend

Long Position:

The moving averages initial range lines signals a possible market turnover. Meaning long might be going short.

Fetches the highest high hit since the opening of the position, setting that value to the new profit target.

Short Position:

The moving averages initial range lines signals a possible market turnover. Meaning short might be going long.

Fetches the lowest low hit since the opening of the position, setting that value to the new profit target.

Поиск скриптов по запросу "ha溢价率"

ICT Silver Bullet [LuxAlgo]The ICT Silver Bullet indicator is inspired from the lectures of "The Inner Circle Trader" (ICT) and highlights the Silver Bullet (SB) window which is a specific 1-hour interval where a Fair Value Gap (FVG) pattern can be formed.

When a FVG is formed during the Silver Bullet window, Support & Resistance lines will be drawn at the end of the SB session.

There are 3 different Silver Bullet windows (New York local time):

The London Open Silver Bullet (3 AM — 4 AM ~ 03:00 — 04:00)

The AM Session Silver Bullet (10 AM — 11 AM ~ 10:00 — 11:00)

The PM Session Silver Bullet (2 PM — 3 PM ~ 14:00 — 15:00)

🔶 USAGE

The ICT Silver Bullet indicator aims to provide users a comprehensive display as similar as possible to how anyone would manually draw the concept on their charts.

It's important to use anything below the 15-minute timeframe to ensure proper setups can display. In this section, we are purely using the 3-minute timeframe.

In the image below, we can see a bullish setup whereas a FVG was successfully retested during the Silver Bullet session. This was then followed by a move upwards to liquidity as our target.

Alternatively, you can also see below a bearish setup utilizing the ICT Silver Bullet indicator outlined.

At this moment, the indicator has removed all other FVGs within the Silver Bullet session & has confirmed this FVG as the retested one.

There is also a support level marked below to be used as a liquidity target as per the ICT Silver Bullet concept suggests.

In the below chart we can see 4 separate consecutive examples of bullish & bearish setups on the 3-minute chart.

🔶 CONCEPTS

This technique can visualize potential support/resistance lines, which can be used as targets.

The script contains 2 main components:

• forming of a Fair Value Gap (FVG)

• drawing support/resistance (S/R) lines

🔹 Forming of FVG

1 basic principle: when a FVG at the end of the SB session is not retraced, it will be made invisible.

Dependable on the settings, different FVG's will be shown.

• 'All FVG': all FVG's are shown, regardless the trend

• 'Only FVG's in the same direction of trend': Only FVG's are shown that are similar to the trend at that moment (trend can be visualized by enabling ' Show ' -> ' Trend ')

-> only bearish FVG when the trend is bearish vs. bullish FVG when trend is bullish

• 'strict': Besides being similar to the trend, only FVG's are shown when the closing price at the end of the SB session is:

– below the top of the FVG box (bearish FVG)

– above bottom of the FVG box (bullish FVG)

• 'super-strict': Besides being similar to the trend, only FVG's are shown when the FVG box is NOT broken

in the opposite direction AND the closing price at the end of the SB session is:

– below bottom of the FVG box (bearish FVG)

– above the top of the FVG box (bullish FVG)

' Super-Strict ' mode resembles ICT lectures the most.

🔹 Drawing support/resistance lines

When the SB session has ended, the script draws potential support/resistance lines, again, dependable on the settings.

• Previous session (any): S/R lines are fetched between current and previous session.

For example, when current session is ' AM SB Session (10 AM — 11 AM) ', then previous session is

' London Open SB (3 AM — 4 AM) ', S/R lines between these 2 sessions alone will be included.

• Previous session (similar): S/R lines are fetched between current and previous - similar - session.

For example, when current session is ' London Open SB (3 AM — 4 AM)' , only S/R lines between

current session and previous ' London Open SB (3 AM — 4 AM) ' session are included.

When a new session starts, S/R lines will be removed, except when enabling ' Keep lines (only in strict mode) '

This is not possible in ' All FVG ' or ' Only FVG's in the same direction of trend ' mode, since the chart would be cluttered.

Note that in ' All FVG ' or ' Only FVG's in the same direction of trend ' mode, both, Support/Resistance lines will be shown,

while in Strict/Super-Strict mode:

• only Support lines will be shown if a bearish FVG appears

• only Resistance lines if a bullish FVG is shown

The lines will still be drawn the the end of the SB session, when a valid FVG appears,

but the S/R lines will remain visible and keep being updated until price reaches that line.

This publication contains a "Minimum Trade Framework (mTFW)", which represents the best-case expected price delivery, this is not your actual trade entry - exit range.

• 40 ticks for index futures or indices

• 15 pips for Forex pairs.

When on ' Strict/Super-Strict ' mode, only S/R lines will be shown which are:

• higher than the lowest FVG bottom + mTFW, in a bullish scenario

• lower than the highest FVG bottom - mTFW, in a bearish scenario

When on ' All FVG/Only FVG's in the same direction of trend ' mode, or on non-Forex/Futures/Indices symbols, S/R needs to be higher/lower than SB session high/low.

🔶 SETTINGS

(Check CONCEPTS for deeper insights and explanation)

🔹 Swing settings (left): Sets the length, which will set the lookback period/sensitivity of the Zigzag patterns (which directs the trend)

🔹 Silver Bullet Session; Show SB session: show lines and labels of SB session

Labels can be disabled separately in the ' Style ' section, color is set at the ' Inputs ' section.

🔹 FVG

– Mode

• All FVG

• Only FVG's in the same direction of trend

• Strict

• Super-Strict

– Colors

– Extend: extend till last bar of SB session

🔹 Targets – support/resistance lines

– Previous session (any): S/R lines fetched between current and previous SB session

– Previous session (similar): S/R lines fetched between current and previous similar SB session

– Colors

– Keep lines (only in strict mode)

🔹 Show

– MSS ~ Session: Show Market Structure Shift , only when this happens during a SB session

– Trend: Show trend (Zigzag, colored ~ trend)

Evolution Fractals with IBA standard fractal high has two lower high (or equal high) candles to its left and right.

For standard fractal low fractals this is vice versa.

-But this indicator plots has the option to plot standard fractals only after candle close is confirmed.

So if the current candle is still forming in live markets, only after this candle has fully closed, then the indicator checks if the fractal is valid and then plotted.

You can select this option On or Off

(with the standard fractal indicator there is a fractal plotted, but when this candle high (or low ) is broken again, the fractal disappears. This re-painting of fractals can cause confusion.

-Added an alert functionality.

When setting an alert on your chart, you can select this indicator to alert you upon the forming of a new fractal high or low.

-Added optional Inside Bar function.

When a candle High/Low does not breach the previous candle High/Low, then a different body color can be shown.

This is particular handy to quickly if this high/low is breached, without having to zoom in on the chart.

ATR GOD Strategy by TradeSmart (PineConnector-compatible)This is a highly-customizable trading strategy made by TradeSmart, focusing mainly on ATR-based indicators and filters. The strategy is mainly intended for trading forex , and has been optimized using the Deep Backtest feature on the 2018.01.01 - 2023.06.01 interval on the EUR/USD (FXCM) 15M chart, with a Slippage value of 3, and a Commission set to 0.00004 USD per contract. The strategy is also made compatible with PineConnector , to provide an easy option to automate the strategy using a connection to MetaTrader. See tooltips for details on how to set up the bot, and check out our website for a detailed guide with images on how to automate the strategy.

The strategy was implemented using the following logic:

Entry strategy:

A total of 4 Supertrend values can be used to determine the entry logic. There is option to set up all 4 Supertrend parameters individually, as well as their potential to be used as an entry signal/or a trend filter. Long/Short entry signals will be determined based on the selected potential Supertrend entry signals, and filtered based on them being in an uptrend/downtrend (also available for setup). Please use the provided tooltips for each setup to see every detail.

Exit strategy:

4 different types of Stop Losses are available: ATR-based/Candle Low/High Based/Percentage Based/Pip Based. Additionally, Force exiting can also be applied, where there is option to set up 4 custom sessions, and exits will happen after the session has closed.

Parameters of every indicator used in the strategy can be tuned in the strategy settings as follows:

Plot settings:

Plot Signals: true by default, Show all Long and Short signals on the signal candle

Plot SL/TP lines: false by default, Checking this option will result in the TP and SL lines to be plotted on the chart.

Supertrend 1-4:

All the parameters of the Supertrends can be set up here, as well as their individual role in the entry logic.

Exit Strategy:

ATR Based Stop Loss: true by default

ATR Length (of the SL): 100 by default

ATR Smoothing (of the SL): RMA/SMMA by default

Candle Low/High Based Stop Loss: false by default, recent lowest or highest point (depending on long/short position) will be used to calculate stop loss value. Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier.

Candle Lookback (of the SL): 50 by default

Percentage Based Stop Loss: false by default, Set the stop loss to current price - % of current price (long) or price + % of current price (short).

Percentage (of the SL): 0.3 by default

Pip Based Stop Loss: Set the stop loss to current price - x pips (long) or price + x pips (short). Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier.

Pip (of the SL): 10 by default

Base Risk Multiplier: 4.5 by default, the stop loss will be placed at this risk level (meaning in case of ATR SL that the ATR value will be multiplied by this factor and the SL will be placed that value away from the entry level)

Risk to Reward Ratio: 1.5 by default, the take profit level will be placed such as this Risk/Reward ratio is met

Force Exiting:

4 total Force exit on custom session close options: none applied by default. If enabled, trades will close automatically after the set session is closed (on next candle's open).

Base Setups:

Allow Long Entries: true by default

Allow Short Entries: true by default

Order Size: 10 by default

Order Type: Capital Percentage by default, allows adjustment on how the position size is calculated: Cash: only the set cash amount will be used for each trade Contract(s): the adjusted number of contracts will be used for each trade Capital Percentage: a % of the current available capital will be used for each trade

ATR Limiter:

Use ATR Limiter: true by default, Only enter into any position (long/short) if ATR value is higher than the Low Boundary and lower than the High Boundary.

ATR Limiter Length: 50 by default

ATR Limiter Smoothing: RMA/SMMA by default

High Boundary: 1000 by default

Low Boundary: 0.0003 by default

MA based calculation: ATR value under MA by default, If not Unspecified, an MA is calculated with the ATR value as source. Only enter into position (long/short) if ATR value is higher/lower than the MA.

MA Type: RMA/SMMA by default

MA Length: 400 by default

Waddah Attar Filter:

Explosion/Deadzone relation: Not specified by default, Explosion over Deadzone: trades will only happen if the explosion line is over the deadzone line; Explosion under Deadzone: trades will only happen if the explosion line is under the deadzone line; Not specified: the opening of trades will not be based on the relation between the explosion and deadzone lines.

Limit trades based on trends: Not specified by default, Strong Trends: only enter long if the WA bar is colored green (there is an uptrend and the current bar is higher then the previous); only enter short if the WA bar is colored red (there is a downtrend and the current bar is higher then the previous); Soft Trends: only enter long if the WA bar is colored lime (there is an uptrend and the current bar is lower then the previous); only enter short if the WA bar is colored orange (there is a downtrend and the current bar is lower then the previous); All Trends: only enter long if the WA bar is colored green or lime (there is an uptrend); only enter short if the WA bar is colored red or orange (there is a downtrend); Not specified: the color of the WA bar (trend) is not relevant when considering entries.

WA bar value: Not specified by default, Over Explosion and Deadzone: only enter trades when the WA bar value is over the Explosion and Deadzone lines; Not specified: the relation between the explosion/deadzone lines to the value of the WA bar will not be used to filter opening trades.

Sensitivity: 150 by default

Fast MA Type: SMA by default

Fast MA Length: 10 by default

Slow MA Type: SMA

Slow MA Length: 20 by default

Channel MA Type: EMA by default

BB Channel Length: 20 by default

BB Stdev Multiplier: 2 by default

Trend Filter:

Use long trend filter 1: false by default, Only enter long if price is above Long MA.

Show long trend filter 1: false by default, Plot the selected MA on the chart.

TF1 - MA Type: EMA by default

TF1 - MA Length: 120 by default

TF1 - MA Source: close by default

Use short trend filter 1: false by default, Only enter long if price is above Long MA.

Show short trend filter 1: false by default, Plot the selected MA on the chart.

TF2 - MA Type: EMA by default

TF2 - MA Length: 120 by default

TF2 - MA Source: close by default

Volume Filter:

Only enter trades where volume is higher then the volume-based MA: true by default, a set type of MA will be calculated with the volume as source, and set length

MA Type: RMA/SMMA by default

MA Length: 200 by default

Date Range Limiter:

Limit Between Dates: false by default

Start Date: Jan 01 2023 00:00:00 by default

End Date: Jun 24 2023 00:00:00 by default

Session Limiter:

Show session plots: false by default, show market sessions on chart: Sidney (red), Tokyo (orange), London (yellow), New York (green)

Use session limiter: false by default, if enabled, trades will only happen in the ticked sessions below.

Sidney session: false by default, session between: 15:00 - 00:00 (EST)

Tokyo session: false by default, session between: 19:00 - 04:00 (EST)

London session: false by default, session between: 03:00 - 11:00 (EST)

New York session: false by default, session between: 08:00 - 17:00 (EST)

Trading Time:

Limit Trading Time: true by default, tick this together with the options below to enable limiting based on day and time

Valid Trading Days Global: 123567 by default, if the Limit Trading Time is on, trades will only happen on days that are present in this field. If any of the not global Valid Trading Days is used, this field will be neglected. Values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) To trade on all days use: 123457

(1) Valid Trading Days: false, 123456 by default, values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) The script will trade on days that are present in this field. Please make sure that this field and also (1) Valid Trading Hours Between is checked

(1) Valid Trading Hours Between: false, 1800-2000 by default, hours between which the trades can happen. The time is always in the exchange's timezone

All other options are also disabled by default

PineConnector Automation:

Use PineConnector Automation: false by default, In order for the connection to MetaTrader to work, you will need do perform prerequisite steps, you can follow our full guide at our website, or refer to the official PineConnector Documentation. To set up PineConnector Automation on the TradingView side, you will need to do the following:

1. Fill out the License ID field with your PineConnector License ID;

2. Fill out the Risk (trading volume) with the desired volume to be traded in each trade (the meaning of this value depends on the EA settings in Metatrader. Follow the detailed guide for additional information);

3. After filling out the fields, you need to enable the 'Use PineConnector Automation' option (check the box in the strategy settings);

4. Check if the chart has updated and you can see the appropriate order comments on your chart;

5. Create an alert with the strategy selected as Condition, and the Message as {{strategy.order.comment}} (should be there by default);

6. Enable the Webhook URL in the Notifications section, set it as the official PineConnector webhook address and enjoy your connection with MetaTrader.

License ID: 60123456789 by default

Risk (trading volume): 1 by default

NOTE! Fine-tuning/re-optimization is highly recommended when using other asset/timeframe combinations.

ICT TGIF_V2 [MK]The ICT T.G.I.F (Thank God Its Friday) works on the following strategy:

1. Friday makes the High/Low of the Week.

2. The Weekly High/Low range is used to calculate 20-30% levels. (see chart above)

3. Trades are taken in the Friday PM session (NY EST) with the idea that price may retrace to the 20-30% level.

The indicator plots the following levels:

1. Week High

2. Week Low

3. Week Open

3. 20-30% level in upper part of weekly range (only shows if Friday has made the high of the week)

4. 20-30% level in lower part of weekly range (only shows if Friday has made the low of the week)

It is possible to show all historical levels listed above for the purpose of back-testing the TGIF strategy.

Also it is possible to disable all the historical and current levels, in which case only the 20-30% levels will show when Friday has made the Week High/Low (the 20-30% level only shows from 1200-1600 on Friday to keep charts as clean as possible.

Users of this script, and any script for that matter, should always do proper back-testing before taking any trades.

Many thanks should be given to ICT (The Inner Circle Trader) for bringing this strategy to the trading community.

Below shows indicator with all levels turned ON

Below shows indicator with all levels turned OFF (this allows for cleaner charts)

Ultimate Customizable EMA/SMAI know, not another EMA indicator, but I promise, I will make it worth your while!

About this indicator:

This is an EMA indicator, plain and simple. But its ultimate! And its ultimate in the sense that I have made it vastly customizable.

I made this indicator as a boring, single line indicator that would allow me to toggle to whichever EMA / SMA I wanted on whatever timeframe I wanted, because with the currently available EMAs and SMAs (and there are tons of them), I could never seem to get one with the precise settings I wanted.

Then I realized, if I struggled with this, chances are other people may be struggling with this. And also chances are not everyone is great with coding things quickly and it may be out of reach for those to code something specific to their individual needs and desires.

So this indicator is meant for those who, like me, may have very specific tastes for their EMA indicator and want to be able to tailor it right down to a T of what they want, but maybe don't have the skills to code things specifically the way they would like it.

So what can I do with it?

Well, you can do really whatever you want. I have made absolutely everything possible customizable, right down to the size of the plotted line (you can adjust the width of the line to make it more or less visible). But let me give you a list of the functions permitted for this indicator:

1. Toggle between an EMA or SMA: The indicator will default to show the EMA. However, you can toggle between an EMA or SMA, depending on your preference.

2. Add 2 EMA's or SMAs: The indicator permits up to 2 EMA's to be added. Both of which can be either EMA or SMA and operate independently (you can have one as EMA and the other as SMA, both as SMA or whatever combination thereof).

3. Specify your timeframes: Each EMA/SMA can have an individual timeframe. If you want to plot 2, 200 EMA's on your chart, 1 on the 5 minute chart and the other on the 1 Day chart, you can do it! The indicator will permit you to individually select which timeframe you want for both of the available EMAs/SMAs. They can both be on separate timeframes.

4. Specify your sources: In addition to both being able to be on separate timeframes, both can also be on separate sources. You can have the 200 EMA of the close price as well as the 200 EMA of the high or low price. The indicator will permit you to specify your preferred sources.

5. Plot Standard Deviation bands: You can plot the standard deviation bands of the primary EMA/SMA (this is only available on the primary EMA/SMA and not both). You can also specify the length of the standard deviation bands that can operate independently of the primary EMA/SMA. So if you have the 50 EMA but want the 200 standard deviation bands, you can do so and specify this in the data inputs.

6. Customize your alerts: The indicator provides 6 pre-programmed condition alerts that are applied to both the primary, secondary and both EMAs. This way, you can customize various alerts based on various conditions you want to look for.

7. Plot crossover / crossunder arrows: The indicator will allow you to request it to plot triangles to signal crossovers and crossunders. This can be toggled on and off based on your visual preference.

8. Provides demographic information: The EMA will provide basic demographic information about the stock's behaviour around the EMA/SMA. This is displayed in a table at the top right of the chart. It will tell you the number of touches a stock has with its various EMA/SMAs, how many closes it has had above or below the EMA/SMA (for example, a bullish ticker should have more closes above an EMA than below it and inverse for bearish), how many times the close price has crossed over or crossed under the two EMA/SMAs and how many time the EMA/SMAs have crossed over and crossed under each other. This all gives an idea of the relative strength and sentiment of a stock in a quantitative way. The length of the lookback period is customizable individually for each EMA/SMA. If you want to look back 100, 200, 500 or just 75 candles, you can specify. You can also toggle on and off each or both tables as you desire.

Final thoughts:

The indicator was meant to tailor to my general need to toggle between very specific EMAs and SMAs to gauge averages. I generally will look at various EMAs and SMAs to calculate various things and I never specifically rely on a single EMA and SMA. Its annoying having to switch between multiple indicators and I always ended up opening pinescript and coding in what exactly I wanted to look at. This was meant to stop me from having to constantly code something specifically each time I wanted very specific information and I felt like I should share it with the community, as if I find it helpful and useful, I hope others will, too!

Hopefully you find it helpful and useful and as always leave your suggestions below!

Logarithmic VolatilityIntroducing the Logarithmic Volatility Indicator , an innovative trading indicator designed especially for trading in low volatility markets. This powerful indicator is aimed at traders of all levels, from beginners to experts, and is based on fundamental concepts of mathematics and statistics applied to the financial market. Its main objective is to provide you with a better understanding of price movements and help you make more accurate investment decisions, especially in low volatility environments.

The purpose of this indicator is to find a volatility estimator that depends on the difference between High and Low, taking into account that this measure is directly proportional to volatility. A first result was obtained by Parkinson (1980) which was later improved by Garman and Klass (1980), who improved the estimator by obtaining one of minimum variance. It is the simplified version (and recommended by them) of the Garman and Klass estimator that is used to calculate the daily volatility of the asset.

The Logarithmic Volatility Indicator is a unique smoothing indicator that uses logarithms and volatility calculation of the opening, high, low and closing prices. It combines these elements to obtain an accurate representation of market volatility in situations where volatility is low.

Features

This indicator has several outstanding features designed to enhance your trading analysis in low volatility environments:

• Intraday Volatility Calculation: This innovative feature allows you to view market volatility levels in real time, providing a clear view of market fluctuations even when volatility is low.

• EMA (Exponential Moving Average) Multi Length: The indicator incorporates three different EMA lengths (Fast, Medium and Slow). This gives you a deeper and more detailed analysis of market volatility, allowing you to detect subtle changes in volatility and make more accurate predictions.

• Visual color change: The indicator uses a color change between green and red to facilitate quick interpretation of the market. Green indicates a decrease in volatility, while red indicates an increase in volatility. This feature helps you quickly identify changes in market dynamics even in periods of low volatility.

• Histogram display: In addition to the colors, the indicator can also be displayed as a histogram. This intuitive representation allows you to visually observe changes in volatility over time and detect emerging patterns or trends in markets with low volatility.

Settings

The Logarithmic Volatility Indicator allows you to customize various settings to suit your specific trading needs:

• Slow EMA length: you can select the length of the slow exponential moving average according to your preferences and trading strategies.

• Fast EMA length: Similarly, you can choose the length of the fast exponential moving average to suit your trading style.

• Average EMA length: In addition to the two EMA lengths above, this indicator offers a third EMA length for even more detailed analysis. This additional feature is especially useful when trading in markets with low volatility, as it allows you to capture subtle changes in market dynamics.

Trading

The Logarithmic Volatility Indicator is designed not only to provide you with essential information about market volatility, but also to give you clear indications on when to trade. Here's how you can use the indicator's colors to guide your trading decisions:

- Long Trading: When the fast EMA has a smaller value than the slow EMA, the indicator will change to green. This is a signal to enter a long trade. That is, you can consider buying at this point, as an increase in price is anticipated due to decreasing volatility. With volatility declining, there is a greater likelihood that the price will continue in the current direction rather than fluctuate erratically.

- b]Short Trading: On the other hand, when the fast EMA has a higher value than the slow EMA, the indicator will turn red. This is a signal to enter a short trade. In other words, you may consider selling at this point, as a decline in price is anticipated due to rising volatility. With volatility on the rise, there is a greater risk of steeper price fluctuations.

It is important to remember that, as with any indicator, the Logarithmic Volatility Indicator does not guarantee 100% success. You should always use this indicator in combination with other analytical tools and good risk management. This tool provides you with an overview of market volatility and can help you identify trading opportunities in low volatility markets, but the final decision on when and how to trade should always be based on your own analysis and judgment.

In conclusion, the Logarithmic Volatility Indicator is an essential trading tool that every trader should have in their arsenal, especially when facing low volatility markets. With its accurate volatility calculation and easy-to-understand visualization, it will help you improve your trading decisions and maximize your profits even in situations where price movements are less pronounced. Try it today and take advantage of its efficiency in low volatility environments!

---------------------------------------------------------------------------------------------------

Presentamos el Indicador de Volatilidad Logarítmica , un innovador indicador de trading diseñado especialmente para operar en mercados con baja volatilidad. Este poderoso indicador está dirigido a traders de todos los niveles, desde principiantes hasta expertos, y se basa en conceptos fundamentales de matemáticas y estadísticas aplicadas al mercado financiero. Su objetivo principal es proporcionarte una mejor comprensión de los movimientos de precios y ayudarte a tomar decisiones de inversión más precisas, especialmente en entornos de baja volatilidad.

Con este indicador se pretende encontrar un estimador de la volatilidad que dependa de la diferencia entre el High y el Low, teniendo en cuenta que esta medida es directamente proporcional a la volatilidad. Un primer resultado fue obtenido por Parkinson (1980) que posteriormente fue mejorado por Garman y Klass (1980), que mejoraron el estimador obteniendo uno de varianza mínima. Es la versión simplificada (y recomendada por ellos mismos) del estimador de Garman y Klass la que se utiliza para calcular la volatilidad diaria del activo.

El Indicador de Volatilidad Logarítmica es un indicador de suavizado único que utiliza logaritmos y el cálculo de la volatilidad de los precios de apertura, máximo, mínimo y cierre. Combina estos elementos para obtener una representación precisa de la volatilidad del mercado en situaciones donde la volatilidad es baja.

Características

Este indicador cuenta con varias características sobresalientes diseñadas para mejorar tu análisis de trading en entornos de baja volatilidad:

• Cálculo de la volatilidad intradía: Esta función innovadora te permite ver los niveles de volatilidad del mercado en tiempo real, lo que brinda una visión clara de las fluctuaciones del mercado incluso cuando la volatilidad es baja.

• EMA (Exponential Moving Average) Multi Longitud: El indicador incorpora tres longitudes diferentes de EMA (Rápida, Media y Lenta). Esto te proporciona un análisis más profundo y detallado de la volatilidad del mercado, permitiéndote detectar cambios sutiles en la volatilidad y realizar predicciones más precisas.

• Cambio de color visual: El indicador utiliza un cambio de color entre verde y rojo para facilitar la interpretación rápida del mercado. El verde indica una disminución de la volatilidad, mientras que el rojo indica un aumento de la volatilidad. Esta característica te ayuda a identificar rápidamente cambios en la dinámica del mercado incluso en períodos de baja volatilidad.

• Visualización Histograma: Además de los colores, el indicador también se puede visualizar como un histograma. Esta representación intuitiva te permite observar de manera visual los cambios en la volatilidad a lo largo del tiempo y detectar patrones o tendencias emergentes en mercados con baja volatilidad.

Ajustes

El Indicador de Volatilidad Logarítmica te permite personalizar varios ajustes para adaptarlos a tus necesidades de trading específicas:

• Longitud de EMA lenta: Puedes seleccionar la longitud de la media móvil exponencial lenta según tus preferencias y estrategias de trading.

• Longitud de EMA rápida: De manera similar, puedes elegir la longitud de la media móvil exponencial rápida para ajustarla a tu estilo de trading.

• Longitud de EMA media: Además de las dos longitudes de EMA anteriores, este indicador ofrece una tercera longitud de EMA para un análisis aún más detallado. Esta característica adicional es especialmente útil cuando operas en mercados con baja volatilidad, ya que te permite capturar cambios sutiles en la dinámica del mercado.

Operativa

El Indicador de Volatilidad Logarítmica está diseñado no solo para brindarte información esencial sobre la volatilidad del mercado, sino también para ofrecerte indicaciones claras sobre cuándo operar. Aquí te explicamos cómo puedes utilizar los colores del indicador para guiar tus decisiones de trading:

• Operativa en Largo: Cuando la EMA rápida tiene un valor más pequeño que la EMA lenta, el indicador cambiará a color verde. Esta es una señal para entrar en una operación en largo. Es decir, puedes considerar comprar en este punto, ya que se anticipa un aumento en el precio debido a la disminución de la volatilidad. Con la volatilidad en descenso, existe una mayor probabilidad de que el precio continúe en la dirección actual en lugar de fluctuar erráticamente.

• Operativa en Corto: Por otro lado, cuando la EMA rápida tiene un valor mayor que la EMA lenta, el indicador se tornará rojo. Esta es una señal para entrar en una operación en corto. En otras palabras, puedes considerar vender en este punto, ya que se anticipa una disminución en el precio debido al aumento de la volatilidad. Con la volatilidad en ascenso, existe un mayor riesgo de fluctuaciones de precio más pronunciadas.

Es importante recordar que, como con cualquier indicador, el Indicador de Volatilidad Logarítmica no garantiza un éxito del 100%. Siempre debes usar este indicador en combinación con otras herramientas de análisis y una buena gestión de riesgos. Esta herramienta te proporciona una visión general de la volatilidad del mercado y puede ayudarte a identificar oportunidades de trading en mercados con baja volatilidad, pero la decisión final de cuándo y cómo operar siempre deberá basarse en tu propio análisis y juicio.

En conclusión, el Indicador de Volatilidad Logarítmica es una herramienta de trading esencial que todo trader debe tener en su arsenal, especialmente cuando se enfrenta a mercados con baja volatilidad. Con su cálculo preciso de la volatilidad y su visualización fácil de entender, te ayudará a mejorar tus decisiones de trading y a maximizar tus ganancias incluso en situaciones donde los movimientos de precios son menos pronunciados. ¡Pruébalo hoy mismo y aprovecha su eficiencia en entornos de baja volatilidad!

AIAE IndicatorAggregate (or Average) Investor Allocation to Equities.

When it comes to predicting long-term equity returns, several well-known indicators come to mind—for example, the CAPE ratio, Tobin’s Q, and Market Cap to GDP, to name a few.

Yet there is another indicator without nearly as high of a profile that has outperformed the aforementioned indicators significantly when it comes to both forecasting and tactical asset allocation.

That indicator, known as the Aggregate (or Average) Investor Allocation to Equities (AIAE), was developed by the pseudonymous financial pundit, Jesse Livermore, and published on his blog in 2013.

In an essay titled, “The Single Greatest Predictor of Future Stock Market Returns,” Livermore makes the case that the primary driver of long-term equity returns is not valuation, but rather the supply of equities relative to the combined supply of bonds and cash.

Accordingly, the AIAE is computed by taking the total market value of equities and dividing by the sum of a) the total market value of equities, b) the total market value of bonds, and c) the total amount of cash available to investors (i.e., that in circulation plus bank deposits):

This ratio gives the market-wide allocation to equities (or, equivalently, the average investor allocation to equities weighted by portfolio size). (Note that every share of stock, every bond, and every unit of cash in existence must be held in some portfolio somewhere at all times.)

Livermore explains that, in practice, the total market value of bonds plus cash can be estimated by the total liabilities held by the five classes of economic borrowers: Households, Non-Financial Corporations, State and Local Governments, the Federal Government, and the Rest of the World.

This follows from the fact that if these entities borrow directly from investors, new bonds are created. Whereas, if they borrow directly from banks, new bank deposits (cash) are created.

As the economy grows, the supply of bonds and cash steadily increases. Historically, the rate of increase of the supply of bonds and cash has been about 7.5% per annum. Consequently, if the market portfolio is to maintain the same allocation to equities, the supply of equities must increase at the exact same rate.

The supply of equities can increase either by new equity issuance or by price increases. Historically, net new equity issuance has been negligible (with issuances being offset by buybacks and acquisitions). Thus, in order for equities not to become an ever-smaller portion of the average investor’s portfolio, the price of stocks must rise over the long-term.

While we often hear that stock prices follow earnings, in the 1980s earnings fell slightly from the beginning of the decade to the end of the decade, yet stocks rose at an annualized rate of 17% during that time. How could this be?

Well, at the beginning of the decade the average investor’s portfolio had a 25% allocation to equities. During the decade, the supply of bonds and cash rose strongly. If the price of equities had not risen, the average investor’s allocation to equities would have fallen to a mere 13% (as the supply of cash and bonds grew). Thus, equities had no choice but to rise despite the fall in earnings.

Super Secret 200 EMAThe indicator is called "Super Secret 200 EMA." It combines two technical indicators, the Supertrend and the 200 Exponential Moving Average (EMA), to generate buy and sell opportunities in a trading chart.

Here's how the indicator works and how you can use it:

Supertrend Calculation:

The Supertrend indicator helps identify the current trend in the market. It uses two parameters: Length and Multiplier.

Length: This parameter determines the number of periods used for the calculation.

Multiplier: It controls the width of the Supertrend line, indicating the level of volatility considered in the calculation.

The Supertrend is calculated by looping through the historical data from length to 1.

For each period, it checks whether the closing price has increased or decreased compared to the previous period.

If the closing price has increased, it updates the highestHigh value with the maximum of the current highest high and the high of the current period.

If the closing price has decreased, it updates the lowestLow value with the minimum of the current lowest low and the low of the current period.

Finally, it calculates the Supertrend value using the following formula:

If the change in the closing price is positive: Supertrend = lowestLow + (multiplier * Average True Range (ATR))

If the change in the closing price is negative: Supertrend = highestHigh - (multiplier * ATR)

The Supertrend line will be green if it is above the 200 EMA line and red if it is below.

200 EMA Calculation:

The 200 EMA is a widely used moving average indicator that gives more weight to recent prices.

The EMA period is set to 200 in this case.

The 200 EMA is calculated using the EMA formula, taking into account the closing prices over the specified period.

Plotting:

The Supertrend and 200 EMA lines are plotted on the chart using the plot function.

The Supertrend line is colored green if it is above the 200 EMA line and red if it is below.

The 200 EMA line is colored green if the closing price is above it and red if it is below.

Buy and Sell Conditions:

The indicator determines the buy and sell conditions based on the crossover and crossunder of the closing price with the 200 EMA line and the Supertrend line.

Buy Condition: A buy signal is generated when the closing price crosses above the 200 EMA line and is also above the Supertrend line.

Sell Condition: A sell signal is generated when the closing price crosses below the 200 EMA line and is also below the Supertrend line.

Plotting Buy and Sell Signals:

You can use this indicator to identify potential buy and sell opportunities in your trading strategy. However, please note that this is a simplified explanation, and it's essential to thoroughly understand the indicator's principles and backtest it with historical data before relying on it for actual trading decisions.

Use this with other confluences for best results and never rely on a single indicator

4H RangeThis script visualizes certain key values based on a 4-hour timeframe of the selected market on the chart. These values include the High, Mid, and Low price levels during each 4-hour period.

These levels can be helpful to identify inside range price action, chop, and consolidation. They can sometimes act as pivots and can be a great reference for potential entries and exits if price continues to hold the same range.

Here's a step-by-step overview of what this indicator does:

1. Inputs: At the beginning of the script, users are allowed to customize some inputs:

Choose the color of lines and labels.

Decide whether to show labels on the chart.

Choose the size of labels ("tiny", "small", "normal", or "large").

Choose whether to display price values in labels.

Set the number of bars to offset the labels to the right.

Set a threshold for the number of ticks that triggers a new calculation of high, mid, and low values.

* Tick settings may need to be increased on equity charts as one tick is usually equal to one cent.

For example, if you want to clear the range when there is a close one point/one dollar above or below the range high/low then on ES

that would be 4 ticks but one whole point on AAPL would be 100 ticks. 100 ticks on an equity chart may or may not be ideal due to

different % change of 100 ticks might be too excessive depending on the price per share.

So be aware that user preferred thresholds can vary greatly depending on which chart you're using.

2. Retrieving Price Data: The script retrieves the high, low, and closing price for every 4-hour period for the current market.

The script also calculates the mid-price of each 4-hour period (the average of the high and low prices).

3. Line Drawing: At the start of the script (first run), it draws three lines (high, mid, and low) at the levels corresponding to the high,

mid, and low prices. Users can also change transparency settings on historical lines to view them. Default setting for historical lines

is for them to be hidden.

4. Updating Lines and Labels: For each subsequent 4-hour period, the script checks whether the close price of the period has gone

beyond a certain threshold (set by user input) above the previous high or below the previous low. If it has, the script deletes the

previous lines and labels, draws new lines at the new high, mid, and low levels, and creates new labels (if the user has opted to

show labels).

5. Displaying Values in the Data Window: In addition to the visual representation on the chart, the script also plots the high, mid, and

low prices. These plotted values appear in the Data Window of TradingView, allowing users to see the exact price levels even when

they're not directly labeled on the chart.

6. Updating Lines and Labels Position: At the end of each period, the script moves the lines and labels (if they're shown) to the right,

keeping them aligned with the current period.

Please note: This script operates based on a 4-hour timeframe, regardless of the timeframe selected on the chart. If a shorter timeframe is selected on the chart, the lines and labels will appear to extend across multiple bars because they represent 4-hour price levels. If a longer timeframe is selected, the lines and labels may not accurately represent high, mid, and low levels within that longer timeframe.

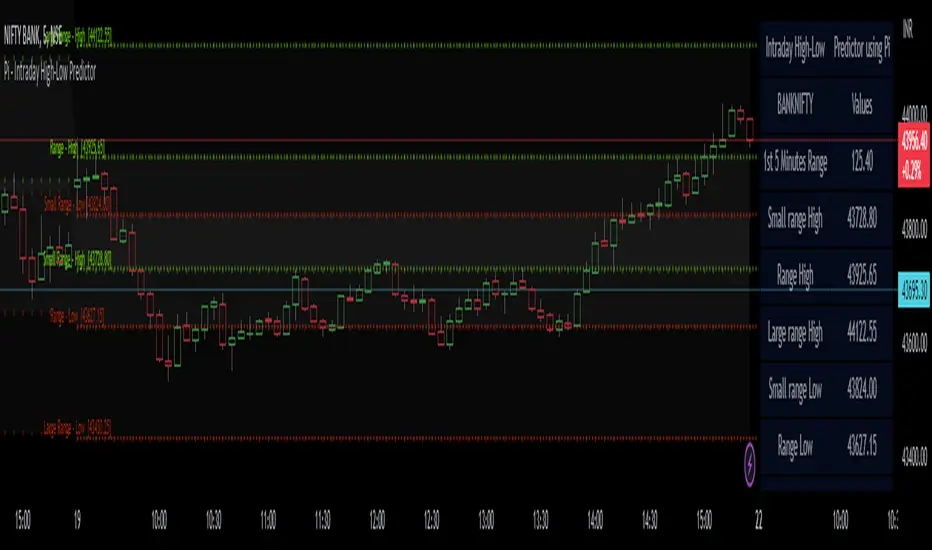

Pi - Intraday High-Low Predictor

Pi - Intraday High-Low Predictor

This is not my Strategy/Research , I've just coded it into a indicator.

I found it interesting & useful so I'm sharing it here.

This Strategy/Research is by Kshirod Chandra Mohanty ( y-o-u-t-u-b-e : Trade with IITIAN )

You can watch his video on y-o-u-t-u-b-e for more info on this one.

the video has following title :

"1Cr Paid Strategy For Free || 10000 Subscribers Special Giveaway || How to find Day High or Low"

This will not tell you which is day high or day low, but it will help you to predict the day high from a day low and day low from a day high.

It will give you a possible range to which the prices could move to.

He has explained/used this on Banknifty.

How to Find out Day High from Day Low & Day Low from Day High :-

He uses the value of Pi (3.14) and the Range of 1st 5minute candle to find out the possible highs from day low and the possible lows from day high.

Range = value of Pi * 1st 5minutes Range

Small range = Range / 2

Large range = Range + Small range

so to find out the possible lows from day high we do following calculations

Small range low = day high - Small range

Range low = day high - Range

Large range low = day high - Large range

and to find out the possible highs from day low we do following calculations

Small range high = day low + Small range

Range high = day low + Range

Large range high = day low + Large range

Note :- This Indicator does Repaint in following ways,

As the script uses the Day High to predict the possible lows ,

so if it's an up-trending day and price keeps on making new High's then the ranges for lows will keep on changing.

similarly the script uses the Day Low to predict the possible high's ,

so if it's an down-trending day and price keeps on making new Low's then the ranges for highs will keep on changing.

My observations / thoughts about this :-

This script does not provide buy/sell recommendations. it just provides possible ranges to where prices can go from Day-High & Day-Low.

It's better to avoid trading when the price is trading between the Small range high & Small range low levels.

As it has high probability that it will be a range bound day and price will stay in between those two levels.

There is a high probability that it will be a trending day if price breaks either the Small range high/low ,

then the price could move to Range low/high.

If price breaks from Range High/Low then there is a high probability that it will be a trending day and the price could move to Large Range low/high.

Note :- If you want to use this on instruments/scripts/indexes which are active for large session such as forex/cryptos , then i suggest that you use the Opening Range period of 4Hours i.e 240minutes, to get better results.

using the default setting of 5minutes will not give good results on them.

play around with this value to find out which one suits that instrument/script/index the best.

Don't trust these levels blindly, do backtest or live testing of this then use for real trade if you want.

Use Price action near these levels to make any trading decision's.

The script provides following options :

1. Option to display Ranges in a Table (which you can enable/hide as you wish)

You can set the Table's location, size , background color & text color according to your preference.

2. Option to enable/hide Predicted-Highs from Day-Low on chart.

3. Option to enable/hide Predicted-Lows from Day-High on chart.

4. Option to set the Opening range period - here you can select your preferred opening range for calculation purpose.

5. Option to enable/hide historical levels on chart.

6. Options to customize the colors & line styles for lines.

7. Options to customize the colors , position & size for labels.

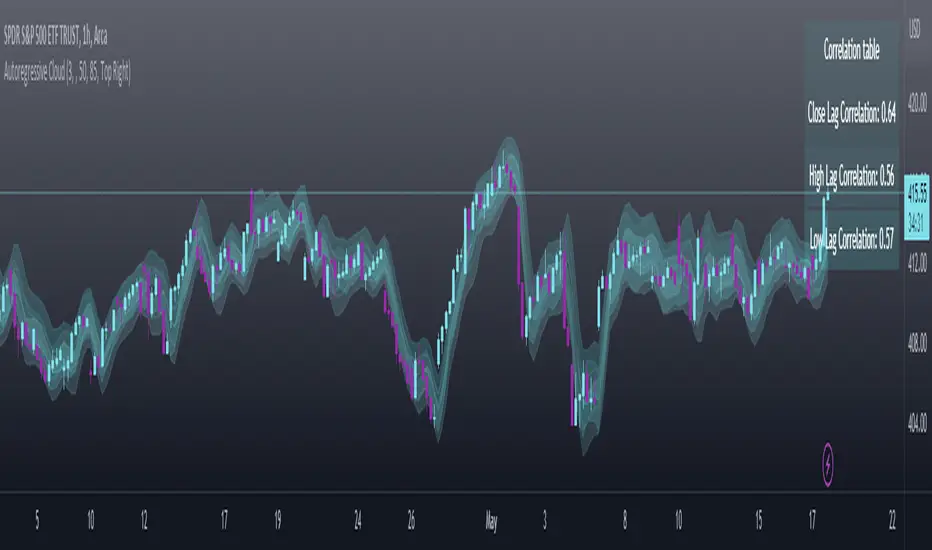

Autoregressive CloudHello,

I am releasing this indicator called the Autoregressive Cloud Indicator.

What it does:

The indicator performs an autoregression analysis on 3 price variables of a ticker, those being the High, the Low and the Close. It uses a 1-lag system and looks back at the previous close, high and low’s effect on the proceeding high, low and close. It then plots out the anticipated range for the ticker based on the autoregression analysis, as well as displays the lag-correlation (autocorrelation) in a table.

What is Autoregression analysis?

Autoregression is a modelling technique used to describe a time series based on its own past values. It assumes that the current value of a variable is a linear combination of its previous values and a random error term.

And what is autocorrelation?

Autocorrelation measures the correlation between a time series and its lagged values. It quantifies the degree to which the current value of a series is related to its past values at different lags, indicating any patterns or dependencies in the data over time. Autoregression and autocorrelation are closely related concepts used to analyze and model time series data.

So how does it work?

The indicator calculates autoregressive values for the close, high, and low prices of a security based on the specified lookback length (which is defaulted to 50). It then plots three sets of clouds representing the smoothed autoregressive values for each price component (done using the SMA function). The transparency of the clouds can be adjusted using the "Transparency" input. Additionally, the code includes a correlation table that displays the correlation coefficients between the lagged values of the close, high, and low prices. The table's position can be customized using the "Position" input.

The indicator defaults to the chart timeframe; however, you can manually adjust the indicator to display the range for whatever timeframe you would like. You can view the 30 minute, 15 or even hourly range on the 1 minute or 5 minute chart if you want.

The indicator will show the anticipated “true trading range” of the stock based on the autoregression and autocorrelation of all 3 variables:

Above is SPY on the 5 minute timeframe with 15 minute levels overlayed. Here, you can see the anticipated trading range for that 15 minute time period.

Using the Correlation Table:

The correlation table displays the Pearson Coefficient for all 3 autoregressions.

A positive correlation: A positive autocorrelation indicates a positive relationship between past and current values of a time series variable. It suggests that when the variable has a high value at a certain time, it is more likely to have a high value in the future, and when it has a low value, it is more likely to have a low value in the future. This positive autocorrelation can imply persistence or trend in the data, indicating that past values can provide useful information for predicting future values. The rule of thumb is anything over 0.5 is considered significant.

A positive correlation among all 3 variables also indicates an uptrend. If you see a strong positive (i.e. the values are all greater than 0.8), it indicates an incredibly decisive and strong uptrend.

A negative correlation: A negative autocorrelation indicates an inverse relationship between past and current values of a time series variable. It suggests that when the variable has a high value at a certain time, it is more likely to have a low value in the future, and vice versa. This negative autocorrelation can imply mean reversion or oscillatory behavior in the data, where extreme values tend to be followed by values closer to the average. It indicates that past values can provide useful information for predicting future values by anticipating a reversal in the direction of the variable. The rule of thumb is anything below or equal to -0.5 is considered significant.

A negative correlation among all 3 variables also indicates a downtrend. If you see a strong negative (i.e. the values are all less than or equal to -0.8), it indicates an incredibly decisive and strong downtrend.

Uses of the Indicator:

The indicator can be used for the following functions:

1. Day trading and scalping within an expected range;

2. Determining the strength or weakness of an uptrend or downtrend on various timeframes;

3. Determining the relationship between previous values and past performance and its effect on future performance;

4. Can alert to changes in trend direction in advance (you may see high, low or close turn negative before others, signifying that weakness is beginning to materialize in an uptrend, or inverse in a downtrend (value changes positive)).

Customizability:

SMA: The autoregression data is smoothed by a 3 period lookback. You can change this if you want, but in order for the indicator to present the true trading range, it is recommended to leave it at <= 3.

Lookback Length: This is the length of the lookback period for the autoregression and autocorrelation functions.

Transparency settings: You can adjust the transparency of the clouds manually.

Timeframe: You can adjust the timeframe, as explained above, to display the timeframe of interest. When you adjust the timeframe, the data will all reflect that timeframe and not necessarily the current TF you have open (i.e. you select 30 minutes while viewing it on the 5 minute, it will show the data for the 30 minute TF period).

Video Tutorial:

I have prepared a video outlining the indicator and also explaining the theory of autoregression/correlation. You can find it below:

Let me know any comments, questions or suggestions below.

Thank you for taking the time to read/watch and check out this indicator.

Safe trades everyone!

hidden & regular rsi divergenceThis is a divergence indicator that draws regular and hidden divergences based on the Zigzag indicator and RSI indicator. There are two degrees of Zigzag. So, in each Zigzag degree, there are two types of regular divergences and one type of hidden divergence.

👉(The logic is written in case of a bearish regular divergence. The opposite will apply for a bullish one.)

Type 1 of regular divergence (Logic 1):

Zigzag has to form a higher high. The highest RSI within both Zigzag legs must form lower highs, but the RSI values which are exactly at the Zigzag highs should not form lower highs.

Type 2 of regular divergence (Logic 2):

Zigzag has to form a higher high. The highest RSI within both Zigzag legs must form lower highs, and the RSI values which are exactly at the Zigzag highs should form lower highs.

👉(The logic is written in case of a bearish hidden divergence. The opposite will apply for a bullish one.)

Zigzag has to form a lower high. The highest RSI within both Zigzag legs must form higher highs.

👉There is also a filter that will be applied to all the divergences. It only shows the divergences whose corresponding RSI value was above/below a level (overbought level/oversold level).

Logic for regular divergences:

Bearish regular divergence's first high's (leftmost) RSI value should be greater than or equal to 70.

Bullish regular divergence's first low's (leftmost) RSI value should be less than or equal to 30.

Logic for hidden divergences:

Bearish hidden divergence's second high's (rightmost) RSI value should be greater than or equal to 70.

Bullish hidden divergence's second low's (rightmost) RSI value should be less than or equal to 30.

👉There is another feature also. This indicator colors the background based on whether the RSI is in a bullish or bearish range.

If it's within 80-60, the background will be colored green (this means that RSI is in a bullish range).

If it's within 40-20, the background will be colored red (this means that RSI is in a bearish range).

Stochastic Chebyshev Smoothed With Zero Lag SmoothingFast and Smooth Stochastic Oscillator with Zero Lag

Introduction

In this post, we will discuss a custom implementation of a Stochastic Oscillator that not only smooths the signal but also does so without introducing any noticeable lag. This is a remarkable achievement, as it allows for a fast Stochastic Oscillator that is less prone to false signals without being slow and sluggish.

We will go through the code step by step, explaining the various functions and the overall structure of the code.

First, let's start with a brief overview of the Stochastic Oscillator and the problem it addresses.

Background

The Stochastic Oscillator is a momentum indicator used in technical analysis to determine potential overbought or oversold conditions in an asset's price. It compares the closing price of an asset to its price range over a specified period. However, the Stochastic Oscillator is susceptible to false signals due to its sensitivity to price movements. This is where our custom implementation comes in, offering a smoother signal without noticeable lag, thus reducing the number of false signals.

Despite its popularity and widespread use in technical analysis, the Stochastic Oscillator has its share of drawbacks. While it is a price scaler that allows for easier comparisons across different assets and timeframes, it is also known for generating false signals, which can lead to poor trading decisions. In this section, we will delve deeper into the limitations of the Stochastic Oscillator and discuss the challenges associated with smoothing to mitigate its drawbacks.

Limitations of the Stochastic Oscillator

False Signals: The primary issue with the Stochastic Oscillator is its tendency to produce false signals. Since it is a momentum indicator, it reacts to short-term price movements, which can lead to frequent overbought and oversold signals that do not necessarily indicate a trend reversal. This can result in traders entering or exiting positions prematurely, incurring losses or missing out on potential gains.

Sensitivity to Market Noise: The Stochastic Oscillator is highly sensitive to market noise, which can create erratic signals in volatile markets. This sensitivity can make it difficult for traders to discern between genuine trend reversals and temporary fluctuations.

Lack of Predictive Power: Although the Stochastic Oscillator can help identify potential overbought and oversold conditions, it does not provide any information about the future direction or strength of a trend. As a result, it is often used in conjunction with other technical analysis tools to improve its predictive power.

Challenges of Smoothing the Stochastic Oscillator

To address the limitations of the Stochastic Oscillator, many traders attempt to smooth the indicator by applying various techniques. However, these approaches are not without their own set of challenges:

Trade-off between Smoothing and Responsiveness: The process of smoothing the Stochastic Oscillator inherently involves reducing its sensitivity to price movements. While this can help eliminate false signals, it can also result in a less responsive indicator, which may not react quickly enough to genuine trend reversals. This trade-off can make it challenging to find the optimal balance between smoothing and responsiveness.

Increased Complexity: Smoothing techniques often involve the use of additional mathematical functions and algorithms, which can increase the complexity of the indicator. This can make it more difficult for traders to understand and interpret the signals generated by the smoothed Stochastic Oscillator.

Lagging Signals: Some smoothing methods, such as moving averages, can introduce a time lag into the Stochastic Oscillator's signals. This can result in late entry or exit points, potentially reducing the profitability of a trading strategy based on the smoothed indicator.

Overfitting: In an attempt to eliminate false signals, traders may over-optimize their smoothing parameters, resulting in a Stochastic Oscillator that is overfitted to historical data. This can lead to poor performance in real-time trading, as the overfitted indicator may not accurately reflect the dynamics of the current market.

In our custom implementation of the Stochastic Oscillator, we used a combination of Chebyshev Type I Moving Average and zero-lag Gaussian-weighted moving average filters to address the indicator's limitations while preserving its responsiveness. In this section, we will discuss the reasons behind selecting these specific filters and the advantages of using the Chebyshev filter for our purpose.

Filter Selection

Chebyshev Type I Moving Average: The Chebyshev filter was chosen for its ability to provide a smoother signal without sacrificing much responsiveness. This filter is designed to minimize the maximum error between the original and the filtered signal within a specific frequency range, effectively reducing noise while preserving the overall shape of the signal. The Chebyshev Type I Moving Average achieves this by allowing a specified amount of ripple in the passband, resulting in a more aggressive filter roll-off and better noise reduction compared to other filters, such as the Butterworth filter.

Zero-lag Gaussian-weighted Moving Average: To further improve the Stochastic Oscillator's performance without introducing noticeable lag, we used the zero-lag Gaussian-weighted moving average (GWMA) filter. This filter combines the benefits of a Gaussian-weighted moving average, which prioritizes recent data points by assigning them higher weights, with a zero-lag approach that minimizes the time delay in the filtered signal. The result is a smoother signal that is less prone to false signals and is more responsive than traditional moving average filters.

Advantages of the Chebyshev Filter

Effective Noise Reduction: The primary advantage of the Chebyshev filter is its ability to effectively reduce noise in the Stochastic Oscillator signal. By minimizing the maximum error within a specified frequency range, the Chebyshev filter suppresses short-term fluctuations that can lead to false signals while preserving the overall trend.

Customizable Ripple Factor: The Chebyshev Type I Moving Average allows for a customizable ripple factor, enabling traders to fine-tune the filter's aggressiveness in reducing noise. This flexibility allows for better adaptability to different market conditions and trading styles.

Responsiveness: Despite its effective noise reduction, the Chebyshev filter remains relatively responsive compared to other smoothing filters. This responsiveness allows for more accurate detection of genuine trend reversals, making it a suitable choice for our custom Stochastic Oscillator implementation.

Compatibility with Zero-lag Techniques: The Chebyshev filter can be effectively combined with zero-lag techniques, such as the Gaussian-weighted moving average filter used in our custom implementation. This combination results in a Stochastic Oscillator that is both smooth and responsive, with minimal lag.

Code Overview

The code begins with defining custom mathematical functions for hyperbolic sine, cosine, and their inverse functions. These functions will be used later in the code for smoothing purposes.

Next, the gaussian_weight function is defined, which calculates the Gaussian weight for a given 'k' and 'smooth_per'. The zero_lag_gwma function calculates the zero-lag moving average with Gaussian weights. This function is used to create a Gaussian-weighted moving average with minimal lag.

The chebyshevI function is an implementation of the Chebyshev Type I Moving Average, which is used for smoothing the Stochastic Oscillator. This function takes the source value (src), length of the moving average (len), and the ripple factor (ripple) as input parameters.

The main part of the code starts by defining input parameters for K and D smoothing and ripple values. The Stochastic Oscillator is calculated using the ta.stoch function with Chebyshev smoothed inputs for close, high, and low. The result is further smoothed using the zero-lag Gaussian-weighted moving average function (zero_lag_gwma).

Finally, the lag variable is calculated using the Chebyshev Type I Moving Average for the Stochastic Oscillator. The Stochastic Oscillator and the lag variable are plotted on the chart, along with upper and lower bands at 80 and 20 levels, respectively. A fill is added between the upper and lower bands for better visualization.

Conclusion

The custom Stochastic Oscillator presented in this blog post combines the Chebyshev Type I Moving Average and zero-lag Gaussian-weighted moving average filters to provide a smooth and responsive signal without introducing noticeable lag. This innovative implementation results in a fast Stochastic Oscillator that is less prone to false signals, making it a valuable tool for technical analysts and traders alike.

However, it is crucial to recognize that the Stochastic Oscillator, despite being a price scaler, has its limitations, primarily due to its propensity for generating false signals. While smoothing techniques, like the ones used in our custom implementation, can help mitigate these issues, they often introduce new challenges, such as reduced responsiveness, increased complexity, lagging signals, and the risk of overfitting.

The selection of the Chebyshev Type I Moving Average and zero-lag Gaussian-weighted moving average filters was driven by their combined ability to provide a smooth and responsive signal while minimizing false signals. The advantages of the Chebyshev filter, such as effective noise reduction, customizable ripple factor, and responsiveness, make it an excellent fit for addressing the limitations of the Stochastic Oscillator.

When using the Stochastic Oscillator, traders should be aware of these limitations and challenges, and consider incorporating other technical analysis tools and techniques to supplement the indicator's signals. This can help improve the overall accuracy and effectiveness of their trading strategies, reducing the risk of losses due to false signals and other limitations associated with the Stochastic Oscillator.

Feel free to use, modify, or improve upon this custom Stochastic Oscillator code in your trading strategies. We hope this detailed walkthrough of the custom Stochastic Oscillator, its limitations, challenges, and filter selection has provided you with valuable insights and a better understanding of how it works. Happy trading!

ObjectHelpersLibrary "ObjectHelpers"

Line | Box | Label | Linefill -- Maker, Setter, Getter Library

TODO: add table functionality

set(object)

set all params for `line`, `box`, `label`, `linefill` objects with 1 function

***

## Overloaded

***

```

method set(line Line, int x1=na, float y1=na, int x2=na, float y2=na,string xloc=na,string extend=na,color color=na,string style=na,int width=na,bool update=na) => line

```

### Params

- **Line** `line` - line object | `required`

- **x1** `int` - value to set x1

- **y1** `float` - value to set y1

- **x2** `int` - value to set x2

- **y2** `float` - value to set y2

- **xloc** `int` - value to set xloc

- **yloc** `int` - value to set yloc

- **extend** `string` - value to set extend

- **color** `color` - value to set color

- **style** `string` - value to set style

- **width** `int` - value to set width

- **update** `bool` - value to set update

***

```

method set(box Box,int left=na,float top=na,int right=na, float bottom=na,color bgcolor=na,color border_color=na,string border_style=na,int border_width=na,string extend=na,string txt=na,color text_color=na,string text_font_family=na,string text_halign=na,string text_valign=na,string text_wrap=na,bool update=false) => box

```

### Params

- **Box** `box` - box object

- **left** `int` - value to set left

- **top** `float` - value to set top

- **right** `int` - value to set right

- **bottom** `float` - value to set bottom

- **bgcolor** `color` - value to set bgcolor

- **border_color** `color` - value to set border_color

- **border_style** `string` - value to set border_style

- **border_width** `int` - value to set border_width

- **extend** `string` - value to set extend

- **txt** `string` - value to set _text

- **text_color** `color` - value to set text_color

- **text_font_family** `string` - value to set text_font_family

- **text_halign** `string` - value to set text_halign

- **text_valign** `string` - value to set text_valign

- **text_wrap** `string` - value to set text_wrap

- **update** `bool` - value to set update

***

```

method set(label Label,int x=na,float y=na, string txt=na,string xloc=na,color color=na,color textcolor=na,string size=na,string style=na,string textalign=na,string tooltip=na,string text_font_family=na,bool update=false) => label

```

### Paramas

- **Label** `label` - label object

- **x** `int` - value to set x

- **y** `float` - value to set y

- **txt** `string` - value to set text add`"+++"` to the _text striing to have the current label text concatenated to the location of the "+++")

- **textcolor** `color` - value to set textcolor

- **size** `string` - value to set size

- **style** `string` - value to set style (use "flip" ,as the style to have label flip to top or bottom of bar depending on if open > close and vice versa)

- **text_font_family** `string` - value to set text_font_family

- **textalign** `string` - value to set textalign

- **tooltip** `string` - value to set tooltip

- **update** `bool` - update label to next bar

***

```

method set(linefill Linefill=na,line line1=na,line line2=na,color color=na) => linefill

```

### Params

- **linefill** `linefill` - linefill object

- **line1** `line` - line object

- **line2** `line` - line object

- **color** `color` - color

Parameters:

object (obj)

Returns: `line`, `box`, `label`, `linefill`

method set(Line, x1, y1, x2, y2, xloc, extend, color, style, width, update)

set the location params of a line with 1 function auto detects time or bar_index for xloc param

Namespace types: series line

Parameters:

Line (line) : `line` - line object | `required`

x1 (int) : `int` - value to set x1

y1 (float) : `float` - value to set y1

x2 (int) : `int` - value to set x2

y2 (float) : `float` - value to set y2

xloc (string) : `int` - value to set xloc

extend (string) : `string` - value to set extend

color (color) : `color` - value to set color

style (string) : `string` - value to set style

width (int) : `int` - value to set width

update (bool) : `bool` - value to set update

Returns: `line`

method set(Box, left, top, right, bottom, bgcolor, border_color, border_style, border_width, extend, txt, text_color, text_font_family, text_halign, text_valign, text_wrap, update)

set the location params of a box with 1 function

Namespace types: series box

Parameters:

Box (box) : `box` - box object | `required`

left (int) : `int` - value to set left

top (float) : `float` - value to set top

right (int) : `int` - value to set right

bottom (float) : `float` - value to set bottom

bgcolor (color) : `color` - value to set bgcolor

border_color (color) : `color` - value to set border_color

border_style (string) : `string` - value to set border_style

border_width (int) : `int` - value to set border_width

extend (string) : `string` - value to set extend

txt (string) : `string` - value to set _text

text_color (color) : `color` - value to set text_color

text_font_family (string) : `string` - value to set text_font_family

text_halign (string) : `string` - value to set text_halign

text_valign (string) : `string` - value to set text_valign

text_wrap (string) : `string` - value to set text_wrap

update (bool) : `bool` - value to set update

Returns: `box`

method set(Label, x, y, txt, xloc, color, textcolor, size, style, textalign, tooltip, text_font_family, update)

set the location params of a label with 1 function auto detects time or bar_index for xloc param

Namespace types: series label

Parameters:

Label (label) : `label` | `required`

x (int) : `int` - value to set x

y (float) : `float` - value to set y

txt (string) : `string` - value to set text add`"+++"` to the _text striing to have the current label text concatenated to the location of the "+++")

xloc (string)

color (color)

textcolor (color) : `color` - value to set textcolor

size (string) : `string` - value to set size

style (string) : `string` - value to set style (use "flip" ,as the style to have label flip to top or bottom of bar depending on if open > close and vice versa)

textalign (string) : `string` - value to set textalign

tooltip (string) : `string` - value to set tooltip

text_font_family (string) : `string` - value to set text_font_family

update (bool) : `bool` - update label to next bar

Returns: `label`

method set(Linefill, line1, line2, color)

change the 1 or 2 of the lines in a linefill object