AlphaAlpha is a measure of the active return on an investment, the performance of that investment compared to the S&P500 index, where 0.01 = 1%

alpha < 0: the investment has earned too little for its risk (or, was too risky for the return)

alpha = 0: the investment has earned a return adequate for the risk taken

alpha > 0: the investment has a return in excess of the reward for the assumed risk

Поиск скриптов по запросу "ha溢价率"

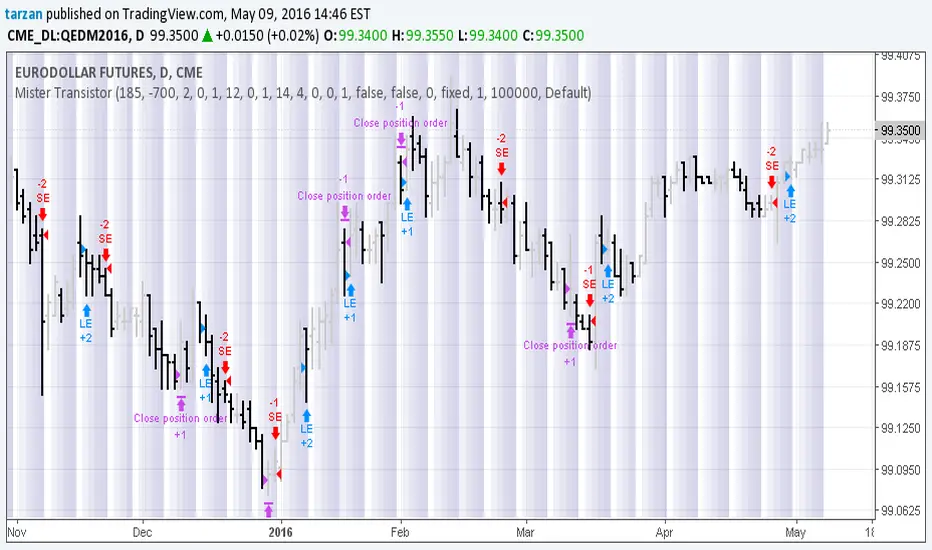

Mister Transistor 3.0This is a general purpose very flexible program to test the effectiveness of HA bars.

Please note that if you are charting at tradingview using Heikin-Ashi charting, your system will be trading fictitious prices even if you check the "use real prices" box. Thought you might like to know that before you lose all your money.

This program performs the HA calcs internally thus allowing you to use HA bars on a standard bar chart and obtaining real prices for your trades.

Courtesy of Boffin Hollow Lab

Author: Tarzan the Ape Man

Trailing Sharpe RatioThe Sharpe ratio allows you to see whether or not an investment has historically provided a return appropriate to its risk level. A Sharpe ratio above one is acceptable, above 2 is good, and above 3 is excellent. A Sharpe ratio less than one would indicate that an investment has not returned a high enough return to justify the risk of holding it. Interesting in this example, SPY's one year avg Sharpe ratio is above 3. This would mean on average SPY returns 3x better returns than the risk associated with holding it, implying there is some sort of underlying value to the investment.

When the sharpe ratio is above its signal, this implies the investment is currently outperforming compared to its typical return, below the signal means the investment is currently under performing. A negative Shape would mean that the investment has not provided a positive return, and may be a possible short candidate.

Zweig Market Breadth Thrust Indicator [LazyBear]The Breadth Thrust (BT) indicator is a market momentum indicator developed by Dr. Martin Zweig. According to Dr. Zweig a Breadth Thrust occurs when, during a 10-day period, the Breadth Thrust indicator rises from below 40 percent to above 61.5 percent.

A "Thrust" indicates that the stock market has rapidly changed from an oversold condition to one of strength, but has not yet become overbought. This is very rare and has happened only a few times. Dr. Zweig also points out that most bull markets begin with a Breadth Thrust.

All parameters are configurable. You can draw BT for NYSE, NASDAQ, AMEX or based on combined data (i.e., AMEX+NYSE+NASD). There is also a "CUSTOM" mode supported, so you can enter your own ADV/DEC symbols.

More info:

Definition: www.investopedia.com

A Breadth Thrust Signal: www.mcoscillator.com

A Rare "Zweig" Buy Signal: www.moneyshow.com

Zweig Breadth Thrust: recessionalert.com

List of my public indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

KK_Traders Dynamic Index_Bar HighlightingHey guys,

this is one of my favorite scripts as it represents a whole trading system that has given me very good results!

I have only used it on Bitcoin so far but I am sure it will also work for other instruments.

The original code to this was created by LazyBear, so all props to him for this great script!

I have linked his original post down below.

You can find the full rules to the system in this PDF (which has also been taken from LBs post):

www.forexmt4.com

Here is a short summary of the rules:

Go long when (all conditions have to be met):

The green line is above 50

The green line is above the red line

The green line is above the orange line

The close is above the upper Band of the Price Action Channel

The candles close is above its open

(The green line is below 68)

Go short when (all conditions have to be met):

The green line is below 50

The green line is below the red line

The green line is below the orange line

The close is below the lower band of the Price Action Channel

The candles close is below its open

(The green line is above 32)

Close when:

Any of these conditions aren't true anymore.

I have marked two of the rules in brackets as they seem to cut out a lot of the profits this system generates. You can choose to still use these rules by checking the box that says "Use Original Ruleset" in the options.

The system also contains rules regarding the Heiken Ashi bars. However these aren't as specific as the other rules. This is where your personal judgement comes in and this part is hard to explain. Take a look at the PDF I have linked to get a better understanding.

So far, this is just the TDI trading system and LBs script, now what have I changed?

I have incorporated the Price Action Channel to the system and changed it so that it highlights the bars whenever the system is giving a signal. As long as the bars are green the system is giving a long signal, as long as they are red the system is giving a short signal. Keep in mind that this doesn't consider the bar size of the HA bars. I recommend coloring all bars grey via the chart settings in order to be able to see the bar highlighting properly.

I have also published the Price Action Channel seperately in case some of you wish to view the Channel.

I am fairly new to creating scripts so use it with caution and let me know what you think!

LBs original post:

The seperate Price Action Channel script:

CM Stochastic POP Method 1 - Jake Bernstein_V1A good friend ucsgears recently published a Stochastic Pop Indicator designed by Jake Bernstein with a modified version he found.

I spoke to Jake this morning and asked if he had any updates to his Stochastic POP Trading Method. Attached is a PDF Jake published a while back (Please read for basic rules, which also Includes a New Method). I will release the Additional Method Tomorrow.

Jake asked me to share that he has Updated this Method Recently. Now across all symbols he has found the Stochastic Values of 60 and 30 to be the most profitable. NOTE - This can be Significantly Optimized for certain Symbols/Markets.

Jake Bernstein will be a contributor on TradingView when Backtesting/Strategies are released. Jake is one of the Top Trading System Developers in the world with 45+ years experience and he is going to teach how to create Trading Systems and how to Optimize the correct way.

Below are a few Strategy Results....Soon You Will Be Able To Find Results Like This Yourself on TradingView.com

BackTesting Results Example: EUR-USD Daily Chart Since 01/01/2005

Strategy 1:

Go Long When Stochastic Crosses Above 60. Go Short When Stochastic Crosses Below 30. Exit Long/Short When Stochastic has a Reverse Cross of Entry Value.

Results:

Total Trades = 164

Profit = 50, 126 Pips

Win% = 38.4%

Profit Factor = 1.35

Avg Trade = 306 Pips Profit

***Most Consecutive Wins = 3 ... Most Consecutive Losses = 6

Strategy 2:

Rules - Proprietary Optimization Jake Will Teach. Only Added 1 Additional Exit Rule.

Results:

Total Trades = 164

Profit = 62, 876 Pips!!!

Win% = 38.4%

Profit Factor = 1.44

Avg Trade = 383 Pips Profit

***Most Consecutive Wins = 3 ... Most Consecutive Losses = 6

Strategy 3:

Rules - Proprietary Optimization Jake Will Teach. Only added 1 Additional Exit Rule.

Results:

Winning Percent Increases to 72.6%!!! , Same Amount of Trades.

***Most Consecutive Wins = 21 ...Most Consecutive Losses = 4

Indicator Includes:

-Ability to Color Candles (CheckBox In Inputs Tab)

Green = Long Trade

Blue = No Trade

Red = Short Trade

-Color Coded Stochastic Line based on being Above/Below or In Between Entry Lines.

Link To Jakes PDF with Rules

dl.dropboxusercontent.com

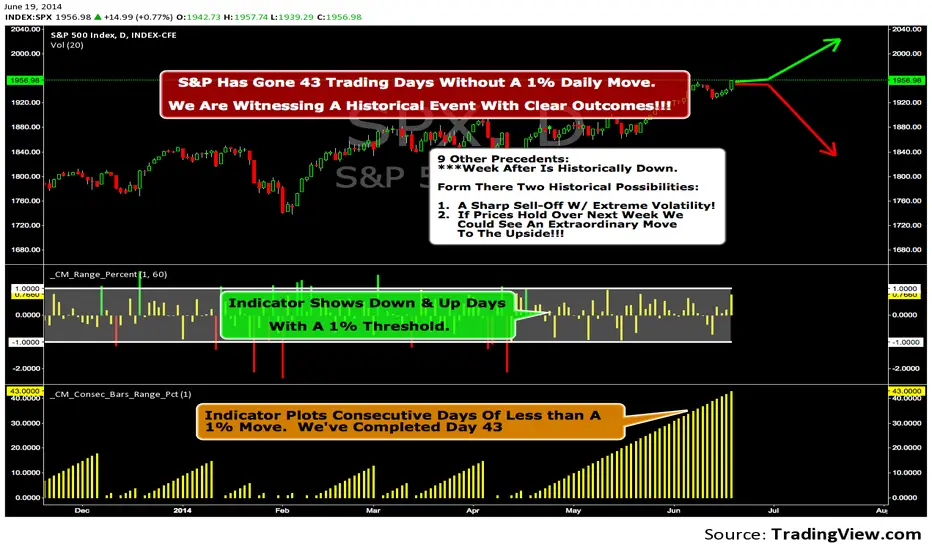

We Are Witnessing A Historical Event With A Clear Outcome!!!"Full Disclosure: I came across this information from www.SentimenTrader.com

I have no financial affiliation…They provide incredible statistical facts on

The General Market, Currencies, and Futures. They offer a two week free trial.

I Highly Recommend.

The S&P 500 has gone 43 trading days without a 1% daily move, up or down.

which is the equivalent of two months and one day in trading days.

During this stretch, the S&P has gained more than 4%,

and it has notched a 52-week high recently as well.

Since 1952, there were nine other precedents. All of

these went 42 trading days without a 1% move, all of

them saw the S&P gain at least 4% during their streaks,

and all of them saw the S&P close at a 52-week highs.

***There was consistent weakness a week later, with only three

gainers, and all below +0.5%.

***After that, stocks did better, often continuing an Extraordinary move higher.

Charts can sometimes give us a better nuance than

numbers from a table, and from the charts we can see a

general pattern -

***if stocks held up well in the following

weeks, then they tended to do extremely well in the

months ahead.

***If stocks started to stumble after this two-

month period of calm, however, then the following months

tended to show a lot more volatility.

We already know we're seeing an exceptional market

environment at the moment, going against a large number

of precedents that argued for weakness here, instead of

the rally we've seen. If we continue to head higher in

spite of everything, these precedents would suggest that

we're in the midst of something that could be TRULY EXTRAORDINARY.

Trading Strategy based on BB/KC squeeze**** [Edit: New version (v02) posted, see the comments section for the code *****

Simple strategy. You only consider taking a squeeze play when both the upper and lower Bollinger Bands go inside the Keltner Channel. When the Bollinger Bands (BOTH lines) start to come out of the Keltner Channel, the squeeze has been released and a move is about to take place.

I have added more support indicators -- I highlight the bullish / bearish KC breaches (using GREEN/RED crosses) and a SAR to see where price action is trending.

Appreciate any feedback. Enjoy!

Color codes for v02:

----------------------------

When both the upper and lower Bollinger Bands go inside the Keltner Channel, the squeeze is on and is highlighted in RED.

When the Bollinger Bands (BOTH lines) start to come out of the Keltner Channel, the squeeze has been released and is highlighted in GREEN.

When one of the Bollinger Bands is out of Keltner Channel, no highlighting is done (this means, the background color shows up, so don't get confused if you have RED/GREEN in your chart's bground :))

Color codes for v01:

----------------------------

When both the upper and lower Bollinger Bands go inside the Keltner Channel, the squeeze is on and is highlighted in YELLOW.

When the Bollinger Bands (BOTH lines) start to come out of the Keltner Channel, the squeeze has been released and is highlighted in BLUE.

Dynamic Equity Allocation Model//@version=6

indicator('Dynamic Equity Allocation Model', shorttitle = 'DEAM', overlay = false, precision = 1, scale = scale.right, max_bars_back = 500)

// DYNAMIC EQUITY ALLOCATION MODEL

// Quantitative framework for dynamic portfolio allocation between stocks and cash.

// Analyzes five dimensions: market regime, risk metrics, valuation, sentiment,

// and macro conditions to generate allocation recommendations (0-100% equity).

//

// Uses real-time data from TradingView including fundamentals (P/E, ROE, ERP),

// volatility indicators (VIX), credit spreads, yield curves, and market structure.

// INPUT PARAMETERS

group1 = 'Model Configuration'

model_type = input.string('Adaptive', 'Allocation Model Type', options = , group = group1, tooltip = 'Conservative: Slower to increase equity, Aggressive: Faster allocation changes, Adaptive: Dynamic based on regime')

use_crisis_detection = input.bool(true, 'Enable Crisis Detection System', group = group1, tooltip = 'Automatic detection and response to crisis conditions')

use_regime_model = input.bool(true, 'Use Market Regime Detection', group = group1, tooltip = 'Identify Bull/Bear/Crisis regimes for dynamic allocation')

group2 = 'Portfolio Risk Management'

target_portfolio_volatility = input.float(12.0, 'Target Portfolio Volatility (%)', minval = 3, maxval = 20, step = 0.5, group = group2, tooltip = 'Target portfolio volatility (Cash reduces volatility: 50% Equity = ~10% vol, 100% Equity = ~20% vol)')

max_portfolio_drawdown = input.float(15.0, 'Maximum Portfolio Drawdown (%)', minval = 5, maxval = 35, step = 2.5, group = group2, tooltip = 'Maximum acceptable PORTFOLIO drawdown (not market drawdown - portfolio with cash has lower drawdown)')

enable_portfolio_risk_scaling = input.bool(true, 'Enable Portfolio Risk Scaling', group = group2, tooltip = 'Scale allocation based on actual portfolio risk characteristics (recommended)')

risk_lookback = input.int(252, 'Risk Calculation Period (Days)', minval = 60, maxval = 504, group = group2, tooltip = 'Period for calculating volatility and risk metrics')

group3 = 'Component Weights (Total = 100%)'

w_regime = input.float(35.0, 'Market Regime Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_risk = input.float(25.0, 'Risk Metrics Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_valuation = input.float(20.0, 'Valuation Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_sentiment = input.float(15.0, 'Sentiment Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_macro = input.float(5.0, 'Macro Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

group4 = 'Crisis Detection Thresholds'

crisis_vix_threshold = input.float(40, 'Crisis VIX Level', minval = 30, maxval = 80, group = group4, tooltip = 'VIX level indicating crisis conditions (COVID peaked at 82)')

crisis_drawdown_threshold = input.float(15, 'Crisis Drawdown Threshold (%)', minval = 10, maxval = 30, group = group4, tooltip = 'Market drawdown indicating crisis conditions')

crisis_credit_spread = input.float(500, 'Crisis Credit Spread (bps)', minval = 300, maxval = 1000, group = group4, tooltip = 'High yield spread indicating crisis conditions')

group5 = 'Display Settings'

show_components = input.bool(false, 'Show Component Breakdown', group = group5, tooltip = 'Display individual component analysis lines')

show_regime_background = input.bool(true, 'Show Dynamic Background', group = group5, tooltip = 'Color background based on allocation signals')

show_reference_lines = input.bool(false, 'Show Reference Lines', group = group5, tooltip = 'Display allocation percentage reference lines')

show_dashboard = input.bool(true, 'Show Analytics Dashboard', group = group5, tooltip = 'Display comprehensive analytics table')

show_confidence_bands = input.bool(false, 'Show Confidence Bands', group = group5, tooltip = 'Display uncertainty quantification bands')

smoothing_period = input.int(3, 'Smoothing Period', minval = 1, maxval = 10, group = group5, tooltip = 'Smoothing to reduce allocation noise')

background_intensity = input.int(95, 'Background Intensity (%)', minval = 90, maxval = 99, group = group5, tooltip = 'Higher values = more transparent background')

// Styling Options

color_scheme = input.string('EdgeTools', 'Color Theme', options = , group = 'Appearance', tooltip = 'Professional color themes')

use_dark_mode = input.bool(true, 'Optimize for Dark Theme', group = 'Appearance')

main_line_width = input.int(3, 'Main Line Width', minval = 1, maxval = 5, group = 'Appearance')

// DATA RETRIEVAL

// Market Data

sp500 = request.security('SPY', timeframe.period, close)

sp500_high = request.security('SPY', timeframe.period, high)

sp500_low = request.security('SPY', timeframe.period, low)

sp500_volume = request.security('SPY', timeframe.period, volume)

// Volatility Indicators

vix = request.security('VIX', timeframe.period, close)

vix9d = request.security('VIX9D', timeframe.period, close)

vxn = request.security('VXN', timeframe.period, close)

// Fixed Income and Credit

us2y = request.security('US02Y', timeframe.period, close)

us10y = request.security('US10Y', timeframe.period, close)

us3m = request.security('US03MY', timeframe.period, close)

hyg = request.security('HYG', timeframe.period, close)

lqd = request.security('LQD', timeframe.period, close)

tlt = request.security('TLT', timeframe.period, close)

// Safe Haven Assets

gold = request.security('GLD', timeframe.period, close)

usd = request.security('DXY', timeframe.period, close)

yen = request.security('JPYUSD', timeframe.period, close)

// Financial data with fallback values

get_financial_data(symbol, fin_id, period, fallback) =>

data = request.financial(symbol, fin_id, period, ignore_invalid_symbol = true)

na(data) ? fallback : data

// SPY fundamental metrics

spy_earnings_per_share = get_financial_data('AMEX:SPY', 'EARNINGS_PER_SHARE_BASIC', 'TTM', 20.0)

spy_operating_earnings_yield = get_financial_data('AMEX:SPY', 'OPERATING_EARNINGS_YIELD', 'FY', 4.5)

spy_dividend_yield = get_financial_data('AMEX:SPY', 'DIVIDENDS_YIELD', 'FY', 1.8)

spy_buyback_yield = get_financial_data('AMEX:SPY', 'BUYBACK_YIELD', 'FY', 2.0)

spy_net_margin = get_financial_data('AMEX:SPY', 'NET_MARGIN', 'TTM', 12.0)

spy_debt_to_equity = get_financial_data('AMEX:SPY', 'DEBT_TO_EQUITY', 'FY', 0.5)

spy_return_on_equity = get_financial_data('AMEX:SPY', 'RETURN_ON_EQUITY', 'FY', 15.0)

spy_free_cash_flow = get_financial_data('AMEX:SPY', 'FREE_CASH_FLOW', 'TTM', 100000000)

spy_ebitda = get_financial_data('AMEX:SPY', 'EBITDA', 'TTM', 200000000)

spy_pe_forward = get_financial_data('AMEX:SPY', 'PRICE_EARNINGS_FORWARD', 'FY', 18.0)

spy_total_debt = get_financial_data('AMEX:SPY', 'TOTAL_DEBT', 'FY', 500000000)

spy_total_equity = get_financial_data('AMEX:SPY', 'TOTAL_EQUITY', 'FY', 1000000000)

spy_enterprise_value = get_financial_data('AMEX:SPY', 'ENTERPRISE_VALUE', 'FY', 30000000000)

spy_revenue_growth = get_financial_data('AMEX:SPY', 'REVENUE_ONE_YEAR_GROWTH', 'TTM', 5.0)

// Market Breadth Indicators

nya = request.security('NYA', timeframe.period, close)

rut = request.security('IWM', timeframe.period, close)

// Sector Performance

xlk = request.security('XLK', timeframe.period, close)

xlu = request.security('XLU', timeframe.period, close)

xlf = request.security('XLF', timeframe.period, close)

// MARKET REGIME DETECTION

// Calculate Market Trend

sma_20 = ta.sma(sp500, 20)

sma_50 = ta.sma(sp500, 50)

sma_200 = ta.sma(sp500, 200)

ema_10 = ta.ema(sp500, 10)

// Market Structure Score

trend_strength = 0.0

trend_strength := trend_strength + (sp500 > sma_20 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_50 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_200 ? 2 : -2)

trend_strength := trend_strength + (sma_50 > sma_200 ? 2 : -2)

// Volatility Regime

returns = math.log(sp500 / sp500 )

realized_vol_20d = ta.stdev(returns, 20) * math.sqrt(252) * 100

realized_vol_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

ewma_vol = ta.ema(math.pow(returns, 2), 20)

realized_vol = math.sqrt(ewma_vol * 252) * 100

vol_premium = vix - realized_vol

// Drawdown Calculation

running_max = ta.highest(sp500, risk_lookback)

current_drawdown = (running_max - sp500) / running_max * 100

// Regime Score

regime_score = 0.0

// Trend Component (40%)

if trend_strength >= 4

regime_score := regime_score + 40

regime_score

else if trend_strength >= 2

regime_score := regime_score + 30

regime_score

else if trend_strength >= 0

regime_score := regime_score + 20

regime_score

else if trend_strength >= -2

regime_score := regime_score + 10

regime_score

else

regime_score := regime_score + 0

regime_score

// Volatility Component (30%)

if vix < 15

regime_score := regime_score + 30

regime_score

else if vix < 20

regime_score := regime_score + 25

regime_score

else if vix < 25

regime_score := regime_score + 15

regime_score

else if vix < 35

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Drawdown Component (30%)

if current_drawdown < 3

regime_score := regime_score + 30

regime_score

else if current_drawdown < 7

regime_score := regime_score + 20

regime_score

else if current_drawdown < 12

regime_score := regime_score + 10

regime_score

else if current_drawdown < 20

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Classify Regime

market_regime = regime_score >= 80 ? 'Strong Bull' : regime_score >= 60 ? 'Bull Market' : regime_score >= 40 ? 'Neutral' : regime_score >= 20 ? 'Correction' : regime_score >= 10 ? 'Bear Market' : 'Crisis'

// RISK-BASED ALLOCATION

// Calculate Market Risk

parkinson_hl = math.log(sp500_high / sp500_low)

parkinson_vol = parkinson_hl / (2 * math.sqrt(math.log(2))) * math.sqrt(252) * 100

garman_klass_vol = math.sqrt((0.5 * math.pow(math.log(sp500_high / sp500_low), 2) - (2 * math.log(2) - 1) * math.pow(math.log(sp500 / sp500 ), 2)) * 252) * 100

market_volatility_20d = math.max(ta.stdev(returns, 20) * math.sqrt(252) * 100, parkinson_vol)

market_volatility_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

market_drawdown = current_drawdown

// Initialize risk allocation

risk_allocation = 50.0

if enable_portfolio_risk_scaling

// Volatility-based allocation

vol_based_allocation = target_portfolio_volatility / math.max(market_volatility_20d, 5.0) * 100

vol_based_allocation := math.max(0, math.min(100, vol_based_allocation))

// Drawdown-based allocation

dd_based_allocation = 100.0

if market_drawdown > 1.0

dd_based_allocation := max_portfolio_drawdown / market_drawdown * 100

dd_based_allocation := math.max(0, math.min(100, dd_based_allocation))

dd_based_allocation

// Combine (conservative)

risk_allocation := math.min(vol_based_allocation, dd_based_allocation)

// Dynamic adjustment

current_equity_estimate = 50.0

estimated_portfolio_vol = current_equity_estimate / 100 * market_volatility_20d

estimated_portfolio_dd = current_equity_estimate / 100 * market_drawdown

vol_utilization = estimated_portfolio_vol / target_portfolio_volatility

dd_utilization = estimated_portfolio_dd / max_portfolio_drawdown

risk_utilization = math.max(vol_utilization, dd_utilization)

risk_adjustment_factor = 1.0

if risk_utilization > 1.0

risk_adjustment_factor := math.exp(-0.5 * (risk_utilization - 1.0))

risk_adjustment_factor := math.max(0.5, risk_adjustment_factor)

risk_adjustment_factor

else if risk_utilization < 0.9

risk_adjustment_factor := 1.0 + 0.2 * math.log(1.0 / risk_utilization)

risk_adjustment_factor := math.min(1.3, risk_adjustment_factor)

risk_adjustment_factor

risk_allocation := risk_allocation * risk_adjustment_factor

risk_allocation

else

vol_scalar = target_portfolio_volatility / math.max(market_volatility_20d, 10)

vol_scalar := math.min(1.5, math.max(0.2, vol_scalar))

drawdown_penalty = 0.0

if current_drawdown > max_portfolio_drawdown

drawdown_penalty := (current_drawdown - max_portfolio_drawdown) / max_portfolio_drawdown

drawdown_penalty := math.min(1.0, drawdown_penalty)

drawdown_penalty

risk_allocation := 100 * vol_scalar * (1 - drawdown_penalty)

risk_allocation

risk_allocation := math.max(0, math.min(100, risk_allocation))

// VALUATION ANALYSIS

// Valuation Metrics

actual_pe_ratio = spy_earnings_per_share > 0 ? sp500 / spy_earnings_per_share : spy_pe_forward

actual_earnings_yield = nz(spy_operating_earnings_yield, 0) > 0 ? spy_operating_earnings_yield : 100 / actual_pe_ratio

total_shareholder_yield = spy_dividend_yield + spy_buyback_yield

// Equity Risk Premium (multi-method calculation)

method1_erp = actual_earnings_yield - us10y

method2_erp = actual_earnings_yield + spy_buyback_yield - us10y

payout_ratio = spy_dividend_yield > 0 and actual_earnings_yield > 0 ? spy_dividend_yield / actual_earnings_yield : 0.4

sustainable_growth = spy_return_on_equity * (1 - payout_ratio) / 100

method3_erp = spy_dividend_yield + sustainable_growth * 100 - us10y

implied_growth = spy_revenue_growth * 0.7

method4_erp = total_shareholder_yield + implied_growth - us10y

equity_risk_premium = method1_erp * 0.35 + method2_erp * 0.30 + method3_erp * 0.20 + method4_erp * 0.15

ev_ebitda_ratio = spy_enterprise_value > 0 and spy_ebitda > 0 ? spy_enterprise_value / spy_ebitda : 15.0

debt_equity_health = spy_debt_to_equity < 1.0 ? 1.2 : spy_debt_to_equity < 2.0 ? 1.0 : 0.8

// Valuation Score

base_valuation_score = 50.0

if equity_risk_premium > 4

base_valuation_score := 95

base_valuation_score

else if equity_risk_premium > 3

base_valuation_score := 85

base_valuation_score

else if equity_risk_premium > 2

base_valuation_score := 70

base_valuation_score

else if equity_risk_premium > 1

base_valuation_score := 55

base_valuation_score

else if equity_risk_premium > 0

base_valuation_score := 40

base_valuation_score

else if equity_risk_premium > -1

base_valuation_score := 25

base_valuation_score

else

base_valuation_score := 10

base_valuation_score

growth_adjustment = spy_revenue_growth > 10 ? 10 : spy_revenue_growth > 5 ? 5 : 0

margin_adjustment = spy_net_margin > 15 ? 5 : spy_net_margin < 8 ? -5 : 0

roe_adjustment = spy_return_on_equity > 20 ? 5 : spy_return_on_equity < 10 ? -5 : 0

valuation_score = base_valuation_score + growth_adjustment + margin_adjustment + roe_adjustment

valuation_score := math.max(0, math.min(100, valuation_score * debt_equity_health))

// SENTIMENT ANALYSIS

// VIX Term Structure

vix_term_structure = vix9d > 0 ? vix / vix9d : 1

backwardation = vix_term_structure > 1.05

steep_backwardation = vix_term_structure > 1.15

// Safe Haven Flows

gold_momentum = ta.roc(gold, 20)

dollar_momentum = ta.roc(usd, 20)

yen_momentum = ta.roc(yen, 20)

treasury_momentum = ta.roc(tlt, 20)

safe_haven_flow = gold_momentum * 0.3 + treasury_momentum * 0.3 + dollar_momentum * 0.25 + yen_momentum * 0.15

// Advanced Sentiment Analysis

vix_percentile = ta.percentrank(vix, 252)

vix_zscore = (vix - ta.sma(vix, 252)) / ta.stdev(vix, 252)

vix_momentum = ta.roc(vix, 5)

vvix_proxy = ta.stdev(vix_momentum, 20) * math.sqrt(252)

risk_reversal_proxy = (vix - realized_vol) / realized_vol

// Sentiment Score

base_sentiment = 50.0

vix_adjustment = 0.0

if vix_zscore < -1.5

vix_adjustment := 40

vix_adjustment

else if vix_zscore < -0.5

vix_adjustment := 20

vix_adjustment

else if vix_zscore < 0.5

vix_adjustment := 0

vix_adjustment

else if vix_zscore < 1.5

vix_adjustment := -20

vix_adjustment

else

vix_adjustment := -40

vix_adjustment

term_structure_adjustment = backwardation ? -15 : steep_backwardation ? -30 : 5

vvix_adjustment = vvix_proxy > 2.0 ? -10 : vvix_proxy < 1.0 ? 10 : 0

sentiment_score = base_sentiment + vix_adjustment + term_structure_adjustment + vvix_adjustment

sentiment_score := math.max(0, math.min(100, sentiment_score))

// MACRO ANALYSIS

// Yield Curve

yield_spread_2_10 = us10y - us2y

yield_spread_3m_10 = us10y - us3m

// Credit Conditions

hyg_return = ta.roc(hyg, 20)

lqd_return = ta.roc(lqd, 20)

tlt_return = ta.roc(tlt, 20)

hyg_duration = 4.0

lqd_duration = 8.0

tlt_duration = 17.0

hyg_log_returns = math.log(hyg / hyg )

lqd_log_returns = math.log(lqd / lqd )

hyg_volatility = ta.stdev(hyg_log_returns, 20) * math.sqrt(252)

lqd_volatility = ta.stdev(lqd_log_returns, 20) * math.sqrt(252)

hyg_yield_proxy = -math.log(hyg / hyg ) * 100

lqd_yield_proxy = -math.log(lqd / lqd ) * 100

tlt_yield = us10y

hyg_spread = (hyg_yield_proxy - tlt_yield) * 100

lqd_spread = (lqd_yield_proxy - tlt_yield) * 100

hyg_distance = (hyg - ta.lowest(hyg, 252)) / (ta.highest(hyg, 252) - ta.lowest(hyg, 252))

lqd_distance = (lqd - ta.lowest(lqd, 252)) / (ta.highest(lqd, 252) - ta.lowest(lqd, 252))

default_risk_proxy = 2.0 - (hyg_distance + lqd_distance)

credit_spread = hyg_spread * 0.5 + (hyg_volatility - lqd_volatility) * 1000 * 0.3 + default_risk_proxy * 200 * 0.2

credit_spread := math.max(50, credit_spread)

credit_market_health = hyg_return > lqd_return ? 1 : -1

flight_to_quality = tlt_return > (hyg_return + lqd_return) / 2

// Macro Score

macro_score = 50.0

yield_curve_score = 0

if yield_spread_2_10 > 1.5 and yield_spread_3m_10 > 2

yield_curve_score := 40

yield_curve_score

else if yield_spread_2_10 > 0.5 and yield_spread_3m_10 > 1

yield_curve_score := 30

yield_curve_score

else if yield_spread_2_10 > 0 and yield_spread_3m_10 > 0

yield_curve_score := 20

yield_curve_score

else if yield_spread_2_10 < 0 or yield_spread_3m_10 < 0

yield_curve_score := 10

yield_curve_score

else

yield_curve_score := 5

yield_curve_score

credit_conditions_score = 0

if credit_spread < 200 and not flight_to_quality

credit_conditions_score := 30

credit_conditions_score

else if credit_spread < 400 and credit_market_health > 0

credit_conditions_score := 20

credit_conditions_score

else if credit_spread < 600

credit_conditions_score := 15

credit_conditions_score

else if credit_spread < 1000

credit_conditions_score := 10

credit_conditions_score

else

credit_conditions_score := 0

credit_conditions_score

financial_stability_score = 0

if spy_debt_to_equity < 0.5 and spy_return_on_equity > 15

financial_stability_score := 20

financial_stability_score

else if spy_debt_to_equity < 1.0 and spy_return_on_equity > 10

financial_stability_score := 15

financial_stability_score

else if spy_debt_to_equity < 1.5

financial_stability_score := 10

financial_stability_score

else

financial_stability_score := 5

financial_stability_score

macro_score := yield_curve_score + credit_conditions_score + financial_stability_score

macro_score := math.max(0, math.min(100, macro_score))

// CRISIS DETECTION

crisis_indicators = 0

if vix > crisis_vix_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if vix > 60

crisis_indicators := crisis_indicators + 2

crisis_indicators

if current_drawdown > crisis_drawdown_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if current_drawdown > 25

crisis_indicators := crisis_indicators + 1

crisis_indicators

if credit_spread > crisis_credit_spread

crisis_indicators := crisis_indicators + 1

crisis_indicators

sp500_roc_5 = ta.roc(sp500, 5)

tlt_roc_5 = ta.roc(tlt, 5)

if sp500_roc_5 < -10 and tlt_roc_5 < -5

crisis_indicators := crisis_indicators + 2

crisis_indicators

volume_spike = sp500_volume > ta.sma(sp500_volume, 20) * 2

sp500_roc_1 = ta.roc(sp500, 1)

if volume_spike and sp500_roc_1 < -3

crisis_indicators := crisis_indicators + 1

crisis_indicators

is_crisis = crisis_indicators >= 3

is_severe_crisis = crisis_indicators >= 5

// FINAL ALLOCATION CALCULATION

// Convert regime to base allocation

regime_allocation = market_regime == 'Strong Bull' ? 100 : market_regime == 'Bull Market' ? 80 : market_regime == 'Neutral' ? 60 : market_regime == 'Correction' ? 40 : market_regime == 'Bear Market' ? 20 : 0

// Normalize weights

total_weight = w_regime + w_risk + w_valuation + w_sentiment + w_macro

w_regime_norm = w_regime / total_weight

w_risk_norm = w_risk / total_weight

w_valuation_norm = w_valuation / total_weight

w_sentiment_norm = w_sentiment / total_weight

w_macro_norm = w_macro / total_weight

// Calculate Weighted Allocation

weighted_allocation = regime_allocation * w_regime_norm + risk_allocation * w_risk_norm + valuation_score * w_valuation_norm + sentiment_score * w_sentiment_norm + macro_score * w_macro_norm

// Apply Crisis Override

if use_crisis_detection

if is_severe_crisis

weighted_allocation := math.min(weighted_allocation, 10)

weighted_allocation

else if is_crisis

weighted_allocation := math.min(weighted_allocation, 25)

weighted_allocation

// Model Type Adjustment

model_adjustment = 0.0

if model_type == 'Conservative'

model_adjustment := -10

model_adjustment

else if model_type == 'Aggressive'

model_adjustment := 10

model_adjustment

else if model_type == 'Adaptive'

recent_return = (sp500 - sp500 ) / sp500 * 100

if recent_return > 5

model_adjustment := 5

model_adjustment

else if recent_return < -5

model_adjustment := -5

model_adjustment

// Apply adjustment and bounds

final_allocation = weighted_allocation + model_adjustment

final_allocation := math.max(0, math.min(100, final_allocation))

// Smooth allocation

smoothed_allocation = ta.sma(final_allocation, smoothing_period)

// Calculate portfolio risk metrics (only for internal alerts)

actual_portfolio_volatility = smoothed_allocation / 100 * market_volatility_20d

actual_portfolio_drawdown = smoothed_allocation / 100 * current_drawdown

// VISUALIZATION

// Color definitions

var color primary_color = #2196F3

var color bullish_color = #4CAF50

var color bearish_color = #FF5252

var color neutral_color = #808080

var color text_color = color.white

var color bg_color = #000000

var color table_bg_color = #1E1E1E

var color header_bg_color = #2D2D2D

switch color_scheme // Apply color scheme

'Gold' =>

primary_color := use_dark_mode ? #FFD700 : #DAA520

bullish_color := use_dark_mode ? #FFA500 : #FF8C00

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #C0C0C0 : #808080

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A00 : #FFFEF0

header_bg_color := use_dark_mode ? #2D2600 : #F5F5DC

header_bg_color

'EdgeTools' =>

primary_color := use_dark_mode ? #4682B4 : #1E90FF

bullish_color := use_dark_mode ? #4CAF50 : #388E3C

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #708090 : #696969

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0F1419 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A3A : #E6F3FF

header_bg_color

'Behavioral' =>

primary_color := #808080

bullish_color := #00FF00

bearish_color := #8B0000

neutral_color := #FFBF00

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A1A : #F8F8F8

header_bg_color := use_dark_mode ? #2D2D2D : #E8E8E8

header_bg_color

'Quant' =>

primary_color := #808080

bullish_color := #FFA500

bearish_color := #8B0000

neutral_color := #4682B4

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0D0D0D : #FAFAFA

header_bg_color := use_dark_mode ? #1A1A1A : #F0F0F0

header_bg_color

'Ocean' =>

primary_color := use_dark_mode ? #20B2AA : #008B8B

bullish_color := use_dark_mode ? #00CED1 : #4682B4

bearish_color := use_dark_mode ? #FF4500 : #B22222

neutral_color := use_dark_mode ? #87CEEB : #2F4F4F

text_color := use_dark_mode ? #F0F8FF : #191970

bg_color := use_dark_mode ? #001F3F : #F0F8FF

table_bg_color := use_dark_mode ? #001A2E : #E6F7FF

header_bg_color := use_dark_mode ? #002A47 : #CCF2FF

header_bg_color

'Fire' =>

primary_color := use_dark_mode ? #FF6347 : #DC143C

bullish_color := use_dark_mode ? #FFD700 : #FF8C00

bearish_color := use_dark_mode ? #8B0000 : #800000

neutral_color := use_dark_mode ? #FFA500 : #CD853F

text_color := use_dark_mode ? #FFFAF0 : #2F1B14

bg_color := use_dark_mode ? #2F1B14 : #FFFAF0

table_bg_color := use_dark_mode ? #261611 : #FFF8F0

header_bg_color := use_dark_mode ? #3D241A : #FFE4CC

header_bg_color

'Matrix' =>

primary_color := use_dark_mode ? #00FF41 : #006400

bullish_color := use_dark_mode ? #39FF14 : #228B22

bearish_color := use_dark_mode ? #FF073A : #8B0000

neutral_color := use_dark_mode ? #00FFFF : #008B8B

text_color := use_dark_mode ? #C0FF8C : #003300

bg_color := use_dark_mode ? #0D1B0D : #F0FFF0

table_bg_color := use_dark_mode ? #0A1A0A : #E8FFF0

header_bg_color := use_dark_mode ? #112B11 : #CCFFCC

header_bg_color

'Arctic' =>

primary_color := use_dark_mode ? #87CEFA : #4169E1

bullish_color := use_dark_mode ? #00BFFF : #0000CD

bearish_color := use_dark_mode ? #FF1493 : #8B008B

neutral_color := use_dark_mode ? #B0E0E6 : #483D8B

text_color := use_dark_mode ? #F8F8FF : #191970

bg_color := use_dark_mode ? #191970 : #F8F8FF

table_bg_color := use_dark_mode ? #141B47 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A5C : #E0F0FF

header_bg_color

// Transparency settings

bg_transparency = use_dark_mode ? 85 : 92

zone_transparency = use_dark_mode ? 90 : 95

band_transparency = use_dark_mode ? 70 : 85

table_transparency = use_dark_mode ? 80 : 15

// Allocation color

alloc_color = smoothed_allocation >= 80 ? bullish_color : smoothed_allocation >= 60 ? color.new(bullish_color, 30) : smoothed_allocation >= 40 ? primary_color : smoothed_allocation >= 20 ? color.new(bearish_color, 30) : bearish_color

// Dynamic background

var color dynamic_bg_color = na

if show_regime_background

if smoothed_allocation >= 70

dynamic_bg_color := color.new(bullish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation <= 30

dynamic_bg_color := color.new(bearish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation > 60 or smoothed_allocation < 40

dynamic_bg_color := color.new(primary_color, math.min(99, background_intensity + 2))

dynamic_bg_color

bgcolor(dynamic_bg_color, title = 'Allocation Signal Background')

// Plot main allocation line

plot(smoothed_allocation, 'Equity Allocation %', color = alloc_color, linewidth = math.max(1, main_line_width))

// Reference lines (static colors for hline)

hline_bullish_color = color_scheme == 'Gold' ? use_dark_mode ? #FFA500 : #FF8C00 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4CAF50 : #388E3C : color_scheme == 'Behavioral' ? #00FF00 : color_scheme == 'Quant' ? #FFA500 : color_scheme == 'Ocean' ? use_dark_mode ? #00CED1 : #4682B4 : color_scheme == 'Fire' ? use_dark_mode ? #FFD700 : #FF8C00 : color_scheme == 'Matrix' ? use_dark_mode ? #39FF14 : #228B22 : color_scheme == 'Arctic' ? use_dark_mode ? #00BFFF : #0000CD : #4CAF50

hline_bearish_color = color_scheme == 'Gold' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'EdgeTools' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'Behavioral' ? #8B0000 : color_scheme == 'Quant' ? #8B0000 : color_scheme == 'Ocean' ? use_dark_mode ? #FF4500 : #B22222 : color_scheme == 'Fire' ? use_dark_mode ? #8B0000 : #800000 : color_scheme == 'Matrix' ? use_dark_mode ? #FF073A : #8B0000 : color_scheme == 'Arctic' ? use_dark_mode ? #FF1493 : #8B008B : #FF5252

hline_primary_color = color_scheme == 'Gold' ? use_dark_mode ? #FFD700 : #DAA520 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4682B4 : #1E90FF : color_scheme == 'Behavioral' ? #808080 : color_scheme == 'Quant' ? #808080 : color_scheme == 'Ocean' ? use_dark_mode ? #20B2AA : #008B8B : color_scheme == 'Fire' ? use_dark_mode ? #FF6347 : #DC143C : color_scheme == 'Matrix' ? use_dark_mode ? #00FF41 : #006400 : color_scheme == 'Arctic' ? use_dark_mode ? #87CEFA : #4169E1 : #2196F3

hline(show_reference_lines ? 100 : na, '100% Equity', color = color.new(hline_bullish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 80 : na, '80% Equity', color = color.new(hline_bullish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 60 : na, '60% Equity', color = color.new(hline_bullish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(50, '50% Balanced', color = color.new(hline_primary_color, 50), linestyle = hline.style_solid, linewidth = 2)

hline(show_reference_lines ? 40 : na, '40% Equity', color = color.new(hline_bearish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 20 : na, '20% Equity', color = color.new(hline_bearish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 0 : na, '0% Equity', color = color.new(hline_bearish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

// Component plots

plot(show_components ? regime_allocation : na, 'Regime', color = color.new(#4ECDC4, 70), linewidth = 1)

plot(show_components ? risk_allocation : na, 'Risk', color = color.new(#FF6B6B, 70), linewidth = 1)

plot(show_components ? valuation_score : na, 'Valuation', color = color.new(#45B7D1, 70), linewidth = 1)

plot(show_components ? sentiment_score : na, 'Sentiment', color = color.new(#FFD93D, 70), linewidth = 1)

plot(show_components ? macro_score : na, 'Macro', color = color.new(#6BCF7F, 70), linewidth = 1)

// Confidence bands

upper_band = plot(show_confidence_bands ? math.min(100, smoothed_allocation + ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Upper Band')

lower_band = plot(show_confidence_bands ? math.max(0, smoothed_allocation - ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Lower Band')

fill(upper_band, lower_band, color = show_confidence_bands ? color.new(neutral_color, zone_transparency) : na, title = 'Uncertainty')

// DASHBOARD

if show_dashboard and barstate.islast

var table dashboard = table.new(position.top_right, 2, 20, border_width = 1, bgcolor = color.new(table_bg_color, table_transparency))

table.clear(dashboard, 0, 0, 1, 19)

// Header

header_color = color.new(header_bg_color, 20)

dashboard_text_color = text_color

table.cell(dashboard, 0, 0, 'DEAM', text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

table.cell(dashboard, 1, 0, model_type, text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

// Core metrics

table.cell(dashboard, 0, 1, 'Equity Allocation', text_color = dashboard_text_color, text_size = size.small)

table.cell(dashboard, 1, 1, str.tostring(smoothed_allocation, '##.#') + '%', text_color = alloc_color, text_size = size.small)

table.cell(dashboard, 0, 2, 'Cash Allocation', text_color = dashboard_text_color, text_size = size.small)

cash_color = 100 - smoothed_allocation > 70 ? bearish_color : primary_color

table.cell(dashboard, 1, 2, str.tostring(100 - smoothed_allocation, '##.#') + '%', text_color = cash_color, text_size = size.small)

// Signal

signal_text = 'NEUTRAL'

signal_color = primary_color

if smoothed_allocation >= 70

signal_text := 'BULLISH'

signal_color := bullish_color

signal_color

else if smoothed_allocation <= 30

signal_text := 'BEARISH'

signal_color := bearish_color

signal_color

table.cell(dashboard, 0, 3, 'Signal', text_color = dashboard_text_color, text_size = size.small)

table.cell(dashboard, 1, 3, signal_text, text_color = signal_color, text_size = size.small)

// Market Regime

table.cell(dashboard, 0, 4, 'Regime', text_color = dashboard_text_color, text_size = size.small)

regime_color_display = market_regime == 'Strong Bull' or market_regime == 'Bull Market' ? bullish_color : market_regime == 'Neutral' ? primary_color : market_regime == 'Crisis' ? bearish_color : bearish_color

table.cell(dashboard, 1, 4, market_regime, text_color = regime_color_display, text_size = size.small)

// VIX

table.cell(dashboard, 0, 5, 'VIX Level', text_color = dashboard_text_color, text_size = size.small)

vix_color_display = vix < 20 ? bullish_color : vix < 30 ? primary_color : bearish_color

table.cell(dashboard, 1, 5, str.tostring(vix, '##.##'), text_color = vix_color_display, text_size = size.small)

// Market Drawdown

table.cell(dashboard, 0, 6, 'Market DD', text_color = dashboard_text_color, text_size = size.small)

market_dd_color = current_drawdown < 5 ? bullish_color : current_drawdown < 10 ? primary_color : bearish_color

table.cell(dashboard, 1, 6, '-' + str.tostring(current_drawdown, '##.#') + '%', text_color = market_dd_color, text_size = size.small)

// Crisis Detection

table.cell(dashboard, 0, 7, 'Crisis Detection', text_color = dashboard_text_color, text_size = size.small)

crisis_text = is_severe_crisis ? 'SEVERE' : is_crisis ? 'CRISIS' : 'Normal'

crisis_display_color = is_severe_crisis or is_crisis ? bearish_color : bullish_color

table.cell(dashboard, 1, 7, crisis_text, text_color = crisis_display_color, text_size = size.small)

// Real Data Section

financial_bg = color.new(primary_color, 85)

table.cell(dashboard, 0, 8, 'REAL DATA', text_color = dashboard_text_color, bgcolor = financial_bg, text_size = size.small)

table.cell(dashboard, 1, 8, 'Live Metrics', text_color = dashboard_text_color, bgcolor = financial_bg, text_size = size.small)

// P/E Ratio

table.cell(dashboard, 0, 9, 'P/E Ratio', text_color = dashboard_text_color, text_size = size.small)

pe_color = actual_pe_ratio < 18 ? bullish_color : actual_pe_ratio < 25 ? primary_color : bearish_color

table.cell(dashboard, 1, 9, str.tostring(actual_pe_ratio, '##.#'), text_color = pe_color, text_size = size.small)

// ERP

table.cell(dashboard, 0, 10, 'ERP', text_color = dashboard_text_color, text_size = size.small)

erp_color = equity_risk_premium > 2 ? bullish_color : equity_risk_premium > 0 ? primary_color : bearish_color

table.cell(dashboard, 1, 10, str.tostring(equity_risk_premium, '##.##') + '%', text_color = erp_color, text_size = size.small)

// ROE

table.cell(dashboard, 0, 11, 'ROE', text_color = dashboard_text_color, text_size = size.small)

roe_color = spy_return_on_equity > 20 ? bullish_color : spy_return_on_equity > 10 ? primary_color : bearish_color

table.cell(dashboard, 1, 11, str.tostring(spy_return_on_equity, '##.#') + '%', text_color = roe_color, text_size = size.small)

// D/E Ratio

table.cell(dashboard, 0, 12, 'D/E Ratio', text_color = dashboard_text_color, text_size = size.small)

de_color = spy_debt_to_equity < 0.5 ? bullish_color : spy_debt_to_equity < 1.0 ? primary_color : bearish_color

table.cell(dashboard, 1, 12, str.tostring(spy_debt_to_equity, '##.##'), text_color = de_color, text_size = size.small)

// Shareholder Yield

table.cell(dashboard, 0, 13, 'Dividend+Buyback', text_color = dashboard_text_color, text_size = size.small)

yield_color = total_shareholder_yield > 4 ? bullish_color : total_shareholder_yield > 2 ? primary_color : bearish_color

table.cell(dashboard, 1, 13, str.tostring(total_shareholder_yield, '##.#') + '%', text_color = yield_color, text_size = size.small)

// Component Scores

component_bg = color.new(neutral_color, 80)

table.cell(dashboard, 0, 14, 'Components', text_color = dashboard_text_color, bgcolor = component_bg, text_size = size.small)

table.cell(dashboard, 1, 14, 'Scores', text_color = dashboard_text_color, bgcolor = component_bg, text_size = size.small)

table.cell(dashboard, 0, 15, 'Regime', text_color = dashboard_text_color, text_size = size.small)

regime_score_color = regime_allocation > 60 ? bullish_color : regime_allocation < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 15, str.tostring(regime_allocation, '##'), text_color = regime_score_color, text_size = size.small)

table.cell(dashboard, 0, 16, 'Risk', text_color = dashboard_text_color, text_size = size.small)

risk_score_color = risk_allocation > 60 ? bullish_color : risk_allocation < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 16, str.tostring(risk_allocation, '##'), text_color = risk_score_color, text_size = size.small)

table.cell(dashboard, 0, 17, 'Valuation', text_color = dashboard_text_color, text_size = size.small)

val_score_color = valuation_score > 60 ? bullish_color : valuation_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 17, str.tostring(valuation_score, '##'), text_color = val_score_color, text_size = size.small)

table.cell(dashboard, 0, 18, 'Sentiment', text_color = dashboard_text_color, text_size = size.small)

sent_score_color = sentiment_score > 60 ? bullish_color : sentiment_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 18, str.tostring(sentiment_score, '##'), text_color = sent_score_color, text_size = size.small)

table.cell(dashboard, 0, 19, 'Macro', text_color = dashboard_text_color, text_size = size.small)

macro_score_color = macro_score > 60 ? bullish_color : macro_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 19, str.tostring(macro_score, '##'), text_color = macro_score_color, text_size = size.small)

// ALERTS

// Major allocation changes

alertcondition(smoothed_allocation >= 80 and smoothed_allocation < 80, 'High Equity Allocation', 'Equity allocation reached 80% - Bull market conditions')

alertcondition(smoothed_allocation <= 20 and smoothed_allocation > 20, 'Low Equity Allocation', 'Equity allocation dropped to 20% - Defensive positioning')

// Crisis alerts

alertcondition(is_crisis and not is_crisis , 'CRISIS DETECTED', 'Crisis conditions detected - Reducing equity allocation')

alertcondition(is_severe_crisis and not is_severe_crisis , 'SEVERE CRISIS', 'Severe crisis detected - Maximum defensive positioning')

// Regime changes

regime_changed = market_regime != market_regime

alertcondition(regime_changed, 'Regime Change', 'Market regime has changed')

// Risk management alerts

risk_breach = enable_portfolio_risk_scaling and (actual_portfolio_volatility > target_portfolio_volatility * 1.2 or actual_portfolio_drawdown > max_portfolio_drawdown * 1.2)

alertcondition(risk_breach, 'Risk Breach', 'Portfolio risk exceeds target parameters')

// USAGE

// The indicator displays a recommended equity allocation percentage (0-100%).

// Example: 75% allocation = 75% stocks, 25% cash/bonds.

//

// The model combines market regime analysis (trend, volatility, drawdowns),

// risk management (portfolio-level targeting), valuation metrics (P/E, ERP),

// sentiment indicators (VIX term structure), and macro factors (yield curve,

// credit spreads) into a single allocation signal.

//

// Crisis detection automatically reduces exposure when multiple warning signals

// converge. Alerts available for major allocation shifts and regime changes.

//

// Designed for SPY/S&P 500 portfolio allocation. Adjust component weights and

// risk parameters in settings to match your risk tolerance.

View in Pine

Moving VWAP-KAMA CloudMoving VWAP-KAMA Cloud

Overview

The Moving VWAP-KAMA Cloud is a high-conviction trend filter designed to solve a major problem with standard indicators: Noise. By combining a smoothed Volume Weighted Average Price (MVWAP) with Kaufman’s Adaptive Moving Average (KAMA), this indicator creates a "Value Zone" that identifies the true structural trend while ignoring choppy price action.

Unlike brittle lines that break constantly, this cloud is "slow" by design—making it exceptionally powerful for spotting genuine trend reversals and filtering out fakeouts.

How It Works

This script uses a unique "Double Smoothing" architecture:

The Anchor (MVWAP): We take the standard VWAP and smooth it with a 30-period EMA. This represents the "Fair Value" baseline where volume has supported price over time.

The Filter (KAMA): We apply Kaufman's Adaptive Moving Average to the already smoothed MVWAP. KAMA is unique because it flattens out during low-volatility (choppy) periods and speeds up during high-momentum trends.

The Cloud:

Green/Teal Cloud: Bullish Structure (MVWAP > KAMA)

Purple Cloud: Bearish Structure (MVWAP < KAMA)

🔥 The "Reversal Slingshot" Strategy

Backtests reveal a powerful behavior during major trend changes, particularly after long bear markets:

The Resistance Phase: During a long-term downtrend, price will repeatedly rally into the Purple Cloud and get rejected. The flattened KAMA line acts as a "concrete ceiling," keeping the bearish trend intact.

The Breakout & Flip: When price finally breaks above the cloud with conviction, and the cloud flips Green, it signals a structural regime change.

The "Slingshot" Retest: Often, immediately after this flip, price will drop back into the top of the cloud. This is the "Slingshot" moment. The old resistance becomes new, hardened support.

The Rally: From this support bounce, stocks often launch into a sustained, multi-month bull run. This setup has been observed repeatedly at the bottom of major corrections.

How to Use This Indicator

1. Dynamic Support & Resistance

The KAMA Wall: When price retraces into the cloud, the KAMA line often flattens out, acting as a hard "floor" or "wall." A break of this wall usually signals a genuine trend change, not just a stop hunt.

2. Trend Confirmation (Regime Filter)

Bullish Regime: If price is holding above the cloud, only look for Long setups.

Bearish Regime: If price is holding below the cloud, only look for Short setups.

No-Trade Zone: If price is stuck inside the cloud, the market is traversing fair value. Stand aside until a clear winner emerges.

3. Multi-Timeframe Versatility

While designed for trend confirmation on higher timeframes (4H, Daily), this indicator adapts beautifully to lower timeframes (5m, 15m) for intraday scalping.

On Lower Timeframes: The cloud reacts much faster, acting as a dynamic "VWAP Band" that helps intraday traders stay on the right side of momentum during the session.

Settings

Moving VWAP Period (30): The lookback period for the base VWAP smoothing.

KAMA Settings (10, 10, 30): Controls the sensitivity of the adaptive filter.

Cloud Transparency: Adjust to keep your chart clean.

Alerts Included

Price Cross Over/Under MVWAP

Price Cross Over/Under KAMA

Cloud Flip (Bullish/Bearish Trend Change)

Tip for Traders

This is not a signal entry indicator. It is a Trend Conviction tool. Use it to filter your entries from faster indicators (like RSI or MACD). If your fast indicator signals "Buy" but the cloud is Purple, the probability is low. Wait for the Cloud Flip

Debt-Cycle vs Bitcoin-CycleDebt-Cycle vs Bitcoin-Cycle Indicator

The Debt-Cycle vs Bitcoin-Cycle indicator is a macro-economic analysis tool that compares traditional financial market cycles (debt/credit cycles) against Bitcoin market cycles. It uses Z-score normalization to track the relative positioning of global financial conditions versus cryptocurrency market sentiment, helping identify potential turning points and divergences between traditional finance and digital assets.

Key Features

Dual-Cycle Analysis: Simultaneously tracks traditional financial cycles and Bitcoin-specific cycles

Z-Score Normalization: Standardizes diverse data sources for meaningful comparison

Multi-Asset Coverage: Analyzes currencies, commodities, bonds, monetary aggregates, and on-chain metrics

Divergence Detection: Identifies when Bitcoin cycles move independently from traditional finance

21-Day Timeframe: Optimized for Long-term cycle analysis

What It Measures

Finance-Cycle (White Line)

Tracks traditional financial market health through:

Currencies: USD strength (DXY), global currency weights (USDWCU, EURWCU)

Commodities: Oil, gold, natural gas, agricultural products, and Bitcoin price

Corporate Bonds: Investment-grade spreads, high-yield spreads, credit conditions

Monetary Aggregates: M2 money supply, foreign exchange reserves (weighted by currency)

Treasury Bonds: Yield curve (2Y/10Y, 3M/10Y), term premiums, long-term rates

Bitcoin-Cycle (Orange Line)

Tracks Bitcoin market positioning through:

On-Chain Metrics:

MVRV Ratio (Market Value to Realized Value)

NUPL (Net Unrealized Profit/Loss)

Profit/Loss Address Distribution

Technical Indicators:

Bitcoin price Z-score

Moving average deviation

Relative Strength:

ETH/BTC ratio (altcoin strength indicator)

Visual Elements

White Line: Finance-Cycle indicator (positive = expansionary conditions, negative = contractionary)

Orange Line: Bitcoin-Cycle indicator (positive = bullish positioning, negative = bearish)

Zero Line: Neutral reference point

Interpretation

Cycle Alignment

Both positive: Risk-on environment, favorable for crypto

Both negative: Risk-off environment, caution warranted

Divergence: Potential opportunities or warning signals

Divergence Signals

Finance positive, Bitcoin negative: Bitcoin may be undervalued relative to macro conditions

Finance negative, Bitcoin positive: Bitcoin may be overextended or decoupling from traditional finance

Important Limitations

This indicator uses some technical and macro data but still has significant gaps:

⚠️ Limited monetary data - missing:

Funding rates (repo, overnight markets)

Comprehensive bond spread analysis

Collateral velocity and quality metrics

Central bank balance sheet details

⚠️ Basic economic coverage - missing:

GDP growth rates

Inflation expectations

Employment data

Manufacturing indices

Consumer confidence

⚠️ Simplified on-chain analysis - missing:

Exchange flow data

Whale wallet movements

Mining difficulty adjustments

Hash rate trends

Network fee dynamics

⚠️ No sentiment data - missing:

Fear & Greed Index

Options positioning

Futures open interest

Social media sentiment

The indicator provides a high-level cycle comparison but should be combined with comprehensive fundamental analysis, detailed on-chain research, and proper risk management.

Settings

Offset: Adjust the horizontal positioning of the indicators (default: 0)

Timeframe: Fixed at 21 days for optimal cycle detection

Use Cases

Macro-crypto correlation analysis: Understand when Bitcoin moves with or against traditional markets

Cycle timing: Identify potential tops and bottoms in both cycles

Risk assessment: Gauge overall market conditions across asset classes

Divergence trading: Spot opportunities when cycles diverge significantly

Portfolio allocation: Balance traditional and crypto assets based on cycle positioning

Technical Notes

Uses Z-score normalization with varying lookback periods (40-60 bars)

Applies HMA (Hull Moving Average) smoothing to reduce noise

Asymmetric multipliers for upside/downside movements in certain metrics

Requires access to FRED economic data, Glassnode, CoinMetrics, and IntoTheBlock feeds

21-day timeframe optimized for cycle analysis

Strategy Applications

This indicator is particularly useful for:

Cross-asset allocation - Decide between traditional finance and crypto exposure

Cycle positioning - Identify where we are in credit/debt cycles vs. Bitcoin cycles

Regime changes - Detect shifts in market leadership and correlation patterns

Risk management - Reduce exposure when both cycles turn negative

Disclaimer: This indicator is a cycle analysis tool and should not be used as the sole basis for investment decisions. It has limited coverage of monetary conditions, economic fundamentals, and on-chain metrics. The indicator provides directional insight but cannot predict exact timing or magnitude of market moves. Always conduct thorough research, consider multiple data sources, and maintain proper risk management in all investment decisions.

Multi-Timeframe Supertrend + MACD + MTF Dashboard if you like it click source code and save it in notepad for back up .

The Multi-Timeframe Supertrend Dashboard is a powerful tool designed to give traders a clear view of market trends across multiple timeframes, all from a single dashboard. This indicator leverages the Supertrend method to calculate buy and sell signals based on the direction of price relative to dynamically calculated support and resistance lines. The dashboard is optimized for dark mode and provides easy-to-interpret color-coded signals for each timeframe.

How It Works

The Supertrend indicator is a trend-following indicator that uses the Average True Range (ATR) to set upper and lower bands around the price, adapting dynamically as volatility changes. When the price is above the Supertrend line, the market is considered in an uptrend, triggering a "BUY" signal. Conversely, when the price falls below the Supertrend line, the market is in a downtrend, triggering a "SELL" signal.

This Multi-Timeframe Supertrend Dashboard calculates Supertrend signals for the following timeframes:

1 minute

5 minutes

15 minutes

1 hour

Daily

Weekly

Monthly

For each timeframe, the dashboard shows either a "BUY" or "SELL" signal, allowing traders to assess whether trends align across timeframes. A "BUY" signal displays in green, and a "SELL" signal displays in red, giving a quick visual reference of the overall trend direction for each timeframe.

Customization Options

ATR Period: Defines the period for the Average True Range (ATR) calculation, which determines how responsive the Supertrend lines are to changes in market volatility.

Multiplier: Sets the sensitivity of the Supertrend bands to price movements. Higher values make the bands less sensitive, while lower values increase sensitivity, allowing quicker reactions to changes in price.

How to Interpret the Dashboard

The Multi-Timeframe Supertrend Dashboard allows traders to see at a glance if trends across multiple timeframes are aligned. Here’s how to interpret the signals:

BUY (Green): The current timeframe’s price is in an uptrend based on the Supertrend calculation.

SELL (Red): The current timeframe’s price is in a downtrend based on the Supertrend calculation.

For example:

If all timeframes display "BUY," the asset is in a strong uptrend across multiple time horizons, which may indicate a bullish market.

If all timeframes display "SELL," the asset is likely in a strong downtrend, signaling a bearish market.

Mixed signals across timeframes suggest market consolidation or differing trends across short- and long-term periods.

Use Cases

Trend Confirmation: Use the dashboard to confirm trends across multiple timeframes before entering or exiting a position.

Quick Market Analysis: Get a snapshot of market conditions across timeframes without having to change charts.

Multi-Timeframe Alignment: Identify alignment across timeframes, which is often a strong indicator of market momentum in one direction.

Dark Mode Optimization

The dashboard has been optimized for dark mode, with white text and contrasting background colors to ensure easy readability on darker TradingView themes.

Nov 4, 2024

Release Notes

Multi-Timeframe Supertrend Dashboard with Alerts

Overview

The Multi-Timeframe Supertrend Dashboard with Alerts is a powerful indicator designed to give traders a comprehensive view of market trends across multiple timeframes. This dashboard uses the Supertrend method to calculate buy and sell signals based on the direction of price relative to dynamic support and resistance levels. The indicator is optimized for dark mode and provides a color-coded display of buy and sell signals for each timeframe, along with optional alerts for trend alignment.

How It Works

The Supertrend indicator is a trend-following indicator that uses the Average True Range (ATR) to set upper and lower bands around the price, adjusting dynamically with market volatility. When the price is above the Supertrend line, the market is considered in an uptrend, triggering a "BUY" signal. Conversely, when the price falls below the Supertrend line, the market is in a downtrend, triggering a "SELL" signal.

The Multi-Timeframe Supertrend Dashboard displays Supertrend signals for the following timeframes:

1 minute

5 minutes

15 minutes

1 hour

Daily

Weekly

Monthly

For each timeframe, the dashboard shows either a "BUY" or "SELL" signal, allowing traders to assess trend alignment across multiple timeframes with a single glance. A "BUY" signal displays in green, and a "SELL" signal displays in red.

Alerts for Trend Alignment

This indicator includes built-in alert conditions that allow traders to receive notifications when all timeframes simultaneously align in a "BUY" or "SELL" signal. This is particularly useful for identifying moments of strong trend alignment across short-term and long-term timeframes. The alerts can be set to notify the trader when:

All timeframes display a "BUY" signal, indicating a strong bullish alignment across all time horizons.

All timeframes display a "SELL" signal, signaling a strong bearish alignment.

Customization Options

ATR Period: Defines the period for the Average True Range (ATR) calculation, which determines how responsive the Supertrend lines are to changes in market volatility.

Multiplier: Sets the sensitivity of the Supertrend bands to price movements. Higher values make the bands less sensitive, while lower values increase sensitivity, allowing quicker reactions to changes in price.

How to Interpret the Dashboard

BUY (Green): The price is above the Supertrend line, indicating an uptrend for that timeframe.

SELL (Red): The price is below the Supertrend line, indicating a downtrend for that timeframe.

Examples:

If all timeframes display "BUY," the asset is in a strong uptrend across multiple time horizons, signaling potential buying opportunities.

If all timeframes display "SELL," the asset is likely in a strong downtrend, signaling potential selling opportunities.

Mixed signals suggest a consolidation phase or differing trends across short- and long-term periods.

Use Cases

Trend Confirmation: Use the dashboard to confirm trends across multiple timeframes before entering or exiting a position.

Alert Notifications: Set alerts to receive notifications when all timeframes align in a "BUY" or "SELL" signal.

Quick Market Analysis: Get an instant overview of market conditions without switching between charts.

Multi-Timeframe Alignment: Identify alignment across timeframes, often a strong indicator of market momentum in one direction.

Dark Mode Optimization

The dashboard has been optimized for dark mode, with white text and contrasting background colors to ensure easy readability on darker TradingView themes.

Nov 6, 2024

Release Notes

Multi-Timeframe Supertrend Dashboard with Custom Alerts

Description:

This Multi-Timeframe Supertrend Dashboard indicator provides a powerful tool for traders who want to monitor multiple timeframes simultaneously and receive alerts when all timeframes align on a single trend (either BUY or SELL). The indicator uses the popular Supertrend calculation, with customizable ATR (Average True Range) period and multiplier values to tailor sensitivity to your trading style.

Key Features:

Customizable Timeframes:

Track and display up to six timeframes, fully configurable to meet any trading strategy. The default timeframes include 1 Minute, 5 Minutes, 15 Minutes, 1 Hour, 1 Day, and 1 Week but can be changed to any intervals supported by TradingView.

Selective Display Options:

With a user-friendly display selection, you can choose which timeframes to show on the dashboard. For example, you may choose to view only Timeframe 1 through Timeframe 5 or any combination of the six.

Real-Time Alignment Alerts:

Alerts can be set to trigger when all selected timeframes align on a BUY or SELL signal. This feature enables traders to catch strong trends across timeframes without constant monitoring. Alerts are fully configurable, allowing for sound notifications, email alerts, or even webhook notifications to automated trading systems.

Custom Supertrend Settings:

Adjust the ATR Period and Multiplier values to control the Supertrend's sensitivity. Lower values result in more frequent trend changes, while higher values smooth out the trend and focus on larger market moves.

Intuitive Color-Coded Dashboard:

The dashboard is visually optimized for quick insights:

Green cells indicate a BUY trend.

Red cells indicate a SELL trend.

Background color changes when all selected timeframes align, giving an instant visual cue for strong trends.

How to Use:

Select Timeframes:

Go to the input settings to choose the timeframes you want to monitor. Each timeframe is labeled (e.g., Timeframe 1, Timeframe 2) for easy reference.

Configure Display Preferences:

Enable or disable specific timeframes to customize your dashboard view. This is useful for focusing only on timeframes relevant to your strategy.

Set ATR and Multiplier Values:

Adjust these settings to define the Supertrend calculation's responsiveness. This customization allows adaptation to various markets, including stocks, forex, and cryptocurrencies.

Enable Alerts:

Turn on alerts to receive notifications when all active timeframes align. Customize the alert type and delivery (sound, popup, email, etc.) to ensure you’re notified on time.

Ideal For:

Trend Traders who want confirmation of trends across multiple timeframes.

Scalpers and Day Traders looking for quick trend changes with smaller timeframes.

Swing Traders who want a broader overview of market alignment across hourly and daily frames.

Automated System Developers looking for reliable signals across multiple timeframes to integrate with other strategies.

EMA CloudSimple EMA cloud using a fast, a slow and an optinal middle EMA.

It has EMA, EMA cloud and candle coloring depending on whether it's a downtrend or an uptrend.

It has a dashboard also with 4 customizable time frames that tells you if they are bullish or bearish and tells you the strength of the trend for the timeframe you are viewing.

Smart Money COTThis indicator implements the method of analysing COT data as defined by Michael Huddleston (I.E. The Inner Circle Trader). It removes all superfluous information contained in the standard COT reports and focusses only on Commercial speculators using the overall Long-Short positions.

Features

The unique feature of this indicator is its ability to look back over time and provide the following information:

Calculation of the range high and low of the specified lookback range.

Calculation of equilibrium of that range.

Automatic colour coding of net long and net short positions when the Long-Short COT calculation is above or below equilibrium of the lookback range.

Instructions

Use the Daily Timeframe only. You may get unexpected results on other timeframes.

Ensure the asset has COT data available. Script is mainly focused on commodity futures, such as ES, NQ, YM. It has not been tested against Forex.

You will need to define the "Lookback" setting in the script settings. Use the total number of trading days required for your analysis. E.g. if you want a 6 month COT analysis, use the measurement tool to count the quantity of daily candles between now and 6 months ago - use this as your Lookback setting. Adjust as needed for other lookback periods, e.g. 3 months, 12 months etc.

Other Info

The script provides the ability to customise colours in its settings.

Range High and Range Low plots can be disabled in settings.

jhehli LiquidityWhat are BSL and SSL?

In the context of Smart Money Concepts, liquidity simply refers to pending orders—specifically Stop Losses and Buy/Sell Stop orders—resting above old highs and below old lows.

BSL (Buy-Side Liquidity): This is found above Swing Highs. Retail traders who are short the market will place their "Buy Stop" protective orders here. Additionally, breakout traders place "Buy Limit" orders here. Smart Money views this area as a pool of willing buyers. To fill large sell orders, institutions must drive price up into this liquidity to pair their massive sell interest with these buy stops.

SSL (Sell-Side Liquidity): This is found below Swing Lows. Retail traders who are long the market place their "Sell Stop" protective orders here. Smart Money targets these levels to accumulate long positions. They need the market to sell off into these levels so they can buy from the willing sellers at a discount.

How this Indicator Works

This tool automates the process of market structure analysis by identifying key Swing Highs and Swing Lows.

Detection: It scans price action to find fractal highs and lows (classic swing points) where price has rejected a level.

Visualization: It projects a line from these points, clearly marking where the "stops" are likely residing.

Liquidity Raids: When price pierces these levels, it is considered a "Liquidity Raid" or "Stop Hunt."

How to Use This in Your Trading

Do not treat these lines simply as Support and Resistance. In the ICT methodology, old highs and lows are targets, not barriers.

For Reversals: Wait for a "Turtle Soup" or "Judas Swing." This occurs when price aggressively expands into a BSL or SSL level to trigger stops, only to quickly reverse back into the trading range. This indicates that Smart Money has finished their accumulation or distribution.

For Bias: If the higher timeframe trend is Bullish, expect SSL to be raided to fuel the move, while BSL becomes the target (Draw on Liquidity).

By using this indicator, you remove the guesswork of manually marking every swing point, allowing you to focus on price action and the reaction at these critical liquidity pools.

Delta Zones Smart Money Concept (SMC) UT Trend Reversal Mul.Sig.🚀 What's New in This Version (V5 Update)

This version is a major overhaul focused on improving trade entry timing and risk management through enhanced UT Bot functionality:

Integrated UT Trailing Stop (ATR-based): The primary trend filter and moving stop-loss mechanism is now fully integrated.

Pre-Warning Line: A revolutionary feature that alerts traders when the price penetrates a specific percentage distance (customizable) from the UT Trailing Stop before the main reversal signal fires.

"Ready" Signal: Plots a "Ready" warning label on the chart and triggers an alert condition (UT Ready Long/Short) for pre-emptive trade preparation.

V5 Compatibility: All code has been optimized for Pine Script version 5, utilizing the modern array and type structures for efficient Order Block and Breaker Block detection.

💡 How to Use This Indicator

This indicator works best when confirming signals across different components:

1. Identify the Trend Bias (UT Trailing Stop)

Uptrend: UT Trailing Stop line is Green (Focus only on Buy/Long opportunities).

Downtrend: UT Trailing Stop line is Red (Focus only on Sell/Short opportunities).

2. Prepare for Entry (Warning Line)

Action: When you see the "Ready" label or the price hits the Pre-Warning Line (Dotted Orange Line), this is your alert to prepare for a trend flip, or to tighten the stop on your current trade.

3. Confirm the Entry (Multi-Signals)

Look for a primary entry signal that aligns with the desired trend:

High-Conviction Entry: Wait for the UT Buy/Sell label (confirmed trend flip) AND a Combined Buy/Sell arrow (confirmed by your selected Oscillator settings).

High-Liquidity Entry: Look for a Delta Zone Box forming near an active Order Block or Breaker Block (SMC zones), and then confirm with a UT or Combined Signal.

4. Manage Risk (Trailing Stop)