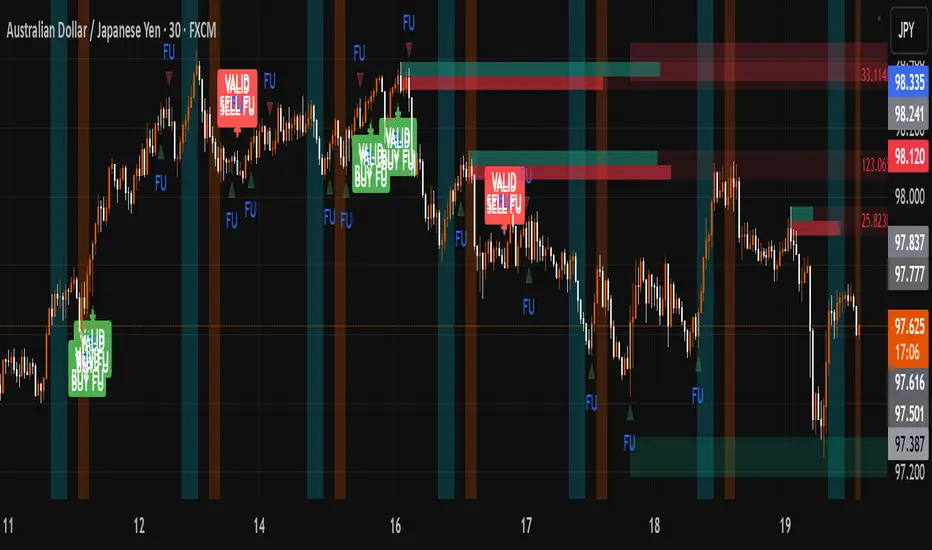

FU + SMI Validator (Proper FU, 30m)Overview

The FU + SMI Validator is a sophisticated technical analysis indicator designed to detect Proper FU (Fakeouts or Liquidity Sweeps) on the 30-minute timeframe. This tool aims to help traders identify high-probability reversal setups that occur when price briefly breaks key levels (sweeping liquidity), then reverses with momentum confirmation.

Fakeouts are common market events where price action “hunts stops” before reversing direction. Correctly identifying these events can offer excellent entry points with defined risk. This indicator combines price action logic with momentum and volatility filters to provide reliable signals.

Core Concepts

Proper FU (Fakeout) Detection

At its core, the script identifies proper fakeouts by checking if the current bar’s price:

For bullish fakeouts: dips below the previous bar’s low (sweeping stops) and then closes above the previous bar’s high

For bearish fakeouts: spikes above the previous bar’s high and then closes below the previous bar’s low

This ensures that the breakout is a true sweep rather than just a one-sided close.

Optionally, the script can require one additional confirmation bar after the FU, ensuring that the momentum is sustained and reducing false signals.

SMI-style Momentum Validation

To improve the quality of signals, the indicator uses a proxy for the Stochastic Momentum Index (SMI) by calculating the difference between current and past linear regression slopes of price. This momentum check helps ensure that fakeouts occur alongside actual directional strength.

Key points:

Momentum must be increasing in the direction of the FU signal.

Momentum filters can be enabled or disabled based on user preference.

Squeeze Condition to Avoid Low-Volatility Traps

The script includes a volatility filter based on a squeeze-like condition:

It compares Bollinger Bands (BB) and Keltner Channels (KC).

When BB bands contract inside KC bands, the market is in a squeeze state, signaling low volatility.

Fakeouts during squeeze conditions are often unreliable; the script can filter these out to reduce false alarms.

Killzone Session Timing Filter

Recognizing that liquidity and volatility vary by session, this tool supports optional filtering for:

London Killzone: 09:00 to 10:30 (UK time)

New York Killzone: 13:00 to 14:30 (UK time)

Signals only trigger during these high-activity windows if enabled, helping traders focus on periods with the best liquidity and market participation.

Note: For Killzone filtering to work accurately, your TradingView chart must be set to the UK timezone.

Features & Benefits

Robust FU detection ensures the breakout price action is meaningful, reducing noise.

Momentum filter via linear regression slope captures trend strength in a smooth, mathematically sound way.

Low-volatility squeeze avoidance helps reduce false signals in choppy or range-bound markets.

Killzone timing filter focuses your attention on the most liquid and active market hours.

Optional confirmation bar increases signal reliability.

Raw FU markers allow visualization of all detected fakeouts for pattern recognition and manual analysis.

Alerts built-in for both valid buy and sell FU setups, enabling real-time notification and quicker decision-making.

Customization Options

Killzone usage: Enable or disable the session timing filter.

Sessions: Configure London and New York killzone time ranges.

Momentum alignment: Enable or disable momentum filter based on SMI proxy.

Volatility filter: Avoid signals during squeeze or low-volatility conditions.

FU confirmation: Option to require one additional confirming candle after the initial FU.

Squeeze and momentum parameters: Adjust Bollinger Bands length and multiplier, Keltner Channel length and ATR multiplier.

Raw FU markers: Show or hide all detected fakeouts regardless of filters.

How to Use This Indicator

Apply to 30-minute charts for forex pairs, indices, cryptocurrencies, or other instruments.

Set your chart timezone to UK time if using Killzone filters.

Adjust input parameters based on your preferred sessions and risk tolerance.

Look for green “VALID BUY FU” labels below bars for bullish fakeout entries.

Look for red “VALID SELL FU” labels above bars for bearish fakeout entries.

Use the alert system to receive notifications on setups.

Combine with your existing analysis or risk management strategy for entries, stops, and profit targets.

Why Use FU + SMI Validator?

Fakeouts are some of the most lucrative but tricky setups for many traders. Without proper filters, they can lead to false entries and losses. This script integrates price action, momentum, volatility, and session timing into one package, providing a robust tool to spot high-quality fakeout opportunities and improve trading confidence.

Limitations

Requires chart to be set to UK timezone for session filters.

Designed specifically for 30-minute timeframe — performance on other timeframes may vary.

Momentum is a proxy, not a direct SMI calculation.

Like all indicators, best used in conjunction with sound risk management and other analysis tools.

Potential Enhancements

Conversion into a full strategy script for backtesting entries and exits.

Addition of other momentum indicators (RSI, MACD) or volume filters.

Customizable time zones or auto time zone detection.

Multi-timeframe analysis capabilities.

Visual dashboard for summary of signal stats.

Поиск скриптов по запросу "one一季度财报"

LSMAsThis indicator calculates and plots two Least Squares Moving Averages (LSMA) based on different lengths and a Smoothed Moving Average (SMMA) of the longer LSMA.

Inputs

lengthA : Period length for the first, longer LSMA.

lengthB : Period length for the second, shorter LSMA.

signAl : Signal period used in SMMA smoothing.

Calculations

LSMA-A and LSMA-B : Calculates the linear regression (least squares) of source over lengthA and lengthB respectively, with no offset. These represent two LSMAs, one slow and one fast.

SMMA : This is a smoothed moving average of the longer LSMA (LSMA-A).

Purpose

This indicator helps traders identify trend directions and momentum by using two least squares regression lines of different lengths to capture short- and long-term trends in price. The SMMA smoothing of the longer LSMA may be used as a signal or confirmation line to reduce noise and produce smoother signals.

It generates buy and sell signals based on the intersection of the LSMA-A and SMMA. If the LSMA-A crosses the SMMA upwards, a BUY signal is generated; if it crosses the SMMA downwards, a SELL signal is generated.

The LSMA-B, which is short-term, can be used for wave analysis. When a peak forms, a high is observed on the chart, and when a valley forms, a low is observed. This allows us to determine whether the wave is rising or falling.

Summary

Two LSMAs are calculated: one slow (lengthA), one fast (lengthB).

A smoothed moving average (SMMA) of the slow LSMA is computed using the signal length (signAl).

All three curves are overlaid on the price chart for visual trend and momentum analysis.

FiniteStateMachine🟩 OVERVIEW

A flexible framework for creating, testing and implementing a Finite State Machine (FSM) in your script. FSMs use rules to control how states change in response to events.

This is the first Finite State Machine library on TradingView and it's quite a different way to think about your script's logic. Advantages of using this vs hardcoding all your logic include:

• Explicit logic : You can see all rules easily side-by-side.

• Validation : Tables show your rules and validation results right on the chart.

• Dual approach : Simple matrix for straightforward transitions; map implementation for concurrent scenarios. You can combine them for complex needs.

• Type safety : Shows how to use enums for robustness while maintaining string compatibility.

• Real-world examples : Includes both conceptual (traffic lights) and practical (trading strategy) demonstrations.

• Priority control : Explicit control over which rules take precedence when multiple conditions are met.

• Wildcard system : Flexible pattern matching for states and events.

The library seems complex, but it's not really. Your conditions, events, and their potential interactions are complex. The FSM makes them all explicit, which is some work. However, like all "good" pain in life, this is front-loaded, and *saves* pain later, in the form of unintended interactions and bugs that are very hard to find and fix.

🟩 SIMPLE FSM (MATRIX-BASED)

The simple FSM uses a matrix to define transition rules with the structure: state > event > state. We look up the current state, check if the event in that row matches, and if it does, output the resulting state.

Each row in the matrix defines one rule, and the first matching row, counting from the top down, is applied.

A limitation of this method is that you can supply only ONE event.

You can design layered rules using widlcards. Use an empty string "" or the special string "ANY" for any state or event wildcard.

The matrix FSM is foruse where you have clear, sequential state transitions triggered by single events. Think traffic lights, or any logic where only one thing can happen at a time.

The demo for this FSM is of traffic lights.

🟩 CONCURRENT FSM (MAP-BASED)

The map FSM uses a more complex structure where each state is a key in the map, and its value is an array of event rules. Each rule maps a named condition to an output (event or next state).

This FSM can handle multiple conditions simultaneously. Rules added first have higher priority.

Adding more rules to existing states combines the entries in the map (if you use the supplied helper function) rather than overwriting them.

This FSM is for more complex scenarios where multiple conditions can be true simultaneously, and you need to control which takes precedence. Like trading strategies, or any system with concurrent conditions.

The demo for this FSM is a trading strategy.

🟩 HOW TO USE

Pine Script libraries contain reusable code for importing into indicators. You do not need to copy any code out of here. Just import the library and call the function you want.

For example, for version 1 of this library, import it like this:

import SimpleCryptoLife/FiniteStateMachine/1

See the EXAMPLE USAGE sections within the library for examples of calling the functions.

For more information on libraries and incorporating them into your scripts, see the Libraries section of the Pine Script User Manual.

🟩 TECHNICAL IMPLEMENTATION

Both FSM implementations support wildcards using blank strings "" or the special string "ANY". Wildcards match in this priority order:

• Exact state + exact event match

• Exact state + empty event (event wildcard)

• Empty state + exact event (state wildcard)

• Empty state + empty event (full wildcard)

When multiple rules match the same state + event combination, the FIRST rule encountered takes priority. In the matrix FSM, this means row order determines priority. In the map FSM, it's the order you add rules to each state.

The library uses user-defined types for the map FSM:

• o_eventRule : Maps a condition name to an output

• o_eventRuleWrapper : Wraps an array of rules (since maps can't contain arrays directly)

Everything uses strings for maximum library compatibility, though the examples show how to use enums for type safety by converting them to strings.

Unlike normal maps where adding a duplicate key overwrites the value, this library's `m_addRuleToEventMap()` method *combines* rules, making it intuitive to build rule sets without breaking them.

🟩 VALIDATION & ERROR HANDLING

The library includes comprehensive validation functions that catch common FSM design errors:

Error detection:

• Empty next states

• Invalid states not in the states array

• Duplicate rules

• Conflicting transitions

• Unreachable states (no entry/exit rules)

Warning detection:

• Redundant wildcards

• Empty states/events (potential unintended wildcards)

• Duplicate conditions within states

You can display validation results in tables on the chart, with tooltips providing detailed explanations. The helper functions to display the tables are exported so you can call them from your own script.

🟩 PRACTICAL EXAMPLES

The library includes four comprehensive demos:

Traffic Light Demo (Simple FSM) : Uses the matrix FSM to cycle through traffic light states (red → red+amber → green → amber → red) with timer events. Includes pseudo-random "break" events and repair logic to demonstrate wildcards and priority handling.

Trading Strategy Demo (Concurrent FSM) : Implements a realistic long-only trading strategy using BOTH FSM types:

• Map FSM converts multiple technical conditions (EMA crosses, gaps, fractals, RSI) into prioritised events

• Matrix FSM handles state transitions (idle → setup → entry → position → exit → re-entry)

• Includes position management, stop losses, and re-entry logic

Error Demonstrations : Both FSM types include error demos with intentionally malformed rules to showcase the validation system's capabilities.

🟩 BRING ON THE FUNCTIONS

f_printFSMMatrix(_mat_rules, _a_states, _tablePosition)

Prints a table of states and rules to the specified position on the chart. Works only with the matrix-based FSM.

Parameters:

_mat_rules (matrix)

_a_states (array)

_tablePosition (simple string)

Returns: The table of states and rules.

method m_loadMatrixRulesFromText(_mat_rules, _rulesText)

Loads rules into a rules matrix from a multiline string where each line is of the form "current state | event | next state" (ignores empty lines and trims whitespace).

This is the most human-readable way to define rules because it's a visually aligned, table-like format.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_rulesText (string)

Returns: No explicit return. The matrix is modified as a side-effect.

method m_addRuleToMatrix(_mat_rules, _currentState, _event, _nextState)

Adds a single rule to the rules matrix. This can also be quite readble if you use short variable names and careful spacing.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_currentState (string)

_event (string)

_nextState (string)

Returns: No explicit return. The matrix is modified as a side-effect.

method m_validateRulesMatrix(_mat_rules, _a_states, _showTable, _tablePosition)

Validates a rules matrix and a states array to check that they are well formed. Works only with the matrix-based FSM.

Checks: matrix has exactly 3 columns; no empty next states; all states defined in array; no duplicate states; no duplicate rules; all states have entry/exit rules; no conflicting transitions; no redundant wildcards. To avoid slowing down the script unnecessarily, call this method once (perhaps using `barstate.isfirst`), when the rules and states are ready.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_a_states (array)

_showTable (bool)

_tablePosition (simple string)

Returns: `true` if the rules and states are valid; `false` if errors or warnings exist.

method m_getStateFromMatrix(_mat_rules, _currentState, _event, _strictInput, _strictTransitions)

Returns the next state based on the current state and event, or `na` if no matching transition is found. Empty (not na) entries are treated as wildcards if `strictInput` is false.

Priority: exact match > event wildcard > state wildcard > full wildcard.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_currentState (string)

_event (string)

_strictInput (bool)

_strictTransitions (bool)

Returns: The next state or `na`.

method m_addRuleToEventMap(_map_eventRules, _state, _condName, _output)

Adds a single event rule to the event rules map. If the state key already exists, appends the new rule to the existing array (if different). If the state key doesn't exist, creates a new entry.

Namespace types: map

Parameters:

_map_eventRules (map)

_state (string)

_condName (string)

_output (string)

Returns: No explicit return. The map is modified as a side-effect.

method m_addEventRulesToMapFromText(_map_eventRules, _configText)

Loads event rules from a multiline text string into a map structure.

Format: "state | condName > output | condName > output | ..." . Pairs are ordered by priority. You can have multiple rules on the same line for one state.

Supports wildcards: Use an empty string ("") or the special string "ANY" for state or condName to create wildcard rules.

Examples: " | condName > output" (state wildcard), "state | > output" (condition wildcard), " | > output" (full wildcard).

Splits lines by \n, extracts state as key, creates/appends to array with new o_eventRule(condName, output).

Call once, e.g., on barstate.isfirst for best performance.

Namespace types: map

Parameters:

_map_eventRules (map)

_configText (string)

Returns: No explicit return. The map is modified as a side-effect.

f_printFSMMap(_map_eventRules, _a_states, _tablePosition)

Prints a table of map-based event rules to the specified position on the chart.

Parameters:

_map_eventRules (map)

_a_states (array)

_tablePosition (simple string)

Returns: The table of map-based event rules.

method m_validateEventRulesMap(_map_eventRules, _a_states, _a_validEvents, _showTable, _tablePosition)

Validates an event rules map to check that it's well formed.

Checks: map is not empty; wrappers contain non-empty arrays; no duplicate condition names per state; no empty fields in o_eventRule objects; optionally validates outputs against matrix events.

NOTE: Both "" and "ANY" are treated identically as wildcards for both states and conditions.

To avoid slowing down the script unnecessarily, call this method once (perhaps using `barstate.isfirst`), when the map is ready.

Namespace types: map

Parameters:

_map_eventRules (map)

_a_states (array)

_a_validEvents (array)

_showTable (bool)

_tablePosition (simple string)

Returns: `true` if the event rules map is valid; `false` if errors or warnings exist.

method m_getEventFromConditionsMap(_currentState, _a_activeConditions, _map_eventRules)

Returns a single event or state string based on the current state and active conditions.

Uses a map of event rules where rules are pre-sorted by implicit priority via load order.

Supports wildcards using empty string ("") or "ANY" for flexible rule matching.

Priority: exact match > condition wildcard > state wildcard > full wildcard.

Namespace types: series string, simple string, input string, const string

Parameters:

_currentState (string)

_a_activeConditions (array)

_map_eventRules (map)

Returns: The output string (event or state) for the first matching condition, or na if no match found.

o_eventRule

o_eventRule defines a condition-to-output mapping for the concurrent FSM.

Fields:

condName (series string) : The name of the condition to check.

output (series string) : The output (event or state) when the condition is true.

o_eventRuleWrapper

o_eventRuleWrapper wraps an array of o_eventRule for use as map values (maps cannot contain collections directly).

Fields:

a_rules (array) : Array of o_eventRule objects for a specific state.

Triple-EMA Cloud (3× configurable EMAs + timeframe + fill)About This Script

Name: Triple-EMA Cloud (3× configurable EMAs + timeframe + fill)

What it does:

The script plots three Exponential Moving Averages (EMAs) on your chart.

You can set each EMA’s length (how many bars or days it averages over), source (for example, closing price, opening price, or the midpoint of high + low), and timeframe (you can have one EMA use daily data, another hourly data, etc.).

The indicator draws a “cloud” or channel by shading the area between the outermost two EMAs of the three. This lets you see a band or zone that the price is moving in, defined by those EMAs.

You also get full control over how each of the three EMA‐lines looks: color, thickness, transparency, and plot style (solid line, steps, circles, etc.).

How to Use It (for Beginners)

Here’s how a trader who’s new to charts can use this tool, especially when looking for pullbacks or undercut price action.

Key Concepts

Trend: Imagine the market price is generally going up or down. EMAs are a way to smooth out price movements so you can see the trend more clearly.

Pullback: When a price has been going up (an uptrend), sometimes it dips down a little before going up again. That dip is the pullback. It’s a chance to enter or add to a position at a “better price.”

Undercut: This is when price drops below an important level (for example an EMA) and then comes back up. It looks like it broke below, but then it recovers. That may show reverse pressure or strength building.

How the Script Helps With Pullbacks & Undercuts

Marking Trend Zones with the Cloud

The cloud between the outer EMA lines gives you a zone of expected support/resistance. If the price is above the cloud, that zone can act like a “floor” in uptrends; if it is below, the cloud might act like a “ceiling” in downtrends.

Watching Price vs the EMAs

If the price pulls back toward the cloud (or toward one of the EMAs) and then bounces back up, that’s a signal that the uptrend might continue.

If the price undercuts (goes a bit below) one of the EMAs or the cloud and then returns above it, that can also be a signal. It suggests that even though there was a temporary drop, buyers stepped in.

Using the Three EMAs for Confirmation

Because the script uses three EMAs, you can see how tightly or loosely they are spaced.

If all three EMAs are broadly aligned (for example, in an uptrend: shorter length above longer length, each pulling from reliable price source), that gives more confidence in trend strength.

If the middle EMA (or different source/timeframe) is holding up as support while others are above, it strengthens signal.

Entry & Exit Points

Entry: For example, after a pullback toward the cloud or “mid‐EMA”, wait for price to show a bounce up. That could be a better entry than buying at the top.

Stop Loss / Risk: You might place a stop loss just below the cloud or the lowest of your selected EMAs so that if price breaks through, the idea is invalidated.

Profit Target: Could be a recent high, resistance level, or a fixed reward-risk multiple (for example aiming to make twice what you risked).

Practical Steps for New Traders

Set up the EMAs

Choose simple lengths like 10, 21, 50.

For example, EMA #1 = length 10, source Close, timeframe “current chart”; EMA #2 = length 21, source (H+L)/2; EMA #3 = length 50, maybe timeframe daily.

Observe the Price Action

When price moves up, then dips, see if it comes back near the shaded cloud or one of the EMAs.

See if the dip touches the EMAs lightly (not a big drop) and then price starts climbing again.

Look for undercuts

If price briefly goes below a line (or below cloud) and then closes back above, that’s undercut + recovery. That bounce back is often meaningful.

Manage risk

Only put in money you can afford to lose.

Use small position size until you get comfortable.

Use stop-loss (as mentioned) in case the price doesn’t bounce as expected.

Practice

Put this indicator on charts (stocks you follow) in past time periods. See how price behaved with pullbacks / undercuts relative to the EMAs & cloud. This helps you learn to see signals.

What It Doesn’t Do (and What to Be Careful Of)

It doesn’t predict the future — it simply shows zones and trends. Price can still break down through the cloud.

In a “choppy” market (i.e. when price is going up and down without a clear trend), signals from EMAs / clouds are less reliable. You’ll get more “false bounces.”

Under / overshoots & big news events can break through clean levels, so always watch for confirmation (volume, price behavior) before putting big money in.

Greer Gap# Greer Gap Indicator (No mitigation: i.e. removing false signals)

## Summary

The **Greer Gap Indicator** identifies **Fair Value Gaps (FVGs)** and introduces specialized **Greer Bull Gaps (Blue)** and **Greer Bear Gaps (Orange)** to highlight high-probability trading opportunities. Unlike traditional FVG indicators, it avoids hindsight bias by not removing historical gaps based on future price action, ensuring transparency in signal accuracy. Built upon LuxAlgo’s FVG logic, it adds unique filtering: only the first Greer Gap after an opposite gap is plotted if its level (min for Bull, max for Bear) is not higher/lower than the previous Greer Gap of the same type, while all valid gaps are recorded for comparison. Traders can use these gaps as support/resistance or entry signals, customizable via timeframe, look back, and display options.

## Description

This indicator detects and displays **Fair Value Gaps (FVGs)** on the chart, with a focus on specialized **Greer Gaps**:

- **Bullish Gaps (Green)**: Areas where the low of the current candle is above the high of a previous candle (look back period), indicating potential upward momentum.

- **Bearish Gaps (Red)**: Areas where the high of the current candle is below the low of a previous candle, indicating potential downward momentum.

- **Greer Bull Gaps (Blue)**: A bullish gap that is above the latest bearish gap's max. Only the first such gap after a bearish gap is plotted if it meets criteria (not higher than the previous Greer Bull Gap's min), but all valid ones are recorded for comparison.

- **Greer Bear Gaps (Orange)**: A bearish gap that is below the latest bullish gap's min. Only the first such gap after a bullish gap is plotted if it meets criteria (not lower than the previous Greer Bear Gap's max), but all valid ones are recorded.

## How It Works

The script uses a dynamic look back period to detect FVGs. It maintains a record of all detected gaps and applies additional logic for Greer Gaps:

- **Greer Bull Gaps**: Checks if the new bullish gap's min is above the latest bearish gap's max. Plots only if it's the first since the last bearish gap and its min is <= previous Greer Bull min (or first one).

- **Greer Bear Gaps**: Checks if the new bearish gap's max is below the latest bullish gap's min. Plots only if it's the first since the last bullish gap and its max is >= previous Greer Bear max (or first one).

- **Resets**: A new bearish gap resets the Greer Bull Gap flag, and a new bullish gap resets the Greer Bear Gap flag.

## How to Use

- **Timeframe**: Set a higher timeframe (e.g., 'D' for daily) to detect gaps from that timeframe on the current chart.

- **Look back Period**: Adjust to change gap detection sensitivity (default: 34). Use 2 if you want to compare to LuxAlgo

- **Extend**: Controls how far right the gap boxes extend.

- **Show Options**: Toggle visibility of all bullish/bearish gaps or Greer Gaps.

- **Colors**: Customize colors for each gap type.

- **Application**: Use Greer Gaps as potential support/resistance levels or entry signals, but combine with other analysis for confirmation.

## Originality and Credits

This script is inspired by and builds upon the **"Fair Value Gap "** indicator by LuxAlgo (available on TradingView: ()).

**Credits**: Thanks to LuxAlgo for the core FVG detection logic.

**Significant Changes**:

- Added **Greer Bull and Bear Gap** logic for filtered, directional gaps with reset mechanisms.

- Introduced recording of all valid Greer Gaps without plotting all, to compare levels without hindsight bias.

- **No mitigation/removal of gaps**: Unlike LuxAlgo's approach, which mitigates (removes or alters) gaps based on future price action (e.g., when filled), this can create a hindsight bias where incorrect signals disappear over time. If a signal is used for a trade and later removed due to new data, it doesn't reflect real-time performance accurately. The Greer Gap avoids this by using gap comparisons to validate signals without altering historical boxes, ensuring transparency in when signals were right or wrong.

NY Anchored VWAP and Auto SMANY Anchored VWAP and Auto SMA

This script is a versatile trading indicator for the TradingView platform that combines two powerful components: a New York-anchored Volume-Weighted Average Price (VWAP) and a dynamic Simple Moving Average (SMA). Designed for traders who utilize VWAP for intraday trend analysis, this tool provides a clear visual representation of average price and volatility-adjusted moving averages, generating automated alerts for key crossover signals.

Indicator Components

1. NY Anchored VWAP

The VWAP is a crucial tool that represents the average price of a security adjusted for volume. This version is "anchored" to the start of the New York trading session, resetting at the beginning of each new session. This provides a clean, session-specific anchor point to gauge market sentiment and trend. The VWAP line changes color to reflect its slope:

Green: When the VWAP is trending upwards, indicating a bullish bias.

Red: When the VWAP is trending downwards, indicating a bearish bias.

2. Auto SMA

The Auto SMA is a moving average with a unique twist: its lookback period is not fixed. Instead, it dynamically adjusts based on market volatility. The script measures volatility using the Average True Range (ATR) and a Z-Score calculation.

When volatility is expanding, the SMA's length shortens, making it more sensitive to recent price changes.

When volatility is contracting, the SMA's length lengthens, smoothing out the price action to filter out noise.

This adaptive approach allows the SMA to react appropriately to different market conditions.

Suggested Trading Strategy

This indicator is particularly effective when used on a one-minute chart for identifying high-probability trade entries. The core of the strategy is to trade the crossover between the VWAP and the Auto SMA, with confirmation from a candle close.

The strategy works best when the entry signal aligns with the overall bias of the higher timeframe market structure. For example, if the daily or 4-hour chart is in an uptrend, you would look for bullish signals on the one-minute chart.

Bullish Entry Signal: A potential entry is signaled when the VWAP crosses above the Auto SMA, and is confirmed when the one-minute candle closes above both the VWAP and the SMA. This indicates a potential continuation of the bullish momentum.

Bearish Entry Signal: A potential entry is signaled when the VWAP crosses below the Auto SMA, and is confirmed when the one-minute candle closes below both the VWAP and the SMA. This indicates a potential continuation of the bearish momentum.

The built-in alerts for these crossovers allow you to receive notifications without having to constantly monitor the charts, ensuring you don't miss a potential setup.

Algo + Trendlines :: Medium PeriodThis indicator helps me to avoid overlooking Trendlines / Algolines. So far it doesn't search explicitly for Algolines (I don't consider volume at all), but it's definitely now already not horribly bad.

These are meant to be used on logarithmic charts btw! The lines would be displayed wrong on linear charts.

The biggest challenge is that there are some technical restrictions in TradingView, f. e. a script stops executing if a for-loop would take longer than 0.5 sec.

So in order to circumvent this and still be able to consider as many candles from the past as possible, I've created multiple versions for different purposes that I use like this:

Algo + Trendlines :: Medium Period : This script looks for "temporary highs / lows" (meaning the bar before and after has lower highs / lows) on the daily chart, connects them and shows the 5 ones that are the closest to the current price (=most relevant). This one is good to find trendlines more thoroughly, but only up to 4 years ago.

Algo + Trendlines :: Long Period : This version looks instead at the weekly charts for "temporary highs / lows" and finds out which days caused these highs / lows and connects them, Taking data from the weekly chart means fewer data points to check whether a trendline is broken, which allows to detect trendlines from up to 12 years ago! Therefore it misses some trendlines. Personally I prefer this one with "Only Confirmed" set to true to really show only the most relevant lines. This means at least 3 candle highs / lows touched the line. These are more likely stronger resistance / support lines compared to those that have been touched only twice.

Very important: sometimes you might see dotted lines that suddenly stop after a few months (after 100 bars to be precise). This indicates you need to zoom further out for TradingView to be able to load the full line. Unfortunately TradingView doesn't render lines if the starting point was too long ago, so this is my workaround. This is also the script's biggest advantage: showing you lines that you might have missed otherwise since the starting bars were outside of the screen, and required you to scroll f. e back to 2015..

One more thing to know:

Weak colored line = only 2 "collision" points with candle highs/lows (= not confirmed)

Usual colored line = 3+ "collision" points (= confirmed)

Make sure to move this indicator above the ticker in the Object Tree, so that it is drawn on top of the ticker's candles!

More infos: www.reddit.com

Algo + Trendlines :: Long PeriodThis indicator helps me to avoid overlooking Trendlines / Algolines. So far it doesn't search explicitly for Algolines (I don't consider volume at all), but it's definitely now already not horribly bad.

These are meant to be used on logarithmic charts btw! The lines would be displayed wrong on linear charts.

The biggest challenge is that there are some technical restrictions in TradingView, f. e. a script stops executing if a for-loop would take longer than 0.5 sec.

So in order to circumvent this and still be able to consider as many candles from the past as possible, I've created multiple versions for different purposes that I use like this:

Algo + Trendlines :: Medium Period : This script looks for "temporary highs / lows" (meaning the bar before and after has lower highs / lows) on the daily chart, connects them and shows the 5 ones that are the closest to the current price (=most relevant). This one is good to find trendlines more thoroughly, but only up to 4 years ago.

Algo + Trendlines :: Long Period : This version looks instead at the weekly charts for "temporary highs / lows" and finds out which days caused these highs / lows and connects them, Taking data from the weekly chart means fewer data points to check whether a trendline is broken, which allows to detect trendlines from up to 12 years ago! Therefore it misses some trendlines. Personally I prefer this one with "Only Confirmed" set to true to really show only the most relevant lines. This means at least 3 candle highs / lows touched the line. These are more likely stronger resistance / support lines compared to those that have been touched only twice.

Very important: sometimes you might see dotted lines that suddenly stop after a few months (after 100 bars to be precise). This indicates you need to zoom further out for TradingView to be able to load the full line. Unfortunately TradingView doesn't render lines if the starting point was too long ago, so this is my workaround. This is also the script's biggest advantage: showing you lines that you might have missed otherwise since the starting bars were outside of the screen, and required you to scroll f. e back to 2015..

One more thing to know:

Weak colored line = only 2 "collision" points with candle highs/lows (= not confirmed)

Usual colored line = 3+ "collision" points (= confirmed)

Make sure to move this indicator above the ticker in the Object Tree, so that it is drawn on top of the ticker's candles!

More infos: www.reddit.com

Cnagda Liquidit Trading SystemCnagda Liquidit Trading System helps spot where price is likely to trap traders and reverse, then gives simple, actionable Level to entry, place SL, and take profits with confidence. It blends imbalance zones, trend bias, order blocks, liquidity pools, high-probability fake Signal, and context-aware candle patterns into one clean workflow.

🟩🟥 Imbalance boxes: “Crowd rushed, gaps left”

What it is: Green/red boxes mark fast, one-sided moves where price “skipped” orders—think FVG-like zones that often get revisited.

Why it helps: Price frequently pulls back to “fill” these zones, creating clean retest entries with logical stops.

⏩How to use:

Green box = potential demand retest; Red box = potential supply retest. Enter on pullback into box, not on first impulse. Put stop on far side of box and aim first targets at recent swing points.

↕️ Swing bias (HH/HL vs LH/LL): “Which way is the road?”

What it is: Higher-highs/higher-lows = up-bias; Lower-highs/lower-lows = down-bias. system plots Buy/Sell OB levels aligned with that bias.

Why it helps: Trading with the broader flow reduces “hero trades” against institutions. Bias gives clearer entries and cleaner drawdowns.

⏩How to use:

Up-bias: look for long on Buy OB retests. Down-bias: look for short on Sell OB retests. Wait for a small rejection/engulfing to confirm before triggering.

🧱Order blocks: “Where big players remember”

What it is: last opposite-colored candle before an impulsive move—these zones often hold memory and reaction. system plots these as Buy/Sell OB lines.

Why it helps: Many breakouts pull back to the origin. Good entries often happen on retest, not on the breakout chase.

⏩ How to use:

Let price return into the OB, show wick rejection, and decent volume. Enter with stop beyond OB; define risk-reward before entry.

📊Volume coloring: “How Volume is move?”

What it is: Bar color reflects relative volume; inside bars are black. The dashboard also shows Volume and “Volume vs Prev.”

Why it helps: Patterns without volume often fade; volume validates strength and intent of moves.

⏩ How to use:

Favor entries where imbalance/OB/liquidity-grab coincide with higher volume. If volume is weak, reduce size or skip.

🧲 BSL/SSL liquidity pools: “Fishing for stops”

What it is: Equal highs cluster stops above (BSL); equal lows cluster stops below (SSL). system plots these and highlights the nearest one (“magnet”).

Why it helps: Price often sweeps these pools to trigger stops before reversing. This is a prime trap-reversal location.

⏩ How to use:

Watch nearest BSL/SSL. If price wicks through and closes back inside, anticipate a reversal. Trade reaction, not first poke. When price closes beyond, consider that pool mitigated and move on.

🟢🔴 Advanced liquidity grab: “Catch fakeout”

What it is: Bullish grab = makes a new low beyond a prior low but closes back above it, with a long lower wick, small body, and higher volume. Bearish is mirror. Labeled automatically.

Why it helps: It exposes trap moves (stop hunts) and often precedes true direction.

⏩ How to use:

Best when it aligns with a nearby imbalance/OB and supportive volume. Enter on reversal candle break or on retest. Stop goes beyond sweep wick.

🧠 Smart candlestick patterns (only in right place)

What it is: Engulfing, Hammer, Shooting Star, Hanging Man, Doji (with high volume), Morning/Evening Star, Piercing—but marked “effective” only if context (swing/trend/location) agrees.

Why it helps: same pattern in the wrong place is noise; in the right place, it’s signal.

⏩ How to use:

Location first (BSL/SSL/OB/imbalance), then pattern. Treat pattern as trigger/confirmation—one fresh label shows to keep chart clean.

🧭 Dashboard: “Context in a glance”

⏩ Reversal Level: current swing anchor—expect turns or reactions nearby; great for alerts and planning.

⏩ Volume vs Prev + Volume: Strength meter for signal candle—higher adds conviction.

⏩ Nearest Pool: next “magnet” area—look for sweeps/rejections there.

🧩Step-by-step trading flow (with mindset)

⏩ Set bias: HH/HL = long bias, LH/LL = short bias. Counter-trend only on clean sweeps with strong confirmation.

⏩ Find magnet: Check Nearest Pool (BSL/SSL). Focus attention there; it saves screen time.

⏩ Wait for event: Look for a sweep/grab label, or sharp rejection at pool/OB/imbalance. Avoid FOMO.

⏩ Add confluence: Stack 2–3 of these—imbalance box, OB, contextual pattern, supportive volume.

⏩Plan entry: Bullish: trigger above reversal candle high or take retest of FVG/OB. Stop below sweep wick/zone. Target at least 1:1.5–1:2.

Bearish: mirror above.

⏩Manage smartly: Take partials, move to breakeven or trail thoughtfully. Don’t drag stops inside zone out of emotion.

🎛️ Parameter tuning (to reduce human error)

⏩ swingLen: Smaller = faster but noisier; larger = cleaner but slower. Backtest first, then go live.

⏩ Tolerance (ATR or percent): ATR tolerance adapts to volatility (good for fast markets and lower TFs). Start around 0.15–0.30. In calm markets, try percent 0.05–0.15%.

⏩ minBarsGap: Start with 3–5 so equal highs/lows are truly equal—reduces false pools.

❌Common mistakes → ✅ Better habits

⏩Chasing every breakout → Wait for sweep/rejection, then confirm.

⏩Ignoring volume → Validate strength; cut size or skip on weak volume.

⏩Losing history of pools → If reviewing/backtesting, keep mitigated pools visible (dashed/faded).

⏩Over-tight tolerance/too small swingLen → Increases false signals; backtest to find balance.

📝 checklist (before entry)

⏩ Is there a nearby BSL/SSL and did a sweep/grab happen there?

⏩ Is there a close imbalance/OB that price can retest?

⏩ Do we have an effective pattern plus supportive volume?

⏩Is the stop beyond the wick/zone and RR ≥ 1:1.5?

•?((¯°·._.• 🎀 𝐻𝒶𝓅𝓅𝓎 𝒯𝓇𝒶𝒹𝒾𝓃𝑔 🎀 •._.·°¯((?•

HorizonSigma Pro [CHE]HorizonSigma Pro

Disclaimer

Not every timeframe will yield good results . Very short charts are dominated by microstructure noise, spreads, and slippage; signals can flip and the tradable edge shrinks after costs. Very high timeframes adapt more slowly, provide fewer samples, and can lag regime shifts. When you change timeframe, you also change the ratios between horizon, lookbacks, and correlation windows—what works on M5 won’t automatically hold on H1 or D1. Liquidity, session effects (overnight gaps, news bursts), and volatility do not scale linearly with time. Always validate per symbol and timeframe, then retune horizon, z-length, correlation window, and either the neutral band or the z-threshold. On fast charts, “components” mode adapts quicker; on slower charts, “super” reduces noise. Keep prior-shift and calibration enabled, monitor Hit Rate with its confidence interval and the Brier score, and execute only on confirmed (closed-bar) values.

For example, what do “UP 61%” and “DOWN 21%” mean?

“UP 61%” is the model’s estimated probability that the close will be higher after your selected horizon—directional probability, not a price target or profit guarantee. “DOWN 21%” still reports the probability of up; here it’s 21%, which implies 79% for down (a short bias). The label switches to “DOWN” because the probability falls below your short threshold. With a neutral-band policy, for example ±7%, signals are: Long above 57%, Short below 43%, Neutral in between. In z-score mode, fixed z-cutoffs drive the call instead of percentages. The arrow length on the chart is an ATR-scaled projection to visualize reach; treat it as guidance, not a promise.

Part 1 — Scientific description

Objective.

The indicator estimates the probability that price will be higher after a user-defined horizon (a chosen number of bars) and emits long, short, or neutral decisions under explicit thresholds. It combines multi‑feature, z‑normalized inputs, adaptive correlation‑based weighting, a prior‑shifted sigmoid mapping, optional rolling probability calibration, and repaint‑safe confirmation. It also visualizes an ATR‑scaled forward projection and prints a compact statistics panel.

Data and labeling.

For each bar, the target label is whether price increased over the past chosen horizon. Learning is deliberately backward‑looking to avoid look‑ahead: features are associated with outcomes that are only known after that horizon has elapsed.

Feature engineering.

The feature set includes momentum, RSI, stochastic %K, MACD histogram slope, a normalized EMA(20/50) trend spread, ATR as a share of price, Bollinger Band width, and volume normalized by its moving average. All features are standardized over rolling windows. A compressed “super‑feature” is available that aggregates core trend and momentum components while penalizing excessive width (volatility). Users can switch between a “components” mode (weighted sum of individual features) and a “super” mode (single compressed driver).

Weighting and learning.

Weights are the rolling correlations between features (evaluated one horizon ago) and realized directional outcomes, smoothed by an EMA and optionally clamped to a bounded range to stabilize outliers. This produces an adaptive, regime‑aware weighting without explicit machine‑learning libraries.

Scoring and probability mapping.

The raw score is either the weighted component sum or the weighted super‑feature. The score is standardized again and passed through a sigmoid whose steepness is user‑controlled. A “prior shift” moves the sigmoid’s midpoint to the current base rate of up moves, estimated over the evaluation window, so that probabilities remain well‑calibrated when markets drift bullish or bearish. Probabilities and standardized scores are EMA‑smoothed for stability.

Decision policy.

Two modes are supported:

- Neutral band: go long if the probability is above one half plus a user‑set band; go short if it is below one half minus that band; otherwise stay neutral.

- Z‑score thresholds: use symmetric positive/negative cutoffs on the standardized score to trigger long/short.

Repaint protection.

All values used for decisions can be locked to confirmed (closed) bars. Intrabar updates are available as a preview, but confirmed values drive evaluation and stats.

Calibration.

An optional rolling linear calibration maps past confirmed probabilities to realized outcomes over the evaluation window. The mapping is clipped to the unit interval and can be injected back into the decision logic if desired. This improves reliability (probabilities that “mean what they say”) without necessarily improving raw separability.

Evaluation metrics.

The table reports: hit rate on signaled bars; a Wilson confidence interval for that hit rate at a chosen confidence level; Brier score as a measure of probability accuracy; counts of long/short trades; average realized return by side; profit factor; net return; and exposure (signal density). All are computed on rolling windows consistent with the learning scheme.

Visualization.

On the chart, an arrowed projection shows the predicted direction from the current bar to the chosen horizon, with magnitude scaled by ATR (optionally scaled by the square‑root of the horizon). Labels display either the decision probability or the standardized score. Neutral states can display a configurable icon for immediate recognition.

Computational properties.

The design relies on rolling means, standard deviations, correlations, and EMAs. Per‑bar cost is constant with respect to history length, and memory is constant per tracked series. Graphical objects are updated in place to obey platform limits.

Assumptions and limitations.

The method is correlation‑based and will adapt after regime changes, not before them. Calibration improves probability reliability but not necessarily ranking power. Intrabar previews are non‑binding and should not be evaluated as historical performance.

Part 2 — Trader‑facing description

What it does.

This tool tells you how likely price is to be higher after your chosen number of bars and converts that into Long / Short / Neutral calls. It learns, in real time, which components—momentum, trend, volatility, breadth, and volume—matter now, adjusts their weights, and shows you a probability line plus a forward arrow scaled by volatility.

How to set it up.

1) Choose your horizon. Intraday scalps: 5–10 bars. Swings: 10–30 bars. The default of 14 bars is a balanced starting point.

2) Pick a feature mode.

- components: granular and fast to adapt when leadership rotates between signals.

- super: cleaner single driver; less noise, slightly slower to react.

3) Decide how signals are triggered.

- Neutral band (probability based): intuitive and easy to tune. Widen the band for fewer, higher‑quality trades; tighten to catch more moves.

- Z‑score thresholds: consistent numeric cutoffs that ignore base‑rate drift.

4) Keep reliability helpers on. Leave prior shift and calibration enabled to stabilize probabilities across bullish/bearish regimes.

5) Smoothing. A short EMA on the probability or score reduces whipsaws while preserving turns.

6) Overlay. The arrow shows the call and a volatility‑scaled reach for the next horizon. Treat it as guidance, not a promise.

Reading the stats table.

- Hit Rate with a confidence interval: your recent accuracy with an uncertainty range; trust the range, not only the point.

- Brier Score: lower is better; it checks whether a stated “70%” really behaves like 70% over time.

- Profit Factor, Net Return, Exposure: quick triage of tradability and signal density.

- Average Return by Side: sanity‑check that the long and short calls each pull their weight.

Typical adjustments.

- Too many trades? Increase the neutral band or raise the z‑threshold.

- Missing the move? Tighten the band, or switch to components mode to react faster.

- Choppy timeframe? Lengthen the z‑score and correlation windows; keep calibration on.

- Volatility regime change? Revisit the ATR multiplier and enable square‑root scaling of horizon.

Execution and risk.

- Size positions by volatility (ATR‑based sizing works well).

- Enter on confirmed values; use intrabar previews only as early signals.

- Combine with your market structure (levels, liquidity zones). This model is statistical, not clairvoyant.

What it is not.

Not a black‑box machine‑learning model. It is transparent, correlation‑weighted technical analysis with strong attention to probability reliability and repaint safety.

Suggested defaults (robust starting point).

- Horizon 14; components mode; weight EMA 10; correlation window 500; z‑length 200.

- Neutral band around seven percentage points, or z‑threshold around one‑third of a standard deviation.

- Prior shift ON, Calibration ON, Use calibrated for decisions OFF to start.

- ATR multiplier 1.0; square‑root horizon scaling ON; EMA smoothing 3.

- Confidence setting equivalent to about 95%.

Disclaimer

No indicator guarantees profits. HorizonSigma Pro is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Best regards

Chervolino

Adaptive Valuation [BackQuant]Adaptive Valuation

What this is

A composite, zero-centered oscillator that standardizes several classic indicators and blends them into one “valuation” line. It computes RSI, CCI, Demarker, and the Price Zone Oscillator, converts each to a rolling z-score, then forms a weighted average. Optional smoothing, dynamic overbought and oversold bands, and an on-chart table make the inputs and the final score easy to inspect.

How it works

Components

• RSI with its own lookback.

• CCI with its own lookback.

• DM (Demarker) with its own lookback.

• PZO (Price Zone Oscillator) with its own lookback.

Standardization via z-score

Each component is transformed using a rolling z-score over lookback bars:

z = (value − mean) ÷ stdev , where the mean is an EMA and the stdev is rolling.

This puts all inputs on a comparable scale measured in standard deviations.

Weighted blend

The z-scores are combined with user weights w_rsi, w_cci, w_dm, w_pzo to produce a single valuation series. If desired, it is then smoothed with a selected moving average (SMA, EMA, WMA, HMA, RMA, DEMA, TEMA, LINREG, ALMA, T3). ALMA’s sigma input shapes its curve.

Dynamic thresholds (optional)

Two ways to set overbought and oversold:

• Static : fixed levels at ob_thres and os_thres .

• Dynamic : ±k·σ bands, where σ is the rolling standard deviation of the valuation over dynLen .

Bands can be centered at zero or around the valuation’s rolling mean ( centerZero ).

Visualization and UI

• Zero line at 0 with gradient fill that darkens as the valuation moves away from 0.

• Optional plotting of band lines and background highlights when OB or OS is active.

• Optional candle and background coloring driven by the valuation.

• Summary table showing each component’s current z-score, the final score, and a compact status.

How it can be used

• Bias filter : treat crosses above 0 as bullish bias and below 0 as bearish bias.

• Mean-reversion context : look for exhaustion when the valuation enters the OB or OS region, then watch for exits from those regions or a return toward 0.

• Signal confirmation : use the final score to confirm setups from structure or price action.

• Adaptive banding : with dynamic thresholds, OB and OS adjust to prevailing variability rather than relying on fixed lines.

• Component tuning : change weights to emphasize trend (raise DM, reduce RSI/CCI) or range behavior (raise RSI/CCI, reduce DM). PZO can help in swing environments.

Why z-score blending helps

Indicators often live on different scales. Z-scoring places them on a common, unitless axis, so a one-sigma move in RSI has comparable influence to a one-sigma move in CCI. This reduces scale bias and allows transparent weighting. It also facilitates regime-aware thresholds because the dynamic bands scale with recent dispersion.

Inputs to know

• Component lookbacks : rsilb, ccilb, dmlb, pzolb control each raw signal.

• Standardization window : lookback sets the z-score memory. Longer smooths, shorter reacts.

• Weights : w_rsi, w_cci, w_dm, w_pzo determine each component’s influence.

• Smoothing : maType, smoothP, sig govern optional post-blend smoothing.

• Dynamic bands : dyn_thres, dynLen, thres_k, centerZero configure the adaptive OB/OS logic.

• UI : toggle the plot, table, candle coloring, and threshold lines.

Reading the plot

• Above 0 : composite pressure is positive.

• Below 0 : composite pressure is negative.

• OB region : valuation above the chosen OB line. Risk of mean reversion rises and momentum continuation needs evidence.

• OS region : mirror logic on the downside.

• Band exits : leaving OB or OS can serve as a normalization cue.

Strengths

• Normalizes heterogeneous signals into one interpretable series.

• Adjustable component weights to match instrument behavior.

• Dynamic thresholds adapt to changing volatility and drift.

• Transparent diagnostics from the on-chart table.

• Flexible smoothing choices, including ALMA and T3.

Limitations and cautions

• Z-scores assume a reasonably stationary window. Sharp regime shifts can make recent bands unrepresentative.

• Highly correlated components can overweight the same effect. Consider adjusting weights to avoid double counting.

• More smoothing adds lag. Less smoothing adds noise.

• Dynamic bands recalibrate with dynLen ; if set too short, bands may swing excessively. If too long, bands can be slow to adapt.

Practical tuning tips

• Trending symbols: increase w_dm , use a modest smoother like EMA or T3, and use centerZero dynamic bands.

• Choppy symbols: increase w_rsi and w_cci , consider ALMA with a higher sigma , and widen bands with a larger thres_k .

• Multiday swing charts: lengthen lookback and dynLen to stabilize the scale.

• Lower timeframes: shorten component lookbacks slightly and reduce smoothing to keep signals timely.

Alerts

• Enter and exit of Overbought and Oversold, based on the active band choice.

• Bullish and bearish zero crosses.

Use alerts as prompts to review context rather than as stand-alone trade commands.

Final Remarks

We created this to show people a different way of making indicators & trading.

You can process normal indicators in multiple ways to enhance or change the signal, especially with this you can utilise machine learning to optimise the weights, then trade accordingly.

All of the different components were selected to give some sort of signal, its made out of simple components yet is effective. As long as the user calibrates it to their Trading/ investing style you can find good results. Do not use anything standalone, ensure you are backtesting and creating a proper system.

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

Multi-TF Trend Table (Configurable)1) What this tool does (in one minute)

A compact, multi‑timeframe dashboard that stacks eight timeframes and tells you:

Trend (fast MA vs slow MA)

Where price sits relative to those MAs

How far price is from the fast MA in ATR terms

MA slope (rising, falling, flat)

Stochastic %K (with overbought/oversold heat)

MACD momentum (up or down)

A single score (0%–100%) per timeframe

Alignment tick when trend, structure, slope and momentum all agree

Use it to:

Frame bias top‑down (M→W→D→…→15m)

Time entries on your execution timeframe when the higher‑TF stack is aligned

Avoid counter‑trend traps when the table is mixed

2) Table anatomy (each column explained)

The table renders 9 columns × 8 rows (one row per timeframe label you define).

TF — The label you chose for that row (e.g., Month, Week, 4H). Cosmetic; helps you read the stack.

Trend — Arrow from fast MA vs slow MA: ↑ if fastMA > slowMA (up‑trend), ↓ otherwise (down‑trend). Cell is green for up, red for down.

Price Pos — One‑character structure cue:

🔼 if price is above both fast and slow MAs (bullish structure)

🔽 if price is below both (bearish structure)

– otherwise (between MAs / mixed)

MA Dist — Distance of price from the fast MA measured in ATR multiples:

XS < S < M < L < XL according to your thresholds (see §3.3). Useful for judging stretch/mean‑reversion risk and stop sizing.

MA Slope — The fast MA one‑bar slope:

↑ if fastMA - fastMA > 0

↓ if < 0

→ if = 0

Stoch %K — Rounded %K value (default 14‑1‑3). Background highlights when it aligns with the trend:

Green heat when trend up and %K ≤ oversold

Red heat when trend down and %K ≥ overbought Tooltip shows K and D values precisely.

Trend % — Composite score (0–100%), the dashboard’s confidence for that timeframe:

+20 if trendUp (fast>slow)

+20 if fast MA slope > 0

+20 if MACD up (signal definition in §2.8)

+20 if price above fast MA

+20 if price above slow MA

Background colours:

≥80 lime (strong alignment)

≥60 green (good)

≥40 orange (mixed)

<40 grey (weak/contrary)

MACD — 🟢 if EMA(12)−EMA(26) > its EMA(9), else 🔴. It’s a simple “momentum up/down” proxy.

Align — ✔ when everything is in gear for that trend direction:

For up: trendUp and price above both MAs and slope>0 and MACD up

For down: trendDown and price below both MAs and slope<0 and MACD down Tooltip spells this out.

3) Settings & how to tune them

3.1 Timeframes (TF1–TF8)

Inputs: TF1..TF8 hold the resolution strings used by request.security().

Defaults: M, W, D, 720, 480, 240, 60, 15 with display labels Month, Week, Day, 12H, 8H, 4H, 1H, 15m.

Tips

Keep a top‑down funnel (e.g., Month→Week→Day→H4→H1→M15) so you can cascade bias into entries.

If you scalp, consider D, 240, 120, 60, 30, 15, 5, 1.

Crypto weekends: consider 2D in place of W to reflect continuous trading.

3.2 Moving Average (MA) group

Type: EMA, SMA, WMA, RMA, HMA. Changes both fast & slow MA computations everywhere.

Fast Length: default 20. Shorten for snappier trend/slope & tighter “price above fast” signals.

Slow Length: default 200. Controls the structural trend and part of the score.

When to change

Swing FX/equities: EMA 20/200 is a solid baseline.

Mean‑reversion style: consider SMA 20/100 so trend flips slower.

Crypto/indices momentum: HMA 21 / EMA 200 will read slope more responsively.

3.3 ATR / Distance group

ATR Length: default 14; longer makes distance less jumpy.

XS/S/M/L thresholds: define the labels in column MA Dist. They are compared to |close − fastMA| / ATR.

Defaults: XS 0.25×, S 0.75×, M 1.5×, L 2.5×; anything ≥L is XL.

Usage

Entries late in a move often occur at L/XL; consider waiting for a pullback unless you are trading breakouts.

For stops, an initial SL around 0.75–1.5 ATR from fast MA often sits behind nearby noise; use your plan.

3.4 Stochastic group

%K Length / Smoothing / %D Smoothing: defaults 14 / 1 / 3.

Overbought / Oversold: defaults 70 / 30 (adjust to 80/20 for trendier assets).

Heat logic (column Stoch %K): highlights when a pullback aligns with the dominant trend (oversold in an uptrend, overbought in a downtrend).

3.5 View

Full Screen Table Mode: centers and enlarges the table (position.middle_center). Great for clean screenshots or multi‑monitor setups.

4) Signal logic (how each datapoint is computed)

Per‑TF data (via a single request.security()):

fastMA, slowMA → based on your MA Type and lengths

%K, %D → Stoch(High,Low,Close,kLen) smoothed by kSmooth, then %D smoothed by dSmooth

close, ATR(atrLen) → for structure and distance

MACD up → (EMA12−EMA26) > EMA9(EMA12−EMA26)

fastMA_prev → yesterday/previous‑bar fast MA for slope

TrendUp → fastMA > slowMA

Price Position → compares close to both MAs

MA Distance Label → thresholds on abs(close − fastMA)/ATR

Slope → fastMA − fastMA

Score (0–100) → sum of the five 20‑point checks listed in §2.7

Align tick → conjunction of trend, price vs both MAs, slope and MACD (see §2.9)

Important behaviour

HTF values are sampled at the execution chart’s bar close using Pine v6 defaults (no lookahead). So the daily row updates only when a daily bar actually closes.

5) How to trade with it (playbooks)

The table is a framework. Entries/exits still follow your plan (e.g., S/D zones, price action, risk rules). Use the table to know when to be aggressive vs patient.

Playbook A — Trend continuation (pullback entry)

Look for Align ✔ on your anchor TFs (e.g., Week+Day both ≥80 and green, Trend ↑, MACD 🟢).

On your execution TF (e.g., H1/H4), wait for Stoch heat with the trend (oversold in uptrend or overbought in downtrend), and MA Dist not at XL.

Enter on your trigger (break of pullback high/low, engulfing, retest of fast MA, or S/D first touch per your plan).

Risk: consider ATR‑based SL beyond structure; size so 0.25–0.5% account risk fits your rules.

Trail or scale at M/L distances or when score deteriorates (<60).

Playbook B — Breakout with confirmation

Mixed stack turns into broad green: Trend % jumps to ≥80 on Day and H4; MACD flips 🟢.

Price Pos shows 🔼 across H4/H1 (above both MAs). Slope arrows ↑.

Enter on the first clean base‑break with volume/impulse; avoid if MA Dist already XL.

Playbook C — Mean‑reversion fade (advanced)

Use only when higher TFs are not aligned and the row you trade shows XL distance against the higher‑TF context. Take quick targets back to fast MA. Lower win‑rate, faster management.

Playbook D — Top‑down filter for Supply/Demand strategy

Trade first retests only in the direction where anchor TFs (Week/Day) have Align ✔ and Trend % ≥60. Skip counter‑trend zones when the stack is red/green against you.

6) Reading examples

Strong bullish stack

Week: ↑, 🔼, S/M, slope ↑, %K=32 (green heat), Trend 100%, MACD 🟢, Align ✔

Day: ↑, 🔼, XS/S, slope ↑, %K=45, Trend 80%, MACD 🟢, Align ✔

Action: Look for H4/H1 pullback into demand or fast MA; buy continuation.

Late‑stage thrust

H1: ↑, 🔼, XL, slope ↑, %K=88

Day/H4: only 60–80%

Action: Likely overextended on H1; wait for mean reversion or multi‑TF alignment before chasing.

Bearish transition

Day flips from 60%→40%, Trend ↓, MACD turns 🔴, Price Pos “–” (between MAs)

Action: Stand aside for longs; watch for lower‑high + Align ✔ on H4/H1 to join shorts.

7) Practical tips & pitfalls

HTF closure: Don’t assume a daily row changed mid‑day; it won’t settle until the daily bar closes. For intraday anticipation, watch H4/H1 rows.

MA Type consistency: Changing MA Type changes slope/structure everywhere. If you compare screenshots, keep the same type.

ATR thresholds: Calibrate per asset class. FX may suit defaults; indices/crypto might need wider S/M/L.

Score ≠ signal: 100% does not mean “must buy now.” It means the environment is favourable. Still execute your trigger.

Mixed stacks: When rows disagree, reduce size or skip. The tool is telling you the market lacks consensus.

8) Customisation ideas

Timeframe presets: Save layouts (e.g., Swing, Intraday, Scalper) as indicator templates in TradingView.

Alternative momentum: Replace the MACD condition with RSI(>50/<50) if desired (would require code edit).

Alerts: You can add alert conditions for (a) Align ✔ changes, (b) Trend % crossing 60/80, (c) Stoch heat events. (Not shipped in this script, but easy to add.)

9) FAQ

Q: Why do I sometimes see a dash in Price Pos? A: Price is between fast and slow MAs. Structure is mixed; seek clarity before acting.

Q: Does it repaint? A: No, higher‑TF values update on the close of their own bars (standard request.security behaviour without lookahead). Intra‑bar they can fluctuate; decisions should be made at your bar close per your plan.

Q: Which columns matter most? A: For trend‑following: Trend, Price Pos, Slope, MACD, then Stoch heat for entries. The Score summarises, and Align enforces discipline.

Q: How do I integrate with ATR‑based risk? A: Use the MA Dist label to avoid chasing at extremes and to size stops in ATR terms (e.g., SL behind structure at ~1–1.5 ATR).

MTF Oscillator Stack [BigBeluga]🔵 OVERVIEW

The MTF Oscillator Stack brings powerful multi-timeframe momentum analysis directly into your price chart. You can select one oscillator— RSI , MFI , or Stochastic RSI —and display it across up to 4 different timeframes. Each panel is neatly stacked horizontally above price , offering quick insight into cross-timeframe conditions like trend direction, exhaustion zones, and momentum shifts.

🔵 CONCEPTS

Single Oscillator Mode: Select one oscillator type (RSI, MFI, or Stoch RSI) to analyze across all selected timeframes.

Top-Chart Horizontal Panels: Oscillator plots are aligned horizontally at the top of the chart for seamless top-down reading.

Signal Comparison Arrows: Arrows (🢁 / 🢃) indicate oscillator position relative to its signal line.

Overbought/Oversold Zones: Transparent 30–70 fill zones highlight key reversal areas.

Dynamic Display Logic: Only enabled panels are shown; spacing adjusts based on active timeframes.

Timeframe Tagging: Each oscillator panel is labeled with its corresponding timeframe (e.g., 1H, 2H, 4H).

🔵 FEATURES

Choose one oscillator (RSI, MFI, or Stoch RSI) and apply it across up to 4 timeframes.

Each oscillator panel includes: price-synced plot, signal line, and zone shading.

Scale alignment allows users to place charts at the bottom or top.

Clear arrow signals show whether oscillator is bullish or bearish.

Individual length and signal settings per timeframe.

Toggle for alignment mode: evenly spaced or floating layout.

All panels use a consistent layout for faster decision-making.

🔵 HOW TO USE