Cointegration Buy and Sell Signals [EdgeTerminal]The Cointegration Buy And Sell Signals is a sophisticated technical analysis tool to spot high-probability market turning points — before they fully develop on price charts.

Most reversal indicators rely on raw price action, visual patterns, or basic and common indicator logic — which often suffer in noisy or trending markets. In most cases, they lag behind the actual change in trend and provide useless and late signals.

This indicator is rooted in advanced concepts from statistical arbitrage, mean reversion theory, and quantitative finance, and it packages these ideas in a user-friendly visual format that works on any timeframe and asset class.

It does this by analyzing how the short-term and long-term EMAs behave relative to each other — and uses statistical filters like Z-score, correlation, volatility normalization, and stationarity tests to issue highly selective Buy and Sell signals.

This tool provides statistical confirmation of trend exhaustion, allowing you to trade mean-reverting setups. It fades overextended moves and uses signal stacking to reduce false entries. The entire indicator is based on a very interesting mathematically grounded model which I will get into down below.

Here’s how the indicator works at a high level:

EMAs as Anchors: It starts with two Exponential Moving Averages (EMAs) — one short-term and one long-term — to track market direction.

Statistical Spread (Regression Residuals): It performs a rolling linear regression between the short and long EMA. Instead of using the raw difference (short - long), it calculates the regression residual, which better models their natural relationship.

Normalize the Spread: The spread is divided by historical price volatility (ATR) to make it scale-invariant. This ensures the indicator works on low-priced stocks, high-priced indices, and crypto alike.

Z-Score: It computes a Z-score of the normalized spread to measure how “extreme” the current deviation is from its historical average.

Dynamic Thresholds: Unlike most tools that use fixed thresholds (like Z = ±2), this one calculates dynamic thresholds using historical percentiles (e.g., top 10% and bottom 10%) so that it adapts to the asset's current behavior to reduce false signals based on market’s extreme volatility at a certain time.

Z-Score Momentum: It tracks the direction of the Z-score — if Z is extreme but still moving away from zero, it's too early. It waits for reversion to start (Z momentum flips).

Correlation Check: Uses a rolling Pearson correlation to confirm the two EMAs are still statistically related. If they diverge (low correlation), no signal is shown.

Stationarity Filter (ADF-like): Uses the volatility of the regression residual to determine if the spread is stationary (mean-reverting) — a key concept in cointegration and statistical arbitrage. It’s not possible to build an exact ADF filter in Pine Script so we used the next best thing.

Signal Control: Prevents noisy charts and overtrading by ensuring no back-to-back buy or sell signals. Each signal must alternate and respect a cooldown period so you won’t be overwhelmed and won’t get a messy chart.

Important Notes to Remember:

The whole idea behind this indicator is to try to use some stat arb models to detect shifting patterns faster than they appear on common indicators, so in some cases, some assumptions are made based on historic values.

This means that in some cases, the indicator can “jump” into the conclusion too quickly. Although we try to eliminate this by using stationary filters, correlation checks, and Z-score momentum detection, there is still a chance some signals that are generated can be too early, in the stock market, that's the same as being incorrect. So make sure to use this with other indicators to confirm the movement.

How To Use The Indicator:

You can use the indicator as a standalone reversal system, as a filter for overbought and oversold setups, in combination with other trend indicators and as a part of a signal stack with other common indicators for divergence spotting and fade trades.

The indicator produces simple buy and sell signals when all criteria is met. Based on our own testing, we recommend treating these signals as standalone and independent from each other . Meaning that if you take position after a buy signal, don’t wait for a sell signal to appear to exit the trade and vice versa.

This is why we recommend using this indicator with other advanced or even simple indicators as an early confirmation tool.

The Display Table:

The floating diagnostic table in the top-right corner of the chart is a key part of this indicator. It's a live statistical dashboard that helps you understand why a signal is (or isn’t) being triggered, and whether the market conditions are lining up for a potential reversal.

1. Z-Score

What it shows: The current Z-score value of the volatility-normalized spread between the short EMA and the regression line of the long EMA.

Why it matters: Z-score tells you how statistically extreme the current relationship is. A Z-score of:

0 = perfectly average

> +2 = very overbought

< -2 = very oversold

How to use it: Look for Z-score reaching extreme highs or lows (beyond dynamic thresholds). Watch for it to start reversing direction, especially when paired with green table rows (see below)

2. Z-Score Momentum

What it shows: The rate of change (ROC) of the Z-score:

Zmomentum=Zt − Zt − 1

Why it matters: This tells you if the Z-score is still stretching out (e.g., getting more overbought/oversold), or reverting back toward the mean.

How to use it: A positive Z-momentum after a very low Z-score = potential bullish reversal A negative Z-momentum after a very high Z-score = potential bearish reversal. Avoid signals when momentum is still pushing deeper into extremes

3. Correlation

What it shows: The rolling Pearson correlation coefficient between the short EMA and long EMA.

Why it matters: High correlation (closer to +1) means the EMAs are still statistically connected — a key requirement for cointegration or mean reversion to be valid.

How to use it: Look for correlation > 0.7 for reliable signals. If correlation drops below 0.5, ignore the Z-score — the EMAs aren’t moving together anymore

4. Stationary

What it shows: A simplified "Yes" or "No" answer to the question:

“Is the spread statistically stable (stationary) and mean-reverting right now?”

Why it matters: Mean reversion strategies only work when the spread is stationary — that is, when the distance between EMAs behaves like a rubber band, not a drifting cloud.

How to use it: A "Yes" means the indicator sees a consistent, stable spread — good for trading. "No" means the market is too volatile, disjointed, or chaotic for reliable mean reversion. Wait for this to flip to "Yes" before trusting signals

5. Last Signal

What it shows: The last signal issued by the system — either "Buy", "Sell", or "None"

Why it matters: Helps avoid confusion and repeated entries. Signals only alternate — you won’t get another Buy until a Sell happens, and vice versa.

How to use it: If the last signal was a "Buy", and you’re watching for a Sell, don’t act on more bullish signals. Great for systems where you only want one position open at a time

6. Bars Since Signal

What it shows: How many bars (candles) have passed since the last Buy or Sell signal.

Why it matters: Gives you context for how long the current condition has persisted

How to use it: If it says 1 or 2, a signal just happened — avoid jumping in late. If it’s been 10+ bars, a new opportunity might be brewing soon. You can use this to time exits if you want to fade a recent signal manually

Indicator Settings:

Short EMA: Sets the short-term EMA period. The smaller the number, the more reactive and more signals you get.

Long EMA: Sets the slow EMA period. The larger this number is, the smoother baseline, and more reliable trend bases are generated.

Z-Score Lookback: The period or bars used for mean & std deviation of spread between short and long EMAs. Larger values result in smoother signals with fewer false positives.

Volatility Window: This value normalizes the spread by historical volatility. This allows you to prevent scale distortion, showing you a cleaner and better chart.

Correlation Lookback: How many periods or how far back to test correlation between slow and long EMAs. This filters out false positives when EMAs lose alignment.

Hurst Lookback: The multiplier to approximate stationarity. Lower leads to more sensitivity to regime change, higher produces a more stricter filtering.

Z Threshold Percentile: This value sets how extreme Z-score must be to trigger a signal. For example, 90 equals only top/bottom 10% of extremes, 80 = more frequent.

Min Bars Between Signals: This hard stop prevents back-to-back signals. The idea is to avoid over-trading or whipsaws in volatile markets even when Hurst lookback and volatility window values are not enough to filter signals.

Some More Recommendations:

We recommend trying different EMA pairs (10/50, 21/100, 5/20) for different asset behaviors. You can set percentile to 85 or 80 if you want more frequent but looser signals. You can also use the Z-score reversion monitor for powerful confirmation.

Поиск скриптов по запросу "one一季度财报"

ADR% Extension Levels from SMA 50I created this indicator inspired by RealSimpleAriel (a swing trader I recommend following on X) who does not buy stocks extended beyond 4 ADR% from the 50 SMA and uses extensions from the 50 SMA at 7-8-9-10-11-12-13 ADR% to take profits with a 20% position trimming.

RealSimpleAriel's strategy (as I understood it):

-> Focuses on leading stocks from leading groups and industries, i.e., those that have grown the most in the last 1-3-6 months (see on Finviz groups and then select sector-industry).

-> Targets stocks with the best technical setup for a breakout, above the 200 SMA in a bear market and above both the 50 SMA and 200 SMA in a bull market, selecting those with growing Earnings and Sales.

-> Buys stocks on breakout with a stop loss set at the day's low of the breakout and ensures they are not extended beyond 4 ADR% from the 50 SMA.

-> 3-5 day momentum burst: After a breakout, takes profits by selling 1/2 or 1/3 of the position after a 3-5 day upward move.

-> 20% trimming on extension from the 50 SMA: At 7 ADR% (ADR% calculated over 20 days) extension from the 50 SMA, takes profits by selling 20% of the remaining position. Continues to trim 20% of the remaining position based on the stock price extension from the 50 SMA, calculated using the 20-period ADR%, thus trimming 20% at 8-9-10-11 ADR% extension from the 50 SMA. Upon reaching 12-13 ADR% extension from the 50 SMA, considers the stock overextended, closes the remaining position, and evaluates a short.

-> Trailing stop with ascending SMA: Uses a chosen SMA (10, 20, or 50) as the definitive stop loss for the position, depending on the stock's movement speed (preferring larger SMAs for slower-moving stocks or for long-term theses). If the stock's closing price falls below the chosen SMA, the entire position is closed.

In summary:

-->Buy a breakout using the day's low of the breakout as the stop loss (this stop loss is the most critical).

--> Do not buy stocks extended beyond 4 ADR% from the 50 SMA.

--> Sell 1/2 or 1/3 of the position after 3-5 days of upward movement.

--> Trim 20% of the position at each 7-8-9-10-11-12-13 ADR% extension from the 50 SMA.

--> Close the entire position if the breakout fails and the day's low of the breakout is reached.

--> Close the entire position if the price, during the rise, falls below a chosen SMA (10, 20, or 50, depending on your preference).

--> Definitively close the position if it reaches 12-13 ADR% extension from the 50 SMA.

I used Grok from X to create this indicator. I am not a programmer, but based on the ADR% I use, it works.

Below is Grok from X's description of the indicator:

Script Description

The script is a custom indicator for TradingView that displays extension levels based on ADR% relative to the 50-period Simple Moving Average (SMA). Below is a detailed description of its features, structure, and behavior:

1. Purpose of the Indicator

Name: "ADR% Extension Levels from SMA 50".

Objective: Draw horizontal blue lines above and below the 50-period SMA, corresponding to specific ADR% multiples (4, 7, 8, 9, 10, 11, 12, 13). These levels represent potential price extension zones based on the average daily percentage volatility.

Overlay: The indicator is overlaid on the price chart (overlay=true), so the lines and SMA appear directly on the price graph.

2. Configurable Inputs

The indicator allows users to customize parameters through TradingView settings:

SMA Length (smaLength):

Default: 50 periods.

Description: Specifies the number of periods for calculating the Simple Moving Average (SMA). The 50-period SMA serves as the reference point for extension levels.

Constraint: Minimum 1 period.

ADR% Length (adrLength):

Default: 20 periods.

Description: Specifies the number of days to calculate the moving average of the daily high/low ratio, used to determine ADR%.

Constraint: Minimum 1 period.

Scale Factor (scaleFactor):

Default: 1.0.

Description: An optional multiplier to adjust the distance of extension levels from the SMA. Useful if levels are too close or too far due to an overly small or large ADR%.

Constraint: Minimum 0.1, increments of 0.1.

Tooltip: "Adjust if levels are too close or far from SMA".

3. Main Calculations

50-period SMA:

Calculated with ta.sma(close, smaLength) using the closing price (close).

Serves as the central line around which extension levels are drawn.

ADR% (Average Daily Range Percentage):

Formula: 100 * (ta.sma(dhigh / dlow, adrLength) - 1).

Details:

dhigh and dlow are the daily high and low prices, obtained via request.security(syminfo.tickerid, "D", high/low) to ensure data is daily-based, regardless of the chart's timeframe.

The dhigh / dlow ratio represents the daily percentage change.

The simple moving average (ta.sma) of this ratio over 20 days (adrLength) is subtracted by 1 and multiplied by 100 to obtain ADR% as a percentage.

The result is multiplied by scaleFactor for manual adjustments.

Extension Levels:

Defined as ADR% multiples: 4, 7, 8, 9, 10, 11, 12, 13.

Stored in an array (levels) for easy iteration.

For each level, prices above and below the SMA are calculated as:

Above: sma50 * (1 + (level * adrPercent / 100))

Below: sma50 * (1 - (level * adrPercent / 100))

These represent price levels corresponding to a percentage change from the SMA equal to level * ADR%.

4. Visualization

Horizontal Blue Lines:

For each level (4, 7, 8, 9, 10, 11, 12, 13 ADR%), two lines are drawn:

One above the SMA (e.g., +4 ADR%).

One below the SMA (e.g., -4 ADR%).

Color: Blue (color.blue).

Style: Solid (style=line.style_solid).

Management:

Each level has dedicated variables for upper and lower lines (e.g., upperLine1, lowerLine1 for 4 ADR%).

Previous lines are deleted with line.delete before drawing new ones to avoid overlaps.

Lines are updated at each bar with line.new(bar_index , level, bar_index, level), covering the range from the previous bar to the current one.

Labels:

Displayed only on the last bar (barstate.islast) to avoid clutter.

For each level, two labels:

Above: E.g., "4 ADR%", positioned above the upper line (style=label.style_label_down).

Below: E.g., "-4 ADR%", positioned below the lower line (style=label.style_label_up).

Color: Blue background, white text.

50-period SMA:

Drawn as a gray line (color.gray) for visual reference.

Diagnostics:

ADR% Plot: ADR% is plotted in the status line (orange, histogram style) to verify the value.

ADR% Label: A label on the last bar near the SMA shows the exact ADR% value (e.g., "ADR%: 2.34%"), with a gray background and white text.

5. Behavior

Dynamic Updating:

Lines update with each new bar to reflect new SMA 50 and ADR% values.

Since ADR% uses daily data ("D"), it remains constant within the same day but changes day-to-day.

Visibility Across All Bars:

Lines are drawn on every bar, not just the last one, ensuring visibility on historical data as well.

Adaptability:

The scaleFactor allows level adjustments if ADR% is too small (e.g., for low-volatility symbols) or too large (e.g., for cryptocurrencies).

Compatibility:

Works on any timeframe since ADR% is calculated from daily data.

Suitable for symbols with varying volatility (e.g., stocks, forex, cryptocurrencies).

6. Intended Use

Technical Analysis: Extension levels represent significant price zones based on average daily volatility. They can be used to:

Identify potential price targets (e.g., take profit at +7 ADR%).

Assess support/resistance zones (e.g., -4 ADR% as support).

Measure price extension relative to the 50 SMA.

Trading: Useful for strategies based on breakouts or mean reversion, where ADR% levels indicate reversal or continuation points.

Debugging: Labels and ADR% plot help verify that values align with the symbol’s volatility.

7. Limitations

Dependence on Daily Data: ADR% is based on daily dhigh/dlow, so it may not reflect intraday volatility on short timeframes (e.g., 1 minute).

Extreme ADR% Values: For low-volatility symbols (e.g., bonds) or high-volatility symbols (e.g., meme stocks), ADR% may require adjustments via scaleFactor.

Graphical Load: Drawing 16 lines (8 upper, 8 lower) on every bar may slow the chart for very long historical periods, though line management is optimized.

ADR% Formula: The formula 100 * (sma(dhigh/dlow, Length) - 1) may produce different values compared to other ADR% definitions (e.g., (high - low) / close * 100), so users should be aware of the context.

8. Visual Example

On a chart of a stock like TSLA (daily timeframe):

The 50 SMA is a gray line tracking the average trend.

Assuming an ADR% of 3%:

At +4 ADR% (12%), a blue line appears at sma50 * 1.12.

At -4 ADR% (-12%), a blue line appears at sma50 * 0.88.

Other lines appear at ±7, ±8, ±9, ±10, ±11, ±12, ±13 ADR%.

On the last bar, labels show "4 ADR%", "-4 ADR%", etc., and a gray label shows "ADR%: 3.00%".

ADR% is visible in the status line as an orange histogram.

9. Code: Technical Structure

Language: Pine Script @version=5.

Inputs: Three configurable parameters (smaLength, adrLength, scaleFactor).

Calculations:

SMA: ta.sma(close, smaLength).

ADR%: 100 * (ta.sma(dhigh / dlow, adrLength) - 1) * scaleFactor.

Levels: sma50 * (1 ± (level * adrPercent / 100)).

Graphics:

Lines: Created with line.new, deleted with line.delete to avoid overlaps.

Labels: Created with label.new only on the last bar.

Plots: plot(sma50) for the SMA, plot(adrPercent) for debugging.

Optimization: Uses dedicated variables for each line (e.g., upperLine1, lowerLine1) for clear management and to respect TradingView’s graphical object limits.

10. Possible Improvements

Option to show lines only on the last bar: Would reduce visual clutter.

Customizable line styles: Allow users to choose color or style (e.g., dashed).

Alert for anomalous ADR%: A message if ADR% is too small or large.

Dynamic levels: Allow users to specify ADR% multiples via input.

Optimization for short timeframes: Adapt ADR% for intraday timeframes.

Conclusion

The script creates a visual indicator that helps traders identify price extension levels based on daily volatility (ADR%) relative to the 50 SMA. It is robust, configurable, and includes debugging tools (ADR% plot and labels) to verify values. The ADR% formula based on dhigh/dlow

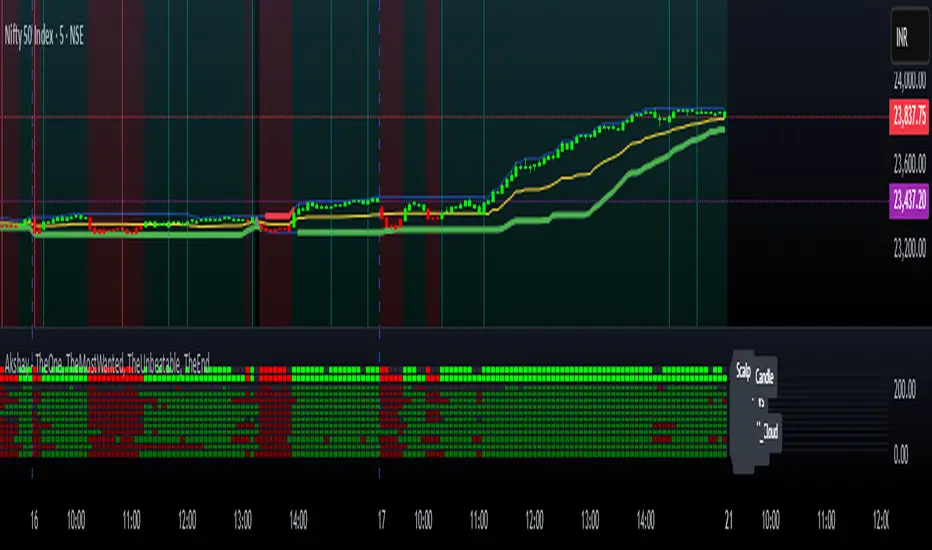

Akshay - TheOne, TheMostWanted, TheUnbeatable, TheEnd➤ All-in-One Solution (❌ No repaint):

This Technical Chart contains, MA24 Condition, Supertrend Indicator, HalfTrend Signal, Ichimoku Cloud Status, Parabolic SAR (P_SAR), First 5-Minute Candle Analysis (ORB5min), Volume-Weighted Moving Average (VWMA), Price-Volume Trend (PVT), Oscillator Composite, RSI Condition, ADX & Trend Strength.

Technicals don't lie.

🚀 Overview and Key Features

Comprehensive Multi-Indicator Approach:

The script is built to be an all-in-one technical indicator on TradingView. It integrates several well-known indicators and overlays—including Supertrend, HalfTrend, Ichimoku Cloud, various moving averages (EMA, SMA, VWMA), oscillators (Klinger, Price Oscillator, Awesome Oscillator, Chaikin Oscillator, Ultimate Oscillator, SMI Ergodic Oscillator, Chande Momentum Oscillator, Detrended Price Oscillator, Money Flow Index), ADX, and Donchian Channels—to create a composite picture of market sentiment.

Signal Generation and Alerts:

It not only calculates these indicators but also aggregates their output into “Master Candle” signals. Vertical lines are drawn on the chart with corresponding alerts to indicate potential buy or sell opportunities based on robust, combined conditions.

Visual Layering:

Through the use of colored histograms, custom candle plots, trend lines, and background color changes, the script offers a multi-layered visual representation of data, providing clarity about both short-term signals and overall market trends.

⚙️ How It Works and Functionality

MA24 Condition:

Uses the 24-period moving average as a proxy; if the price is above it, the bar is colored green, and red if below, with neutrality when conditions aren’t met.

Supertrend Indicator:

Evaluates price relative to the Supertrend level (calculated via ATR), coloring green when price is above it and red when below.

HalfTrend Signal:

Determines trend shifts by comparing the current close to a calculated trend level; green indicates an upward trend, while red suggests a downtrend.

Ichimoku Cloud Status:

Analyzes the relationship between the Conversion and Base lines; a bullish (green) signal is given when price is above both or the Conversion line is higher than the Base line.

Parabolic SAR (P_SAR):

Colors the signal based on whether the current price is above (green) or below (red) the Parabolic SAR marker, indicating stop and reverse conditions.

First 5-Minute Candle Analysis (ORB5min):

Uses key levels from the first 5-minute candle; if price exceeds the candle’s low, VWAP, and MA, it’s bullish (green), otherwise bearish (red).

Volume-Weighted Moving Average (VWMA):

Compares the current price to volume-weighted averages; a price above these levels is shown in green, below in red.

Price-Volume Trend (PVT):

Determines bullish or bearish momentum by comparing PVT to its VWAP—green when above and red when below.

Oscillator Composite:

Aggregates signals from multiple oscillators; a majority of positive results turn it green, while negative dominance results in red.

RSI Condition:

Uses a simple RSI threshold of 50, with values above signifying bullish (green) momentum and below marking bearish (red) conditions.

ADX & Trend Strength:

Reflects overall trend strength through ADX and directional movements; a combination favoring bullish conditions colors it green, with red signaling bearish pressure.

Master Candle Overall Signal:

Combines multiple indicator outputs into one “Master” signal—green for a consensus bullish trend and red for a bearish outlook.

Scalp Signal Variation:

Focused on short-term price changes, this signal adjusts quickly; green indicates improving short-term conditions, while red signals a downturn.

📊 Visualizations and 🎨 User Experience (❌ no repaint)

Dynamic Histograms & Bar Plots:

Each indicator is represented as a colored bar (with added vertical offsets) to facilitate easy comparison of their respective bullish or bearish contributions.

Clear Color-Coding & Labels:

Green (e.g., GreenFluorescent) indicates bullish sentiment.

Red (e.g., RedFluorescent) indicates bearish sentiment.

Custom labels and descriptive text accompany each bar for clarity.

Interactive Charting:

The overall background color adapts based on the “Master Candle” condition, offering an instant read on market sentiment.

The current candlestick is overlaid with color cues to reinforce the indicator’s signal, enhancing the trading experience.

Real-Time Alerts:

Vertical lines appear on signal events (buy/sell triggers), complemented by alerts that help traders stay on top of actionable market moves.

Sharp lines:

The Sharp lines are plotted based upon the EMA5 cross over with the same market trend, marks this as good time to reentry.

🔧 Settings and Customization

Flexible Timeframe Input:

Users can select their preferred timeframe for analysis, making the indicator adaptable to intraday or longer-term trading styles.

Customizable Indicator Parameters:

➤ Supertrend: Adjust ATR length and multiplier factors.

➤ HalfTrend: Tweak amplitude and channel deviation settings.

➤ Ichimoku Cloud & Oscillators: Fine-tune the conversion/base lines and oscillator lengths to match individual trading strategies.

Visual Customization:

The script’s color schemes and plotting styles can be altered as needed, giving users the freedom to tailor the interface to their taste or existing chart setups.

🌟 Uniqueness of the Concept

Integrated Multi-Indicator Synergy:

Combines a diverse range of trend, momentum, and volume-based indicators into a single cohesive system for a holistic market view.

Master Candle Aggregation:

Consolidates numerous individual signals into a "Master Candle" that filters out noise and provides a clear, consensus-based trading signal.

Layered Visual Feedback:

Uses color-coded histograms, adaptive background cues, and dynamic overlays to deliver a visually intuitive guide to market sentiment at a glance.

Customization and Flexibility:

Offers adjustable parameters for each indicator, allowing users to tailor the system to fit diverse trading styles and market conditions.

✅ Conclusion:

Robust Trading Tool & Non-Repainting Reliability:

This versatile technical analysis tool computes an extensive range of indicators, aggregates them into a stable, non-repainting “Master Candle” signal, and maintains consistent, verifiable outputs on historical data.

Holistic Market Insight & Consistent Signal Generation:

By combining trend detection, momentum oscillators, and volume analysis, the indicator delivers a comprehensive snapshot of market conditions and generates dependable signals across varying timeframes.

User-Centric Design with Rich Visual Feedback:

Customizable settings, clear color-coded outputs, adaptive backgrounds, and real-time alerts work together to provide actionable, transparent feedback—enhancing the overall trading experience.

A Unique All-in-One Solution:

The integrated approach not only simplifies complex market dynamics into an easy-to-read visual guide but also empowers systematic traders with a powerful, adaptable asset for accurate decision-making.

❤️ Credits:

Pine Script™ User Manual

Supertrend

Ichimoku Cloud

Parabolic SAR

Price Volume Trend (PVT)

Average Directional Index (ADX)

Volume Oscillator

HalfTrend

Donchian Trend

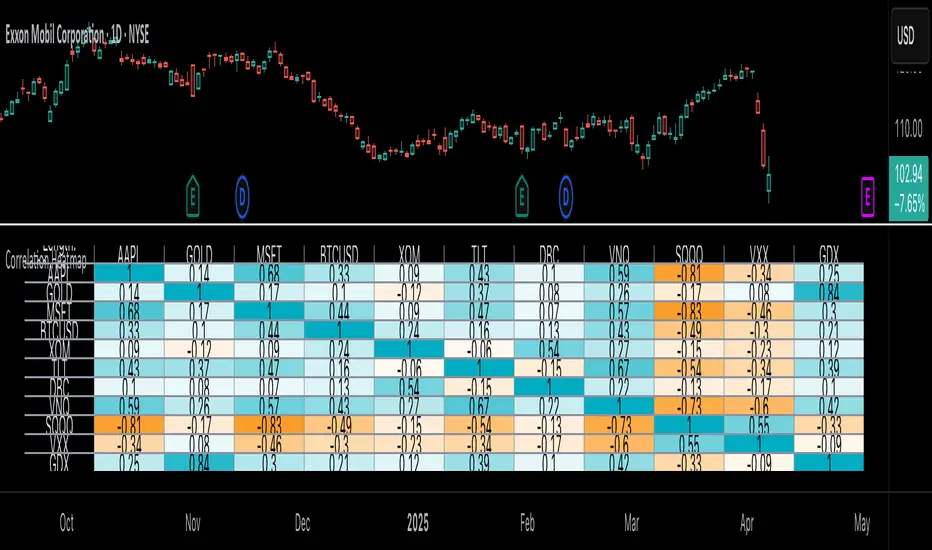

Correlation Heatmap█ OVERVIEW

This indicator creates a correlation matrix for a user-specified list of symbols based on their time-aligned weekly or monthly price returns. It calculates the Pearson correlation coefficient for each possible symbol pair, and it displays the results in a symmetric table with heatmap-colored cells. This format provides an intuitive view of the linear relationships between various symbols' price movements over a specific time range.

█ CONCEPTS

Correlation

Correlation typically refers to an observable statistical relationship between two datasets. In a financial time series context, it usually represents the extent to which sampled values from a pair of datasets, such as two series of price returns, vary jointly over time. More specifically, in this context, correlation describes the strength and direction of the relationship between the samples from both series.

If two separate time series tend to rise and fall together proportionally, they might be highly correlated. Likewise, if the series often vary in opposite directions, they might have a strong anticorrelation . If the two series do not exhibit a clear relationship, they might be uncorrelated .

Traders frequently analyze asset correlations to help optimize portfolios, assess market behaviors, identify potential risks, and support trading decisions. For instance, correlation often plays a key role in diversification . When two instruments exhibit a strong correlation in their returns, it might indicate that buying or selling both carries elevated unsystematic risk . Therefore, traders often aim to create balanced portfolios of relatively uncorrelated or anticorrelated assets to help promote investment diversity and potentially offset some of the risks.

When using correlation analysis to support investment decisions, it is crucial to understand the following caveats:

• Correlation does not imply causation . Two assets might vary jointly over an analyzed range, resulting in high correlation or anticorrelation in their returns, but that does not indicate that either instrument directly influences the other. Joint variability between assets might occur because of shared sensitivities to external factors, such as interest rates or global sentiment, or it might be entirely coincidental. In other words, correlation does not provide sufficient information to identify cause-and-effect relationships.

• Correlation does not predict the future relationship between two assets. It only reflects the estimated strength and direction of the relationship between the current analyzed samples. Financial time series are ever-changing. A strong trend between two assets can weaken or reverse in the future.

Correlation coefficient

A correlation coefficient is a numeric measure of correlation. Several coefficients exist, each quantifying different types of relationships between two datasets. The most common and widely known measure is the Pearson product-moment correlation coefficient , also known as the Pearson correlation coefficient or Pearson's r . Usually, when the term "correlation coefficient" is used without context, it refers to this correlation measure.

The Pearson correlation coefficient quantifies the strength and direction of the linear relationship between two variables. In other words, it indicates how consistently variables' values move together or in opposite directions in a proportional, linear manner. Its formula is as follows:

𝑟(𝑥, 𝑦) = cov(𝑥, 𝑦) / (𝜎𝑥 * 𝜎𝑦)

Where:

• 𝑥 is the first variable, and 𝑦 is the second variable.

• cov(𝑥, 𝑦) is the covariance between 𝑥 and 𝑦.

• 𝜎𝑥 is the standard deviation of 𝑥.

• 𝜎𝑦 is the standard deviation of 𝑦.

In essence, the correlation coefficient measures the covariance between two variables, normalized by the product of their standard deviations. The coefficient's value ranges from -1 to 1, allowing a more straightforward interpretation of the relationship between two datasets than what covariance alone provides:

• A value of 1 indicates a perfect positive correlation over the analyzed sample. As one variable's value changes, the other variable's value changes proportionally in the same direction .

• A value of -1 indicates a perfect negative correlation (anticorrelation). As one variable's value increases, the other variable's value decreases proportionally.

• A value of 0 indicates no linear relationship between the variables over the analyzed sample.

Aligning returns across instruments

In a financial time series, each data point (i.e., bar) in a sample represents information collected in periodic intervals. For instance, on a "1D" chart, bars form at specific times as successive days elapse.

However, the times of the data points for a symbol's standard dataset depend on its active sessions , and sessions vary across instrument types. For example, the daily session for NYSE stocks is 09:30 - 16:00 UTC-4/-5 on weekdays, Forex instruments have 24-hour sessions that span from 17:00 UTC-4/-5 on one weekday to 17:00 on the next, and new daily sessions for cryptocurrencies start at 00:00 UTC every day because crypto markets are consistently open.

Therefore, comparing the standard datasets for different asset types to identify correlations presents a challenge. If two symbols' datasets have bars that form at unaligned times, their correlation coefficient does not accurately describe their relationship. When calculating correlations between the returns for two assets, both datasets must maintain consistent time alignment in their values and cover identical ranges for meaningful results.

To address the issue of time alignment across instruments, this indicator requests confirmed weekly or monthly data from spread tickers constructed from the chart's ticker and another specified ticker. The datasets for spreads are derived from lower-timeframe data to ensure the values from all symbols come from aligned points in time, allowing a fair comparison between different instrument types. Additionally, each spread ticker ID includes necessary modifiers, such as extended hours and adjustments.

In this indicator, we use the following process to retrieve time-aligned returns for correlation calculations:

1. Request the current and previous prices from a spread representing the sum of the chart symbol and another symbol ( "chartSymbol + anotherSymbol" ).

2. Request the prices from another spread representing the difference between the two symbols ( "chartSymbol - anotherSymbol" ).

3. Calculate half of the difference between the values from both spreads ( 0.5 * (requestedSum - requestedDifference) ). The results represent the symbol's prices at times aligned with the sample points on the current chart.

4. Calculate the arithmetic return of the retrieved prices: (currentPrice - previousPrice) / previousPrice

5. Repeat steps 1-4 for each symbol requiring analysis.

It's crucial to note that because this process retrieves prices for a symbol at times consistent with periodic points on the current chart, the values can represent prices from before or after the closing time of the symbol's usual session.

Additionally, note that the maximum number of weeks or months in the correlation calculations depends on the chart's range and the largest time range common to all the requested symbols. To maximize the amount of data available for the calculations, we recommend setting the chart to use a daily or higher timeframe and specifying a chart symbol that covers a sufficient time range for your needs.

█ FEATURES

This indicator analyzes the correlations between several pairs of user-specified symbols to provide a structured, intuitive view of the relationships in their returns. Below are the indicator's key features:

Requesting a list of securities

The "Symbol list" text box in the indicator's "Settings/Inputs" tab accepts a comma-separated list of symbols or ticker identifiers with optional spaces (e.g., "XOM, MSFT, BITSTAMP:BTCUSD"). The indicator dynamically requests returns for each symbol in the list, then calculates the correlation between each pair of return series for its heatmap display.

Each item in the list must represent a valid symbol or ticker ID. If the list includes an invalid symbol, the script raises a runtime error.

To specify a broker/exchange for a symbol, include its name as a prefix with a colon in the "EXCHANGE:SYMBOL" format. If a symbol in the list does not specify an exchange prefix, the indicator selects the most commonly used exchange when requesting the data.

Note that the number of symbols allowed in the list depends on the user's plan. Users with non-professional plans can compare up to 20 symbols with this indicator, and users with professional plans can compare up to 32 symbols.

Timeframe and data length selection

The "Returns timeframe" input specifies whether the indicator uses weekly or monthly returns in its calculations. By default, its value is "1M", meaning the indicator analyzes monthly returns. Note that this script requires a chart timeframe lower than or equal to "1M". If the chart uses a higher timeframe, it causes a runtime error.

To customize the length of the data used in the correlation calculations, use the "Max periods" input. When enabled, the indicator limits the calculation window to the number of periods specified in the input field. Otherwise, it uses the chart's time range as the limit. The top-left corner of the table shows the number of confirmed weeks or months used in the calculations.

It's important to note that the number of confirmed periods in the correlation calculations is limited to the largest time range common to all the requested datasets, because a meaningful correlation matrix requires analyzing each symbol's returns under the same market conditions. Therefore, the correlation matrix can show different results for the same symbol pair if another listed symbol restricts the aligned data to a shorter time range.

Heatmap display

This indicator displays the correlations for each symbol pair in a heatmap-styled table representing a symmetric correlation matrix. Each row and column corresponds to a specific symbol, and the cells at their intersections correspond to symbol pairs . For example, the cell at the "AAPL" row and "MSFT" column shows the weekly or monthly correlation between those two symbols' returns. Likewise, the cell at the "MSFT" row and "AAPL" column shows the same value.

Note that the main diagonal cells in the display, where the row and column refer to the same symbol, all show a value of 1 because any series of non-na data is always perfectly correlated with itself.

The background of each correlation cell uses a gradient color based on the correlation value. By default, the gradient uses blue hues for positive correlation, orange hues for negative correlation, and white for no correlation. The intensity of each blue or orange hue corresponds to the strength of the measured correlation or anticorrelation. Users can customize the gradient's base colors using the inputs in the "Color gradient" section of the "Settings/Inputs" tab.

█ FOR Pine Script® CODERS

• This script uses the `getArrayFromString()` function from our ValueAtTime library to process the input list of symbols. The function splits the "string" value by its commas, then constructs an array of non-empty strings without leading or trailing whitespaces. Additionally, it uses the str.upper() function to convert each symbol's characters to uppercase.

• The script's `getAlignedReturns()` function requests time-aligned prices with two request.security() calls that use spread tickers based on the chart's symbol and another symbol. Then, it calculates the arithmetic return using the `changePercent()` function from the ta library. The `collectReturns()` function uses `getAlignedReturns()` within a loop and stores the data from each call within a matrix . The script calls the `arrayCorrelation()` function on pairs of rows from the returned matrix to calculate the correlation values.

• For consistency, the `getAlignedReturns()` function includes extended hours and dividend adjustment modifiers in its data requests. Additionally, it includes other settings inherited from the chart's context, such as "settlement-as-close" preferences.

• A Pine script can execute up to 40 or 64 unique `request.*()` function calls, depending on the user's plan. The maximum number of symbols this script compares is half the plan's limit, because `getAlignedReturns()` uses two request.security() calls.

• This script can use the request.security() function within a loop because all scripts in Pine v6 enable dynamic requests by default. Refer to the Dynamic requests section of the Other timeframes and data page to learn more about this feature, and see our v6 migration guide to learn what's new in Pine v6.

• The script's table uses two distinct color.from_gradient() calls in a switch structure to determine the cell colors for positive and negative correlation values. One call calculates the color for values from -1 to 0 based on the first and second input colors, and the other calculates the colors for values from 0 to 1 based on the second and third input colors.

Look first. Then leap.

ADR Nivele Horizontale dhe EMAThe user provided a Pine Script code for an indicator called "ADR Nivele Horizontale dhe EMA". The task is to explain how this code works. Hmm, first, I need to understand what this indicator does. The title mentions ADR levels and EMA, so it's probably combining horizontal lines based on Average Daily Range and some Exponential Moving Averages.

Looking at the code, the first part is the indicator declaration with version 6. The settings include an ADR period, levels above and below the mid, and line style. Then there's a section for calculations. They request daily high and low to compute the daily range. The ADR is the SMA of the daily range over the specified period. The mid is the average of daily high and low. The adr_val is half of ADR, maybe to create symmetrical levels around the mid.

Next, they create arrays for lines and labels above and below the mid. The loops go from 1 to levels_above/below, calculate each level, draw lines and labels. The mid line is also drawn with a different color. Then, there are several EMAs plotted: 13, 50, 200, 400, 600, 800, each with different colorsWait, but in Pine Script, when you use arrays to store lines and labels, you have to manage them properly to avoid repainting or memory issues. The code uses array.concat to add new lines and labels each bar. However, since this code is running on each bar, the for loops might be creating multiple lines each time, leading to too many objects. Oh right, but they use var to initialize the arrays, so they are only initialized once. Wait, no. The var keyword initializes the variable once, but in each iteration, they are concatenating new lines. Wait, no: the for loops are inside the main script, which runs on each bar. So every time a new bar is processed, the loops will run again, adding new lines and labels. That's a problem because each bar would create new lines, leading to an ever-increasing number of lines, which could hit the maximum limit (max_lines_count is set to 20, but maybe they have more bars). Oh, the indicator has max_lines_count=20, but the code might be creating multiple lines per bar. So maybe the code isn't handling the line management correctly. For example, if levels_above is 2, then each bar would create 2 new lines above and 2 below, plus the mid line. Over 20 bars, that's way over 20 lines. So this could cause the indicator to stop drawing after 20 lines. The user might not have realized that the lines are being recreated every bar, leading to a buildup. But perhaps the original code intended to have the lines update each bar, extending to the current bar. Let's see: in line.new, they use bar_index as the starting x1 and bar_index as x2. So each line is drawn from the previous bar's index to the current one. But since this is done on every bar, each line is only one bar long. Wait, no. Because on each new bar, the code creates a new line from the previous bar's index (bar_index , which is now the bar before the current one) to the current bar_index. So each line is just a segment from the previous bar to the current bar. But when the next bar comes, a new line is created again. So the result is that each level line is a series of one-bar-length segments, which might not be intended. The user probably wants continuous lines that extend from the left to the right, not just per bar. So this approach is incorrect. The correct way would be to have a line that starts at the first bar of the calculation and extends to the right, updating each bar. But the current code creates a new line each bar, leading to multiple short lines instead of one continuous line. That's a mistake.

So the main issue here is that the code is generating a new line segment for each bar, which is not efficient and would quickly hit the line limit. To fix this, instead of creating a new line every bar, they should create the line once and then update its position each bar. But in Pine Script, you can't directly update a line after it's created; instead, you need to track the line ID and use line.set_xy() to extend it. However, the current code uses array.concat to add new lines each bar, which isn't the right approach.

Therefore, the code as written will create multiple short lines instead of continuous horizontal lines. The correct approach for horizontal levels that extend to the right is to create the line once, starting at a certain bar and extending indefinitely, or to update the line's end point each new bar. But in Pine Script, you can't extend lines infinitely; you have to manage them each bar. Alternatively, using the 'line.extend' style might help, but I think the original code's logic is flawed here.

Additionally, the EMA part is straightforward: plotting multiple EMAs with different periods. That part should work as expected.

So the explanation should mention that the ADR levels are calculated based on the daily high and low, then the code attempts to draw horizontal lines above and below the mid-point. However, the way the lines are drawn may lead to multiple short segments instead of continuous lines, potentially causing performance issues or hitting the maximum line count. The EMAs are plotted correctly with various periods..

MA SniperThis indicator automatically finds the most effective moving average to use in a price crossover strategy—so you can focus on trading, not testing. It continuously evaluates a wide range of moving average periods, ranks them based on real-time market performance, and selects the one delivering the highest quality signals. The result? A smarter, adaptive tool that shows you exactly when price crosses its optimal moving average—bullish signals in green, bearish in red.

What makes it unique is the way it thinks.

Under the hood, the script doesn’t just pick a random MA or let you choose one manually. Instead, it backtests a large panel of moving average lengths for the current asset and timeframe. It evaluates each one by calculating its **Profit Factor**—a key performance metric used by pros to measure the quality of a strategy. Then, it assigns each MA a score and ranks them in a clean, built-in table so you can see, at a glance, which ones are currently most effective.

From that list, it picks the top-performing MA and uses it to generate live crossover signals on your chart. That MA is plotted automatically, and the signals adapt in real-time. This isn’t a static setup—it’s a dynamic system that evolves as the market evolves.

Even better: the indicator detects the type of instrument you’re trading (forex, stocks, etc.) and adjusts its internal calculations accordingly, including how many bars per day to consider. That means it remains highly accurate whether you’re trading EURUSD, SPX500, or TSLA.

You also get a real-time dashboard (via the table) that acts as a transparent scorecard. Want to see how other MAs are doing? You can. Want to understand why a certain MA was selected? The data is right there.

This tool is for traders who love crossover strategies but want something smarter, faster, and more precise—without spending hours manually testing. Whether you're scalping or swing trading, it offers a data-driven edge that’s hard to ignore.

Give it a try—you’ll quickly see how powerful it can be when your MA does the thinking for you.

This tool is for informational and educational purposes only. Trading involves risk, and past performance does not guarantee future results. Use responsibly.

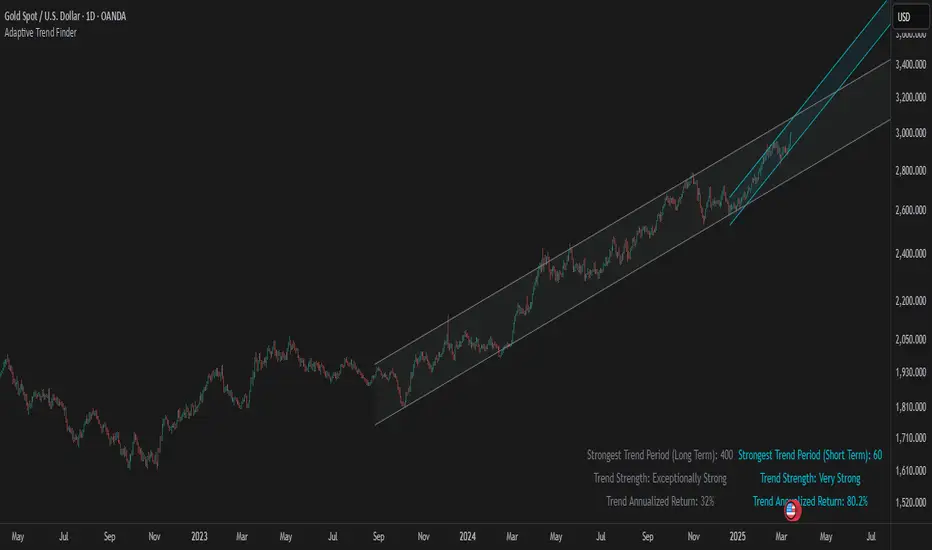

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

[GYTS-CE] Market Regime Detector🧊 Market Regime Detector (Community Edition)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 What is the Market Regime Detector?

The Market Regime Detector is an advanced, consensus-based indicator that identifies the current market state to increase the probability of profitable trades. By distinguishing between trending (bullish or bearish) and cyclic (range-bound) market conditions, this detector helps you select appropriate tactics for different environments. Instead of forcing a single strategy across all market conditions, our detector allows you to adapt your approach based on real-time market behaviour.

💮 The Importance of Market Regimes

Markets constantly shift between different behavioural states or "regimes":

• Bullish trending markets - characterised by sustained upward price movement

• Bearish trending markets - characterised by sustained downward price movement

• Cyclic markets - characterised by range-bound, oscillating behaviour

Each regime requires fundamentally different trading approaches. Trend-following strategies excel in trending markets but fail in cyclic ones, while mean-reversion strategies shine in cyclic markets but underperform in trending conditions. Detecting these regimes is essential for successful trading, which is why we've developed the Market Regime Detector to accurately identify market states using complementary detection methods.

🌸 --------- KEY FEATURES --------- 🌸

💮 Consensus-Based Detection

Rather than relying on a single method, our detector employs two complementary detection methodologies that analyse different aspects of market behaviour:

• Dominant Cycle Average (DCA) - analyzes price movement relative to its lookback period, a proxy for the dominant cycle

• Volatility Channel - examines price behaviour within adaptive volatility bands

These diverse perspectives are synthesised into a robust consensus that minimises false signals while maintaining responsiveness to genuine regime changes.

💮 Dominant Cycle Framework

The Market Regime Detector uses the concept of dominant cycles to establish a reference framework. You can input the dominant cycle period that best represents the natural rhythm of your market, providing a stable foundation for regime detection across different timeframes.

💮 Intuitive Parameter System

We've distilled complex technical parameters into intuitive controls that traders can easily understand:

• Adaptability - how quickly the detector responds to changing market conditions

• Sensitivity - how readily the detector identifies transitions between regimes

• Consensus requirement - how much agreement is needed among detection methods

This approach makes the detector accessible to traders of all experience levels while preserving the power of the underlying algorithms.

💮 Visual Market Feedback

The detector provides clear visual feedback about the current market regime through:

• Colour-coded chart backgrounds (purple shades for bullish, pink for bearish, yellow for cyclic)

• Colour-coded price bars

• Strength indicators showing the degree of consensus

• Customizable colour schemes to match your preferences or trading system

💮 Integration in the GYTS suite

The Market Regime Detector is compatible with the GYTS Suite , i.e. it passes the regime into the 🎼 Order Orchestrator where you can set how to trade the trending and cyclic regime.

🌸 --------- CONFIGURATION SETTINGS --------- 🌸

💮 Adaptability

Controls how quickly the Market Regime detector adapts to changing market conditions. You can see it as a low-frequency, long-term change parameter:

Very Low: Very slow adaptation, most stable but may miss regime changes

Low: Slower adaptation, more stability but less responsiveness

Normal: Balanced between stability and responsiveness

High: Faster adaptation, more responsive but less stable

Very High: Very fast adaptation, highly responsive but may generate false signals

This setting affects lookback periods and filter parameters across all detection methods.

💮 Sensitivity

Controls how sensitive the detector is to market regime transitions. This acts as a high-frequency, short-term change parameter:

Very Low: Requires substantial evidence to identify a regime change

Low: Less sensitive, reduces false signals but may miss some transitions

Normal: Balanced sensitivity suitable for most markets

High: More sensitive, detects subtle regime changes but may have more noise

Very High: Very sensitive, detects minor fluctuations but may produce frequent changes

This setting affects thresholds for regime detection across all methods.

💮 Dominant Cycle Period

This parameter allows you to specify the market's natural rhythm in bars. This represents a complete market cycle (up and down movement). Finding the right value for your specific market and timeframe might require some experimentation, but it's a crucial parameter that helps the detector accurately identify regime changes. Most of the times the cycle is between 20 and 40 bars.

💮 Consensus Mode

Determines how the signals from both detection methods are combined to produce the final market regime:

• Any Method (OR) : Signals bullish/bearish if either method detects that regime. If methods conflict (one bullish, one bearish), the stronger signal wins. More sensitive, catches more regime changes but may produce more false signals.

• All Methods (AND) : Signals only when both methods agree on the regime. More conservative, reduces false signals but might miss some legitimate regime changes.

• Weighted Decision : Balances both methods with equal weighting. Provides a middle ground between sensitivity and stability.

Each mode also calculates a continuous regime strength value that's used for colour intensity in the 'unconstrained' display mode.

💮 Display Mode

Choose how to display the market regime colours:

• Unconstrained regime: Shows the regime strength as a continuous gradient. This provides more nuanced visualisation where the intensity of the colour indicates the strength of the trend.

• Consensus only: Shows only the final consensus regime with fixed colours based on the detected regime type.

The background and bar colours will change to indicate the current market regime:

• Purple shades: Bullish trending market (darker purple indicates stronger bullish trend)

• Pink shades: Bearish trending market (darker pink indicates stronger bearish trend)

• Yellow: Cyclic (range-bound) market

💮 Custom Colour Options

The Market Regime Detector allows you to customize the colour scheme to match your personal preferences or to coordinate with other indicators:

• Use custom colours: Toggle to enable your own colour choices instead of the default scheme

• Transparency: Adjust the transparency level of all regime colours

• Bullish colours: Define custom colours for strong, medium, weak, and very weak bullish trends

• Bearish colours: Define custom colours for strong, medium, weak, and very weak bearish trends

• Cyclic colour: Define a custom colour for cyclic (range-bound) market conditions

🌸 --------- DETECTION METHODS --------- 🌸

💮 Dominant Cycle Average (DCA)

The Dominant Cycle Average method forms a key part of our detection system:

1. Theoretical Foundation :

The DCA method builds on cycle analysis and the observation that in trending markets, price consistently remains on one side of a moving average calculated using the dominant cycle period. In contrast, during cyclic markets, price oscillates around this average.

2. Calculation Process :

• We calculate a Simple Moving Average (SMA) using the specified lookback period - a proxy for the dominant cycle period

• We then analyse the proportion of time that price spends above or below this SMA over a lookback window. The theory is that the price should cross the SMA each half cycle, assuming that the dominant cycle period is correct and price follows a sinusoid.

• This lookback window is adaptive, scaling with the dominant cycle period (controlled by the Adaptability setting)

• The different values are standardised and normalised to possess more resolving power and to be more robust to noise.

3. Regime Classification :

• When the normalised proportion exceeds a positive threshold (determined by Sensitivity setting), the market is classified as bullish trending

• When it falls below a negative threshold, the market is classified as bearish trending

• When the proportion remains between these thresholds, the market is classified as cyclic

💮 Volatility Channel

The Volatility Channel method complements the DCA method by focusing on price movement relative to adaptive volatility bands:

1. Theoretical Foundation :

This method is based on the observation that trending markets tend to sustain movement outside of normal volatility ranges, while cyclic markets tend to remain contained within these ranges. By creating adaptive bands that adjust to current market volatility, we can detect when price behaviour indicates a trending or cyclic regime.

2. Calculation Process :

• We first calculate a smooth base channel center using a low pass filter, creating a noise-reduced centreline for price

• True Range (TR) is used to measure market volatility, which is then smoothed and scaled by the deviation factor (controlled by Sensitivity)

• Upper and lower bands are created by adding and subtracting this scaled volatility from the centreline

• Price is smoothed using an adaptive A2RMA filter, which has a very flat and stable behaviour, to reduce noise while preserving trend characteristics

• The position of this smoothed price relative to the bands is continuously monitored

3. Regime Classification :

• When smoothed price moves above the upper band, the market is classified as bullish trending

• When smoothed price moves below the lower band, the market is classified as bearish trending

• When price remains between the bands, the market is classified as cyclic

• The magnitude of price's excursion beyond the bands is used to determine trend strength

4. Adaptive Behaviour :

• The smoothing periods and deviation calculations automatically adjust based on the Adaptability setting

• The measured volatility is calculated over a period proportional to the dominant cycle, ensuring the detector works across different timeframes

• Both the center line and the bands adapt dynamically to changing market conditions, making the detector responsive yet stable

This method provides a unique perspective that complements the DCA approach, with the consensus mechanism synthesising insights from both methods.

🌸 --------- USAGE GUIDE --------- 🌸

💮 Starting with Default Settings

The default settings (Normal for Adaptability and Sensitivity, Weighted Decision for Consensus Mode) provide a balanced starting point suitable for most markets and timeframes. Begin by observing how these settings identify regimes in your preferred instruments.

💮 Finding the Optimal Dominant Cycle

The dominant cycle period is a critical parameter. Here are some approaches to finding an appropriate value:

• Start with typical values, usually something around 25 works well

• Visually identify the average distance between significant peaks and troughs

• Experiment with different values and observe which provides the most stable regime identification

• Consider using cycle-finding indicators to help identify the natural rhythm of your market

💮 Adjusting Parameters

• If you notice too many regime changes → Decrease Sensitivity or increase Consensus requirement

• If regime changes seem delayed → Increase Adaptability

• If a trending regime is not detected, the market is automatically assigned to be in a cyclic state

• If you want to see more nuanced regime transitions → Try the "unconstrained" display mode (note that this will not affect the output to other indicators)

💮 Trading Applications

Regime-Specific Strategies:

• Bullish Trending Regime - Use trend-following strategies, trail stops wider, focus on breakouts, consider holding positions longer, and emphasize buying dips

• Bearish Trending Regime - Consider shorts, tighter stops, focus on breakdown points, sell rallies, implement downside protection, and reduce position sizes

• Cyclic Regime - Apply mean-reversion strategies, trade range boundaries, apply oscillators, target definable support/resistance levels, and use profit-taking at extremes

Strategy Switching:

Create a set of rules for each market regime and switch between them based on the detector's signal. This approach can significantly improve performance compared to applying a single strategy across all market conditions.

GYTS Suite Integration:

• In the GYTS 🎼 Order Orchestrator, select the '🔗 STREAM-int 🧊 Market Regime' as the market regime source

• Note that the consensus output (i.e. not the "unconstrained" display) will be used in this stream

• Create different strategies for trending (bullish/bearish) and cyclic regimes. The GYTS 🎼 Order Orchestrator is specifically made for this.

• The output stream is actually very simple, and can possibly be used in indicators and strategies as well. It outputs 1 for bullish, -1 for bearish and 0 for cyclic regime.

🌸 --------- FINAL NOTES --------- 🌸

💮 Development Philosophy

The Market Regime Detector has been developed with several key principles in mind:

1. Robustness - The detection methods have been rigorously tested across diverse markets and timeframes to ensure reliable performance.

2. Adaptability - The detector automatically adjusts to changing market conditions, requiring minimal manual intervention.

3. Complementarity - Each detection method provides a unique perspective, with the collective consensus being more reliable than any individual method.

4. Intuitiveness - Complex technical parameters have been abstracted into easily understood controls.

💮 Ongoing Refinement

The Market Regime Detector is under continuous development. We regularly:

• Fine-tune parameters based on expanded market data

• Research and integrate new detection methodologies

• Optimise computational efficiency for real-time analysis

Your feedback and suggestions are very important in this ongoing refinement process!

TimezoneLibrary with pre-defined timezone enums that can be used to request a timezone input from the user. The library provides a `tostring()` function to convert enum values to a valid string that can be used as a `timezone` parameter in pine script built-in functions. The library also includes a bonus function to get a formatted UTC offset from a UNIX timestamp.

The timezone enums in this library were compiled by referencing the available timezone options from TradingView chart settings as well as multiple Wikipedia articles relating to lists of time zones.

Some enums from this library are used to retrieve an IANA time zone identifier, while other enums only use UTC/GMT offset notation. It is important to note that the Pine Script User Manual recommends using IANA notation in most cases.

HOW TO USE

This library is intended to be used by Pine Coders who wish to provide their users with a simple way to input a timezone. Using this library is as easy as 1, 2, 3:

Step 1

Import the library into your script. Replace with the latest available version number for this library.

//@version=6

indicator("Example")

import n00btraders/Timezone/ as tz

Step 2

Select one of the available enums from the library and use it as an input. Tip: view the library source code and scroll through the enums at the top to find the best choice for your script.

timezoneInput = input.enum(tz.TimezoneID.EXCHANGE, "Timezone")

Step 3

Convert the user-selected input into a valid string that can be used in one of the pine script built-in functions that have a `timezone` parameter.

string timezone = tz.tostring(timezoneInput)

EXPORTED FUNCTIONS

There are multiple 𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐() functions in this library: one for each timezone enum. The function takes a single parameter: any enum field from one of the available timezone enums that are exported by this library. Depending on the selected enum, the function will return a time zone string in either UTC/GMT notation or IANA notation.

Note: to avoid confusion with the built-in `str.tostring()` function, it is recommended to use this library's `tostring()` as a method rather than a function:

string timezone = timezoneInput.tostring()

offset(timestamp, format, timezone, prefix, colon)

Formats the time offset from a UNIX timestamp represented in a specified timezone.

Namespace types: series OffsetFormat

Parameters:

timestamp (int) : (series int) A UNIX time.

format (series OffsetFormat) : (series OffsetFormat) A time offset format.

timezone (string) : (series string) A UTC/GMT offset or IANA time zone identifier.

prefix (string) : (series string) Optional 'UTC' or 'GMT' prefix for the result.

colon (bool) : (series bool) Optional usage of colon separator.

Returns: Time zone offset using the selected format.

The 𝚘𝚏𝚏𝚜𝚎𝚝() function is provided as a convenient alternative to manually using `str.format_time()` and then manipulating the result.

The OffsetFormat enum is used to decide the format of the result from the `offset()` function. The library source code contains comments above this enum declaration that describe how each enum field will modify a time offset.

Tip: hover over the `offset()` function call in the Pine Editor to display a pop-up containing:

Function description

Detailed parameter list, including default values

Example function calls

Example outputs for different OffsetFormat.* enum values

NOTES

At the time of this publication, Pine cannot be used to access a chart's selected time zone. Therefore, the main benefit of this library is to provide a quick and easy way to create a pine script input for a time zone (most commonly, the same time zone selected in the user's chart settings).

At the time of the creation of this library, there are 95 Time Zones made available in the TradingView chart settings. If any changes are made to the time zone settings, this library will be updated to match the new changes.

All time zone enums (and their individual fields) in this library were manually verified and tested to ensure correctness.

An example usage of this library is included at the bottom of the source code.

Credits to HoanGhetti for providing a nice Markdown resource which I referenced to be able to create a formatted informational pop-up for this library's `offset()` function.

Uptrick: Time Based ReversionIntroduction

The Uptrick: Time Based Reversion indicator is designed to provide a comprehensive view of market momentum and potential trend shifts by combining multiple moving averages, a streak-based trend analysis system, and adaptive color visualization. It helps traders identify strong trends, spot potential reversals, and make more informed trading decisions.

Purpose

The primary goal of this indicator is to assist traders in distinguishing between sustained market movements and short-lived fluctuations. By evaluating how price behaves relative to its moving averages, and by measuring consecutive streaks above or below these averages, the indicator highlights areas where trends are likely to continue or lose momentum.

Overview

Uptrick: Time Based Reversion calculates one or more moving averages of price data and then tracks the number of consecutive bars (streaks) above or below these averages. This streak-based detection provides insight into whether a trend is gaining strength or nearing a potential reversal point. The indicator offers:

• Multiple moving average types (SMA, EMA, WMA)

• Optional second and third moving average layers for additional smoothing of first moving average

• A streak detection system to quantify trend intensity

• A dynamic color scheme that changes with streak strength

• Optional buy and sell signals for potential trade entries and exits

• A ribbon mode that applies moving averages to Open, High, Low, and Close prices for a more detailed visualization of overall trend alignment

Originality and Uniqueness

Unlike traditional moving average indicators, Uptrick: Time Based Reversion incorporates a streak measurement system to detect trend strength. This approach helps clarify whether a price movement is merely a quick fluctuation or part of a longer-lasting trend. Additionally, the optional ribbon mode extends this logic to Open, High, Low, and Close prices, creating a layered and intuitive visualization that shows complete trend alignment.

Inputs and Features

1. Enable Ribbon Mode

This input lets you activate or deactivate the ribbon display of multiple moving averages. When enabled, the script plots moving averages for the Open, High, Low, and Close prices and uses color fills to show whether these four data points are collectively above or below their respective moving averages.

2. Color Scheme Selection

Users can choose from several predefined color schemes, such as Default, Emerald, Crimson, Sapphire, Gold, Purple, Teal, Orange, Gray, Lime, or Aqua. Each scheme assigns distinct bullish, bearish and neutral colors..

3. Show Buy/Sell Signals

The indicator can display buy or sell signals based on its streak analysis logic. These signals appear as markers on the chart, indicating a “Safe Uptrend” (buy) or “Safe Downtrend” (sell).

4. Moving Average Types and Lengths

• First MA Type and Length: Choose SMA, EMA, or WMA along with a customizable period.

• Second and Third MA Types and Lengths: You can optionally stack additional moving averages for further smoothing, each with its own customizable type and period.

5. Streak Threshold Multiplier

This numeric input determines how strong a streak must be before the script considers it a “safe” trend. A higher multiplier requires a longer or more intense streak for a buy or sell signal.

6. Dynamic Transparency Calculation

The color intensity adapts to the streak’s strength. Longer streaks increase the transparency of the opposing color, making the current dominant color stand out. This feature ensures that a vigorous uptrend or downtrend is visually distinct from short-lived or weaker moves.

7. Ribbon Moving Averages

In ribbon mode, the script calculates moving averages for the Open, High, Low, and Close prices. Each of these is optionally smoothed again if the second and/or third moving average layers are active. The final result is a ribbon of moving averages that helps confirm whether the market is uniformly aligned above or below these key reference points.

Calculation Methodology

1. Initial Moving Average

The script calculates the first moving average (SMA, EMA, or WMA) of the closing price over a user-defined period.

2. Optional Secondary and Tertiary Averages

If selected, the script then applies a second and/or third smoothing step. Each of these steps can be a different type of moving average (SMA, EMA, or WMA) with its own period length.

3. Streak Detection

The indicator counts consecutive bars above or below the smoothed moving average. A running total (streakUp or streakDown) increments with every bar that remains above or below that average.

4. Reversion Intensity

The script compares the current streak value to its own average (calculated over the final chosen period). This ratio determines whether the streak is nearing a likely reversion or is strong enough to continue.

5. Color Assignment and Signals

The indicator calculates color transparency based on streak intensity. Buy and sell signals appear when the streak meets or exceeds the threshold multiplier, indicating a safe uptrend or downtrend.

Color Schemes and Visualization

This indicator offers multiple predefined color sets. Each scheme specifies a unique bullish color, bearish color and neutral color. The script automatically varies transparency to highlight strong trends and fade weaker ones, making it visually clear when a trend is intensifying or losing momentum.

Smoothing Techniques