5 MAs w. alerts [LucF]Is this gazillionth MA indicator worth an addition to the already crowded field of contenders? I say yes! This one shows up to 5 MAs and 6 different marker conditions that can be used to create alerts, among many other goodies.

Features

MAs can be darkened when they are falling.

MAs from another time frame can be displayed, with the option of smoothing them.

Markers can be filtered to Longs or Shorts only.

EMAs can be selected for either all or the two shortest MAs.

The background can be colored using any of the marker states except no. 3.

Markers are:

1. On crosses between any two user-defined MAs,

2. When price is above or below an MA,

3. On Quick Flips (a specific setup involving a cross, multiple MA states and increasing volume, when available),

4. When the difference between two MAs is within a % of its high/low historic values,

5. When an MA has been rising/falling for n bars,

6. When the difference between two MAs is greater than a multiple of ATR.

Some markers use similar visual cues, so distinguishing them will be a challenge if they are used concurrently.

Alerts

Alerts can be created on any combination of alerts. Only non-consecutive instances of markers 5 and 6 will trigger the alert condition. Make sure you are on the interval you want the alert to run at. Using the “Once Per Bar Close” trigger condition is usually the best option.

When an alert is created in TradingView, a snapshot of the indicator’s settings is saved with the alert, which then takes on a life of its own. That is why even though there is only one alert to choose from when you bring up the alert creation dialog box and choose “5 MAs”, that alert can be triggered from any number of conditions. You select those conditions by activating the markers you want the alert to trigger on before creating the alert. If you have selected multiple conditions, then it can be a good idea to record a reminder in the alert’s message field. When the alert triggers, you will need the indicator on the chart to figure out which one of your conditions triggered the alert, as there is currently no way to dynamically change the alert’s message field from within the script.

Background settings will not trigger alerts; only marker configurations.

Notes

MAs are just… averages. Trader lure would have them act as support and resistance levels. I’m not sure about that, and not the only one thinking along these lines. Adam Grimes has studied moving averages in quite a bit of detail. His numbers point to no evidence indicating they act as support/resistance, and to specific MA lengths not being more meaningful than others. His point of view is debated by some—not by me. Mean reversion does not entail that price stops when it reaches its MA; rather, it makes sense to me that price would often more or less oscillate around its MA, which entails the MA does not act as support/resistance. Aren’t the best mean reversion opportunities when price is furthest away from its MA? If so, it should be more profitable to identify these areas, which some of this indicator’s markers try to do.

I think MAs can be much more powerful when thought of as instruments we can use to situate price events in contexts of various resolutions, from the instantaneous to the big picture. Accordingly, I use the relative positions and slopes of MAs in both discretionary and automated trading; but never their purported ability to support/resist.

Regardless of how you use MAs, I hope you will find this indicator useful.

Biased References

The Art and Science of Technical Analysis: Market Structure, Price Action, and Trading Strategies, Adam Grimes, 2012.

Does the 200 day moving average “work”?

Moving averages: digging deeper

Поиск скриптов по запросу "one一季度财报"

[CS] NWMA Moving Average 3.0PineScript Implementation of Moving Average 3.0 first referenced by Manfred G. Dürschner as New wma or Nwma.

See amazing original paper Moving Averages 3.0 at page 27:

ifta.org

As shown in the picture Nwma is performing better than DEMA, TEMA, EMA, and other common used moving averages such as Hull MA that is prone to overshooting. With NWMA lag is extremely reduced.

As already implemented in NinjaTrader C# Nwma plugin by sumana.m:

ninjatrader.com

(from the original paper)

Nyquist Criterion

In signal processing theory, the application of a MA to itself can be seen as a Sampling procedure. The sampled signal is the MA (referred to as MA1) and the sampling signal is the MA as well (referred to as MA2). If additional periodic cycles which are not included in the price series are to be avoided sampling must obey the Nyquist Criterion . With the cycle period as parameter, the usual one in Technical Analysis, the Nyquist Criterion reads as follows: n1 = λ*n2 , with λ ≥ 2. n1 is the cycle period of the sampled signal to which a sampling signal with cycle period n2 is applied. n1 must at least be twice as large as n2. In Mulloy´s and Ehlers´ approaches (referred to as Moving Averages 2.0) both cycle periods are equal. Moving Averages 3.0 Using the Nyquist Criterion there is a relation by which the application of a MA to itself can be described more precisely. In figure 2 a price series C (black line), one MA (MA1, red line) with lag L1 to the price series and another MA with lag L2 to MA1 (MA2, blue line) are illustrated. Based on the approximation and the relations described in figure 2 the following equation holds: (1) D1/D2 = (C – MA1)/(MA1 – MA2) = L1/L2 According to the lag formulas in the introduction L1/L2 can be written as follows:

α := L1/L2 = (n1 – 1)/(n2 – 1).

In this expression denominator 2 for the SMA and EMA as well as denominator 3 for the WMA are missing. α is therefore valid for all three MAs.

Using the Nyquist Criterion one gets for α the following result:

(2) α = λ* (n1 – 1)/(n1 – λ).

α put in (1) and C replaced by the approximation term NMA, the notation for the new MA, one gets:

NMA = (1 +α) MA1 – α MA2.

In detail, equation (2) reads as follows:

(3) NMA = (1 + α) MA1 – α

MA2 ,

(4) α = λ* (n1 – 1)/(n1 – λ), with λ ≥ 2.

(3) and (4) are equations for a group of MAs (notation: Moving Averages 3.0). They are independent of the choice of an MA. As the WMA shows the smallest lag (see introduction), it should generally be the first choice for the NMA. n1 = n2 results in the value 1 for α and λ, respectively. Then equation (3) passes into Ehlers´ formula. Thus Ehlers´ formula is included in the NMA formula as limiting value. It follows from a short calculation that the lag for NMA results in a theoretical value zero.

Please enjoy,

CryptoStatistical

General Filter Estimator-An Experiment on Estimating EverythingIntroduction

The last indicators i posted where about estimating the least squares moving average, the task of estimating a filter is a funny one because its always a challenge and it require to be really creative. After the last publication of the 1LC-LSMA , who estimate the lsma with 1 line of code and only 3 functions i felt like i could maybe make something more flexible and less complex with the ability to approximate any filter output. Its possible, but the methods to do so are not something that pinescript can do, we have to use another base for our estimation using coefficients, so i inspired myself from the alpha-beta filter and i started writing the code.

Calculation and The Estimation Coefficients

Simplicity is the key word, its also my signature style, if i want something good it should be simple enough, so my code look like that :

p = length/beta

a = close - nz(b ,close)

b = nz(b ,close) + a/p*gamma

3 line, 2 function, its a good start, we could put everything in one line of code but its easier to see it this way. length control the smoothing amount of the filter, for any filter f(Period) Period should be equal to length and f(Period) = p , it would be inconvenient to have to use a different length period than the one used in the filter we want to estimate (imagine our estimation with length = 50 estimating an ema with period = 100) , this is where the first coefficients beta will be useful, it will allow us to leave length as it is. In general beta will be greater than 1, the greater it will be the less lag the filter will have, this coefficient will be useful to estimate low lagging filters, gamma however is the coefficient who will estimate lagging filters, in general it will range around .

We can get loose easily with those coefficients estimation but i will leave a coefficients table in the code for estimating popular filters, and some comparison below.

Estimating a Simple Moving Average

Of course, the boxcar filter, the running mean, the simple moving average, its an easy filter to use and calculate.

For an SMA use the following coefficients :

beta = 2

gamma = 0.5

Our filter is in red and the moving average in white with both length at 50 (This goes for every comparison we will do)

Its a bit imprecise but its a simple moving average, not the most interesting thing to estimate.

Estimating an Exponential Moving Average

The ema is a great filter because its length times more computing efficient than a simple moving average. For the EMA use the following coefficients :

beta = 3

gamma = 0.4

N.B : The EMA is rougher than the SMA, so it filter less, this is why its faster and closer to the price

Estimating The Hull Moving Average

Its a good filter for technical analysis with tons of use, lets try to estimate it ! For the HMA use the following coefficients :

beta = 4

gamma = 0.85

Looks ok, of course if you find better coefficients i will test them and actualize the coefficient table, i will also put a thank message.

Estimating a LSMA

Of course i was gonna estimate it, but this time this estimation does not have anything a lsma have, no moving average, no standard deviation, no correlation coefficient, lets do it.

For the LSMA use the following coefficients :

beta = 3.5

gamma = 0.9

Its far from being the best estimation, but its more efficient than any other i previously made.

Estimating the Quadratic Least Square Moving Average

I doubted about this one but it can be approximated as well. For the QLSMA use the following coefficients :

beta = 5.25

gamma = 1

Another ok estimate, the estimate filter a bit more than needed but its ok.

Jurik Moving Average

Its far from being a filter that i like and its a bit old. For the comparison i will use the JMA provided by @everget described in this article : c.mql5.com

For the JMA use the following coefficients :

for phase = 0

beta = pow*2 (pow is a parameter in the Jma)

gamma = 0.5

Here length = 50, phase = 0, pow = 5 so beta = 10

Looks pretty good considering the fact that the Jma use an adaptive architecture.

Discussion

I let you the task to judge if the estimation is good or not, my motivation was to estimate such filters using the less amount of calculations as possible, in itself i think that the code is quite elegant like all the codes of IIR filters (IIR Filters = Infinite Impulse Response : Filters using recursion) .

It could be possible to have a better estimate of the coefficients using optimization methods like the gradient descent. This is not feasible in pinescript but i could think about it using python or R.

Coefficients should be dependant of length but this would lead to a massive work, the variation of the estimation using fixed coefficients when using different length periods is just ok if we can allow some errors of precision.

I dont think it should be possible to estimate adaptive filter relying a lot on their adaptive parameter/smoothing constant except by making our coefficients adaptive (gamma could be)

So at the end ? What make a filter truly unique ? From my point of sight the architecture of a filter and the problem he is trying to solve is what make him unique rather than its output result. If you become a signal, hide yourself into noise, then look at the filters trying to find you, what a challenging game, this is why we need filters.

Conclusion

I wanted to give a simple filter estimator relying on two coefficients in order to estimate both lagging and low-lagging filters. I will try to give more precise estimate and update the indicator with new coefficients.

Thanks for reading !

BTC Volume Lines [v2018-11-17] @ LekkerCryptisch.nlCombine the volume of 8 BTCUSD exchanges in one graph.

Three use cases:

1) See the absolute volumes in one graph

2) See the relative volumes in one graph

3) See the deviation of the EMA the volumes in one graph

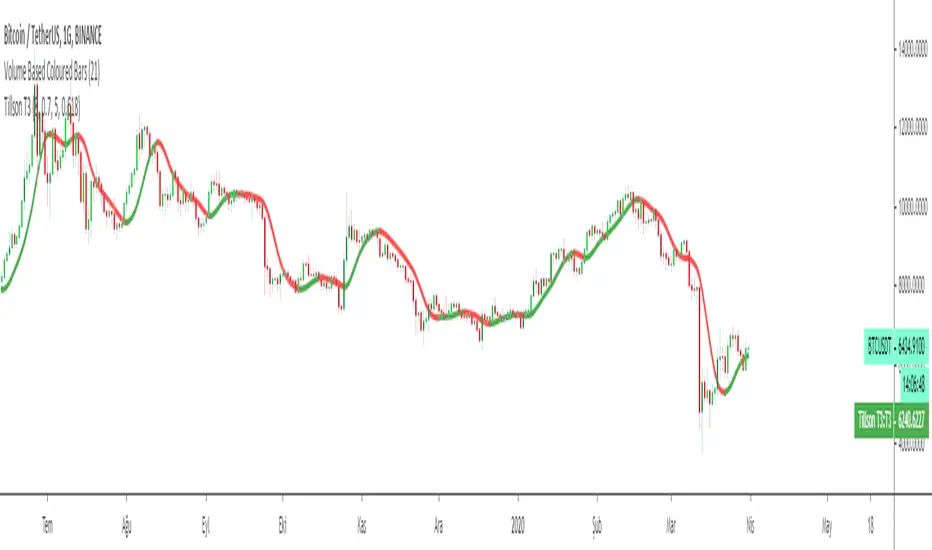

Tillson T3 Moving Average MTFMULTIPLE TIME FRAME version of Tillson T3 Moving Average Indicator

Developed by Tim Tillson, the T3 Moving Average is considered superior -1.60% to traditional moving averages as it is smoother, more responsive and thus performs better in ranging market conditions as well. However, it bears the disadvantage of overshooting the price as it attempts to realign itself to current market conditions.

It incorporates a smoothing technique which allows it to plot curves more gradual than ordinary moving averages and with a smaller lag. Its smoothness is derived from the fact that it is a weighted sum of a single EMA , double EMA , triple EMA and so on. When a trend is formed, the price action will stay above or below the trend during most of its progression and will hardly be touched by any swings. Thus, a confirmed penetration of the T3 MA and the lack of a following reversal often indicates the end of a trend.

The T3 Moving Average generally produces entry signals similar to other moving averages and thus is traded largely in the same manner. Here are several assumptions:

If the price action is above the T3 Moving Average and the indicator is headed upward, then we have a bullish trend and should only enter long trades (advisable for novice/intermediate traders). If the price is below the T3 Moving Average and it is edging lower, then we have a bearish trend and should limit entries to short. Below you can see it visualized in a trading platform.

Although the T3 MA is considered as one of the best swing following indicators that can be used on all time frames and in any market, it is still not advisable for novice/intermediate traders to increase their risk level and enter the market during trading ranges (especially tight ones). Thus, for the purposes of this article we will limit our entry signals only to such in trending conditions.

Once the market is displaying trending behavior, we can place with-trend entry orders as soon as the price pulls back to the moving average (undershooting or overshooting it will also work). As we know, moving averages are strong resistance/support levels, thus the price is more likely to rebound from them and resume its with-trend direction instead of penetrating it and reversing the trend.

And so, in a bull trend, if the market pulls back to the moving average, we can fairly safely assume that it will bounce off the T3 MA and resume upward momentum, thus we can go long. The same logic is in force during a bearish trend .

And last but not least, the T3 Moving Average can be used to generate entry signals upon crossing with another T3 MA with a longer trackback period (just like any other moving average crossover). When the fast T3 crosses the slower one from below and edges higher, this is called a Golden Cross and produces a bullish entry signal. When the faster T3 crosses the slower one from above and declines further, the scenario is called a Death Cross and signifies bearish conditions.

I Personally added a second T3 line with a volume factor of 0.618 (Fibonacci Ratio) and length of 3 (fibonacci number) which can be added by selecting the box in the input section. traders can combine the two lines to have Buy/Sell signals from the crosses.

Developed by Tim Tillson

Inverse Fisher Transform on STOCHASTIC (modified graphics)Modified the graphic representation of the script from John Ehlers - From California, USA, he is a veteran trader. With 35 years trading experience he has seen it all. John has an engineering background that led to his technical approach to trading ignoring fundamental analysis (with one important exception). John strongly believes in cycles. He’d rather exit a trade when the cycle ends or a new one starts. He uses the MESA principle to make predictions about cycles in the market and trades one hundred percent automatically.

In the show John reveals:

• What is more appropriate than trading individual stocks

• The one thing he relies upon in his approach to the market

• The detail surrounding his unique trading style

• What important thing underpins the market and gives every trader an edge

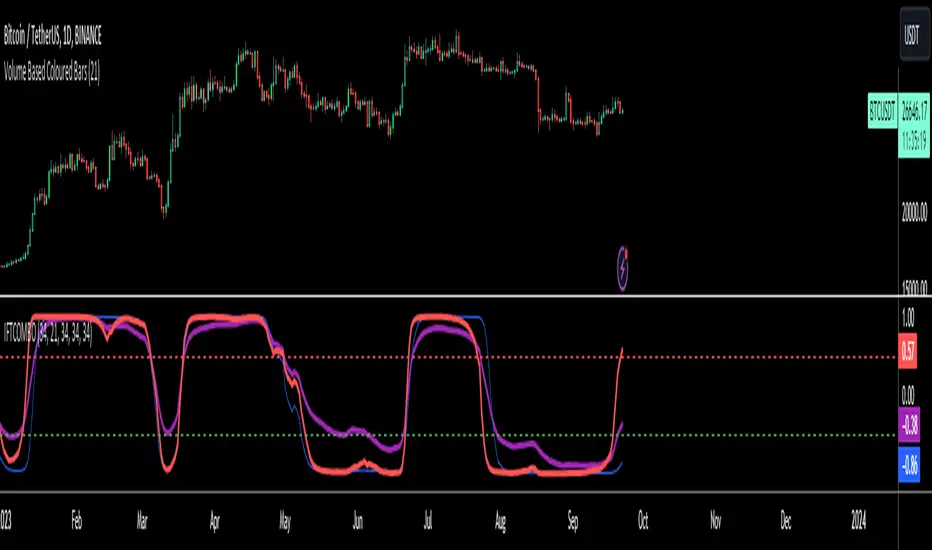

About INVERSE FISHER TRANSFORM:

The purpose of technical indicators is to help with your timing decisions to buy or sell. Hopefully, the signals are clear and unequivocal. However, more often than not your decision to pull the trigger is accompanied by crossing your fingers. Even if you have placed only a few trades you know the drill. In this article I will show you a way to make your oscillator-type indicators make clear black-or-white indication of the time to buy or sell. I will do this by using the Inverse Fisher Transform to alter the Probability Distribution Function (PDF) of your indicators. In the past12 I have noted that the PDF of price and indicators do not have a Gaussian, or Normal, probability distribution. A Gaussian PDF is the familiar bell-shaped curve where the long “tails” mean that wide deviations from the mean occur with relatively low probability. The Fisher Transform can be applied to almost any normalized data set to make the resulting PDF nearly Gaussian, with the result that the turning points are sharply peaked and easy to identify. The Fisher Transform is defined by the equation

1)

Whereas the Fisher Transform is expansive, the Inverse Fisher Transform is compressive. The Inverse Fisher Transform is found by solving equation 1 for x in terms of y. The Inverse Fisher Transform is:

2)

The transfer response of the Inverse Fisher Transform is shown in Figure 1. If the input falls between –0.5 and +0.5, the output is nearly the same as the input. For larger absolute values (say, larger than 2), the output is compressed to be no larger than unity. The result of using the Inverse Fisher Transform is that the output has a very high probability of being either +1 or –1. This bipolar probability distribution makes the Inverse Fisher Transform ideal for generating an indicator that provides clear buy and sell signals.

Tillson T3 Moving Average by KIVANÇ fr3762Developed by Tim Tillson, the T3 Moving Average is considered superior to traditional moving averages as it is smoother, more responsive and thus performs better in ranging market conditions as well. However, it bears the disadvantage of overshooting the price as it attempts to realign itself to current market conditions.

It incorporates a smoothing technique which allows it to plot curves more gradual than ordinary moving averages and with a smaller lag. Its smoothness is derived from the fact that it is a weighted sum of a single EMA , double EMA , triple EMA and so on. When a trend is formed, the price action will stay above or below the trend during most of its progression and will hardly be touched by any swings. Thus, a confirmed penetration of the T3 MA and the lack of a following reversal often indicates the end of a trend.

The T3 Moving Average generally produces entry signals similar to other moving averages and thus is traded largely in the same manner. Here are several assumptions:

If the price action is above the T3 Moving Average and the indicator is headed upward, then we have a bullish trend and should only enter long trades (advisable for novice/intermediate traders). If the price is below the T3 Moving Average and it is edging lower, then we have a bearish trend and should limit entries to short. Below you can see it visualized in a trading platform.

Although the T3 MA is considered as one of the best swing following indicators that can be used on all time frames and in any market, it is still not advisable for novice/intermediate traders to increase their risk level and enter the market during trading ranges (especially tight ones). Thus, for the purposes of this article we will limit our entry signals only to such in trending conditions.

Once the market is displaying trending behavior, we can place with-trend entry orders as soon as the price pulls back to the moving average (undershooting or overshooting it will also work). As we know, moving averages are strong resistance/support levels, thus the price is more likely to rebound from them and resume its with-trend direction instead of penetrating it and reversing the trend.

And so, in a bull trend, if the market pulls back to the moving average, we can fairly safely assume that it will bounce off the T3 MA and resume upward momentum, thus we can go long. The same logic is in force during a bearish trend .

And last but not least, the T3 Moving Average can be used to generate entry signals upon crossing with another T3 MA with a longer trackback period (just like any other moving average crossover). When the fast T3 crosses the slower one from below and edges higher, this is called a Golden Cross and produces a bullish entry signal. When the faster T3 crosses the slower one from above and declines further, the scenario is called a Death Cross and signifies bearish conditions.

I Personally added a second T3 line with a volume factor of 0.618 (Fibonacci Ratio) and length of 3 (fibonacci number) which can be added by selecting the box in the input section. traders can combine the two lines to have Buy/Sell signals from the crosses.

Developed by Tim Tillson

Inverse Fisher Transform COMBO STO+RSI+CCIv2 by KIVANÇ fr3762A combined 3in1 version of pre shared INVERSE FISHER TRANSFORM indicators on RSI , on STOCHASTIC and on CCIv2 to provide space for 2 more indicators for users...

About John EHLERS:

From California, USA, John is a veteran trader. With 35 years trading experience he has seen it all. John has an engineering background that led to his technical approach to trading ignoring fundamental analysis (with one important exception).

John strongly believes in cycles. He’d rather exit a trade when the cycle ends or a new one starts. He uses the MESA principle to make predictions about cycles in the market and trades one hundred percent automatically.

In the show John reveals:

• What is more appropriate than trading individual stocks

• The one thing he relies upon in his approach to the market

• The detail surrounding his unique trading style

• What important thing underpins the market and gives every trader an edge

About INVERSE FISHER TRANSFORM:

The purpose of technical indicators is to help with your timing decisions to buy or

sell. Hopefully, the signals are clear and unequivocal. However, more often than

not your decision to pull the trigger is accompanied by crossing your fingers.

Even if you have placed only a few trades you know the drill.

In this article I will show you a way to make your oscillator-type indicators make

clear black-or-white indication of the time to buy or sell. I will do this by using the

Inverse Fisher Transform to alter the Probability Distribution Function ( PDF ) of

your indicators. In the past12 I have noted that the PDF of price and indicators do

not have a Gaussian, or Normal, probability distribution. A Gaussian PDF is the

familiar bell-shaped curve where the long “tails” mean that wide deviations from

the mean occur with relatively low probability. The Fisher Transform can be

applied to almost any normalized data set to make the resulting PDF nearly

Gaussian, with the result that the turning points are sharply peaked and easy to

identify. The Fisher Transform is defined by the equation

1)

Whereas the Fisher Transform is expansive, the Inverse Fisher Transform is

compressive. The Inverse Fisher Transform is found by solving equation 1 for x

in terms of y. The Inverse Fisher Transform is:

2)

The transfer response of the Inverse Fisher Transform is shown in Figure 1. If

the input falls between –0.5 and +0.5, the output is nearly the same as the input.

For larger absolute values (say, larger than 2), the output is compressed to be no

larger than unity . The result of using the Inverse Fisher Transform is that the

output has a very high probability of being either +1 or –1. This bipolar

probability distribution makes the Inverse Fisher Transform ideal for generating

an indicator that provides clear buy and sell signals.

Creator: John EHLERS

Inverse Fisher Transform on SMI (Stochastic Momentum Index)Inverse Fisher Transform on SMI (Stochastic Momentum Index)

About John EHLERS:

From California, USA, John is a veteran trader. With 35 years trading experience he has seen it all. John has an engineering background that led to his technical approach to trading ignoring fundamental analysis (with one important exception).

John strongly believes in cycles. He’d rather exit a trade when the cycle ends or a new one starts. He uses the MESA principle to make predictions about cycles in the market and trades one hundred percent automatically.

In the show John reveals:

• What is more appropriate than trading individual stocks

• The one thing he relies upon in his approach to the market

• The detail surrounding his unique trading style

• What important thing underpins the market and gives every trader an edge

About INVERSE FISHER TRANSFORM:

The purpose of technical indicators is to help with your timing decisions to buy or

sell. Hopefully, the signals are clear and unequivocal. However, more often than

not your decision to pull the trigger is accompanied by crossing your fingers.

Even if you have placed only a few trades you know the drill.

In this article I will show you a way to make your oscillator-type indicators make

clear black-or-white indication of the time to buy or sell. I will do this by using the

Inverse Fisher Transform to alter the Probability Distribution Function (PDF) of

your indicators. In the past12 I have noted that the PDF of price and indicators do

not have a Gaussian, or Normal, probability distribution. A Gaussian PDF is the

familiar bell-shaped curve where the long “tails” mean that wide deviations from

the mean occur with relatively low probability. The Fisher Transform can be

applied to almost any normalized data set to make the resulting PDF nearly

Gaussian, with the result that the turning points are sharply peaked and easy to

identify. The Fisher Transform is defined by the equation

1)

Whereas the Fisher Transform is expansive, the Inverse Fisher Transform is

compressive. The Inverse Fisher Transform is found by solving equation 1 for x

in terms of y. The Inverse Fisher Transform is:

2)

The transfer response of the Inverse Fisher Transform is shown in Figure 1. If

the input falls between –0.5 and +0.5, the output is nearly the same as the input.

For larger absolute values (say, larger than 2), the output is compressed to be no

larger than unity. The result of using the Inverse Fisher Transform is that the

output has a very high probability of being either +1 or –1. This bipolar

probability distribution makes the Inverse Fisher Transform ideal for generating

an indicator that provides clear buy and sell signals.

Big Snapper Alerts R2.0 by JustUncleLThis is a diversified Binary Option or Scalping Alert indicator originally designed for lower Time Frame Trend or Swing trading. Although you will find it a useful tool for higher time frames as well.

The Alerts are generated by the changing direction of the ColouredMA (HullMA by default), you then have the choice of selecting the Directional filtering on these signals or a Bollinger swing reversal filter.

The filters include:

Type 1 - The three MAs (EMAs 21,55,89 by default) in various combinations or by themselves. When only one directional MA selected then direction filter is given by ColouredMA above(up)/below(down) selected MA. If more than one MA selected the direction is given by MAs being in correct order for trend direction.

Type 2 - The SuperTrend direction is used to filter ColouredMA signals.

Type 3 - Bollinger Band Outside In is used to filter ColouredMA for swing reversals.

Type 4 - No directional filtering, all signals from the ColouredMA are shown.

Notes:

Each Type can be combined with another type to form more complex filtration.

Alerts can also be disabled completely if you just want one indicator with one colouredMA and/or 3xMAs and/or Bollinger Bands and/or SuperTrend painted on the chart.

Warning:

Be aware that combining Bollinger OutsideIn swing filter and a directional filter can be counter productive as they are opposites. So careful consideration is needed when combining Bollinger OutsideIn with any of the directional filters.

Hints:

For Binary Options try ColouredMA = HullMA(13) or HullMA(8) with Type 2 or 3 Filter.

When using Trend filters SuperTrend and/or 3xMA Trend, you will find if price reverses and breaks back through the Big Fat Signal line, then this can be a good reversal trade.

Some explanation about the what Hull Moving average and ideas of how the generated in Big Snapper can be used:

tradingsim.com

forextradingstrategies4u.com

Inspiration from @vdubus

Big Snapper's Bollinger OutsideIn Swing filter in Action:

2-step Moving Average by HAH Financial- longer SMAs tend to sit too far from daily action

- shorter SMAs are too jittery

- the idea here is to create a smooth line, that is sits much closer to the daily price ranges

- this is achieved by mixing 2 MAs, a longer one and a shorter one

- the long one gives smoothness

- while averaging it with a shorter one, brings it (much in some cases) closer to the daily range

Price Action Doji Harami v0.2 by JustUncleLThis is an updated and final version of this indicator. This version distinguishes between the true Harami and the other Doji candlestick patterns as used with the Heikin Ashi candle charts. These candle patterns indicate a potential trend reversal or pullback.

The patterns identified are:

- Bearish Harami (Red Highlight above Bar):

One to three (default 3) large body Bull (green) candles followed by a small (red)

or no body candle (less than 0.5pip) with wicks top and bottom that are at least 60% of candle.

- Bullish Harami (Green Highlight below Bar):

One to three (default 3) large body Bear (red) candles followed by a small (green)

or no body candle (less than 0.5pip) with wicks top and bottom that are at least 60% of candle.

- Bearish Doji (Fuchsia Highlight above Bar):

One to three (default 3) large body Bull (green) candles followed by a small (green)

with wicks top and bottom that are at least 60% of candle.

- Bullish Doji (Aqua Highlight below Bar):

One to three (default 3) large body Bear (red) candles followed by a small (red)

with wicks top and bottom that are at least 60% of candle.

You can optionally specify how large the candles prior to Harami/Doji are in pips, default is 0 pip.

If you set this to zero then it will have no candle size consideration. You can also specify how many look back candles (1-3) are used in Harami/Doji calculations (default 3).

Included option to perform Calculations purely on Heikin Ashi candles, this helps when you want to see the HA Doji/Harami bars with the normal candle stick chart.

Also can optionally set an alert condition for when Harami/Doji found, this also displays a circle on the bottom of the screen when alert is triggered.

extended session - Regular Opening-Range- JayyOpening Range and some other scripts updated to plot correctly (see comments below.) There are three variations of the fibonacci expansion beyond the opening range and retracements within the opening range of the US Market session - I have not put in the script for the other markets yet.

The three scripts have different uses and strengths:

The extended session script (with the script here below) will plot the opening range whether you are using the extended session or the regular session. (that is to say whether "ext" in the lower right hand corner is highlighted or not.). While in the extended session the opening range has some plotting issues with periods like 13 minutes or any period that is not divisible into 330 mins with a round number outcome (eg 330/60 =5.5. Therefore an hour long opening range has problems in the extended session.

The pre session script is only for the premarket. You can select any opening range period you like. I have set the opening range to be the full premarket session. If you select a different session you will have to unselect "pre open to 9:30 EST for Opening Range?" in the format section. The script defaults to 15 minutes in the "period Of Pre Opening Range?". To go back to the 4 am to 9:30 pre opening range select "pre open to 9:30 EST for Opening Range?" there is no automatic 330 minute selection.

The past days offset script only works in 5 min or 15 minute period. It will show the opening range from up to 20 days past over the current days price action. Use this for the regular session only. 0 shows the current day's opening range. Use the positive integers for number of days back ie 1, 2, 3 etc not -1, -2, -3 etc. The script is preprogrammed to use the current day (0).

Scripts updated to plot correctly: One thing they all have in common is a way of they deal with a somewhat random problem that shifts the plots 4 hours in one direction or the other ie the plot started at 9:30 EST or 1:30PM EST. This issue started to occur approximately June 22, 2015 and impacts any script that tried to use "session" times to manage a plot in my scripts. The issue now seems to have been resolved during this past week.

Just in case the problem reoccurs I have added a "Switch session plot?" to each script. If the plot looks funny check or uncheck the "Switch session plot?" and see the difference. Of course if a new issue crops up it will likely require a different fix.

I have updated all of the scripts shown on this chart. If you are using a script of mine that suffers from the compiler issue then you will find an update on this chart. You can get any and all of the scripts by clicking on the small sideways wishbone on the left middle of the chart. You will see a dialogue box. Then click "make it mine". This will import all of the scripts to your computer and you can play around with them all to decide what you want and what you don't want. This is the easiest way to get all of the scripts in one fell swoop. It is also the easiest way for me to make all of the scripts available. I do not have all of the plots visible since it is too messy and one of the scripts (pre OR) is only for the regular session. To view the scripts click on the blue eye to the right of the script title to show it on this script. If you can only use the regular session. The scripts will all (with the exception of the pre OR) work fine.

If for any reason this script seems flakey refresh the page r try a slightly different period. I have noticed that sometimes randomly the script loves to return to the 5 min OR. This is a very new issue transient issue. As always if you see an issue please let me know.

Cheers Jayy

Camarilla - formula updated for 5 and 6 levelsSince levels 5 and 6 formulas are kind of surrounded in mystery it's difficult to find a widely agreed one.

While for the level 5 there is some consensus the 6th one is hard to find. I updated level 5 with the most common use of lvl 5 formula , some links like this one or from books (Secrets of a Pivot Boss) . Level 6 is a tough one, so please use this one experimentally . If you have other formulas for level 6, let me know. The 5 and 6 lvls are useful in volatile days.

forums.babypips.com

Grok/Claude Turtle Soup Alert SystemReplaces previous Turtle Soup Strategy/Indicator as Tradingview will not let me update it.

# 🥣 Turtle Soup Strategy (Enhanced)

## A Mean-Reversion Strategy Based on Failed Breakouts

---

## Historical Origins

### The Original Turtle Traders (1983-1988)

The Turtle Trading system is one of the most famous experiments in trading history. In 1983, legendary commodities trader **Richard Dennis** made a bet with his partner **William Eckhardt** about whether great traders were born or made. Dennis believed trading could be taught; Eckhardt believed it was innate.

To settle the debate, Dennis recruited 23 ordinary people through newspaper ads—including a professional blackjack player, a fantasy game designer, and an accountant—and taught them his trading system in just two weeks. He called them "Turtles" after turtle farms he had visited in Singapore, saying *"We are going to grow traders just like they grow turtles in Singapore."*

The results were extraordinary. Over the next five years, the Turtles reportedly earned over **$175 million in profits**. The experiment proved Dennis right: trading could indeed be taught.

#### The Original Turtle Rules:

- **Entry:** Buy when price breaks above the 20-day high (System 1) or 55-day high (System 2)

- **Exit:** Sell when price breaks below the 10-day low (System 1) or 20-day low (System 2)

- **Stop Loss:** 2x ATR (Average True Range) from entry

- **Position Sizing:** Based on volatility (ATR)

- **Philosophy:** Pure trend-following—catch big moves by riding breakouts

The Turtle system was a **trend-following** strategy that assumed breakouts would lead to sustained trends. It worked brilliantly in trending markets but suffered during choppy, range-bound conditions.

---

### The Turtle Soup Strategy (1990s)

In the 1990s, renowned trader **Linda Bradford Raschke** (along with Larry Connors) observed something interesting: many of the breakouts that the Turtle system traded actually *failed*. Price would spike above the 20-day high, trigger Turtle buy orders, then immediately reverse—trapping the breakout traders.

Raschke realized these failed breakouts were predictable and tradeable. She developed the **Turtle Soup** strategy, which does the *exact opposite* of the original Turtle system:

> *"Instead of buying the breakout, we wait for it to fail—then fade it."*

The name "Turtle Soup" is a clever play on words: the strategy essentially "eats" the Turtles by trading against them when their breakouts fail.

#### Original Turtle Soup Rules:

- **Setup:** Price makes a new 20-day high (or low)

- **Qualifier:** The previous 20-day high must be at least 3-4 days old (not a fresh breakout)

- **Entry Trigger:** Price reverses back inside the channel (failed breakout)

- **Entry:** Go SHORT (against the failed breakout above), or LONG (against the failed breakdown below)

- **Philosophy:** Mean-reversion—fade false breakouts and profit from trapped traders

#### Turtle Soup Plus One Variant:

Raschke also developed a more conservative variant called "Turtle Soup Plus One" which waits for the *next bar* after the breakout to confirm the failure before entering. This reduces false signals but may miss some opportunities.

---

## Our Enhanced Turtle Soup Strategy

We have taken the classic Turtle Soup concept and enhanced it with modern technical indicators and filters to improve signal quality and adapt to today's markets.

### Core Logic Preserved

The fundamental strategy remains true to Raschke's original concept:

| Turtle (Original) | Turtle Soup (Our Strategy) |

|-------------------|---------------------------|

| BUY breakout above 20-day high | SHORT when that breakout FAILS |

| SELL breakout below 20-day low | LONG when that breakdown FAILS |

| Trend-following | Mean-reversion |

| "The trend is your friend" | "Failed breakouts trap traders" |

---

### Enhancements & Improvements

#### 1. RSI Exhaustion Filter

**Addition:** RSI must confirm exhaustion before entry

- **For SHORT entries:** RSI > 60 (buyers exhausted)

- **For LONG entries:** RSI < 40 (sellers exhausted)

**Why:** The original Turtle Soup had no momentum filter. Adding RSI ensures we only fade breakouts when the market is showing signs of exhaustion, significantly reducing false signals. This enhancement was inspired by later traders who found RSI extremes (originally 90/10, softened to 60/40) dramatically improved win rates.

#### 2. ADX Trending Filter

**Addition:** ADX must be > 20 for trades to execute

**Why:** While the original Turtle Soup was designed for ranging markets, we found that requiring *some* trend strength (ADX > 20) actually improves results. This ensures we're trading in markets with enough directional movement to create meaningful failed breakouts, rather than random noise in dead markets.

#### 3. Heikin Ashi Smoothing

**Addition:** Optional Heikin Ashi calculations for breakout detection

**Why:** Heikin Ashi candles smooth out price noise and make trend reversals more visible. When enabled, the strategy uses HA values to detect breakouts and failures, reducing whipsaws from erratic price spikes.

#### 4. Dynamic Donchian Channels with Regime Detection

**Addition:** Color-coded channels based on market regime

- 🟢 **Green:** Bullish regime (uptrend + DI+ > DI- + OBV bullish)

- 🔴 **Red:** Bearish regime (downtrend + DI- > DI+ + OBV bearish)

- 🟡 **Yellow:** Neutral regime

**Why:** Visual regime detection helps traders understand the broader market context. The original Turtle Soup had no regime awareness—our enhancement lets traders see at a glance whether conditions favor the strategy.

#### 5. Volume Spike Detection (Optional)

**Addition:** Optional filter requiring volume surge on the breakout bar

**Why:** Failed breakouts are more significant when they occur on high volume. A volume spike on the breakout bar (default 1.2x average) indicates more traders got trapped, creating stronger reversal potential.

#### 6. ATR-Based Stops and Targets

**Addition:** Configurable ATR-based stop losses and profit targets

- **Stop Loss:** 1.5x ATR (default)

- **Profit Target:** 2.0x ATR (default)

**Why:** The original Turtle Soup used fixed stop placement. ATR-based stops adapt to current volatility, providing tighter stops in calm markets and wider stops in volatile conditions.

#### 7. Signal Cooldown

**Addition:** Minimum bars between trades (default 5)

**Why:** Prevents overtrading during choppy conditions where multiple failed breakouts might occur in quick succession.

#### 8. Real-Time Info Panel

**Addition:** Comprehensive dashboard showing:

- Current regime (Bullish/Bearish/Neutral)

- RSI value and zone

- ADX value and trending status

- Breakout status

- Bars since last high/low

- Current setup status

- Position status

**Why:** Gives traders instant visibility into all strategy conditions without needing to check multiple indicators.

---

## Entry Rules Summary

### SHORT Entry (Fading Failed Breakout Above)

1. ✅ Price breaks ABOVE the 20-period Donchian high

2. ✅ Previous 20-period high was at least 1 bar ago

3. ✅ Price closes back BELOW the Donchian high (failed breakout)

4. ✅ RSI > 60 (exhausted buyers)

5. ✅ ADX > 20 (trending market)

6. ✅ Cooldown period met

→ **Enter SHORT**, betting the breakout will fail

### LONG Entry (Fading Failed Breakdown Below)

1. ✅ Price breaks BELOW the 20-period Donchian low

2. ✅ Previous 20-period low was at least 1 bar ago

3. ✅ Price closes back ABOVE the Donchian low (failed breakdown)

4. ✅ RSI < 40 (exhausted sellers)

5. ✅ ADX > 20 (trending market)

6. ✅ Cooldown period met

→ **Enter LONG**, betting the breakdown will fail

---

## Exit Rules

1. **ATR Stop Loss:** Position closed if price moves 1.5x ATR against entry

2. **ATR Profit Target:** Position closed if price moves 2.0x ATR in favor

3. **Channel Exit:** Position closed if price breaks the exit channel in the opposite direction

4. **Mid-Channel Exit:** Position closed if price returns to channel midpoint

---

## Best Market Conditions

The Turtle Soup strategy performs best when:

- ✅ Markets are prone to false breakouts

- ✅ Volatility is moderate (not too low, not extreme)

- ✅ Price is oscillating within a broader range

- ✅ There are clear support/resistance levels

The strategy may struggle when:

- ❌ Strong trends persist (breakouts follow through)

- ❌ Volatility is extremely low (no meaningful breakouts)

- ❌ Markets are in news-driven directional moves

---

## Default Settings

| Parameter | Default | Description |

|-----------|---------|-------------|

| Lookback Period | 20 | Donchian channel period |

| Min Bars Since Extreme | 1 | Bars since last high/low |

| RSI Length | 14 | RSI calculation period |

| RSI Short Level | 60 | RSI must be above this for shorts |

| RSI Long Level | 40 | RSI must be below this for longs |

| ADX Length | 14 | ADX calculation period |

| ADX Threshold | 20 | Minimum ADX for trades |

| ATR Period | 20 | ATR calculation period |

| ATR Stop Multiplier | 1.5 | Stop loss distance in ATR |

| ATR Target Multiplier | 2.0 | Profit target distance in ATR |

| Cooldown Period | 5 | Minimum bars between trades |

| Volume Multiplier | 1.2 | Volume spike threshold |

---

## Philosophy

> *"The Turtle system made millions by following breakouts. The Turtle Soup strategy makes money when those breakouts fail. In trading, there's always someone on the other side of the trade—this strategy profits by being the smart money that fades the trapped breakout traders."*

The beauty of the Turtle Soup strategy is its elegant simplicity: it exploits a known, repeatable pattern (failed breakouts) while using modern filters (RSI, ADX) to improve timing and reduce false signals.

---

## Credits

- **Original Turtle System:** Richard Dennis & William Eckhardt (1983)

- **Turtle Soup Strategy:** Linda Bradford Raschke & Larry Connors (1990s)

- **RSI Enhancement:** Various traders who discovered RSI extremes improve reversal detection

- **This Implementation:** Enhanced with Heikin Ashi smoothing, regime detection, ADX filtering, and comprehensive visualization

---

*"We're not following the turtles—we're making soup out of them."* 🥣

MSS + Multi FVG TrackerMSS + Multi FVG Tracker

Description

An advanced institutional trading tool that combines Market Structure Shift (MSS) detection with multi-level Fair Value Gap (FVG) tracking. This indicator identifies breakouts of previous swing highs/lows on higher timeframes, then systematically tracks and validates multiple FVGs within each trend direction, generating precise entry signals when price respects the gap structure.

How It Works

Higher Timeframe Trend Detection

The indicator analyzes a higher timeframe (default 15-minute) to determine the overall bias, displaying background colors that show bullish or bearish directionality. This ensures you only trade with institutional trend direction.

Market Structure Shift (MSS/BOS)

When price closes above a previous swing high (in uptrends) or below a previous swing low (in downtrends), a BOS (Break of Structure) is marked with a line and label. This signals that the institutional structure has shifted and a new trend impulse is beginning.

Multi-Level FVG Tracking

Once an MSS occurs:

The indicator begins scanning for Fair Value Gaps (gaps between candles where no trading occurred)

Bullish FVGs: Gaps above the closing price of a bearish candle (low > high )

Bearish FVGs: Gaps below the closing price of a bullish candle (high < low )

Multiple FVGs are tracked simultaneously (up to 5 configurable) across the same impulse

Intelligent FVG Validation

Each FVG is continuously monitored:

Invalidated: If price closes through the gap (below a bullish FVG or above a bearish FVG), it's automatically deleted

Touched: If price enters the gap zone, it's marked as "touched"

Signal Generated: When a touched FVG shows strong directional confirmation (bullish candle closing above the FVG top, or bearish candle closing below the FVG bottom), a LONG or SHORT signal is triggered

Key Features

HTF Trend Confirmation: Only trades aligned with higher timeframe bias (eliminates counter-trend noise)

Multi-FVG Architecture: Tracks up to 5 gaps per trend impulse simultaneously

Automatic Gap Invalidation: Removes FVGs that break below/above, keeping only valid levels

Smart Signal Generation: Entry signals require both FVG respect + directional confirmation

Color-Coded Structure: Bullish signals in green, bearish in red with instant visual clarity

Background Trend Visualization: Subtle background shading shows HTF bias at all times

Customizable Parameters: Adjust swing period, HTF timeframe, and max FVGs to track

Ideal For

ICT Smart Money traders using FVG + MSS methodologies

Institutional order flow analysts trading market structure

Multi-timeframe traders looking for confluence-based entries

Scalpers to swing traders on 5-minute to 1-hour charts

Anyone seeking high-probability setups with clear invalidation rules

Trading Applications

Scalp FVG reversals: Enter when price respects a touched FVG with confirmation

Trade impulses with structure: Follow MSS with FVG confluence for institutional-grade entries

Identify pullback opportunities: Track multiple FVGs during retracements for re-entry zones

Confirm breakout validity: Only take breaks when aligned with HTF trend + FVG structure

Avoid false breakouts: Invalidated FVGs signal that the move is losing structure

How to Use

Wait for the MSS: Background color shift + BOS line confirms market structure break

Monitor FVG Creation: Boxes appear as gaps form within the new impulse

Watch for Invalidation: Red boxes disappear if price breaks the gap—signal invalid

Wait for Touch + Confirmation: FVG must be touched AND show strong directional candle

Take the Signal: Triangle entry markers appear with audio/visual alerts

Clear Risk Management: Use the invalidated FVG level as your stop loss

Signal Strength Indicators

Strongest Setup: Multiple FVGs created + one respects while others invalidate (shows structure)

Medium Setup: Single FVG touched and confirmed

Weaker Setup: Quick touch with weak confirmation candle (wait for better structure)

Customization Options

HTF Timeframe: Change from 15-min to 5, 30, 60 min or higher for different trading styles

Swing Period: Adjust from 10 bars for faster detection to 20+ for structural shifts

Max FVGs: Track 1-5 simultaneous gaps (lower = cleaner, higher = more opportunities)

Colors: Customize bullish/bearish colors to match your chart theme

Default Settings Optimized For

NASDAQ futures and liquid forex pairs

5-minute to 1-hour timeframe trading

Smart Money / ICT methodology

High-probability impulse + gap trading

Pro Tips

The cleaner your chart (fewer invalidated FVGs), the stronger the structural move

Multiple valid FVGs in one impulse suggest institutional accumulation/distribution

HTF background color changes are early warnings of trend structure shift

Best setups occur when 2-3 FVGs exist and one shows clear confirmation

NQUSB Sector Industry Stocks Strength

A Comprehensive Multi-Industry Performance Comparison Tool

The complete Pine Script code and supporting Python automation scripts are available on GitHub:

GitHub Repository: github.com

Original idea from by www.tradingview.com

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ WHAT'S NEW ═══

4-Level Hierarchical Navigation:

Primary: All 11 NQUSB sectors (NQUSB10, NQUSB15, NQUSB20, etc.)

Secondary (Default): Broad sectors like Technology, Energy

Tertiary: Industry groups within sectors

Quaternary: Individual stocks within industries (37 semiconductors)

Enhanced Stock Coverage:

1,176 total stocks across 129 industries

37 semiconductor stocks

Market-cap weighted selection: 60% tech / 35% others

Range: 1-37 stocks per industry

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ CORE FEATURES ═══

1. Drill-Down/Drill-Up Navigation

View NVDA at different granularity levels:

Quaternary: ● NVDA ranks #3 of 37 semiconductors

Tertiary: ✓ Semiconductors at 85% (strongest in tech hardware)

Secondary: ✓ Tech Hardware at 82% (stronger than software)

Primary: ✓ Technology at 78% (#1 sector overall)

Insight: One indicator, one stock, four perspectives - instantly see if strength is stock-specific, industry-specific, or sector-wide.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

2. Visual Current Stock Identification

Violet Markers - Instant Recognition:

● (dot) marker when current stock is in top N performers

✕ (cross) marker when current stock is below top N

Violet color (#9C27B0) on both symbol and value labels

Example: "NVDA ● ranks #3 of 37"

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

3. Rank Display in Title

Dynamic title shows performance context:

"Semiconductors (RS Rating - 3 Months) | NVDA ranks #3 of 37"

#1 = Best performer, higher number = lower rank

Total adjusts if current stock auto-added

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

4. Auto-Add Current Stock

Always Included:

Current stock automatically added if not in predefined list

Example: Viewing PRSO → "PRSO ranks #37 of 39 ✕"

Works for any stock - from NVDA to obscure small-caps

Violet markers ensure visibility even when ranked low

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ DUAL PERFORMANCE METRICS ═══

RS Rating (Relative Strength):

Normalized strength score 1-99

Compare stocks across different price ranges

Default benchmark: SPX

% Return:

Simple percentage price change

Direct performance comparison

11 Time Periods:

1 Week, 2 Weeks, 1 Month, 2 Months, 3 Months (Default) , 6 Months, 1 Year, YTD, MTD, QTD, Custom (1-500 days)

Result: 22 analytical combinations (2 metrics × 11 periods)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ USE CASES ═══

Sector Rotation Analysis:

Is NVDA's strength semiconductors-specific or tech-wide?

Drill through all 4 levels to find answer

Identify which industry groups are leading/lagging

Finding Hidden Gems:

JPM ranks #3 of 13 in Major Banks

But Financials sector weak overall (68%)

= Relative strength play in weak sector

Cross-Industry Comparison:

129 industries covered

Market-wide scan capability

Find strongest performers across all sectors

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ TECHNICAL SPECIFICATIONS ═══

V32 Stats:

Total Industries: 129

Total Stocks: 1,176

File Size: 82,032 bytes (80.1 KB)

Request Limit: 39 max (Semiconductors), 10-16 typical

Granularity Levels: 4 (Primary → Quaternary)

Smart Stock Allocation:

Technology industries: 60% coverage

Other industries: 35% coverage

Market-cap weighted selection

Formula: MIN(39, MAX(5, CEILING(total × percentage)))

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

═══ KEY ADVANTAGES ═══

vs. Single Industry Tools:

✓ 129 industries vs 1

✓ Market-wide perspective

✓ Hierarchical navigation

✓ Sector rotation detection

vs. Manual Comparison:

✓ No ETF research needed

✓ Instant visual markers

✓ Automatic ranking

✓ One-click drill-down

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

For complete documentation, Python automation scripts, and CSV data files:

github.com

Version: V32

Last Updated: 2025-11-30

Pine Script Version: v5

Grok/Claude Turtle Soup Strategy # 🥣 Turtle Soup Strategy (Enhanced)

## A Mean-Reversion Strategy Based on Failed Breakouts

---

## Historical Origins

### The Original Turtle Traders (1983-1988)

The Turtle Trading system is one of the most famous experiments in trading history. In 1983, legendary commodities trader **Richard Dennis** made a bet with his partner **William Eckhardt** about whether great traders were born or made. Dennis believed trading could be taught; Eckhardt believed it was innate.

To settle the debate, Dennis recruited 23 ordinary people through newspaper ads—including a professional blackjack player, a fantasy game designer, and an accountant—and taught them his trading system in just two weeks. He called them "Turtles" after turtle farms he had visited in Singapore, saying *"We are going to grow traders just like they grow turtles in Singapore."*

The results were extraordinary. Over the next five years, the Turtles reportedly earned over **$175 million in profits**. The experiment proved Dennis right: trading could indeed be taught.

#### The Original Turtle Rules:

- **Entry:** Buy when price breaks above the 20-day high (System 1) or 55-day high (System 2)

- **Exit:** Sell when price breaks below the 10-day low (System 1) or 20-day low (System 2)

- **Stop Loss:** 2x ATR (Average True Range) from entry

- **Position Sizing:** Based on volatility (ATR)

- **Philosophy:** Pure trend-following—catch big moves by riding breakouts

The Turtle system was a **trend-following** strategy that assumed breakouts would lead to sustained trends. It worked brilliantly in trending markets but suffered during choppy, range-bound conditions.

---

### The Turtle Soup Strategy (1990s)

In the 1990s, renowned trader **Linda Bradford Raschke** (along with Larry Connors) observed something interesting: many of the breakouts that the Turtle system traded actually *failed*. Price would spike above the 20-day high, trigger Turtle buy orders, then immediately reverse—trapping the breakout traders.

Raschke realized these failed breakouts were predictable and tradeable. She developed the **Turtle Soup** strategy, which does the *exact opposite* of the original Turtle system:

> *"Instead of buying the breakout, we wait for it to fail—then fade it."*

The name "Turtle Soup" is a clever play on words: the strategy essentially "eats" the Turtles by trading against them when their breakouts fail.

#### Original Turtle Soup Rules:

- **Setup:** Price makes a new 20-day high (or low)

- **Qualifier:** The previous 20-day high must be at least 3-4 days old (not a fresh breakout)

- **Entry Trigger:** Price reverses back inside the channel (failed breakout)

- **Entry:** Go SHORT (against the failed breakout above), or LONG (against the failed breakdown below)

- **Philosophy:** Mean-reversion—fade false breakouts and profit from trapped traders

#### Turtle Soup Plus One Variant:

Raschke also developed a more conservative variant called "Turtle Soup Plus One" which waits for the *next bar* after the breakout to confirm the failure before entering. This reduces false signals but may miss some opportunities.

---

## Our Enhanced Turtle Soup Strategy

We have taken the classic Turtle Soup concept and enhanced it with modern technical indicators and filters to improve signal quality and adapt to today's markets.

### Core Logic Preserved

The fundamental strategy remains true to Raschke's original concept:

| Turtle (Original) | Turtle Soup (Our Strategy) |

|-------------------|---------------------------|

| BUY breakout above 20-day high | SHORT when that breakout FAILS |

| SELL breakout below 20-day low | LONG when that breakdown FAILS |

| Trend-following | Mean-reversion |

| "The trend is your friend" | "Failed breakouts trap traders" |

---

### Enhancements & Improvements

#### 1. RSI Exhaustion Filter

**Addition:** RSI must confirm exhaustion before entry

- **For SHORT entries:** RSI > 60 (buyers exhausted)

- **For LONG entries:** RSI < 40 (sellers exhausted)

**Why:** The original Turtle Soup had no momentum filter. Adding RSI ensures we only fade breakouts when the market is showing signs of exhaustion, significantly reducing false signals. This enhancement was inspired by later traders who found RSI extremes (originally 90/10, softened to 60/40) dramatically improved win rates.

#### 2. ADX Trending Filter

**Addition:** ADX must be > 20 for trades to execute

**Why:** While the original Turtle Soup was designed for ranging markets, we found that requiring *some* trend strength (ADX > 20) actually improves results. This ensures we're trading in markets with enough directional movement to create meaningful failed breakouts, rather than random noise in dead markets.

#### 3. Heikin Ashi Smoothing

**Addition:** Optional Heikin Ashi calculations for breakout detection

**Why:** Heikin Ashi candles smooth out price noise and make trend reversals more visible. When enabled, the strategy uses HA values to detect breakouts and failures, reducing whipsaws from erratic price spikes.

#### 4. Dynamic Donchian Channels with Regime Detection

**Addition:** Color-coded channels based on market regime

- 🟢 **Green:** Bullish regime (uptrend + DI+ > DI- + OBV bullish)

- 🔴 **Red:** Bearish regime (downtrend + DI- > DI+ + OBV bearish)

- 🟡 **Yellow:** Neutral regime

**Why:** Visual regime detection helps traders understand the broader market context. The original Turtle Soup had no regime awareness—our enhancement lets traders see at a glance whether conditions favor the strategy.

#### 5. Volume Spike Detection (Optional)

**Addition:** Optional filter requiring volume surge on the breakout bar

**Why:** Failed breakouts are more significant when they occur on high volume. A volume spike on the breakout bar (default 1.2x average) indicates more traders got trapped, creating stronger reversal potential.

#### 6. ATR-Based Stops and Targets

**Addition:** Configurable ATR-based stop losses and profit targets

- **Stop Loss:** 1.5x ATR (default)

- **Profit Target:** 2.0x ATR (default)

**Why:** The original Turtle Soup used fixed stop placement. ATR-based stops adapt to current volatility, providing tighter stops in calm markets and wider stops in volatile conditions.

#### 7. Signal Cooldown

**Addition:** Minimum bars between trades (default 5)

**Why:** Prevents overtrading during choppy conditions where multiple failed breakouts might occur in quick succession.

#### 8. Real-Time Info Panel

**Addition:** Comprehensive dashboard showing:

- Current regime (Bullish/Bearish/Neutral)

- RSI value and zone

- ADX value and trending status

- Breakout status

- Bars since last high/low

- Current setup status

- Position status

**Why:** Gives traders instant visibility into all strategy conditions without needing to check multiple indicators.

---

## Entry Rules Summary

### SHORT Entry (Fading Failed Breakout Above)

1. ✅ Price breaks ABOVE the 20-period Donchian high

2. ✅ Previous 20-period high was at least 1 bar ago

3. ✅ Price closes back BELOW the Donchian high (failed breakout)

4. ✅ RSI > 60 (exhausted buyers)

5. ✅ ADX > 20 (trending market)

6. ✅ Cooldown period met

→ **Enter SHORT**, betting the breakout will fail

### LONG Entry (Fading Failed Breakdown Below)

1. ✅ Price breaks BELOW the 20-period Donchian low

2. ✅ Previous 20-period low was at least 1 bar ago

3. ✅ Price closes back ABOVE the Donchian low (failed breakdown)

4. ✅ RSI < 40 (exhausted sellers)

5. ✅ ADX > 20 (trending market)

6. ✅ Cooldown period met

→ **Enter LONG**, betting the breakdown will fail

---

## Exit Rules

1. **ATR Stop Loss:** Position closed if price moves 1.5x ATR against entry

2. **ATR Profit Target:** Position closed if price moves 2.0x ATR in favor

3. **Channel Exit:** Position closed if price breaks the exit channel in the opposite direction

4. **Mid-Channel Exit:** Position closed if price returns to channel midpoint

---

## Best Market Conditions

The Turtle Soup strategy performs best when:

- ✅ Markets are prone to false breakouts

- ✅ Volatility is moderate (not too low, not extreme)

- ✅ Price is oscillating within a broader range

- ✅ There are clear support/resistance levels

The strategy may struggle when:

- ❌ Strong trends persist (breakouts follow through)

- ❌ Volatility is extremely low (no meaningful breakouts)

- ❌ Markets are in news-driven directional moves

---

## Default Settings

| Parameter | Default | Description |

|-----------|---------|-------------|

| Lookback Period | 20 | Donchian channel period |

| Min Bars Since Extreme | 1 | Bars since last high/low |

| RSI Length | 14 | RSI calculation period |

| RSI Short Level | 60 | RSI must be above this for shorts |

| RSI Long Level | 40 | RSI must be below this for longs |

| ADX Length | 14 | ADX calculation period |

| ADX Threshold | 20 | Minimum ADX for trades |

| ATR Period | 20 | ATR calculation period |

| ATR Stop Multiplier | 1.5 | Stop loss distance in ATR |

| ATR Target Multiplier | 2.0 | Profit target distance in ATR |

| Cooldown Period | 5 | Minimum bars between trades |

| Volume Multiplier | 1.2 | Volume spike threshold |

---

## Philosophy

> *"The Turtle system made millions by following breakouts. The Turtle Soup strategy makes money when those breakouts fail. In trading, there's always someone on the other side of the trade—this strategy profits by being the smart money that fades the trapped breakout traders."*

The beauty of the Turtle Soup strategy is its elegant simplicity: it exploits a known, repeatable pattern (failed breakouts) while using modern filters (RSI, ADX) to improve timing and reduce false signals.

---

## Credits

- **Original Turtle System:** Richard Dennis & William Eckhardt (1983)

- **Turtle Soup Strategy:** Linda Bradford Raschke & Larry Connors (1990s)

- **RSI Enhancement:** Various traders who discovered RSI extremes improve reversal detection

- **This Implementation:** Enhanced with Heikin Ashi smoothing, regime detection, ADX filtering, and comprehensive visualization

---

*"We're not following the turtles—we're making soup out of them."* 🥣

Expected Move BandsExpected move is the amount that an asset is predicted to increase or decrease from its current price, based on the current levels of volatility.

In this model, we assume asset price follows a log-normal distribution and the log return follows a normal distribution.

Note: Normal distribution is just an assumption, it's not the real distribution of return

Settings:

"Estimation Period Selection" is for selecting the period we want to construct the prediction interval.

For "Current Bar", the interval is calculated based on the data of the previous bar close. Therefore changes in the current price will have little effect on the range. What current bar means is that the estimated range is for when this bar close. E.g., If the Timeframe on 4 hours and 1 hour has passed, the interval is for how much time this bar has left, in this case, 3 hours.

For "Future Bars", the interval is calculated based on the current close. Therefore the range will be very much affected by the change in the current price. If the current price moves up, the range will also move up, vice versa. Future Bars is estimating the range for the period at least one bar ahead.

There are also other source selections based on high low.

Time setting is used when "Future Bars" is chosen for the period. The value in time means how many bars ahead of the current bar the range is estimating. When time = 1, it means the interval is constructing for 1 bar head. E.g., If the timeframe is on 4 hours, then it's estimating the next 4 hours range no matter how much time has passed in the current bar.

Note: It's probably better to use "probability cone" for visual presentation when time > 1

Volatility Models :

Sample SD: traditional sample standard deviation, most commonly used, use (n-1) period to adjust the bias

Parkinson: Uses High/ Low to estimate volatility, assumes continuous no gap, zero mean no drift, 5 times more efficient than Close to Close

Garman Klass: Uses OHLC volatility, zero drift, no jumps, about 7 times more efficient

Yangzhang Garman Klass Extension: Added jump calculation in Garman Klass, has the same value as Garman Klass on markets with no gaps.

about 8 x efficient

Rogers: Uses OHLC, Assume non-zero mean volatility, handles drift, does not handle jump 8 x efficient

EWMA: Exponentially Weighted Volatility. Weight recently volatility more, more reactive volatility better in taking account of volatility autocorrelation and cluster.

YangZhang: Uses OHLC, combines Rogers and Garmand Klass, handles both drift and jump, 14 times efficient, alpha is the constant to weight rogers volatility to minimize variance.

Median absolute deviation: It's a more direct way of measuring volatility. It measures volatility without using Standard deviation. The MAD used here is adjusted to be an unbiased estimator.

Volatility Period is the sample size for variance estimation. A longer period makes the estimation range more stable less reactive to recent price. Distribution is more significant on a larger sample size. A short period makes the range more responsive to recent price. Might be better for high volatility clusters.

Standard deviations:

Standard Deviation One shows the estimated range where the closing price will be about 68% of the time.

Standard Deviation two shows the estimated range where the closing price will be about 95% of the time.

Standard Deviation three shows the estimated range where the closing price will be about 99.7% of the time.

Note: All these probabilities are based on the normal distribution assumption for returns. It's the estimated probability, not the actual probability.

Manually Entered Standard Deviation shows the range of any entered standard deviation. The probability of that range will be presented on the panel.

People usually assume the mean of returns to be zero. To be more accurate, we can consider the drift in price from calculating the geometric mean of returns. Drift happens in the long run, so short lookback periods are not recommended. Assuming zero mean is recommended when time is not greater than 1.

When we are estimating the future range for time > 1, we typically assume constant volatility and the returns to be independent and identically distributed. We scale the volatility in term of time to get future range. However, when there's autocorrelation in returns( when returns are not independent), the assumption fails to take account of this effect. Volatility scaled with autocorrelation is required when returns are not iid. We use an AR(1) model to scale the first-order autocorrelation to adjust the effect. Returns typically don't have significant autocorrelation. Adjustment for autocorrelation is not usually needed. A long length is recommended in Autocorrelation calculation.

Note: The significance of autocorrelation can be checked on an ACF indicator.

ACF

The multimeframe option enables people to use higher period expected move on the lower time frame. People should only use time frame higher than the current time frame for the input. An error warning will appear when input Tf is lower. The input format is multiplier * time unit. E.g. : 1D

Unit: M for months, W for Weeks, D for Days, integers with no unit for minutes (E.g. 240 = 240 minutes). S for Seconds.

Smoothing option is using a filter to smooth out the range. The filter used here is John Ehler's supersmoother. It's an advance smoothing technique that gets rid of aliasing noise. It affects is similar to a simple moving average with half the lookback length but smoother and has less lag.

Note: The range here after smooth no long represent the probability

Panel positions can be adjusted in the settings.

X position adjusts the horizontal position of the panel. Higher X moves panel to the right and lower X moves panel to the left.

Y position adjusts the vertical position of the panel. Higher Y moves panel up and lower Y moves panel down.

Step line display changes the style of the bands from line to step line. Step line is recommended because it gets rid of the directional bias of slope of expected move when displaying the bands.

Warnings:

People should not blindly trust the probability. They should be aware of the risk evolves by using the normal distribution assumption. The real return has skewness and high kurtosis. While skewness is not very significant, the high kurtosis should be noticed. The Real returns have much fatter tails than the normal distribution, which also makes the peak higher. This property makes the tail ranges such as range more than 2SD highly underestimate the actual range and the body such as 1 SD slightly overestimate the actual range. For ranges more than 2SD, people shouldn't trust them. They should beware of extreme events in the tails.

Different volatility models provide different properties if people are interested in the accuracy and the fit of expected move, they can try expected move occurrence indicator. (The result also demonstrate the previous point about the drawback of using normal distribution assumption).

Expected move Occurrence Test

The prediction interval is only for the closing price, not wicks. It only estimates the probability of the price closing at this level, not in between. E.g., If 1 SD range is 100 - 200, the price can go to 80 or 230 intrabar, but if the bar close within 100 - 200 in the end. It's still considered a 68% one standard deviation move.

️Omega RatioThe Omega Ratio is a risk-return performance measure of an investment asset, portfolio, or strategy. It is defined as the probability-weighted ratio, of gains versus losses for some threshold return target. The ratio is an alternative for the widely used Sharpe ratio and is based on information the Sharpe ratio discards.

█ OVERVIEW

As we have mentioned many times, stock market returns are usually not normally distributed. Therefore the models that assume a normal distribution of returns may provide us with misleading information. The Omega Ratio improves upon the common normality assumption among other risk-return ratios by taking into account the distribution as a whole.

█ CONCEPTS

Two distributions with the same mean and variance, would according to the most commonly used Sharpe Ratio suggest that the underlying assets of the distribution offer the same risk-return ratio. But as we have mentioned in our Moments indicator, variance and standard deviation are not a sufficient measure of risk in the stock market since other shape features of a distribution like skewness and excess kurtosis come into play. Omega Ratio tackles this problem by employing all four Moments of the distribution and therefore taking into account the differences in the shape features of the distributions. Another important feature of the Omega Ratio is that it does not require any estimation but is rather calculated directly from the observed data. This gives it an advantage over standard statistical estimators that require estimation of parameters and are therefore sampling uncertainty in its calculations.

█ WAYS TO USE THIS INDICATOR

Omega calculates a probability-adjusted ratio of gains to losses, relative to the Minimum Acceptable Return (MAR). This means that at a given MAR using the simple rule of preferring more to less, an asset with a higher value of Omega is preferable to one with a lower value. The indicator displays the values of Omega at increasing levels of MARs and creating the so-called Omega Curve. Knowing this one can compare Omega Curves of different assets and decide which is preferable given the MAR of your strategy. The indicator plots two Omega Curves. One for the on chart symbol and another for the off chart symbol that u can use for comparison.

When comparing curves of different assets make sure their trading days are the same in order to ensure the same period for the Omega calculations. Value interpretation: Omega<1 will indicate that the risk outweighs the reward and therefore there are more excess negative returns than positive. Omega>1 will indicate that the reward outweighs the risk and that there are more excess positive returns than negative. Omega=1 will indicate that the minimum acceptable return equals the mean return of an asset. And that the probability of gain is equal to the probability of loss.

█ FEATURES

• "Low-Risk security" lets you select the security that you want to use as a benchmark for Omega calculations.

• "Omega Period" is the size of the sample that is used for the calculations.

• “Increments” is the number of Minimal Acceptable Return levels the calculation is carried on. • “Other Symbol” lets you select the source of the second curve.