MTF Intraday v2.0📊 Description

MTF Intraday v2.0 is an informative indicator for analyzing trend strength across multiple timeframes simultaneously. Designed specifically for intraday (session) trading during European and US market hours.

The indicator shows the real market picture without lagging signals - you see the trend strength right now for each timeframe.

🎯 Key Features

1. Multi-Timeframe Analysis (D1, H4, H1, M30, M15)

Analyzes 4 indicators on each TF: SuperTrend, RSI, EMA crossover, EMA200

Shows strength for each timeframe: STRONG / MED / WEAK

Color indication: 🟢 green (LONG strong), 🔴 red (SHORT strong), 🟡 yellow (medium), ⚪ gray (weak)

2. Intraday Trading Hierarchy

D1 - global context (affects quality assessment)

H4 - general (sets the main trend)

H1 - reference point for intraday

M30/M15 - finding entry points during sessions

3. Market Pulse

🔥 HOT - when both H4 and H1 are STRONG (best time to enter!)

✓ GOOD - when H4 or H1 is STRONG

L:45 S:20 - balance of power between LONG and SHORT (statistics instead of "wait")

4. Volume Indicator (24 hours)

Shows volume change over the last 24 hours

SPIKE! - when volume increased by the set % (default 50%)

Considers candle color: 🟢 LONG spike (rise + green candle), 🔴 SHORT spike (rise + red candle)

Works on any timeframe (automatically recalculates)

5. Compact Mode

OFF - shows all details: every indicator for each TF

ON - only strength per timeframe (for clean chart)

⚙️ Settings

Main:

SuperTrend Period (21) / Multiplier (6.3)

RSI Length (14)

EMA Short (50) / Long (100) / 200

Compact Mode - hide detailed indicators

Volume:

Show Volume - show/hide volume indicator

Volume Alerts ON/OFF - enable/disable volume alerts

Volume Spike (%) - spike threshold (30% / 50% / 100%)

🔔 Alerts

The indicator has 5 types of alerts:

Market HOT - H4 and H1 simultaneously became STRONG

VOL LONG - volume spike on bullish candle

VOL SHORT - volume spike on bearish candle

EMA200 UP - price crossed EMA200 upward

EMA200 DN - price crossed EMA200 downward

Set up in TradingView: Create Alert → Select desired alert from the list

📈 How to Use

For finding entry points:

Check H4 - should be at least MED (better STRONG)

Verify H1 - main filter for intraday

Wait for pulse "🔥 HOT" or at least "✓ GOOD"

Look at M30/M15 - seek confirmation

Check 24h VOL - if SPIKE, momentum has started

Quality Assessment:

EXCELLENT ⭐ - all stars aligned (D1 with us, high score)

GOOD - good setup

WARNING ⚠️ - D1 against trend (counter-trend, be careful!)

Color Indication:

🟢 Green cells - bullish signal

🔴 Red cells - bearish signal

🟡 Yellow cells - neutral/waiting

🟠 Orange TF labels - for readability

⚠️ Important

This is an informative indicator, not a trading system

Does not give "entry/exit" signals - shows trend strength in the moment

Use together with Price Action and your trading strategy

RSI on M15 is displayed but not counted (too much noise)

💡 Who is it for

✅ Intraday traders (Europe/US sessions)

✅ Scalpers on crypto and forex

✅ Swing traders for trend confirmation

✅ Those who trade on multiple timeframes simultaneously

Поиск скриптов по запросу "sessions"

Friday & Monday HighlighterFriday & Monday Institutional Range Marker — Know Where Big Firms Set the Trap!

🧠 Description

This indicator automatically highlights Friday and Monday sessions on your chart — days when institutional players and algorithmic firms (like Citadel, Jane Street, or Tower Research) quietly shape the upcoming week’s price structure.

🔍 Why Friday & Monday matter

Friday : Large institutions often book profits or hedge into the weekend. Their final-hour moves reveal the next week’s bias.

Monday : Big players rebuild positions, absorbing liquidity left behind by retail traders.

Together, these two days define the range traps and breakout zones that often control price action until midweek.

> In short, the Friday–Monday high and low often act as invisible walls — guiding scalpers, option sellers, and swing traders alike.

🧩 What this tool does

✅ Highlights Friday (red) and Monday (green) sessions

✅ Adds optional day labels above bars

✅ Works across all timeframes (best on 15min to 1hr charts)

✅ Helps you visually identify where institutions likely built their positions

Use it to quickly spot:

* Range boundaries that trap traders

* Gap zones likely to get filled

* High–low sweeps before reversals

⚙️ Recommended Use

1. Mark Friday’s high–low → Watch for liquidity sweeps on Monday.

2. When Monday holds above Friday’s high , breakout continuation is likely.

3. When Monday fails below Friday’s low , expect a reversal or trap.

4. Combine this with OI shifts, IV crush, and FII–DII flow data for confirmation.

⚠️ Disclaimer

This indicator is for **educational and analytical purposes only**.

It does **not constitute financial advice** or a trading signal.

Markets are dynamic — always perform your own research before trading or investing.

Luxy Momentum, Trend, Bias and Breakout Indicators V7

TABLE OF CONTENTS

This is Version 7 (V7) - the latest and most optimized release. If you are using any older versions (V6, V5, V4, V3, etc.), it is highly recommended to replace them with V7.

Why This Indicator is Different

Who Should Use This

Core Components Overview

The UT Bot Trading System

Understanding the Market Bias Table

Candlestick Pattern Recognition

Visual Tools and Features

How to Use the Indicator

Performance and Optimization

FAQ

---

### CREDITS & ATTRIBUTION

This indicator implements proven trading concepts using entirely original code developed specifically for this project.

### CONCEPTUAL FOUNDATIONS

• UT Bot ATR Trailing System

- Original concept by @QuantNomad: (search "UT-Bot-Strategy"

- Our version is a complete reimplementation with significant enhancements:

- Volume-weighted momentum adjustment

- Composite stop loss from multiple S/R layers

- Multi-filter confirmation system (swing, %, 2-bar, ZLSMA)

- Full integration with multi-timeframe bias table

- Visual audit trail with freeze-on-touch

- NOTE: No code was copied - this is a complete reimplementation with enhancements.

• Standard Technical Indicators (Public Domain Formulas):

- Supertrend: ATR-based trend calculation with custom gradient fills

- MACD: Gerald Appel's formula with separation filters

- RSI: J. Welles Wilder's formula with pullback zone logic

- ADX/DMI: Custom trend strength formula inspired by Wilder's directional movement concept, reimplemented with volume weighting and efficiency metrics

- ZLSMA: Zero-lag formula enhanced with Hull MA and momentum prediction

### Custom Implementations

- Trend Strength: Inspired by Wilder's ADX concept but using volume-weighted pressure calculation and efficiency metrics (not traditional +DI/-DI smoothing)

- All code implementations are original

### ORIGINAL FEATURES (70%+ of codebase)

- Multi-Timeframe Bias Table with live updates

- Risk Management System (R-multiple TPs, freeze-on-touch)

- Opening Range Breakout tracker with session management

- Composite Stop Loss calculator using 6+ S/R layers

- Performance optimization system (caching, conditional calcs)

- VIX Fear Index integration

- Previous Day High/Low auto-detection

- Candlestick pattern recognition with interactive tooltips

- Smart label and visual management

- All UI/UX design and table architecture

### DEVELOPMENT PROCESS

**AI Assistance:** This indicator was developed over 2+ months with AI assistance (ChatGPT/Claude) used for:

- Writing Pine Script code based on design specifications

- Optimizing performance and fixing bugs

- Ensuring Pine Script v6 compliance

- Generating documentation

**Author's Role:** All trading concepts, system design, feature selection, integration logic, and strategic decisions are original work by the author. The AI was a coding tool, not the system designer.

**Transparency:** We believe in full disclosure - this project demonstrates how AI can be used as a powerful development tool while maintaining creative and strategic ownership.

---

1. WHY THIS INDICATOR IS DIFFERENT

Most traders use multiple separate indicators on their charts, leading to cluttered screens, conflicting signals, and analysis paralysis. The Suite solves this by integrating proven technical tools into a single, cohesive system.

Key Advantages:

All-in-One Design: Instead of loading 5-10 separate indicators, you get everything in one optimized script. This reduces chart clutter and improves TradingView performance.

Multi-Timeframe Bias Table: Unlike standard indicators that only show the current timeframe, the Bias Table aggregates trend signals across multiple timeframes simultaneously. See at a glance whether 1m, 5m, 15m, 1h are aligned bullish or bearish - no more switching between charts.

Smart Confirmations: The indicator doesn't just give signals - it shows you WHY. Every entry has multiple layers of confirmation (MA cross, MACD momentum, ADX strength, RSI pullback, volume, etc.) that you can toggle on/off.

Dynamic Stop Loss System: Instead of static ATR stops, the SL is calculated from multiple support/resistance layers: UT trailing line, Supertrend, VWAP, swing structure, and MA levels. This creates more intelligent, price-action-aware stops.

R-Multiple Take Profits: Built-in TP system calculates targets based on your initial risk (1R, 1.5R, 2R, 3R). Lines freeze when touched with visual checkmarks, giving you a clean audit trail of partial exits.

Educational Tooltips Everywhere: Every single input has detailed tooltips explaining what it does, typical values, and how it impacts trading. You're not guessing - you're learning as you configure.

Performance Optimized: Smart caching, conditional calculations, and modular design mean the indicator runs fast despite having 15+ features. Turn off what you don't use for even better performance.

No Repainting: All signals respect bar close. Alerts fire correctly. What you see in history is what you would have gotten in real-time.

What Makes It Unique:

Integrated UT Bot + Bias Table: No other indicator combines UT Bot's ATR trailing system with a live multi-timeframe dashboard. You get precision entries with macro trend context.

Candlestick Pattern Recognition with Interactive Tooltips: Patterns aren't just marked - hover over any emoji for a full explanation of what the pattern means and how to trade it.

Opening Range Breakout Tracker: Built-in ORB system for intraday traders with customizable session times and real-time status updates in the Bias Table.

Previous Day High/Low Auto-Detection: Automatically plots PDH/PDL on intraday charts with theme-aware colors. Updates daily without manual input.

Dynamic Row Labels in Bias Table: The table shows your actual settings (e.g., "EMA 10 > SMA 20") not generic labels. You know exactly what's being evaluated.

Modular Filter System: Instead of forcing a fixed methodology, the indicator lets you build your own strategy. Start with just UT Bot, add filters one at a time, test what works for your style.

---

2. WHO WHOULD USE THIS

Designed For:

Intermediate to Advanced Traders: You understand basic technical analysis (MAs, RSI, MACD) and want to combine multiple confirmations efficiently. This isn't a "one-click profit" system - it's a professional toolkit.

Multi-Timeframe Traders: If you trade one asset but check multiple timeframes for confirmation (e.g., enter on 5m after checking 15m and 1h alignment), the Bias Table will save you hours every week.

Trend Followers: The indicator excels at identifying and following trends using UT Bot, Supertrend, and MA systems. If you trade breakouts and pullbacks in trending markets, this is built for you.

Intraday and Swing Traders: Works equally well on 5m-1h charts (day trading) and 4h-D charts (swing trading). Scalpers can use it too with appropriate settings adjustments.

Discretionary Traders: This isn't a black-box system. You see all the components, understand the logic, and make final decisions. Perfect for traders who want tools, not automation.

Works Across All Markets:

Stocks (US, international)

Cryptocurrency (24/7 markets supported)

Forex pairs

Indices (SPY, QQQ, etc.)

Commodities

NOT Ideal For :

Complete Beginners: If you don't know what a moving average or RSI is, start with basics first. This indicator assumes foundational knowledge.

Algo Traders Seeking Black Box: This is discretionary. Signals require context and confirmation. Not suitable for blind automated execution.

Mean-Reversion Only Traders: The indicator is trend-following at its core. While VWAP bands support mean-reversion, the primary methodology is trend continuation.

---

3. CORE COMPONENTS OVERVIEW

The indicator combines these proven systems:

Trend Analysis:

Moving Averages: Four customizable MAs (Fast, Medium, Medium-Long, Long) with six types to choose from (EMA, SMA, WMA, VWMA, RMA, HMA). Mix and match for your style.

Supertrend: ATR-based trend indicator with unique gradient fill showing trend strength. One-sided ribbon visualization makes it easier to see momentum building or fading.

ZLSMA : Zero-lag linear-regression smoothed moving average. Reduces lag compared to traditional MAs while maintaining smooth curves.

Momentum & Filters:

MACD: Standard MACD with separation filter to avoid weak crossovers.

RSI: Pullback zone detection - only enter longs when RSI is in your defined "buy zone" and shorts in "sell zone".

ADX/DMI: Trend strength measurement with directional filter. Ensures you only trade when there's actual momentum.

Volume Filter: Relative volume confirmation - require above-average volume for entries.

Donchian Breakout: Optional channel breakout requirement.

Signal Systems:

UT Bot: The primary signal generator. ATR trailing stop that adapts to volatility and gives clear entry/exit points.

Base Signals: MA cross system with all the above filters applied. More conservative than UT Bot alone.

Market Bias Table: Multi-timeframe dashboard showing trend alignment across 7 timeframes plus macro bias (3-day, weekly, monthly, quarterly, VIX).

Candlestick Patterns: Six major reversal patterns auto-detected with interactive tooltips.

ORB Tracker: Opening range high/low with breakout status (intraday only).

PDH/PDL: Previous day levels plotted automatically on intraday charts.

VWAP + Bands : Session-anchored VWAP with up to three standard deviation band pairs.

---

4. THE UT BOT TRADING SYSTEM

The UT Bot is the heart of the indicator's signal generation. It's an advanced ATR trailing stop that adapts to market volatility.

Why UT Bot is Superior to Fixed Stops:

Traditional ATR stops use a fixed multiplier (e.g., "stop = entry - 2×ATR"). UT Bot is smarter:

It TRAILS the stop as price moves in your favor

It WIDENS during high volatility to avoid premature stops

It TIGHTENS during consolidation to lock in profits

It FLIPS when price breaks the trailing line, signaling reversals

Visual Elements You'll See:

Orange Trailing Line: The actual UT stop level that adapts bar-by-bar

Buy/Sell Labels: Aqua triangle (long) or orange triangle (short) when the line flips

ENTRY Line: Horizontal line at your entry price (optional, can be turned off)

Suggested Stop Loss: A composite SL calculated from multiple support/resistance layers:

- UT trailing line

- Supertrend level

- VWAP

- Swing structure (recent lows/highs)

- Long-term MA (200)

- ATR-based floor

Take Profit Lines: TP1, TP1.5, TP2, TP3 based on R-multiples. When price touches a TP, it's marked with a checkmark and the line freezes for audit trail purposes.

Status Messages: "SL Touched ❌" or "SL Frozen" when the trade leg completes.

How UT Bot Differs from Other ATR Systems:

Multiple Filters Available: You can require 2-bar confirmation, minimum % price change, swing structure alignment, or ZLSMA directional filter. Most UT implementations have none of these.

Smart SL Calculation: Instead of just using the UT line as your stop, the indicator suggests a better SL based on actual support/resistance. This prevents getting stopped out by wicks while keeping risk controlled.

Visual Audit Trail: All SL/TP lines freeze when touched with clear markers. You can review your trades weeks later and see exactly where entries, stops, and targets were.

Performance Options: "Draw UT visuals only on bar close" lets you reduce rendering load without affecting logic or alerts - critical for slower machines or 1m charts.

Trading Logic:

UT Bot flips direction (Buy or Sell signal appears)

Check Bias Table for multi-timeframe confirmation

Optional: Wait for Base signal or candlestick pattern

Enter at signal bar close or next bar open

Place stop at "Suggested Stop Loss" line

Scale out at TP levels (TP1, TP2, TP3)

Exit remaining position on opposite UT signal or stop hit

---

5. UNDERSTANDING THE MARKET BIAS TABLE

This is the indicator's unique multi-timeframe intelligence layer. Instead of looking at one chart at a time, the table aggregates signals across seven timeframes plus macro trend bias.

Why Multi-Timeframe Analysis Matters:

Professional traders check higher and lower timeframes for context:

Is the 1h uptrend aligning with my 5m entry?

Are all short-term timeframes bullish or just one?

Is the daily trend supportive or fighting me?

Doing this manually means opening multiple charts, checking each indicator, and making mental notes. The Bias Table does it automatically in one glance.

Table Structure:

Header Row:

On intraday charts: 1m, 5m, 15m, 30m, 1h, 2h, 4h (toggle which ones you want)

On daily+ charts: D, W, M (automatic)

Green dot next to title = live updating

Headline Rows - Macro Bias:

These show broad market direction over longer periods:

3 Day Bias: Trend over last 3 trading sessions (uses 1h data)

Weekly Bias: Trend over last 5 trading sessions (uses 4h data)

Monthly Bias: Trend over last 30 daily bars

Quarterly Bias: Trend over last 13 weekly bars

VIX Fear Index: Market regime based on VIX level - bullish when low, bearish when high

Opening Range Breakout: Status of price vs. session open range (intraday only)

These rows show text: "BULLISH", "BEARISH", or "NEUTRAL"

Indicator Rows - Technical Signals:

These evaluate your configured indicators across all active timeframes:

Fast MA > Medium MA (shows your actual MA settings, e.g., "EMA 10 > SMA 20")

Price > Long MA (e.g., "Price > SMA 200")

Price > VWAP

MACD > Signal

Supertrend (up/down/neutral)

ZLSMA Rising

RSI In Zone

ADX ≥ Minimum

These rows show emojis: GREEB (bullish), RED (bearish), GRAY/YELLOW (neutral/NA)

AVG Column:

Shows percentage of active timeframes that are bullish for that row. This is the KEY metric:

AVG > 70% = strong multi-timeframe bullish alignment

AVG 40-60% = mixed/choppy, no clear trend

AVG < 30% = strong multi-timeframe bearish alignment

How to Use the Table:

For a long trade:

Check AVG column - want to see > 60% ideally

Check headline bias rows - want to see BULLISH, not BEARISH

Check VIX row - bullish market regime preferred

Check ORB row (intraday) - want ABOVE for longs

Scan indicator rows - more green = better confirmation

For a short trade:

Check AVG column - want to see < 40% ideally

Check headline bias rows - want to see BEARISH, not BULLISH

Check VIX row - bearish market regime preferred

Check ORB row (intraday) - want BELOW for shorts

Scan indicator rows - more red = better confirmation

When AVG is 40-60%:

Market is choppy, mixed signals. Either stay out or reduce position size significantly. These are low-probability environments.

Unique Features:

Dynamic Labels: Row names show your actual settings (e.g., "EMA 10 > SMA 20" not generic "Fast > Slow"). You know exactly what's being evaluated.

Customizable Rows: Turn off rows you don't care about. Only show what matters to your strategy.

Customizable Timeframes: On intraday charts, disable 1m or 4h if you don't trade them. Reduces calculation load by 20-40%.

Automatic HTF Handling: On Daily/Weekly/Monthly charts, the table automatically switches to D/W/M columns. No configuration needed.

Performance Smart: "Hide BIAS table on 1D or above" option completely skips all table calculations on higher timeframes if you only trade intraday.

---

6. CANDLESTICK PATTERN RECOGNITION

The indicator automatically detects six major reversal patterns and marks them with emojis at the relevant bars.

Why These Six Patterns:

These are the most statistically significant reversal patterns according to trading literature:

High win rate when appearing at support/resistance

Clear visual structure (not subjective)

Work across all timeframes and assets

Studied extensively by institutions

The Patterns:

Bullish Patterns (appear at bottoms):

Bullish Engulfing: Green candle completely engulfs prior red candle's body. Strong reversal signal.

Hammer: Small body with long lower wick (at least 2× body size). Shows rejection of lower prices by buyers.

Morning Star: Three-candle pattern (large red → small indecision → large green). Very strong bottom reversal.

Bearish Patterns (appear at tops):

Bearish Engulfing: Red candle completely engulfs prior green candle's body. Strong reversal signal.

Shooting Star: Small body with long upper wick (at least 2× body size). Shows rejection of higher prices by sellers.

Evening Star: Three-candle pattern (large green → small indecision → large red). Very strong top reversal.

Interactive Tooltips:

Unlike most pattern indicators that just draw shapes, this one is educational:

Hover your mouse over any pattern emoji

A tooltip appears explaining: what the pattern is, what it means, when it's most reliable, and how to trade it

No need to memorize - learn as you trade

Noise Filter:

"Min candle body % to filter noise" setting prevents false signals:

Patterns require minimum body size relative to price

Filters out tiny candles that don't represent real buying/selling pressure

Adjust based on asset volatility (higher % for crypto, lower for low-volatility stocks)

How to Trade Patterns:

Patterns are NOT standalone entry signals. Use them as:

Confirmation: UT Bot gives signal + pattern appears = stronger entry

Reversal Warning: In a trade, opposite pattern appears = consider tightening stop or taking profit

Support/Resistance Validation: Pattern at key level (PDH, VWAP, MA 200) = level is being respected

Best combined with:

UT Bot or Base signal in same direction

Bias Table alignment (AVG > 60% or < 40%)

Appearance at obvious support/resistance

---

7. VISUAL TOOLS AND FEATURES

VWAP (Volume Weighted Average Price):

Session-anchored VWAP with standard deviation bands. Shows institutional "fair value" for the trading session.

Anchor Options: Session, Day, Week, Month, Quarter, Year. Choose based on your trading timeframe.

Bands: Up to three pairs (X1, X2, X3) showing statistical deviation. Price at outer bands often reverses.

Auto-Hide on HTF: VWAP hides on Daily/Weekly/Monthly charts automatically unless you enable anchored mode.

Use VWAP as:

Directional bias (above = bullish, below = bearish)

Mean reversion levels (outer bands)

Support/resistance (the VWAP line itself)

Previous Day High/Low:

Automatically plots yesterday's high and low on intraday charts:

Updates at start of each new trading day

Theme-aware colors (dark text for light charts, light text for dark charts)

Hidden automatically on Daily/Weekly/Monthly charts

These levels are critical for intraday traders - institutions watch them closely as support/resistance.

Opening Range Breakout (ORB):

Tracks the high/low of the first 5, 15, 30, or 60 minutes of the trading session:

Customizable session times (preset for NYSE, LSE, TSE, or custom)

Shows current breakout status in Bias Table row (ABOVE, BELOW, INSIDE, BUILDING)

Intraday only - auto-disabled on Daily+ charts

ORB is a classic day trading strategy - breakout above opening range often leads to continuation.

Extra Labels:

Change from Open %: Shows how far price has moved from session open (intraday) or daily open (HTF). Green if positive, red if negative.

ADX Badge: Small label at bottom of last bar showing current ADX value. Green when above your minimum threshold, red when below.

RSI Badge: Small label at top of last bar showing current RSI value with zone status (buy zone, sell zone, or neutral).

These labels provide quick at-a-glance confirmation without needing separate indicator windows.

---

8. HOW TO USE THE INDICATOR

Step 1: Add to Chart

Load the indicator on your chosen asset and timeframe

First time: Everything is enabled by default - the chart will look busy

Don't panic - you'll turn off what you don't need

Step 2: Start Simple

Turn OFF everything except:

UT Bot labels (keep these ON)

Bias Table (keep this ON)

Moving Averages (Fast and Medium only)

Suggested Stop Loss and Take Profits

Hide everything else initially. Get comfortable with the basic UT Bot + Bias Table workflow first.

Step 3: Learn the Core Workflow

UT Bot gives a Buy or Sell signal

Check Bias Table AVG column - do you have multi-timeframe alignment?

If yes, enter the trade

Place stop at Suggested Stop Loss line

Scale out at TP levels

Exit on opposite UT signal

Trade this simple system for a week. Get a feel for signal frequency and win rate with your settings.

Step 4: Add Filters Gradually

If you're getting too many losing signals (whipsaws in choppy markets), add filters one at a time:

Try: "Require 2-Bar Trend Confirmation" - wait for 2 bars to confirm direction

Try: ADX filter with minimum threshold - only trade when trend strength is sufficient

Try: RSI pullback filter - only enter on pullbacks, not chasing

Try: Volume filter - require above-average volume

Add one filter, test for a week, evaluate. Repeat.

Step 5: Enable Advanced Features (Optional)

Once you're profitable with the core system, add:

Supertrend for additional trend confirmation

Candlestick patterns for reversal warnings

VWAP for institutional anchor reference

ORB for intraday breakout context

ZLSMA for low-lag trend following

Step 6: Optimize Settings

Every setting has a detailed tooltip explaining what it does and typical values. Hover over any input to read:

What the parameter controls

How it impacts trading

Suggested ranges for scalping, day trading, and swing trading

Start with defaults, then adjust based on your results and style.

Step 7: Set Up Alerts

Right-click chart → Add Alert → Condition: "Luxy Momentum v6" → Choose:

"UT Bot — Buy" for long entries

"UT Bot — Sell" for short entries

"Base Long/Short" for filtered MA cross signals

Optionally enable "Send real-time alert() on UT flip" in settings for immediate notifications.

Common Workflow Variations:

Conservative Trader:

UT signal + Base signal + Candlestick pattern + Bias AVG > 70%

Enter only at major support/resistance

Wider UT sensitivity, multiple filters

Aggressive Trader:

UT signal + Bias AVG > 60%

Enter immediately, no waiting

Tighter UT sensitivity, minimal filters

Swing Trader:

Focus on Daily/Weekly Bias alignment

Ignore intraday noise

Use ORB and PDH/PDL less (or not at all)

Wider stops, patient approach

---

9. PERFORMANCE AND OPTIMIZATION

The indicator is optimized for speed, but with 15+ features running simultaneously, chart load time can add up. Here's how to keep it fast:

Biggest Performance Gains:

Disable Unused Timeframes: In "Time Frames" settings, turn OFF any timeframe you don't actively trade. Each disabled TF saves 10-15% calculation time. If you only day trade 5m, 15m, 1h, disable 1m, 2h, 4h.

Hide Bias Table on Daily+: If you only trade intraday, enable "Hide BIAS table on 1D or above". This skips ALL table calculations on higher timeframes.

Draw UT Visuals Only on Bar Close: Reduces intrabar rendering of SL/TP/Entry lines. Has ZERO impact on logic or alerts - purely visual optimization.

Additional Optimizations:

Turn off VWAP bands if you don't use them

Disable candlestick patterns if you don't trade them

Turn off Supertrend fill if you find it distracting (keep the line)

Reduce "Limit to 10 bars" for SL/TP lines to minimize line objects

Performance Features Built-In:

Smart Caching: Higher timeframe data (3-day bias, weekly bias, etc.) updates once per day, not every bar

Conditional Calculations: Volume filter only calculates when enabled. Swing filter only runs when enabled. Nothing computes if turned off.

Modular Design: Every component is independent. Turn off what you don't need without breaking other features.

Typical Load Times:

5m chart, all features ON, 7 timeframes: ~2-3 seconds

5m chart, core features only, 3 timeframes: ~1 second

1m chart, all features: ~4-5 seconds (many bars to calculate)

If loading takes longer, you likely have too many indicators on the chart total (not just this one).

---

10. FAQ

Q: How is this different from standard UT Bot indicators?

A: Standard UT Bot (originally by @QuantNomad) is just the ATR trailing line and flip signals. This implementation adds:

- Volume weighting and momentum adjustment to the trailing calculation

- Multiple confirmation filters (swing, %, 2-bar, ZLSMA)

- Smart composite stop loss system from multiple S/R layers

- R-multiple take profit system with freeze-on-touch

- Integration with multi-timeframe Bias Table

- Visual audit trail with checkmarks

Q: Can I use this for automated trading?

A: The indicator is designed for discretionary trading. While it has clear signals and alerts, it's not a mechanical system. Context and judgment are required.

Q: Does it repaint?

A: No. All signals respect bar close. UT Bot logic runs intrabar but signals only trigger on confirmed bars. Alerts fire correctly with no lookahead.

Q: Do I need to use all the features?

A: Absolutely not. The indicator is modular. Many profitable traders use just UT Bot + Bias Table + Moving Averages. Start simple, add complexity only if needed.

Q: How do I know which settings to use?

A: Every single input has a detailed tooltip. Hover over any setting to see:

What it does

How it affects trading

Typical values for scalping, day trading, swing trading

Start with defaults, adjust gradually based on results.

Q: Can I use this on crypto 24/7 markets?

A: Yes. ORB will not work (no defined session), but everything else functions normally. Use "Day" anchor for VWAP instead of "Session".

Q: The Bias Table is blank or not showing.

A: Check:

"Show Table" is ON

Table position isn't overlapping another indicator's table (change position)

At least one row is enabled

"Hide BIAS table on 1D or above" is OFF (if on Daily+ chart)

Q: Why are candlestick patterns not appearing?

A: Patterns are relatively rare by design - they only appear at genuine reversal points. Check:

Pattern toggles are ON

"Min candle body %" isn't too high (try 0.05-0.10)

You're looking at a chart with actual reversals (not strong trending market)

Q: UT Bot is too sensitive/not sensitive enough.

A: Adjust "Sensitivity (Key×ATR)". Lower number = tighter stop, more signals. Higher number = wider stop, fewer signals. Read the tooltip for guidance.

Q: Can I get alerts for the Bias Table?

A: The Bias Table is a dashboard for visual analysis, not a signal generator. Set alerts on UT Bot or Base signals, then manually check Bias Table for confirmation.

Q: Does this work on stocks with low volume?

A: Yes, but turn OFF the volume filter. Low volume stocks will never meet relative volume requirements.

Q: How often should I check the Bias Table?

A: Before every entry. It takes 2 seconds to glance at the AVG column and headline rows. This one check can save you from fighting the trend.

Q: What if UT signal and Base signal disagree?

A: UT Bot is more aggressive (ATR trailing). Base signals are more conservative (MA cross + filters). If they disagree, either:

Wait for both to align (safest)

Take the UT signal but with smaller size (aggressive)

Skip the trade (conservative)

There's no "right" answer - depends on your risk tolerance.

---

FINAL NOTES

The indicator gives you an edge. How you use that edge determines results.

For questions, feedback, or support, comment on the indicator page or message the author.

Happy Trading!

ICT Essentials [LDT]ICT Essentials

Overview

ICT Essentials is an all-in-one trading utility built to create a natural and efficient workflow for ICT-based traders.

Every component has been designed to integrate seamlessly and update dynamically across timeframes.

The indicator focuses on clarity, performance and customization, allowing traders to tailor every part of their trading experience.

Equal Highs & Lows

This feature automatically detects and marks Equal Highs (EQH) and Equal Lows (EQL) with full control over visuals and behavior.

Users can customize line colors, widths, and styles, label size, color, background transparency and text offset.

The logic uses an optimized scanning and caching system that maintains smooth performance even on higher timeframes.

It provides a precise and adaptive way to identify structural liquidity points whilst keeping the chart clean and readable.

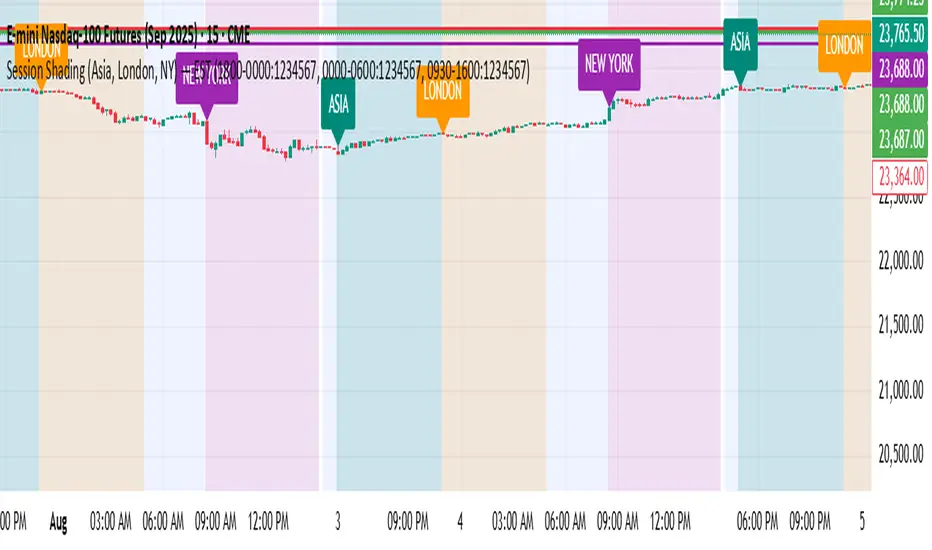

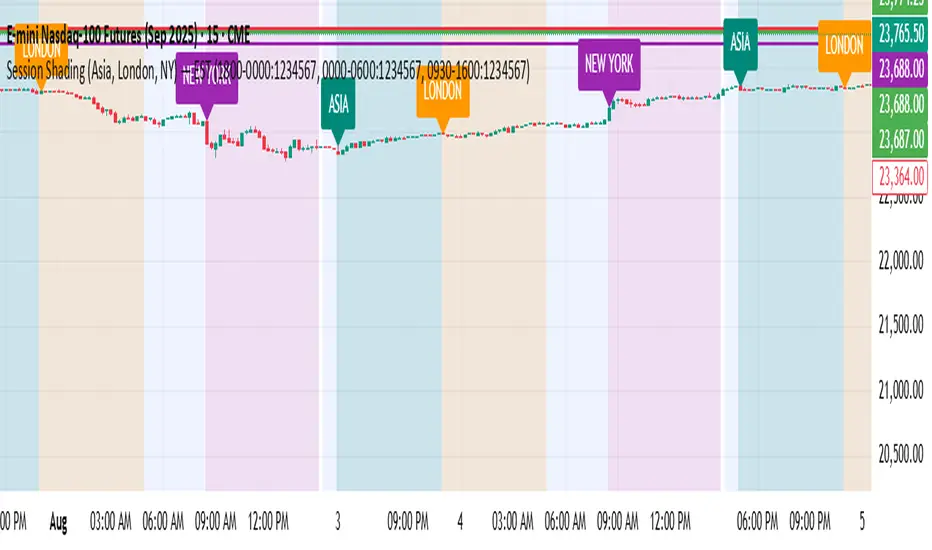

Killzones & Session Pivots

Plots the main trading sessions such as Asia, London and New York (AM, Lunch, PM) with full flexibility and styling options.

Each session can be enabled or disabled individually, with its own color, transparency and label preferences.

Session highs and lows are automatically tracked and plotted as pivots with extension modes like Until Mitigated or Past Mitigation.

This system gives traders the ability to organize market sessions exactly how they prefer whilst keeping the chart consistent and efficient.

Daily Pivots and Tier System

Alongside session pivots, the script tracks daily highs and lows to provide a broader structural view of price. These pivots are stored and displayed on the chart with their appearance updating automatically when price interacts with them.

The system includes a unique tier-based visibility filter that maintains a clean chart by preventing duplicate or overlapping pivots. Recent daily pivots are cached and compared to session pivots and when two levels fall within a defined proximity, the redundant one is automatically hidden. This creates a clear hierarchy of daily and session levels, keeping the most relevant structure visible whilst removing noise.

All aspects of the daily pivot system are fully customizable, including the number of tracked pivots, color, style settings and how mitigated levels are handled. The caching and filtering logic ensures smooth performance and a visually organized workspace even as the data updates in real time.

Key Times

Allows up to five custom key time markers such as the Midnight Open, 6:00 AM or 10:00 AM.

Each marker can be fully customized with its own text, color, line style and thickness.

This makes it simple to visualize key reaction points that align with each traders timing model.

Higher Timeframe Candles

Displays higher timeframe candles such as 1H, 4H or Daily directly on the active chart to provide context without switching views.

Users can customize body, wick and border colors, along with adding optional trace lines for the open, close, high and low and can also show the countdown timers for remaining candle time.

Adjustable spacing, positioning and label visibility makes the display blend naturally with any trading setup.

This module helps traders connect multiple timeframes visually in a clean and intuitive way.

Watermark

Adds a customizable watermark with title, subtitle and symbol or timeframe information.

Every element can be adjusted for color, size, transparency, alignment and position.

The result is a polished, professional chart layout that adapts to the user's personal style.

Optimization and Design

ICT Essentials is built for performance, using cached arrays and lightweight calculations to maintain responsiveness on all timeframes.

Each feature can be toggled individually to suit the traders focus or system performance.

The script delivers a fluid, customizable and highly optimized trading experience designed to feel natural and effortless in day-to-day use.

Credits

This script takes reference and inspiration from several open-source indicators:

Equal Highs and Lows by jzstur

ICT HTF Candles (fadi) by fadizeidan

ICT Killzones + Pivots EP by tradeforopp

AG FX - Watermark by AGFXTRADING

All components have been refactored, optimized and unified into a single framework for a smoother and more efficient workflow.

Session First 5-Min High/LowHere's a professional description for your indicator:

Session First 5-Min High/Low Marker

This indicator automatically identifies and marks the high and low price levels established during the first 5 minutes of major trading sessions, helping traders identify key intraday support and resistance zones.

Key Features:

Tracks three major trading sessions in IST (Indian Standard Time):

Asian Session: 5:30 AM - 5:35 AM

London Session: 12:30 PM - 12:35 PM

New York Session: 5:30 PM - 5:35 PM

Draws horizontal lines at the highest and lowest prices reached during each session's opening 5-minute window

Color-coded for easy identification (Yellow for Asian, Blue for London, Red for New York)

Lines extend across the chart to help track price reactions throughout the day

Clean, minimal design with optional labels

Best Used For:

Identifying key intraday support and resistance levels

Session breakout trading strategies

Understanding institutional order flow at market opens

Works on 1-minute timeframe for precise tracking

Customizable Settings:

Toggle line extensions on/off

Adjust line width (1-5)

Change colors for each session

Show/hide session labels

Perfect for day traders and scalpers who trade around major session openings and want to identify high-probability support/resistance zones established during peak liquidity periods.

This description explains what the indicator does, its practical applications, and its key features in a way that's clear for TradingView users.RetryClaude can make mistakes. Please double-check responses.

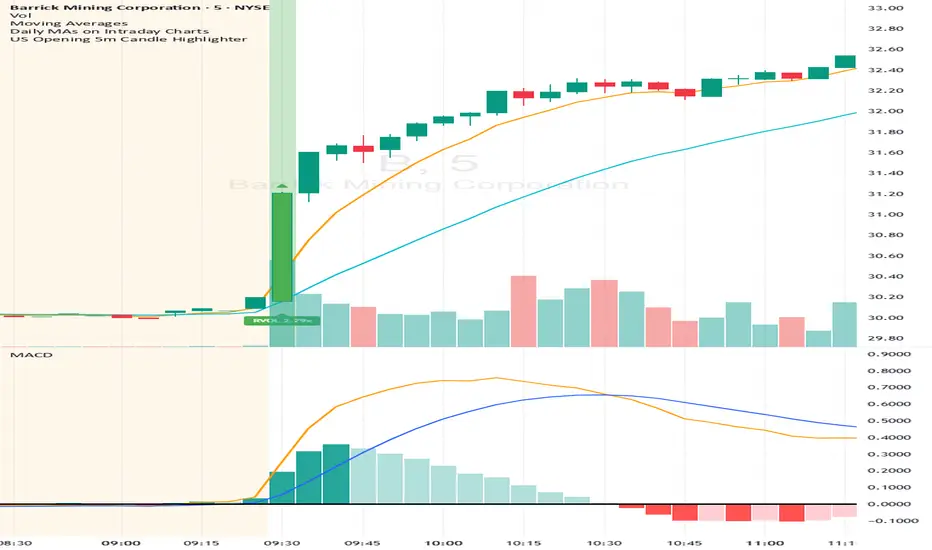

US Opening 5-Minute Candle HighlighterUS Opening 5-Minute Candle Highlighter — True RVOL (Two-Tier + Label)

What it does (in plain English)

This indicator finds the first 5-minute bar of the US cash session (09:30–09:35 ET) and highlights it when the candle has the specific “strong open” look you want:

Opens near the low of its own range, and

Closes near the high of its own range, and

Has a decisive real body (not a wick-y doji), and

(Optionally) is a green candle, and

Meets a TRUE opening-bar RVOL filter (compares today’s 09:30–09:35 volume only to prior sessions’ 09:30–09:35 volumes).

You get two visual intensities based on opening RVOL:

Tier-1 (≥ threshold 1, default 1.0×) → light green highlight + lime arrow

Tier-2 (≥ threshold 2, default 1.5×) → darker green highlight + green arrow

An RVOL label (e.g., RVOL 1.84x) can be shown above or below the opening bar.

Designed for 5-minute charts. On other timeframes the “opening bar” will be the bar that starts at 09:30 on that timeframe (e.g., 15-minute 09:30–09:45). For best results keep the chart on 5m.

How the pattern is defined

For the opening 5-minute bar, we compute:

Range = high − low

Body = |close − open|

Then we measure where the open and close sit within the bar’s own range on a 0→1 scale:

0 means exactly at the low

1 means exactly at the high

Using two quantiles:

Open ≤ position in range (0–1) (default 0.20)

Example: 0.20 means “open must be in the lowest 20% of the bar’s range.”

Close ≥ position in range (0–1) (default 0.80)

Example: 0.80 means “close must be in the top 20% of the bar’s range.”

This keeps the logic range-normalized so it adapts across different tickers and vol regimes (you’re not using fixed cents or % of price).

Body ≥ fraction of range (0–1) (default 0.55)

Requires the real body to be at least that fraction of the total range.

0.55 = body fills ≥ 55% of the candle.

Purpose: filter out indecisive, wick-heavy bars.

Raise to 0.7–0.8 for only the fattest thrusts; lower to 0.3–0.4 to admit more bars.

Require green candle? (default ON)

If ON, close > open must be true. Turn OFF if you also want to catch strong red opens for shorts.

Minimum range (ticks)

Ignore tiny, illiquid opens: e.g., set to 2–5 ticks to suppress micro bars.

TRUE Opening-Bar RVOL (why it’s “true”)

Most “RVOL” compares against any recent bars, which isn’t fair at the open.

This indicator calculates only against prior opening bars:

At 09:30–09:35 ET, take today’s opening 5-minute volume.

Compare it to the average of the last N sessions’ opening 5-minute volumes.

RVOL = today_open_volume / average_prior_open_volumes.

So:

1.0× = equal to average prior opens.

1.5× = 150% of average prior opens.

2.0× = double the typical opening participation.

A minimum prior samples guard (default 10) ensures you don’t judge with too little history. Until enough samples exist, the RVOL gate won’t pass (you can disable RVOL temporarily if needed).

Visuals & tiers

Light green highlight + lime arrow → price filters pass and RVOL ≥ Tier-1 (default 1.0×)

Dark green highlight + green arrow → price filters pass and RVOL ≥ Tier-2 (default 1.5×)

Optional bar paint in matching green tones for extra visibility.

Optional RVOL label (e.g., RVOL 1.84x) above or below the opening bar.

You can show the label only when the candle qualifies, or on every open.

Inputs (step-by-step)

Price-action filters

Open ≤ position in range (0–1): default 0.20. Smaller = stricter (must open nearer the low).

Close ≥ position in range (0–1): default 0.80. Larger = stricter (must close nearer the high).

Body ≥ fraction of range (0–1): default 0.55. Raise to demand a “fatter” body.

Require green candle?: default ON. Turn OFF to also mark bearish thrusts.

Minimum range (ticks): default 0. Set to 2–5 for liquid mid/large caps.

Time settings

Timezone: default America/New_York. Leave as is for US equities.

Start hour / minute: defaults 09:30. The bar that starts at this time is evaluated.

TRUE Opening-Bar RVOL (two-tier)

Require TRUE opening-bar RVOL?: ON = must pass Tier-1 to highlight; OFF = price filters alone can highlight (still shows Tier-2 when hit).

RVOL lookback (prior opens count): default 20. How many prior openings to average.

Min prior opens required: default 10. Warm-up guard.

Tier-1 RVOL threshold (× avg): default 1.00× (light green).

Tier-2 RVOL threshold (× avg): default 1.50× (dark green).

Display

Also paint candle body?: OFF by default. Turn ON for instant visibility on a chart wall.

Arrow size: tiny/small/normal/large.

Light/Dark opacity: tune highlight strength.

Show RVOL label?: ON/OFF.

Show label only when candle qualifies?: ON by default; OFF to see RVOL every open.

Label position: Above candle or Below candle.

Label size: tiny/small/normal/large.

How to use (quick start)

Apply to a 5-minute chart.

Keep defaults: Open ≤ 0.20, Close ≥ 0.80, Body ≥ 0.55, Require green ON.

Turn RVOL required ON, with Tier-1 = 1.0×, Tier-2 = 1.5×, Lookback = 20, Min prior = 10.

Optional: enable Paint bar and set Arrow size = large for monitor-wall visibility.

Optional: show RVOL label below the bar to keep wicks clean.

Interpretation:

Dark green = A+ opening thrust with strong participation (≥ Tier-2).

Light green = Valid opening thrust with at least average participation (≥ Tier-1).

No highlight = one or more filters failed (quantiles, body, green, range, or RVOL if required).

Alerts

Two alert conditions are included:

Opening 5m Match — Tier-2 RVOL → fires when the opening candle passes price filters and RVOL ≥ Tier-2.

Opening 5m Match — Tier-1 RVOL → fires when the opening candle passes price filters and RVOL ≥ Tier-1 (but < Tier-2).

Recommended alert settings

Condition: choose the script + desired tier.

Options: Once Per Bar Close (you want the confirmed 09:30–09:35 bar).

Set your watchlist to symbols of interest (themes/sectors) and let the alerts pull you to the right charts.

Recommended starting values

Quantiles: Open ≤ 0.20, Close ≥ 0.80

Body fraction: 0.55

Require green: ON

RVOL: Required ON, Tier-1 = 1.0×, Tier-2 = 1.5×, Lookback 20, Min prior 10

Display: Paint bar ON, Arrow large, Label ON, Below candle

Tune tighter for A-plus selectivity:

Open ≤ 0.15, Close ≥ 0.85, Body ≥ 0.65, Tier-2 2.0×.

Notes, tips & limitations

5-minute timeframe is the intended use. On higher TFs, the 09:30 bar spans more than 5 minutes; geometry may not reflect the first 5 minutes alone.

RTH only: The opening detection looks at the clock (09:30 ET). Pre-market bars are ignored for the signal and for RVOL history.

Warm-up period: Until you have Min prior opens required samples, the RVOL gate won’t pass. You can temporarily toggle RVOL off.

DST & timezone: Leave timezone on America/New_York for US equities. If you trade non-US exchanges, set the appropriate TZ and opening time.

Illiquid tickers: Use Minimum range (ticks) and require RVOL to reduce noise.

No strategy orders: This is a visual/alert tool. Combine with your execution and risk plan.

Why this is useful on multi-monitor setups

Instant pattern recognition: the two-shade green makes A vs A+ opens pop at a glance.

Adaptive thresholds: quantiles & body are within-bar, so it works across $5 and $500 names.

Fair volume test: TRUE opening RVOL avoids comparing to pre-market or midday bars.

Optional labels: glanceable RVOL x-value helps triage the strongest themes quickly.

X Pax ORThis indicator captures and visualizes the first 30 seconds of price action starting at 9:30 AM New York time and projects its influence throughout the trading day. Inspired by Pax's open range and level analysis, it provides a structured framework for observing how markets interact with an initial volatility burst.

Core Features

Opening 30s Range Box

At the 9:30:00–9:30:30 window, the indicator records the high and low of that short-lived but impactful moment. A translucent blue box is drawn from this range and extends to 4:00 PM, clearly defining the market’s first key battleground.

User-Defined Extension Levels

From the Opening Range High, upward extensions are projected in user-defined step sizes and counts.

From the Opening Range Low, downward extensions are projected using the same configurable step settings.

These levels adapt to your market and trading style, serving as volatility-based expansion markers to track order flow clustering and potential turning points.

Historical Preservation

Each day’s range box and extension lines are stored, allowing you to review prior sessions for pattern recognition.

Independent toggles let you display or hide historical boxes and historical extensions, keeping the chart clean when needed while retaining analytical depth when desired.

Real-Time Updates

Unlike delayed higher-timeframe methods, this indicator anchors directly to intraday action as it unfolds, ensuring levels are available in real time rather than only after candle closure.

Practical Use

Spot early breakouts or failed retests of the Opening 30s range.

Use extension levels as reference points for intraday trend continuation or reversal setups.

Compare current session levels vs. prior sessions to identify recurring order flow behavior.

Design Notes

Step size, extension count, color transparency, and historical storage are fully configurable.

Clean, minimalist presentation keeps focus on price interaction with levels rather than clutter.

Built for traders who value precision and structure in intraday analysis.

Total Points Range by exp3rtsThis indicator measures and displays the true intraday movement of a market by approximating tick-level activity using 1-second data aggregation. Instead of only looking at net candle movement, it sums every price change during a session, giving traders a more accurate picture of market effort and volatility.

Total Points Moved (TPM) – Captures the full distance traveled by price, not just the net gain/loss.

Bullish vs. Bearish Movement – Separates upward and downward moves so you can see who dominated the session.

Custom Sessions – Define your own session start/end times and time zone for precise tracking.

End-of-Session Summary – Automatically plots a label at session completion with totals for TPM, bullish, and bearish movement.

Visual Session Highlighting – Background shading makes it easy to see when the chosen session is active.

This tool is useful for:

Understanding the true effort vs. result of price movement

Comparing volatility across sessions

Identifying whether bulls or bears contributed more to market swings

Supporting order flow and tick-based trading strategies

MK_OSFT-Momentum Confluence DetectorMOMENTUM CONFLUENCE DETECTOR - Trading Indicator Overview

What This Indicator Does

The Momentum Confluence Detector is a comprehensive Pine Script indicator designed to identify high-probability trading opportunities by detecting momentum bars that align with multiple confluence factors. It combines traditional technical analysis with advanced Smart Money Concepts to filter out noise and highlight the most significant price movements.

CORE FUNCTIONALITY

📊 Momentum Bar Detection Identifies unusual volume and bar size expansion using customizable multipliers

Detects bullish, bearish, and neutral momentum bars based on OHLC relationships

Uses moving averages to establish baseline volume and bar size thresholds

🔄 Multi-Filter Confluence System

The indicator employs up to 5 different filter types to validate momentum signals:

Level Concept Filter - Choose between:

- Support/Resistance Levels : Traditional pivot-based S/R zones with touch counting and break tracking

- Smart Money Concepts : Institutional order flow analysis including Order Blocks, Fair Value Gaps (FVGs), and market structure breaks

Trend Filter : EMA/SMA-based trend direction confirmation with alignment requirements

Breakout Filter : Detects price breakouts beyond recent highs/lows with percentage thresholds

Volatility Filter : ATR expansion confirmation to ensure signals occur during active market conditions

Market Session Filter : Filters signals to specific trading sessions (Tokyo, London, New York)

ADVANCED FEATURES

🎯 Smart Money Concepts Integration

Order Blocks : Identifies institutional supply/demand zones from major and minor structure breaks

Fair Value Gaps (FVGs) : Detects price imbalances and tracks their evolution through partial fills and inversions

Market Structure : Recognizes Break of Structure (BOS) and Change of Character (CHoCH) patterns

Retracement Patterns : Tracks HLH (Higher-Low-Higher) and LHL (Lower-High-Lower) institutional patterns

📈 Support/Resistance System

Multi-timeframe pivot detection (3, 5, 7-bar spans)

Volume-weighted strength calculation for level importance

Dynamic level merging and break tracking

Automatic level type classification (Support/Resistance/Flip zones)

⚙️ Intelligent Filtering Logic

ALL Mode : Requires all enabled filters to pass (high precision)

ANY Mode : Requires at least one filter to pass (higher frequency)

Real-time filter status tracking and visualization

Visual Features

Signal Markers : Clear triangular markers for qualified momentum bars

Unfiltered Signals : Optional display of raw momentum bars for comparison

Level Visualization : Dynamic S/R level boxes and lines with strength indicators

Structure Lines : BOS/CHoCH break visualization with major/minor classification

Fair Value Gaps : Color-coded boxes showing bullish/bearish FVGs with partial fill tracking and IFVG conversion

Order Blocks : Institutional supply/demand zones displayed as colored boxes with major/minor classification

Information Table : Real-time display of signal details and filter status

Session Boxes : Visual representation of active trading sessions

Practical Applications

✅ Swing Trading : Identify high-probability reversal and continuation setups

✅ Day Trading : Spot intraday momentum shifts with institutional backing

✅ Multi-Timeframe Analysis : Combine major and minor structure analysis

✅ Risk Management : Filter out low-quality setups using confluence requirements

✅ Educational : Understand market structure and institutional order flow

Customization Options

Adjustable momentum thresholds for different market conditions

Comprehensive filter settings with individual enable/disable controls

Visual customization for colors, sizes, and display preferences

Alert system with detailed signal information

Performance optimization settings for different chart timeframes

Who Should Use This Indicator

This indicator is suitable for traders who:

Want to combine multiple technical analysis approaches

Seek to understand institutional market behavior

Prefer confluence-based trading setups

Need customizable filtering for different market conditions

Value comprehensive signal validation over high-frequency alerts

The Momentum Confluence Detector transforms complex market analysis into clear, actionable signals by requiring multiple forms of confirmation before highlighting trading opportunities.

Daily Midnight Lines# Daily Midnight Lines

A simple and efficient TradingView indicator that automatically draws vertical lines at the start of each new day.

* *

## Features

✅ **Precise Timing**: Draws lines at exactly 00:00 or on the first bar of the new day

✅ **Calendar Days**: Uses calendar days, not trading sessions

✅ **Customizable Design**: Green color with transparency for comfortable viewing

✅ **High Performance**: Optimized code without unnecessary calculations

✅ **Universal**: Works on all timeframes and instruments

## Settings

- **Line Color**: Green with 30% transparency (customizable)

- **Line Width**: 1 pixel (1 to 3)

- **Mode**: Exactly at 00:00 or first bar of new day

## Applications

- Separating trading days on the chart

- Analyzing price behavior at the start of the day

- Planning trading strategies

- Statistical analysis by days

## Compatibility

- Pine Script v6

- All timeframes (1m - 1M)

- All instruments (stocks, forex, crypto, futures)

- All markets (24/7, daily, night sessions)

Perfect for day traders, scalpers, and analysts who want better chart orientation and intraday pattern analysis.

---

## Ежедневные Полночные Линии

Простой и эффективный индикатор TradingView, который автоматически рисует вертикальные линии в начале каждого нового дня.

## Особенности

✅ **Точное время**: Рисует линии в 00:00 или на первом баре нового дня

✅ **Календарные дни**: Использует календарные дни, а не торговые сессии

✅ **Настраиваемый дизайн**: Зеленый цвет с прозрачностью для комфортного просмотра

✅ **Высокая производительность**: Оптимизированный код без лишних вычислений

✅ **Универсальность**: Работает на всех таймфреймах и инструментах

## Настройки

- **Цвет линий**: Зеленый с прозрачностью 30% (настраивается)

- **Толщина линий**: 1 пиксель (от 1 до 3)

- **Режим**: Точно в 00:00 или первый бар нового дня

## Применение

- Разделение торговых дней на графике

- Анализ поведения цены в начале дня

- Планирование торговых стратегий

- Статистический анализ по дням

## Совместимость

- Pine Script v6

- Все таймфреймы (1м - 1М)

- Все инструменты (акции, форекс, крипто, фьючерсы)

- Все рынки (24/7, дневные, ночные сессии)

Идеально подходит для дневных трейдеров, скальперов и аналитиков, которые хотят лучше ориентироваться на графике и анализировать внутридневные паттерны.

**Pine Script v6** | **Updated: October 2024** | **Обновлено: Октябрь 2024**

SCTI - D14SCTI - D14 Comprehensive Technical Analysis Suite

English Description

SCTI D14 is an advanced multi-component technical analysis indicator designed for professional traders and analysts. This comprehensive suite combines multiple analytical tools into a single, powerful indicator that provides deep market insights across various timeframes and methodologies.

Core Components:

1. EMA System (Exponential Moving Averages)

13 customizable EMA lines with periods ranging from 8 to 2584

Fibonacci-based periods (8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584)

Color-coded visualization for easy trend identification

Individual toggle controls for each EMA line

2. TFMA (Multi-Timeframe Moving Averages)

Cross-timeframe analysis with 3 independent EMA calculations

Real-time labels showing trend direction and price relationships

Customizable timeframes for each moving average

Percentage deviation display from current price

3. PMA (Precision Moving Average Cloud)

7-layer moving average system with customizable periods

Fill areas between moving averages for trend visualization

Support and resistance zone identification

Dynamic color-coded trend clouds

4. VWAP (Volume Weighted Average Price)

Multiple anchor points (Session, Week, Month, Quarter, Year, Earnings, Dividends, Splits)

Standard deviation bands for volatility analysis

Automatic session detection and anchoring

Statistical price level identification

5. Advanced Divergence Detector

12 technical indicators for divergence analysis (MACD, RSI, Stochastic, CCI, Williams %R, Bias, Momentum, OBV, VW-MACD, CMF, MFI, External)

Regular and hidden divergences detection

Bullish and bearish signals with visual confirmation

Customizable sensitivity and filtering options

Real-time alerts for divergence formations

6. Volume Profile & Node Analysis

Comprehensive volume distribution analysis

Point of Control (POC) identification

Value Area High/Low (VAH/VAL) calculations

Volume peaks and troughs detection

Support and resistance levels based on volume

7. Smart Money Concepts

Market structure analysis with Break of Structure (BOS) and Change of Character (CHoCH)

Internal and swing structure detection

Equal highs and lows identification

Fair Value Gaps (FVG) detection and visualization

Liquidity zones and institutional flow analysis

8. Trading Sessions

9 major trading sessions (Asia, Sydney, Tokyo, Shanghai, Hong Kong, Europe, London, New York, NYSE)

Real-time session status and countdown timers

Session volume and performance tracking

Customizable session boxes and labels

Statistical session analysis table

Key Features:

Modular Design: Enable/disable any component independently

Real-time Analysis: Live updates with market data

Multi-timeframe Support: Works across all chart timeframes

Customizable Alerts: Set alerts for any detected pattern or signal

Professional Visualization: Clean, organized display with customizable colors

Performance Optimized: Efficient code for smooth chart performance

Use Cases:

Trend Analysis: Identify market direction using multiple EMA systems

Entry/Exit Points: Use divergences and structure breaks for timing

Risk Management: Utilize volume profiles and session analysis for better positioning

Multi-timeframe Analysis: Confirm signals across different timeframes

Institutional Analysis: Track smart money flows and market structure

Perfect For:

Day traders seeking comprehensive market analysis

Swing traders needing multi-timeframe confirmation

Professional analysts requiring detailed market structure insights

Algorithmic traders looking for systematic signal generation

---

中文描述

SCTI - D14是一个先进的多组件技术分析指标,专为专业交易者和分析师设计。这个综合套件将多种分析工具整合到一个强大的指标中,在各种时间框架和方法论中提供深度市场洞察。

核心组件:

1. EMA系统(指数移动平均线)

13条可定制EMA线,周期从8到2584

基于斐波那契的周期(8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, 2584)

颜色编码可视化,便于趋势识别

每条EMA线的独立切换控制

2. TFMA(多时间框架移动平均线)

跨时间框架分析,包含3个独立的EMA计算

实时标签显示趋势方向和价格关系

每个移动平均线的可定制时间框架

显示与当前价格的百分比偏差

3. PMA(精密移动平均云)

7层移动平均系统,周期可定制

移动平均线间填充区域用于趋势可视化

支撑阻力区域识别

动态颜色编码趋势云

4. VWAP(成交量加权平均价格)

多个锚点(交易时段、周、月、季、年、财报、分红、拆股)

标准差带用于波动性分析

自动时段检测和锚定

统计价格水平识别

5. 高级背离检测器

12个技术指标用于背离分析(MACD、RSI、随机指标、CCI、威廉姆斯%R、Bias、动量、OBV、VW-MACD、CMF、MFI、外部指标)

常规和隐藏背离检测

看涨看跌信号配视觉确认

可定制敏感度和过滤选项

背离形成的实时警报

6. 成交量分布与节点分析

全面的成交量分布分析

控制点(POC)识别

价值区域高/低点(VAH/VAL)计算

成交量峰值和低谷检测

基于成交量的支撑阻力水平

7. 聪明钱概念

市场结构分析,包括结构突破(BOS)和结构转变(CHoCH)

内部和摆动结构检测

等高等低识别

公允价值缺口(FVG)检测和可视化

流动性区域和机构资金流分析

8. 交易时区

9个主要交易时段(亚洲、悉尼、东京、上海、香港、欧洲、伦敦、纽约、纽交所)

实时时段状态和倒计时器

时段成交量和表现跟踪

可定制时段框和标签

统计时段分析表格

主要特性:

模块化设计:可独立启用/禁用任何组件

实时分析:随市场数据实时更新

多时间框架支持:适用于所有图表时间框架

可定制警报:为任何检测到的模式或信号设置警报

专业可视化:清洁、有序的显示界面,颜色可定制

性能优化:高效代码确保图表流畅运行

使用场景:

趋势分析:使用多重EMA系统识别市场方向

入场/出场点:利用背离和结构突破进行时机选择

风险管理:利用成交量分布和时段分析进行更好定位

多时间框架分析:在不同时间框架间确认信号

机构分析:跟踪聪明钱流向和市场结构

适用于:

寻求全面市场分析的日内交易者

需要多时间框架确认的摆动交易者

需要详细市场结构洞察的专业分析师

寻求系统化信号生成的算法交易者

Dr.Yazdani V063 Session OR + A-Lines

**ACD Indicator: Mark Fisher's Opening Range Breakout Strategy**

**Overview**

The ACD system, developed by legendary trader Mark Fisher in his book *The Logical Trader*, is a powerful methodology for identifying high-probability trade setups based on the market's opening range (OR). This indicator automates Layers 1 and 2 of the ACD strategy, helping you spot breakout opportunities, trend direction, and key support/resistance levels. Perfect for day traders, scalpers, and swing traders in forex, stocks, futures, or crypto.

**How It Works**

1. **Opening Range (OR)**: Calculated from the high/low of the first X minutes (default: 30-60 min) of major sessions (e.g., Tokyo, London, New York).

2. **A Levels**: Drawn at a percentage (default: 0.5% of OR range or ATR-based) above/below the OR. A breakout above A-Up signals a bullish setup; below A-Down signals bearish.

3. **C Levels**: Wider levels (default: 1-2% or ATR multiplier) for stronger confirmation. Breakouts here confirm trend strength and filter fakeouts.

4. **Pivot Ranges**: Includes daily and N-day pivots to gauge overall market bias (above pivots = bullish; below = bearish).

**Key Features**

- **Customizable Sessions**: Tokyo (00:00-01:00 GMT), London (08:00-09:00 GMT), New York (13:30-14:30 GMT) – adjustable.

- **ATR Integration**: Uses Average True Range for dynamic A/C levels (period: 14 by default).

- **Visual Alerts**: Color-coded lines (green for bullish, red for bearish) + optional labels for breakouts.

- **Pivot Display**: Show/hide daily or multi-day pivots with customizable colors.

- **Risk Management**: Built-in stop-loss suggestions based on OR width.

**Trading Rules**

- **Bullish Setup**: Price breaks and holds above A-Up → Enter long at C-Up confirmation. Target: Next pivot or 1:2 risk-reward.

- **Bearish Setup**: Price breaks below A-Down → Enter short at C-Down.

- **Avoid Fakeouts**: Wait for stabilization (e.g., close above/below level).

- **Trend Filter**: Combine with PMA (Pivot Moving Average) for Layer 3 confirmation (search "ACD PMA" in TradingView).

**Settings Guide**

- **OR Timeframe**: Session start time and duration (e.g., 30 min).

- **A Multiplier (%)**: Distance for A levels (default: 0.5).

- **C Multiplier (%)**: Distance for C levels (default: 1.0).

- **ATR Period**: For volatility-based levels (default: 14).

- **Show Pivots**: Toggle daily/N-day ranges.

This indicator balances supply/demand by analyzing volume and price action within the opening range. Backtest on your favorite pairs (e.g., EURUSD, BTCUSD) and adjust for your style. Not financial advice – always use proper risk management!

**Inspired by**: Mark Fisher's ACD Methodology. Open-source for community review. Questions? Comment below!

#ACD #OpeningRange #Breakout #DayTrading #FisherStrategy

BioSwarm Imprinter™BioSwarm Imprinter™ — Agent-Based Consensus for Traders

What it is

BioSwarm Imprinter™ is a non-repainting, agent-based sentiment oscillator. It fuses many short-to-medium lookback “opinions” into one 0–100 consensus line that is easy to read at a glance (50 = neutral, >55 bullish bias, <45 bearish bias). The engine borrows from swarm intelligence: many simple voters (agents) adapt their influence over time based on how well they’ve been predicting price, so the crowd gets smarter as conditions change.

Use it to:

• Detect emerging trends sooner without overreacting to noise.

• Filter mean-reversion vs continuation opportunities.

• Gate entries with a confidence score that reflects both strength and persistence of the move.

• Combine with your execution tools (VWAP/ORB/levels) as a state filter rather than a trade signal by itself.

⸻

Why it’s different

• Swarm learning: Each agent improves or decays its “fitness” depending on whether its vote matched the next bar’s direction. High-fitness agents matter more; weak agents fade.

• Multi-horizon by design: The crowd is composed of fixed, simple lookbacks spread from lenMin to lenMax. You get a blended, robust view instead of a single fragile parameter.

• Two complementary lenses: Each agent evaluates RSI-style balance (via Wilder’s RMA) and momentum (EMA deviation). You decide the weight of each.

• No repaint, no MTF pitfalls: Everything runs on the chart’s timeframe with bar-close confirmation; no request.security() or forward references.

• Actionable UI: A clean consensus line, optional regime background, confidence heat, and triangle markers when thresholds are crossed.

⸻

What you see on the chart

• Consensus line (0–100): Smoothed to your preference; color/area makes bull/bear zones obvious.

• Regime coloring (optional): Light green in bull zone, light red in bear zone; neutral otherwise.

• Confidence heat: A small gauge/number (0–100) that combines distance from neutral and recent persistence.

• Markers (optional): Triangles when consensus crosses up through your bull threshold (e.g., 55) or down through your bear threshold (e.g., 45).

• Info panel (optional): Consensus value, regime, confidence, number of agents, and basic diagnostics.

⸻

How it works (under the hood)

1. Horizon bins: The range is divided into numBins. Each bin has a fixed, simple integer length (crucial for Pine’s safety rules).

2. Per-bin features (computed every bar):

• RSI-style balance using Wilder’s RMA (not ta.rsi()), then mapped to −1…+1.

• Momentum as (close − EMA(L)) / EMA(L) (dimensionless drift).

3. Agent vote: For its assigned bin, an agent forms a weighted score: score = wRSI*RSI_like + wMOM*Momentum. A small dead-band near zero suppresses chop; votes are +1/−1/0.

4. Fitness update (bar close): If the agent’s previous vote agreed with the next bar’s direction, multiply its fitness by learnGain; otherwise by learnPain. Fitness is clamped so it never explodes or dies.

5. Consensus: Weighted average of all votes using fitness as weights → map to 0–100 and smooth with EMA.

Why it doesn’t repaint:

• No future references, no MTF resampling, fitness updates only on confirmed bars.

• All TA primitives (RMA/EMA/deltas) are computed every bar unconditionally.

⸻

Signals & confidence

• Bullish bias: consensus ≥ bullThr (e.g., 55).

• Bearish bias: consensus ≤ bearThr (e.g., 45).

• Confidence (0–100):

• Distance score: how far consensus is from 50.

• Momentum score: how strong the recent change is versus its recent average.

• Combined into a single gate; start filtering entries at ≥60 for higher quality.

Tip: For range sessions, raise thresholds (60/40) and increase smoothing; for momentum sessions, lower smoothing and keep thresholds at 55/45.

⸻

Inputs you’ll actually tune

• Agents & horizons:

• N_agents (e.g., 64–128)

• lenMin / lenMax (e.g., 6–30 intraday, 10–60 swing)

• numBins (e.g., 12–24)

• Weights & smoothing:

• wRSI vs wMOM (e.g., 0.7/0.3 for FX & indices; 0.6/0.4 for crypto)

• deadBand (0.03–0.08)

• consSmooth (3–8)

• Thresholds & hygiene:

• bullThr/bearThr (55/45 default)

• cooldownBars to avoid signal spam

⸻

Playbooks (ready-to-use)

1) Breakout / Trend continuation

• Timeframe: 15m–1h for day/swing.

• Filter: Take longs only when consensus > 55 and confidence ≥ 60.

• Execution: Use your ORB/VWAP/pullback trigger for entry. Trail with swing lows or 1.5×ATR. Exit on a close back under 50 or when a bearish signal prints.

2) Mean reversion (fade)

• When: Sideways days or low-volatility clusters.

• Setup: Increase deadBand and consSmooth.

• Signal: Bearish fades when consensus rolls over below ≈55 but stays above 50; bullish fades when it rolls up above ≈45 but stays below 50.

• Targets: The neutral zone (~50) as the first take-profit.

3) Multi-TF alignment

• Keep BioSwarm on 1H for bias, execute on 5–15m:

• Only take entries in the direction of the 1H consensus.

• Skip counter-bias scalps unless confidence is very low (explicit mean-reversion plan).

⸻

Integrations that work

• DynamoSent Pro+ (macro bias): Only act when macro bias and swarm consensus agree.

• ORB + Session VWAP Pro: Trade London/NY ORB breakouts that retest while consensus >55 (long) or <45 (short).

• Levels/Orderflow: BioSwarm is your “go / no-go”; execution stays with your usual triggers.

⸻

Quick start

1. Drop the indicator on a 1H chart.

2. Start with: N_agents=64, lenMin=6, lenMax=30, numBins=16, deadBand=0.06, consSmooth=5, thresholds 55/45.

3. Trade only when confidence ≥ 60.

4. Add your favorite execution tool (VWAP/levels/OR) for entries & exits.

⸻

Non-repainting & safety notes

• No request.security(); no hidden lookahead.

• Bar-close confirmation for fitness and signals.

• All TA calls are unconditional (no “sometimes called” warnings).

• No series-length inputs to RSI/EMA — we use RMA/EMA formulas that accept fixed simple ints per bin.

⸻

Known limits & tips

• Too many signals? Raise deadBand, increase consSmooth, widen thresholds to 60/40.

• Too few signals? Lower deadBand, reduce consSmooth, narrow thresholds to 53/47.

• Over-fitting risk: Keep learnGain/learnPain modest (e.g., ×1.04 / ×0.96).

• Compute load: Large N_agents × numBins is heavier; scale to your device.

⸻

Example recipes

EURUSD 1H (swing):

lenMin=8, lenMax=34, numBins=16, wRSI=0.7, wMOM=0.3, deadBand=0.06, consSmooth=6, thr=55/45

Buy breakouts when consensus >55 and confidence ≥60; confirm with 5–15m pullback to VWAP or level.

SPY 15m (US session):

lenMin=6, lenMax=24, numBins=12, consSmooth=4, deadBand=0.05

On trend days, stay with longs as long as consensus >55; add on shallow pullbacks.

BTC 1H (24/7):

Increase momentum weight: wRSI=0.6, wMOM=0.4, extend lenMax to ~50. Use dynamic stops (ATR) and partials on strong verticals.

⸻

Final word

BioSwarm is a state engine: it tells you when the market is primed to continue or mean-revert. Pair it with your entries and risk framework to turn that state into trades. If you’d like, I can supply a companion strategy template that consumes the consensus and back-tests the three playbooks (Breakout/Fade/Flip) with standard risk management.

Flux Power Dashboard (Updated and Renamed)Flux Power Dashboard is a compact market-state heads-up display for TradingView. It blends trend, momentum, and volume-flow into a single on-chart panel with color-coded cues and minimal lag. You get:

Clean visual trend via fast/slow MA with slope/debounce filters

MACD state and most recent cross (with “freshness” tint)

OBV confirmation and gating to reduce noise

Session awareness (Asia/London/New York + pre-sessions + overlap)

Optional HTF Regime row and regime gate to align signals to higher-timeframe bias

Context from VIX/VXN (volatility regime)

A single Flux Score (0–100) as a top-level read

It is deliberately “dashboard-first”: fast to read, consistent between symbols/timeframes, and designed to limit overtrading in chop.

What it can do (capabilities)

Signal gating: You can require multiple pillars to agree (Trend, MACD, OBV) before a “strong” bias is shown.

Debounced trend: Uses slope + confirmation bars to avoid flip-flopping.

Session presets: Auto-adjust the minimum confirmation bars by session (e.g., NY vs London vs Asia) to better match liquidity/volatility.

MACD presets: Quick switch between Scalp / Classic / Slow or roll your own custom speeds.

OBV confirmation: Volume flow must agree for trend/entries to “count” (optional).

HTF Regime awareness: Shows the higher-timeframe backdrop and (optionally) gates signals so you don’t fight the dominant trend.

Volatility context: VIX/VXN auto-colored cells based on your thresholds.

Top-center Session Title: Broadcasts the active session (or Overlap) with a matched background color.

Customizable UI: Column fonts, params font, transparency, dashboard corner, marker styles, colors, widths—tune it to your chart.

Practical use: Start with Flux Score + Summary for a snapshot, confirm with Trend & MACD, check OBV agreement (implicit in signal strength), glance at Regime to avoid counter-trend trades, and use Session + VIX/VXN for timing and risk context.

How it avoids common pitfalls

Repaint-aware: “Confirm on Close” can be enabled to read prior bar states, reducing intrabar noise.

Auto MA sanity: If fast ≥ slow length, it auto-swaps under the hood to keep calculations valid.

Debounce & confirm: Trend flips only after X bars satisfy conditions, cutting false flips in chop.

Freshness tint: New Cross/Signal rows tint slightly brighter for a few bars, so you can spot recency at a glance.

Every line of the dashboard (what it shows, how it’s colored)

Flux Score

What: Composite 0–100 built from three pillars: Trend (40%), MACD (30%), OBV (30%).

Read: ≥70 Bullish, ≤30 Bearish, else Neutral.

Use: Quick “state of play” gauge—stronger alignment pushes the score toward extremes.

Regime (optional row)

What: Higher-timeframe (your Regime TF) backdrop using the same MA pair with HTF slope/ATR buffer.

Values: Bull / Bear / Range.

Gate (optional): If Regime Gate is ON, Trend/Signals only go directional when HTF agrees.

Summary

What: One-line narrative combining the three pillars: MACD (up/down/flat), OBV (up/down/flat), Trend (up/down/flat).

Use: Human-readable cross-check; should rhyme with Flux Score.

Trend

What: Debounced MA relationship on the current chart.

Strict: needs fast > slow and slow rising (mirror for down) + slope debounce + confirmation bars.

Lenient: allows fast > slow or slow rising (mirror for down) with the same debounce/confirm.

Color: Green = UP, Red = DOWN, Gray = FLAT.

Use: Your structural bias on the trading timeframe.

MACD