Pullback SARPullback SAR - Parabolic SAR with Pullback Detection

Description: The "Pullback SAR" is an advanced indicator built on the classic Parabolic SAR but with additional functionality for detecting pullbacks. It helps identify moments when the price pulls back from the main trend, offering potential entry signals. Perfect for traders looking to enter the market after a correction.

Key Features:

SAR (Parabolic SAR): The Parabolic SAR indicator is used to determine potential trend reversal points. It marks levels where the price could reverse its direction.

Pullback Detection: The indicator catches periods when the price moves away from the main trend and then returns, which may suggest a re-entry opportunity.

Long and Short Signals: Once a pullback in the direction of the main trend is identified, the indicator generates signals that could be used to open positions.

Simple and Clear Construction: The indicator is based on the classic SAR, with added pullback detection logic to enhance the accuracy of the signals.

Parameters:

Start (SAR Step): Determines the initial step for the SAR calculation, which controls the rate of change in the indicator at the beginning.

Increment (SAR Increment): Defines the maximum step size for SAR, allowing traders to adjust the indicator’s sensitivity to market volatility.

Max Value (SAR Max): Sets the upper limit for the SAR value, controlling its volatility.

Usage:

Swing Trading: Ideal for swing strategies, aiming to capture larger price moves while maintaining a safe margin.

Scalping: Due to its precise pullback detection, it can also be used in scalping, especially when the price quickly returns to the main trend.

Risk Management: The combination of SAR and pullback detection allows traders to adjust their positions according to changing market conditions.

Special Notes:

Adjusting Parameters: Depending on the market and trading style, users can adjust the SAR parameters (Start, Increment, Max Value) to fit their needs.

Combination with Other Indicators: It's recommended to use the indicator alongside other technical analysis tools (e.g., EMA, RSI) to enhance the accuracy of the signals.

Link to the script: This open-source version of the indicator is available on TradingView, enabling full customization and adjustments to meet your personal trading strategy. Share your experiences and suggestions!

Поиск скриптов по запросу "swing trading"

Multiple MAsHere's a well-written description in English for your "Multiple MAs" indicator that you can use when publishing on TradingView. It’s concise, professional, and highlights the key features of the indicator while explaining its purpose for traders.

---

### Multiple MAs Indicator

#### Overview

The **Multiple MAs** indicator is a versatile and straightforward tool designed to help traders visualize price trends using multiple Simple Moving Averages (SMAs) on a single chart. By plotting six SMAs with customizable lengths (MA5, MA10, MA20, MA50, MA100, and MA200), this indicator provides a clear view of short-term, medium-term, and long-term trends, making it ideal for trend-following strategies, crossover analysis, and identifying potential support/resistance levels.

#### Features

- **Customizable MA Lengths**: Adjust the periods of all six moving averages (MA5, MA10, MA20, MA50, MA100, MA200) to suit your trading style and timeframe.

- **Distinct Visuals**: Each MA is plotted with a unique color and line width for easy identification:

- MA5 (Dodger Blue, 1px)

- MA10 (Green, 1px)

- MA20 (Red, 2px)

- MA50 (Purple, 3px)

- MA100 (Gray, 3px)

- MA200 (White, 3px)

- **Overlay on Price Chart**: The indicator overlays directly on the price chart, allowing for seamless integration with other technical analysis tools.

- **High Precision**: Displays values with 8-decimal precision, ensuring accuracy for assets with small price movements (e.g., forex pairs or cryptocurrencies).

#### How to Use

1. **Trend Identification**: Use the longer MAs (e.g., MA100, MA200) to determine the overall trend direction. If the price is above these MAs, the trend is likely bullish; if below, it’s likely bearish.

2. **Crossover Signals**: Look for crossovers between shorter MAs (e.g., MA5 crossing MA20) for potential entry or exit signals. For example:

- A bullish signal occurs when a shorter MA crosses above a longer MA.

- A bearish signal occurs when a shorter MA crosses below a longer MA.

3. **Support and Resistance**: MAs often act as dynamic support or resistance levels. Watch for price reactions around these lines, especially the MA50, MA100, and MA200.

4. **Divergence Analysis**: Compare the slope of different MAs to identify potential trend reversals or weakening momentum.

#### Settings

- **MA5 Length**: Default is 5 bars.

- **MA10 Length**: Default is 10 bars.

- **MA20 Length**: Default is 20 bars.

- **MA50 Length**: Default is 50 bars.

- **MA100 Length**: Default is 100 bars.

- **MA200 Length**: Default is 200 bars.

#### Best Practices

- **Timeframe**: This indicator works on any timeframe but is particularly effective on daily, 4-hour, and 1-hour charts for swing trading or trend-following strategies.

- **Combine with Other Tools**: Pair the Multiple MAs with other indicators like RSI, MACD, or volume analysis to confirm signals and avoid false breakouts.

- **Adjust for Volatility**: For highly volatile assets, consider increasing the MA lengths to reduce noise and focus on broader trends.

#### Notes

- The indicator is lightweight and optimized for performance, ensuring it runs smoothly even on lower timeframes.

- Colors and line widths are pre-set for clarity but can be customized in the indicator settings if needed.

#### Credits

Created by kosar_v. Feedback and suggestions are welcome to improve this tool for the TradingView community!

[TehThomas] - ICT Inversion Fair value Gap (IFVG) The Inversion Fair Value Gap (IFVG) indicator is a powerful tool designed for traders who utilize ICT (Inner Circle Trader) strategies. It focuses on identifying and displaying Inversion Fair Value Gaps, which are critical zones that emerge when traditional Fair Value Gaps (FVGs) are invalidated by price action. These gaps represent key areas where price often reacts, making them essential for identifying potential reversals, trend continuations, and liquidity zones.

What Are Inversion Fair Value Gaps?

Inversion Fair Value Gaps occur when price revisits a traditional FVG and breaks through it, effectively flipping its role in the market. For example:

A bullish FVG that is invalidated becomes a bearish zone, often acting as resistance.

A bearish FVG that is invalidated transforms into a bullish zone, serving as support.

These gaps are significant because they often align with institutional trading activity. They highlight areas where large orders have been executed or where liquidity has been targeted. Understanding these gaps provides traders with a deeper insight into market structure and helps them anticipate future price movements with greater accuracy.

Why This Strategy Works

The IFVG concept is rooted in ICT principles, which emphasize liquidity dynamics, market inefficiencies, and institutional order flow. Traditional FVGs represent imbalances in price action caused by gaps between candles. When these gaps are invalidated, they become inversion zones that can act as magnets for price. These zones frequently serve as high-probability areas for price reversals or trend continuations.

This strategy works because it aligns with how institutional traders operate. Inversion gaps often mark areas of interest for "smart money," making them reliable indicators of potential market turning points. By focusing on these zones, traders can align their strategies with institutional behavior and improve their overall trading edge.

How the Indicator Works

This indicator simplifies the process of identifying and tracking IFVGs by automating their detection and visualization on the chart. It scans the chart in real-time to identify bullish and bearish FVGs that meet user-defined thresholds for inversion. Once identified, these gaps are dynamically displayed on the chart with distinct colors for bullish and bearish zones.

The indicator also tracks whether these gaps are mitigated or broken by price action. When an IFVG is broken, it extends the zone for a user-defined number of bars to visualize its potential role as a new support or resistance level. Additionally, alerts can be enabled to notify traders when new IFVGs form or when existing ones are broken, ensuring timely decision-making in fast-moving markets.

Key Features

Automatic Detection: The indicator automatically identifies bullish and bearish IFVGs based on user-defined thresholds.

Dynamic Visualization: It displays IFVGs directly on the chart with customizable colors for easy differentiation.

Real-Time Updates: The status of each IFVG is updated dynamically based on price action.

Zone Extensions: Broken IFVGs are extended to visualize their potential as support or resistance levels.

Alerts: Notifications can be set up to alert traders when key events occur, such as the formation or breaking of an IFVG.

These features make the tool highly efficient and reduce the need for manual analysis, allowing traders to focus on execution rather than tedious chart work.

Benefits of Using This Indicator

The IFVG indicator offers several advantages that make it an indispensable tool for ICT traders. By automating the detection of inversion gaps, it saves time and reduces errors in analysis. The clearly defined zones improve risk management by providing precise entry points, stop-loss levels, and profit targets based on market structure.

This tool is also highly versatile and adapts seamlessly across different timeframes. Whether you’re scalping lower timeframes or swing trading higher ones, it provides actionable insights tailored to your trading style. Furthermore, by aligning your strategy with institutional logic, you gain a significant edge in anticipating market movements.

Practical Applications

This indicator can be used across various trading styles:

Scalping: Identify quick reversal points on lower timeframes using real-time alerts.

Day Trading: Use inversion gaps as key levels for intraday support/resistance or trend continuation setups.

Swing Trading: Analyse higher timeframes to identify major inversion zones that could act as critical turning points in larger trends.

By integrating this tool into your trading routine, you can streamline your analysis process and focus on executing high-probability setups.

Conclusion

The Inversion Fair Value Gap (IFVG) indicator is more than just a technical analysis tool—it’s a strategic ally for traders looking to refine their edge in the markets. By automating the detection and tracking of inversion gaps based on ICT principles, it simplifies complex market analysis while maintaining accuracy and depth. Whether you’re new to ICT strategies or an experienced trader seeking greater precision, this indicator will elevate your trading game by aligning your approach with institutional behavior.

If you’re serious about improving your trading results while saving time and effort, this tool is an essential addition to your toolkit. It provides clarity in chaotic markets, enhances precision in trade execution, and ensures you never miss critical opportunities in your trading journey.

__________________________________________

Thanks for your support!

If you found this idea helpful or learned something new, drop a like 👍 and leave a comment, I’d love to hear your thoughts! 🚀

Make sure to follow me for more price action insights, free indicators, and trading strategies. Let’s grow and trade smarter together! 📈

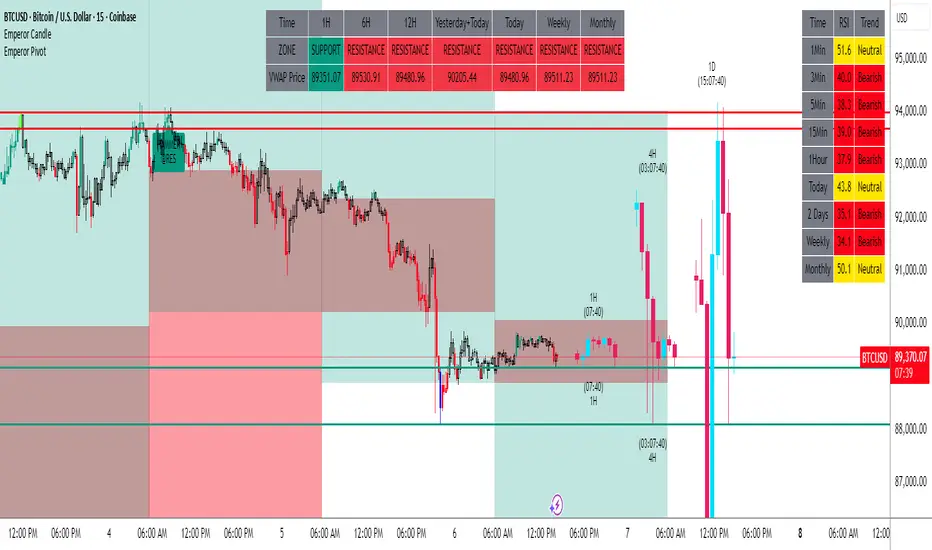

Emperor RSI CandleDescription:

The Emperor RSI Candle is a real-time, non-lagging trading indicator that colors candles based on RSI (Relative Strength Index) levels. It offers instant visual feedback on market momentum, making it easy to identify trend strength, overbought/oversold zones, and potential reversals with precision.

Unlike traditional RSI indicators, which display RSI values in a separate panel, Emperor RSI Candle integrates RSI signals directly into the candles, providing a cleaner, more intuitive charting experience. Its multi-timeframe RSI box shows RSI values across different timeframes, offering confluence confirmation for better trade decisions.

🔥 Emperor RSI Candle is original because it includes a multi-timeframe RSI box that displays RSI values from:

1 min → Monthly timeframes simultaneously.

📊 How this is unique:

Traders can instantly compare RSI values across different timeframes.

This helps them spot confluence and divergences, which is not possible with standard RSI indicators.

The multi-timeframe confluence feature makes the indicator highly effective for both short-term and long-term traders.

🚀 What the script does:

Real-time candle coloring based on RSI levels.

Multi-timeframe RSI box for confluence insights.

Customizable RSI settings for adaptability.

How it benefits traders:

Instant visual feedback for momentum and reversals.

No lag signals for precise trading decisions.

Flexible customization for different trading styles.

Unique visual signals:

Green, red, parrot green, and blue candles → Clearly indicating bullish/bearish momentum and overbought/oversold zones.

Multi-timeframe RSI box → For cross-timeframe confluence.

⚡️ 🔥 UNIQUE FEATURES 🔥:

✅ Multi-Timeframe RSI Box:

Displays RSI values from 1 min to monthly timeframes, helping traders confirm confluence across different timeframes.

✅ Fully Customizable RSI Levels & Display:

Modify RSI thresholds, source, and appearance to fit your trading style.

✅ Dynamic Candle Borders for Weak Signals:

Green border → Weak bullishness (RSI between 50-60).

Red border → Weak bearishness (RSI between 40-50).

✅ Lag-Free, Real-Time Accuracy:

No repainting or delay—instant visual signals for accurate decisions.

✅ Scalable for Any Trading Style:

Perfect for both intraday scalping and positional trading.

📊 🔥 HOW IT WORKS 🔥:

The indicator dynamically colors candles based on RSI values, providing real-time visual signals:

🟢 Above 60 RSI → Green candle:

Indicates bullish momentum, signaling potential upward continuation.

🟩 Above 80 RSI → Parrot green candle:

Overbought zone → Possible reversal or profit booking.

🟥 Below 40 RSI → Red candle:

Signals bearish momentum, indicating potential downward continuation.

🔵 Below 20 RSI → Blue candle:

Oversold zone → Possible reversal opportunity.

🔲 Neutral candles:

50-60 RSI → Green border: Weak bullishness.

40-50 RSI → Red border: Weak bearishness.

📊 🔥 MULTI-TIMEFRAME RSI BOX 🔥:

The Emperor RSI Candle includes an RSI box displaying multi-timeframe RSI values from 1 min to monthly. This provides:

✅ Confluence confirmation:

Compare RSI across multiple timeframes to strengthen trade conviction.

✅ Spot divergences:

Identify hidden trends by comparing smaller and larger timeframes.

✅ Validate trade entries/exits:

Use higher timeframe RSI to confirm smaller timeframe signals

⚙️ 🔥 HOW TO USE IT 🔥:

To maximize the accuracy and clarity of Emperor RSI Candle, follow these steps:

🔧 STEP 1: Chart Settings Configuration

Go to Chart Settings → Symbols

Uncheck the following options:

Body

Borders

Wick

✅ This ensures that only the Emperor Candle colors are visible, making the signals clear and distinct.

🔧 STEP 2: Style Settings for Emperor Candle

After applying the Emperor RSI Candle:

Go to Settings → Style tab

Wick section:

Select Color 2 and Color 3 → Set Opacity to 100%.

Border section:

Select Color 2 and Color 3 → Set Opacity to 100%.

✅ This ensures the candles display with full visibility and accurate colors.

⚙️ 🔥 CUSTOMIZATION OPTIONS 🔥:

Emperor RSI Candle offers full flexibility to match your trading style:

✅ RSI Length:

Modify the period used for RSI calculation (default: 10).

✅ Top & Bottom Levels:

Adjust the overbought (default: 80) and oversold (default: 20) thresholds.

✅ Intermediate Levels:

Up Level: Default: 60 → Bullish RSI threshold.

Down Level: Default: 40 → Bearish RSI threshold.

Mid Level: Default: 50 → Neutral zone.

✅ RSI Source:

Select the price source for RSI calculation (Close, Open, High, Low).

✅ RSI Period:

Customize the RSI calculation period (default: 10).

✅ Font Size:

Adjust the RSI box font size for better visibility.

✅ Box Position:

Choose where to display the RSI box:

Top Left / Top Center / Top Right

Bottom Left / Bottom Center / Bottom Right

💡 🔥 HOW IT IMPROVES TRADING 🔥:

✅ Clear trend identification:

Instantly recognize bullish, bearish, or neutral conditions through candle colors.

✅ Precise entries and exits:

Spot overbought and oversold zones with visual clarity.

✅ Multi-timeframe confirmation:

Validate trades with RSI confluence across multiple timeframes.

✅ No lag, real-time accuracy:

Immediate visual signals for faster and more reliable trade decisions.

✅ Customizable settings:

Tailor the indicator to fit your trading strategy and preferences.

✅ Works for all trading styles:

Suitable for scalping, day trading, and swing trading.

🔥How Traders Can Use Emperor RSI Candle for Trading:

🟢 Green Candles (Above 60 RSI) → Bullish Momentum:

Indicates strong upward movement → Ideal for long entries.

Traders can hold until RSI approaches 80 for profit booking.

🟥 Red Candles (Below 40 RSI) → Bearish Momentum:

Signals strong downward movement → Ideal for short trades.

Traders can exit or book profits near RSI 20.

2. Spotting Overbought and Oversold Zones for Reversals:

🟩 Parrot Green Candles (Above 80 RSI) → Overbought Zone:

Indicates potential for reversals or profit booking.

Traders can tighten stop-losses or exit positions.

🔵 Blue Candles (Below 20 RSI) → Oversold Zone:

Signals a potential reversal opportunity.

Traders can look for buy signals with confluence confirmation.

3. Catching Weak Bullish and Bearish Trends with Border Colors:

🟢 Green Border (RSI 50-60) → Weak Bullishness:

Indicates mild upward momentum.

Traders can consider cautious long entries.

🔴 Red Border (RSI 40-50) → Weak Bearishness:

Indicates mild downward pressure.

Traders can consider cautious short entries.

4. Using the RSI Multi-Timeframe Box for Confluence:

✅ Displays RSI values from 1 min to monthly timeframes.

Usage:

Confluence confirmation:

Multiple timeframes showing bullish RSI → Strong uptrend → Reliable buy signals.

Multiple timeframes showing bearish RSI → Strong downtrend → Reliable sell signals.

Spotting divergences:

If lower timeframes are bullish but higher timeframes are bearish, it indicates a potential reversal.

5. Customization Tips for Different Trading Styles:

✅ For Scalping:

Use a smaller RSI period (9-10) for faster signals.

Check the multi-timeframe RSI box to confirm signals quickly.

✅ For Swing Trading:

Use the default RSI period (14-15) for more accurate signals.

Focus on higher timeframes (1 hr, 4 hr, daily) for stronger trend confirmation.

Enhanced Bar Count IndicatorThe Enhanced Bar Count Indicato r is a versatile tool designed for traders who follow price action methodologies, particularly those inspired by Al Brooks. Built for TradingView and optimized for 5-minute charts during Regular Trading Hours, this indicator combines bar counting with multiple analytical features to help traders identify key market moments, trends, and potential reversal points. While it excels on intraday timeframes, its customizable settings make it adaptable to various trading styles and timeframes.

Key Features

Bar Counting and Diamond Placement

At its core, the indicator numbers each bar starting from the beginning of the trading day, helping traders keep track of bar sequences without manual counting. It highlights specific bars—such as the 7th, 18th, 40th, 48th, 67th, and 73rd bars—with colored diamonds. These bars are significant in Al Brooks’ trading approach for identifying potential reversals or key price action setups:

Bar 7 (Purple Diamond): Occurring around 35 minutes into the session, this bar often marks the end of the initial market open phase, signaling potential opening reversals or the formation of double tops/bottoms.

Bar 18 (Green Diamond): Statistically significant for marking the high or low of the day, making it a critical point for assessing potential trend reversals.

Bar 40 (Red Diamond): Positioned around midday, this bar is often associated with reversal opportunities as the market shifts from morning to afternoon trading.

Bar 48 (Purple Diamond): Around 11:50 AM EST, this bar signals the start of the afternoon swing setup, offering opportunities for midday swing trades.

Bar 67 (Purple Diamond): Appearing in the last hour (around 2:35 PM EST), this bar is key for late-day swing setups, often used for end-of-day strategies like buy-the-close or sell-the-close.

Bar 73 (Purple Diamond): Tied to a 12:30 PM PDT (3:30 PM EST) setup, this bar is significant for US market traders as a late-session decision point for trend continuation or reversal.

This feature allows traders to spot these critical bars at a glance, aligning with Al Brooks’ methodology for intraday trading.

Customizable 10-Period EMA for Scalping

A customizable 10-period Exponential Moving Average (EMA) is included to help scalpers quickly assess short-term trends. By default, it’s set to 10 periods, but users can adjust both the period and color to suit their strategy. When the price is above the EMA, it suggests an uptrend; below it, a downtrend. Scalpers can use pullbacks to the EMA as potential entry points in the direction of the trend. While optimized for 2-minute charts, it also provides valuable context on 5-minute charts for intraday traders.

Multi-Timeframe 20-Period EMAs

To provide a broader trend perspective, the indicator plots 20-period EMAs from three different timeframes—5-minute, 15-minute, and 60-minute—directly on the chart. This allows traders to see how the trend aligns across multiple timeframes, which is crucial for confirming the strength and direction of a move. Each EMA is toggleable and color-coded:

Green for 5m

Orange for 15m

Red for 60m

For instance, if all three EMAs are sloping upwards, it reinforces a strong uptrend, increasing the probability of successful trades in that direction.

Inside/Outside Bar Detection

The indicator automatically detects and marks inside bars with an 'i' and outside bars with an 'O' above the respective bars. Inside bars (where the high is lower than the previous high and the low is higher than the previous low) often signal consolidation and potential breakouts. Outside bars (where the high is higher and the low is lower than the previous bar) indicate increased volatility and possible trend reversals or continuations. These markers help traders quickly spot these patterns, which are essential for timing entries and exits in both range-bound and trending markets.

50% Pullback Retracement

Dynamic support and resistance levels are provided through the 50% retracement (midpoint) of the current and previous day’s price ranges. These levels are plotted as horizontal lines:

A solid line for the current day’s midpoint.

A dashed line for the previous day’s midpoint.

The lines are color-coded—green if below the current price and red if above—helping traders visualize potential reversal or continuation zones. This feature aligns with Fibonacci retracement principles and is particularly useful for intraday traders looking to identify areas where price might stall or reverse.

Customization and Usage

All features in the indicator are toggleable, allowing traders to enable or disable them based on their preferences. The settings are organized into groups—such as 'Bar Counting,' '10 EMA Scalp,' and 'Multi-Timeframe EMAs'—for easy navigation. This flexibility ensures that the indicator can be tailored to various trading styles, from scalping to swing trading. Traders can experiment with different combinations of features to find what works best for their strategy.

The Enhanced Bar Count Indicator is a comprehensive tool that brings together bar counting, trend analysis, pattern recognition, and dynamic support/resistance levels. Inspired by Al Brooks’ price action methodology, it offers traders a multifaceted approach to analyzing the markets. With its customizable and toggleable features, it adapts to different trading styles and timeframes, making it a valuable addition to any trader’s toolkit. Best of all, it’s available for free to the TradingView community—feel free to explore, customize, and integrate it into your trading strategy.

ICT Concepts [SB]ICT Market Structure Shift (MSS) Alert Indicator

This indicator identifies Market Structure Shifts (MSS) based on ICT concepts, helping traders spot key reversal or continuation points in price action.

Features:

✅ Detects bullish and bearish MSS using swing highs and swing lows.

✅ Customizable lookback period to fine-tune structure identification.

✅ Alerts for confirmed MSS when price breaks structure with momentum.

✅ Option to filter MSS by higher timeframe bias for confluence.

✅ Highlights liquidity sweeps before a shift to confirm smart money activity.

✅ Works on all timeframes and asset classes, including Forex, Stocks, Crypto, and Futures.

How It Works:

Bullish MSS: Occurs when price breaks above a recent swing high after taking out a previous swing low (liquidity grab).

Bearish MSS: Occurs when price breaks below a recent swing low after taking out a previous swing high.

Can be used standalone or combined with FVGs, Order Blocks, and Premium/Discount zones for high-probability setups.

Best Usage:

Scalping: 1m–5m timeframe for intraday reversals.

Intraday Trading: 15m–1H for session-based structure shifts.

Swing Trading: 4H–Daily for macro trend reversals.

Look for retest of MSS for entries after they fail as appears in chart highlighted by green horizontal lines or FVG to support after shifts.

Perfect for traders who use ICT, Smart Money Concepts (SMC), and Market Structure-based strategies.

CandelaCharts - Fractal Range Model📝 Overview

The Fractal Range Model (FRM) is an all-encompassing and sophisticated trading framework that incorporates multiple market dynamics to provide a deeper understanding of price movements.

This model is built around several key principles, including Market Swing Points, Sweeps, Candle Mean, and Change in State of Delivery (CISD), which together offer a nuanced and effective approach to trading.

At its core, the model focuses on Market Swing Points, which represent crucial turning points in the market where price action shifts direction.

These points provide insight into potential reversals and momentum changes, allowing traders to identify key support and resistance areas.

Recognizing these swings is critical in anticipating future price movements and understanding the market’s underlying structure.

The Fractal Range Model (FRM) is a versatile trading strategy that adapts to various styles, whether you're into scalping, day trading, swing trading, or long-term investment. Its flexibility makes it suitable for traders with different time horizons and risk preferences, allowing it to be effectively applied across multiple market conditions.

📦 Features

Timeframe Alignment: This indicator reveals lower Timeframe movements within higher Timeframe candles, offering insights into micro trends, structure shifts, and key entry points.

Bias Selection: This feature lets analysts control bias and setup detection, viewing bullish, bearish, or neutral formations to align with higher Timeframe trends.

Double Purge Sweeps: A double purge is a type of Sweep where the price exceeds both the high and low of the previous candle (via wicks) and then closes within the range of the prior candle.

Time Filters: Sync Time and price by selecting custom Time windows to focus on relevant formations.

Higher Timeframe Candles: The Fractal Range Model integrates ICT Power of Three, helping traders spot key turning points and market transitions across Timeframes.

Higher Timeframe PD Arrays: The HTF PD Arrays (FVG, IFVG) are key points of interest that indicate significant market levels where valid sweeps are likely to occur.

Lower Timeframe PD Arrays: The LTF PD Arrays (FVG, IFVG), on the other hand, are used for identifying entry points.

Smart Money Technique: In the context of the Fractal Range Model (FRM), the SMT (Smart Money Technique) serves as a crucial confluence indicator that strengthens the reliability of a formed model.

Info Panel: Display a customizable table with key details like timeframe pairing, time to next candle close, bias, and time filter settings, with full control over size, location, and borders.

Suitable for any Market: Ideal for all markets - stocks, forex, crypto, futures, commodities and more - delivering consistent results and insights across diverse trading environments.

⚙️ Settings

Core

Status: Filter models based on status

Bias: Controls what model type will be displayed, bullish or bearish

Fractal: Controls the timeframe pairing will be used

Mean: Plots the equilibrium of the previous HTF candle

Liquidity: Displays the liquidity levels that belongs to the model

Sweep: Shows the sweep that forms a model

I-sweep: Controls the visibility of invalidated sweeps

D-purge: Plots the double purge sweeps

CISD: Displays the Change In State of Delivery for a model

Labels: Adjust the HTF candle label size

C-area: Highlights the region between current candle open and previous candle equilibrium

History

History: Controls the mount of past models displayed on the chart

Filters

Asia: Filter models based on Asia Killzone hours

London: Filter models based on London Killzone hours

NY AM: Filter models based on NY AM Killzone hours

NY Launch: Filter models based on NY Launch Killzone hours

NY PM: Filter models based on NY PM Killzone hours

Custom: Filter models based on user Custom hours

HTF

Candles: Controls the number of HTF candles that will be visible on the chart

Open: Highlights with a line the open price of current HTF candle

Show True Day Open: Display True Day Open line

Offset: Controls the distance of HTF from the current chart

Space: Controls the space between HTF candles

Size: Controls the size of HTF candles

PD Array: Displays ICT PD Arrays

CE Line: Style the equilibrium line of PD Array

Border: Style the border of PD Array

LTF

H/L Line: Displays on the LTF chart High and Low of each HTF candle

O/C Line: Displays on the LTF chart Open and Close of each HTF candle

PD Array: Displays ICT PD Arrays

CE Line: Style the equilibrium line of PD Array

Border: Style the border of PD Array

Projections

StDev: Controls standard deviation available levels

Labels: Controls the size of standard deviation levels

Anchor: Controls the anchor point of standard deviation levels (wick, body)

Lines: Controls the line widths and color of standard deviation levels

SMT

Show: Display SMT

Symbol: Symbol 1

Symbol: Symbol 2

Style: Controls the color of Bearish and Bullish SMTs

Dashboard

Panel: Display information about current model

💡 Framework

The model includes the following timeframe parings:

15s - 5m

1m - 15m

1m - 30m

2m - 20m

3m - 30m

3m - 60m

5m - 1H

15m - 4H

15m - 8H

30m - 9H

30m - 12H

1H - 1D

2H - 2D

3H - 3D

4H - 1W

8H - 2W

12H - 3W

1D - 1M

2D - 2M

1W - 3M

2W - 6M

3W - 9M

1M - 12M

The Fractal Range Model follows a specific lifecycle, which highlights the current state of the model and determines whether a trade opportunity is valid.

The model's lifecycle includes the following statuses:

Formation (grey)

Invalidation (red)

Success (green)

1. Formation

The Formation phase marks the initial setup of the Fractal Range Model. During this stage, the model identifies and plots key components, such as:

Sweeps: Market movements that indicate a potential reversal or strong shift in trend.

CISD (Change In State of Delivery): A structural change that provides insight into trend shifts.

Once these components are detected, the model automatically calculates and displays Projections and Liquidity Levels , offering insights into potential price action movements.

At this stage, the model also identifies and displays the following key elements:

HTF PD Arrays (Higher-Timeframe Price Delivery Arrays)

LTF PD Arrays (Lower-Timeframe Price Delivery Arrays)

Smart Money Technique (SMT)

If any of these elements are present, they will be automatically displayed on the chart.

2. Invalidation

A Fractal Range Model is considered invalidated when the price does not reach the 2 Standard Deviation level or the first identified liquidity level, and when the price breaks above the high that formed the Sweep.

Invalidation signals that the original setup is no longer reliable, and traders should avoid taking action based on the model's original parameters.

Key invalidation conditions:

Price fails to reach the 2 Standard Deviation level.

Price fails to reach the first liquidity level.

Price breaks the high/low that initiated the Sweep.

A potentially invalidated model is marked with a purple color above the label, indicating the sweep is invalidated by the next candle, but not the high that formed the sweep.

3. Success

A Fractal Range Model is considered successful when the price reaches the 2 Standard Deviation level or the first identified liquidity level. This indicates that the model's predictions align with actual market movements, confirming the setup's validity and providing a potential trading signal.

At this stage, alongside Projections and Liquidity levels, you'll also notice the C-area — the region between the current candle's open and the previous candle's mean. If respected, price action will follow the model's direction.

Key success conditions:

Price reaches the 2 Standard Deviation level.

Price reaches the first liquidity level.

By leveraging these phases, Formation, Invalidation, and Success, traders can effectively manage their positions, minimize risk, and capitalize on high-probability setups based on the Fractal Range Model.

⚡️ Showcase

Introducing Fractal Range Model is a powerful trading tool designed to elevate your market analysis and boost your trading success. Built with precision and advanced algorithms, this indicator helps you identify key trends, potential entry and exit points, and optimize your strategy for better decision-making.

History

HTF Candles

HTF PD Arrays

LTF PD Arrays

SMT

Unlock your full trading potential and experience the difference with Fractal Range Model — your ultimate tool for smarter, more informed trading decisions.

🚨 Alerts

This script offers alert options for all model types. The alerts need to be setup manually from Tradingview.

Bearish Model

A bearish model alert is triggered when a model forms, signaling a high sweep and CISD.

Bullish Model

A bullish model alert is triggered when a model forms, signaling a low sweep and CISD.

⚠️ Disclaimer

These tools are exclusively available on the TradingView platform.

Our charting tools are intended solely for informational and educational purposes and should not be regarded as financial, investment, or trading advice. They are not designed to predict market movements or offer specific recommendations. Users should be aware that past performance is not indicative of future results and should not rely on these tools for financial decisions. By using these charting tools, the purchaser agrees that the seller and creator hold no responsibility for any decisions made based on information provided by the tools. The purchaser assumes full responsibility and liability for any actions taken and their consequences, including potential financial losses or investment outcomes that may result from the use of these products.

By purchasing, the customer acknowledges and accepts that neither the seller nor the creator is liable for any undesired outcomes stemming from the development, sale, or use of these products. Additionally, the purchaser agrees to indemnify the seller from any liability. If invited through the Friends and Family Program, the purchaser understands that any provided discount code applies only to the initial purchase of Candela's subscription. The purchaser is responsible for canceling or requesting cancellation of their subscription if they choose not to continue at the full retail price. In the event the purchaser no longer wishes to use the products, they must unsubscribe from the membership service, if applicable.

We do not offer reimbursements, refunds, or chargebacks. Once these Terms are accepted at the time of purchase, no reimbursements, refunds, or chargebacks will be issued under any circumstances.

By continuing to use these charting tools, the user confirms their understanding and acceptance of these Terms as outlined in this disclaimer.

MTF Fibonacci Pivots with Mandelbrot FractalsMTF Fibonacci Pivots with Mandelbrot Fractals: Advanced Market Structure Analysis

Overview

The MTF Fibonacci Pivots with Mandelbrot Fractals indicator represents a significant advancement in technical analysis by combining multi-timeframe Fibonacci pivot levels with sophisticated fractal pattern recognition. This powerful tool identifies key support and resistance zones while predicting potential price reversals with remarkable accuracy.

Key Capabilities

This indicator provides traders with three distinct layers of market structure analysis:

Automatic Timeframe Adaptation: The primary pivot set automatically adjusts to your chart's timeframe, ensuring relevant support and resistance levels for your specific trading horizon.

1-Year Fibonacci Pivots: The second layer displays yearly pivots that reveal long-term market cycles and institutional price levels that often act as significant reversal points.

3-Year Fibonacci Pivots: The third layer unveils major market structure zones that typically remain relevant for extended periods, offering strategic context for position trading and long-term investment decisions.

Predictive Technology

What truly distinguishes this indicator is its advanced predictive capability powered by:

Mandelbrot Fractal Pattern Recognition: The indicator implements a sophisticated fractal detection algorithm that identifies recurring price patterns across multiple timeframes. Unlike conventional fractal indicators, it incorporates noise filtering and adaptive sensitivity to market volatility.

Tesla's 3-6-9 Principle Integration: The system incorporates Nikola Tesla's mathematical principle through a cubic Mandelbrot equation (Z_{n+1} = Z_n^3 + C where Z_0 = 0), creating a unique approach to pattern recognition that aligns with natural market rhythms.

Historical Pattern Matching: When a current price pattern exhibits strong similarity to historical formations, the indicator generates predictive targets with confidence ratings. Each prediction undergoes rigorous validation against multiple parameters including trend alignment, volatility context, and mathematical coherence.

Visual Intelligence System

The indicator's visual presentation enhances trading decision-making through:

Confidence-Based Visualization: Predictions display with intuitive star ratings, percentage confidence scores, and contextual information including price movement magnitude and estimated time to target.

Adaptive Color Harmonization: The color system intelligently adjusts to provide optimal visibility while maintaining a professional appearance suitable for any chart setup.

Trend Alignment Indicators: Each prediction includes references to the broader trend context, helping traders avoid counter-trend trades unless the reversal signal carries exceptional strength.

Strategic Applications

This indicator excels in multiple trading scenarios:

Intraday Trading: Identify high-probability reversal zones with precise timing

Swing Trading: Anticipate significant market turns at key structural levels

Position Trading: Recognize major cycle shifts for strategic entry and exit

The automatic 1-year and 3-year Fibonacci pivots provide institutional-grade reference points that typically define major market movements. These longer timeframes reveal critical zones that might be invisible on shorter-term analysis, giving you a significant edge in understanding where price is likely to encounter substantial buying or selling pressure.

This innovative approach to market analysis combines classical Fibonacci mathematics with cutting-edge fractal theory to create a comprehensive market structure visualization system that illuminates both present support/resistance levels and future price targets with exceptional clarity.

Setting Up MTF Fibonacci Pivots with Mandelbrot Fractals

Initial Setup

Adding this indicator to your TradingView charts is straightforward:

Navigate to the "Indicators" button on your chart toolbar

Search for "MTF Fibonacci Pivots with Mandelbrot Fractals"

Select the indicator to add it to your chart

A configuration panel will appear with various setting categories

Recommended Settings

The indicator comes pre-configured with optimal default settings, but you may want to adjust them based on your trading style:

For Day Trading (Timeframes 1-minute to 1-hour)

Pivots Timeframe 1: Auto (automatically adapts to your chart)

Pivots Timeframe 2: Daily

Pivots Timeframe 3: Weekly

Fractal Sensitivity: 2-3

Fractal Lookback Period: 20

Prediction Strength: 2

Color Theme: High Contrast or Dark Mode

For Swing Trading (Timeframes 4-hour to Daily)

Pivots Timeframe 1: Daily

Pivots Timeframe 2: Weekly

Pivots Timeframe 3: Monthly

Fractal Sensitivity: 1-2

Fractal Lookback Period: 30

Prediction Strength: 2-3

Color Theme: Default or Dimmed

For Position Trading (Timeframes Daily to Weekly)

Pivots Timeframe 1: Weekly

Pivots Timeframe 2: Monthly

Pivots Timeframe 3: Quarterly

Fractal Sensitivity: 1

Fractal Lookback Period: 50

Prediction Strength: 1

Color Theme: Monochrome or Pastel

Restoring Default Settings

If you've adjusted settings and wish to return to the defaults:

Right-click on the indicator name on your chart

Select "Settings" from the context menu

In the settings dialog, look for the "Reset All" button at the bottom

Confirm the reset when prompted

Alternatively, you can remove the indicator and add it again for a fresh start with default settings.

Advanced Settings Guidance

Visual Appearance

Use Gradient Colors: Enable for better visual differentiation between pivot levels

Color Transparency: 15% provides an optimal balance between visibility and chart clutter

Line Width: 1-2 for cleaner charts, 3+ for enhanced visibility

Fractal Analysis

Enable Fractal Analysis: Keep enabled for prediction capabilities

Fractal Box Spacing: Higher values (5-10) for cleaner displays, lower values (1-3) for more signals

Maximum Forecast Bars: 20 is optimal for most timeframes, adjust higher for longer predictions

Performance Considerations

Enable Self-Optimization: Keep enabled to maintain smooth chart performance

Resource Priority: Use "Balanced" for most computers, "Performance" for older systems

Force Pivot Display: Enable only when checking specific historical periods

Common Setup Mistakes to Avoid

Setting all timeframes too close together (e.g., Daily, Daily, Weekly) reduces the multi-timeframe advantage

Using high fractal sensitivity (4+) on noisy markets creates excessive signals

Setting fractal box spacing too low causes cluttered prediction boxes

Disabling self-optimization may cause performance issues on complex charts

Using incompatible color themes for your chart background reduces visibility

The indicator's power comes from its default 1-year and 3-year Fibonacci pivot settings, which highlight institutional levels while the auto-timeframe setting adapts to your trading horizon. These carefully balanced defaults provide an excellent starting point for most traders.

For optimal results, I recommend making minimal adjustments at first, then gradually customizing settings as you become familiar with the indicator's behavior in your specific markets and timeframes.

Screenshots:

EBP Candle Marker### **EBP Candle Marker – TradingView Indicator**

The **EBP Candle Marker** is a specialized TradingView indicator designed to identify and highlight potential liquidity sweep candles. This indicator visually emphasizes key price action patterns where the market sweeps previous highs or lows and closes in the opposite direction, often signaling potential reversals or liquidity grabs.

---

### 📊 **Indicator Logic:**

1. **Bullish Sweep:**

- The current candle’s **low** is lower than the previous candle’s **low** (indicating a liquidity sweep).

- The **close** is above both the **open** and **close** of the previous candle.

2. **Bearish Sweep:**

- The current candle’s **high** is higher than the previous candle’s **high** (indicating a liquidity sweep).

- The **close** is below both the **open** and **close** of the previous candle.

---

### 🎨 **Visual Representation:**

- **Yellow Candle Body:** Highlights any candle meeting the bullish or bearish sweep conditions.

---

### 🔔 **Alert Functionality:**

The indicator supports setting custom alerts in TradingView for:

- **Bullish Sweep Detected** – Notifies when a bullish sweep occurs.

- **Bearish Sweep Detected** – Notifies when a bearish sweep occurs.

These alerts are compatible across any timeframe, providing flexibility to monitor key market conditions.

---

### 📈 **Use Cases:**

- **Liquidity Sweep Detection:** Identify areas where the market may be triggering stop-loss orders or liquidity hunts.

- **Reversal Confirmation:** Enhance trade confirmation by identifying potential reversal zones.

- **Scalping & Swing Trading:** Suitable for both short-term and long-term trading strategies across multiple timeframes.

Pipnotic Supply and DemandDescription

The Pipnotic Supply and Demand Indicator was originally developed in 2011 for another trading platform and is currently being rewritten for TradingView due to user demand. It is a powerful tool designed for traders who utilize supply and demand concepts in technical analysis. This script automatically detects and highlights key supply and demand zones (as well as buy and sell zones) on the chart, enabling traders to identify potential reversal points, trend continuations, and price imbalances. We will continue to actively develop this indicator for existing and this new version for TradingView.

How It Works

The indicator follows a structured methodology to analyse price action and identify high-probability supply and demand zones:

Zone Identification:

Detects accumulation and distribution phases using volatility and range conditions.

Identifies zones where price imbalances occur, signalling potential trading opportunities.

Expansion and Confirmation:

Assesses whether the price expands away from a zone significantly enough to validate it as a supply or demand zone.

Uses a risk-to-reward ratio to ensure zones meet predefined trading criteria, adjustable via the configuration.

Visualization and Management:

Plots supply (bearish) and demand (bullish) zones directly on the chart.

Labels the percentage of expansion from the zone, giving traders insights into the strength of the imbalance.

Updates zones dynamically, marking tested and consumed levels and preventing outdated information from cluttering the chart.

Key Features & Inputs

Customizable Zone Display: Traders can adjust the maximum number of supply and demand zones shown on the chart.

Dynamic Volatility Sampling: Uses the ATR (Average True Range) to adapt to changing market conditions.

Flexible Risk Management: Allows traders to define a minimum zone size and a risk-to-reward ratio for filtering zones.

Enhanced Visualization:

Adjustable colours for bullish and bearish zones.

Configurable border width for zone clarity.

Optional display of consumed zones to avoid redundant signals, but to also identify price sensitive zones on the flip side of the book when zones are consumed.

Swing Significance Detection: Enables boxing of significant price swings to refine the accuracy of identified zones.

Benefits of Using the Pipnotic Supply and Demand Indicator

Automates Supply and Demand Analysis: Eliminates the need for manual zone drawing, saving time and reducing subjectivity.

Enhances Trade Decision-Making: By providing precise entry and exit points based on supply and demand principles, traders can optimize their strategies.

Adapts to Market Conditions: The indicator dynamically adjusts to price movements, ensuring relevant zones are displayed.

Works Across All Timeframes: Suitable for scalping, swing trading, and long-term investing.

Compatible with Multiple Trading Strategies: Can be used alongside trend-following, breakout, and reversal strategies for improved trade confirmation.

MTF Fractals [RunRox]🔽 MTF Fractals is a powerful indicator designed to visualize fractals from multiple timeframes directly on your chart, highlight liquidity sweeps at these fractal levels, and provide several additional features we’ll cover in detail below.

We created this indicator because we couldn’t find a suitable tool that met our specific needs on TradingView. Therefore, we decided to develop a valuable indicator for the entire TradingView community, combining simplicity and versatility.

⁉️ WHAT IS A FRACTALS?

In trading, a fractal is a technical analysis pattern composed of five consecutive candles, typically highlighting local market turning points. Specifically, a fractal high is formed when a candle’s high is higher than the highs of the two candles on either side, whereas a fractal low occurs when a candle’s low is lower than the lows of the two adjacent candles on both sides.

Traders use fractals as reference points for identifying significant support and resistance levels, potential reversal areas, and liquidity zones within price action analysis. Below is a screenshot illustrating clearly formed fractals on the chart.

📙 FRACTAL FORMATION

Here’s how fractals form depending on your chosen setting (3, 5, 7, or 9):

▶️ 3-bar fractal – forms when the central candle is higher (for highs) or lower (for lows) than one candle on each side.

▶️ 5-bar fractal – forms when the central candle is higher or lower than two candles on both sides.

▶️ 7-bar fractal – forms when the central candle is higher or lower compared to the three candles on each side.

▶️ 9-bar fractal – forms similarly but requires four candles on each side, making the fractal significantly more reliable and robust.

A higher number of bars ensures stronger fractal levels, highlighting more significant potential reversal points on the chart.

Now that we’ve covered the theory behind fractal formation, let’s explore the indicator’s functionality in more detail.

Below, I’ll explain each feature clearly and illustrate how you can effectively utilize this indicator in your trading.

🕐 MULTI-TIMEFRAME FRACTALS

We realized that displaying fractals only from the current timeframe isn’t always convenient, so we’ve introduced Multi-Timeframe Fractals into this indicator.

Now you can easily display fractals from higher timeframes directly on your current chart, providing you with broader market context and clearer trading signals.

Fractals from Current Timeframe – Fractals identified directly on the chart’s current timeframe.

Fractals from Higher Timeframes – Fractals sourced from higher timeframes and displayed clearly on your current chart for enhanced market perspective.

📈 FRACTAL LINES

Since fractals represent areas of high liquidity, we’ve added an option to extend fractal levels horizontally as Fractal Lines across your chart.

This feature allows you to clearly visualize critical liquidity areas from higher timeframes, directly on your current timeframe chart, as demonstrated in the screenshot below.

With this approach, you can clearly visualize significant fractal levels from higher timeframes directly on your current chart - for example, projecting fractals from the 1-hour (1H) timeframe onto a 3-minute (3m) chart. ✅ This helps you easily identify critical liquidity areas and potential reversal zones without the need to switch between multiple timeframes.

💰 LIQUDITY SWEEP (LIQUDITY GRAB)

To enhance your trading experience, we’ve introduced a feature that clearly identifies liquidity sweeps of fractal levels.

A Liquidity Sweep occurs when a candle closes beyond a fractal line, leaving a wick that pierces through it, signaling that liquidity has been collected at this level.

Below, you’ll find two examples illustrating this functionality:

▶️ Fractal lines from the current timeframe

▶️ Fractal lines projected from higher timeframes

The first example illustrates liquidity being swept from fractals on the current timeframe .

Here, the candle clearly closes beyond the fractal line, leaving a wick through it. This indicates a liquidity sweep at the fractal level, visually highlighting a potential reversal or continuation opportunity directly on your chart.

In the second example, fractals from the higher timeframe are projected onto your current chart.

When a candle on your current timeframe closes beyond an HTF fractal line - leaving a wick through this level - the indicator highlights it clearly. This signals to traders a potential reversal zone, indicating that liquidity has been swept, and price may reverse or significantly react from this area.

You can also enable the display of additional labels on the chart. These labels clearly mark liquidity sweeps at fractal levels, making it easier to visually identify potential reversal points directly on your chart.

⚙️ SETTINGS

Below are the indicator settings with detailed explanations for each parameter.

🔷 Bars in Fractal – Number of candles to the right and left required to form a fractal.

🔷 Fractal Timeframe – Select the timeframe from which you want to display fractals on the current chart.

🔷 Max Age, bars – Number of bars during which the fractal will remain active.

🔷 Show Fractal Line – Display or hide fractal lines.

🔷 Line Style – Choose the style of the line displayed on the chart.

🔷 Line Width – Thickness of the fractal line.

🔷 High Fractal – Style and color of bearish fractals.

🔷 Low Fractal – Style and color of bullish fractals.

🔷 Fractal Label Size – Select the size of fractal labels.

🔷 Show Sweep Labels – Option to display labels when a liquidity sweep occurs.

🔷 Label Color – Color and transparency of the area marked on the chart during a sweep.

🔷 Shade Sweep Area – Show or hide the sweep area shading.

🔷 Area Color – Color and transparency settings for the sweep area.

🔶 We’d love to hear your feedback and any suggestions for additional features you’d like to see in this indicator. We’ll be happy to consider your ideas and continue improving the indicator!

GRID EXTENSIONGRID EXTENSION

Overview

The GRID EXTENSION is a simple grid-based indicator for TradingView, built with Pine Script v6. It plots horizontal price levels starting from a user-defined anchor price, with spacing set by a tick increment. Use it to identify key support, resistance, or price zones on charts for Crypto, Forex, or Futures.

Key Features

Custom Grid Levels: Plot up to 22 levels (e.g., 0, 0.25, 1.25, -2.50) with options to show/hide, set values, and choose colors.

Market-Specific Tick Increments: Select your asset type (Crypto, Forex, Futures) and choose from a range of tick increments tailored for each market:

Crypto: 1 to 5000 ticks (e.g., 100 ticks = $0.001 on ADA/USD, 5000 ticks = $50 on BTC/USD).

Forex: 5 to 5000 ticks (e.g., 100 ticks = 1 pip on EUR/USD, 5000 ticks = 50 pips).

Futures: 1 to 2500 ticks (e.g., 25 ticks = 6.25 points on E-mini S&P 500, $312.50 per contract).

Visual Options:

Extend lines to the right.

Show price and level labels (as values or percentages).

Place labels on the left or right.

Adjust background transparency for filled areas between levels.

How to Use

Set Asset Type: Choose "Crypto," "Forex," or "Futures" to match your chart.

Set Anchor Price: Enter a starting price for the grid.

Pick Tick Increment: Select a tick increment from the dropdown, following the guidance for your asset type (see Key Features).

Customize Levels: Turn levels on/off, set values, and pick colors.

Add to Chart: Apply the indicator to see the grid on your chart.

Tips

Use levels to mark support/resistance zones for entries or exits.

Extend lines to project future price zones.

Choose smaller increments (e.g., 5 ticks) for scalping, or larger ones (e.g., 1000 ticks) for swing trading.

Combine with indicators like moving averages for better signals.

Settings

Asset Type: Select "Crypto," "Forex," or "Futures" (default: "Crypto").

Anchor Price: Starting price for the grid (default: 0.0).

Tick Increment: Space between levels (options: 1, 5, 10, 25, 50, 100, 250, 500, 1000, 2500, 5000). Choose based on asset type.

Extend Right: Extend lines to the right (default: true).

Show Prices: Show price labels (default: true).

Show Levels: Show level values or percentages (default: true).

Format: Display levels as "Values" or "Percent" (default: "Values").

Labels Position: Place labels on "Left" or "Right" (default: "Left").

Background Transparency: Set transparency for filled areas (default: 100, range 0-100).

Level Options: Enable/disable levels, set values, and choose colors.

Notes

Set the anchor price to a key level (like a recent high or low) for best results.

Check the tick increment tooltip to ensure the spacing suits your market type.

Works on any chart, best for clear price trends or ranges.

Acknowledgments

Made with Pine Script v6 for TradingView. This is v1.0—feedback welcome for future updates!

Vortex Sniper Elite @DaviddTechVortex Sniper Elite @DaviddTech

Vortex Sniper Elite @DaviddTech is a comprehensive trading system designed to deliver high-probability trade setups across all market conditions. By seamlessly integrating adaptive baseline detection, squeeze momentum analysis, and advanced vortex filtering, this indicator provides traders with a complete edge-based approach to market analysis.

🔥 Key Features:

Complete Model Integration:

Baseline: Advanced McGinley Dynamic indicator for superior trend detection

Confirmation #1: Enhanced TTM Squeeze for momentum and volatility analysis

Confirmation #2: Dual Tether Line system for dynamic market structure mapping

Volatility Filter: Specialized Vortex indicator for precision entry timing

Adaptive Stop Loss: Proprietary trailing stop system based on ATR calculations

Advanced Visual Dashboard:

Real-time component analysis with strength metrics

Color-coded signal status for immediate trade assessment

Squeeze state monitoring with visual confirmation

Vortex divergence strength percentage for optimal entries

Premium Signal Detection:

Multi-timeframe compatible system for scaling strategies

Automated buy/sell signals at optimal entry points

Clear exit signals for risk management

Squeeze momentum visualization for timing precision

DaviddTech Alpha Edge System:

Gradient transparency algorithm for visual trend strength confirmation

Bar coloring system based on momentum direction

Background highlighting for active signal states

Dashboard for ease of understanding

💰 Trading Applications:

Sniper Entries: Utilize the Vortex confirmation to pinpoint precise entry points

Trend Alignment: McGinley baseline establishes the primary market direction

Volatility Awareness: TTM Squeeze identifies optimal market conditions

Risk Management: Set stops based on the adaptive trailing stop system

Position Management: Monitor dashboard metrics for changing market conditions

Vortex Sniper Elite @DaviddTech represents the culmination of the DaviddTech methodology in one cohesive system. Whether you're a day trader seeking precise entries or a swing trader looking for significant market moves, this indicator delivers the structured approach needed to consistently extract profits from any market condition.

DaviddTech Trading System Explained:

The DaviddTech methodology follows a strict component-based approach:

The Baseline establishes the primary trend direction, acting as your first filter

Confirmation Indicators validate potential trade setups only when aligned with the baseline

The Volatility/Volume Indicator ensures you only enter trades with sufficient directional momentum

A Trailing Stop System provides mathematically optimized exit points

Vortex Sniper Elite integrates all these components into a visually intuitive system that eliminates guesswork and enforces disciplined trading decisions.

Recommended Settings:

This indicator comes pre-configured with optimized parameters, but feel free to adjust based on your timeframe:

For day trading: Reduce Baseline and TTM lengths by 30-40%

For swing trading: Consider increasing Tether and Trail Stop lengths by 25-50%

For scalping: Focus on Vortex confirmation with shorter timeframes

Best Practices:

Wait for all components to align before entering trades

Use the dashboard to evaluate the strength of each signal

Monitor squeeze states for potential volatility expansion

Let the trailing stop system handle your exits

Backtest across multiple timeframes to find your optimal settings

High Timeframe POCIntroducing the High Timeframe POC (HTF POC) Indicator

What It Does

The HTF POC Indicator is a powerful tool that helps traders identify key price levels on your chart based on the Point of Control (POC)—the price level where the most trading activity (volume or time) occurred over a specific timeframe. Think of it as a "magnet" where price tends to return or bounce off. This indicator works across multiple timeframes (1-hour, 4-hour, 6-hour, weekly, monthly, and custom periods like 3M or 6M), giving you a clear view of significant support and resistance levels from both short-term and long-term perspectives.

Key Features:

Displays POC lines for different timeframes (e.g., 1H, 4H, 6H) as horizontal lines on your chart.

Limits the number of lines per timeframe (default 5, adjustable) to avoid clutter.

Allows customizable line lengths (e.g., 1 day for 1H, 7 days for 6H) and label positioning to keep your chart clean.

Highlights developing POCs (current price action) and optional Value Area (VA) levels for added context.

Removes crossed POC lines automatically to focus on relevant levels.

Why It Matters

Traders use POCs because they act as support (price floor) or resistance (price ceiling) zones. By seeing POCs from multiple timeframes, you can:

Spot where price is likely to reverse or consolidate.

Align your trades with both short-term (1H, 4H) and longer-term (6H, monthly) trends.

Avoid overcomplicating your chart with too many lines, thanks to customizable settings.

How to Use It

Here are practical ways to leverage the HTF POC Indicator in your trading:

Identify Entry and Exit Points:

Look for price approaching a POC line (e.g., a 4H POC in green). If price bounces off this level, it’s a potential buy (support) or sell (resistance) signal.

Example: If the 1H POC is near current price and price respects it, enter a trade in the direction of the bounce.

Combine Timeframes for Confirmation:

Use shorter timeframes (1H, 4H) for precise entries and longer timeframes (6H, monthly) for trend direction.

Example: If a 6H POC aligns with a monthly POC and price holds, it’s a stronger signal to trade in that direction.

Set Stop Losses and Targets:

Place your stop loss just beyond the POC level (e.g., 1-2% below a support POC).

Set your profit target at the next POC level (e.g., the next 4H POC above your entry).

Spot Reversal Zones:

Watch for price stalling or reversing at multiple POC alignments (e.g., 1H and 6H POCs stacking). This is a high-probability reversal zone.

Example: If price drops to a 1H POC and a 4H POC at the same level, consider it a key area to watch.

Adjust for Clarity:

Tweak the “Max lines to display” (e.g., set 1H to 3 lines) and “Line length” (e.g., 1 day for 1H) in the settings to focus on the most recent and relevant levels.

Move labels (left for 1H, right for 6H) to avoid overlap and keep your chart readable.

Quick Tips

Enable Timeframes: Turn on 1H, 4H, or 6H based on your trading style (short-term or swing).

Color Coding: Red for 1H, Green for 4H, Blue for 6H—easy to distinguish on the chart.

Test It: Apply it on a daily chart and adjust settings to see how POCs align with past price action.

Get Started

Add the HTF POC Indicator to your TradingView chart, customize the settings to match your strategy, and watch how POC levels guide your trades. Whether you’re scalping or swing trading, this tool helps you stay ahead by highlighting where the market “remembers” its past!

AlgoCados x ICT ToolkitAlgoCados x ICT Toolkit is a TradingView tool designed to integrate ICT (Inner Circle Trader) Smart Money Concepts (SMC) into a structured trading framework.

It provides traders with institutional liquidity insights, precise price level tracking, and session-based analysis, making it an essential tool for intraday, swing, and position trading.

Optimized for Forex, Futures, and Crypto, this toolkit offers multi-timeframe liquidity tracking, killzone mapping, RTH analysis, standard deviation projections, and dynamic price level updates, ensuring traders stay aligned with institutional market behavior.

# Key Features

Multi-Timeframe Institutional Price Levels

The indicator provides a structured approach to analyzing liquidity and market structure across different time horizons, helping traders understand institutional order flow.

- Previous Day High/Low (PDH/PDL) – Tracks the Previous Day’s High/Low, crucial for intraday liquidity analysis.

- Previous Week High/Low (PWH/PWL) – Monitors the Previous Week’s High/Low, aiding in higher timeframe liquidity zone tracking.

- Previous Month High/Low (PMH/PML) – Highlights the Previous Month’s High/Low, critical for swing trading and long-term bias confirmation.

- True Day Open (TDO) – Marks the NY Midnight Opening Price, providing a reference point for intraday bias and liquidity movements.

- Automatic Level Cleanup – When enabled. pxHigh/pxLow levels gets automatically deleted when raided, keeping the chart clean and focused on valid liquidity zones.

- Monthly, Weekly, Daily Open Levels – Identifies HTF price action context, allowing traders to track institutional order flow and potential liquidity draws.

# Regular Trading Hours (RTH) High, Low & Mid-Equilibrium (EQ)

For futures traders, the toolkit accurately identifies RTH liquidity zones to align with institutional trading behavior.

- RTH High/Low (RTH H/L) – Defines the RTH Gap high and low dynamically, marking key liquidity levels.

- RTH Equilibrium (EQ) – Calculates the midpoint of the RTH range, acting as a mean reversion level where price often reacts.

# Killzones & Liquidity Mapping

The indicator provides a time-based liquidity structure that helps traders anticipate market movements during high-impact trading windows.

ICT Killzones (Visible on 30-minute timeframe or lower)

- Asia Killzone (Asia) – Tracks overnight liquidity accumulation.

- London Open Killzone (LOKZ) – Marks early European liquidity grabs.

- New York Killzone (NYKZ) – Captures US session volatility.

- New York PM Session (PMKZ) – Available only for futures markets, tracking late-day liquidity shifts.

Forex-Specific Killzones (Visible on 30-minute timeframe or lower)

- London Close Killzone (LCKZ) – Available only for Forex, marks the European end of Day liquidity Points of Interests (POI).

- Central Bank Dealers Range (CBDR) – Available only for Forex, providing a liquidity framework used by central banks.

- Flout (CBDR + Asian Range) – Available only for Forex, extending CBDR with Asian session liquidity behavior.

- Killzone History Option – When enabled, Killzones remain visible beyond the current day; otherwise, they reset daily.

- Customizable Killzone Boxes – Modify opacity, colors, and border styles for seamless integration into different trading styles.

CME_MINI:NQH2025 FOREXCOM:EURUSD

# Standard Deviation (STDV) Liquidity Projections

A statistical approach to forecasting price movements based on Standard Deviations of HOTD (High of the Day) and LOTD (Low of the Day).

- Asia, CBDR, and Flout STDV Calculations (Visible on 30-minute timeframe or lower) – Predicts liquidity grabs based on price expansion behavior.

- Customizable Display Modes – Choose between Compact (e.g., "+2.5") or Verbose (e.g., "Asia +2.5") labels.

- Real-Time STDV Updates – Projections dynamically adjust as new price data is formed, allowing traders to react to developing market conditions.

CME_MINI:NQH2025

# Daily Session Dividers

- Visualizes Trading Days (Visible on 1-hour timeframe or lower) – Helps segment the trading session for better structure analysis.

- Daily Divider History Option – When enabled, dividers remain visible beyond the current trading week; otherwise, they reset weekly.

# Customization & User Experience

- Flexible Label Options – Adjust label size, font type, and color for improved readability.

- Intraday-Optimized Data – Killzones (30m or lower), STDV (30m or lower), and Daily Dividers (1H or lower) ensure efficient use of chart space.

- Configurable Line Styles – Customize solid, dotted, or dashed styles for various levels, making charts aesthetically clean and data-rich.

# Usage & Configurations

The AlgoCados x ICT Toolkit is designed to seamlessly fit different trading methodologies.

Scalping & Intraday Trading

- Track PDH/PDL levels for liquidity sweeps and market reversals.

- Utilize Killzones & Session Open levels to identify high-probability entry zones.

- Analyze RTH High/Low & Mid-EQ for potential liquidity targets and reversals.

- Enable STDV projections for potential price expansion and reversals.

Swing & Position Trading

- Use PWH/PWL and PMH/PML levels to determine HTF liquidity shifts.

- Monitor RTH Gap, TDO, and session liquidity markers for trade confirmation.

- Combine HTF bias with LTF liquidity structures for optimized entries and exits.

# Inputs & Configuration Options

Customizable Parameters

- Offset Adjustment – Allows users to shift displayed data horizontally for better visibility.

- Killzone Box Styling – Customize colors, opacity, and border styles for session boxes.

- Session Dividers – Modify line styles and colors for better time segmentation.

- Killzone & Daily Divider History Toggle – Enables users to view past killzones and dividers instead of resetting them daily/weekly.

- Label Formatting – Toggle between Compact and Verbose display modes for streamlined analysis.

# Advanced Features

Real-Time Data Processing & Dynamic Object Management

- Auto Cleanup of pxLevels – Prevents clutter by removing invalidated levels upon liquidity raids.

- Session History Control – Users can toggle historical data for daily dividers and killzones to maintain a clean chart layout.

- Daily & Weekly Resets – Ensures accurate session tracking by resetting daily dividers at the start of each new trading week.

CME_MINI:NQH2025

# Example Use Cases

- Day Traders & Scalpers – Utilize Killzones, PDH/PDL, DO and TDO levels for precise liquidity-based trading opportunities.

- Swing Traders – Leverage HTF Open Levels, PWH/PWL liquidity mapping, and TDO for trend-based trade execution.

- Futures Traders – Optimize trading with RTH High/Low, Mid-EQ, and PMKZ for session liquidity tracking.

- Forex Traders – Use CBDR, Flout, and session liquidity mapping to align with institutional order flow.

CME_MINI:ESH2025

"By integrating institutional concepts, liquidity mapping, and smart money methodologies, the AlgoCados x ICT Toolkit empowers traders with a data-driven approach to market inefficiencies and liquidity pools."

# Disclaimer

This tool is designed to assist in trading decisions but should be used in conjunction with other analysis methods and proper risk management. Trading involves significant risk, and traders should ensure they understand market conditions before executing trades.

Advanced Support and Resistance Levels[MAP]Advanced Support and Resistance Levels Indicator

Author

Developed by:

Overview

The "Advanced Support and Resistance Levels" indicator, created, is a sophisticated tool designed for TradingView's Pine Script v6 platform. It identifies and plots key support and resistance levels on a price chart, enhancing technical analysis by incorporating pivot strength, volume weighting, and level decay. The indicator overlays lines, zones, and labels on the chart, providing a visual representation of significant price levels where the market has historically reversed or consolidated.

Purpose

This indicator, authored by , aims to:

Detect significant pivot points (highs and lows) with customizable strength requirements.

Track and rank support/resistance levels based on their recency, volume, and number of touches.

Display these levels as lines and optional zones, with strength-based visual cues (e.g., line thickness and opacity).

Offer flexibility through user-configurable settings to adapt to different trading styles and market conditions.

Features

Pivot Detection:

Identifies high and low pivots using a strength parameter, requiring a specified number of bars on either side where no higher highs or lower lows occur.

Incorporates closing price checks and SMA-based trend confirmation to filter out noise and ensure pivots align with the broader market direction.

Level Management:

Maintains a dynamic array of levels with attributes: price, type (support/resistance), bars since last touch, strength, and volume.

Merges nearby levels within a tolerance percentage, updating prices with a strength-weighted average.

Prunes weaker or older levels when exceeding the maximum allowed, prioritizing those with higher calculated strength.

Strength Calculation:

Combines the number of touches (strength), volume (if enabled), and age decay (if enabled) into a single metric.

Volume weighting uses a logarithmic scale to emphasize high-volume pivots without over-amplifying extreme values.

Age decay reduces the importance of older levels over time, ensuring relevance to current price action.

Visualization:

Draws horizontal lines at each level, with thickness reflecting the number of touches (up to a user-defined maximum).

Optional price zones around levels, sized as a percentage of the price, to indicate areas of influence.

Labels display the level type (S for support, R for resistance), price, and strength score, with position (left or right) customizable.

Line opacity varies with strength, providing a visual hierarchy of level significance.

Plots small triangles at detected pivot points for reference.

Inputs

Lookback Period (lookback, default: 20): Number of bars to consider for trend confirmation via SMA. Range: 5–100.

Pivot Strength (strength, default: 2): Number of bars required on each side of a pivot to confirm it. Range: 1–10.

Price Tolerance % (tolerance, default: 0.5): Percentage range for merging similar levels. Range: 0.1–5.

Max Levels to Show (maxLevels, default: 10): Maximum number of levels displayed. Range: 2–50.

Zone Size % (zoneSizePercent, default: 0.1): Size of the S/R zone as a percentage of the price. Range: 0–1.