Honest Volatility Grid [Honestcowboy]The Honest Volatility Grid is an attempt at creating a robust grid trading strategy but without standard levels.

Normal grid systems use price levels like 1.01;1.02;1.03;1.04... and place an order at each of these levels. In this program instead we create a grid using keltner channels using a long term moving average.

🟦 IS THIS EVEN USEFUL?

The idea is to have a more fluid style of trading where levels expand and follow price and do not stick to precreated levels. This however also makes each closed trade different instead of using fixed take profit levels. In this strategy a take profit level can even be a loss. It is useful as a strategy because it works in a different way than most strategies, making it a good tool to diversify a portfolio of trading strategies.

🟦 STRATEGY

There are 10 levels below the moving average and 10 above the moving average. For each side of the moving average the strategy uses 1 to 3 orders maximum (3 shorts at top, 3 longs at bottom). For instance you buy at level 2 below moving average and you increase position size when level 6 is reached (a cheaper price) in order to spread risks.

By default the strategy exits all trades when the moving average is reached, this makes it a mean reversion strategy. It is specifically designed for the forex market as these in my experience exhibit a lot of ranging behaviour on all the timeframes below daily.

There is also a stop loss at the outer band by default, in case price moves too far from the mean.

What are the risks?

In case price decides to stay below the moving average and never reaches the outer band one trade can create a very substantial loss, as the bands will keep following price and are not at a fixed level.

Explanation of default parameters

By default the strategy uses a starting capital of 25000$, this is realistic for retail traders.

Lot sizes at each level are set to minimum lot size 0.01, there is no reason for the default to be risky, if you want to risk more or increase equity curve increase the number at your own risk.

Slippage set to 20 points: that's a normal 2 pip slippage you will find on brokers.

Fill limit assumtion 20 points: so it takes 2 pips to confirm a fill, normal forex spread.

Commission is set to 0.00005 per contract: this means that for each contract traded there is a 5$ or whatever base currency pair has as commission. The number is set to 0.00005 because pinescript does not know that 1 contract is 100000 units. So we divide the number by 100000 to get a realistic commission.

The script will also multiply lot size by 100000 because pinescript does not know that lots are 100000 units in forex.

Extra safety limit

Normally the script uses strategy.exit() to exit trades at TP or SL. But because these are created 1 bar after a limit or stop order is filled in pinescript. There are strategy.orders set at the outer boundaries of the script to hedge against that risk. These get deleted bar after the first order is filled. Purely to counteract news bars or huge spikes in price messing up backtest.

🟦 VISUAL GOODIES

I've added a market profile feature to the edge of the grid. This so you can see in which grid zone market has been the most over X bars in the past. Some traders may wish to only turn on the strategy whenever the market profile displays specific characteristics (ranging market for instance).

These simply count how many times a high, low, or close price has been in each zone for X bars in the past. it's these purple boxes at the right side of the chart.

🟦 Script can be fully automated to MT5

There are risk settings in lot sizes or % for alerts and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

Поиск скриптов по запросу "the strat"

Strategy Tester [Cometreon]Strategy Tester is a powerful backtesting engine designed to evaluate and optimize trading strategies built with the Strategy Builder or signals triggered by the Signal Tester.

It provides a full-featured environment for assessing strategy performance across symbols and timeframes, offering smart tools for risk management, capital allocation, and alert handling.

Whether you're refining a custom strategy or validating signals, Strategy Tester helps you test with confidence and clarity.

🔷 Key Features

🟩 Multi-Symbol, Multi-Timeframe Testing

Easily test strategies across different assets and timeframes to understand how they behave in diverse market conditions.

🟩 Advanced Risk Management

Implement multiple Take Profit and Stop Loss combinations, break-even, trailing systems, and exit rules tailored to your style.

🟩 Flexible Session and Capital Settings

Customize trading hours, session windows, and initial capital allocation for ultra-precise testing scenarios.

🟩 Custom Alerts

Generate personalized alerts for entries, exits, and SL/TP adjustments to simulate real-time execution.

🔷 Technical Details and Customizable Inputs

1️⃣ Source Entry Long and Short - Select entry conditions for the strategy from the "Signal Tester" or "Strategy Builder".

2️⃣ Source Exit Long and Short - Select exit conditions for the strategy from the "Signal Tester" or "Strategy Builder".

3️⃣ Trading Session - Choose the period in which the strategy will enter positions, selecting from: Months, Days, up to 3 hourly sessions, and the strategy's activity range, i.e., start and end date.

4️⃣ Alert Message - Set custom messages for each type of Alert, such as Entry Long, Exit Short, or Change SL Long.

5️⃣ Plot - Choose whether to show Long and Short positions on the chart.

🔷 Risk Management Settings

1️⃣ Initial Capital - Set the starting capital for the strategy.

2️⃣ Quantity - Choose the entry quantity for each type of position, selecting from: Contracts, USD, Percentage of equity, or percentage of initial capital.

3️⃣ Take Profit - Configure up to 4 Take Profits using one of the following types:

%: Percentage from the entry price

USD: Distance in dollars

Pip: Distance in Pips

ATR: Based on ATR multiplier

Swing: Uses swing length

Risk Reward: Linked to Stop Loss or vice versa

4️⃣ Stop Loss - Set the SL using the same types as TP for maximum flexibility.

5️⃣ Break Even - Automatically modify SL when price hits a TP level, adjusting by % / USD / Pip from entry.

6️⃣ Trailing Take Profit - Activates a dynamic TP when a condition is met, updating it as price evolves (e.g., new highs).

7️⃣ Trailing Stop Loss - Updates SL automatically when the market moves in your favor (e.g., new lows in long trades).

8️⃣ Exit Before End Session - Exit positions a few candles before the session ends to avoid overnight risks.

🔍 How to Use Strategy Tester

🧩 Add the Indicator:

Load Strategy Tester onto your chart and connect it to any Cometreon signal generator.

⚙️ Configure Risk Settings:

Set up capital, risk, SL/TP parameters, and time filters to match your strategy profile.

🧪 Run the Test:

Execute the backtest and analyze the visual + data output for insight.

📊 Optimize and Repeat:

Adjust key parameters and re-run until your strategy achieves optimal performance.

☄️ Take your trading to the next level with TradeLab Beta's Strategy Tester this powerful backtesting tool and start optimizing your trading strategies today.

👉 Don't waste any more time and visit the link to get access to all Cometreon indicators.

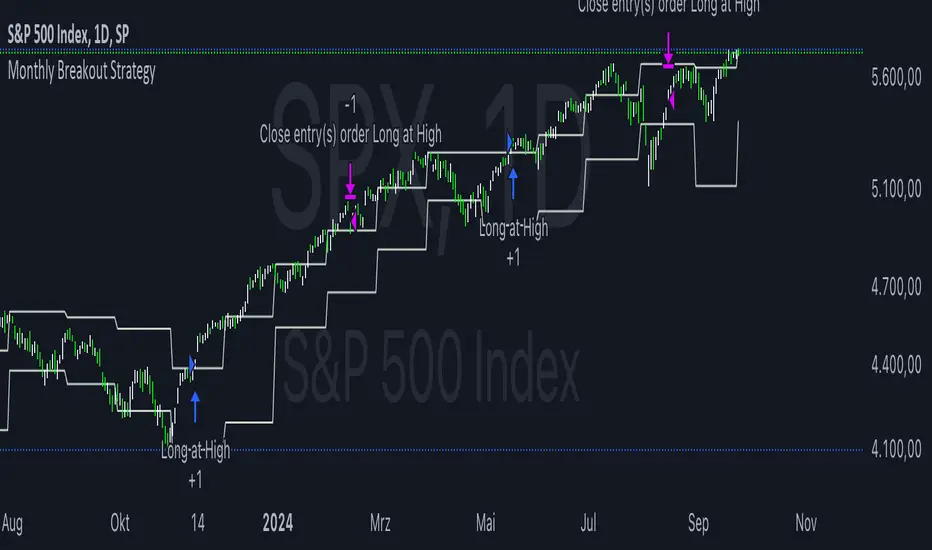

Monthly Breakout StrategyThis Monthly High/Low Breakout Strategy is designed to take long or short positions based on breakouts from the high or low of the previous month. Users can select whether they want to go long at a breakout above the previous month’s high, short at a breakdown below the previous month’s low, or use the reverse logic. Additionally, it includes a month filter, allowing trades to be executed only during user-specified months.

Breakout strategies, particularly those based on monthly highs and lows, aim to capitalize on price momentum. These systems rely on the assumption that once a significant price level is breached (such as the previous month's high or low), the market is likely to continue moving in the same direction due to increased volatility and trend-following behaviors by traders. Studies have demonstrated the potential effectiveness of breakout strategies in financial markets.

Scientific Evidence Supporting Breakout Strategies:

Momentum in Financial Markets:

Research on momentum-based strategies, which include breakout trading, shows that securities breaking key levels of support or resistance tend to continue their price movement in the direction of the breakout. Jegadeesh and Titman (1993) found that stocks with strong performance over a given period tend to continue performing well in subsequent periods, a principle also applied to breakout strategies.

Behavioral Finance:

The psychological factor of herd behavior is one of the driving forces behind breakout strategies. When prices break out of a key level (such as a monthly high), it triggers increased buying or selling pressure as traders join the trend. Barberis, Shleifer, and Vishny (1998) explained how cognitive biases, such as overconfidence and sentiment, can amplify price trends, which breakout strategies attempt to exploit.

Market Efficiency:

While markets are generally efficient, periods of inefficiency can occur, particularly around the breakouts of significant price levels. These inefficiencies often result in temporary price trends, which breakout strategies can exploit before the market corrects itself (Fama, 1970).

Risk Considerations:

Despite the potential for profit, the Monthly Breakout Strategy comes with several risks:

False Breakouts:

One of the most common risks in breakout strategies is the occurrence of false breakouts. These happen when the price temporarily moves above (or below) a key level but quickly reverses direction, causing losses for traders who entered positions too early. This is particularly risky in low-volatility environments.

Market Volatility:

Monthly breakout strategies rely on momentum, which may not be consistent across different market conditions. During periods of low volatility, price breakouts might lack the follow-through required for the strategy to succeed, leading to poor performance.

Whipsaw Risk:

The strategy is vulnerable to whipsaw markets, where prices oscillate around key levels without establishing a clear direction. This can result in frequent entry and exit signals that lead to losses, especially if trading costs are not managed properly.

Overfitting to Past Data:

If the month-selection filter is overly optimized based on historical data, the strategy may suffer from overfitting—performing well in backtests but poorly in real-time trading. This happens when strategies are tailored to past market conditions that may not repeat.

Conclusion:

While monthly breakout strategies can be effective in markets with strong momentum, they are subject to several risks, including false breakouts, volatility dependency, and whipsaw behavior. It is crucial to backtest this strategy thoroughly and ensure it aligns with your risk tolerance before implementing it in live trading.

References:

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Barberis, N., Shleifer, A., & Vishny, R. (1998). A Model of Investor Sentiment. Journal of Financial Economics, 49(3), 307-343.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, 25(2), 383-417.

Larry Connors RSI 3 StrategyThe Larry Connors RSI 3 Strategy is a short-term mean-reversion trading strategy. It combines a moving average filter and a modified version of the Relative Strength Index (RSI) to identify potential buying opportunities in an uptrend. The strategy assumes that a short-term pullback within a long-term uptrend is an opportunity to buy at a discount before the trend resumes.

Components of the Strategy:

200-Day Simple Moving Average (SMA): The price must be above the 200-day SMA, indicating a long-term uptrend.

2-Period RSI: This is a very short-term RSI, used to measure the speed and magnitude of recent price changes. The standard RSI is typically calculated over 14 periods, but Connors uses just 2 periods to capture extreme overbought and oversold conditions.

Three-Day RSI Drop: The RSI must decline for three consecutive days, with the first drop occurring from an RSI reading above 60.

RSI Below 10: After the three-day drop, the RSI must reach a level below 10, indicating a highly oversold condition.

Buy Condition: All the above conditions must be satisfied to trigger a buy order.

Sell Condition: The strategy closes the position when the RSI rises above 70, signaling that the asset is overbought.

Who Was Larry Connors?

Larry Connors is a trader, author, and founder of Connors Research, a firm specializing in quantitative trading research. He is best known for developing strategies that focus on short-term market movements. Connors co-authored several popular books, including "Street Smarts: High Probability Short-Term Trading Strategies" with Linda Raschke, which has become a staple among traders seeking reliable, rule-based strategies. His research often emphasizes simplicity and robust testing, which appeals to both retail and institutional traders.

Scientific Foundations

The Relative Strength Index (RSI), originally developed by J. Welles Wilder in 1978, is a momentum oscillator that measures the speed and change of price movements. It oscillates between 0 and 100 and is typically used to identify overbought or oversold conditions in an asset. However, the use of a 2-period RSI in Connors' strategy is unconventional, as most traders rely on longer periods, such as 14. Connors' research showed that using a shorter period like 2 can better capture short-term reversals, particularly when combined with a longer-term trend filter such as the 200-day SMA.

Connors' strategies, including this one, are built on empirical research using historical data. For example, in a study of over 1,000 signals generated by this strategy, Connors found that it performed consistently well across various markets, especially when trading ETFs and large-cap stocks (Connors & Alvarez, 2009).

Risks and Considerations

While the Larry Connors RSI 3 Strategy is backed by empirical research, it is not without risks:

Mean-Reversion Assumption: The strategy is based on the premise that markets revert to the mean. However, in strong trending markets, the strategy may underperform as prices can remain oversold or overbought for extended periods.

Short-Term Nature: The strategy focuses on very short-term movements, which can result in frequent trading. High trading frequency can lead to increased transaction costs, which may erode profits.

Market Conditions: The strategy performs best in certain market environments, particularly in stable uptrends. In highly volatile or strongly trending markets, the strategy's performance can deteriorate.

Data and Backtesting Limitations: While backtests may show positive results, they rely on historical data and do not account for future market conditions, slippage, or liquidity issues.

Scientific literature suggests that while technical analysis strategies like this can be effective in certain market conditions, they are not foolproof. According to Lo et al. (2000), technical strategies may show patterns that are statistically significant, but these patterns often diminish once they are widely adopted by traders.

References

Connors, L., & Alvarez, C. (2009). Short-Term Trading Strategies That Work. TradingMarkets Publishing Group.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of Technical Analysis: Computational Algorithms, Statistical Inference, and Empirical Implementation. The Journal of Finance, 55(4), 1705-1770.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research

RunRox - Backtesting System (ASMC)Introducing RunRox - Backtesting System (ASMC), a specially designed backtesting system built on the robust structure of our Advanced SMC indicator. This innovative tool evaluates various Smart Money Concept (SMC) trading setups and serves as an automatic optimizer, displaying which entry and exit points have historically shown the best results. With cutting-edge technology, RunRox - Backtesting System (ASMC) provides you with effective strategies, maximizing your trading potential and taking your trading to the next level

🟠 HOW OUR BACKTESTING SYSTEM WORKS

Our backtesting system for the Advanced SMC (ASMC) indicator is meticulously designed to provide traders with a thorough analysis of their Smart Money Concept (SMC) strategies. Here’s an overview of how it works:

🔸 Advanced SMC Structure

Our ASMC indicator is built upon an enhanced SMC structure that integrates the Institutional Distribution Model (IDM), precise retracements, and five types of order blocks (CHoCH OB, IDM OB, Local OB, BOS OB, Extreme OB). These components allow for a detailed understanding of market dynamics and the identification of key trading opportunities.

🔸 Data Integration and Analysis

1. Historical Data Testing:

Our system tests various entry and exit points using historical market data.

The ASMC indicator is used to simulate trades based on predefined SMC setups, evaluating their effectiveness over a specified time period.

Traders can select different parameters such as entry points, stop-loss, and take-profit levels to see how these setups would have performed historically.

2. Entry and Exit Events:

The backtester can simulate trades based on 12 different entry events, 14 target events, and 14 stop-loss events, providing a comprehensive testing framework.

It allows for testing with multiple combinations of entry and exit strategies, ensuring a robust evaluation of trading setups.

3. Order Block Sensitivity:

The system uses the sensitivity settings from the ASMC indicator to determine the most relevant order blocks and fair value gaps (FVGs) for entry and exit points.

It distinguishes between different types of order blocks, helping traders identify strong institutional zones versus local zones.

🔸 Optimization Capabilities

1. Auto-Optimizer:

The backtester includes an auto-optimizer feature that evaluates various setups to find those with the best historical performance.

It automatically adjusts parameters to identify the most effective strategies for both trend-following and counter-trend trading.

2. Stop Loss and Take Profit Optimization:

It optimizes stop-loss and take-profit levels by testing different settings and identifying those that provided the best historical results.

This helps traders refine their risk management and maximize potential returns.

3. Trailing Stop Optimization:

The system also optimizes trailing stops, ensuring that traders can maximize their profits by adjusting their stops dynamically as the market moves.

🔸 Comprehensive Reporting

1. Performance Metrics:

The backtesting system provides detailed reports, including key performance metrics such as Net Profit, Win Rate, Profit Factor, and Max Drawdown.

These metrics help traders understand the historical performance of their strategies and make data-driven decisions.

2. Flexible Settings:

Traders can adjust initial balance, commission rates, and risk per trade settings to simulate real-world trading conditions.

The system supports testing with different leverage settings, allowing for realistic assessments even with tight stop-loss levels.

🔸 Conclusion

The RunRox Backtesting System (ASMC) is a powerful tool for traders seeking to validate and optimize their SMC strategies. By leveraging historical data and sophisticated optimization algorithms, it provides insights into the most effective setups, enhancing trading performance and decision-making.

🟠 HERE ARE THE AVAILABLE FEATURES

Historical backtesting for any setup – Select any entry point, exit point, and various stop-loss options to see the results of your setup on historical data.

Auto-optimizer for finding the best setups – The indicator displays settings that have shown the best results historically, providing valuable insights.

Auto-optimizer for counter-trend setups – Discover entry and exit points for counter-trend trading based on historical performance.

Auto-optimizer for stop-loss – The indicator shows stop-loss points that have been most effective historically.

Auto-optimizer for take-profit – The indicator identifies take-profit points that have performed well in historical trading data.

Auto-optimizer for trailing stop – The indicator presents trailing stop settings that have shown the best historical results.

And much more within our indicator, all of which we will cover in this post. Next, we will showcase the possible entry points, targets, and stop-loss options available for testing your strategies

🟠 ENTRY SETTINGS

12 Event Triggers for Trade Entry

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Trade Direction Options

Long Only: Enter long positions only

Short Only: Enter short positions only

Long and Short: Enter both long and short positions based on trend

3 Levels for Order Block/FVG Entries

Beginning: Enter the trade at the first touch of the Order Block/FVG

Middle: Enter the trade when the middle of the Order Block/FVG is reached

End: Enter the trade upon full filling of the Order Block/FVG

*Three levels work only for Order Blocks and FVG. For trade entries based on BOS or CHoCH, these settings do not apply as these parameters are not available for these types of entries

You can choose any combination of trade entries imaginable.

🟠 TARGET SETTINGS

14 Target Events, Including Fixed % and Fixed RR (Risk/Reward):

Fixed - % change in price

Fixed RR - Risk Reward per trade

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Levels of Order Block/FVG for Target

Beginning: Close the trade at the first touch of your target.

Middle: Close the trade at the midpoint of your chosen target.

End: Close the trade when your target is fully filled.

Customizable Parameters

Easily set your Fixed % and Fixed RR targets with a user-friendly input field. This field works only for the Fixed and Fixed RR entry parameters. When selecting a different entry point, this field is ignored

Choose any combination of target events to suit your trading strategy.

🟠 STOPLOSS SETTINGS

14 Possible StopLoss Events Including Entry Orderblock/FVG

Fixed - Fix the loss on the trade when the price moves by N%

Entry Block

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Levels for Order Blocks/FVG Exits

Beginning: Exit the trade at the first touch of the order block/FVG.

Middle: Exit the trade at the middle of the order block/FVG.

End: Exit the trade at the full completion of the order block/FVG.

Dedicated Field for Setting Fixed % Value

Set a fixed % value in a dedicated field for the Fixed parameter. This field works only for the Fixed parameter. When selecting other exit parameters, this field is ignored.

🟠 ADDITIONAL SETTINGS

Trailing Stop, %

Set a Trailing Stop as a percentage of your trade to potentially increase profit based on historical data.

Move SL to Breakeven, bars

Move your StopLoss to breakeven after exiting the entry zone for a specified number of bars. This can enhance your potential WinRate based on historical performance.

Skip trade if RR less than

This feature allows you to skip trades where the potential Risk-to-Reward ratio is less than the number set in this field.

🟠 EXAMPLE OF MANUAL SETUP

For example, let me show you how it works on the chart. You select entry parameters, stop loss parameters, and take profit parameters for your trades, and the strategy automatically tests this setup on historical data, allowing you to see the results of this strategy.

In the screenshot above, the parameters were as follows:

Trade Entry: CHoCH OB (Beginning)

Stop Loss: Entry Block

Take Profit: Break of BOS

The indicator will automatically test all possible trades on the chart and display the results for this setup.

🟠 AUTO OPTIMIZATION SETTINGS

In the screenshot above, you can see the optimization table displaying various entry points, exits, and stop-loss settings, along with their historical performance results and other parameters. This feature allows you to identify trading setups that have shown the best historical outcomes.

This functionality will enhance your trading approach, providing you with valuable insights based on historical data. You’ll be aware of the Smart Money Concept settings that have historically worked best for any specific chart and timeframe.

Our indicator includes various optimization options designed to help you find the most effective settings based on historical data. There are 5 optimization modes, each offering unique benefits for every trader

Trend Entry - Optimization of the best settings for trend-following trades. The strategy will enter trades only in the direction of the trend. If the trend is upward, it will look for long entry points and vice versa.

Counter Trend Entry - Finding setups against the trend. If the trend is upward, the script will search for short entry points. This is the opposite of trend entry optimization.

Stop Loss - Identifying stop-loss points that showed the best historical performance for the specific setup you have configured. This helps in finding effective exit points to minimize losses.

Take Profit - Determining targets for the configured setup based on historical performance, helping to identify potentially profitable take profit levels.

Trailing Stop - Finding optimal percentages for the trailing stop function based on historical data, which can potentially increase the profit of your trades.

Ability to set parameters for auto-optimization within a specified range. For example, if you choose FixRR TP from 1 to 10, the indicator will automatically test all possible Risk Reward Take Profit variations from 1 to 10 and display the results for each parameter individually.

Ability to set initial deposit parameters, position commissions, and risk per trade as a fixed percentage or fixed amount. Additionally, you can set the maximum leverage for a trade.

There are times when the stop loss is very close to the entry point, and adhering to the risk per trade values set in the settings may not allow for such a loss in any situation. That’s why we added the ability to set the maximum possible leverage, allowing you to test your trading strategy even with very tight stop losses.

Duplicated Smart Money Structure settings from our Advanced SMC indicator that you can adjust to match your trading style flexibly. All these settings will be taken into account during the optimization process or when manually calculating settings.

Additionally, you can test your strategy based on higher timeframe order blocks. For example, you can test a strategy on a 1-minute chart while displaying order blocks from a 15-minute timeframe. The auto-optimizer will consider all these parameters, including higher timeframe order blocks, and will enter trades based on these order blocks.

Highly flexible dashboard and results optimization settings allow you to display the tables you need and sort results by six different criteria: Profit Factor, Profit, Winrate, Max Drawdown, Wins, and Trades. This enables you to find the exact setup you desire, based on these comprehensive data points.

🟠 ALERT CUSTOMIZATION

With this indicator, you can set up buy and sell alerts based on the test results, allowing you to create a comprehensive trading strategy. This feature enables you to receive real-time signals, making it a powerful tool for implementing your trading strategies.

🟠 STRATEGY PROPERTIES

For backtesting, we used realistic initial data for entering trades, such as:

Starting balance: $1000

Commission: 0.01%

Risk per trade: 1%

To ensure realistic data, we used the above settings. We offer two methods for calculating your order size, and in our case, we used a 1% risk per trade. Here’s what it means:

Risk per trade: This is the maximum loss from your deposit if the trade goes against you. The trade volume can change depending on your stop-loss distance from the entry point. Here’s the formula we use to calculate the possible volume for a single trade:

1. quantity = percentage_risk * balance / loss_per_1_contract (incl. fee)

Then, we calculate the maximum allowed volume based on the specified maximum leverage:

2. max_quantity = maxLeverage * balance / entry_price

3. If quantity < max_quantity, meaning the leverage is less than the maximum allowed, we keep quantity. If quantity > max_quantity, we use max_quantity (the maximum allowed volume according to the set leverage).

This way, depending on the stop-loss distance, the position size can vary and be up to 100% of your deposit, but the loss in each trade will not exceed the set percentage, which in our case is 1% for this backtest. This is a standard risk calculation method based on your stop-loss distance.

🔸 Statistical Significance of Trade Data

In our strategy, you may notice there weren’t enough trades to form statistically significant data. This is inherent to the Smart Money Concept (SMC) strategy, where the focus is not on the number of trades but rather on the risk-to-reward ratio per trade. In SMC strategies, it’s crucial to avoid taking numerous uncertain setups and instead perform a comprehensive analysis of the market situation.

Therefore, our strategy results show fewer than 100 trades. It’s important to understand that this small sample size isn’t statistically significant and shouldn’t be relied upon for strategy analysis. Backtesting with a small number of trades should not be used to draw conclusions about the effectiveness of a strategy.

🔸 Versatile Use Cases

The methods of using this indicator are numerous, ranging from identifying potentially the best-performing order blocks on the chart to creating a comprehensive trading strategy based on the data provided by our indicator. We believe that every trader will find a valuable application for this tool, enhancing their entry and exit points in trades.

Disclaimer

Past performance is not indicative of future results. The results shown by this indicator do not guarantee similar outcomes in the future. Use this tool as part of a comprehensive trading strategy, considering all market conditions and risks.

How to access

For access to this indicator, please read the author’s instructions below this post

Strategic Multi-Step Supertrend - Strategy [presentTrading]The code is mainly developed for me to stimulate the multi-step taking profit function for strategies. The result shows the drawdown can be reduced but at the same time reduced the profit as well. It can be a heuristic for futures leverage traders.

█ Introduction and How it is Different

The "Strategic Multi-Step Supertrend" is a trading strategy designed to leverage the power of multiple steps to optimize trade entries and exits across the Supertrend indicator. Unlike traditional strategies that rely on single entry and exit points, this strategy employs a multi-step approach to take profit, allowing traders to lock in gains incrementally. Additionally, the strategy is adaptable to both long and short trades, providing a comprehensive solution for dynamic market conditions.

This template strategy lies in its dual Supertrend calculation, which enhances the accuracy of trend detection and provides more reliable signals for trade entries and exits. This approach minimizes false signals and increases the overall profitability of trades by ensuring that positions are entered and exited at optimal points.

BTC 6h L/S Performance

█ Strategy, How It Works: Detailed Explanation

The "Strategic Multi-Step Supertrend Trader" strategy utilizes two Supertrend indicators calculated with different parameters to determine the direction and strength of the market trend. This dual approach increases the robustness of the signals, reducing the likelihood of entering trades based on false signals. Here is a detailed breakdown of how the strategy operates:

🔶 Supertrend Indicator Calculation

The Supertrend indicator is a trend-following overlay on the price chart, typically used to identify the direction of the trend. It is calculated using the Average True Range (ATR) to ensure that the indicator adapts to market volatility. The formula for the Supertrend indicator is:

Upper Band = (High + Low) / 2 + (Factor * ATR)

Lower Band = (High + Low) / 2 - (Factor * ATR)

Where:

- High and Low are the highest and lowest prices of the period.

- Factor is a user-defined multiplier.

- ATR is the Average True Range over a specified period.

The Supertrend changes its direction based on the closing price in relation to these bands.

🔶 Entry-Exit Conditions

The strategy enters long positions when both Supertrend indicators signal an uptrend, and short positions when both indicate a downtrend. Specifically:

- Long Condition: Supertrend1 < 0 and Supertrend2 < 0

- Short Condition: Supertrend1 > 0 and Supertrend2 > 0

- Long Exit Condition: Supertrend1 > 0 and Supertrend2 > 0

- Short Exit Condition: Supertrend1 < 0 and Supertrend2 < 0

🔶 Multi-Step Take Profit Mechanism

The strategy features a multi-step take profit mechanism, which allows traders to lock in profits incrementally. This is achieved through four user-configurable take profit levels. For each level, the strategy specifies a percentage increase (for long trades) or decrease (for short trades) in the entry price at which a portion of the position is exited:

- Step 1: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent1 / 100)

- Step 2: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent2 / 100)

- Step 3: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent3 / 100)

- Step 4: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent4 / 100)

This staggered exit strategy helps in locking profits at multiple levels, thereby reducing risk and increasing the likelihood of capturing the maximum possible profit from a trend.

BTC Local

█ Trade Direction

The strategy is highly flexible, allowing users to specify the trade direction. There are three options available:

- Long Only: The strategy will only enter long trades.

- Short Only: The strategy will only enter short trades.

- Both: The strategy will enter both long and short trades based on the Supertrend signals.

This flexibility allows traders to adapt the strategy to various market conditions and their own trading preferences.

█ Usage

1. Add the strategy to your trading platform and apply it to the desired chart.

2. Configure the take profit settings under the "Take Profit Settings" group.

3. Set the trade direction under the "Trade Direction" group.

4. Adjust the Supertrend settings in the "Supertrend Settings" group to fine-tune the indicator calculations.

5. Monitor the chart for entry and exit signals as indicated by the strategy.

█ Default Settings

- Use Take Profit: True

- Take Profit Percentages: Step 1 - 6%, Step 2 - 12%, Step 3 - 18%, Step 4 - 50%

- Take Profit Amounts: Step 1 - 12%, Step 2 - 8%, Step 3 - 4%, Step 4 - 0%

- Number of Take Profit Steps: 3

- Trade Direction: Both

- Supertrend Settings: ATR Length 1 - 10, Factor 1 - 3.0, ATR Length 2 - 11, Factor 2 - 4.0

These settings provide a balanced starting point, which can be customized further based on individual trading preferences and market conditions.

IsAlgo - AI Trend Strategy► Overview:

The AI Trend Strategy employs a combination of technical indicators to guide trading decisions across various markets and timeframes. It uses a custom Super Trend indicator and an Exponential Moving Average (EMA) to analyze market trends and executes trades based on specific candlestick patterns. This strategy includes options for setting stop losses, take profit levels, and features an alert system for trade notifications.

► Description:

This strategy focuses on identifying the optimal "entry candle," which signals either a potential correction within the ongoing trend or the emergence of a new trend. The entry criteria for this candle are highly customizable, allowing traders to specify dimensions such as the candle's minimum and maximum size and body ratio. Additional settings include whether this candle should be the highest or lowest compared to recent candles and if a confirmation candle is necessary to validate the entry.

The Super Trend indicator is central to the strategy’s operation, dictating the direction of trades by identifying bullish or bearish trends. Traders have the option to configure trades to align with the direction of the trend identified by this indicator, or alternatively, to take positions counter to the trend for potential reversal strategies. This flexibility can be crucial during varying market conditions.

Additionally, the strategy incorporates an EMA alongside the Super Trend indicator to further analyze trend directions. This combined approach aims to reduce the occurrence of false signals and improve the strategy's overall trend analysis.

The learning algorithm is a standout feature of the AI Trend Strategy. After accumulating data from a predefined number of trades (e.g., after the first 100 trades), the algorithm begins to analyze past performances to identify patterns in wins and losses. It considers variables such as the distance from the current price to the trend line, the range between the highest and lowest prices during the trend, and the duration of the trend. This data informs the algorithm's predictions for future trades, aiming to improve accuracy and reduce losses by adapting to the evolving market conditions.

► Examples of Trade Execution:

1. In an Uptrend: The strategy might detect a suitable entry candle during a correction phase, which aligns with the continuing uptrend for a potential long trade.

2. In a Downtrend: Alternatively, the strategy might identify an entry candle at the end of a downtrend, suggesting a potential reversal or correction where a long trade could be initiated.

3. In an Uptrend: The strategy may also spot an entry candle at the end of an uptrend and execute a short trade, anticipating a reversal or significant pullback.

4. In a Downtrend: The strategy might find a suitable entry candle during a correction phase, indicating a continuation of the downtrend for a potential short trade.

These examples illustrate how the strategy identifies potential trading opportunities based on trend behavior and candlestick patterns.

► Features and Settings:

⚙︎ Trend: Utilizes a custom Super Trend indicator to identify the direction of the market trend. Users can configure the strategy to execute trades in alignment with this trend, take positions contrary to the trend, or completely ignore the trend information for their trading decisions.

⚙︎ Moving average: Employs an Exponential Moving Average (EMA) to further confirm the trend direction indicated by the Super Trend indicator. This setting can be used in conjunction with the Super Trend or disabled if preferred.

⚙︎ Entry candle: Defines the criteria for the candle that triggers a trade. Users can customize aspects such as the candle's size, body, and its relative position to previous candles to ensure it meets specific trading requirements before initiating a trade.

⚙︎ Learning algorithm: This component uses historical trade data to refine the strategy. It assesses various aspects of past trades, such as price trends and market conditions, to make more informed trading decisions in the future.

⚙︎ Trading session: Users can define specific trading hours during which the strategy should operate, allowing trades to be executed only during preferred market periods.

⚙︎ Trading days: This option enables users to specify which days the strategy should be active, providing the flexibility to avoid trading on certain days of the week if desired.

⚙︎ Backtesting: Enables a period during which the strategy can be tested over a selected start and end date, with an option to deactivate this feature if not needed.

⚙︎ Trades: Detailed configuration options include the direction of trades (long, short, or both), position sizing (fixed or percentage-based), the maximum number of open trades, and limitations on the number of trades per day or based on trend changes.

⚙︎ Trades Exit: Offers various strategies for exiting trades, such as setting limits on profits or losses, specifying the duration a trade should remain open, or closing trades based on trend reversal signals.

⚙︎ Stop loss: Various methods for setting stop losses are available, including fixed pips, based on Average True Range (ATR), or utilizing the highest or lowest price points within a designated number of previous candles. Another option allows for closing the trade after a specific number of candles moving in the opposite direction.

⚙︎ Break even: This feature adjusts the stop loss to a break-even point under certain conditions, such as reaching predefined profit levels, to protect gains.

⚙︎ Trailing stop: The trailing stop feature adjusts the stop loss as the trade moves into profit, aiming to secure gains while potentially capturing further upside.

⚙︎ Take profit: Up to three take profit levels can be established using various methods, such as a fixed amount of pips, risk-to-reward ratios based on the stop loss, ATR, or after a set number of candles that move in the direction of the trade.

⚙︎ Alerts: Includes a comprehensive alert system that informs the user of all significant actions taken by the strategy, such as trade openings and closings. It supports placeholders for dynamic values like take profit levels, stop loss prices, and more.

⚙︎ Dashboard: Provides a visual display of detailed information about ongoing and past trades on the chart, helping users monitor the strategy’s performance and make informed decisions.

► Backtesting Details:

Timeframe: 15-minute BTCUSD chart.

Initial Balance: $10,000.

Order Size: 4% of equity per trade.

Commission: 0.01%.

Slippage: 5 ticks.

Risk Management: Strategic stop loss settings are applied based on the most extreme price points within the last 18 candles.

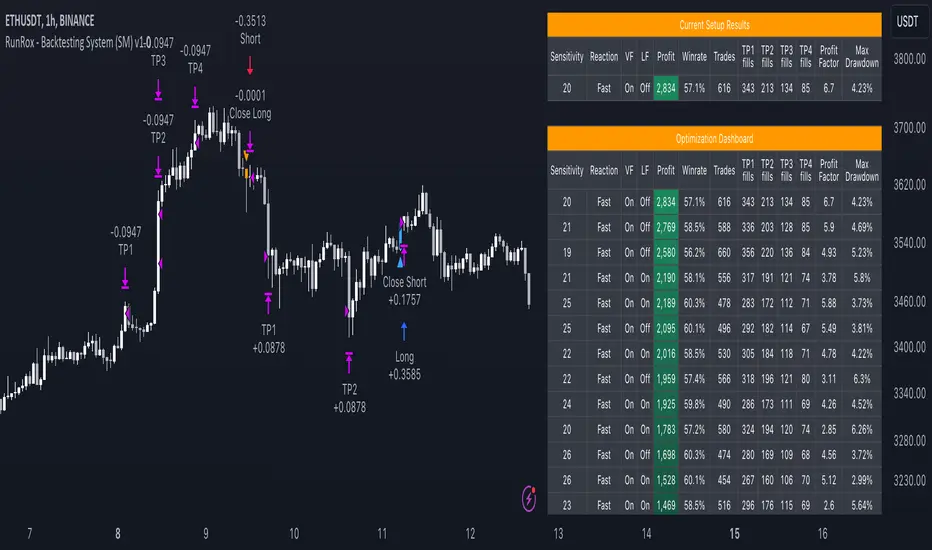

RunRox - Backtesting System (SM)RunRox - Backtesting System (SM) is designed for flexible and comprehensive testing of trading strategies, closely integrated with our RunRox - Signals Master indicator. This combination enhances your ability to refine strategies efficiently, providing you with insights to adapt and optimize your trading tactics seamlessly.

The Backtesting System (SM) excels in pinpointing the optimal settings for the RunRox - Signals Master indicator, efficiently highlighting the most effective configurations.

Capabilities of the Backtesting System (SM)

Optimal Settings Determination: Identifies the best configurations for the Signals Master indicator to enhance its effectiveness.

Timeframe-Specific Strategy Testing: Allows strategies to be tested over specific historical time periods to assess their viability.

Customizable Initial Conditions: Enables setting of initial deposit, risk per trade, and commission rates to mirror real-world trading conditions.

Flexible Money Management: Provides options to set take profits and stop losses, optimizing potential returns and risk management.

Intuitive Dashboard: Features a user-friendly dashboard that visually displays all pertinent information, making it easy to analyze and adjust strategies.

Trading Flexibility Across Three Modes:

Dual-Direction Trading: Engage in both buying and selling with this mode. Our dashboard optimizes and identifies the best settings for trading in two directions, streamlining the process to maximize effectiveness for both buy and sell orders.

Buy-Only Mode: Tailored for traders focusing exclusively on purchasing assets. In this mode, our backtester pinpoints the most advantageous sensitivity, speed reaction, and filter settings specifically for buying. Optimal settings in this mode may differ from those used in dual-direction trading, providing a customized approach to single-direction strategies.

Sell-Only Mode: Perfect for strategies primarily based on selling. This setting allows you to discover the ideal configurations for asset sales, which can be particularly useful if you are looking for optimal exit points in long-term transactions or under specific market conditions.

Here's an example of how profits can differ on the same asset when trading using two distinct strategies: exclusively buying or trading in both directions.

Above in the image, you can see how one-directional trading influences the results of backtests on historical data. While this does not guarantee future outcomes, it provides insight into how the strategy's performance can vary with different trading directions.

As you can also see from the image, one-directional trading has affected the optimal combination of settings for Sensitivity, Speed Reaction, and Filters.

Stop Loss and Take Profit

Our backtesting system, as you might have gathered, includes flexible settings for take profits and stop losses. Here are the main features:

Multiple Take Profits: Ability to set from 1 to 4 take profit levels.

Fixed Percentage: Option to assign a fixed percentage for each take profit.

Trade Proportion Fixation: Ability to set a fixed size from the trade for securing profits.

Stop Loss Installation: Option to establish a stop loss.

Break-Even Stop Loss: Ability to move the stop loss to a break-even point upon reaching a specified take profit level.

These settings offer extensive flexibility and can be customized according to your preferences and trading style. They are suitable for both novice and professional traders looking to test their trading strategies on historical data.

As illustrated in the image above, we have implemented money management by setting fixed take profits and stop losses. Utilizing money management has improved indicators such as profit, maximum drawdown, and profit factor, turning even historically unprofitable strategies into profitable ones. Although this does not guarantee future results, it serves as a valuable tool for understanding the effectiveness of money management.

Additionally, as you can see, the optimal settings for Signals Master have been adjusted, highlighting the best configurations for the most favorable outcomes.

Disclaimer:

Historical data is not indicative of future results. All indicators and strategies provided by RunRox are intended for integration with traders' strategies and should be used as tools for analysis rather than standalone solutions. Traders should use their own discretion and understand that all trading involves risk.

FreedX Backtest Plus█ Our new FreedX Backtest PLUS template enhances TradingView backtesting with smart features like Mean Reversion, Flexible Volatility, Liquidation Filter, and Better Trend Filtering, making strategies more effective. It lets users set up automated alerts easily. This guide explains how to make the most of these improved features.

The Trading Date Settings feature in our TradingView script allows you to refine their backtesting parameters by specifying trading dates and hours. This feature enhances the accuracy of the backtest by aligning it with specific time frames and days, ensuring that the strategy is tested under relevant market conditions.

Features:

⚙️ Enable Trading Between Specific Dates:

🎯 Purpose:

→ Allows you to limit the backtesting of their strategy to a specific date range.

💡 How to Use:

→ Input the Start Date and End Date for the backtest period.

→ The script will execute the strategy only within this specified date range.

⚙️ Enable Trading Between Specific Hours:

🎯 Purpose:

→ Allows you to limit the backtesting of their strategy to a specific hour range.

💡 How to Use:

→ Input the start and end hour for in Trading Session section.

→ The script will execute the strategy only within this specified hour range.

⚙️ Enable Trading on Specified Days of the Week:

🎯 Purpose:

→ Gives you the option to conduct backtesting on selected days of the week, tailoring the strategy to particular market behaviours that may occur on these days.

💡 How to Use:

→ Select the days of the week for the backtest.

→ The script will activate the trading strategy only on these chosen days.

█ BUY/SELL TRIGGER SETTINGS

The Buy/Sell Trigger Settings feature is designed to provide users with flexibility in defining the conditions for 'LONG' and 'SHORT' signals based on various indicator types. This customization is crucial for tailoring strategies to different trading styles and market conditions.

Features:

⚙️ Single-Line Plotted Indicators :

🎯 Purpose:

→ Enables you to select a single-line plotted indicator as a source for backtesting. You can define specific levels to trigger 'LONG' or 'SHORT' signals.

💡 How to Use:

→ Choose a Single-Line Plotted indicator as the source.

→ Set the top and bottom levels for the indicator.

→ The script triggers 'LONG' signals at the bottom level and 'SHORT' signals at the top level.

⚙️ Two-Line Plotted Indicators :

🎯 Purpose:

→ Allows backtesting with two-line cross plot sources. Signals are generated based on the crossover of these lines.

💡 How to Use:

→ Select two lines as 'Source 1' and 'Source 2' for the indicator.

→ The script triggers a 'LONG' signal when 'Source 1' crosses above 'Source 2'.

→ Conversely, a 'SHORT' signal is triggered when 'Source 2' crosses above 'Source 1'.

⚙️ Custom Signals :

🎯 Purpose:

→ This setting enables users to define their own criteria for LONG, SHORT, and CLOSE signals based on custom indicator outputs.

💡 How to Use:

→ Select the custom source for your signals.

→ Define the output values that correspond to each signal type (e.g., “1” for 'LONG', “-1” for SHORT, and “0” for CLOSE).

→ The script will trigger signals according to these custom-defined values.

█ TP/SL SETTINGS

The TP/SL (Take Profit/Stop Loss) Settings feature is designed to give users control over their profit securing and risk mitigation strategies. This feature allows for setting custom TP and SL levels, which can be critical in managing trades effectively.

Features:

Custom TP/SL Levels for Long/Short Signals:

🎯 Purpose:

→ Enables users to set specific percentage levels for Take Profit and Stop Loss on long and short signals.

💡 How to Use:

→ In the TP/SL Settings, input the desired percentage for Take Profit (TP) and Stop Loss (SL).

→ For example, to secure a profit at a 10% price increase on LONG signals, set the “Long TP Percentage” to “10”.

█ STRATEGY SETTINGS

Strategy Settings provide a range of options to customize the trading strategy. These settings include leverage, position direction changes, and more, allowing users to tailor their strategy to their risk tolerance and market view.

Features:

⚙️ Enable Reverse Position:

🎯 Purpose:

→ Automatically closes a current position and opens a new one in the opposite direction upon detecting a signal for a market trend change.

🎯 Example:

→ If a LONG signal is received while in a SHORT position, the script will close the SHORT position and open a LONG position.

💡 How to Use:

→ Activate this feature in the Strategy Settings.

⚙️ Enable Spot Mode:

🎯 Purpose:

→ Disables short orders, using short signals only for closing long positions.

💡 How to Use:

→ Select the 'Spot Mode' option in the Strategy Settings.

⚙️ Enable Invert Signals:

🎯 Purpose:

→ Inverts all indicator signals, changing LONG signals to SHORT and vice versa.

💡 How to Use:

→ Opt for the 'Invert Signals' feature in the Strategy Settings.

⚙️ Enable Trailing Stop:

🎯 Purpose:

→ Triggers a trailing stop order on the exchange instead of a standard stop market order.

☢️ Caution:

→ The backtesting of this feature on TradingView may not accurately reflect actual strategy performance due to discrepancies between TradingView and exchange mechanisms.

💡 How to Use:

→ Select 'Trailing Stop' in the Strategy Settings.

⚙️ Enable Realistic TP & SL:

🎯 Purpose:

→ Goal is protect the user from unrealistic stop loss and take profit prices in live exchange trading conditions.

→ That feature continuously checks the take profit, stop loss and move stop loss prices to prevent unrealistic values. It changes their values according to (minimum realistic percent %)

💡 How to Use:

→ Select 'Enable Realistic TP & SL' in the Strategy Settings. Write min allowed percents.

█ LIMITER SETTINGS

Limiter Settings provide a range of options to customize the trading strategy. These settings include drawdown limits,contract limit, tradable ratio, for allowing users to tailor their strategy to their risk tolerance and market view.

⚙️ Leverage :

🎯 Purpose:

→ Allows users to apply leverage to their trades.

☢️ Caution:

→ High leverage can significantly increase the risk of liquidation.

→ High leverage and a high stop-loss price may override your fixed stoploss percentage, adjusting the stop-loss to the liquidation price.

💡 How to Use:

→ Set the desired leverage ratio in the Strategy Settings.

⚙️ Drawdown Limit:

🎯 Purpose:

→ Sets a maximum drawdown limit, automatically halting the strategy if this limit is reached, thereby controlling risk.

💡 How to Use:

→ Input the maximum drawdown limit (default: 100, min: 0, max: 100).

⚙️ Contract Limit:

🎯 Purpose:

→ Sets a maximum contract limit, beyond which the compound effect cannot be used. This is important to prevent market manipulation through large-volume orders.

💡 How to Use:

→ Input the maximum contract limit (min: 0).

⚙️ Tradable Ratio:

🎯 Purpose:

→ Sets a tradable ratio, it uses that ratio calculating entry cost for position. Main purpose is cash-out and cash-in according to balance change.

💡 How to Use:

→ Input the tradable ratio percent (default: 98, min: 0.1, max: 100).

█ CASH-OUT SETTINGS

Cash-Out Settings offer a money-saving mechanism that prevents entering positions with the entire balance due to cashed-out funds. It functions with a webhook alerts, but the 'Override Allocation %' option must be enabled.

⚙️ Cash-out Threshold %:

🎯 Purpose:

→ It is cash-out mechanism, it saves money with a target threshold.

💡 How to Use:

→ Input the threshold (min: 0).

⚙️ Cash-out Per Profitable Trades %:

🎯 Purpose:

→ It is cash-out mechanism, it saves money from every trade with a percent like commission.

💡 How to Use:

→ Input save percent% (min: 0).

█ ADAPTIVE VOLATILITY STRATEGY SETTINGS

Advanced Strategy Settings offer sophisticated methods for managing Stop Loss (SL) and Take Profit (TP) using the Average True Range (ATR). These settings are ideal for traders who want to incorporate volatility into their exit strategies.

Features:

⚙️ Enable ATR Stop Loss:

🎯 Purpose:

→ Automatically sets the Stop Loss price using the Average True Range at the time of entry.

💡 How to Use:

→ Activate 'ATR Stop Loss' to have the SL price calculated based on the current ATR.

⛓ Enable ATR Trailing Stop:

→ Dynamically updates the Stop Loss price with each new bar, according to the Average True Range.

→ Activate 'ATR Trailing Stop'.

→ Set the ATR Period to define the number of bars for ATR calculation.

→ Adjust the ATR SL Multiplier to determine the stop loss distance.

→ Modify the ATR TP Multiplier for setting the take profit distance.

⚙️ Enable ATR Take Profit:

🎯 Purpose:

→ Sets the Take Profit price based on the Average True Range at the time of entry.

💡 How to Use:

→ Choose 'ATR Take Profit' for TP price determination using ATR.

⚙️ Enable ATR Limit Entry:

🎯 Purpose:

→ Trade can not open in candle close price. Price should hit target price that based on average true range value.

💡 How to Use:

→ Choose 'ATR Limit Entry' for entry price determination using ATR.

⛓ Enable ATR Limit Entry Trailing Price:

→ Dynamically updates the entry price with each new bar, according to the Average True Range.

→ Activate 'ATR Limit Entry Trailing Price'.

→ Set the ATR Period to define the number of bars for ATR calculation.

→ Adjust the ATR SL Multiplier to determine the stop loss distance.

→ Modify the ATR TP Multiplier for setting the take profit distance.

█ TREND FILTERING SETTINGS

Trend Filtering Settings are designed to align trading strategies with the prevailing market trend, enhancing the precision of trade entries and exits. These settings utilize moving averages for trend analysis and decision-making.

Features:

⚙️ Enable Moving Average Filtering:

🎯 Purpose:

→ Limits trades based on moving average trends, blocking short trades in an uptrend and vice versa.

💡 How to Use:

→ Enable 'Trend Filtering'.

→ Set Fast and Slow MA Lengths for trend analysis.

→ Select the Timeframe for moving averages.

→ Choose the Moving Average Type for trend filtering.

🎯 Note:

→ Be cautious with timeframe selections; lower timeframes than the base may cause inconsistencies.

⛓ Exit on Trend Reversal:

→ Automatically closes a position when a market trend reversal is detected.

→ Turn on 'Exit on Trend Reversal' in the settings.

⛓ Ignore Counter Signals:

→ Ignores counter signals during trending market way.

→ If the trend way is long. All short signals will ignore and vice versa.

⛓ Enable Drawing On Chart:

→ Visually represents the trend filter directly on the chart for easy reference.

→ Activate 'Drawing On Chart' to see the trend filter overlaid on the trading chart.

⚙️ Enable Adx Filtering:

🎯 Purpose:

→ Limits trades based on adx value, blocking trades if trend strength is not enough or vice versa for invert mode.

💡 How to Use:

→ Enable 'Adx Filtering'.

→ Set Smoothing and Lengths for adx trend analysis.

→ Select level barrier for trend strength.

⚙️ Enable Custom Filtering:

🎯 Purpose:

→ Limits trades based on custom sources, blocking trades according to custom trades.

💡 How to Use:

→ Enable 'Custom Filtering'.

→ Select fast source.

→ Select slow source.

→ Enable lag mode.

█ MEAN REVERSION FILTERING SETTINGS

Mean Reversion Filtering Settings are designed to align trading strategies during accumulation market conditions. They set a distance from a line to permit trading. The purpose is to ensure that when the price strays too far from the mean line, it should revert back. In accumulation markets, price movements are generally horizontal. In such situations, mean reversion will operate like a grid, enabling profitable trades with low drawdown. However, when the market structure begins to trend, mean reversion filters may not be as profitable as in accumulation markets. For instance, let's say the price is rising and we are shorting the market until it reaches the mean price line. As the price goes up and the mean also rises, we will end up closing the position at a higher price, rendering the mean reversion system non-profitable. Therefore, consider this filter wisely; greater distances might work better in trending markets.

Features:

⚙️ Enable Kairi Filter:

🎯 Purpose:

→ Blocks trades based on distance percent between price and moving average.

💡 How to Use:

→ Enable 'Kairi Filter'.

→ Set Length and Distance Percent.

⛓ Enable Trend Drawing On Chart:

→ Visually represents the trend filter directly on the chart for easy reference.

→ Enable 'Drawing On Chart' to see the allowed regions overlaid on the trading chart with arrows.

⚙️ Enable VWAP Filter:

🎯 Purpose:

→ Blocks trades based on distance percent between price and volume weighted average price.

💡 How to Use:

→ Enable 'VWAP Filter'.

→ Set Timeframe as minutes and distance as percent.

⛓ Exit on Crossing with VWAP:

→ Automatically closes a position when the closing price of a candle crosses the VWAP.

→ Choose "Enable", 'Exit on Crossing with VWAP' in the settings.

⛓ Enable Drawing On Chart:

→ Visually represents the trend filter directly on the chart for easy reference.

→ Enable 'Drawing On Chart' to see the allowed regions overlaid on the trading chart with arrows.

█ LIQUIDATION FILTER SETTINGS

Liquidation filter compares the volume data of futures and spot markets.

Large differences in volume indicate unexpected market conditions, such as massive trading activities, which may signal liquidations.

Features:

⚙️ Enable Liquidation Filter:

🎯 Purpose:

→ Blocks trades based on extra ordinary volume differences in spot and futures market.

💡 How to Use:

→ Enable 'Liquidation Filter'.

→ Set behavior to react during that market conditions.

→ Set base amount to filter volume. This amount changes according to timeframe, you should find right amounts.

→ Liquidation candle count means, it is sum of liquidated candle count in last 20 bars.If you set 0, it means feature is disabled.

→ Detection, try to select the spot and perpetual symbols automatically, symbol names varies, it do not support all symbols, you should choose manually in that situation.

█ AUTOMATED ALERT SETTINGS

Automated Alert Settings are designed to integrate your TradingView script with webhook alerts. These settings allow for enhanced strategy execution and management.

Features:

Enable Webhook Alerts:

🎯 Purpose:

→ Trigger BUY, SELL, CHANGE_DIRECTION or MOVE_STOP_LOSS .

💡 How to Use:

→ Enable 'Webhook Alerts' in the settings.

→ Enter your Strategy Key.

→ Optionally, activate 'Override Allocation Percentage' to bypass the preset allocation percentage.

☢️ Caution:

→ Overriding the allocation percentage may result in trade entry errors due to misalignment between entry cost and available balance.

Enable Custom Alerts:

🎯 Purpose:

→ User can produce unique messages for different purposes.

💡 How to Use:

→ Enable 'Custom Alerts' in the settings.

→ Enter your message format type.

█ DEBUGGING SETTINGS

Debugging Settings are crucial for users who want to analyze and optimize their strategies. These settings provide tools for visualizing alerts on charts and accessing detailed data outputs.

Features:

⚙️ Enable Alert Plotting:

🎯 Purpose:

→ Allows users to visualize trading alerts directly on the chart, aiding in strategy analysis and refinement.

💡 How to Use:

→ Activate 'Alert Plotting' to draw alerts on the chart.

☢️ Caution:

→ It is recommended to disable this feature when creating actual trading alerts, as it can cause latency in signal processing.

⚙️ Enable Debugger Mode:

🎯 Purpose:

→ Facilitates strategy debugging by providing detailed data output in the TradingView Data Window.

💡 How to Use:

→ Turn on 'Debugger Mode' to access real-time data and metrics relevant to your strategy.

⚙️ Enable Table:

🎯 Purpose:

→ Facilitates strategy debugging by providing detailed data output in the TradingView Table on chart.

💡 How to Use:

→ Turn on 'Table' to access last closed candle data and metrics relevant to your strategy.

█ ADDITIONAL SETTINGS

⚙️ Enable Bar Magnifier

⚙️ Enable Using standard OHLC

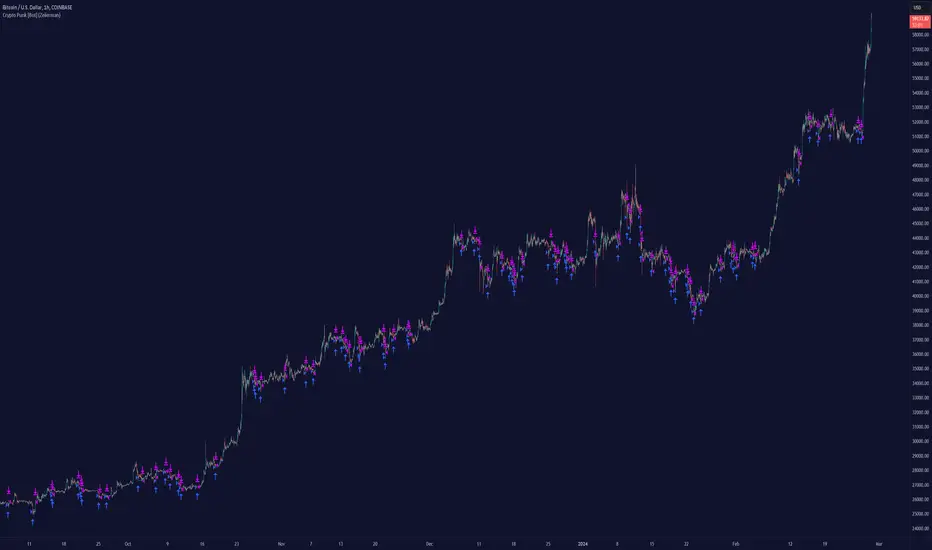

Crypto Punk [Bot] (Zeiierman)█ Overview

The Crypto Punk (Zeiierman) is a trading strategy designed for the dynamic and volatile cryptocurrency market. It utilizes algorithms that incorporate price action analysis and principles inspired by Geometric Brownian Motion (GBM). The bot's core functionality revolves around analyzing differences in high and low prices over various timeframes, estimating drift (trend) and volatility, and applying this information to generate trading signals.

█ How to use the Crypto Punk Bot

Utilize the Crypto Punk Bot as a technical analysis tool to enhance your trading strategy. The signals generated by the bot can serve as a confirmation of your existing approach to entering and exiting the market. Additionally, the backtest report provided by the bot is a valuable resource for identifying the optimal settings for the specific market and timeframe you are trading in.

One method is to use the bot's signals to confirm entry points around key support and resistance levels.

█ Key Features

Let's explain how the core features work in the strategy.

⚪ Strategy Filter

The strategy filter plays a vital role in the entries and exits. By setting this filter, the bot can identify higher or lower price points at which to execute trades. Opting for higher values will make the bot target more long-term extreme points, resulting in fewer but potentially more significant signals. Conversely, lower values focus on short-term extreme points, offering more frequent signals focusing on immediate market movements.

How is it calculated?

This filter identifies significant price points within a specified dynamic range by applying linear regression to the absolute deviation of the range, smoothing out fluctuations, and determining the trend direction. The algorithm then normalizes the data and searches for extreme points.

⚪ External AI filter

The external AI filter allows traders to incorporate two external sources as signal filters. This feature is particularly useful for refining their signal accuracy with additional data inputs.

External sources can include any indicator applied to your TradingView chart that produces a plot as an output, such as a moving average, RSI, supertrend, MACD, etc. Traders can use these indicators of their choice to set filters for screening signals within the strategy.

This approach offers traders increased flexibility to select filters that align with their trading style. For instance, one trader might prefer to take trades when the price is above a moving average, while another might opt for trades when the MACD is below the MACD signal line. These external filters enable traders to choose options that best fit their trading strategies. See the example below. Note that the input sources for the External AI filter can be any indicator applied to the chart, and the input source per se does not make this strategy unique. The AI filter takes the selected input source and applies our function to it. So, if a trader selects RSI as an input filter, RSI is not unique, but how the source is computed within the AI functions is.

How is it calculated?

Once the external filters are selected and enabled within the settings panel, our AI function is applied to enhance the filter's ability to execute trades, even when the set conditions of the filter are not met. For instance, if a trader wants to take trades only when the price is above a moving average, the AI filter can actually execute trades even if the price is below the moving average.

The filter works by combining k-nearest Neighbors (KNN) with Geometric Brownian Motion (GBM) involves first using GBM to model the historical price trends of an asset, identifying patterns of drift and volatility. KNN is then applied to compare the current market conditions with historical instances, identifying the closest matches based on similar market behaviors. By examining the drift values of these nearest historical neighbors, KNN predicts the current trend's direction.

The AI adaptability value is a setting that determines how flexible the AI algorithm is when applying the external AI filter. Setting the adaptability to 10 indicates minimal adaptability, suggesting that the bot will strictly adhere to the set filter criteria. On the other hand, a higher adaptability value grants the algorithm more leeway to "think outside the box," allowing it to consider signals that may not strictly meet the filter criteria but are deemed viable trading opportunities by the AI.

█ Examples

In this example, the RSI is used to filter out signals when the RSI is below the smoothing line, indicating that prices are declining.

Note that the external filter is specifically designed to work with either 'LONG ONLY' or 'SHORT ONLY' modes; it does not apply when the bot is set to trade on 'BOTH' modes. For 'LONG ONLY' positions, the filter criteria are met when source 1 is greater than source 2 (source 1 >= source 2). Conversely, for 'SHORT ONLY' positions, the filter criteria require source 1 to be less than source 2 (source 1 <= source 2).

Examples of Filter Usage:

Long Signals: To receive long signals when the closing price is higher than a moving average, set Source 1 to the 'close' price and Source 2 to a moving average value. This setup ensures that signals are generated only when the closing price exceeds the moving average, indicating a potential upward trend.

█ Settings

⚪ Set Timeframe

Choosing the correct entry and exit timeframes is crucial for the bot's performance. The general guideline is to select a timeframe that is higher than the one currently displayed on the trading chart but still relatively close in duration. For instance, if trading on a 1-minute chart, setting the bot's Timeframe to 5 minutes is advisable.

⚪ Entry

Traders have the flexibility to configure the bot according to their trading strategy, allowing them to choose whether the bot should engage in long positions only, short positions only or both. This customization ensures that the bot aligns with the trader's market outlook and risk tolerance.

⚪ Pyramiding

Pyramiding functionality is available to enhance the bot's trading strategy. If the current position experiences a drawdown by a specified number of points, the bot is programmed to add new positions to the existing one, potentially capitalizing on lower prices to average down the entry cost. To utilize this feature, access the settings panel, navigate to 'Properties,' and look for 'Pyramiding' to specify the number of times the bot can re-enter the market (e.g., setting it to 2 allows for two additional entries).

⚪ Risk Management

The bot incorporates several risk management methods, including a regular stop loss, trailing stop, and risk-reward-based stop loss and exit strategies. These features assist traders in managing their risk.

Stop Loss

Trailing Stop

⚪ Trading on specific days

This feature allows trading on specific days by setting which days of the week the bot can execute trades on. It enables traders to tailor their strategies according to market behavior on particular days.

⚪ Alerts

Alerts can be set for entry, exit, and risk management. This feature allows traders to automate their trading strategy, ensuring timely actions are taken according to predefined criteria.

█ How is Crypto Punk calculated?

The Crypto Punk Bot is a trading bot that utilizes a combination of price action analysis and elements inspired by Geometric Brownian Motion (GBM) to generate buy and sell signals for cryptocurrencies. The bot focuses on analyzing the difference between high and low prices over various timeframes, alongside estimates of drift (trend) and volatility derived from GBM principles.

Timeframe Analysis for Price Action

The bot examines multiple timeframes (e.g., daily, weekly) to identify the range between the highest and lowest prices within each period. This range analysis helps in understanding market volatility and the potential for significant price movements. The algorithm calculates the trading range by applying maximum and minimum functions to the set of prices over your selected timeframe. It then subtracts these values to determine the range's width. This method offers a quantitative measure of the asset's price volatility for the specified period.

Estimating Drift (Trend)

The bot estimates the drift component, which reflects the underlying trend or expected return of the cryptocurrency. The algorithm does this by estimating the drift (trend) using Geometric Brownian Motion (GBM), which involves determining an asset's average rate of return over time, reflecting the asset's expected direction of movement.

Estimating Volatility

Volatility is estimated by calculating the standard deviation of the logarithmic returns of the cryptocurrency's price over the same timeframe used for the drift calculation. Geometric Brownian Motion (GBM) involves measuring the extent of variation or dispersion in the returns of an asset over time. In the context of GBM, volatility quantifies the degree to which the price of an asset is expected to fluctuate around its drift.

Combining Drift and Volatility for Signal Generation

The bot uses the calculated drift and volatility to understand the current market conditions. A higher drift coupled with manageable volatility may indicate a strong upward trend, suggesting a potential buy signal. Conversely, a low or negative drift with increasing volatility might suggest a weakening market, triggering a sell signal.

█ Strategy Properties

This script backtest is done on the 1 hour chart Bitcoin, using the following backtesting properties:

Balance (default): 10 000 (default base currency)

Order Size: 10% of the equity

Commission: 0.05 %

Slippage: 500 ticks

Stop Loss: Risk Reward set to 1

These parameters are set to provide an accurate representation of the backtesting environment. It's important to recognize that default settings may vary for several reasons outlined below:

Order Size: The standard is set at one contract to facilitate compatibility with a wide range of instruments, including futures.

Commission: This fee is subject to fluctuation based on the specific market and financial instrument, and as such, there isn't a standard rate that will consistently yield accurate outcomes.

We advise users to customize the Script Properties in the strategy settings to match their personal trading accounts and preferred platforms. This adjustment is crucial for obtaining practical insights from the deployed strategies.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Платный скрипт

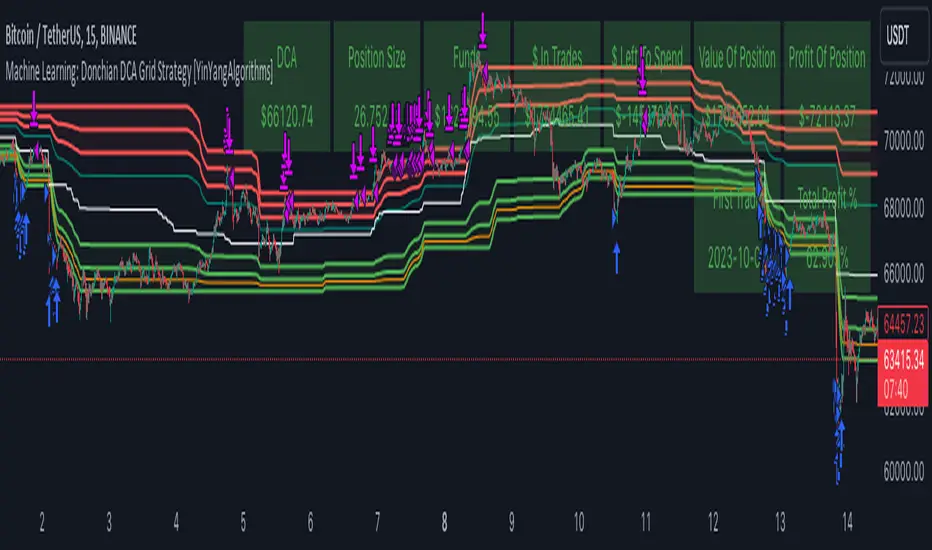

CryptoGraph Dynamic DCAA system to backtest and automate comprehensive trading strategies

═════════════════════════════════════════════════════════════════════════

🟣 Supporting Your Trades

CryptoGraph Dynamic DCA serves as a comprehensive tool on TradingView, designed to refine your approach to cryptocurrency trading. It utilises dynamic dollar-cost averaging (DCA), based on external indicator sources, to provide structured market entry and exit strategies. Suitable for both short-term trading and long-term portfolio management, CryptoGraph Dynamic DCA can offer a methodical way to support your trading decisions.