ADR TableTrack volatility and session momentum in real-time with customizable precision.

Key Features:

Average Daily Range (ADR): Configurable length (default 5 days), based on previous daily high–low ranges.

Session Anchor Options: Choose anchor at 4 am NY, 6 pm NY, 9:30 am NY, 8:30 am NY, Previous Day Close, or Current Bar.

Session Range & %ADR: Displays the real-time range from the chosen anchor, plus what percentage of ADR has been covered.

High / Low Target Levels: Calculates ADR targets based on anchor: anchor ± ADR.

Optional Target Lines: Draw horizontal lines for high and low targets across the session; customize color and width.

Dynamic Table Display: User-selectable table size and text size (Tiny to Huge) for optimal readability.

Robust Anchor Logic: Uses the first bar at-or-after anchor time each NY day, ensuring stability even on irregular intraday timeframes.

How to Use

Choose your anchor in settings.

View ADR, session range (with %ADR), and target price levels in the top-right pane.Toggle High/Low lines to overlay targets on the chart.

Adjust table and text size to match your workspace.

Why It Matters

Quickly assess where price stands relative to typical volatility.

Easily identify intraday price exhaustion or breakout zones.

Anchor flexibility enables use for both futures and equities, aligning with your trading session.

Clean, professional display—no clutter, no guesswork.

Поиск скриптов по запросу "track"

Today's Daily LevelsTrack daily price action like a pro with instant visibility of key levels, percentages, and P&L values - all in one clean view.

• Shows Daily Open, High, Low & Median levels

• Dynamic color-coding: green above open, red below

• Real-time price labels with:

Exact price levels

% distance between levels

Point values

Dollar values per contract

• Auto-repaints on timeframe changes

• 30min alerts for median crosses

Daily Price LevelsTrack daily price action like a pro with instant visibility of key levels, percentages, and P&L values - all in one clean view."

Bullet points:

• Shows Daily Open, High, Low & Median levels

• Dynamic color-coding: green above open, red below

• Real-time price labels with:

Exact price levels

% distance between levels

Point values

Dollar values per contract

• Auto-repaints on timeframe changes

• 30min alerts for median crosses

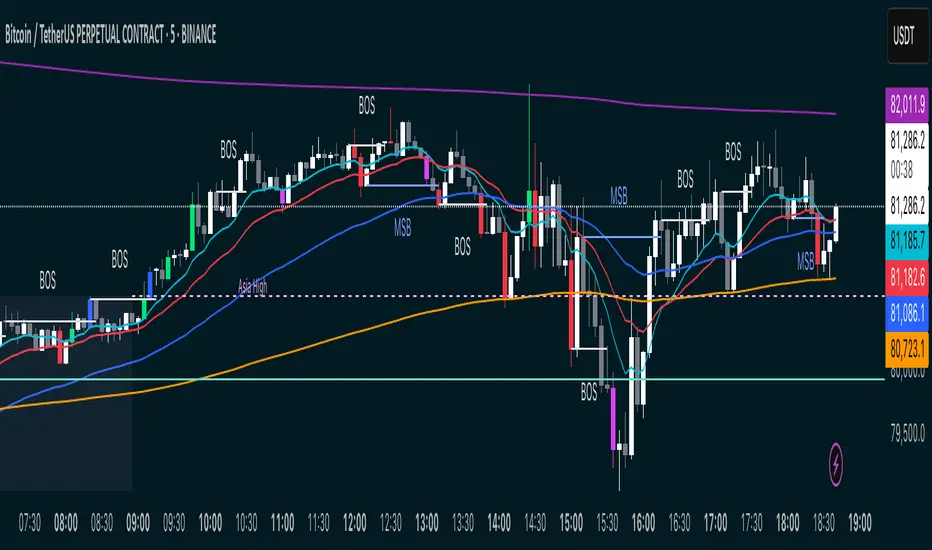

MSB BOS Market Structure [FTB]Track Market Structure Breaks (MSB) and Breaks of Structure (BOS) on your charts. This indicator does exactly that without clutter and with easy-to-spot.

🔑 Features:

MSB (Market Structure Break): Shows when price flips and breaks the previous high/low — possible start of a new trend.

BOS (Break of Structure): Highlights key structural breakouts in line with the existing trend.

✅ Pivot-Based Analysis (Body Focused)

Uses candle body-based pivot highs and lows to find clean market structure points (no wicks confusion here!).

Adjustable pivot strength — control how many candles you want on either side to define a swing.

✅ Clean Visual Markings

MSB and BOS lines with optional labels so you see exactly where breaks happen.

Customizable line style (Solid, Dashed, Dotted) to match your chart aesthetic.

Optional pivot markers to show minor swing highs/lows.

✅ Alerts Ready

Set alerts for any MSB or BOS, or filter to specific bullish/bearish breaks — never miss a key level again

💡 How to Use This Indicator:

Identify Trend Shifts: Use MSB to spot early trend reversals — when a previous structure breaks against the trend.

Catch Continuations: Watch for BOS to confirm trend continuation — great for riding the trend!

⚙️ Settings You Can Adjust:

Pivot Strength: How many candles to look back and forward for swing points (default: 3).

Show Pivots: Optional — highlight swing highs and lows for extra clarity.

Federal Funds Rate Projections [tedtalksmacro]Track the Federal Funds Rate projections for each month via the Fed Funds Rate Futures Contracts CBOT:ZQ1!

This will be updated monthly to ensure that the current and relevant contracts are implemented.

Traders can use this to speculate on whether the Federal Reserve is likely to raise, cut or do nothing to their key interest rate at the next meeting.

FANG INDICATORTrack the strength of any group of stocks that are driving markets. This defaults to FANG. In the settings, replace the symbols to better fit the environment such as replacing NFLX with AAPL.

Multi Timeframe Rolling Bitmex Liquidation LevelsTrack Bitmex liquidations levels in real-time with a rolling VWMA or VWAP basis.

Allows the input of a different time frame if you wish.

200/100 vs 190/80 EMA [jarederaj]Track the 200/100 EMA cross Vs the 180/90 EMA cross. Also, see the dates when these periods start on the chart.

Consecutive Highs/LowsTrack consecutive new highs/lows outside the Donchian range. Fans of the oldschool Turtle Strategy should enjoy the visualization.

Same logic as my "Walking the Bands" script, just with Donchian breaks instead of Bollinger tags.

Altcoin PortfolioTrack your altcoin portfolio balance in Fiat currency.

Make sure to open the data window to the right of your charts, it makes everything alot easier to read at a glance.

To learn more about customizing this script to fit your portfolio, watch the video here: youtu.be

To get more cool scripts and up-to-date information about Autoview, join us in slack slack.with.pink

As per the usual, we hope this script helps with your trading venture.

Good luck, and happy trading.

SMC Ultimate: Command Center @darshaksscTitle: SMC Ultimate: Command Center

Description: This indicator is a specialized Smart Money Concepts (SMC) toolkit meticulously adjusted and optimized for the unique volatility and volume profiles of the Indian markets, specifically Nifty 50 and Bank Nifty.

Unlike other SMC tools, this version uses displacement logic tuned to the Average True Range (ATR) of Indian indices to identify high-probability Institutional Order Blocks while filtering out retail noise.

Key Features:

1). Institutional Order Blocks: Automatically detects and plots Supply/Demand zones where significant institutional volume (displacement) has entered the market.

2). Optimized for Nifty/BankNifty: Sensitivity parameters have been adjusted to handle the explosive moves often seen in the NSE sessions.

3). Live Command Center: A movable, high-detail dashboard that tracks:

4). Real-Time Day High/Low: Accurate intraday tracking that resets with each session.

5). Volume Force: Measures current volume relative to the average to spot institutional activity.

6).Trend Bias (50 EMA): Immediate directional context.

7). Momentum (RSI) & Strength (ADX): To confirm if a breakout is genuine or a trap.

8). Auto-Mitigation: Zones are automatically removed once price closes through them, ensuring a clean and professional workspace.

9). Theme Support: Includes built-in Light and Dark mode options for the dashboard to match any chart setup.

How to Use:

1). Identify the Zone: Wait for a Green (Demand) or Red (Supply) box to form.

2). Confirm Bias: Use the "TREND" and "VOL FORCE" metrics in the dashboard to confirm institutional intent.

3). Wait for Retest: High-probability entries occur when price returns to test a fresh zone without closing through it.

Disclaimer: This script is for educational and technical analysis purposes only. It is fully TradingView Policy compliant and does not repaint.

Tradehook.tech-MTMGBS- OTE Price Action HTF Trend DependentProfessional ICT-inspired strategy combining Optimal Trade Entry (OTE) with Dealing Range Theory, featuring HTF trend dependency, smart money concepts, and multi-timeframe confluence.

█ OVERVIEW

OTE Price Action Model #1 (OTE•PAM1 Pro) is a comprehensive trading strategy

built on institutional trading concepts. It combines Optimal Trade Entry (OTE)

zones with Dealing Range Theory to identify high-probability entries that

align with higher timeframe trend direction.

The strategy automatically adapts to market conditions:

• BULLISH HTF → Only generates LONG signals in discount zones

• BEARISH HTF → Only generates SHORT signals in premium zones

This ensures you're always trading WITH the trend, not against it.

█ PRICE ACTION MODEL #1 RULES

The strategy implements the following systematic approach:

┌─────────────────────────────────────────────────────────┐

│ BULLISH SETUP │

├───────────────────────────────────────────────────────┤

│ ✓ HTF Trend is BULLISH (EMA 9 > EMA 21, Price > EMA 50) │

│ ✓ Price is in DISCOUNT zone of Dealing Range (below 50%) │

│ ✓ Current time is BEFORE 10AM │

│ ✓ Day is Monday-Wednesday (ideal) or Thursday (conditional)│

│ ✓ Price enters OTE Zone (62%-79% Fibonacci retracement) │

│ ✓ Bullish candle confirmation │

└───────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────┐

│ ENTRY EXECUTION │

├─────────────────────────────────────────────────────────┤

│ • Entry: 62% Fib Level + 5 ticks │

│ • Stop Loss: OTE Anchor Low - 5 ticks │

│ • TP1: OTE Anchor High (Swing High) │

│ • TP2: 161.8% Fibonacci Extension │

│ • TP3: 200% Fibonacci Extension (Runner) │

└───────────────────────────────────────────────────────┘

┌─────────────────────────────────────────────────────────┐

│ EXIT MANAGEMENT │

├─────────────────────────────────────────────────────────┤

│ 1. Take 33% at TP1 → Move stop to breakeven + 10 ticks │

│ 2. Take 33% at TP2 → Trail stop on swing lows │

│ 3. Runner (34%) → Exit on CISD or TP3 │

│ 4. CISD Exit: Close if Change in State of Delivery occurs │

└─────────────────

█ KEY FEATURES

▸ HTF TREND DEPENDENCY

Strategy only generates signals aligned with higher timeframe trend.

Configurable HTF (default: 4H). Prevents counter-trend trades.

▸ DEALING RANGE THEORY

Automatically calculates premium/discount zones.

Visual zones: Extreme Premium, Premium, Discount, Extreme Discount.

Only enters LONGS in discount, SHORTS in premium.

▸ OPTIMAL TRADE ENTRY (OTE)

Identifies 62%-79% Fibonacci retracement zones.

Dynamic calculation based on recent swing highs/lows.

OTE zones only display when aligned with HTF trend.

▸ SMART MONEY CONCEPTS

• CISD Detection (Change in State of Delivery)

• Displacement candle identification

• Institutional order flow analysis

• Swing structure tracking

▸ SESSION & KILLZONE FILTERS

• Configurable "No trades after X AM" (default: 10AM)

• London Killzone highlighting

• New York Killzone highlighting

• Day-of-week filters (Thu conditional on price < prev high)

▸ ADVANCED EXIT MANAGEMENT

• Three-tier partial profit system

• Automatic breakeven adjustment

• Swing-based trailing stop for runners

• CISD-triggered exits

█ RECOMMENDED SETTINGS

┌────────────────┬─────────────────────────────────────┐

│ INSTRUMENT │ SETTINGS │

├────────────────┼─────────────────────────────────────┤

│ ES / MES │ Tick Size: 0.25, HTF: 240 (4H) │

│ NQ / MNQ │ Tick Size: 0.25, HTF: 240 (4H) │

│ CL / MCL │ Tick Size: 0.01, HTF: 240 (4H) │

│ FOREX │ Tick Size: 0.0001, HTF: 240 (4H) │

│ CRYPTO │ Tick Size: 0.01, HTF: 240 (4H) │

└────────────────┴─────────────────────────────────────┘

█ HOW TO USE

1. Add to your chart (recommended: 5-minute timeframe)

2. Configure the Higher Timeframe for trend (default: 4H)

3. Adjust tick size for your instrument

4. Set your preferred killzone times

5. Wait for signals aligned with HTF trend

6. Strategy automatically manages entries and exits

█ VISUAL GUIDE

🟢 Green Background = HTF Bullish (look for LONGS)

🔴 Red Background = HTF Bearish (look for SHORTS)

🔵 Blue Zone = OTE Entry Zone

💚 Green Fill = Discount Zone (buy zone)

🟠 Orange Fill = Premium Zone (sell zone)

█ ALERTS

• 🎯 LONG Entry - Bullish entry signal triggered

• 🎯 SHORT Entry - Bearish entry signal triggered

• 💎 OTE Zone - Price entered OTE zone

• ⚠️ CISD - Change in State of Delivery detected

█ DISCLAIMER

This strategy is for educational purposes only. Trading involves

substantial risk of loss. Past performance does not guarantee future

results. Always use proper risk management and never risk more than

you can afford to lose.

The developer is not responsible for any financial losses incurred

from using this strategy. Backtest thoroughly and paper trade before

risking real capital.

█ VERSION HISTORY

v1.0 - Initial release

• Full Price Action Model #1 implementation

• HTF trend dependency

• Multi-partial exit system

• CISD detection

• Comprehensive visual suite

█ CREDITS

Based on ICT (Inner Circle Trader) concepts including:

• Optimal Trade Entry (OTE)

• Dealing Range Theory

• Smart Money Concepts

• Killzone Trading

═══════════════════════════════════════════════════════════

Made with ❤️ for the trading community

═══════════════════════════════════════════════════════════

MACDHistogram CrossoverScript Title:

MACD Histogram Zero-Cross with 9/20 EMA Overlay

Script Description:

This indicator is a combined trend and momentum tool designed to identify market shifts directly on the price chart. It tracks MACD Histogram crossovers while providing 9 and 20 Exponential Moving Average (EMA) filters for trend confirmation.

How it Works:

The script monitors the MACD Histogram (12, 26, 9) for "Zero-Cross" events and labels them for maximum clarity:

Green "L" (Long/Bullish): Appears below the candle when the Histogram moves from negative to positive. This indicates a shift toward bullish momentum.

Red "P" (Put/Bearish): Appears above the candle when the Histogram moves from positive to negative. This indicates a shift toward bearish momentum.

Trend Filter Integration:

To help filter out "fake" signals in choppy markets, the script includes two essential EMAs:

9 EMA (Blue): Fast-reacting line for short-term price action.

20 EMA (Orange): Medium-term trend line.

Trading Logic:

Bullish Setup: Look for the green "L" when price is trading above the 9 and 20 EMAs.

Bearish Setup: Look for the red "P" when price is trading below the 9 and 20 EMAs.

Exit/Caution: If an "L" or "P" appears against the EMA trend, it may signal a period of consolidation or a potential reversal.

Features:

Clean Visuals: Signal letters are sized small to avoid obstructing price action.

Real-time Overlay: Calculates MACD momentum in the background while keeping your main chart focused on price.

Versatile: Works on any timeframe (Intraday, Daily, or Weekly).

Disclaimer: This script is for educational purposes and should be used as part of a comprehensive trading strategy. Always practice proper risk management.

DeeptestDeeptest: Quantitative Backtesting Library for Pine Script

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ OVERVIEW

Deeptest is a Pine Script library that provides quantitative analysis tools for strategy backtesting. It calculates over 100 statistical metrics including risk-adjusted return ratios (Sharpe, Sortino, Calmar), drawdown analysis, Value at Risk (VaR), Conditional VaR, and performs Monte Carlo simulation and Walk-Forward Analysis.

█ WHY THIS LIBRARY MATTERS

Pine Script is a simple yet effective coding language for algorithmic and quantitative trading. Its accessibility enables traders to quickly prototype and test ideas directly within TradingView. However, the built-in strategy tester provides only basic metrics (net profit, win rate, drawdown), which is often insufficient for serious strategy evaluation.

Due to this limitation, many traders migrate to alternative backtesting platforms that offer comprehensive analytics. These platforms require other language programming knowledge, environment setup, and significant time investment—often just to test a simple trading idea.

Deeptest bridges this gap by bringing institutional-level quantitative analytics directly to Pine Script. Traders can now perform sophisticated analysis without leaving TradingView or learning complex external platforms. All calculations are derived from strategy.closedtrades.* , ensuring compatibility with any existing Pine Script strategy.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ ORIGINALITY AND USEFULNESS

This library is original work that adds value to the TradingView community in the following ways:

1. Comprehensive Metric Suite: Implements 112+ statistical calculations in a single library, including advanced metrics not available in TradingView's built-in tester (p-value, Z-score, Skewness, Kurtosis, Risk of Ruin).

2. Monte Carlo Simulation: Implements trade-sequence randomization to stress-test strategy robustness by simulating 1000+ alternative equity curves.

3. Walk-Forward Analysis: Divides historical data into rolling in-sample and out-of-sample windows to detect overfitting by comparing training vs. testing performance.

4. Rolling Window Statistics: Calculates time-varying Sharpe, Sortino, and Expectancy to analyze metric consistency throughout the backtest period.

5. Interactive Table Display: Renders professional-grade tables with color-coded thresholds, tooltips explaining each metric, and period analysis cards for drawdowns/trades.

6. Benchmark Comparison: Automatically fetches S&P 500 data to calculate Alpha, Beta, and R-squared, enabling objective assessment of strategy skill vs. passive investing.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ KEY FEATURES

Performance Metrics

Net Profit, CAGR, Monthly Return, Expectancy

Profit Factor, Payoff Ratio, Sample Size

Compounding Effect Analysis

Risk Metrics

Sharpe Ratio, Sortino Ratio, Calmar Ratio (MAR)

Martin Ratio, Ulcer Index

Max Drawdown, Average Drawdown, Drawdown Duration

Risk of Ruin, R-squared (equity curve linearity)

Statistical Distribution

Value at Risk (VaR 95%), Conditional VaR

Skewness (return asymmetry)

Kurtosis (tail fatness)

Z-Score, p-value (statistical significance testing)

Trade Analysis

Win Rate, Breakeven Rate, Loss Rate

Average Trade Duration, Time in Market

Consecutive Win/Loss Streaks with Expected values

Top/Worst Trades with R-multiple tracking

Advanced Analytics

Monte Carlo Simulation (1000+ iterations)

Walk-Forward Analysis (rolling windows)

Rolling Statistics (time-varying metrics)

Out-of-Sample Testing

Benchmark Comparison

Alpha (excess return vs. benchmark)

Beta (systematic risk correlation)

Buy & Hold comparison

R-squared vs. benchmark

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK START

Basic Usage

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as *

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ METRIC EXPLANATIONS

The Deeptest table displays 23 metrics across the main row, with 23 additional metrics in the complementary row. Each metric includes detailed tooltips accessible by hovering over the value.

Main Row — Performance Metrics (Columns 0-6)

Net Profit — (Final Equity - Initial Capital) / Initial Capital × 100

— >20%: Excellent, >0%: Profitable, <0%: Loss

— Total return percentage over entire backtest period

Payoff Ratio — Average Win / Average Loss

— >1.5: Excellent, >1.0: Good, <1.0: Losses exceed wins

— Average winning trade size relative to average losing trade. Breakeven win rate = 100% / (1 + Payoff)

Sample Size — Count of closed trades

— >=30: Statistically valid, <30: Insufficient data

— Number of completed trades. Includes 95% confidence interval for win rate in tooltip

Profit Factor — Gross Profit / Gross Loss

— >=1.5: Excellent, >1.0: Profitable, <1.0: Losing

— Ratio of total winnings to total losses. Uses absolute values unlike payoff ratio

CAGR — (Final / Initial)^(365.25 / Days) - 1

— >=10%: Excellent, >0%: Positive growth

— Compound Annual Growth Rate - annualized return accounting for compounding

Expectancy — Sum of all returns / Trade count

— >0.20%: Excellent, >0%: Positive edge

— Average return per trade as percentage. Positive expectancy indicates profitable edge

Monthly Return — Net Profit / (Months in test)

— >0%: Profitable month average

— Average monthly return. Geometric monthly also shown in tooltip

Main Row — Trade Statistics (Columns 7-14)

Avg Duration — Average time in position per trade

— Mean holding period from entry to exit. Influenced by timeframe and trading style

Max CW — Longest consecutive winning streak

— Maximum consecutive wins. Expected value = ln(trades) / ln(1/winRate)

Max CL — Longest consecutive losing streak

— Maximum consecutive losses. Important for psychological risk tolerance

Win Rate — Wins / Total Trades

— Higher is better

— Percentage of profitable trades. Breakeven win rate shown in tooltip

BE Rate — Breakeven Trades / Total Trades

— Lower is better

— Percentage of trades that broke even (neither profit nor loss)

Loss Rate — Losses / Total Trades

— Lower is better

— Percentage of unprofitable trades. Together with win rate and BE rate, sums to 100%

Frequency — Trades per month

— Trading activity level. Displays intelligently (e.g., "12/mo", "1.5/wk", "3/day")

Exposure — Time in market / Total time × 100

— Lower = less risk

— Percentage of time the strategy had open positions

Main Row — Risk Metrics (Columns 15-22)

Sharpe Ratio — (Return - Rf) / StdDev × sqrt(Periods)

— >=3: Excellent, >=2: Good, >=1: Fair, <1: Poor

— Measures risk-adjusted return using total volatility. Annualized using sqrt(252) for daily

Sortino Ratio — (Return - Rf) / DownsideDev × sqrt(Periods)

— >=2: Excellent, >=1: Good, <1: Needs improvement

— Similar to Sharpe but only penalizes downside volatility. Can be higher than Sharpe

Max DD — (Peak - Trough) / Peak × 100

— <5%: Excellent, 5-15%: Moderate, 15-30%: High, >30%: Severe

— Largest peak-to-trough decline in equity. Critical for risk tolerance and position sizing

RoR — Risk of Ruin probability

— <1%: Excellent, 1-5%: Acceptable, 5-10%: Elevated, >10%: Dangerous

— Probability of losing entire trading account based on win rate and payoff ratio

R² — R-squared of equity curve vs. time

— >=0.95: Excellent, 0.90-0.95: Good, 0.80-0.90: Moderate, <0.80: Erratic

— Coefficient of determination measuring linearity of equity growth

MAR — CAGR / |Max Drawdown|

— Higher is better, negative = bad

— Calmar Ratio. Reward relative to worst-case loss. Negative if max DD exceeds CAGR

CVaR — Average of returns below VaR threshold

— Lower absolute is better

— Conditional Value at Risk (Expected Shortfall). Average loss in worst 5% of outcomes

p-value — Binomial test probability

— <0.05: Significant, 0.05-0.10: Marginal, >0.10: Likely random

— Probability that observed results are due to chance. Low p-value means statistically significant edge

Complementary Row — Extended Metrics

Compounding — (Compounded Return / Total Return) × 100

— Percentage of total profit attributable to compounding (position sizing)

Avg Win — Sum of wins / Win count

— Average profitable trade return in percentage

Avg Trade — Sum of all returns / Total trades

— Same as Expectancy (Column 5). Displayed here for convenience

Avg Loss — Sum of losses / Loss count

— Average unprofitable trade return in percentage (negative value)

Martin Ratio — CAGR / Ulcer Index

— Similar to Calmar but uses Ulcer Index instead of Max DD

Rolling Expectancy — Mean of rolling window expectancies

— Average expectancy calculated across rolling windows. Shows consistency of edge

Avg W Dur — Avg duration of winning trades

— Average time from entry to exit for winning trades only

Max Eq — Highest equity value reached

— Peak equity achieved during backtest

Min Eq — Lowest equity value reached

— Trough equity point. Important for understanding worst-case absolute loss

Buy & Hold — (Close_last / Close_first - 1) × 100

— >0%: Passive profit

— Return of simply buying and holding the asset from backtest start to end

Alpha — Strategy CAGR - Benchmark CAGR

— >0: Has skill (beats benchmark)

— Excess return above passive benchmark. Positive alpha indicates genuine value-added skill

Beta — Covariance(Strategy, Benchmark) / Variance(Benchmark)

— <1: Less volatile than market, >1: More volatile

— Systematic risk correlation with benchmark

Avg L Dur — Avg duration of losing trades

— Average time from entry to exit for losing trades only

Rolling Sharpe/Sortino — Dynamic based on win rate

— >2: Good consistency

— Rolling metric across sliding windows. Shows Sharpe if win rate >50%, Sortino if <=50%

Curr DD — Current drawdown from peak

— Lower is better

— Present drawdown percentage. Zero means at new equity high

DAR — CAGR adjusted for target DD

— Higher is better

— Drawdown-Adjusted Return. DAR^5 = CAGR if max DD = 5%

Kurtosis — Fourth moment / StdDev^4 - 3

— ~0: Normal, >0: Fat tails, <0: Thin tails

— Measures "tailedness" of return distribution (excess kurtosis)

Skewness — Third moment / StdDev^3

— >0: Positive skew (big wins), <0: Negative skew (big losses)

— Return distribution asymmetry

VaR — 5th percentile of returns

— Lower absolute is better

— Value at Risk at 95% confidence. Maximum expected loss in worst 5% of outcomes

Ulcer — sqrt(mean(drawdown^2))

— Lower is better

— Ulcer Index - root mean square of drawdowns. Penalizes both depth AND duration

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ MONTE CARLO SIMULATION

Purpose

Monte Carlo simulation tests strategy robustness by randomizing the order of trades while keeping trade returns unchanged. This simulates alternative equity curves to assess outcome variability.

Method

Extract all historical trade returns

Randomly shuffle the sequence (1000+ iterations)

Calculate cumulative equity for each shuffle

Build distribution of final outcomes

Output

The stress test table shows:

Median Outcome: 50th percentile result

5th Percentile: Worst 5% of outcomes

95th Percentile: Best 95% of outcomes

Success Rate: Percentage of simulations that were profitable

Interpretation

If 95% of simulations are profitable: Strategy is robust

If median is far from actual result: High variance/unreliability

If 5th percentile shows large loss: High tail risk

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ WALK-FORWARD ANALYSIS

Purpose

Walk-Forward Analysis (WFA) is the gold standard for detecting strategy overfitting. It simulates real-world trading by dividing historical data into rolling "training" (in-sample) and "validation" (out-of-sample) periods. A strategy that performs well on unseen data is more likely to succeed in live trading.

Method

The implementation uses a non-overlapping window approach following AmiBroker's gold standard methodology:

Segment Calculation: Total trades divided into N windows (default: 12), IS = ~75%, OOS = ~25%, Step = OOS length

Window Structure: Each window has IS (training) followed by OOS (validation). Each OOS becomes the next window's IS (rolling forward)

Metrics Calculated: CAGR, Sharpe, Sortino, MaxDD, Win Rate, Expectancy, Profit Factor, Payoff

Aggregation: IS metrics averaged across all IS periods, OOS metrics averaged across all OOS periods

Output

IS CAGR: In-sample annualized return

OOS CAGR: Out-of-sample annualized return ( THE key metric )

IS/OOS Sharpe: In/out-of-sample risk-adjusted return

Success Rate: % of OOS windows that were profitable

Interpretation

Robust: IS/OOS CAGR gap <20%, OOS Success Rate >80%

Some Overfitting: CAGR gap 20-50%, Success Rate 50-80%

Severe Overfitting: CAGR gap >50%, Success Rate <50%

Key Principles:

OOS is what matters — Only OOS predicts live performance

Consistency > Magnitude — 10% IS / 9% OOS beats 30% IS / 5% OOS

Window count — More windows = more reliable validation

Non-overlapping OOS — Prevents data leakage

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ TABLE DISPLAY

Main Table — Organized into three sections:

Performance Metrics (Cols 0-6): Net Profit, Payoff, Sample Size, Profit Factor, CAGR, Expectancy, Monthly

Trade Statistics (Cols 7-14): Avg Duration, Max CW, Max CL, Win, BE, Loss, Frequency, Exposure

Risk Metrics (Cols 15-22): Sharpe, Sortino, Max DD, RoR, R², MAR, CVaR, p-value

Color Coding

🟢 Green: Excellent performance

🟠 Orange: Acceptable performance

⚪ Gray: Neutral / Fair

🔴 Red: Poor performance

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ IMPLEMENTATION NOTES

Data Source: All metrics calculated from strategy.closedtrades , ensuring compatibility with any Pine Script strategy

Calculation Timing: All calculations occur on barstate.islastconfirmedhistory to optimize performance

Limitations: Requires at least 1 closed trade for basic metrics, 30+ trades for reliable statistical analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK NOTES

➙ This library has been developed and refined over two years of real-world strategy testing. Every calculation has been validated against industry-standard quantitative finance references.

➙ The entire codebase is thoroughly documented inline. If you are curious about how a metric is calculated or want to understand the implementation details, dive into the source code -- it is written to be read and learned from.

➙ This description focuses on usage and concepts rather than exhaustively listing every exported type and function. The library source code is thoroughly documented inline -- explore it to understand implementation details and internal logic.

➙ All calculations execute on barstate.islastconfirmedhistory to minimize runtime overhead. The library is designed for efficiency without sacrificing accuracy.

➙ Beyond analysis, this library serves as a learning resource. Study the source code to understand quantitative finance concepts, Pine Script advanced techniques, and proper statistical methodology.

➙ Metrics are their own not binary good/bad indicators. A high Sharpe ratio with low sample size is misleading. A deep drawdown during a market crash may be acceptable. Study each function and metric individually -- evaluate your strategy contextually, not by threshold alone.

➙ All strategies face alpha decay over time. Instead of over-optimizing a single strategy on one timeframe and market, build a diversified portfolio across multiple markets and timeframes. Deeptest helps you validate each component so you can combine robust strategies into a trading portfolio.

➙ Screenshots shown in the documentation are solely for visual representation to demonstrate how the tables and metrics will be displayed. Please do not compare your strategy's performance with the metrics shown in these screenshots -- they are illustrative examples only, not performance targets or benchmarks.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW-TO

Using Deeptest is intentionally straightforward. Just import the library and call DT.runDeeptest() at the end of your strategy code in main scope. .

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as DT

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

And yes... it's compatible with any TradingView Strategy! 🪄

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ CREDITS

Author: @Fractalyst

Font Library: by @fikira - @kaigouthro - @Duyck

Community: Inspired by the @PineCoders community initiative, encouraging developers to contribute open-source libraries and continuously enhance the Pine Script ecosystem for all traders.

if you find Deeptest valuable in your trading journey, feel free to use it in your strategies and give a shoutout to @Fractalyst -- Your recognition directly supports ongoing development and open-source contributions to Pine Script.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ DISCLAIMER

This library is provided for educational and research purposes. Past performance does not guarantee future results. Always test thoroughly and use proper risk management. The author is not responsible for any trading losses incurred through the use of this code.

Enigma UnlockedENIGMA Indicator: A Comprehensive Market Bias & Success Tracker

The ENIGMA Indicator is a powerful tool designed for traders who aim to identify market bias, track price movements, and evaluate trade performance using multiple timeframes. It combines multiple indicators and advanced logic to provide real-time insights into market trends, helping traders make more informed decisions.

Key Features

1. Multi-Timeframe Bias Calculation:

The ENIGMA Indicator tracks the market bias across multiple timeframes—Daily (D), 4-Hour (H4), 1-Hour (H1), 30-Minute (30M), 15-Minute (15M), 5-Minute (5M), and 1-Minute (1M).

How the Bias is Created:

The Bias is a key feature of the ENIGMA Indicator and is determined by comparing the current price with previous price levels for each timeframe.

- Bullish Bias (1): The market is considered **bullish** if the **current closing price** is higher than the **previous timeframe’s high**. This suggests that the market is trending upwards, and buyers are in control.

- Bearish Bias (-1): The market is considered **bearish** if the **current closing price** is lower than the **previous timeframe’s low**. This suggests that the market is trending downwards, and sellers are in control.

- Neutral Bias (0): The market is considered **neutral** if the price is between the **previous high** and **previous low**, indicating indecision or a range-bound market.

This bias calculation is performed independently for each timeframe. The **Bias** for each timeframe is then displayed in the **Bias Table** on your chart, providing a clear view of market direction across multiple timeframes.

2. **Customizable Table Display:**

- The indicator provides a table that displays the bias for each selected timeframe, clearly marking whether the market is **Bullish**, **Bearish**, or **Neutral**.

- Users can choose where to place the table on the chart: top-left, top-right, bottom-left, bottom-right, or center positions, allowing for easy and personalized chart management.

3. **Win/Loss Tracker:**

- The table also tracks the **success rate** of **buy** and **sell** trades based on price retests of key bias levels.

- For each period (Day, Week, Month), it tracks how often the price has moved in the direction of the initial bias, counting **Buy Wins**, **Sell Wins**, **Buy Losses**, and **Sell Losses**.

- This helps traders assess the effectiveness of the market bias over time and adjust their strategies accordingly.

#### **How the Success Calculation Determines the Success Rate:**

The **Success Calculation** is designed to track how often the price follows the direction of the market bias. It does this by evaluating how the price retests key levels associated with the identified market bias:

1. **Buy Success Calculation**:

- The success of a **Buy Trade** is determined when the price breaks above the **previous high** after a **bullish bias** has been identified.

- If the price continues to move higher (i.e., makes a new high) after breaking the previous high, the **buy trade is considered successful**.

- The indicator tracks how many times this condition is met and counts it as a **Buy Win**.

2. **Sell Success Calculation**:

- The success of a **Sell Trade** is determined when the price breaks below the **previous low** after a **bearish bias** has been identified.

- If the price continues to move lower (i.e., makes a new low) after breaking the previous low, the **sell trade is considered successful**.

- The indicator tracks how many times this condition is met and counts it as a **Sell Win**.

3. **Failure Calculations**:

- If the price does not move as expected (i.e., it does not continue in the direction of the identified bias), the trade is considered a **loss** and is tracked as **Buy Loss** or **Sell Loss**, depending on whether it was a bullish or bearish trade.

The ENIGMA Indicator keeps a running tally of **Buy Wins**, **Sell Wins**, **Buy Losses**, and **Sell Losses** over a set period (which can be customized to Days, Weeks, or Months). These statistics are updated dynamically in the **Bias Table**, allowing you to track your success rate in real-time and gain insights into the effectiveness of the market bias.

#### **Customizable Period Tracking:**

- The ENIGMA Indicator allows you to set custom tracking periods (e.g., 30 days, 2 weeks, etc.). The performance metrics reset after each tracking period, helping you monitor your success in different market conditions.

5. **Interactive Settings:**

- **Lookback Period**: Define how many bars the indicator should consider for bias calculations.

- **Success Tracking**: Set the number of candles to track for calculating the win/loss performance.

- **Time Threshold**: Set a time threshold to help define the period during which price retests are considered valid.

- **Info Tooltip**: You can enable the information tool in the settings to view detailed explanations of how wins and losses are calculated, ensuring you understand how the indicator works and how the results are derived.

#### **How to Use the ENIGMA Indicator:**

1. **Install the Indicator**:

- Add the ENIGMA Indicator to your chart. It will automatically calculate and display the bias for multiple timeframes.

2. **Interpret the Bias Table**:

- The bias table will show whether the market is **Bullish**, **Bearish**, or **Neutral** across different timeframes.

- Look for alignment between the timeframes—when multiple timeframes show the same bias, it may indicate a stronger trend.

3. **Use the Win/Loss Tracker**:

- Track how well your trades align with the bias using the **Win/Loss Tracker**. This helps you refine your strategy by understanding which timeframes and biases lead to higher success rates.

- For example, if you see a high number of **Buy Wins** and a low number of **Sell Wins**, you may decide to focus more on buying during bullish trends and avoid selling during bearish retracements.

4. **Track Your Period Performance**:

- The indicator will automatically track your performance over the set period (Days, Weeks, Months). Use this data to adjust your approach and evaluate the effectiveness of your trading strategy.

5. **Position the Table**:

- Customize the placement of the table on your chart based on your preferences. You can choose from options like **Top Left**, **Top Right**, **Bottom Left**, **Bottom Right**, or **Center** to keep the chart uncluttered.

6. **Adjust Settings**:

- Modify the indicator settings according to your trading style. You can adjust the **Lookback Period**, **Number of Candles to Track**, and **Time Threshold** to match the pace of your trading.

7. **Use the Info Tooltip**:

- Enable the **Info Tool** in the settings to understand how the Buy/Sell Wins and Losses are calculated. The tooltip provides a breakdown of how the indicator tracks price movements and calculates the success rate.

**Conclusion:**

The **ENIGMA Indicator** is designed to help traders make informed decisions by providing a clear view of the market bias and performance data. With the ability to track bias across multiple timeframes and evaluate your trading success, it can be a powerful tool for refining your trading strategies.

Whether you're looking to focus on a single timeframe or analyze multiple timeframes for a stronger bias, the ENIGMA Indicator adapts to your needs, providing both real-time market insights and performance feedback.

Contrarian Period High & LowContrarian Period High & Low

This indicator pairs nicely with the Contrarian 100 MA and can be located here:

Overview

The "Contrarian Period High & Low" indicator is a powerful technical analysis tool designed for traders seeking to identify key support and resistance levels and capitalize on contrarian trading opportunities. By tracking the highest highs and lowest lows over user-defined periods (Daily, Weekly, or Monthly), this indicator plots historical levels and generates buy and sell signals when price breaks these levels in a contrarian manner. A unique blue dot counter and action table enhance decision-making, making it ideal for swing traders, trend followers, and those trading forex, stocks, or cryptocurrencies. Optimized for daily charts, it can be adapted to other timeframes with proper testing.

How It Works

The indicator identifies the highest high and lowest low within a specified period (e.g., daily, weekly, or monthly) and draws horizontal lines for the previous period’s extremes on the chart. These levels act as dynamic support and resistance zones. Contrarian signals are generated when the price crosses below the previous period’s low (buy signal) or above the previous period’s high (sell signal), indicating potential reversals. A blue dot counter tracks consecutive buy signals, and a table displays the count and recommended action, helping traders decide whether to hold or flip positions.

Key Components

Period High/Low Levels: Tracks the highest high and lowest low for each period, plotting red lines for highs and green lines for lows from the bar where they occurred, extending for a user-defined length (default: 200 bars).

Contrarian Signals: Generates buy signals (blue circles) when price crosses below the previous period’s low and sell signals (white circles) when price crosses above the previous period’s high, designed to capture potential reversals.

Blue Dot Tracker: Counts consecutive buy signals (“blue dots”). If three or more occur, it suggests a stronger trend, with the table recommending whether to “Hold Investment” or “Flip Investment.”

Action Table: A 2x2 table in the bottom-right corner displays the blue dot count and action (“Hold Investment” if count ≥ 4, else “Flip Investment”) for quick reference.

Mathematical Concepts

Period Detection: Uses an approximate bar count to define periods (1 bar for Daily, 5 bars for Weekly, 20 bars for Monthly on a daily chart). When a new period starts, the previous period’s high/low is finalized and plotted.

High/Low Tracking:

Highest high (periodHigh) and lowest low (periodLow) are updated within the period.

Lines are drawn at these levels when the period ends, starting from the bar where the extreme occurred (periodHighBar, periodLowBar).

Signal Logic:

Buy signal: ta.crossunder(close , prevPeriodLow) and not lowBroken and barstate.isconfirmed

Sell signal: ta.crossover(close , prevPeriodHigh) and not highBroken and barstate.isconfirmed

Flags (highBroken, lowBroken) prevent multiple signals for the same level within a period.

Blue Dot Counter: Increments on each buy signal, resets on a sell signal or if price exceeds the entry price after three or more buy signals.

Entry and Exit Rules

Buy Signal (Blue Circle): Triggered when the price crosses below the previous period’s low, suggesting a potential oversold condition and buying opportunity. The signal appears as a blue circle below the price bar.

Sell Signal (White Circle): Triggered when the price crosses above the previous period’s high, indicating a potential overbought condition and selling opportunity. The signal appears as a white circle above the price bar.

Blue Dot Tracker:

Increments blueDotCount on each buy signal and sets an entryPrice on the first buy.

Resets on a sell signal or if price exceeds entryPrice after three or more buy signals.

If blueDotCount >= 3, the table suggests holding; if >= 4, it reinforces “Hold Investment.”

Exit Rules: Exit a buy position on a sell signal or when price exceeds the entry price after three or more buy signals. Combine with other tools (e.g., trendlines, support/resistance) for additional confirmation. Always apply proper risk management.

Recommended Usage

The "Contrarian Period High & Low" indicator is optimized for daily charts but can be adapted to other timeframes (e.g., 1H, 4H) with adjustments to the period bar count. It excels in markets with clear support/resistance levels and potential reversal zones. Traders should:

Backtest the indicator on their chosen asset and timeframe to validate signal reliability.

Combine with other technical tools (e.g., moving averages, Fibonacci levels) for stronger trade confirmation.

Adjust barsPerPeriod (e.g., ~120 bars for Weekly on hourly charts) based on the chart timeframe and market volatility.

Monitor the action table to guide position management based on blue dot counts.

Customization Options

Period Type: Choose between Daily, Weekly, or Monthly periods (default: Monthly).

Line Length: Set the length of high/low lines in bars (default: 200).

Show Highs/Lows: Toggle visibility of period high (red) and low (green) lines.

Max Lines to Keep: Limit the number of historical lines displayed (default: 10).

Hide Signals: Toggle buy/sell signal visibility for a cleaner chart.

Table Display: A fixed table in the bottom-right corner shows the blue dot count and action, with yellow (Hold) or green (Flip) backgrounds based on the count.

Why Use This Indicator?

The "Contrarian Period High & Low" indicator offers a unique blend of support/resistance visualization and contrarian signal generation, making it a versatile tool for identifying potential reversals. Its clear visual cues (lines and signals), blue dot tracker, and actionable table provide traders with an intuitive way to monitor market structure and manage trades. Whether you’re a beginner or an experienced trader, this indicator enhances your ability to spot key levels and time entries/exits effectively.

Tips for Users

Test the indicator thoroughly on your chosen market and timeframe to optimize settings (e.g., adjust barsPerPeriod for non-daily charts).

Use in conjunction with price action or other indicators for stronger trade setups.

Monitor the action table to decide whether to hold or flip positions based on blue dot counts.

Ensure your chart timeframe aligns with the selected period type (e.g., daily chart for Monthly periods).

Apply strict risk management to protect against false breakouts.

Happy trading with the Contrarian Period High & Low indicator! Share your feedback and strategies in the TradingView community!

ORB Fusion🎯 CORE INNOVATION: INSTITUTIONAL ORB FRAMEWORK WITH FAILED BREAKOUT INTELLIGENCE

ORB Fusion represents a complete institutional-grade Opening Range Breakout system combining classic Market Profile concepts (Initial Balance, day type classification) with modern algorithmic breakout detection, failed breakout reversal logic, and comprehensive statistical tracking. Rather than simply drawing lines at opening range extremes, this system implements the full trading methodology used by professional floor traders and market makers—including the critical concept that failed breakouts are often higher-probability setups than successful breakouts .

The Opening Range Hypothesis:

The first 30-60 minutes of trading establishes the day's value area —the price range where the majority of participants agree on fair value. This range is formed during peak information flow (overnight news digestion, gap reactions, early institutional positioning). Breakouts from this range signal directional conviction; failures to hold breakouts signal trapped participants and create exploitable reversals.

Why Opening Range Matters:

1. Information Aggregation : Opening range reflects overnight news, pre-market sentiment, and early institutional orders. It's the market's initial "consensus" on value.

2. Liquidity Concentration : Stop losses cluster just outside opening range. Breakouts trigger these stops, creating momentum. Failed breakouts trap traders, forcing reversals.

3. Statistical Persistence : Markets exhibit range expansion tendency —when price accepts above/below opening range with volume, it often extends 1.0-2.0x the opening range size before mean reversion.

4. Institutional Behavior : Large players (market makers, institutions) use opening range as reference for the day's trading plan. They fade extremes in rotation days and follow breakouts in trend days.

Historical Context:

Opening Range Breakout methodology originated in commodity futures pits (1970s-80s) where floor traders noticed consistent patterns: the first 30-60 minutes established a "fair value zone," and directional moves occurred when this zone was violated with conviction. J. Peter Steidlmayer formalized this observation in Market Profile theory, introducing the "Initial Balance" concept—the first hour (two 30-minute periods) defining market structure.

📊 OPENING RANGE CONSTRUCTION

Four ORB Timeframe Options:

1. 5-Minute ORB (0930-0935 ET):

Captures immediate market direction during "opening drive"—the explosive first few minutes when overnight orders hit the tape.

Use Case:

• Scalping strategies

• High-frequency breakout trading

• Extremely liquid instruments (ES, NQ, SPY)

Characteristics:

• Very tight range (often 0.2-0.5% of price)

• Early breakouts common (7 of 10 days break within first hour)

• Higher false breakout rate (50-60%)

• Requires sub-minute chart monitoring

Psychology: Captures panic buyers/sellers reacting to overnight news. Range is small because sample size is minimal—only 5 minutes of price discovery. Early breakouts often fail because they're driven by retail FOMO rather than institutional conviction.

2. 15-Minute ORB (0930-0945 ET):

Balances responsiveness with statistical validity. Captures opening drive plus initial reaction to that drive.

Use Case:

• Day trading strategies

• Balanced scalping/swing hybrid

• Most liquid instruments

Characteristics:

• Moderate range (0.4-0.8% of price typically)

• Breakout rate ~60% of days

• False breakout rate ~40-45%

• Good balance of opportunity and reliability

Psychology: Includes opening panic AND the first retest/consolidation. Sophisticated traders (institutions, algos) start expressing directional bias. This is the "Goldilocks" timeframe—not too reactive, not too slow.

3. 30-Minute ORB (0930-1000 ET):

Classic ORB timeframe. Default for most professional implementations.

Use Case:

• Standard intraday trading

• Position sizing for full-day trades

• All liquid instruments (equities, indices, futures)

Characteristics:

• Substantial range (0.6-1.2% of price)

• Breakout rate ~55% of days

• False breakout rate ~35-40%

• Statistical sweet spot for extensions

Psychology: Full opening auction + first institutional repositioning complete. By 10:00 AM ET, headlines are digested, early stops are hit, and "real" directional players reveal themselves. This is when institutional programs typically finish their opening positioning.

Statistical Advantage: 30-minute ORB shows highest correlation with daily range. When price breaks and holds outside 30m ORB, probability of reaching 1.0x extension (doubling the opening range) exceeds 60% historically.

4. 60-Minute ORB (0930-1030 ET) - Initial Balance:

Steidlmayer's "Initial Balance"—the foundation of Market Profile theory.

Use Case:

• Swing trading entries

• Day type classification

• Low-frequency institutional setups

Characteristics:

• Wide range (0.8-1.5% of price)

• Breakout rate ~45% of days

• False breakout rate ~25-30% (lowest)

• Best for trend day identification

Psychology: Full first hour captures A-period (0930-1000) and B-period (1000-1030). By 10:30 AM ET, all early positioning is complete. Market has "voted" on value. Subsequent price action confirms (trend day) or rejects (rotation day) this value assessment.

Initial Balance Theory:

IB represents the market's accepted value area . When price extends significantly beyond IB (>1.5x IB range), it signals a Trend Day —strong directional conviction. When price remains within 1.0x IB, it signals a Rotation Day —mean reversion environment. This classification completely changes trading strategy.

🔬 LTF PRECISION TECHNOLOGY

The Chart Timeframe Problem:

Traditional ORB indicators calculate range using the chart's current timeframe. This creates critical inaccuracies:

Example:

• You're on a 5-minute chart

• ORB period is 30 minutes (0930-1000 ET)

• Indicator sees only 6 bars (30min ÷ 5min/bar = 6 bars)

• If any 5-minute bar has extreme wick, entire ORB is distorted

The Problem Amplifies:

• On 15-minute chart with 30-minute ORB: Only 2 bars sampled

• On 30-minute chart with 30-minute ORB: Only 1 bar sampled

• Opening spike or single large wick defines entire range (invalid)

Solution: Lower Timeframe (LTF) Precision:

ORB Fusion uses `request.security_lower_tf()` to sample 1-minute bars regardless of chart timeframe:

```

For 30-minute ORB on 15-minute chart:

- Traditional method: Uses 2 bars (15min × 2 = 30min)

- LTF Precision: Requests thirty 1-minute bars, calculates true high/low

```

Why This Matters:

Scenario: ES futures, 15-minute chart, 30-minute ORB

• Traditional ORB: High = 5850.00, Low = 5842.00 (range = 8 points)

• LTF Precision ORB: High = 5848.50, Low = 5843.25 (range = 5.25 points)

Difference: 2.75 points distortion from single 15-minute wick hitting 5850.00 at 9:31 AM then immediately reversing. LTF precision filters this out by seeing it was a fleeting wick, not a sustained high.

Impact on Extensions:

With inflated range (8 points vs 5.25 points):

• 1.5x extension projects +12 points instead of +7.875 points

• Difference: 4.125 points (nearly $200 per ES contract)

• Breakout signals trigger late; extension targets unreachable

Implementation:

```pinescript

getLtfHighLow() =>

float ha = request.security_lower_tf(syminfo.tickerid, "1", high)

float la = request.security_lower_tf(syminfo.tickerid, "1", low)

```

Function returns arrays of 1-minute high/low values, then finds true maximum and minimum across all samples.

When LTF Precision Activates:

Only when chart timeframe exceeds ORB session window:

• 5-minute chart + 30-minute ORB: LTF used (chart TF > session bars needed)

• 1-minute chart + 30-minute ORB: LTF not needed (direct sampling sufficient)

Recommendation: Always enable LTF Precision unless you're on 1-minute charts. The computational overhead is negligible, and accuracy improvement is substantial.

⚖️ INITIAL BALANCE (IB) FRAMEWORK

Steidlmayer's Market Profile Innovation:

J. Peter Steidlmayer developed Market Profile in the 1980s for the Chicago Board of Trade. His key insight: market structure is best understood through time-at-price (value area) rather than just price-over-time (traditional charts).

Initial Balance Definition:

IB is the price range established during the first hour of trading, subdivided into:

• A-Period : First 30 minutes (0930-1000 ET for US equities)

• B-Period : Second 30 minutes (1000-1030 ET)

A-Period vs B-Period Comparison:

The relationship between A and B periods forecasts the day:

B-Period Expansion (Bullish):

• B-period high > A-period high

• B-period low ≥ A-period low

• Interpretation: Buyers stepping in after opening assessed

• Implication: Bullish continuation likely

• Strategy: Buy pullbacks to A-period high (now support)

B-Period Expansion (Bearish):

• B-period low < A-period low

• B-period high ≤ A-period high

• Interpretation: Sellers stepping in after opening assessed

• Implication: Bearish continuation likely

• Strategy: Sell rallies to A-period low (now resistance)

B-Period Contraction:

• B-period stays within A-period range

• Interpretation: Market indecisive, digesting A-period information

• Implication: Rotation day likely, stay range-bound

• Strategy: Fade extremes, sell high/buy low within IB

IB Extensions:

Professional traders use IB as a ruler to project price targets:

Extension Levels:

• 0.5x IB : Initial probe outside value (minor target)

• 1.0x IB : Full extension (major target for normal days)

• 1.5x IB : Trend day threshold (classifies as trending)

• 2.0x IB : Strong trend day (rare, ~10-15% of days)

Calculation:

```

IB Range = IB High - IB Low

Bull Extension 1.0x = IB High + (IB Range × 1.0)

Bear Extension 1.0x = IB Low - (IB Range × 1.0)

```

Example:

ES futures:

• IB High: 5850.00

• IB Low: 5842.00

• IB Range: 8.00 points

Extensions:

• 1.0x Bull Target: 5850 + 8 = 5858.00

• 1.5x Bull Target: 5850 + 12 = 5862.00

• 2.0x Bull Target: 5850 + 16 = 5866.00

If price reaches 5862.00 (1.5x), day is classified as Trend Day —strategy shifts from mean reversion to trend following.

📈 DAY TYPE CLASSIFICATION SYSTEM

Four Day Types (Market Profile Framework):

1. TREND DAY:

Definition: Price extends ≥1.5x IB range in one direction and stays there.

Characteristics:

• Opens and never returns to IB

• Persistent directional movement

• Volume increases as day progresses (conviction building)

• News-driven or strong institutional flow

Frequency: ~20-25% of trading days

Trading Strategy:

• DO: Follow the trend, trail stops, let winners run

• DON'T: Fade extremes, take early profits

• Key: Add to position on pullbacks to previous extension level

• Risk: Getting chopped in false trend (see Failed Breakout section)

Example: FOMC decision, payroll report, earnings surprise—anything creating one-sided conviction.

2. NORMAL DAY:

Definition: Price extends 0.5-1.5x IB, tests both sides, returns to IB.

Characteristics:

• Two-sided trading

• Extensions occur but don't persist

• Volume balanced throughout day

• Most common day type

Frequency: ~45-50% of trading days

Trading Strategy:

• DO: Take profits at extension levels, expect reversals

• DON'T: Hold for massive moves

• Key: Treat each extension as a profit-taking opportunity

• Risk: Holding too long when momentum shifts

Example: Typical day with no major catalysts—market balancing supply and demand.

3. ROTATION DAY:

Definition: Price stays within IB all day, rotating between high and low.

Characteristics:

• Never accepts outside IB

• Multiple tests of IB high/low

• Decreasing volume (no conviction)

• Classic range-bound action

Frequency: ~25-30% of trading days

Trading Strategy:

• DO: Fade extremes (sell IB high, buy IB low)

• DON'T: Chase breakouts

• Key: Enter at extremes with tight stops just outside IB

• Risk: Breakout finally occurs after multiple failures

Example: [/b> Pre-holiday trading, summer doldrums, consolidation after big move.

4. DEVELOPING:

Definition: Day type not yet determined (early in session).

Usage: Classification before 12:00 PM ET when IB extension pattern unclear.

ORB Fusion's Classification Algorithm:

```pinescript

if close > ibHigh:

ibExtension = (close - ibHigh) / ibRange

direction = "BULLISH"

else if close < ibLow:

ibExtension = (ibLow - close) / ibRange

direction = "BEARISH"

if ibExtension >= 1.5:

dayType = "TREND DAY"

else if ibExtension >= 0.5:

dayType = "NORMAL DAY"

else if close within IB:

dayType = "ROTATION DAY"

```

Why Classification Matters:

Same setup (bullish ORB breakout) has opposite implications:

• Trend Day : Hold for 2.0x extension, trail stops aggressively

• Normal Day : Take profits at 1.0x extension, watch for reversal

• Rotation Day : Fade the breakout immediately (likely false)

Knowing day type prevents catastrophic errors like fading a trend day or holding through rotation.

🚀 BREAKOUT DETECTION & CONFIRMATION

Three Confirmation Methods:

1. Close Beyond Level (Recommended):

Logic: Candle must close above ORB high (bull) or below ORB low (bear).

Why:

• Filters out wicks (temporary liquidity grabs)

• Ensures sustained acceptance above/below range

• Reduces false breakout rate by ~20-30%

Example:

• ORB High: 5850.00

• Bar high touches 5850.50 (wick above)

• Bar closes at 5848.00 (inside range)

• Result: NO breakout signal

vs.

• Bar high touches 5850.50

• Bar closes at 5851.00 (outside range)

• Result: BREAKOUT signal confirmed

Trade-off: Slightly delayed entry (wait for close) but much higher reliability.

2. Wick Beyond Level:

Logic: [/b> Any touch of ORB high/low triggers breakout.

Why:

• Earliest possible entry

• Captures aggressive momentum moves

Risk:

• High false breakout rate (60-70%)

• Stop runs trigger signals

• Requires very tight stops (difficult to manage)

Use Case: Scalping with 1-2 point profit targets where any penetration = trade.

3. Body Beyond Level:

Logic: [/b> Candle body (close vs open) must be entirely outside range.

Why:

• Strictest confirmation

• Ensures directional conviction (not just momentum)

• Lowest false breakout rate

Example: Trade-off: [/b> Very conservative—misses some valid breakouts but rarely triggers on false ones.

Volume Confirmation Layer:

All confirmation methods can require volume validation:

Volume Multiplier Logic: Rationale: [/b> True breakouts are driven by institutional activity (large size). Volume spike confirms real conviction vs. stop-run manipulation.

Statistical Impact: [/b>

• Breakouts with volume confirmation: ~65% success rate

• Breakouts without volume: ~45% success rate

• Difference: 20 percentage points edge

Implementation Note: [/b>

Volume confirmation adds complexity—you'll miss breakouts that work but lack volume. However, when targeting 1.5x+ extensions (ambitious goals), volume confirmation becomes critical because those moves require sustained institutional participation.

Recommended Settings by Strategy: [/b>

Scalping (1-2 point targets): [/b>

• Method: Close

• Volume: OFF

• Rationale: Quick in/out doesn't need perfection

Intraday Swing (5-10 point targets): [/b>

• Method: Close

• Volume: ON (1.5x multiplier)

• Rationale: Balance reliability and opportunity

Position Trading (full-day holds): [/b>

• Method: Body

• Volume: ON (2.0x multiplier)

• Rationale: Must be certain—large stops require high win rate

🔥 FAILED BREAKOUT SYSTEM

The Core Insight: [/b>

Failed breakouts are often more profitable [/b> than successful breakouts because they create trapped traders with predictable behavior.

Failed Breakout Definition: [/b>

A breakout that:

1. Initially penetrates ORB level with confirmation

2. Attracts participants (volume spike, momentum)

3. Fails to extend (stalls or immediately reverses)

4. Returns inside ORB range within N bars

Psychology of Failure: [/b>

When breakout fails:

• Breakout buyers are trapped [/b>: Bought at ORB high, now underwater

• Early longs reduce: Take profit, fearful of reversal

• Shorts smell blood: See failed breakout as reversal signal

• Result: Cascade of selling as trapped bulls exit + new shorts enter

Mirror image for failed bearish breakouts (trapped shorts cover + new longs enter).

Failure Detection Parameters: [/b>

1. Failure Confirmation Bars (default: 3): [/b>

How many bars after breakout to confirm failure?

Logic: Settings: [/b>

• 2 bars: Aggressive failure detection (more signals, more false failures)

• 3 bars Balanced (default)

• 5-10 bars: Conservative (wait for clear reversal)

Why This Matters:

Too few bars: You call "failed breakout" when price is just consolidating before next leg.

Too many bars: You miss the reversal entry (price already back in range).

2. Failure Buffer (default: 0.1 ATR): [/b>

How far inside ORB must price return to confirm failure?

Formula: Why Buffer Matters: clear rejection [/b> (not just hovering at level).

Settings: [/b>

• 0.0 ATR: No buffer, immediate failure signal

• 0.1 ATR: Small buffer (default) - filters noise

• [b>0.2-0.3 ATR: Large buffer - only dramatic failures count

Example: Reversal Entry System: [/b>

When failure confirmed, system generates complete reversal trade:

For Failed Bull Breakout (Short Reversal): [/b>

Entry: [/b> Current close when failure confirmed

Stop Loss: [/b> Extreme high since breakout + 0.10 ATR padding

Target 1: [/b> ORB High - (ORB Range × 0.5)

Target 2: Target 3: [/b> ORB High - (ORB Range × 1.5)

Example:

• ORB High: 5850, ORB Low: 5842, Range: 8 points

• Breakout to 5853, fails, reverses to 5848 (entry)

• Stop: 5853 + 1 = 5854 (6 point risk)

• T1: 5850 - 4 = 5846 (-2 points, 1:3 R:R)

• T2: 5850 - 8 = 5842 (-6 points, 1:1 R:R)

• T3: 5850 - 12 = 5838 (-10 points, 1.67:1 R:R)

[b>Why These Targets? [/b>

• T1 (0.5x ORB below high): Trapped bulls start panic

• T2 (1.0x ORB = ORB Mid): Major retracement, momentum fully reversed

• T3 (1.5x ORB): Reversal extended, now targeting opposite side

Historical Performance: [/b>

Failed breakout reversals in ORB Fusion's tracking system show:

• Win Rate: 65-75% (significantly higher than initial breakouts)

• Average Winner: 1.2x ORB range

• Average Loser: 0.5x ORB range (protected by stop at extreme)

• Expectancy: Strongly positive even with <70% win rate

Why Failed Breakouts Outperform: [/b>

1. Information Advantage: You now know what price did (failed to extend). Initial breakout trades are speculative; reversal trades are reactive to confirmed failure.

2. Trapped Participant Pressure: Every trapped bull becomes a seller. This creates sustained pressure.

3. Stop Loss Clarity: Extreme high is obvious stop (just beyond recent high). Breakout trades have ambiguous stops (ORB mid? Recent low? Too wide or too tight).

4. Mean Reversion Edge: Failed breakouts return to value (ORB mid). Initial breakouts try to escape value (harder to sustain).

Critical Insight: [/b>

"The best trade is often the one that trapped everyone else."

Failed breakouts create asymmetric opportunity because you're trading against [/b> trapped participants rather than with [/b> them. When you see a failed breakout signal, you're seeing real-time evidence that the market rejected directional conviction—that's exploitable.

📐 FIBONACCI EXTENSION SYSTEM

Six Extension Levels: [/b>

Extensions project how far price will travel after ORB breakout. Based on Fibonacci ratios + empirical market behavior.

1. 1.272x (27.2% Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.272)

Psychology: [/b> Initial probe beyond ORB. Early momentum + trapped shorts (on bull side) covering.

Probability of Reach: [/b> ~75-80% after confirmed breakout

Trading: [/b>

• First resistance/support after breakout

• Partial profit target (take 30-50% off)

• Watch for rejection here (could signal failure in progress)

Why 1.272? [/b> Related to harmonic patterns (1.272 is √1.618). Empirically, markets often stall at 25-30% extension before deciding whether to continue or fail.

2. 1.5x (50% Extension):

Formula: [/b> ORB High/Low + (ORB Range × 0.5)

Psychology: [/b> Breakout gaining conviction. Requires sustained buying/selling (not just momentum spike).

Probability of Reach: [/b> ~60-65% after confirmed breakout

Trading: [/b>

• Major partial profit (take 50-70% off)

• Move stops to breakeven

• Trail remaining position

Why 1.5x? [/b> Classic halfway point to 2.0x. Markets often consolidate here before final push. If day type is "Normal," this is likely the high/low for the day.

3. 1.618x (Golden Ratio Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.618)

Psychology: [/b> Strong directional day. Institutional conviction + retail FOMO.

Probability of Reach: [/b> ~45-50% after confirmed breakout

Trading: [/b>

• Final partial profit (close 80-90%)

• Trail remainder with wide stop (allow breathing room)

Why 1.618? [/b> Fibonacci golden ratio. Appears consistently in market geometry. When price reaches 1.618x extension, move is "mature" and reversal risk increases.

4. 2.0x (100% Extension): [/b>

Formula: ORB High/Low + (ORB Range × 1.0)

Psychology: [/b> Trend day confirmed. Opening range completely duplicated.

Probability of Reach: [/b> ~30-35% after confirmed breakout

Trading: Why 2.0x? [/b> Psychological level—range doubled. Also corresponds to typical daily ATR in many instruments (opening range ~ 0.5 ATR, daily range ~ 1.0 ATR).

5. 2.618x (Super Extension):

Formula: [/b> ORB High/Low + (ORB Range × 1.618)

Psychology: [/b> Parabolic move. News-driven or squeeze.

Probability of Reach: [/b> ~10-15% after confirmed breakout

[b>Trading: Why 2.618? [/b> Fibonacci ratio (1.618²). Rare to reach—when it does, move is extreme. Often precedes multi-day consolidation or reversal.

6. 3.0x (Extreme Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 2.0)

Psychology: [/b> Market melt-up/crash. Only in extreme events.

[b>Probability of Reach: [/b> <5% after confirmed breakout

Trading: [/b>

• Close immediately if reached

• These are outlier events (black swans, flash crashes, squeeze-outs)

• Holding for more is greed—take windfall profit

Why 3.0x? [/b> Triple opening range. So rare it's statistical noise. When it happens, it's headline news.

Visual Example:

ES futures, ORB 5842-5850 (8 point range), Bullish breakout:

• ORB High : 5850.00 (entry zone)

• 1.272x : 5850 + 2.18 = 5852.18 (first resistance)

• 1.5x : 5850 + 4.00 = 5854.00 (major target)

• 1.618x : 5850 + 4.94 = 5854.94 (strong target)

• 2.0x : 5850 + 8.00 = 5858.00 (trend day)

• 2.618x : 5850 + 12.94 = 5862.94 (extreme)

• 3.0x : 5850 + 16.00 = 5866.00 (parabolic)

Profit-Taking Strategy:

Optimal scaling out at extensions:

• Breakout entry at 5850.50

• 30% off at 1.272x (5852.18) → +1.68 points

• 40% off at 1.5x (5854.00) → +3.50 points

• 20% off at 1.618x (5854.94) → +4.44 points

• 10% off at 2.0x (5858.00) → +7.50 points

[b>Average Exit: Conclusion: [/b> Scaling out at extensions produces 40% higher expectancy than holding for home runs.

📊 GAP ANALYSIS & FILL PSYCHOLOGY

[b>Gap Definition: [/b>

Price discontinuity between previous close and current open:

• Gap Up : Open > Previous Close + noise threshold (0.1 ATR)

• Gap Down : Open < Previous Close - noise threshold

Why Gaps Matter: [/b>

Gaps represent unfilled orders [/b>. When market gaps up, all limit buy orders between yesterday's close and today's open are never filled. Those buyers are "left behind." Psychology: they wait for price to return ("fill the gap") so they can enter. This creates magnetic pull [/b> toward gap level.

Gap Fill Statistics (Empirical): [/b>

• Gaps <0.5% [/b>: 85-90% fill within same day

• Gaps 0.5-1.0% [/b>: 70-75% fill within same day, 90%+ within week

• Gaps >1.0% [/b>: 50-60% fill within same day (major news often prevents fill)

Gap Fill Strategy: [/b>

Setup 1: Gap-and-Go

Gap opens, extends away from gap (doesn't fill).

• ORB confirms direction away from gap

• Trade WITH ORB breakout direction

• Expectation: Gap won't fill today (momentum too strong)

Setup 2: Gap-Fill Fade

Gap opens, but fails to extend. Price drifts back toward gap.

• ORB breakout TOWARD gap (not away)

• Trade toward gap fill level

• Target: Previous close (gap fill complete)

Setup 3: Gap-Fill Rejection

Gap fills (touches previous close) then rejects.

• ORB breakout AWAY from gap after fill

• Trade away from gap direction

• Thesis: Gap filled (orders executed), now resume original direction

[b>Example: Scenario A (Gap-and-Go):

• ORB breaks upward to $454 (away from gap)

• Trade: LONG breakout, expect continued rally

• Gap becomes support ($452)

Scenario B (Gap-Fill):

• ORB breaks downward through $452.50 (toward gap)

• Trade: SHORT toward gap fill at $450.00

• Target: $450.00 (gap filled), close position

Scenario C (Gap-Fill Rejection):

• Price drifts to $450.00 (gap filled) early in session

• ORB establishes $450-$451 after gap fill

• ORB breaks upward to $451.50

• Trade: LONG breakout (gap is filled, now resume rally)

ORB Fusion Integration: [/b>

Dashboard shows:

• Gap type (Up/Down/None)

• Gap size (percentage)

• Gap fill status (Filled ✓ / Open)

This informs setup confidence:

• ORB breakout AWAY from unfilled gap: +10% confidence (gap becomes support/resistance)

• ORB breakout TOWARD unfilled gap: -10% confidence (gap fill may override ORB)

[b>📈 VWAP & INSTITUTIONAL BIAS [/b>

[b>Volume-Weighted Average Price (VWAP): [/b>

Average price weighted by volume at each price level. Represents true "average" cost for the day.

[b>Calculation: Institutional Benchmark [/b>: Institutions (mutual funds, pension funds) use VWAP as performance benchmark. If they buy above VWAP, they underperformed; below VWAP, they outperformed.

2. [b>Algorithmic Target [/b>: Many algos are programmed to buy below VWAP and sell above VWAP to achieve "fair" execution.

3. [b>Support/Resistance [/b>: VWAP acts as dynamic support (price above) or resistance (price below).

[b>VWAP Bands (Standard Deviations): [/b>

• [b>1σ Band [/b>: VWAP ± 1 standard deviation

- Contains ~68% of volume

- Normal trading range

- Bounces common

• [b>2σ Band [/b>: VWAP ± 2 standard deviations

- Contains ~95% of volume

- Extreme extension

- Mean reversion likely

ORB + VWAP Confluence: [/b>

Highest-probability setups occur when ORB and VWAP align:

Bullish Confluence: [/b>

• ORB breakout upward (bullish signal)

• Price above VWAP (institutional buying)

• Confidence boost: +15%

Bearish Confluence: [/b>

• ORB breakout downward (bearish signal)

• Price below VWAP (institutional selling)

• Confidence boost: +15%

[b>Divergence Warning:

• ORB breakout upward BUT price below VWAP

• Conflict: Breakout says "buy," VWAP says "sell"

• Confidence penalty: -10%

• Interpretation: Retail buying but institutions not participating (lower quality breakout)

📊 MOMENTUM CONTEXT SYSTEM

[b>Innovation: Candle Coloring by Position

Rather than fixed support/resistance lines, ORB Fusion colors candles based on their [b>relationship to ORB :

[b>Three Zones: [/b>

1. Inside ORB (Blue Boxes): [/b>

[b>Calculation:

• Darker blue: Near extremes of ORB (potential breakout imminent)

• Lighter blue: Near ORB mid (consolidation)

[b>Trading: [/b> Coiled spring—await breakout.

[b>2. Above ORB (Green Boxes):

[b>Calculation: 3. Below ORB (Red Boxes):

Mirror of above ORB logic.

[b>Special Contexts: [/b>

[b>Breakout Bar (Darkest Green/Red): [/b>

The specific bar where breakout occurs gets maximum color intensity regardless of distance. This highlights the pivotal moment.

[b>Failed Breakout Bar (Orange/Warning): [/b>

When failed breakout is confirmed, that bar gets orange/warning color. Visual alert: "reversal opportunity here."

[b>Near Extension (Cyan/Magenta Tint): [/b>

When price is within 0.5 ATR of an extension level, candle gets tinted cyan (bull) or magenta (bear). Indicates "target approaching—prepare to take profit."