FlexiMA x FlexiST - Strategy [presentTrading]█ Introduction and How it is Different

The FlexiMA x FlexiST Strategy blends two analytical methods - FlexiMA and FlexiST, which are opened in my early post.

- FlexiMA calculates deviations between an indicator source and a dynamic moving average, controlled by a starting factor and increment factor.

- FlexiST, on the other hand, leverages the SuperTrend model, adjusting the Average True Range (ATR) length for a comprehensive trend-following oscillator.

This synergy offers traders a more nuanced and multifaceted tool for market analysis.

BTC 6H L/S Performance

Local

█ Strategy, How It Works: Detailed Explanation

The strategy combines two components: FlexiMA and FlexiST, each utilizing unique methodologies to analyze market trends.

🔶FlexiMA Component:

- Calculates deviations between an indicator source and moving averages of variable lengths.

- Moving average lengths are dynamically adjusted using a starting factor and increment factor.

- Deviations are normalized and analyzed to produce median and standard deviation values, forming the FlexiMA oscillator.

Length indicator (50)

🔶FlexiST Component:

- Uses SuperTrend indicators with varying ATR (Average True Range) lengths.

- Trends are identified based on the position of the indicator source relative to the SuperTrend bands.

- Deviations between the indicator source and SuperTrend values are calculated and normalized.

Starting Factor (5)

🔶Combined Strategy Logic:

- Entry Signals:

- Long Entry: Triggered when median values of both FlexiMA and FlexiST are positive.

- Short Entry: Triggered when median values of both FlexiMA and FlexiST are negative.

- Exit Signals:

- Long Exit: Triggered when median values of FlexiMA or FlexiST turn negative.

- Short Exit: Triggered when median values of FlexiMA or FlexiST turn positive.

This strategic blend of FlexiMA and FlexiST allows for a nuanced analysis of market trends, providing traders with signals based on a comprehensive view of market momentum and trend strength.

█ Trade Direction

The strategy is designed to cater to various trading preferences, offering "Long", "Short", and "Both" options. This flexibility allows traders to align the strategy with their specific market outlook, be it bullish, bearish, or a combination of both.

█ Usage

Traders can effectively utilize the FlexiMA x FlexiST Strategy by first selecting their desired trade direction. The strategy then generates entry signals when the conditions for either the FlexiMA or FlexiST are met, indicating potential entry points in the market. Conversely, exit signals are generated when the conditions for these indicators diverge, thus signaling a potential shift in market trends and suggesting a strategic exit point.

█ Default Settings

1. Indicator Source (HLC3): Provides a balanced and stable price source, reducing the impact of extreme market fluctuations.

2. Indicator Lengths (20 for FlexiMA, 10 for FlexiST): Longer FlexiMA length smooths out short-term fluctuations, while shorter FlexiST length allows for quicker response to market changes.

3. Starting Factors (1.0 for FlexiMA, 0.618 for FlexiST): Balanced start for FlexiMA and a harmonized approach for FlexiST, resonating with natural market cycles.

4. Increment Factors (1.0 for FlexiMA, 0.382 for FlexiST): FlexiMA captures a wide range of market behaviors, while FlexiST provides a gradual transition to capture finer trend shifts.

5. Normalization Methods ('None'): Uses raw deviations, suitable for markets where absolute price movements are more significant.

6. Trade Direction ('Both'): Allows strategy to consider both long and short opportunities, ideal for versatile market engagement.

*More details:

1. FlexiMA

2. FlexiST

Поиск скриптов по запросу "track"

[astropark] Trend Skywalker V1 [strategy]Dear Followers,

today another awesome Swing and Scalping Trading Strategy indicator: Trend Skywalker !

It shows a trend cloud that reacts very fast to price action, so it's perfect for trending markets: it helps a lot to find out

when a trend is going to end and a new is going to start

when to enter again within a trending market

where to put your stoploss

In this example below you can see the three points above:

In fact in a trending market it will highlight that:

price consolidation within the could is a trend weakening signal , so you can easily spot when a trend is going to end and a new is going to start

bullish/bearish trend cloud retests are nice opportunity to re-enter within a trending market, especially if cloud is thick

where to put your stoploss ( below the cloud and/or recent low in a buy scenario , above the cloud and/or recent high in a sell scenario )

This strategy/indicator has the following options:

change analysis window (the lower, the more reactive; the higher, the less reactive)

enable/disable signals on chart

enable/disable "more confirmations" signals filter

enable/disable bars and background coloring based on trend

enable/disable an automatic Trailing Stop strategy option (Automatic Stops)

enable/disable a peak profit tracker (the max percentage profit labels)

enable/disable highlights of trend cloud retests

enable/disable highlights of trend cloud price breakouts

Here below some examples how the indicator works on many markets and timeframe.

ETH/USD 4h

EUR/USD 15m

LTC/BTC 1h

This strategy only trigger 1 buy (where to start a long trade) or 1 sell (for short trade).

Keep in mind that proper risk management and money management strategies are very important to manage your trades (DM me if you need any clarification on these points).

This script will let you backtest the strategy performance over the backtesting period you set in input (it may be a lower period, depending on tradingview candles limitation related to your account).

The one for setting alarms can be found by searching for the astropark's "Trend Skywalker" and then choosing the indicator with "alarms" suffix in the name.

Strategy results are calculated on the time window from February 2018 to now, so about 3 years, using 10000$ as initial capital and working at 1x leverage (so no leverage at all! If you like to use leverage, be sure to use a safe option, like 2x or 3x at most in order to have liquidation price very far).

This is not the "Holy Grail", so use proper money and risk management strategies.

This is a premium indicator , so send me a private message in order to get access to this script.

BB+K strategyApplying Bollinger Bands and K-bar strategies

Suitable for long time periods

Suitable for forex trading, when the forex deviation is too large, the Fed will intervene and thus correct

Strategy: Enter when the price hits the upper or lower BB track and there is a reversal of the strong signal, and exit when it hits the other track and there is a reversal signal.

Systematic Momentum strategy v 1.0Systematic Momentum strategy v 1.0

This is a long-only strategy optimized taking into consideration the underlying's momentum and volatily.

Long story short it opens positions when the momentum is highest and the risk is lowest and closes the same position when the risk-to-reward is no longer optimal.

How to use:

-> To be used on an Index or a tracker ETF

-> Position sizing should be set up to 100% of the portfolio

XPloRR S&P500 Stock Market Crash Detection Strategy v2XPloRR S&P500 Stock Market Crash Detection Strategy v2

Long-Term Trailing-Stop strategy detecting S&P500 Stock Market Crashes/Corrections and showing Volatility as warning signal for upcoming crashes

Detecting or avoiding stock market crashes seems to be the 'Holy Grail' of strategies.

Since none of the strategies that I tested can beat the long term Buy&Hold strategy, the purpose was to detect a stock market crash on the S&P500 and step out in time to minimize losses and beat the Buy&Hold strategy. So beat the Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

With the default parameters the strategy generates 10262% profit (starting at 01/01/1962 until release date), with 10 closed trades, 100% profitable, while the Buy&Hold strategy only generates 3633% profit, so this strategy beats the Buy&Hold strategy by 2.82 times !

Also the strategy detects all major S&P500 stock market crashes and corrections since 1962 depending on the Trailing Stop Smoothness parameter, and steps out in time to cut losses and steps in again after the bottom has been reached. The 5 major crashes/corrections of 1987, 1990, 2001, 2008 and 2010 were successfully detected with the default parameters.

The script was first released on November 03 2019 and detected the Corona Crash on March 04 2020 with a Volatility crash-alert and a Sell crash-alert.

I have also created an Alerter Study Script based on the engine of this script, which generates Buy, Sell and Volatility signals.

If you are interested in this Alerter version script, please drop me a mail.

The script shows a lot of graphical information:

the Close value is shown in light-green. When the Close value is temporarily lower than the Buy value, the Close value is shown in light-red. This way it is possible to evaluate the virtual losses during the current trade.

the Trailing Stop value is shown in dark-green. When the Sell value is lower than the Buy value, the last color of the trade will be red (best viewed when zoomed)

the EMA and SMA values for both Buy and Sell signals are shown as colored graphs

the Buy signals are labeled in blue and the Sell signals are labeled in purple

the Volatility is shown below in green and red. The Alert Threshold (red) is default set to 2 (see Volatility Threshold parameter below)

How to use this Strategy?

Select the SPX (S&P500) graph and add this script to the graph.

Look in the strategy tester overview to optimize the values Percent Profitable and Net Profit (using the strategy settings icon, you can increase/decrease the parameters), then keep using these parameters for future Buy/Sell signals on the S&P500.

More trades don't necessarily generate more overall profit. It is important to detect only the major crashes and avoid closing trades on the smaller corrections. Bearing the smaller corrections generates a higher profit.

Watch out for the Volatility Alerts generated at the bottom (red). The Threshold can by changed by the Volatility Threshold parameter (default=2% ATR). In almost all crashes/corrections there is an alert ahead of the crash.

Although the signal doesn't predict the exact timing of the crash/correction, it is a clear warning signal that bearish times are ahead!

The correction in December 2018 was not a major crash but there was already a red Volatility warning alert. If the Volatility Alert repeats the next weeks/months, chances are higher that a bigger crash or correction is near. As can be seen in the graphic, the deeper the crash is, the higher and wider the red Volatility signal goes. So keep an eye on the red flag!

Here are the parameters:

Fast MA Buy: buy trigger when Fast MA Buy crosses over the Slow MA Buy value (use values between 10-20)

Slow MA Buy: buy trigger when Fast MA Buy crosses over the Slow MA Buy value (use values between 21-50)

Minimum Buy Strength: minimum upward trend value of the Fast MA Buy value (directional coefficient)(use values between 10-100)

Fast MA Sell: sell trigger when Fast MA Sell crosses under the Slow MA Sell value (use values between 10-20)

Slow MA Sell: sell trigger when Fast MA Sell crosses under the Slow MA Sell value (use values between 21-50)

Minimum Sell Strength: minimum downward trend value of the Fast MA Sell value (directional coefficient)(use values between 10-100)

Trailing Stop ATR: trailing stop % distance from the smoothed Close value (use values between 2-20)

Trailing Stop Smoothness: MA value for smoothing out the Trailing Stop close value

Buy On Start Date: force Buy on start date even without Buy signal (default: true)

Sell On End Date: force Sell on end date even without Sell signal (default: true)

Volatility EMA Period: MA value of the Volatility value (default 15)

Volatility Threshold: Threshold value to change volatility graph to red (default 2)

Volatility Graph Scaler: Scaling of the volatility graph (default 5)

Important : optimizing and using these parameters is no guarantee for future winning trades!

OBV Divergence Tracker StrategyThis strategy combines OBV Z Scores and price Z Scores to identify divergences and generate entry and exit signals.

Trend TrackerWorks best on the Daily Something Iv'e been playing around with for a while seems to work real well on High Beta Names

Dual Thrust StrategyThe Dual Thrust trading algorithm is a famous strategy developed by Michael Chalek. Its logical prototype is one of the most common Day trading strategies. The opening range breakout strategy is based on today’s opening price plus or minus a certain percentage of yesterday’s amplitude to determine the upper and lower rails. When the price breaks through the upper track, it will buy long, and when it breaks the lower track, it will sell short.

When using this strategy, on the one hand, you can refer to the optimal parameters of historical data testing. On the other hand, you can start to adjust K1 and K2 in stages according to your own judgment of the post-trend or from other major cycle technical indicators.

Trend tracker by ClefsphereThis script attempts to identify the trend and go with it. Green colored squares are bullish, Black squares are bearish. Script is written to show back-test results. Dates of back-test period can be adjusted. Strategy is for Long trades only, but closed trades could possibly be considered for Short trades. Coded with latest PineScript version 3.

For more information and to request for use, go to: marketcast.wordpress.com

Thanks for your interest and support!

Disclaimer: This information is not trading advice and is for educational purposes only. Past performance is not a guarantee of future results.

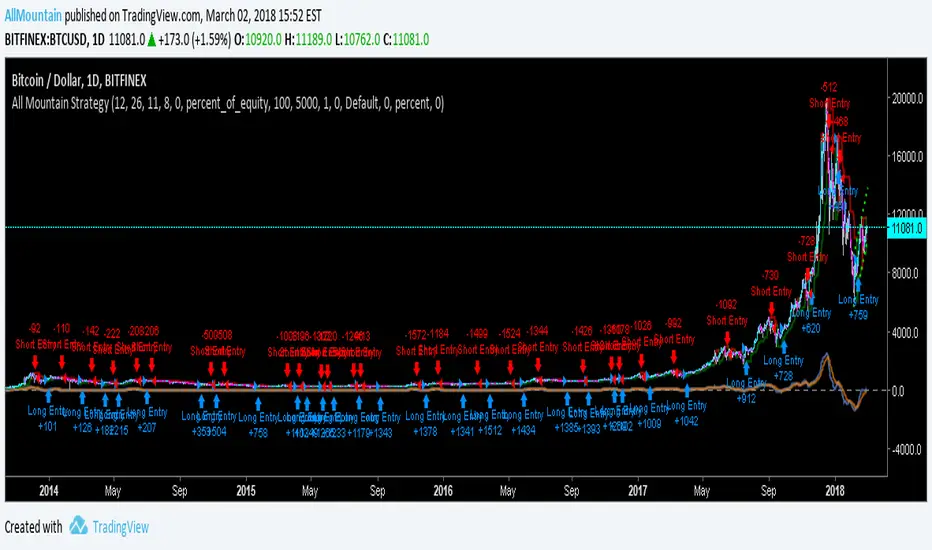

All Mountain StrategyBest use in cryptocurrency.

Use on daily chart for best results.

This strategy does not repaint. It works with trend trackers.

The strategy closes one operation on the inverse signal and initiates another trade.

Good Luck!

Bitcoin donations:: 19fGUD9WXNHxtPE4v2ugbNjqp5dT9VVE3N

TigerBot Percentage Tracker Skeleton (Faster Backtesting)The logic for this strategy is based on percentage of price movement within a given time frame. It works both as a momentum catcher and a reversal catcher. Customize the input parameters and test on various charts and timeframes for maximum profit potential.

Note: This is a TigerBot Strategy, which means that it is set up and ready for you to use it with our full set of automation and risk management features such as:

Thorough event triggers for automated order execution

Profit/Loss Zones

Profit/Loss Indicators

Take Profit

Normal Stop Loss

Trailing Stop Loss

Advanced Trailing Stop

Profit Locker Stop Loss

Advanced Pyramiding Support

Leverage Support

Much more

Each TigerBot Strategy includes a set of 3 scripts that belong together:

STRATEGY - used for full-featured customization with all our visuals

STUDY - with alert triggers for automation

SKELETON - for faster backtesting without the visuals enabled

This is the SKELETON version of this script. Please also see the other 2 related scripts.

Visit TheTigerBot.com to gain access and take advantage of the full TigerBot features on this strategy, or submit your own script for TigerBot automation!

TigerBot Percentage Tracker Strategy (Backtesting)The logic for this strategy is based on percentage of price movement within a given time frame. It works both as a momentum catcher and a reversal catcher. Customize the input parameters and test on various charts and timeframes for maximum profit potential.

Note: This is a TigerBot Strategy, which means that it is set up and ready for you to use it with our full set of automation and risk management features such as:

Thorough event triggers for automated order execution

Profit/Loss Zones

Profit/Loss Indicators

Take Profit

Normal Stop Loss

Trailing Stop Loss

Advanced Trailing Stop

Profit Locker Stop Loss

Advanced Pyramiding Support

Leverage Support

Much more

Each TigerBot Strategy includes a set of 3 scripts that belong together:

STRATEGY - used for full-featured customization with all our visuals

STUDY - with alert triggers for automation

SKELETON - for faster backtesting without the visuals enabled

This is the STRATEGY version of this script. Please also see the other 2 related scripts.

Visit TheTigerBot.com to gain access and take advantage of the full TigerBot features on this strategy, or submit your own script for TigerBot automation!

RF SMC Strategy V1.7 PROD.RF SMC PRO V1.7 is a multi-timeframe Smart Money Concepts framework that builds a rule-based view of market structure and then trades directly off that structure. It’s designed for traders who want to systematize SMC logic, keep their charts readable, and automate their trading.

Instead of relying on lagging oscillators, the strategy continuously tracks the active price levels and reacts to structural shifts in real time. It does this on multiple time frames, to find the best entries, and entry models, based on specific criteria.

There are multiple entry models, based on the lower time frame structure, using the higher time frame bias, to find those sniper entries. You can use a combination of different entry models as well to find the highest win rate set-ups.

Risk management is fully structure-based. Stops are always placed beyond the current structure high/low, with a few different take profit models:

Fixed RR – simple R-multiple targeting off the structure-based stop.

HTF Weak High/Low – targets the opposing side of the active HTF leg.

Opposite CHoCH – stays in the trade, until the LTF structure flips against the position. Meaning your winners can run, and losers have the ability to be cut early.

Key Features:

Multi-timeframe functionality

Primary and optional secondary HTF bias filters.

Discount/premium gating

Entry model combinations

TP models

Extra filtering based on days, sessions, and other bias filters.

Get Access on Whop Here: whop.com

ES Multi-Timeframe SMC Entry SystemOverviewThis is a comprehensive Smart Money Concepts (SMC) trading strategy for ES1! (E-mini S&P 500) futures that provides simultaneous buy and sell signals across three timeframes: Daily, Weekly, and Monthly. It incorporates your complete entry checklists, confluence scoring system, and automated risk management.Core Features1. Multi-Timeframe Signal Generation

Daily Signals (D) - For intraday/swing trades (1-3 day holds)

Weekly Signals (W) - For swing trades (3-10 day holds)

Monthly Signals (M) - For position trades (weeks to months)

All three timeframes can trigger simultaneously (pyramiding enabled)

2. Smart Money Concepts ImplementationOrder Blocks (OB)

Automatically detects bullish and bearish order blocks

Bullish OB = Down candle before strong impulse up

Bearish OB = Up candle before strong impulse down

Validates freshness (< 10 bars = higher quality)

Visual boxes displayed on chart

Fair Value Gaps (FVG)

Identifies 3-candle imbalance patterns

Bullish FVG = Gap between high and current low

Bearish FVG = Gap between low and current high

Tracks unfilled gaps as targets/entry zones

Auto-removes when filled

Premium/Discount Zones

Calculates 50-period swing range

Premium = Upper 50% (short from here)

Discount = Lower 50% (long from here)

Deep zones (<30% or >70%) for higher quality setups

Visual shading: Red = Premium, Green = Discount

Liquidity Sweeps

Sell-Side Sweep (SSL) = False break below lows → reversal up

Buy-Side Sweep (BSL) = False break above highs → reversal down

Marked with yellow labels on chart

Valid for 10 bars after occurrence

Break of Structure (BOS)

Identifies when price breaks recent swing high/low

Confirms trend continuation

Marked with small circles on chart

3. Confluence Scoring SystemEach timeframe has a 10-point scoring system based on your checklist requirements:Daily Score (10 points max)

HTF Trend Alignment (2 pts) - 4H and Daily EMAs aligned

SMC Structure (2 pts) - OB in correct zone with HTF bias

Liquidity Sweep (1 pt) - Recent SSL/BSL occurred

Volume Confirmation (1 pt) - Volume > 1.2x 20-period average

Optimal Time (1 pt) - 9:30-12 PM or 2-4 PM ET (avoids lunch)

Risk-Reward >2:1 (1 pt) - Built into exit strategy

Clean Price Action (1 pt) - BOS occurred

FVG Present (1 pt) - Near unfilled fair value gap

Minimum Required: 6/10 (adjustable)Weekly Score (10 points max)

Weekly/Monthly Alignment (2 pts) - W and M EMAs aligned

Daily/Weekly Alignment (2 pts) - D and W trends match

Premium/Discount Correct (2 pts) - Deep zone + trend alignment

Major Liquidity Event (1 pt) - SSL/BSL sweep

Order Block Present (1 pt) - Valid OB detected

Risk-Reward >3:1 (1 pt) - Built into exit

Fresh Order Block (1 pt) - OB < 10 bars old

Minimum Required: 7/10 (adjustable)Monthly Score (10 points max)

Monthly/Weekly Alignment (2 pts) - M and W trends match

Weekly OB in Monthly Zone (2 pts) - OB in deep discount/premium

Major Liquidity Sweep (2 pts) - Significant SSL/BSL

Strong Trend Alignment (2 pts) - D, W, M all aligned

Risk-Reward >4:1 (1 pt) - Built into exit

Extreme Zone (1 pt) - Price <20% or >80% of range

Minimum Required: 8/10 (adjustable)4. Entry ConditionsDaily Long Entry

✅ Daily score ≥ 6/10

✅ 4H trend bullish (price > EMAs)

✅ Price in discount zone

✅ Bullish OB OR SSL sweep OR near bullish FVG

✅ NOT during avoid times (lunch/first 5 min)Daily Short Entry

✅ Daily score ≥ 6/10

✅ 4H trend bearish

✅ Price in premium zone

✅ Bearish OB OR BSL sweep OR near bearish FVG

✅ NOT during avoid timesWeekly Long Entry

✅ Weekly score ≥ 7/10

✅ Weekly trend bullish

✅ Daily trend bullish

✅ Price in discount

✅ Bullish OB OR SSL sweepWeekly Short Entry

✅ Weekly score ≥ 7/10

✅ Weekly trend bearish

✅ Daily trend bearish

✅ Price in premium

✅ Bearish OB OR BSL sweepMonthly Long Entry

✅ Monthly score ≥ 8/10

✅ Monthly trend bullish

✅ Weekly trend bullish

✅ Price in DEEP discount (<30%)

✅ Bullish order block presentMonthly Short Entry

✅ Monthly score ≥ 8/10

✅ Monthly trend bearish

✅ Weekly trend bearish

✅ Price in DEEP premium (>70%)

✅ Bearish order block present5. Automated Risk ManagementPosition Sizing (Per Entry)

Daily: 1.0% account risk per trade

Weekly: 0.75% account risk per trade

Monthly: 0.5% account risk per trade

Formula:

Contracts = (Account Equity × Risk%) ÷ (Stop Points × $50)

Minimum = 1 contractStop Losses

Daily: 12 points ($600 per contract)

Weekly: 40 points ($2,000 per contract)

Monthly: 100 points ($5,000 per contract)

Profit Targets (Risk:Reward)

Daily: 2:1 = 24 points ($1,200 profit)

Weekly: 3:1 = 120 points ($6,000 profit)

Monthly: 4:1 = 400 points ($20,000 profit)

Example with $50,000 AccountDaily Trade:

Risk = $500 (1% of $50k)

Stop = 12 points × $50 = $600

Contracts = $500 ÷ $600 = 0.83 → 1 contract

Target = 24 points = $1,200 profit

Weekly Trade:

Risk = $375 (0.75% of $50k)

Stop = 40 points × $50 = $2,000

Contracts = $375 ÷ $2,000 = 0.18 → 1 contract

Target = 120 points = $6,000 profit

Monthly Trade:

Risk = $250 (0.5% of $50k)

Stop = 100 points × $50 = $5,000

Contracts = $250 ÷ $5,000 = 0.05 → 1 contract

Target = 400 points = $20,000 profit

6. Visual Elements on ChartKey Levels

Previous Daily High/Low - Red/Green solid lines

Previous Weekly High/Low - Red/Green circles

Previous Monthly High/Low - Red/Green crosses

Equilibrium Line - White dotted line (50% of range)

Zones

Premium Zone - Light red shading (upper 50%)

Discount Zone - Light green shading (lower 50%)

SMC Markings

Bullish Order Blocks - Green boxes with "Bull OB" label

Bearish Order Blocks - Red boxes with "Bear OB" label

Bullish FVGs - Green boxes with "FVG↑"

Bearish FVGs - Red boxes with "FVG↓"

Liquidity Sweeps - Yellow "SSL" (down) or "BSL" (up) labels

Break of Structure - Small lime/red circles

Entry Signals

Daily Long - Small lime triangle ▲ with "D" below price

Daily Short - Small red triangle ▼ with "D" above price

Weekly Long - Medium green triangle ▲ with "W" below price

Weekly Short - Medium maroon triangle ▼ with "W" above price

Monthly Long - Large aqua triangle ▲ with "M" below price

Monthly Short - Large fuchsia triangle ▼ with "M" above price

7. Information TablesConfluence Score Table (Top Right)

┌──────────┬────────┬────────┬────────┐

│ TF │ SCORE │ STATUS │ SIGNAL │

├──────────┼────────┼────────┼────────┤

│ 📊 DAILY │ 7/10 │ ✓ PASS │ 🔼 │

│ 📈 WEEKLY│ 6/10 │ ✗ WAIT │ ━ │

│ 🌙 MONTH │ 9/10 │ ✓ PASS │ 🔽 │

├──────────┴────────┴────────┴────────┤

│ P&L: $2,450 │

└─────────────────────────────────────┘

Green scores = Pass (meets minimum threshold)

Orange/Red scores = Fail (wait for better setup)

🔼 = Long signal active

🔽 = Short signal active

━ = No signal

Entry Checklist Table (Bottom Right)

┌──────────────┬───┐

│ CHECKLIST │ ✓ │

├──────────────┼───┤

│ ━ DAILY ━ │ │

│ HTF Trend │ ✓ │

│ Zone │ ✓ │

│ OB │ ✗ │

│ Liq Sweep │ ✓ │

│ Volume │ ✓ │

│ ━ WEEKLY ━ │ │

│ W/M Align │ ✓ │

│ Deep Zone │ ✗ │

│ ━ MONTHLY ━ │ │

│ M/W/D Align │ ✓ │

│ Zone: Discount│ │

└──────────────┴───┘

Green ✓ = Condition met

Red ✗ = Condition not met

Real-time updates as market conditions change

8. Alert SystemIndividual Alerts:

"Daily Long" - Triggers when daily long setup appears

"Daily Short" - Triggers when daily short setup appears

"Weekly Long" - Triggers when weekly long setup appears

"Weekly Short" - Triggers when weekly short setup appears

"Monthly Long" - Triggers when monthly long setup appears

"Monthly Short" - Triggers when monthly short setup appears

Combined Alerts:

"Any Long Signal" - Catches any bullish opportunity (D/W/M)

"Any Short Signal" - Catches any bearish opportunity (D/W/M)

Alert Messages Include:

🔼/🔽 Direction indicator

Timeframe (DAILY/WEEKLY/MONTHLY)

Current confluence score

New Rate - PREMIUM v2New Rate - PREMIUM v2

New Rate - PREMIUM v2 is an intraday Opening Range Breakout (ORB) strategy built around a strict one-trade-per-day execution model.

The strategy defines a price range using the first N candles of a user-defined session, freezes the High/Low at the close of candle N, and places OCO stop orders exactly at those levels. The first breakout fills, the opposite order is canceled, and no further trades are allowed until the next trading day.

This script is published for educational and research purposes, with documented mechanics and backtest settings to support transparency and reproducibility.

How the strategy works

Session range construction

The user selects a minutes-based timeframe, a session start time, and the number of candles N. During the session window, the strategy tracks the highest High and lowest Low formed by the first N candles. These candles are visually highlighted on the chart.

Range freeze

When candle N closes, the range is locked. Horizontal High/Low lines are drawn and extended forward. An optional 50% midpoint can be displayed for reference.

OCO breakout execution

Immediately after the range is frozen, the strategy places:

A buy stop at the frozen High

A sell stop at the frozen Low

Orders are linked using OCO (One-Cancels-Other) logic. When one side fills, the opposite order is automatically canceled.

Exit management

Two exit frameworks are available:

Tick-based exits: stop-loss and take-profit are fixed distances in ticks from entry.

Risk/Reward exits: optional stop at the opposite side of the range, with TP calculated as RR × risk.

Both modes can display SL/TP boxes projected forward for visual review.

Daily execution lock

After the first filled trade of the day, the strategy blocks any new entries until the next daily reset. This enforces strict discipline and prevents over-trading.

Visual features

Configurable High/Low lines and labels (color, style, width, alignment)

Optional midpoint (50%) line

Session background highlight with adjustable opacity

Optional SL/TP boxes with configurable colors, borders, and projection length

Weekday filter (trade only selected days)

Settings used for the published backtest (replication)

The performance screenshots included with this publication were generated using the following configuration:

Market & chart

Symbol: FX:XAUUSD

Timeframe: 15 minutes

Session & range

Session start: as configured on chart (exchange time)

Range candles (N): 1

Auto range end: enabled (TF × N)

Line extension: 20 bars

Exits

Exit mode: SL/TP by ticks

Stop-loss: 1500 ticks

Take-profit: 2000 ticks

Weekdays

Monday to Friday enabled

Strategy Properties (TradingView settings)

Initial capital: 1,000 USD

Commission: 0.1 (as set in Strategy Properties)

Slippage: 1 tick

Users should adjust commission, slippage, and position sizing to match their own broker and execution conditions.

Backtest context and limitations

This strategy uses stop orders that may fill intrabar depending on TradingView’s execution model.

Results vary by symbol, timeframe, session selection, and trading costs.

Past performance does not guarantee future results.

This script is not financial advice.

Originality and usefulness

While opening-range breakouts are a known concept, this strategy’s implementation focuses on:

Exact range-freeze timing: orders are armed precisely at the close of the N-th candle.

True OCO + hard daily lock: one-and-done execution enforced at the engine level.

Dual exit framework: fixed-tick and RR exits analyzed with the same SL/TP visual logic.

Operational safeguards: weekday filters and drawing limits designed for stable long-term backtesting.

Tether Dynamics - Statistical Exhaustion EngineOverview

This strategy detects statistical exhaustion in price movement by modeling price as a particle tethered to a dynamic anchor. When price stretches too far from equilibrium and multiple independent statistical detectors confirm anomalous behavior, the strategy identifies high-probability mean-reversion opportunities.

Unlike simple oversold/overbought indicators, this system fuses concepts from classical mechanics , stochastic filtering , multivariate statistics , and statistical process control into a unified detection framework.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

THEORETICAL FOUNDATION

1. The Tethered Particle Model

The framework draws inspiration from Polyak's heavy ball method in optimization theory, where a particle with momentum navigates a loss landscape. Here, price is modeled as a particle connected to a moving anchor (adaptive EMA) by an elastic "chain" whose length scales with volatility (ATR). This creates a natural physics framework:

Displacement (x) : Distance from anchor, normalized by chain length

Velocity (v) : Rate of change of displacement

Acceleration (a) : Rate of change of velocity

This state vector defines the system's "phase space" — a complete description of price dynamics relative to equilibrium.

2. Adaptive Anchor (Kaufman Efficiency)

The anchor uses an adaptive smoothing approach inspired by Perry Kaufman's Adaptive Moving Average. The Efficiency Ratio measures trend strength:

ER = |Direction| / Volatility = |Price - Price | / Σ|ΔPrice|

High efficiency (trending) → faster adaptation

Low efficiency (choppy) → slower, more stable anchor

This prevents whipsaws in ranging markets while staying responsive in trends.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DETECTION ARCHITECTURE

The strategy employs three independent statistical detectors , each grounded in distinct mathematical frameworks. A signal fires when price shows extended tension AND any detector confirms anomalous behavior AND momentum is decelerating (exhaustion).

Detector 1: Mahalanobis Distance (Multivariate Outlier Detection)

The Mahalanobis distance measures how "unusual" the current state vector is, accounting for correlations between displacement, velocity, and acceleration:

D² = (x - μ)ᵀ Σ⁻¹ (x - μ)

Where Σ is the full 3×3 covariance matrix. Under multivariate normality, D² follows a chi-squared distribution with 3 degrees of freedom:

χ²(3, 0.90) = 6.25 → 10% of observations exceed this

χ²(3, 0.95) = 7.81 → 5% of observations exceed this

This detector identifies states that are jointly extreme — even if no single variable looks unusual alone.

Why it matters: A price might have moderate displacement and moderate velocity, but the combination could be highly improbable. Mahalanobis captures this multivariate structure that univariate indicators miss.

Detector 2: CUSUM Change-Point Detection

Cumulative Sum (CUSUM) is a sequential analysis technique from statistical process control. It accumulates standardized deviations from the mean:

S⁺ₜ = max(0, S⁺ₜ₋₁ + zₜ - drift)

S⁻ₜ = min(0, S⁻ₜ₋₁ + zₜ + drift)

When either cumulative sum breaches a threshold, a "change point" is detected — the process has shifted from its baseline regime.

Why it matters: CUSUM detects subtle, persistent shifts that might not trigger on any single bar. It's sensitive to regime changes that precede reversals.

Detector 3: Kalman Innovation Filter (Ornstein-Uhlenbeck Model)

This detector models displacement as an Ornstein-Uhlenbeck process — the continuous-time analog of AR(1) mean-reversion:

dx = θ(μ - x)dt + σdW

A Kalman filter tracks the expected displacement and computes the innovation (prediction error):

νₜ = (yₜ - x̂ₜ|ₜ₋₁) / √Sₜ

Under correct model specification, normalized innovations should be ~N(0,1). Large innovations indicate the mean-reversion model is breaking down — price is behaving "unexpectedly" relative to equilibrium dynamics.

Adaptive Q Estimation: The filter continuously adjusts its process noise estimate based on innovation autocorrelation, maintaining calibration across different volatility regimes.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SIGNAL LOGIC

Long Signal Requirements:

Z-Displacement < -σ threshold (price stretched below anchor)

ANY detector fires (Mahalanobis outlier OR CUSUM change OR Kalman innovation < -2σ)

Z-Acceleration > 0 (downward momentum decelerating)

Short Signal Requirements:

Z-Displacement > +σ threshold (price stretched above anchor)

ANY detector fires

Z-Acceleration < 0 (upward momentum decelerating)

The deceleration requirement ensures we're catching exhaustion rather than fighting momentum.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK MANAGEMENT

Scale-Out Exit Strategy

Rather than all-or-nothing exits, the strategy takes profits at multiple R-levels:

Scale 1: 20% at 0.5R

Scale 2: 20% at 1.0R

Scale 3: 10% at 1.5R (optional)

Remainder: Trailing stop

This locks in gains while allowing winners to run.

Adaptive Trailing Stop

After reaching the activation threshold (default 1R), the stop trails from the highest high (longs) or lowest low (shorts) at a configurable ATR multiple.

Reversal Logic

When an opposite signal fires while in position, the strategy can close and flip direction rather than waiting for a stop-out.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PARAMETER GUIDANCE

Anchor Period (24) : Base period for adaptive anchor

ATR Period (14) : Volatility measurement

Chain Length Mult (2.5) : Tether elasticity — higher = more stretch allowed

Long Tension σ (1.5) : Lower = more signals

Short Tension σ (2.0) : Higher threshold for shorts (trend asymmetry)

Mahalanobis Threshold (6.25) : χ²(3, 0.90) — adjust for signal frequency

CUSUM Threshold (3.0) : Lower = more sensitive to regime shifts

Lookback Window (100) : Statistical estimation window

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BACKTEST NOTES

Historical testing on NQ (2020-2025) suggests:

Long signals show stronger edge than shorts in equity indices

1H and 30-min timeframes balance signal quality vs. frequency

"Long Only" mode recommended for equity index futures

Important: Past performance does not guarantee future results. This strategy involves significant risk of loss.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MATHEMATICAL REFERENCES

Polyak, B.T. (1964). "Some methods of speeding up the convergence of iteration methods" (Heavy ball method)

Bertsekas, D.P. (1999). "Nonlinear Programming" (Heavy ball method / momentum dynamics)

Mahalanobis, P.C. (1936). "On the generalized distance in statistics"

Page, E.S. (1954). "Continuous inspection schemes" (CUSUM)

Kalman, R.E. (1960). "A new approach to linear filtering and prediction problems"

Uhlenbeck, G.E. & Ornstein, L.S. (1930). "On the theory of Brownian motion"

Kaufman, P. (1995). "Smarter Trading" (Adaptive Moving Average)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This strategy is provided for educational and research purposes. Trading futures involves substantial risk of loss. The statistical methods employed do not guarantee profitable outcomes. Always use appropriate position sizing and risk management.

NQ Lunch High Low First Sweep StrategyThis script identifies the FIRST liquidity sweep of the Lunch session high or low

after the Lunch session has ended, based on ICT / Killzone concepts.

Logic summary:

• Tracks Lunch session High and Low (New York time)

• After Lunch session closes, monitors the market on 5-minute timeframe

• Triggers ONLY on the first sweep:

– Price wicks beyond Lunch High and closes back below → SHORT signal

– Price wicks beyond Lunch Low and closes back above → LONG signal

• Generates an alert at the exact bar where entry is expected

• Designed specifically for Nasdaq (NQ) futures

• One trade per day – no overtrading

Notes:

• Intended for 5-minute charts only

• Uses New York session timing

• This script does NOT manage exits (TP/SL) – entry logic only

• Best used as a confluence tool, not a standalone system

Educational & discretionary use only.

Elliott Wave Full Fractal System v2.0Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.

Change markets and timeframes to see where the logic behaves best.

Adapt to your own risk profile

If you plan to use it live:

Set Initial Capital to your real account size.

Adjust default_qty_value to a risk level you are comfortable with (often 0.5–2% per trade).

Set commission and slippage to realistic broker values.

Re-run the backtest after every major change.

Use as a framework, not a signal machine

Treat this as a structured Elliott/R:R framework:

Filter signals by higher-timeframe trend, major S/R, volume, or fundamentals.

Optionally hide some wave degrees or ABC labels if you want a cleaner chart.

Combine the system’s structure with your own trade management and discretion.

Best Practices & Limitations

This is an approximate Elliott Wave engine based on fractal pivots. It does not replace a full discretionary Elliott analysis.

All wave counts are algorithmic and can differ from a manual analyst’s interpretation.

Like any backtest, results depend heavily on:

Symbol and timeframe.

Sample size (more trades are better).

Realistic commission/slippage settings.

The 0-slippage default is chosen only to show the “raw logic”. In real markets, slippage can significantly impact performance.

No strategy wins all the time. Losing streaks and drawdowns will still occur even with a strict R:R framework.

Disclaimer

This script is for educational and research purposes only and does not constitute financial advice or a recommendation to buy or sell any security. Past performance, whether real or simulated, is not indicative of future results. Always test on multiple symbols/timeframes, use conservative risk, and consult your financial advisor before trading live capital.

BTC DCA Risk Metric StrategyBTC DCA Risk Strategy - Automated Dollar Cost Averaging with 3Commas Integration

Overview

This strategy combines the proven Oakley Wood Risk Metric with an intelligent tiered Dollar Cost Averaging (DCA) system, designed to help traders systematically accumulate Bitcoin during periods of low risk and take profits during high-risk conditions.

Key Features

📊 Multi-Component Risk Assessment

4-Year SMA Deviation: Measures Bitcoin's distance from its long-term mean

20-Week MA Analysis: Tracks medium-term momentum shifts

50-Day/50-Week MA Ratio: Captures short-to-medium term trend strength

All metrics are normalized by time to account for Bitcoin's maturing market dynamics

💰 3-Tier DCA Buy System

Level 1 (Low Risk): Conservative entry with base allocation

Level 2 (Lower Risk): Increased allocation as opportunity improves

Level 3 (Extreme Low Risk): Maximum allocation during rare buying opportunities

Buys execute every bar while risk remains below thresholds, enabling true DCA accumulation

📈 Progressive Profit Taking

Sell Level 1: Take initial profits as risk increases

Sell Level 2: Scale out further positions during elevated risk

Sell Level 3: Final exit during extreme market conditions

Sell levels automatically reset when new buy signals occur, allowing flexible re-entry

🤖 3Commas Integration

Fully automated webhook alerts for Custom Signal Bots

JSON payloads formatted per 3Commas API specifications

Supports multiple exchanges (Binance, Coinbase, Kraken, Gemini, Bybit)

Configurable quote currency (USD, USDT, BUSD)

How It Works

The strategy calculates a composite risk metric (0-1 scale):

0.0-0.2: Extreme buying opportunity (green zone)

0.2-0.5: Favorable accumulation range (yellow zone)

0.5-0.8: Neutral to cautious territory (orange zone)

0.8-1.0+: High risk, profit-taking zone (red zone)

Buy Logic: As risk decreases, position sizes increase automatically. If risk drops from L1 to L3 threshold, the strategy combines all three tier allocations for maximum exposure.

Sell Logic: Sequential profit-taking ensures you capture gains progressively. The system won't advance to Sell L2 until L1 completes, preventing premature full exits.

Configuration

Risk Metric Parameters:

All calculations use Bitcoin price data (any BTC chart works)

Time-normalized formulas adapt to market maturity

No manual parameter tuning required

Buy Settings:

Set risk thresholds for each tier (default: 0.20, 0.10, 0.00)

Define dollar amounts per tier (default: $10, $15, $20)

Fully customizable to your risk tolerance and capital

Sell Settings:

Configure risk thresholds for profit-taking (default: 1.00, 1.50, 2.00)

Set percentage of position to sell at each level (default: 25%, 35%, 40%)

3Commas Setup:

Create a Custom Signal Bot in 3Commas

Copy Bot UUID and Secret Token into strategy inputs

Enable 3Commas Alerts checkbox

Create TradingView alert: Condition → "alert() function calls only", Webhook → api.3commas.io

Backtesting Results

Strengths:

Systematically buys dips without emotion

Averages down during extended bear markets

Captures explosive bull run profits through tiered exits

Pyramiding (1000 max orders) allows true DCA behavior

Considerations:

Requires sufficient capital for multiple buys during prolonged downtrends

Backtest on Daily timeframe for most reliable signals

Past performance does not guarantee future results

Visual Design

The indicator pane displays:

Color-coded risk metric line: Changes from white→red→orange→yellow→green as risk decreases

Background zones: Green (buy), yellow (hold), red (sell) areas

Dashed threshold lines: Clear visual markers for each buy/sell level

Entry/Exit labels: Green buy labels and orange/red sell labels mark all trades

Credits

Original Risk Metric: Oakley Wood

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Modifications: pommesUNDwurst

Disclaimer

This strategy is for educational and informational purposes only. Cryptocurrency trading carries substantial risk of loss. Always conduct your own research and never invest more than you can afford to lose. The authors are not financial advisors and assume no responsibility for trading decisions made using this tool.

Sniper PRO: The "Buffett Mode" VFI System"The stock market is a device for transferring money from the impatient to the patient." — Warren Buffett

Most traders lose money because they try to catch every small move. Sniper PRO is designed for the opposite: It identifies the massive, multi-week and multi-month trends driven by Institutional "Smart Money", and keeps you in the trade until the real move is over.

This is not a scalping tool. This is a Wealth Compounding Engine.

🚀 Why is this the "Secret Weapon"?

We combined the most searched and respected indicators into a single, high-probability algorithm:

VFI (Smart Money Flow): Tracks what the "Whales" are doing, not the retail traders.

Fibonacci Golden Ratio: Uses math to secure profits, not guesswork.

Trend Protocol: Filters out 90% of market noise.

🔥 The "Diamond Hands" Logic (VFI Shield)

The biggest problem in long-term trading is getting shaken out by a temporary dip. Sniper PRO solves this with the VFI Shield:

Even if price drops below your Stop Loss, the algorithm checks the Institutional Volume.

If Big Money is still holding? The Shield holds. You stay in the trade.

This feature alone allows you to ride trends for Weeks and Months (like NVDA, TSLA, BTC runs) without exiting prematurely.

⚙️ How It Works

1. The "Buffett" Entry We only enter when the odds are stacked in our favor:

Trend: Price must be above the EMA 50 (Bull Market).

Volume: VFI must be Positive (Accumulation Phase).

Volatility: The market must be active, not chopping sideways.

2. The Compounding Exit (Fibonacci Ladder) Instead of selling too early, the system builds a Fibonacci Ladder behind the price.

As the asset grows, your Stop Loss climbs automatically to the next Fibonacci level (0.382 -> 0.5 -> 0.618).

This locks in profits step-by-step while giving the asset room to breathe and grow.

3. Asymmetric Safety Shorting is risky in a long-term bull market. The system automatically reduces the size of Short trades to protect your capital, while maximizing exposure to Long rallies.

📊 Visual Guide

🔵 Blue Line: The Trend Baseline.

🔴 Red Steps: Your "Locked" Profit Level (Trailing Stop).

🟣 Purple 'X': Where the trade finally closed (Transparency).

Background Color:

Green: Bull Market (Safe to hold).

Orange: Choppy/Dangerous (Cash is King).

Best For:

Swing Traders & Investors (1D, 4H Timeframes).

People who want to catch the Big Moves and ignore the noise.

Disclaimer: This tool is designed for trend following. Past performance is not indicative of future results. Always manage your risk.

QuantBot StrategyAutomated opening range breakout strategy for futures and intraday trading. Identifies the initial trading range and executes trades on breakouts with multiple confluence filters.

Key Features:

Opening Range Detection: Automatically identifies and tracks the opening range

Multi-Filter Entry System: Optional confluence filters to improve entry quality

Flexible Profit Targets: Dynamic targets based on recent volatility, or fixed tick/dollar targets

Advanced Position Management: Add to positions at key levels; partial profit-taking with trailing runners

Risk Controls: Multiple stop loss methods, maximum trade limits, and distance filters

Time-Based Filters: Configurable trading hours and days, with optional holiday blackouts

Visual Indicators: Displays trend lines, bands, and range levels on your chart

Designed for disciplined, systematic trading with customizable risk management and position sizing.

Super-AO with Risk Management Strategy Template - 11-29-25Super-AO Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to the Super-AO Strategy. This is more than just a buy/sell indicator; it is a complete, open-source Risk Management (RM) Template designed for the Pine Script community.

At its core, this script implements a robust swing-trading strategy combining the SuperTrend (for macro direction) and the Awesome Oscillator (for momentum). However, the real power lies under the hood: a custom-built Risk Management Engine that handles trade states, prevents repainting, and manages complex exit conditions like Staged Take Profits and Advanced Adaptive Trailing Stops (AATS).

We are releasing this code to help traders transition from simple indicators to professional-grade strategy structures.

2. Quick Action Guide (TL;DR)

Best Timeframe: 4 Hours (H4) and above. Designed for Swing Trading.

Best Assets: "Well-behaved" assets with clear liquidity (Major Forex pairs, BTC, ETH, Indices).

Strategy Type: Trend Following + Momentum Confirmation.

Key Feature: The Risk Management Engine is modular. You can strip out the "Super-AO" logic and insert your own strategy logic into the template easily.

Repainting: Strictly Non-Repainting. The engine calculates logic based on confirmed candle closes.

3. Detailed Report: How It Works

A. The Strategy Logic: Super-AO

The entry logic is based on the convergence of two classic indicators:

SuperTrend: Determines the overall trend bias (Green/Red).

Awesome Oscillator (AO): Measures market momentum.

The Signal:

LONG (+2): SuperTrend is Green AND AO is above the Zero Line AND AO is Rising.

SHORT (-2): SuperTrend is Red AND AO is below the Zero Line AND AO is Falling.

By requiring momentum to agree with the trend, this system filters out many false signals found in ranging markets.

B. The Risk Management (RM) Engine

This script features a proprietary State Machine designed by Signal Lynx. Unlike standard strategies that simply fire orders, this engine separates the Signal from the Execution.

Logic Injection: The engine listens for a specific integer signal: +2 (Buy) or -2 (Sell). This makes the code a Template. You can delete the Super-AO section, write your own logic, and simply pass a +2 or -2 to the RM_EngineInput variable. The engine handles the rest.

Trade States: The engine tracks the state of the trade (Entry, In-Trade, Exiting) to prevent signal spamming.

Aggressive vs. Conservative:

Conservative Mode: Waits for a full trend reversal before taking a new trade.

Aggressive Mode: Allows for re-entries if the trend is strong and valid conditions present themselves again (Pyramiding Type 1).

C. Advanced Exit Protocols

The strategy does not rely on a single exit point. It employs a "Layered Defense" approach:

Hard Stop Loss: A fixed percentage safety net.

Staged Take Profits (Scaling Out): The script allows you to set 3 distinct Take Profit levels. For example, you can close 10% of your position at TP1, 10% at TP2, and let the remaining 80% ride the trend.

Trailing Stop: A standard percentage-based trailer.

Advanced Adaptive Trailing Stop (AATS): This is a highly sophisticated volatility stop. It calculates market structure using Hirashima Sugita (HSRS) levels and Bollinger Bands to determine the "floor" and "ceiling" of price action.

If volatility is high: The stop loosens to prevent wicking out.

If volatility is low: The stop tightens to protect profit.

D. Repainting Protection

Many Pine Script strategies look great in backtesting but fail in live trading because they rely on "real-time" price data that disappears when the candle closes.

This Risk Management engine explicitly pulls data from the previous candle close (close , high , low ) for its calculations. This ensures that the backtest results you see match the reality of live execution.

4. For Developers & Modders

We encourage you to tear this code apart!

Look for the section titled // Super-AO Strategy Logic.

Replace that block with your own RSI, MACD, or Price Action logic.

Ensure your logic outputs a 2 for Buy and -2 for Sell.

Connect it to RM_EngineInput.

You now have a fully functioning Risk Management system for your custom strategy.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

This code has been in action since 2022 and is a known performer in PineScript v5. We provide this open source to help the community build better, safer automated systems.

If you are looking to automate your strategies, please take a look at Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source). If you make beneficial modifications, please release them back to the community!

黃金1KDual Indicator Collaborative Verification

Bollinger Stochastic System: Combines Bollinger Band breakouts with stochastic oscillator overbought/oversold conditions to accurately capture reversal opportunities

Dynamic Trend Channels: ATR-based adaptive channel system that tracks market trend strength and direction in real-time

Dual Signal Confirmation: Two independent systems working together to significantly improve signal reliability

⏰ Intelligent Time Management

Scheduled Closing Mechanism: Automatic position closing at fixed time daily (05:45 exchange time) to lock profits and avoid overnight risks

Exchange Time Zone Adaptation: Full support for GMT+8 time zone, precisely matching Asian trading sessions

Cross-day Logic Processing: Comprehensive trading day switching mechanism ensuring strategy continuity

🛡️ Rigorous Money Management

Fixed Percentage Stop Loss: 0.35% fixed stop loss per trade to strictly control single loss

Optimized Risk-Reward Ratio: 1:3.4 profit-to-loss ratio ensuring long-term positive expected returns

Automatic Position Sizing: 2% account equity-based position calculation for steady compound growth

📊 Advanced Visualization

Dynamic Channel Drawing: Real-time display of trend channel support/resistance and future price predictions

Long/Short Signal Marking: Clear entry markers with price labels for intuitive display

Real-time Alert System: Built-in trading signal notifications ensuring no missed opportunities

Technical Architecture

Indicator Fusion Logic

Trend Confirmation: FTC channels determine primary trend direction

Entry Timing: BBSR system provides precise entry points at channel boundaries

Signal Filtering: Dual conditions ensure entries only on high-quality signals