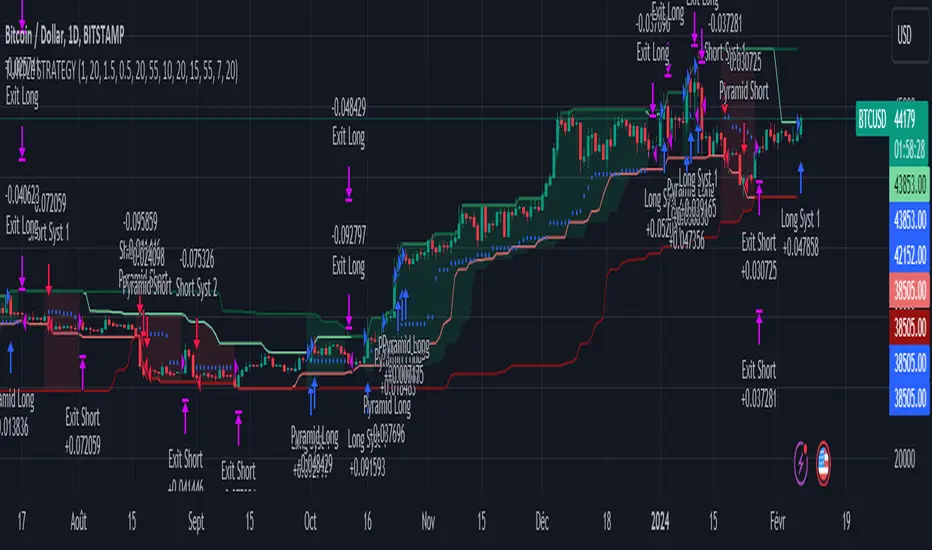

Quick scan for drift🙏🏻

ML based algorading is all about detecting any kind of non-randomness & exploiting it, kinda speculative stuff, not my way, but still...

Drift is one of the patterns that can be exploited, because pure random walks & noise aint got no drift.

This is an efficient method to quickly scan tons of timeseries on the go & detect the ones with drift by simply checking wherther drift < -0.5 or drift > 0.5. The code can be further optimized both in general and for specific needs, but I left it like dat for clarity so you can understand how it works in a minute not in an hour

^^ proving 0.5 and -0.5 are natural limits with no need to optimize anything, we simply put the metric on random noise and see it sits in between -0.5 and 0.5

You can simply take this one and never check anything again if you require numerous live scans on the go. The metric is purely geometrical, no connection to stats, TSA, DSA or whatever. I've tested numerous formulas involving other scaling techniques, drift estimates etc (even made a recursive algo that had a great potential to be written about in a paper, but not this time I gues lol), this one has the highest info gain aka info content.

The timeseries filtered by this lil metric can be further analyzed & modelled with more sophisticated tools.

Live Long and Prosper

P.S.: there's no such thing as polynomial trend/drift, it's alwasy linear, these curves you see are just really long cycles

P.S.: does cheer still work on TV? @admin

Поиск скриптов по запросу "通达信+选股公式+换手率+0.5+源码"

ICT Master Suite [Trading IQ]Hello Traders!

We’re excited to introduce the ICT Master Suite by TradingIQ, a new tool designed to bring together several ICT concepts and strategies in one place.

The Purpose Behind the ICT Master Suite

There are a few challenges traders often face when using ICT-related indicators:

Many available indicators focus on one or two ICT methods, which can limit traders who apply a broader range of ICT related techniques on their charts.

There aren't many indicators for ICT strategy models, and we couldn't find ICT indicators that allow for testing the strategy models and setting alerts.

Many ICT related concepts exist in the public domain as indicators, not strategies! This makes it difficult to verify that the ICT concept has some utility in the market you're trading and if it's worth trading - it's difficult to know if it's working!

Some users might not have enough chart space to apply numerous ICT related indicators, which can be restrictive for those wanting to use multiple ICT techniques simultaneously.

The ICT Master Suite is designed to offer a comprehensive option for traders who want to apply a variety of ICT methods. By combining several ICT techniques and strategy models into one indicator, it helps users maximize their chart space while accessing multiple tools in a single slot.

Additionally, the ICT Master Suite was developed as a strategy . This means users can backtest various ICT strategy models - including deep backtesting. A primary goal of this indicator is to let traders decide for themselves what markets to trade ICT concepts in and give them the capability to figure out if the strategy models are worth trading!

What Makes the ICT Master Suite Different

There are many ICT-related indicators available on TradingView, each offering valuable insights. What the ICT Master Suite aims to do is bring together a wider selection of these techniques into one tool. This includes both key ICT methods and strategy models, allowing traders to test and activate strategies all within one indicator.

Features

The ICT Master Suite offers:

Multiple ICT strategy models, including the 2022 Strategy Model and Unicorn Model, which can be built, tested, and used for live trading.

Calculation and display of key price areas like Breaker Blocks, Rejection Blocks, Order Blocks, Fair Value Gaps, Equal Levels, and more.

The ability to set alerts based on these ICT strategies and key price areas.

A comprehensive, yet practical, all-inclusive ICT indicator for traders.

Customizable Timeframe - Calculate ICT concepts on off-chart timeframes

Unicorn Strategy Model

2022 Strategy Model

Liquidity Raid Strategy Model

OTE (Optimal Trade Entry) Strategy Model

Silver Bullet Strategy Model

Order blocks

Breaker blocks

Rejection blocks

FVG

Strong highs and lows

Displacements

Liquidity sweeps

Power of 3

ICT Macros

HTF previous bar high and low

Break of Structure indications

Market Structure Shift indications

Equal highs and lows

Swings highs and swing lows

Fibonacci TPs and SLs

Swing level TPs and SLs

Previous day high and low TPs and SLs

And much more! An ongoing project!

How To Use

Many traders will already be familiar with the ICT related concepts listed above, and will find using the ICT Master Suite quite intuitive!

Despite this, let's go over the features of the tool in-depth and how to use the tool!

The image above shows the ICT Master Suite with almost all techniques activated.

ICT 2022 Strategy Model

The ICT Master suite provides the ability to test, set alerts for, and live trade the ICT 2022 Strategy Model.

The image above shows an example of a long position being entered following a complete setup for the 2022 ICT model.

A liquidity sweep occurs prior to an upside breakout. During the upside breakout the model looks for the FVG that is nearest 50% of the setup range. A limit order is placed at this FVG for entry.

The target entry percentage for the range is customizable in the settings. For instance, you can select to enter at an FVG nearest 33% of the range, 20%, 66%, etc.

The profit target for the model generally uses the highest high of the range (100%) for longs and the lowest low of the range (100%) for shorts. Stop losses are generally set at 0% of the range.

The image above shows the short model in action!

Whether you decide to follow the 2022 model diligently or not, you can still set alerts when the entry condition is met.

ICT Unicorn Model

The image above shows an example of a long position being entered following a complete setup for the ICT Unicorn model.

A lower swing low followed by a higher swing high precedes the overlap of an FVG and breaker block formed during the sequence.

During the upside breakout the model looks for an FVG and breaker block that formed during the sequence and overlap each other. A limit order is placed at the nearest overlap point to current price.

The profit target for this example trade is set at the swing high and the stop loss at the swing low. However, both the profit target and stop loss for this model are configurable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

For Longs, the selectable stop losses are:

Swing Low

Bottom of FVG or breaker block

The image above shows the short version of the Unicorn Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

For Shorts, the selectable stop losses are:

Swing High

Top of FVG or breaker block

The image above shows the profit target and stop loss options in the settings for the Unicorn Model.

Optimal Trade Entry (OTE) Model

The image above shows an example of a long position being entered following a complete setup for the OTE model.

Price retraces either 0.62, 0.705, or 0.79 of an upside move and a trade is entered.

The profit target for this example trade is set at the -0.5 fib level. This is also adjustable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

The image above shows the short version of the OTE Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

Liquidity Raid Model

The image above shows an example of a long position being entered following a complete setup for the Liquidity Raid Modell.

The user must define the session in the settings (for this example it is 13:30-16:00 NY time).

During the session, the indicator will calculate the session high and session low. Following a “raid” of either the session high or session low (after the session has completed) the script will look for an entry at a recently formed breaker block.

If the session high is raided the script will look for short entries at a bearish breaker block. If the session low is raided the script will look for long entries at a bullish breaker block.

For Longs, the profit target options are:

Swing high

User inputted Lib level

For Longs, the stop loss options are:

Swing low

User inputted Lib level

Breaker block bottom

The image above shows the short version of the Liquidity Raid Model in action!

For Shorts, the profit target options are:

Swing Low

User inputted Lib level

For Shorts, the stop loss options are:

Swing High

User inputted Lib level

Breaker block top

Silver Bullet Model

The image above shows an example of a long position being entered following a complete setup for the Silver Bullet Modell.

During the session, the indicator will determine the higher timeframe bias. If the higher timeframe bias is bullish the strategy will look to enter long at an FVG that forms during the session. If the higher timeframe bias is bearish the indicator will look to enter short at an FVG that forms during the session.

For Longs, the profit target options are:

Nearest Swing High Above Entry

Previous Day High

For Longs, the stop loss options are:

Nearest Swing Low

Previous Day Low

The image above shows the short version of the Silver Bullet Model in action!

For Shorts, the profit target options are:

Nearest Swing Low Below Entry

Previous Day Low

For Shorts, the stop loss options are:

Nearest Swing High

Previous Day High

Order blocks

The image above shows indicator identifying and labeling order blocks.

The color of the order blocks, and how many should be shown, are configurable in the settings!

Breaker Blocks

The image above shows indicator identifying and labeling order blocks.

The color of the breaker blocks, and how many should be shown, are configurable in the settings!

Rejection Blocks

The image above shows indicator identifying and labeling rejection blocks.

The color of the rejection blocks, and how many should be shown, are configurable in the settings!

Fair Value Gaps

The image above shows indicator identifying and labeling fair value gaps.

The color of the fair value gaps, and how many should be shown, are configurable in the settings!

Additionally, you can select to only show fair values gaps that form after a liquidity sweep. Doing so reduces "noisy" FVGs and focuses on identifying FVGs that form after a significant trading event.

The image above shows the feature enabled. A fair value gap that occurred after a liquidity sweep is shown.

Market Structure

The image above shows the ICT Master Suite calculating market structure shots and break of structures!

The color of MSS and BoS, and whether they should be displayed, are configurable in the settings.

Displacements

The images above show indicator identifying and labeling displacements.

The color of the displacements, and how many should be shown, are configurable in the settings!

Equal Price Points

The image above shows the indicator identifying and labeling equal highs and equal lows.

The color of the equal levels, and how many should be shown, are configurable in the settings!

Previous Custom TF High/Low

The image above shows the ICT Master Suite calculating the high and low price for a user-defined timeframe. In this case the previous day’s high and low are calculated.

To illustrate the customizable timeframe function, the image above shows the indicator calculating the previous 4 hour high and low.

Liquidity Sweeps

The image above shows the indicator identifying a liquidity sweep prior to an upside breakout.

The image above shows the indicator identifying a liquidity sweep prior to a downside breakout.

The color and aggressiveness of liquidity sweep identification are adjustable in the settings!

Power Of Three

The image above shows the indicator calculating Po3 for two user-defined higher timeframes!

Macros

The image above shows the ICT Master Suite identifying the ICT macros!

ICT Macros are only displayable on the 5 minute timeframe or less.

Strategy Performance Table

In addition to a full-fledged TradingView backtest for any of the ICT strategy models the indicator offers, a quick-and-easy strategy table exists for the indicator!

The image above shows the strategy performance table in action.

Keep in mind that, because the ICT Master Suite is a strategy script, you can perform fully automatic backtests, deep backtests, easily add commission and portfolio balance and look at pertinent metrics for the ICT strategies you are testing!

Lite Mode

Traders who want the cleanest chart possible can toggle on “Lite Mode”!

In Lite Mode, any neon or “glow” like effects are removed and key levels are marked as strict border boxes. You can also select to remove box borders if that’s what you prefer!

Settings Used For Backtest

For the displayed backtest, a starting balance of $1000 USD was used. A commission of 0.02%, slippage of 2 ticks, a verify price for limit orders of 2 ticks, and 5% of capital investment per order.

A commission of 0.02% was used due to the backtested asset being a perpetual future contract for a crypto currency. The highest commission (lowest-tier VIP) for maker orders on many exchanges is 0.02%. All entered positions take place as maker orders and so do profit target exits. Stop orders exist as stop-market orders.

A slippage of 2 ticks was used to simulate more realistic stop-market orders. A verify limit order settings of 2 ticks was also used. Even though BTCUSDT.P on Binance is liquid, we just want the backtest to be on the safe side. Additionally, the backtest traded 100+ trades over the period. The higher the sample size the better; however, this example test can serve as a starting point for traders interested in ICT concepts.

Community Assistance And Feedback

Given the complexity and idiosyncratic applications of ICT concepts amongst its proponents, the ICT Master Suite’s built-in strategies and level identification methods might not align with everyone's interpretation.

That said, the best we can do is precisely define ICT strategy rules and concepts to a repeatable process, test, and apply them! Whether or not an ICT strategy is trading precisely how you would trade it, seeing the model in action, taking trades, and with performance statistics is immensely helpful in assessing predictive utility.

If you think we missed something, you notice a bug, have an idea for strategy model improvement, please let us know! The ICT Master Suite is an ongoing project that will, ideally, be shaped by the community.

A big thank you to the @PineCoders for their Time Library!

Thank you!

Hurst Exponent SmoothedDescription:

The Hurst Exponent Smoothed indicator provides a dynamic analysis of market behavior by calculating the Hurst Exponent over a specified lookback period. This tool is especially useful for identifying whether a market is trending or mean-reverting.

Key Features:

Lookback Period: Set to 90 by default, this parameter controls how many periods the indicator considers for its calculations. Adjusting this value allows you to fine-tune the sensitivity of the indicator to recent price action.

Market Analysis: The Hurst Exponent gives insights into the nature of price movement:

A value near 0.5 suggests a random walk, indicating that the market is unpredictable.

Values above 0.5 indicate a trending market where price movements exhibit persistence, suggesting that the current trend may continue.

Values below 0.5 point to a mean-reverting market, where price movements tend to reverse, making it a potential signal for contrarian trading strategies.

Usage:

Trend Following: When the Hurst Exponent is consistently above 0.5, it may indicate a strong trend. Traders can use this information to align with the current market direction.

Mean Reversion: If the Hurst Exponent falls below 0.5, it could signal that the market is more likely to revert to the mean, offering opportunities for mean-reversion strategies.

Visuals:

The indicator displays a smooth line oscillating between values, giving traders a clear visual cue for the current market condition.

The script is optimized for various timeframes, as demonstrated on the BTCUSD pair on a 270-minute chart. Traders can adapt the lookback period based on their trading style and the specific asset being analyzed.

Open Source: This script is open-source and free to use. Feel free to customize and adapt it to your needs!

Correlation ZonesThis indicator highlights zones with strong, weak and negative correlation. Unlike standard coefficient indicator it will help to filter out noise when analyzing dependencies between two assets.

With default input setting Correlation_Threshold=0.5:

- Zones with correlation above 0.5, will be colored in green (strong correlation)

- Zones with correlation from -0.5 to 0.5 will be colored grey (weak correlation)

- Zones with correlation below -0.5 will be colore red (strong negative correlation)

Input parameter "Correlation_Threshold" can be modified in settings.

Provided example demonstrates BTCUSD correlation with NASDAQ Composite . I advice to use weekly timeframe and set length to 26 week for this study

Capped Standard Power Option [Loxx]Power options can lead to very high leverage and thus entail potentially very large losses for short positions in these options. It is therefore common to cap the payoff. The maximum payoff is set to some predefined level C. The payoff at maturity for a capped power call is min . Esser (2003) gives the closed-form solution: (via "The Complete Guide to Option Pricing Formulas")

c = S^i * (e^((i - 1) * (r + i*v^2 / 2) - i * (r - b))*T) * (N(e1) - N(e3)) - e^(-r*T) * (X*N(e2) - (C + X) * N(e4))

while the value of a put is

e1 = (log(S/X^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

e3 = (log(S/(C + X)^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

e4 = e3 - i * v * T^0.5

In the case of a capped power put, we have

p = e^(-r*T) * (X*N(-e2) - (C + X) * N(-e4)) - S^i * (e^((i - 1) * (r + i*v^2 / 2) - i * (r - b))*T) * (N(-e1) - N(-e3))

where e1 and e2 is as before. e3 and e4 has to be changed to

e3 = (log(S/(X - C)^(1/i)) + (b + (i - 1/2)*v^2)*T) / v*T^0.5

e4 = e3 - i * v * T^0.5

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

i = power

c = Capped on pay off

cnd1(x) = Cumulative Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

3 more indicators: Inverse Fisher on RSI/MFI and CyberCycleSuggested by John Ehlers, IFT helps you to determine the exact oversold/overbought points in any oscillator-type indicators.

The 3 IFT based indicators in this chart are:

- Inverse Fisher on RSI (IFTRSI)

- Inverse Fisher on MFI (IFTMFI)

- Inverse Fisher on CyberCycle (IFTCC)

Suggested method to use any IFT indicator is to buy when the indicator crosses over –0.5 or crosses over +0.5 if it has not previously crossed over –0.5 and to sell short when the indicators crosses under +0.5 or crosses under –0.5 if it has not previously crossed under +0.5.

More info: www.mesasoftware.com

You can use these indicators by doing "Make it mine" (Click on "Share" to open the dialog box with this button).

Let me know what you think, would love to hear how these indicators are used and how effective these are for other instruments.

Fisher (zero-color + simple OB assist)//@version=5

indicator("Fisher (zero-color + simple OB assist)", overlay=false)

// Inputs

length = input.int(10, "Fisher Period", minval=1)

pivotLen = input.int(3, "Structure pivot length (SMC-lite)", minval=1)

showZero = input.bool(true, "Show Zero Line")

colPos = input.color(color.lime, "Color Above 0 (fallback)")

colNeg = input.color(color.red, "Color Below 0 (fallback)")

useOB = input.bool(true, "Color by OB proximity (Demand below = green, Supply above = red)")

showOBMarks = input.bool(true, "Show OB markers")

// Fisher (MT4-style port)

price = (high + low) / 2.0

hh = ta.highest(high, length)

ll = ta.lowest(low, length)

rng = hh - ll

norm = rng != 0 ? (price - ll) / rng : 0.5

var float v = 0.0

var float fish = 0.0

v := 0.33 * 2.0 * (norm - 0.5) + 0.67 * nz(v , 0)

v := math.min(math.max(v, -0.999), 0.999)

fish := 0.5 * math.log((1 + v) / (1 - v)) + 0.5 * nz(fish , 0)

// SMC-lite OB

ph = ta.pivothigh(high, pivotLen, pivotLen)

pl = ta.pivotlow(low, pivotLen, pivotLen)

var float lastSwingHigh = na

var float lastSwingLow = na

if not na(ph)

lastSwingHigh := ph

if not na(pl)

lastSwingLow := pl

bosUp = not na(lastSwingHigh) and close > lastSwingHigh

bosDn = not na(lastSwingLow) and close < lastSwingLow

bearishBar = close < open

bullishBar = close > open

demHigh_new = ta.valuewhen(bearishBar, high, 0)

demLow_new = ta.valuewhen(bearishBar, low, 0)

supHigh_new = ta.valuewhen(bullishBar, high, 0)

supLow_new = ta.valuewhen(bullishBar, low, 0)

// แยกประกาศตัวแปรทีละตัว และใช้ชนิดให้ชัดเจน

var float demHigh = na

var float demLow = na

var float supHigh = na

var float supLow = na

var bool demActive = false

var bool supActive = false

if bosUp and not na(demHigh_new) and not na(demLow_new)

demHigh := demHigh_new

demLow := demLow_new

demActive := true

if bosDn and not na(supHigh_new) and not na(supLow_new)

supHigh := supHigh_new

supLow := supLow_new

supActive := true

// Mitigation (แตะโซน)

if demActive and not na(demHigh) and not na(demLow)

if low <= demHigh

demActive := false

if supActive and not na(supHigh) and not na(supLow)

if high >= supLow

supActive := false

demandBelow = useOB and demActive and not na(demHigh) and demHigh <= close

supplyAbove = useOB and supActive and not na(supLow) and supLow >= close

colDimUp = color.new(colPos, 40)

colDimDown = color.new(colNeg, 40)

barColor = demandBelow ? colPos : supplyAbove ? colNeg : fish > 0 ? colDimUp : colDimDown

// Plots

plot(0, title="Zero", color=showZero ? color.new(color.gray, 70) : color.new(color.gray, 100))

plot(fish, title="Fisher", style=plot.style_columns, color=barColor, linewidth=2)

plotchar(showOBMarks and demandBelow ? fish : na, title="Demand below", char="D", location=location.absolute, color=color.teal, size=size.tiny)

plotchar(showOBMarks and supplyAbove ? fish : na, title="Supply above", char="S", location=location.absolute, color=color.fuchsia, size=size.tiny)

alertcondition(ta.crossover(fish, 0.0), "Fisher Cross Up", "Fisher crosses above 0")

alertcondition(ta.crossunder(fish, 0.0), "Fisher Cross Down", "Fisher crosses below 0")

TimeSeriesBenchmarkMeasuresLibrary "TimeSeriesBenchmarkMeasures"

Time Series Benchmark Metrics. \

Provides a comprehensive set of functions for benchmarking time series data, allowing you to evaluate the accuracy, stability, and risk characteristics of various models or strategies. The functions cover a wide range of statistical measures, including accuracy metrics (MAE, MSE, RMSE, NRMSE, MAPE, SMAPE), autocorrelation analysis (ACF, ADF), and risk measures (Theils Inequality, Sharpness, Resolution, Coverage, and Pinball).

___

Reference:

- github.com .

- medium.com .

- www.salesforce.com .

- towardsdatascience.com .

- github.com .

mae(actual, forecasts)

In statistics, mean absolute error (MAE) is a measure of errors between paired observations expressing the same phenomenon. Examples of Y versus X include comparisons of predicted versus observed, subsequent time versus initial time, and one technique of measurement versus an alternative technique of measurement.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Absolute Error (MAE).

___

Reference:

- en.wikipedia.org .

- The Orange Book of Machine Learning - Carl McBride Ellis .

mse(actual, forecasts)

The Mean Squared Error (MSE) is a measure of the quality of an estimator. As it is derived from the square of Euclidean distance, it is always a positive value that decreases as the error approaches zero.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Squared Error (MSE).

___

Reference:

- en.wikipedia.org .

rmse(targets, forecasts, order, offset)

Calculates the Root Mean Squared Error (RMSE) between target observations and forecasts. RMSE is a standard measure of the differences between values predicted by a model and the values actually observed.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - RMSE value.

nmrse(targets, forecasts, order, offset)

Normalised Root Mean Squared Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - NRMSE value.

rmse_interval(targets, forecasts)

Root Mean Squared Error for a set of interval windows. Computes RMSE by converting interval forecasts (with min/max bounds) into point forecasts using the mean of the interval bounds, then compares against actual target values.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - RMSE value for the combined interval list.

mape(targets, forecasts)

Mean Average Percentual Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

Returns: - MAPE value.

smape(targets, forecasts, mode)

Symmetric Mean Average Percentual Error. Calculates the Mean Absolute Percentage Error (MAPE) between actual targets and forecasts. MAPE is a common metric for evaluating forecast accuracy, expressed as a percentage, lower values indicate a better forecast accuracy.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

mode (int) : Type of method: default=0:`sum(abs(Fi-Ti)) / sum(Fi+Ti)` , 1:`mean(abs(Fi-Ti) / ((Fi + Ti) / 2))` , 2:`mean(abs(Fi-Ti) / (abs(Fi) + abs(Ti))) * 100`

Returns: - SMAPE value.

mape_interval(targets, forecasts)

Mean Average Percentual Error for a set of interval windows.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - MAPE value for the combined interval list.

acf(data, k)

Autocorrelation Function (ACF) for a time series at a specified lag.

Parameters:

data (array) : Sample data of the observations.

k (int) : The lag period for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - The autocorrelation value at the specified lag, ranging from -1 to 1.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

acf_multiple(data, k)

Autocorrelation function (ACF) for a time series at a set of specified lags.

Parameters:

data (array) : Sample data of the observations.

k (array) : List of lag periods for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - List of ACF values for provided lags.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

adfuller(data, n_lag, conf)

: Augmented Dickey-Fuller test for stationarity.

Parameters:

data (array) : Data series.

n_lag (int) : Maximum lag.

conf (string) : Confidence Probability level used to test for critical value, (`90%`, `95%`, `99%`).

Returns: - `adf` The test statistic.

- `crit` Critical value for the test statistic at the 10 % levels.

- `nobs` Number of observations used for the ADF regression and calculation of the critical values.

___

The Augmented Dickey-Fuller test is used to determine whether a time series is stationary

or contains a unit root (non-stationary). The null hypothesis is that the series has a unit root

(is non-stationary), while the alternative hypothesis is that the series is stationary.

A stationary time series has statistical properties that do not change over time, making it

suitable for many time series forecasting models. If the test statistic is less than the

critical value, we reject the null hypothesis and conclude the series is stationary.

___

Reference:

- www.jstor.org

- en.wikipedia.org

theils_inequality(targets, forecasts)

Calculates Theil's Inequality Coefficient, a measure of forecast accuracy that quantifies the relative difference between actual and predicted values.

Parameters:

targets (array) : List of target observations.

forecasts (array) : Matrix with list of forecasts, ordered column wise.

Returns: - Theil's Inequality Coefficient value, value closer to 0 is better.

___

Theil's Inequality Coefficient is calculated as: `sqrt(Sum((y_i - f_i)^2)) / (sqrt(Sum(y_i^2)) + sqrt(Sum(f_i^2)))`

where `y_i` represents actual values and `f_i` represents forecast values.

This metric ranges from 0 to infinity, with 0 indicating perfect forecast accuracy.

___

Reference:

- en.wikipedia.org

sharpness(forecasts)

The average width of the forecast intervals across all observations, representing the sharpness or precision of the predictive intervals.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Sharpness The sharpness level, which is the average width of all prediction intervals across the forecast horizon.

___

Sharpness is an important metric for evaluating forecast quality. It measures how narrow or wide the

prediction intervals are. Higher sharpness (narrower intervals) indicates greater precision in the

forecast intervals, while lower sharpness (wider intervals) suggests less precision.

The sharpness metric is calculated as the mean of the interval widths across all observations, where

each interval width is the difference between the upper and lower bounds of the prediction interval.

Note: This function assumes that the forecasts matrix has at least 2 columns, with the first column

representing the lower bounds and the second column representing the upper bounds of prediction intervals.

___

Reference:

- Hyndman, R. J., & Athanasopoulos, G. (2018). Forecasting: principles and practice. OTexts. otexts.com

resolution(forecasts)

Calculates the resolution of forecast intervals, measuring the average absolute difference between individual forecast interval widths and the overall sharpness measure.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The average absolute difference between individual forecast interval widths and the overall sharpness measure, representing the resolution of the forecasts.

___

Resolution is a key metric for evaluating forecast quality that measures the consistency of prediction

interval widths. It quantifies how much the individual forecast intervals vary from the average interval

width (sharpness). High resolution indicates that the forecast intervals are relatively consistent

across observations, while low resolution suggests significant variation in interval widths.

The resolution is calculated as the mean absolute deviation of individual interval widths from the

overall sharpness value. This provides insight into the uniformity of the forecast uncertainty

estimates across the forecast horizon.

Note: This function requires the forecasts matrix to have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (sites.stat.washington.edu)

- (www.jstor.org)

coverage(targets, forecasts)

Calculates the coverage probability, which is the percentage of target values that fall within the corresponding forecasted prediction intervals.

Parameters:

targets (array) : List of target values.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Percent of target values that fall within their corresponding forecast intervals, expressed as a decimal value between 0 and 1 (or 0% and 100%).

___

Coverage probability is a crucial metric for evaluating the reliability of prediction intervals.

It measures how well the forecast intervals capture the actual observed values. An ideal forecast

should have a coverage probability close to the nominal confidence level (e.g., 90%, 95%, or 99%).

For example, if a 95% prediction interval is used, we expect approximately 95% of the actual

target values to fall within those intervals. If the coverage is significantly lower than the

nominal level, the intervals may be too narrow; if it's significantly higher, the intervals may

be too wide.

Note: This function requires the targets array and forecasts matrix to have the same number of

observations, and the forecasts matrix must have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (www.jstor.org)

pinball(tau, target, forecast)

Pinball loss function, measures the asymmetric loss for quantile forecasts.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

target (float) : The actual observed value to compare against.

forecast (float) : The forecasted value.

Returns: - The Pinball loss value, which quantifies the distance between the forecast and target relative to the specified quantile level.

___

The Pinball loss function is specifically designed for evaluating quantile forecasts. It is

asymmetric, meaning it penalizes underestimates and overestimates differently depending on the

quantile level being evaluated.

For a given quantile τ, the loss function is defined as:

- If target >= forecast: (target - forecast) * τ

- If target < forecast: (forecast - target) * (1 - τ)

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

pinball_mean(tau, targets, forecasts)

Calculates the mean pinball loss for quantile regression.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

targets (array) : The actual observed values to compare against.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The mean pinball loss value across all observations.

___

The pinball_mean() function computes the average Pinball loss across multiple observations,

making it suitable for evaluating overall forecast performance in quantile regression tasks.

This function leverages the asymmetric Pinball loss function to evaluate how well forecasts

capture specific quantiles of the target distribution. The choice of which column from the

forecasts matrix to use depends on the quantile level:

- For τ ≤ 0.5: Uses the first column (min) of forecasts

- For τ > 0.5: Uses the second column (max) of forecasts

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

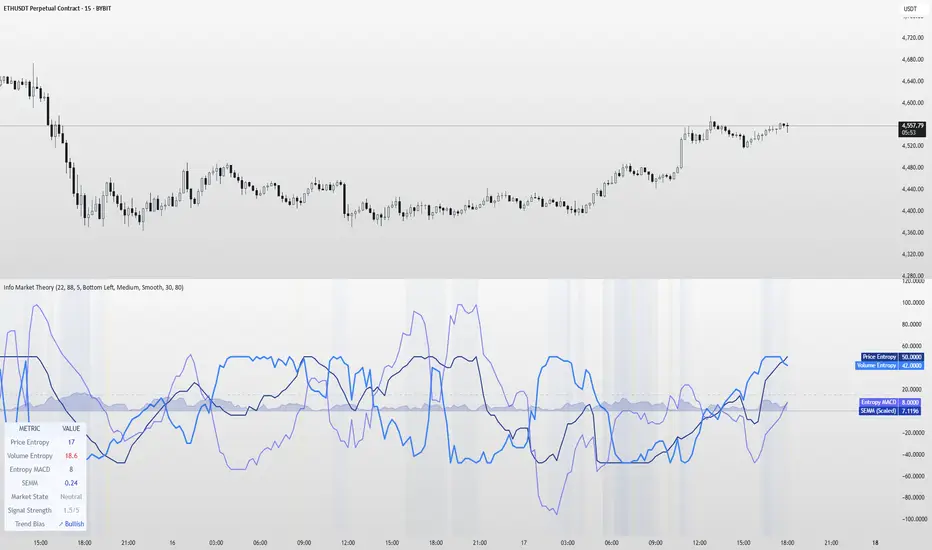

Information Theory Market AnalysisINFORMATION THEORY MARKET ANALYSIS

OVERVIEW

This indicator applies mathematical concepts from information theory to analyze market behavior, measuring the randomness and predictability of price and volume movements through entropy calculations. Unlike traditional technical indicators, it provides insight into market structure and regime changes.

KEY COMPONENTS

Four Main Signals:

• Price Entropy (Deep Blue): Measures randomness in price movements

• Volume Entropy (Bright Blue): Analyzes volume pattern predictability

• Entropy MACD (Purple): Shows relationship between price and volume entropy

• SEMM (Royal Blue): Stochastic Entropy Market Monitor - overall market randomness gauge

Market State Detection:

The indicator identifies seven distinct market states:

• Strong Trending (SEMM < 0.1)

• Weak Trending (0.1-0.2)

• Neutral (0.2-0.3)

• Moderate Random (0.3-0.5)

• High Randomness (0.5-0.8)

• Very Random (0.8-1.0)

• Chaotic (>1.0)

KEY FEATURES

Advanced Analytics:

• Signal Strength Confluence: 0-5 scale measuring alignment of multiple factors

• Entropy Crossovers: Detects shifts between accumulation and distribution phases

• Extreme Readings: Identifies statistical outliers for potential reversals

• Trend Bias Analysis: Directional momentum assessment

Information Dashboard:

• Real-time entropy values and market state

• Signal strength indicator with visual highlighting

• Trend bias with directional arrows

• Color-coded alerts for extreme conditions

Customizable Display:

• Adjustable SEMM scaling (5x to 100x) for optimal visibility

• Multiple line styles: Smooth, Stepped, Dotted

• 9 table positions with 3 size options

• Professional blue color scheme with transparency controls

Comprehensive Alert System - 15 Alert Types Including:

• Extreme entropy readings (price/volume)

• Crossover signals (dominance shifts)

• Market state changes (trending ↔ random)

• High confluence signals (3+ factors aligned)

HOW TO USE

Reading the Signals:

• Entropy Values > ±25: Strong structural signals

• Entropy Values > ±40: Extreme readings, potential reversals

• SEMM < 0.2: Trending market favors directional strategies

• SEMM > 0.5: Random market favors range/scalping strategies

Signal Confluence:

Look for multiple factors aligning:

• Signal Strength ≥ 3.0 for higher probability setups

• Background highlighting indicates confluence

• Table shows real-time strength assessment

Timeframe Optimization:

• Short-term (1m-15m): Entropy Length 14-22, Sensitivity 3-5

• Swing Trading (1H-4H): Default settings optimal

• Position Trading (Daily+): Entropy Length 34-55, Sensitivity 8-12

EDUCATIONAL APPLICATIONS

Market Structure Analysis:

• Understand when markets are trending vs. ranging

• Identify accumulation and distribution phases

• Recognize extreme market conditions

• Measure information content in price movements

Information Theory Concepts:

• Binary entropy calculations applied to financial data

• Probability distribution analysis of returns

• Statistical ranking and percentile analysis

• Momentum-adjusted randomness measurement

TECHNICAL DETAILS

Calculations:

• Uses binary entropy formula: -

• Percentile ranking across multiple timeframes

• Volume-weighted probability distributions

• RSI-adjusted momentum entropy (SEMM)

Customization Options:

• Entropy Length: 5-100 bars (default: 22)

• Average Length: 10-200 bars (default: 88)

• Sensitivity: 1.0-20.0 (default: 5.0, lower = more sensitive)

• SEMM Scaling: 5.0-100.0x (default: 30.0)

IMPORTANT NOTES

Risk Considerations:

• Indicator measures probabilities, not certainties

• High SEMM values (>0.5) suggest increased market randomness

• Extreme readings may persist longer than expected

• Always combine with proper risk management

Educational Purpose:

This indicator is designed for:

• Market structure analysis and education

• Understanding information theory applications in finance

• Developing probabilistic thinking about markets

• Research and analytical purposes

Performance Tips:

• Allow 200+ bars for proper initialization

• Adjust scaling and transparency for optimal visibility

• Use confluence signals for higher probability analysis

• Consider multiple timeframes for comprehensive analysis

DISCLAIMER

This indicator is for educational and analytical purposes. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and consider your risk tolerance before making trading decisions.

Version: 5.0

Category: Oscillators, Volume, Market Structure

Best For: All timeframes, trending and ranging markets

Complexity: Intermediate to Advanced

SMC Structures and FVGสวัสดีครับ! ผมจะอธิบายอินดิเคเตอร์ "SMC Structures and FVG + MACD" ที่คุณให้มาอย่างละเอียดในแต่ละส่วน เพื่อให้คุณเข้าใจการทำงานของมันอย่างถ่องแท้ครับ

อินดิเคเตอร์นี้เป็นการผสมผสานแนวคิดของ Smart Money Concept (SMC) ซึ่งเน้นการวิเคราะห์โครงสร้างตลาด (Market Structure) และ Fair Value Gap (FVG) เข้ากับอินดิเคเตอร์ MACD เพื่อใช้เป็นตัวกรองหรือตัวยืนยันสัญญาณ Choch/BoS (Change of Character / Break of Structure)

1. ภาพรวมอินดิเคเตอร์ (Overall Purpose)

อินดิเคเตอร์นี้มีจุดประสงค์หลักคือ:

ระบุโครงสร้างตลาด: ตีเส้นและป้ายกำกับ Choch (Change of Character) และ BoS (Break of Structure) บนกราฟโดยอัตโนมัติ

ผสานการยืนยันด้วย MACD: สัญญาณ Choch/BoS จะถูกพิจารณาก็ต่อเมื่อ MACD Histogram เกิดการตัดขึ้นหรือลง (Zero Cross) ในทิศทางที่สอดคล้องกัน

แสดง Fair Value Gap (FVG): หากเปิดใช้งาน จะมีการตีกล่อง FVG บนกราฟ

แสดงระดับ Fibonacci: คำนวณและแสดงระดับ Fibonacci ที่สำคัญตามโครงสร้างตลาดปัจจุบัน

ปรับตาม Timeframe: การคำนวณและการแสดงผลทั้งหมดจะปรับตาม Timeframe ที่คุณกำลังใช้งานอยู่โดยอัตโนมัติ

2. ส่วนประกอบหลักของโค้ด (Code Breakdown)

โค้ดนี้สามารถแบ่งออกเป็นส่วนหลัก ๆ ได้ดังนี้:

2.1 Inputs (การตั้งค่า)

ส่วนนี้คือตัวแปรที่คุณสามารถปรับแต่งได้ในหน้าต่างการตั้งค่าของอินดิเคเตอร์ (คลิกที่รูปฟันเฟืองข้างชื่ออินดิเคเตอร์บนกราฟ)

MACD Settings (ตั้งค่า MACD):

fast_len: ความยาวของ Fast EMA สำหรับ MACD (ค่าเริ่มต้น 12)

slow_len: ความยาวของ Slow EMA สำหรับ MACD (ค่าเริ่มต้น 26)

signal_len: ความยาวของ Signal Line สำหรับ MACD (ค่าเริ่มต้น 9)

= ta.macd(close, fast_len, slow_len, signal_len): คำนวณค่า MACD Line, Signal Line และ Histogram โดยใช้ราคาปิด (close) และค่าความยาวที่กำหนด

is_bullish_macd_cross: ตรวจสอบว่า MACD Histogram ตัดขึ้นเหนือเส้น 0 (จากค่าลบเป็นบวก)

is_bearish_macd_cross: ตรวจสอบว่า MACD Histogram ตัดลงใต้เส้น 0 (จากค่าบวกเป็นลบ)

Fear Value Gap (FVG) Settings:

isFvgToShow: (Boolean) เปิด/ปิดการแสดง FVG บนกราฟ

bullishFvgColor: สีสำหรับ Bullish FVG

bearishFvgColor: สีสำหรับ Bearish FVG

mitigatedFvgColor: สีสำหรับ FVG ที่ถูก Mitigate (ลดทอน) แล้ว

fvgHistoryNbr: จำนวน FVG ย้อนหลังที่จะแสดง

isMitigatedFvgToReduce: (Boolean) เปิด/ปิดการลดขนาด FVG เมื่อถูก Mitigate

Structures (โครงสร้างตลาด) Settings:

isStructBodyCandleBreak: (Boolean) หากเป็น true การ Break จะต้องเกิดขึ้นด้วย เนื้อเทียน ที่ปิดเหนือ/ใต้ Swing High/Low หากเป็น false แค่ไส้เทียนทะลุก็ถือว่า Break

isCurrentStructToShow: (Boolean) เปิด/ปิดการแสดงเส้นโครงสร้างตลาดปัจจุบัน (เส้นสีน้ำเงินในภาพตัวอย่าง)

pivot_len: ความยาวของแท่งเทียนที่ใช้ในการมองหาจุด Pivot (Swing High/Low) ยิ่งค่าน้อยยิ่งจับ Swing เล็กๆ ได้, ยิ่งค่ามากยิ่งจับ Swing ใหญ่ๆ ได้

bullishBosColor, bearishBosColor: สีสำหรับเส้นและป้าย BOS ขาขึ้น/ขาลง

bosLineStyleOption, bosLineWidth: สไตล์ (Solid, Dotted, Dashed) และความหนาของเส้น BOS

bullishChochColor, bearishChochColor: สีสำหรับเส้นและป้าย CHoCH ขาขึ้น/ขาลง

chochLineStyleOption, chochLineWidth: สไตล์ (Solid, Dotted, Dashed) และความหนาของเส้น CHoCH

currentStructColor, currentStructLineStyleOption, currentStructLineWidth: สี, สไตล์ และความหนาของเส้นโครงสร้างตลาดปัจจุบัน

structHistoryNbr: จำนวนการ Break (Choch/BoS) ย้อนหลังที่จะแสดง

Structure Fibonacci (จากโค้ดต้นฉบับ):

เป็นชุด Input สำหรับเปิด/ปิด, กำหนดค่า, สี, สไตล์ และความหนาของเส้น Fibonacci Levels ต่างๆ (0.786, 0.705, 0.618, 0.5, 0.382) ที่จะถูกคำนวณจากโครงสร้างตลาดปัจจุบัน

2.2 Helper Functions (ฟังก์ชันช่วยทำงาน)

getLineStyle(lineOption): ฟังก์ชันนี้ใช้แปลงค่า String ที่เลือกจาก Input (เช่น "─", "┈", "╌") ให้เป็นรูปแบบ line.style_ ที่ Pine Script เข้าใจ

get_structure_highest_bar(lookback): ฟังก์ชันนี้พยายามหา Bar Index ของแท่งเทียนที่ทำ Swing High ภายในช่วง lookback ที่กำหนด

get_structure_lowest_bar(lookback): ฟังก์ชันนี้พยายามหา Bar Index ของแท่งเทียนที่ทำ Swing Low ภายในช่วง lookback ที่กำหนด

is_structure_high_broken(...): ฟังก์ชันนี้ตรวจสอบว่าราคาปัจจุบันได้ Break เหนือ _structureHigh (Swing High) หรือไม่ โดยพิจารณาจาก _highStructBreakPrice (ราคาปิดหรือราคา High ขึ้นอยู่กับการตั้งค่า isStructBodyCandleBreak)

FVGDraw(...): ฟังก์ชันนี้รับ Arrays ของ FVG Boxes, Types, Mitigation Status และ Labels มาประมวลผล เพื่ออัปเดตสถานะของ FVG (เช่น ถูก Mitigate หรือไม่) และปรับขนาด/ตำแหน่งของ FVG Box และ Label บนกราฟ

2.3 Global Variables (ตัวแปรทั่วทั้งอินดิเคเตอร์)

เป็นตัวแปรที่ประกาศด้วย var ซึ่งหมายความว่าค่าของมันจะถูกเก็บไว้และอัปเดตในแต่ละแท่งเทียน (persists across bars)

structureLines, structureLabels: Arrays สำหรับเก็บอ็อบเจกต์ line และ label ของเส้น Choch/BoS ที่วาดบนกราฟ

fvgBoxes, fvgTypes, fvgLabels, isFvgMitigated: Arrays สำหรับเก็บข้อมูลของ FVG Boxes และสถานะต่างๆ

structureHigh, structureLow: เก็บราคาของ Swing High/Low ที่สำคัญของโครงสร้างตลาดปัจจุบัน

structureHighStartIndex, structureLowStartIndex: เก็บ Bar Index ของจุดเริ่มต้นของ Swing High/Low ที่สำคัญ

structureDirection: เก็บสถานะของทิศทางโครงสร้างตลาด (1 = Bullish, 2 = Bearish, 0 = Undefined)

fiboXPrice, fiboXStartIndex, fiboXLine, fiboXLabel: ตัวแปรสำหรับเก็บข้อมูลและอ็อบเจกต์ของเส้น Fibonacci Levels

isBOSAlert, isCHOCHAlert: (Boolean) ใช้สำหรับส่งสัญญาณ Alert (หากมีการตั้งค่า Alert ไว้)

2.4 FVG Processing (การประมวลผล FVG)

ส่วนนี้จะตรวจสอบเงื่อนไขการเกิด FVG (Bullish FVG: high < low , Bearish FVG: low > high )

หากเกิด FVG และ isFvgToShow เป็น true จะมีการสร้าง box และ label ใหม่เพื่อแสดง FVG บนกราฟ

มีการจัดการ fvgBoxes และ fvgLabels เพื่อจำกัดจำนวน FVG ที่แสดงตาม fvgHistoryNbr และลบ FVG เก่าออก

ฟังก์ชัน FVGDraw จะถูกเรียกเพื่ออัปเดตสถานะของ FVG (เช่น การถูก Mitigate) และปรับการแสดงผล

2.5 Structures Processing (การประมวลผลโครงสร้างตลาด)

Initialization: ที่ bar_index == 0 (แท่งเทียนแรกของกราฟ) จะมีการกำหนดค่าเริ่มต้นให้กับ structureHigh, structureLow, structureHighStartIndex, structureLowStartIndex

Finding Current High/Low: highest, highestBar, lowest, lowestBar ถูกใช้เพื่อหา High/Low ที่สุดและ Bar Index ของมันใน 10 แท่งล่าสุด (หรือทั้งหมดหากกราฟสั้นกว่า 10 แท่ง)

Calculating Structure Max/Min Bar: structureMaxBar และ structureMinBar ใช้ฟังก์ชัน get_structure_highest_bar และ get_structure_lowest_bar เพื่อหา Bar Index ของ Swing High/Low ที่แท้จริง (ไม่ใช่แค่ High/Low ที่สุดใน lookback แต่เป็นจุด Pivot ที่สมบูรณ์)

Break Price: lowStructBreakPrice และ highStructBreakPrice จะเป็นราคาปิด (close) หรือราคา Low/High ขึ้นอยู่กับ isStructBodyCandleBreak

isStuctureLowBroken / isStructureHighBroken: เงื่อนไขเหล่านี้ตรวจสอบว่าราคาได้ทำลาย structureLow หรือ structureHigh หรือไม่ โดยพิจารณาจากราคา Break, ราคาแท่งก่อนหน้า และ Bar Index ของจุดเริ่มต้นโครงสร้าง

Choch/BoS Logic (ส่วนสำคัญที่ถูกผสานกับ MACD):

if(isStuctureLowBroken and is_bearish_macd_cross): นี่คือจุดที่ MACD เข้ามามีบทบาท หากราคาทำลาย structureLow (สัญญาณขาลง) และ MACD Histogram เกิด Bearish Zero Cross (is_bearish_macd_cross เป็น true) อินดิเคเตอร์จะพิจารณาว่าเป็น Choch หรือ BoS

หาก structureDirection == 1 (เดิมเป็นขาขึ้น) หรือ 0 (ยังไม่กำหนด) จะตีเป็น "CHoCH" (เปลี่ยนทิศทางโครงสร้างเป็นขาลง)

หาก structureDirection == 2 (เดิมเป็นขาลง) จะตีเป็น "BOS" (ยืนยันโครงสร้างขาลง)

มีการสร้าง line.new และ label.new เพื่อวาดเส้นและป้ายกำกับ

structureDirection จะถูกอัปเดตเป็น 1 (Bullish)

structureHighStartIndex, structureLowStartIndex, structureHigh, structureLow จะถูกอัปเดตเพื่อกำหนดโครงสร้างใหม่

else if(isStructureHighBroken and is_bullish_macd_cross): เช่นกันสำหรับขาขึ้น หากราคาทำลาย structureHigh (สัญญาณขาขึ้น) และ MACD Histogram เกิด Bullish Zero Cross (is_bullish_macd_cross เป็น true) อินดิเคเตอร์จะพิจารณาว่าเป็น Choch หรือ BoS

หาก structureDirection == 2 (เดิมเป็นขาลง) หรือ 0 (ยังไม่กำหนด) จะตีเป็น "CHoCH" (เปลี่ยนทิศทางโครงสร้างเป็นขาขึ้น)

หาก structureDirection == 1 (เดิมเป็นขาขึ้น) จะตีเป็น "BOS" (ยืนยันโครงสร้างขาขึ้น)

มีการสร้าง line.new และ label.new เพื่อวาดเส้นและป้ายกำกับ

structureDirection จะถูกอัปเดตเป็น 2 (Bearish)

structureHighStartIndex, structureLowStartIndex, structureHigh, structureLow จะถูกอัปเดตเพื่อกำหนดโครงสร้างใหม่

การลบเส้นเก่า: d.delete_line (หากไลบรารีทำงาน) จะถูกเรียกเพื่อลบเส้นและป้ายกำกับเก่าออกเมื่อจำนวนเกิน structHistoryNbr

Updating Structure High/Low (else block): หากไม่มีการ Break เกิดขึ้น แต่ราคาปัจจุบันสูงกว่า structureHigh หรือต่ำกว่า structureLow ในทิศทางที่สอดคล้องกัน (เช่น ยังคงเป็นขาขึ้นและทำ High ใหม่) structureHigh หรือ structureLow จะถูกอัปเดตเพื่อติดตาม High/Low ที่สุดของโครงสร้างปัจจุบัน

Current Structure Display:

หาก isCurrentStructToShow เป็น true อินดิเคเตอร์จะวาดเส้น structureHighLine และ structureLowLine เพื่อแสดงขอบเขตของโครงสร้างตลาดปัจจุบัน

Fibonacci Display:

หาก isFiboXToShow เป็น true อินดิเคเตอร์จะคำนวณและวาดเส้น Fibonacci Levels ต่างๆ (0.786, 0.705, 0.618, 0.5, 0.382) โดยอิงจาก structureHigh และ structureLow ของโครงสร้างตลาดปัจจุบัน

Alerts:

alertcondition: ใช้สำหรับตั้งค่า Alert ใน TradingView เมื่อเกิดสัญญาณ BOS หรือ CHOCH

plot(na):

plot(na) เป็นคำสั่งที่สำคัญในอินดิเคเตอร์ที่ไม่ได้ต้องการพล็อต Series ของข้อมูลบนกราฟ (เช่น ไม่ได้พล็อตเส้น EMA หรือ RSI) แต่ใช้วาดอ็อบเจกต์ (Line, Label, Box) โดยตรง

การมี plot(na) ช่วยให้ Pine Script รู้ว่าอินดิเคเตอร์นี้มีเอาต์พุตที่แสดงผลบนกราฟ แม้ว่าจะไม่ได้เป็น Series ที่พล็อตตามปกติก็ตาม

3. วิธีใช้งาน

คัดลอกโค้ดทั้งหมด ที่อยู่ในบล็อก immersive ด้านบน

ไปที่ TradingView และเปิดกราฟที่คุณต้องการ

คลิกที่เมนู "Pine Editor" ที่อยู่ด้านล่างของหน้าจอ

ลบโค้ดเดิมที่มีอยู่ และ วางโค้ดที่คัดลอกมา ลงไปแทน

คลิกที่ปุ่ม "Add to Chart"

อินดิเคเตอร์จะถูกเพิ่มลงในกราฟของคุณโดยอัตโนมัติ คุณสามารถคลิกที่รูปฟันเฟืองข้างชื่ออินดิเคเตอร์บนกราฟเพื่อเข้าถึงหน้าต่างการตั้งค่าและปรับแต่งตามความต้องการของคุณได้

Hello! I will explain the "SMC Structures and FVG + MACD" indicator you provided in detail, section by section, so you can fully understand how it works.This indicator combines the concepts of Smart Money Concept (SMC), which focuses on analyzing Market Structure and Fair Value Gaps (FVG), with the MACD indicator to serve as a filter or confirmation for Choch (Change of Character) and BoS (Break of Structure) signals.1. Overall PurposeThe main purposes of this indicator are:Identify Market Structure: Automatically draw lines and label Choch (Change of Character) and BoS (Break of Structure) on the chart.Integrate MACD Confirmation: Choch/BoS signals will only be considered when the MACD Histogram performs a cross (Zero Cross) in the corresponding direction.Display Fair Value Gap (FVG): If enabled, FVG boxes will be drawn on the chart.Display Fibonacci Levels: Calculate and display important Fibonacci levels based on the current market structure.Adapt to Timeframe: All calculations and displays will automatically adjust to the timeframe you are currently using.2. Code BreakdownThis code can be divided into the following main sections:2.1 Inputs (Settings)This section contains variables that you can adjust in the indicator's settings window (click the gear icon next to the indicator's name on the chart).MACD Settings:fast_len: Length of the Fast EMA for MACD (default 12)slow_len: Length of the Slow EMA for MACD (default 26)signal_len: Length of the Signal Line for MACD (default 9) = ta.macd(close, fast_len, slow_len, signal_len): Calculates the MACD Line, Signal Line, and Histogram using the closing price (close) and the specified lengths.is_bullish_macd_cross: Checks if the MACD Histogram crosses above the 0 line (from negative to positive).is_bearish_macd_cross: Checks if the MACD Histogram crosses below the 0 line (from positive to negative).Fear Value Gap (FVG) Settings:isFvgToShow: (Boolean) Enables/disables the display of FVG on the chart.bullishFvgColor: Color for Bullish FVG.bearishFvgColor: Color for Bearish FVG.mitigatedFvgColor: Color for FVG that has been mitigated.fvgHistoryNbr: Number of historical FVG to display.isMitigatedFvgToReduce: (Boolean) Enables/disables reducing the size of FVG when mitigated.Structures (โครงสร้างตลาด) Settings:isStructBodyCandleBreak: (Boolean) If true, the break must occur with the candle body closing above/below the Swing High/Low. If false, a wick break is sufficient.isCurrentStructToShow: (Boolean) Enables/disables the display of the current market structure lines (blue lines in the example image).pivot_len: Lookback length for identifying Pivot points (Swing High/Low). A smaller value captures smaller, more frequent swings; a larger value captures larger, more significant swings.bullishBosColor, bearishBosColor: Colors for bullish/bearish BOS lines and labels.bosLineStyleOption, bosLineWidth: Style (Solid, Dotted, Dashed) and width of BOS lines.bullishChochColor, bearishChochColor: Colors for bullish/bearish CHoCH lines and labels.chochLineStyleOption, chochLineWidth: Style (Solid, Dotted, Dashed) and width of CHoCH lines.currentStructColor, currentStructLineStyleOption, currentStructLineWidth: Color, style, and width of the current market structure lines.structHistoryNbr: Number of historical breaks (Choch/BoS) to display.Structure Fibonacci (from original code):A set of inputs to enable/disable, define values, colors, styles, and widths for various Fibonacci Levels (0.786, 0.705, 0.618, 0.5, 0.382) that will be calculated from the current market structure.2.2 Helper FunctionsgetLineStyle(lineOption): This function converts the selected string input (e.g., "─", "┈", "╌") into a line.style_ format understood by Pine Script.get_structure_highest_bar(lookback): This function attempts to find the Bar Index of the Swing High within the specified lookback period.get_structure_lowest_bar(lookback): This function attempts to find the Bar Index of the Swing Low within the specified lookback period.is_structure_high_broken(...): This function checks if the current price has broken above _structureHigh (Swing High), considering _highStructBreakPrice (closing price or high price depending on isStructBodyCandleBreak setting).FVGDraw(...): This function takes arrays of FVG Boxes, Types, Mitigation Status, and Labels to process and update the status of FVG (e.g., whether it's mitigated) and adjust the size/position of FVG Boxes and Labels on the chart.2.3 Global VariablesThese are variables declared with var, meaning their values are stored and updated on each bar (persists across bars).structureLines, structureLabels: Arrays to store line and label objects for Choch/BoS lines drawn on the chart.fvgBoxes, fvgTypes, fvgLabels, isFvgMitigated: Arrays to store FVG box data and their respective statuses.structureHigh, structureLow: Stores the price of the significant Swing High/Low of the current market structure.structureHighStartIndex, structureLowStartIndex: Stores the Bar Index of the start point of the significant Swing High/Low.structureDirection: Stores the status of the market structure direction (1 = Bullish, 2 = Bearish, 0 = Undefined).fiboXPrice, fiboXStartIndex, fiboXLine, fiboXLabel: Variables to store data and objects for Fibonacci Levels.isBOSAlert, isCHOCHAlert: (Boolean) Used to trigger alerts in TradingView (if alerts are configured).2.4 FVG ProcessingThis section checks the conditions for FVG formation (Bullish FVG: high < low , Bearish FVG: low > high ).If FVG occurs and isFvgToShow is true, a new box and label are created to display the FVG on the chart.fvgBoxes and fvgLabels are managed to limit the number of FVG displayed according to fvgHistoryNbr and remove older FVG.The FVGDraw function is called to update the FVG status (e.g., whether it's mitigated) and adjust its display.2.5 Structures ProcessingInitialization: At bar_index == 0 (the first bar of the chart), structureHigh, structureLow, structureHighStartIndex, and structureLowStartIndex are initialized.Finding Current High/Low: highest, highestBar, lowest, lowestBar are used to find the highest/lowest price and its Bar Index of it in the last 10 bars (or all bars if the chart is shorter than 10 bars).Calculating Structure Max/Min Bar: structureMaxBar and structureMinBar use get_structure_highest_bar and get_structure_lowest_bar functions to find the Bar Index of the true Swing High/Low (not just the highest/lowest in the lookback but a complete Pivot point).Break Price: lowStructBreakPrice and highStructBreakPrice will be the closing price (close) or the Low/High price, depending on the isStructBodyCandleBreak setting.isStuctureLowBroken / isStructureHighBroken: These conditions check if the price has broken structureLow or structureHigh, considering the break price, previous bar prices, and the Bar Index of the structure's starting point.Choch/BoS Logic (Key Integration with MACD):if(isStuctureLowBroken and is_bearish_macd_cross): This is where MACD plays a role. If the price breaks structureLow (bearish signal) AND the MACD Histogram performs a Bearish Zero Cross (is_bearish_macd_cross is true), the indicator will consider it a Choch or BoS.If structureDirection == 1 (previously bullish) or 0 (undefined), it will be labeled "CHoCH" (changing structure direction to bearish).If structureDirection == 2 (already bearish), it will be labeled "BOS" (confirming bearish structure).line.new and label.new are used to draw the line and label.structureDirection will be updated to 1 (Bullish).structureHighStartIndex, structureLowStartIndex, structureHigh, structureLow will be updated to define the new structure.else if(isStructureHighBroken and is_bullish_macd_cross): Similarly for bullish breaks. If the price breaks structureHigh (bullish signal) AND the MACD Histogram performs a Bullish Zero Cross (is_bullish_macd_cross is true), the indicator will consider it a Choch or BoS.If structureDirection == 2 (previously bearish) or 0 (undefined), it will be labeled "CHoCH" (changing structure direction to bullish).If structureDirection == 1 (already bullish), it will be labeled "BOS" (confirming bullish structure).line.new and label.new are used to draw the line and label.structureDirection will be updated to 2 (Bearish).structureHighStartIndex, structureLowStartIndex, structureHigh, structureLow will be updated to define the new structure.Deleting Old Lines: d.delete_line (if the library works) will be called to delete old lines and labels when their number exceeds structHistoryNbr.Updating Structure High/Low (else block): If no break occurs, but the current price is higher than structureHigh or lower than structureLow in the corresponding direction (e.g., still bullish and making a new high), structureHigh or structureLow will be updated to track the highest/lowest point of the current structure.Current Structure Display:If isCurrentStructToShow is true, the indicator draws structureHighLine and structureLowLine to show the boundaries of the current market structure.Fibonacci Display:If isFiboXToShow is true, the indicator calculates and draws various Fibonacci Levels (0.786, 0.705, 0.618, 0.5, 0.382) based on the structureHigh and structureLow of the current market structure.Alerts:alertcondition: Used to set up alerts in TradingView when BOS or CHOCH signals occur.plot(na):plot(na) is an important statement in indicators that do not plot data series directly on the chart (e.g., not plotting EMA or RSI lines) but instead draw objects (Line, Label, Box).Having plot(na) helps Pine Script recognize that this indicator has an output displayed on the chart, even if it's not a regularly plotted series.3. How to UseCopy all the code in the immersive block above.Go to TradingView and open your desired chart.Click on the "Pine Editor" menu at the bottom of the screen.Delete any existing code and paste the copied code in its place.Click the "Add to Chart" button.The indicator will be added to your chart automatically. You can click the gear icon next to the indicator's name on the chart to access the settings window and customize it to your needs.I hope this explanation helps you understand this indicator in detail. If anything is unclear, or you need further adjustments, please let me know.

Logarithmic Moving Average (LMA) [QuantAlgo]🟢 Overview

The Logarithmic Moving Average (LMA) uses advanced logarithmic weighting to create a dynamic trend-following indicator that prioritizes recent price action while maintaining statistical significance. Unlike traditional moving averages that use linear or exponential weights, this indicator employs logarithmic decay functions to create a more sophisticated price averaging system that adapts to market volatility and momentum conditions.

The indicator displays a smoothed signal line that oscillates around zero, with positive values indicating bullish momentum and negative values indicating bearish momentum. The signal incorporates trend quality assessment, momentum confirmation, and multiple filtering mechanisms to help traders and investors identify trend continuation and reversal opportunities across different timeframes and asset classes.

🟢 How It Works

The indicator's core innovation lies in its logarithmic weighting system, where weights are calculated using the formula: w = 1.0 / math.pow(math.log(i + steepness), 2) The steepness parameter controls how aggressively recent data is prioritized over historical data, creating a dynamic weight decay that can be fine-tuned for different trading styles. This logarithmic approach provides more nuanced weight distribution compared to exponential moving averages, offering better responsiveness while maintaining stability.

The LMA calculation combines multiple sophisticated components. First, it calculates the logarithmic weighted average of closing prices. Then it measures the slope of this average over a 10-period lookback: lmaSlope = (lma - lma ) / lma * 100 The system also incorporates trend quality assessment using R-squared correlation analysis of log-transformed prices, measuring how well the price data fits a linear trend model over the specified period.

The final signal generation uses the formula: signal = lmaSlope * (0.5 + rSquared * 0.5) which combines the LMA slope with trend quality weighting. When momentum confirmation is enabled, the indicator calculates annualized log-return momentum and applies a multiplier when the momentum direction aligns with the signal direction, strengthening confirmed signals while filtering out weak or counter-trend movements.

🟢 How to Use

1. Signal Interpretation and Threshold Zones

Positive Values (Above Zero): LMA slope indicating bullish momentum with upward price trajectory relative to logarithmic baseline

Negative Values (Below Zero): LMA slope indicating bearish momentum with downward price trajectory relative to logarithmic baseline

Zero Line Crosses: Signal transitions between bullish and bearish regimes, indicating potential trend changes

Long Entry Threshold Zone: Area above positive threshold (default 0.5) indicating confirmed bullish signals suitable for long positions

Short Entry Threshold Zone: Area below negative threshold (default -0.5) indicating confirmed bearish signals suitable for short positions

Extreme Values: Signals exceeding ±1.0 represent strong momentum conditions with higher probability of continuation

2. Momentum Confirmation and Visual Analysis

Signal Color Intensity: Gradient coloring shows signal strength, with brighter colors indicating stronger momentum

Bar Coloring: Optional price bar coloring matches signal direction for quick visual trend identification

Position Labels: Real-time position classification (Bullish/Bearish/Neutral) displayed on the latest bar

Momentum Weight Factor: When short-term log-return momentum aligns with LMA signal direction, the signal receives additional weight confirmation

Trend Quality Component: R-squared values weight the signal strength, with higher correlation indicating more reliable trend conditions

3. Examples: Preconfigured Settings

Default: Universally applicable configuration balanced for medium-term investing and general trading across multiple timeframes and asset classes.

Scalping: Highly responsive setup with shorter period and higher steepness for ultra-short-term trades on 1-15 minute charts, optimized for quick momentum shifts.

Swing Trading: Extended period with moderate steepness and increased smoothing for multi-day positions, designed to filter noise while capturing larger price swings on 1-4 hour and daily charts.

Trend Following: Maximum smoothing with lower steepness for established trend identification, generating fewer but more reliable signals optimal for daily and weekly timeframes.

Mean Reversion: Shorter period with high steepness for counter-trend strategies, more sensitive to extreme moves and reversal opportunities in ranging market conditions.

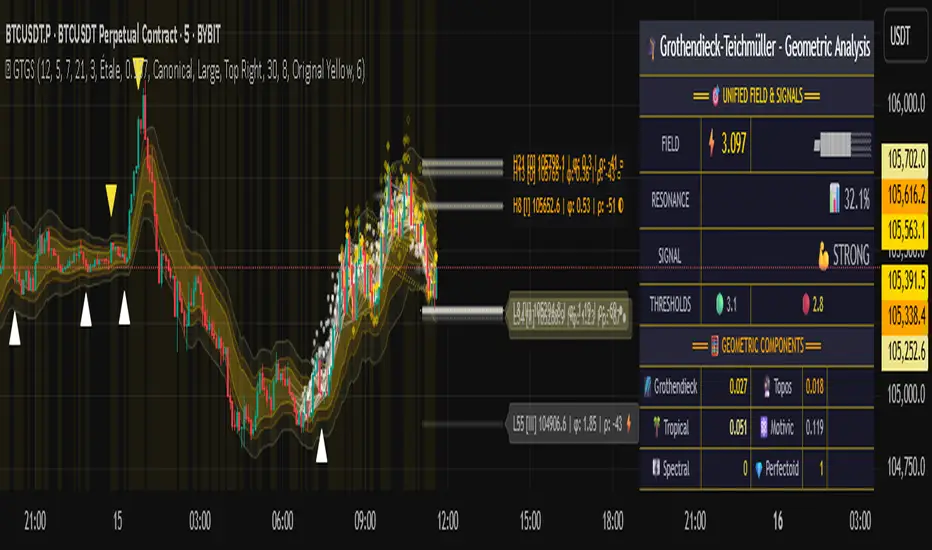

Grothendieck-Teichmüller Geometric SynthesisDskyz's Grothendieck-Teichmüller Geometric Synthesis (GTGS)

THEORETICAL FOUNDATION: A SYMPHONY OF GEOMETRIES

The 🎓 GTGS is built upon a revolutionary premise: that market dynamics can be modeled as geometric and topological structures. While not a literal academic implementation—such a task would demand computational power far beyond current trading platforms—it leverages core ideas from advanced mathematical theories as powerful analogies and frameworks for its algorithms. Each component translates an abstract concept into a practical market calculation, distinguishing GTGS by identifying deeper structural patterns rather than relying on standard statistical measures.

1. Grothendieck-Teichmüller Theory: Deforming Market Structure

The Theory : Studies symmetries and deformations of geometric objects, focusing on the "absolute" structure of mathematical spaces.

Indicator Analogy : The calculate_grothendieck_field function models price action as a "deformation" from its immediate state. Using the nth root of price ratios (math.pow(price_ratio, 1.0/prime)), it measures market "shape" stretching or compression, revealing underlying tensions and potential shifts.

2. Topos Theory & Sheaf Cohomology: From Local to Global Patterns

The Theory : A framework for assembling local properties into a global picture, with cohomology measuring "obstructions" to consistency.

Indicator Analogy : The calculate_topos_coherence function uses sine waves (math.sin) to represent local price "sections." Summing these yields a "cohomology" value, quantifying price action consistency. High values indicate coherent trends; low values signal conflict and uncertainty.

3. Tropical Geometry: Simplifying Complexity

The Theory : Transforms complex multiplicative problems into simpler, additive, piecewise-linear ones using min(a, b) for addition and a + b for multiplication.

Indicator Analogy : The calculate_tropical_metric function applies tropical_add(a, b) => math.min(a, b) to identify the "lowest energy" state among recent price points, pinpointing critical support levels non-linearly.

4. Motivic Cohomology & Non-Commutative Geometry

The Theory : Studies deep arithmetic and quantum-like properties of geometric spaces.

Indicator Analogy : The motivic_rank and spectral_triple functions compute weighted sums of historical prices to capture market "arithmetic complexity" and "spectral signature." Higher values reflect structured, harmonic price movements.

5. Perfectoid Spaces & Homotopy Type Theory

The Theory : Abstract fields dealing with p-adic numbers and logical foundations of mathematics.

Indicator Analogy : The perfectoid_conv and type_coherence functions analyze price convergence and path identity, assessing the "fractal dust" of price differences and price path cohesion, adding fractal and logical analysis.

The Combination is Key : No single theory dominates. GTGS ’s Unified Field synthesizes all seven perspectives into a comprehensive score, ensuring signals reflect deep structural alignment across mathematical domains.

🎛️ INPUTS: CONFIGURING THE GEOMETRIC ENGINE

The GTGS offers a suite of customizable inputs, allowing traders to tailor its behavior to specific timeframes, market sectors, and trading styles. Below is a detailed breakdown of key input groups, their functionality, and optimization strategies, leveraging provided tooltips for precision.

Grothendieck-Teichmüller Theory Inputs

🧬 Deformation Depth (Absolute Galois) :

What It Is : Controls the depth of Galois group deformations analyzed in market structure.

How It Works : Measures price action deformations under automorphisms of the absolute Galois group, capturing market symmetries.

Optimization :

Higher Values (15-20) : Captures deeper symmetries, ideal for major trends in swing trading (4H-1D).

Lower Values (3-8) : Responsive to local deformations, suited for scalping (1-5min).

Timeframes :

Scalping (1-5min) : 3-6 for quick local shifts.

Day Trading (15min-1H) : 8-12 for balanced analysis.

Swing Trading (4H-1D) : 12-20 for deep structural trends.

Sectors :

Stocks : Use 8-12 for stable trends.

Crypto : 3-8 for volatile, short-term moves.

Forex : 12-15 for smooth, cyclical patterns.

Pro Tip : Increase in trending markets to filter noise; decrease in choppy markets for sensitivity.

🗼 Teichmüller Tower Height :

What It Is : Determines the height of the Teichmüller modular tower for hierarchical pattern detection.

How It Works : Builds modular levels to identify nested market patterns.

Optimization :

Higher Values (6-8) : Detects complex fractals, ideal for swing trading.

Lower Values (2-4) : Focuses on primary patterns, faster for scalping.

Timeframes :

Scalping : 2-3 for speed.

Day Trading : 4-5 for balanced patterns.

Swing Trading : 5-8 for deep fractals.

Sectors :

Indices : 5-8 for robust, long-term patterns.

Crypto : 2-4 for rapid shifts.

Commodities : 4-6 for cyclical trends.

Pro Tip : Higher towers reveal hidden fractals but may slow computation; adjust based on hardware.

🔢 Galois Prime Base :

What It Is : Sets the prime base for Galois field computations.

How It Works : Defines the field extension characteristic for market analysis.

Optimization :

Prime Characteristics :

2 : Binary markets (up/down).

3 : Ternary states (bull/bear/neutral).

5 : Pentagonal symmetry (Elliott waves).

7 : Heptagonal cycles (weekly patterns).

11,13,17,19 : Higher-order patterns.

Timeframes :

Scalping/Day Trading : 2 or 3 for simplicity.

Swing Trading : 5 or 7 for wave or cycle detection.

Sectors :

Forex : 5 for Elliott wave alignment.

Stocks : 7 for weekly cycle consistency.

Crypto : 3 for volatile state shifts.

Pro Tip : Use 7 for most markets; 5 for Elliott wave traders.

Topos Theory & Sheaf Cohomology Inputs

🏛️ Temporal Site Size :

What It Is : Defines the number of time points in the topological site.

How It Works : Sets the local neighborhood for sheaf computations, affecting cohomology smoothness.

Optimization :

Higher Values (30-50) : Smoother cohomology, better for trends in swing trading.

Lower Values (5-15) : Responsive, ideal for reversals in scalping.

Timeframes :

Scalping : 5-10 for quick responses.

Day Trading : 15-25 for balanced analysis.

Swing Trading : 25-50 for smooth trends.

Sectors :

Stocks : 25-35 for stable trends.

Crypto : 5-15 for volatility.

Forex : 20-30 for smooth cycles.

Pro Tip : Match site size to your average holding period in bars for optimal coherence.

📐 Sheaf Cohomology Degree :

What It Is : Sets the maximum degree of cohomology groups computed.

How It Works : Higher degrees capture complex topological obstructions.

Optimization :

Degree Meanings :

1 : Simple obstructions (basic support/resistance).

2 : Cohomological pairs (double tops/bottoms).

3 : Triple intersections (complex patterns).

4-5 : Higher-order structures (rare events).

Timeframes :

Scalping/Day Trading : 1-2 for simplicity.

Swing Trading : 3 for complex patterns.

Sectors :

Indices : 2-3 for robust patterns.

Crypto : 1-2 for rapid shifts.

Commodities : 3-4 for cyclical events.

Pro Tip : Degree 3 is optimal for most trading; higher degrees for research or rare event detection.

🌐 Grothendieck Topology :

What It Is : Chooses the Grothendieck topology for the site.

How It Works : Affects how local data integrates into global patterns.

Optimization :

Topology Characteristics :

Étale : Finest topology, captures local-global principles.

Nisnevich : A1-invariant, good for trends.

Zariski : Coarse but robust, filters noise.

Fpqc : Faithfully flat, highly sensitive.

Sectors :

Stocks : Zariski for stability.

Crypto : Étale for sensitivity.

Forex : Nisnevich for smooth trends.

Indices : Zariski for robustness.

Timeframes :

Scalping : Étale for precision.

Swing Trading : Nisnevich or Zariski for reliability.

Pro Tip : Start with Étale for precision; switch to Zariski in noisy markets.

Unified Field Configuration Inputs

⚛️ Field Coupling Constant :

What It Is : Sets the interaction strength between geometric components.

How It Works : Controls signal amplification in the unified field equation.

Optimization :

Higher Values (0.5-1.0) : Strong coupling, amplified signals for ranging markets.

Lower Values (0.001-0.1) : Subtle signals for trending markets.

Timeframes :

Scalping : 0.5-0.8 for quick, strong signals.

Swing Trading : 0.1-0.3 for trend confirmation.

Sectors :