ChainAggLib - library for aggregation of main chain tickersLibrary "ChainAggLib"

ChainAggLib — token -> main protocol coin (chain) and top-5 exchange tickers for volume aggregation.

Library only (no plots). All helpers are pure functions and do not modify globals.

norm_sym(s)

Parameters:

s (string)

get_base_from_symbol(full_symbol)

Parameters:

full_symbol (string)

get_chain_for_token(token_symbol)

Parameters:

token_symbol (string)

get_top5_exchange_tickers_for_chain(chain_code)

Parameters:

chain_code (string)

get_top5_exchange_tickers_for_token(token_symbol)

Parameters:

token_symbol (string)

join_tickers(arr)

Parameters:

arr (array)

contains_symbol(arr, symbol)

Parameters:

arr (array)

symbol (string)

contains_current(arr)

Parameters:

arr (array)

get_arr_for_current_token()

get_chain_for_current()

Statistics

korea time with 200 korea time

start time

08

09

17

18

23

00

This script makes it easier to look at the charts

The time automatically displays even if you don't bother to bring the mouse by hand

Now you can see the time intuitively

Run a very happy trading session

India Vix based Strangle StrikesA clean Nifty–VIX dashboard that converts India VIX into expected daily moves, price ranges, and suggested strangle strikes. Includes VIX %, expanded 1.2× range, and smart rounded strike levels for options trading.

This script provides a professional on-chart dashboard that converts India VIX into actionable trading levels for Nifty. It calculates the VIX-based expected daily move, projected price ranges, expanded 1.2× ranges, and suggested strangle strike prices. Includes clean formatting, color-coded sections, and real-time updates.

Ideal for traders using straddles, strangles, intraday volatility models, range-bound setups, and options-based risk management.

1.2x expanded range is better success probability, may keep 20% of strangle value as stop loss.

The vix based system is intended to give approx. 70%+ success rate.

Custom Horizontal Lines | Trade Symmetry📊 Custom Horizontal Lines

🔍 Overview

The Custom Horizontal Lines is a precision utility designed for traders who perform manual higher-timeframe analysis and want to preserve their marked price levels directly on the chart.

It doesn’t calculate or detect anything automatically — instead, it acts as your personal level memory, preserving your analyzed zones and reference prices throughout the session.

Ideal for traders who manually mark the High, Low, Open, Close, Mean Thresholds, and Quarter Levels of Order Blocks, Fair Value Gaps, Inversion Fair Value Gaps and Wicks before the trading day begins.

⚙️ Key Features

✅ Manual Level Entry — Input your analyzed price levels (OB, FVG, WICK,etc) directly into the indicator settings.

✅ Preserved Levels — Once entered, your lines stay visible and consistent — even after switching symbols, timeframes, or reloading the chart.

✅ Supports All Level Types — Store any kind of manually defined level: OB highs/lows, FVG boundaries, Wicks, Mean Thresholds, Quarter levels, or custom reference prices.

✅ Clean Visualization — Customize line color, style, and labels for easy visual organization.

✅ Session-Ready Workflow — Built for pre-market preparation — enter your HTF levels once, and trade around them all day.

✅ No Auto Calculations — 100% manual by design — ensuring only your analyzed levels are shown, exactly as you defined them.

💡 How to Use

Open the indicator’s settings and manually enter those price values.

The indicator will plot and preserve those exact levels on your chart.

Switch to your lower timeframe and observe how price reacts around them — without ever needing to redraw.

🎯 Why It’s Useful

Keeps your HTF levels organized and persistent across sessions.

Saves time by avoiding redrawing.

Fits perfectly into ICT / Smart Money trading workflows.

Ensures full manual control and precision over what’s displayed on your chart.

🧩 Ideal For

ICT and Smart Money traders

Institutional-style manual analysts

Traders marking Mean Thresholds, or Quarter Levels of OBs, FVGs, Wicks etc

Anyone who wants a clean, reliable way to preserve their manual analysis

LibVPrfLibrary "LibVPrf"

This library provides an object-oriented framework for volume

profile analysis in Pine Script®. It is built around the `VProf`

User-Defined Type (UDT), which encapsulates all data, settings,

and statistical metrics for a single profile, enabling stateful

analysis with on-demand calculations.

Key Features:

1. **Object-Oriented Design (UDT):** The library is built around

the `VProf` UDT. This object encapsulates all profile data

and provides methods for its full lifecycle management,

including creation, cloning, clearing, and merging of profiles.

2. **Volume Allocation (`AllotMode`):** Offers two methods for

allocating a bar's volume:

- **Classic:** Assigns the entire bar's volume to the close

price bucket.

- **PDF:** Distributes volume across the bar's range using a

statistical price distribution model from the `LibBrSt` library.

3. **Buy/Sell Volume Splitting (`SplitMode`):** Provides methods

for classifying volume into buying and selling pressure:

- **Classic:** Classifies volume based on the bar's color (Close vs. Open).

- **Dynamic:** A specific model that analyzes candle structure

(body vs. wicks) and a short-term trend factor to

estimate the buy/sell share at each price level.

4. **Statistical Analysis (On-Demand):** Offers a suite of

statistical metrics calculated using a "Lazy Evaluation"

pattern (computed only when requested via `get...` methods):

- **Central Tendency:** Point of Control (POC), VWAP, and Median.

- **Dispersion:** Value Area (VA) and Population Standard Deviation.

- **Shape:** Skewness and Excess Kurtosis.

- **Delta:** Cumulative Volume Delta, including its

historical high/low watermarks.

5. **Structural Analysis:** Includes a parameter-free method

(`getSegments`) to decompose a profile into its fundamental

unimodal segments, allowing for modality detection (e.g.,

identifying bimodal profiles).

6. **Dynamic Profile Management:**

- **Auto-Fitting:** Profiles set to `dynamic = true` will

automatically expand their price range to fit new data.

- **Manipulation:** The resolution, price range, and Value Area

of a dynamic profile can be changed at any time. This

triggers a resampling process that uses a **linear

interpolation model** to re-bucket existing volume.

- **Assumption:** Non-dynamic profiles are fixed and will throw

a `runtime.error` if `addBar` is called with data

outside their initial range.

7. **Bucket-Level Access:** Provides getter methods for direct

iteration and analysis of the raw buy/sell volume and price

boundaries of each individual price bucket.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

create(buckets, rangeUp, rangeLo, dynamic, valueArea, allot, estimator, cdfSteps, split, trendLen)

Construct a new `VProf` object with fixed bucket count & range.

Parameters:

buckets (int) : series int number of price buckets ≥ 1

rangeUp (float) : series float upper price bound (absolute)

rangeLo (float) : series float lower price bound (absolute)

dynamic (bool) : series bool Flag for dynamic adaption of profile ranges

valueArea (int) : series int Percentage of total volume to include in the Value Area (1..100)

allot (series AllotMode) : series AllotMode Allocation mode `classic` or `pdf` (default `classic`)

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : series LibBrSt.PriceEst PDF model when `model == PDF`. (deflault = 'uniform')

cdfSteps (int) : series int even #sub-intervals for Simpson rule (default 20)

split (series SplitMode) : series SplitMode Buy/Sell determination (default `classic`)

trendLen (int) : series int Look‑back bars for trend factor (default 3)

Returns: VProf freshly initialised profile

method clone(self)

Create a deep copy of the volume profile.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object to copy

Returns: VProf A new, independent copy of the profile

method clear(self)

Reset all bucket tallies while keeping configuration intact.

Namespace types: VProf

Parameters:

self (VProf) : VProf profile object

Returns: VProf cleared profile (chaining)

method merge(self, srcABuy, srcASell, srcRangeUp, srcRangeLo, srcCvd, srcCvdHi, srcCvdLo)

Merges volume data from a source profile into the current profile.

If resizing is needed, it performs a high-fidelity re-bucketing of existing

volume using a linear interpolation model inferred from neighboring buckets,

preventing aliasing artifacts and ensuring accurate volume preservation.

Namespace types: VProf

Parameters:

self (VProf) : VProf The target profile object to merge into.

srcABuy (array) : array The source profile's buy volume bucket array.

srcASell (array) : array The source profile's sell volume bucket array.

srcRangeUp (float) : series float The upper price bound of the source profile.

srcRangeLo (float) : series float The lower price bound of the source profile.

srcCvd (float) : series float The final Cumulative Volume Delta (CVD) value of the source profile.

srcCvdHi (float) : series float The historical high-water mark of the CVD from the source profile.

srcCvdLo (float) : series float The historical low-water mark of the CVD from the source profile.

Returns: VProf `self` (chaining), now containing the merged data.

method addBar(self, offset)

Add current bar’s volume to the profile (call once per realtime bar).

classic mode: allocates all volume to the close bucket and classifies

by `close >= open`. PDF mode: distributes volume across buckets by the

estimator’s CDF mass. For `split = dynamic`, the buy/sell share per

price is computed via context-driven piecewise s(u).

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

offset (int) : series int To offset the calculated bar

Returns: VProf `self` (method chaining)

method setBuckets(self, buckets)

Sets the number of buckets for the volume profile.

Behavior depends on the `isDynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-bucketing to a new resolution.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

buckets (int) : series int The new number of buckets

Returns: VProf `self` (chaining)

method setRanges(self, rangeUp, rangeLo)

Sets the price range for the volume profile.

Behavior depends on the `dynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-bucketing existing volume.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

rangeUp (float) : series float The new upper price bound

rangeLo (float) : series float The new lower price bound

Returns: VProf `self` (chaining)

method setValueArea(self, valueArea)

Set the percentage of volume for the Value Area. If the value

changes, the profile is finalized again.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

valueArea (int) : series int The new Value Area percentage (0..100)

Returns: VProf `self` (chaining)

method getBktBuyVol(self, idx)

Get Buy volume of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns: series float Buy volume ≥ 0

method getBktSellVol(self, idx)

Get Sell volume of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns: series float Sell volume ≥ 0

method getBktBnds(self, idx)

Get Bounds of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns:

up series float The upper price bound of the bucket.

lo series float The lower price bound of the bucket.

method getPoc(self)

Get POC information.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

Returns:

pocIndex series int The index of the Point of Control (POC) bucket.

pocPrice. series float The mid-price of the Point of Control (POC) bucket.

method getVA(self)

Get Value Area (VA) information.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

Returns:

vaUpIndex series int The index of the upper bound bucket of the Value Area.

vaUpPrice series float The upper price bound of the Value Area.

vaLoIndex series int The index of the lower bound bucket of the Value Area.

vaLoPrice series float The lower price bound of the Value Area.

method getMedian(self)

Get the profile's median price and its bucket index. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

medianIndex series int The index of the bucket containing the Median.

medianPrice series float The Median price of the profile.

method getVwap(self)

Get the profile's VWAP and its bucket index. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

vwapIndex series int The index of the bucket containing the VWAP.

vwapPrice series float The Volume Weighted Average Price of the profile.

method getStdDev(self)

Get the profile's volume-weighted standard deviation. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Standard deviation of the profile.

method getSkewness(self)

Get the profile's skewness. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Skewness of the profile.

method getKurtosis(self)

Get the profile's excess kurtosis. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Kurtosis of the profile.

method getSegments(self)

Get the profile's fundamental unimodal segments. Calculates on-demand if stale.

Uses a parameter-free, pivot-based recursive algorithm.

Namespace types: VProf

Parameters:

self (VProf) : VProf The profile object.

Returns: matrix A 2-column matrix where each row is an pair.

method getCvd(self)

Cumulative Volume Delta (CVD) like metric over all buckets.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

cvd series float The final Cumulative Volume Delta (Total Buy Vol - Total Sell Vol).

cvdHi series float The running high-water mark of the CVD as volume was added.

cvdLo series float The running low-water mark of the CVD as volume was added.

VProf

VProf Bucketed Buy/Sell volume profile plus meta information.

Fields:

buckets (series int) : int Number of price buckets (granularity ≥1)

rangeUp (series float) : float Upper price range (absolute)

rangeLo (series float) : float Lower price range (absolute)

dynamic (series bool) : bool Flag for dynamic adaption of profile ranges

valueArea (series int) : int Percentage of total volume to include in the Value Area (1..100)

allot (series AllotMode) : AllotMode Allocation mode `classic` or `pdf`

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : LibBrSt.PriceEst Price density model when `model == PDF`

cdfSteps (series int) : int Simpson integration resolution (even ≥2)

split (series SplitMode) : SplitMode Buy/Sell split strategy per bar

trendLen (series int) : int Look‑back length for trend factor (≥1)

maxBkt (series int) : int User-defined number of buckets (unclamped)

aBuy (array) : array Buy volume per bucket

aSell (array) : array Sell volume per bucket

cvd (series float) : float Final Cumulative Volume Delta (Total Buy Vol - Total Sell Vol).

cvdHi (series float) : float Running high-water mark of the CVD as volume was added.

cvdLo (series float) : float Running low-water mark of the CVD as volume was added.

poc (series int) : int Index of max‑volume bucket (POC). Is `na` until calculated.

vaUp (series int) : int Index of upper Value‑Area bound. Is `na` until calculated.

vaLo (series int) : int Index of lower value‑Area bound. Is `na` until calculated.

median (series float) : float Median price of the volume distribution. Is `na` until calculated.

vwap (series float) : float Profile VWAP (Volume Weighted Average Price). Is `na` until calculated.

stdDev (series float) : float Standard Deviation of volume around the VWAP. Is `na` until calculated.

skewness (series float) : float Skewness of the volume distribution. Is `na` until calculated.

kurtosis (series float) : float Excess Kurtosis of the volume distribution. Is `na` until calculated.

segments (matrix) : matrix A 2-column matrix where each row is an pair. Is `na` until calculated.

LibBrStLibrary "LibBrSt"

This is a library for quantitative analysis, designed to estimate

the statistical properties of price movements *within* a single

OHLC bar, without requiring access to tick data. It provides a

suite of estimators based on various statistical and econometric

models, allowing for analysis of intra-bar volatility and

price distribution.

Key Capabilities:

1. **Price Distribution Models (`PriceEst`):** Provides a selection

of estimators that model intra-bar price action as a probability

distribution over the range. This allows for the

calculation of the intra-bar mean (`priceMean`) and standard

deviation (`priceStdDev`) in absolute price units. Models include:

- **Symmetric Models:** `uniform`, `triangular`, `arcsine`,

`betaSym`, and `t4Sym` (Student-t with fat tails).

- **Skewed Models:** `betaSkew` and `t4Skew`, which adjust

their shape based on the Open/Close position.

- **Model Assumptions:** The skewed models rely on specific

internal constants. `betaSkew` uses a fixed concentration

parameter (`BETA_SKEW_CONCENTRATION = 4.0`), and `t4Sym`/`t4Skew`

use a heuristic scaling factor (`T4_SHAPE_FACTOR`)

to map the distribution.

2. **Econometric Log-Return Estimators (`LogEst`):** Includes a set of

econometric estimators for calculating the volatility (`logStdDev`)

and drift (`logMean`) of logarithmic returns within a single bar.

These are unit-less measures. Models include:

- **Parkinson (1980):** A High-Low range estimator.

- **Garman-Klass (1980):** An OHLC-based estimator.

- **Rogers-Satchell (1991):** An OHLC estimator that accounts

for non-zero drift.

3. **Distribution Analysis (PDF/CDF):** Provides functions to work

with the Probability Density Function (`pricePdf`) and

Cumulative Distribution Function (`priceCdf`) of the

chosen price model.

- **Note on `priceCdf`:** This function uses analytical (exact)

calculations for the `uniform`, `triangular`, and `arcsine`

models. For all other models (e.g., `betaSkew`, `t4Skew`),

it uses **numerical integration (Simpson's rule)** as

an approximation of the cumulative probability.

4. **Mathematical Functions:** The library's Beta distribution

models (`betaSym`, `betaSkew`) are supported by an internal

implementation of the natural log-gamma function, which is

based on the Lanczos approximation.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

priceStdDev(estimator, offset)

Estimates **σ̂** (standard deviation) *in price units* for the current

bar, according to the chosen `PriceEst` distribution assumption.

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float σ̂ ≥ 0 ; `na` if undefined (e.g. zero range).

priceMean(estimator, offset)

Estimates **μ̂** (mean price) for the chosen `PriceEst` within the

current bar.

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float μ̂ in price units.

pricePdf(estimator, price, offset)

Probability-density under the chosen `PriceEst` model.

**Returns 0** when `p` is outside the current bar’s .

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

price (float) : series float Price level to evaluate.

offset (int) : series int To offset the calculated bar

Returns: series float Density value.

priceCdf(estimator, upper, lower, steps, offset)

Cumulative probability **between** `upper` and `lower` under

the chosen `PriceEst` model. Outside-bar regions contribute zero.

Uses a fast, analytical calculation for Uniform, Triangular, and

Arcsine distributions, and defaults to numerical integration

(Simpson's rule) for more complex models.

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

upper (float) : series float Upper Integration Boundary.

lower (float) : series float Lower Integration Boundary.

steps (int) : series int # of sub-intervals for numerical integration (if used).

offset (int) : series int To offset the calculated bar.

Returns: series float Probability mass ∈ .

logStdDev(estimator, offset)

Estimates **σ̂** (standard deviation) of *log-returns* for the current bar.

Parameters:

estimator (series LogEst) : series LogEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float σ̂ (unit-less); `na` if undefined.

logMean(estimator, offset)

Estimates μ̂ (mean log-return / drift) for the chosen `LogEst`.

The returned value is consistent with the assumptions of the

selected volatility estimator.

Parameters:

estimator (series LogEst) : series LogEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float μ̂ (unit-less log-return).

Scientific Correlation Testing FrameworkScientific Correlation Testing Framework - Comprehensive Guide

Introduction to Correlation Analysis

What is Correlation?

Correlation is a statistical measure that describes the degree to which two assets move in relation to each other. Think of it like measuring how closely two dancers move together on a dance floor.

Perfect Positive Correlation (+1.0): Both dancers move in perfect sync, same direction, same speed

Perfect Negative Correlation (-1.0): Both dancers move in perfect sync but in opposite directions

Zero Correlation (0): The dancers move completely independently of each other

In financial markets, correlation helps us understand relationships between different assets, which is crucial for:

Portfolio diversification

Risk management

Pairs trading strategies

Hedging positions

Market analysis

Why This Script is Special

This script goes beyond simple correlation calculations by providing:

Two different correlation methods (Pearson and Spearman)

Statistical significance testing to ensure results are meaningful

Rolling correlation analysis to track how relationships change over time

Visual representation for easy interpretation

Comprehensive statistics table with detailed metrics

Deep Dive into the Script's Components

1. Input Parameters Explained-

Symbol Selection:

This allows you to select the second asset to compare with the chart's primary asset

Default is Apple (NASDAQ:AAPL), but you can change this to any symbol

Example: If you're viewing a Bitcoin chart, you might set this to "NASDAQ:TSLA" to see if Bitcoin and Tesla are correlated

Correlation Window (60): This is the number of periods used to calculate the main correlation

Larger values (e.g., 100-500) provide more stable, long-term correlation measures

Smaller values (e.g., 10-50) are more responsive to recent price movements

60 is a good balance for most daily charts (about 3 months of trading days)

Rolling Correlation Window (20): A shorter window to detect recent changes in correlation

This helps identify when the relationship between assets is strengthening or weakening

Default of 20 is roughly one month of trading days

Return Type: This determines how price changes are calculated

Simple Returns: (Today's Price - Yesterday's Price) / Yesterday's Price

Easy to understand: "The asset went up 2% today"

Log Returns: Natural logarithm of (Today's Price / Yesterday's Price)

More mathematically elegant for statistical analysis

Better for time-additive properties (returns over multiple periods)

Less sensitive to extreme values.

Confidence Level (95%): This determines how certain we want to be about our results

95% confidence means we accept a 5% chance of being wrong (false positive)

Higher confidence (e.g., 99%) makes the test more strict

Lower confidence (e.g., 90%) makes the test more lenient

95% is the standard in most scientific research

Show Statistical Significance: When enabled, the script will test if the correlation is statistically significant or just due to random chance.

Display options control what you see on the chart:

Show Pearson/Spearman/Rolling Correlation: Toggle each correlation type on/off

Show Scatter Plot: Displays a scatter plot of returns (limited to recent points to avoid performance issues)

Show Statistical Tests: Enables the detailed statistics table

Table Text Size: Adjusts the size of text in the statistics table

2.Functions explained-

calcReturns():

This function calculates price returns based on your selected method:

Log Returns:

Formula: ln(Price_t / Price_t-1)

Example: If a stock goes from $100 to $101, the log return is ln(101/100) = ln(1.01) ≈ 0.00995 or 0.995%

Benefits: More symmetric, time-additive, and better for statistical modeling

Simple Returns:

Formula: (Price_t - Price_t-1) / Price_t-1

Example: If a stock goes from $100 to $101, the simple return is (101-100)/100 = 0.01 or 1%

Benefits: More intuitive and easier to understand

rankArray():

This function calculates the rank of each value in an array, which is used for Spearman correlation:

How ranking works:

The smallest value gets rank 1

The second smallest gets rank 2, and so on

For ties (equal values), they get the average of their ranks

Example: For values

Sorted:

Ranks: (the two 2s tie for ranks 1 and 2, so they both get 1.5)

Why this matters: Spearman correlation uses ranks instead of actual values, making it less sensitive to outliers and non-linear relationships.

pearsonCorr():

This function calculates the Pearson correlation coefficient:

Mathematical Formula:

r = (nΣxy - ΣxΣy) / √

Where x and y are the two variables, and n is the sample size

What it measures:

The strength and direction of the linear relationship between two variables

Values range from -1 (perfect negative linear relationship) to +1 (perfect positive linear relationship)

0 indicates no linear relationship

Example:

If two stocks have a Pearson correlation of 0.8, they have a strong positive linear relationship

When one stock goes up, the other tends to go up in a fairly consistent proportion

spearmanCorr():

This function calculates the Spearman rank correlation:

How it works:

Convert each value in both datasets to its rank

Calculate the Pearson correlation on the ranks instead of the original values

What it measures:

The strength and direction of the monotonic relationship between two variables

A monotonic relationship is one where as one variable increases, the other either consistently increases or decreases

It doesn't require the relationship to be linear

When to use it instead of Pearson:

When the relationship is monotonic but not linear

When there are significant outliers in the data

When the data is ordinal (ranked) rather than interval/ratio

Example:

If two stocks have a Spearman correlation of 0.7, they have a strong positive monotonic relationship

When one stock goes up, the other tends to go up, but not necessarily in a straight-line relationship

tStatistic():

This function calculates the t-statistic for correlation:

Mathematical Formula: t = r × √((n-2)/(1-r²))

Where r is the correlation coefficient and n is the sample size

What it measures:

How many standard errors the correlation is away from zero

Used to test the null hypothesis that the true correlation is zero

Interpretation:

Larger absolute t-values indicate stronger evidence against the null hypothesis

Generally, a t-value greater than 2 (in absolute terms) is considered statistically significant at the 95% confidence level

criticalT() and pValue():

These functions provide approximations for statistical significance testing:

criticalT():

Returns the critical t-value for a given degrees of freedom (df) and significance level

The critical value is the threshold that the t-statistic must exceed to be considered statistically significant

Uses approximations since Pine Script doesn't have built-in statistical distribution functions

pValue():

Estimates the p-value for a given t-statistic and degrees of freedom

The p-value is the probability of observing a correlation as strong as the one calculated, assuming the true correlation is zero

Smaller p-values indicate stronger evidence against the null hypothesis

Standard interpretation:

p < 0.01: Very strong evidence (marked with **)

p < 0.05: Strong evidence (marked with *)

p ≥ 0.05: Weak evidence, not statistically significant

stdev():

This function calculates the standard deviation of a dataset:

Mathematical Formula: σ = √(Σ(x-μ)²/(n-1))

Where x is each value, μ is the mean, and n is the sample size

What it measures:

The amount of variation or dispersion in a set of values

A low standard deviation indicates that the values tend to be close to the mean

A high standard deviation indicates that the values are spread out over a wider range

Why it matters for correlation:

Standard deviation is used in calculating the correlation coefficient

It also provides information about the volatility of each asset's returns

Comparing standard deviations helps understand the relative riskiness of the two assets.

3.Getting Price Data-

price1: The closing price of the primary asset (the chart you're viewing)

price2: The closing price of the secondary asset (the one you selected in the input parameters)

Returns are used instead of raw prices because:

Returns are typically stationary (mean and variance stay constant over time)

Returns normalize for price levels, allowing comparison between assets of different values

Returns represent what investors actually care about: percentage changes in value

4.Information Table-

Creates a table to display statistics

Only shows on the last bar to avoid performance issues

Positioned in the top right of the chart

Has 2 columns and 15 rows

Populating the Table

The script then populates the table with various statistics:

Header Row: "Metric" and "Value"

Sample Information: Sample size and return type

Pearson Correlation: Value, t-statistic, p-value, and significance

Spearman Correlation: Value, t-statistic, p-value, and significance

Rolling Correlation: Current value

Standard Deviations: For both assets

Interpretation: Text description of the correlation strength

The table uses color coding to highlight important information:

Green for significant positive results

Red for significant negative results

Yellow for borderline significance

Color-coded headers for each section

=> Practical Applications and Interpretation

How to Interpret the Results

Correlation Strength

0.0 to 0.3 (or 0.0 to -0.3): Weak or no correlation

The assets move mostly independently of each other

Good for diversification purposes

0.3 to 0.7 (or -0.3 to -0.7): Moderate correlation

The assets show some tendency to move together (or in opposite directions)

May be useful for certain trading strategies but not extremely reliable

0.7 to 1.0 (or -0.7 to -1.0): Strong correlation

The assets show a strong tendency to move together (or in opposite directions)

Can be useful for pairs trading, hedging, or as a market indicator

Statistical Significance

p < 0.01: Very strong evidence that the correlation is real

Marked with ** in the table

Very unlikely to be due to random chance

p < 0.05: Strong evidence that the correlation is real

Marked with * in the table

Unlikely to be due to random chance

p ≥ 0.05: Weak evidence that the correlation is real

Not marked in the table

Could easily be due to random chance

Rolling Correlation

The rolling correlation shows how the relationship between assets changes over time

If the rolling correlation is much different from the long-term correlation, it suggests the relationship is changing

This can indicate:

A shift in market regime

Changing fundamentals of one or both assets

Temporary market dislocations that might present trading opportunities

Trading Applications

1. Portfolio Diversification

Goal: Reduce overall portfolio risk by combining assets that don't move together

Strategy: Look for assets with low or negative correlations

Example: If you hold tech stocks, you might add some utilities or bonds that have low correlation with tech

2. Pairs Trading

Goal: Profit from the relative price movements of two correlated assets

Strategy:

Find two assets with strong historical correlation

When their prices diverge (one goes up while the other goes down)

Buy the underperforming asset and short the outperforming asset

Close the positions when they converge back to their normal relationship

Example: If Coca-Cola and Pepsi are highly correlated but Coca-Cola drops while Pepsi rises, you might buy Coca-Cola and short Pepsi

3. Hedging

Goal: Reduce risk by taking an offsetting position in a negatively correlated asset

Strategy: Find assets that tend to move in opposite directions

Example: If you hold a portfolio of stocks, you might buy some gold or government bonds that tend to rise when stocks fall

4. Market Analysis

Goal: Understand market dynamics and interrelationships

Strategy: Analyze correlations between different sectors or asset classes

Example:

If tech stocks and semiconductor stocks are highly correlated, movements in one might predict movements in the other

If the correlation between stocks and bonds changes, it might signal a shift in market expectations

5. Risk Management

Goal: Understand and manage portfolio risk

Strategy: Monitor correlations to identify when diversification benefits might be breaking down

Example: During market crises, many assets that normally have low correlations can become highly correlated (correlation convergence), reducing diversification benefits

Advanced Interpretation and Caveats

Correlation vs. Causation

Important Note: Correlation does not imply causation

Example: Ice cream sales and drowning incidents are correlated (both increase in summer), but one doesn't cause the other

Implication: Just because two assets move together doesn't mean one causes the other to move

Solution: Look for fundamental economic reasons why assets might be correlated

Non-Stationary Correlations

Problem: Correlations between assets can change over time

Causes:

Changing market conditions

Shifts in monetary policy

Structural changes in the economy

Changes in the underlying businesses

Solution: Use rolling correlations to monitor how relationships change over time

Outliers and Extreme Events

Problem: Extreme market events can distort correlation measurements

Example: During a market crash, many assets may move in the same direction regardless of their normal relationship

Solution:

Use Spearman correlation, which is less sensitive to outliers

Be cautious when interpreting correlations during extreme market conditions

Sample Size Considerations

Problem: Small sample sizes can produce unreliable correlation estimates

Rule of Thumb: Use at least 30 data points for a rough estimate, 60+ for more reliable results

Solution:

Use the default correlation length of 60 or higher

Be skeptical of correlations calculated with small samples

Timeframe Considerations

Problem: Correlations can vary across different timeframes

Example: Two assets might be positively correlated on a daily basis but negatively correlated on a weekly basis

Solution:

Test correlations on multiple timeframes

Use the timeframe that matches your trading horizon

Look-Ahead Bias

Problem: Using information that wouldn't have been available at the time of trading

Example: Calculating correlation using future data

Solution: This script avoids look-ahead bias by using only historical data

Best Practices for Using This Script

1. Appropriate Parameter Selection

Correlation Window:

For short-term trading: 20-50 periods

For medium-term analysis: 50-100 periods

For long-term analysis: 100-500 periods

Rolling Window:

Should be shorter than the main correlation window

Typically 1/3 to 1/2 of the main window

Return Type:

For most applications: Log Returns (better statistical properties)

For simplicity: Simple Returns (easier to interpret)

2. Validation and Testing

Out-of-Sample Testing:

Calculate correlations on one time period

Test if they hold in a different time period

Multiple Timeframes:

Check if correlations are consistent across different timeframes

Economic Rationale:

Ensure there's a logical reason why assets should be correlated

3. Monitoring and Maintenance

Regular Review:

Correlations can change, so review them regularly

Alerts:

Set up alerts for significant correlation changes

Documentation:

Keep notes on why certain assets are correlated and what might change that relationship

4. Integration with Other Analysis

Fundamental Analysis:

Combine correlation analysis with fundamental factors

Technical Analysis:

Use correlation analysis alongside technical indicators

Market Context:

Consider how market conditions might affect correlations

Conclusion

This Scientific Correlation Testing Framework provides a comprehensive tool for analyzing relationships between financial assets. By offering both Pearson and Spearman correlation methods, statistical significance testing, and rolling correlation analysis, it goes beyond simple correlation measures to provide deeper insights.

For beginners, this script might seem complex, but it's built on fundamental statistical concepts that become clearer with use. Start with the default settings and focus on interpreting the main correlation lines and the statistics table. As you become more comfortable, you can adjust the parameters and explore more advanced applications.

Remember that correlation analysis is just one tool in a trader's toolkit. It should be used in conjunction with other forms of analysis and with a clear understanding of its limitations. When used properly, it can provide valuable insights for portfolio construction, risk management, and pair trading strategy development.

LibWghtLibrary "LibWght"

This is a library of mathematical and statistical functions

designed for quantitative analysis in Pine Script. Its core

principle is the integration of a custom weighting series

(e.g., volume) into a wide array of standard technical

analysis calculations.

Key Capabilities:

1. **Universal Weighting:** All exported functions accept a `weight`

parameter. This allows standard calculations (like moving

averages, RSI, and standard deviation) to be influenced by an

external data series, such as volume or tick count.

2. **Weighted Averages and Indicators:** Includes a comprehensive

collection of weighted functions:

- **Moving Averages:** `wSma`, `wEma`, `wWma`, `wRma` (Wilder's),

`wHma` (Hull), and `wLSma` (Least Squares / Linear Regression).

- **Oscillators & Ranges:** `wRsi`, `wAtr` (Average True Range),

`wTr` (True Range), and `wR` (High-Low Range).

3. **Volatility Decomposition:** Provides functions to decompose

total variance into distinct components for market analysis.

- **Two-Way Decomposition (`wTotVar`):** Separates variance into

**between-bar** (directional) and **within-bar** (noise)

components.

- **Three-Way Decomposition (`wLRTotVar`):** Decomposes variance

relative to a linear regression into **Trend** (explained by

the LR slope), **Residual** (mean-reversion around the

LR line), and **Within-Bar** (noise) components.

- **Local Volatility (`wLRLocTotStdDev`):** Measures the total

"noise" (within-bar + residual) around the trend line.

4. **Weighted Statistics and Regression:** Provides a robust

function for Weighted Linear Regression (`wLinReg`) and a

full suite of related statistical measures:

- **Between-Bar Stats:** `wBtwVar`, `wBtwStdDev`, `wBtwStdErr`.

- **Residual Stats:** `wResVar`, `wResStdDev`, `wResStdErr`.

5. **Fallback Mechanism:** All functions are designed for reliability.

If the total weight over the lookback period is zero (e.g., in

a no-volume period), the algorithms automatically fall back to

their unweighted, uniform-weight equivalents (e.g., `wSma`

becomes a standard `ta.sma`), preventing errors and ensuring

continuous calculation.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

wSma(source, weight, length)

Weighted Simple Moving Average (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

the arithmetic mean if Σweight = 0.

wEma(source, weight, length)

Weighted EMA (exponential kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Exponential-kernel weighted mean; falls

back to classic EMA if Σweight = 0.

wWma(source, weight, length)

Weighted WMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic WMA if Σweight = 0.

wRma(source, weight, length)

Weighted RMA (Wilder kernel, α = 1/len).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Wilder-kernel weighted mean; falls back to

classic RMA if Σweight = 0.

wHma(source, weight, length)

Weighted HMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic HMA if Σweight = 0.

wRsi(source, weight, length)

Weighted Relative Strength Index.

Parameters:

source (float) : series float Price series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted RSI; uniform if Σw = 0.

wAtr(tr, weight, length)

Weighted ATR (Average True Range).

Implemented as WRMA on *true range*.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted ATR; uniform weights if Σw = 0.

wTr(tr, weight, length)

Weighted True Range over a window.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of TR; uniform if Σw = 0.

wR(r, weight, length)

Weighted High-Low Range over a window.

Parameters:

r (float) : series float High-Low per bar.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of range; uniform if Σw = 0.

wBtwVar(source, weight, length, biased)

Weighted Between Variance (biased/unbiased).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

variance series float The calculated between-bar variance (σ²btw), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wBtwStdDev(source, weight, length, biased)

Weighted Between Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σbtw uniform if Σw = 0.

wBtwStdErr(source, weight, length, biased)

Weighted Between Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²btw / N_eff) uniform if Σw = 0.

wTotVar(mu, sigma, weight, length, biased)

Weighted Total Variance (= between-group + within-group).

Useful when each bar represents an aggregate with its own

mean* and pre-estimated σ (e.g., second-level ranges inside a

1-minute bar). Assumes the *weight* series applies to both the

group means and their σ estimates.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

varBtw series float The between-bar variance component (σ²btw).

varWtn series float The within-bar variance component (σ²wtn).

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wTotStdDev(mu, sigma, weight, length, biased)

Weighted Total Standard Deviation.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σtot.

wTotStdErr(mu, sigma, weight, length, biased)

Weighted Total Standard Error.

SE = √( total variance / N_eff ) with the same effective sample

size logic as `wster()`.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²tot / N_eff).

wLinReg(source, weight, length)

Weighted Linear Regression.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

Returns:

mid series float The estimated value of the regression line at the most recent bar.

slope series float The slope of the regression line.

intercept series float The intercept of the regression line.

wResVar(source, weight, midLine, slope, length, biased)

Weighted Residual Variance.

linear regression – optionally biased (population) or

unbiased (sample).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weighting series (volume, etc.).

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population variance (σ²_P), denominator ≈ N_eff.

false → sample variance (σ²_S), denominator ≈ N_eff - 2.

(Adjusts for 2 degrees of freedom lost to the regression).

Returns:

variance series float The calculated residual variance (σ²res), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wResStdDev(source, weight, midLine, slope, length, biased)

Weighted Residual Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σres; uniform if Σw = 0.

wResStdErr(source, weight, midLine, slope, length, biased)

Weighted Residual Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²res / N_eff); uniform if Σw = 0.

wLRTotVar(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Variance **around the

window’s weighted mean μ**.

σ²_tot = E_w ⟶ *within-group variance*

+ Var_w ⟶ *residual variance*

+ Var_w ⟶ *trend variance*

where each bar i in the look-back window contributes

m_i = *mean* (e.g. 1-sec HL2)

σ_i = *sigma* (pre-estimated intrabar σ)

w_i = *weight* (volume, ticks, …)

ŷ_i = b₀ + b₁·x (value of the weighted LR line)

r_i = m_i − ŷ_i (orthogonal residual)

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns:

varRes series float The residual variance component (σ²res).

varWtn series float The within-bar variance component (σ²wtn).

varTrd series float The trend variance component (σ²trd), explained by the linear regression.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wLRTotStdDev(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Standard Deviation.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √(σ²tot).

wLRTotStdErr(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Standard Error.

SE = √( σ²_tot / N_eff ) with N_eff = Σw² / Σw² (like in wster()).

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √((σ²res, σ²wtn, σ²trd) / N_eff).

wLRLocTotStdDev(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Local Total Standard Deviation.

Measures the total "noise" (within-bar + residual) around the trend.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √(σ²wtn + σ²res).

wLRLocTotStdErr(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Local Total Standard Error.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √((σ²wtn + σ²res) / N_eff).

wLSma(source, weight, length)

Weighted Least Square Moving Average.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

Returns: series float Least square weighted mean. Falls back

to unweighted regression if Σw = 0.

Central Limit Theorem Reversion IndicatorDear TV community, let me introduce you to the first-ever Central Limit Theorem indicator on TradingView.

The Central Limit Theorem is used in statistics and it can be quite useful in quant trading and understanding market behaviors.

In short, the CLT states: "When you take repeated samples from any population and calculate their averages, those averages will form a normal (bell curve) distribution—no matter what the original data looks like."

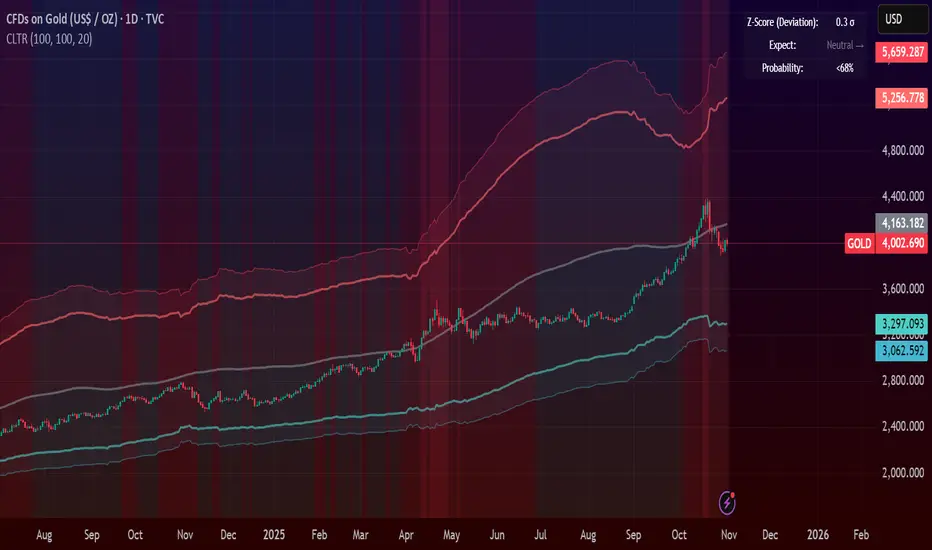

In this CLT indicator, I use statistical theory to identify high-probability mean reversion opportunities in the markets. It calculates statistical confidence bands and z-scores to identify when price movements deviate significantly from their expected distribution, signaling potential reversion opportunities with quantifiable probability levels.

Mathematical Foundation

The Central Limit Theorem (CLT) says that when you average many data points together, those averages will form a predictable bell-curve pattern, even if the original data is completely random and unpredictable (which often is in the markets). This works no matter what you're measuring, and it gets more reliable as you use more data points.

Why using it for trading?

Individual price movements seem random and chaotic, but when we look at the average of many price movements, we can actually predict how they should behave statistically. This lets us spot when prices have moved "too far" from what's normal—and those extreme moves tend to snap back (mean reversion).

Key Formula:

Z = (X̄ - μ) / (σ / √n)

Where:

- X̄ = Sample mean (average return over n periods)

- μ = Population mean (long-term expected return)

- σ = Population standard deviation (volatility)

- n = Sample size

- σ/√n = Standard error of the mean

How I Apply CLT

Step 1: Calculate Returns

Measures how much price changed from one bar to the next (using logarithms for better statistical properties)

Step 2: Average Recent Returns

Takes the average of the last n returns (e.g., last 100 bars). This is your "sample mean."

Step 3: Find What's "Normal"

Looks at historical data to determine: a) What the typical average return should be (the long-term mean) and b) How volatile the market usually is (standard deviation)

Step 4: Calculate Standard Error

Determines how much sample averages naturally vary. Larger samples = smaller expected variation.

Step 5: Calculate Z-Score

Measures how unusual the current situation is.

Step 6: Draw Confidence Bands

Converts these statistical boundaries into actual price levels on your chart, showing where price is statistically expected to stay 95% and 99% of the time.

Interpretation & Usage

The Z-Score:

The z-score tells you how statistically unusual the current price deviation is:

|Z| < 1.0 → Normal behavior, no action

|Z| = 1.0 to 1.96 → Moderate deviation, watch closely

|Z| = 1.96 to 2.58 → Significant deviation (95%+), consider entry

|Z| > 2.58 → Extreme deviation (99%+), high probability setup

The Confidence Bands

- Upper Red Bands: 95% and 99% overbought zones → Expect mean reversion downward as the price is not likely to cross these lines.

- Center Gray Line: Statistical expectation (fair value)

- Lower Blue Bands: 95% and 99% oversold zones → Expect mean reversion upward

Trading Logic:

- When price exceeds the upper 95% band (z-score > +1.96), there's only a 5% probability this is random noise → Strong sell/short signal

- When price falls below the lower 95% band (z-score < -1.96), there's a 95% statistical expectation of upward reversion → Strong buy/long signal

Background Gradient

The background color provides real-time visual feedback:

- Blue shades: Oversold conditions, expect upward reversion

- Red shades: Overbought conditions, expect downward reversion

- Intensity: Darker colors indicate stronger statistical significance

Trading Strategy Examples

Hypothetically, this is how the indicator could be used:

- Long: Z-score < -1.96 (below 95% confidence band)

- Short: Z-score > +1.96 (above 95% confidence band)

- Take profit when price returns to center line (Z ≈ 0)

Input Parameters

Sample Size (n) - Default: 100

Lookback Period (m) - Default: 100

You can also create alerts based on the indicator.

Final notes:

- The indicator uses logarithmic returns for better statistical properties

- Converts statistical bands back to price space for practical use

- Adaptive volatility: Bands automatically widen in high volatility, narrow in low volatility

- No repainting: yay! All calculations use historical data only

Feedback is more than welcome!

Henri

Stablecoin Liquidity Delta (Aggregate Market Cap Flow)Hi All,

This indicator visualizes the bar-to-bar change in the aggregate market capitalization of major stablecoins, including USDT, USDC, DAI, and others. It serves as a proxy for monitoring on-chain liquidity and measuring capital inflows or outflows across the crypto market.

Stablecoins are the primary liquidity layer of the crypto economy. Their combined market capitalization acts as a mirror of the available fiat-denominated liquidity in digital markets:

🟩 An increase in the total stablecoin market capitalization indicates new issuance (capital entering the market).

🟥 A decrease reflects redemption or burning (liquidity exiting the system).

Tracking these flows helps anticipate macro-level liquidity trends that often lead overall market direction, providing context for broader price movements.

All values are derived from TradingView’s public CRYPTOCAP tickers, which represent the market capitalization of each stablecoin. While minor deviations can occur due to small price fluctuations around the $1 peg, these figures serve as a proxy for circulating supply and net issuance across the stablecoin ecosystem.

Continuation Probability (0–100)This indicator helps measure how likely the current candle trend will continue or reverse, giving a probability score between 0–100.

It combines multiple market factors trend, candle strength, volume, and volatility to create a single, intuitive signal.

Simple FloatFloat Display Indicator

A simple, clean indicator that displays the current float (shares outstanding float) for any stock directly in your indicator status line at the top left of the chart.

Features:

- Shows the float value with automatic K/M formatting for thousands and millions

- No chart clutter - value only appears in the status line, nothing plotted on the chart

- Works on any stock that has float data available

- Lightweight and efficient

Perfect for traders who want quick access to float information without switching between windows or cluttering their charts.

Note: Float data availability depends on TradingView's financial data for the specific ticker. Some tickers may not have this data available.

Vandan V2Vandan V2 is an automated trend-following strategy for NASDAQ E-mini Futures (NQ1!).

It uses multi-timeframe momentum and volatility filters to identify high-probability entries.

Includes dynamic risk management and trailing logic optimized for intraday trading.

Risk Position Sizer (Entry=Close, Stop=Daily Low)This is for trading stocks/shares. Its main goal is to help you gauge how big or how small of a position you should add based on your account size.

Info Box⚙️ Purpose

Shows useful trade and event-related data such as:

% Distance from stop levels (D, DH)

Earnings countdown in bars

All displayed in a single floating info box (table) on the chart.

📋 Key Features

Customizable Display

Choose table position (Top Right, Bottom Center, etc.)

Choose table size (Auto, Large, Tiny, etc.)

Custom text and background colors

Metrics Shown

D: % Distance from stop (difference between close and low/high)

DH: % Distance from midpoint of the candle

Earnings Countdown: Number of bars until next earnings event

Conditional Styling

If earnings are within 3 bars, text color turns red as a warning.

Execution Conditions

Runs only on daily timeframe

Updates on last bar only (no historical clutter)

Output

Displays all selected metrics in one line, separated by “×”

e.g. → D: -2.1% × 5 × DH: 1.4%

🧩 Overall Function

Creates a clean, customizable “info box” showing trade distances and upcoming earnings countdown for quick decision-making directly on your TradingView chart.

Nqaba Goldminer StrategyThis indicator plots the New York session key timing levels used in institutional intraday models.

It automatically marks the 03:00 AM, 10:00 AM, and 2:00 PM (14:00) New York times each day:

Vertical lines show exactly when those time windows open — allowing traders to identify major global liquidity shifts between London, New York, and U.S. session overlaps.

Horizontal lines mark the opening price of the 5-minute candle that begins at each of those key times, providing precision reference levels for potential reversals, continuation setups, and intraday bias shifts.

Users can customize each line’s color, style (solid/dashed/dotted), width, and horizontal-line length.

A history toggle lets you display all past occurrences or just today’s key levels for a cleaner chart.

These reference levels form the foundation for strategies such as:

London Breakout to New York Reversal models

Opening Range / Session Open bias confirmation

Institutional volume transfer windows (London → NY → Asia)

The tool provides a simple visual structure for traders to frame intraday decision-making around recurring institutional time events.

Percentile Rank Oscillator (Price + VWMA)A statistical oscillator designed to identify potential market turning points using percentile-based price analytics and volume-weighted confirmation.

What is PRO?

Percentile Rank Oscillator measures how extreme current price behavior is relative to its own recent history. It calculates a rolling percentile rank of price midpoints and VWMA deviation (volume-weighted price drift). When price reaches historically rare levels – high or low percentiles – it may signal exhaustion and potential reversal conditions.

How it works

Takes midpoint of each candle ((H+L)/2)

Ranks the current value vs previous N bars using rolling percentile rank

Maps percentile to a normalized oscillator scale (-1..+1 or 0–100)

Optionally evaluates VWMA deviation percentile for volume-confirmed signals

Highlights extreme conditions and confluence zones

Why percentile rank?

Median-based percentiles ignore outliers and read the market statistically – not by fixed thresholds. Instead of guessing “overbought/oversold” values, the indicator adapts to current volatility and structure.

Key features

Rolling percentile rank of price action

Optional VWMA-based percentile confirmation

Adaptive, noise-robust structure

User-selectable thresholds (default 95/5)

Confluence highlighting for price + VWMA extremes

Optional smoothing (RMA)

Visual extreme zone fills for rapid signal recognition

How to use

High percentile values –> statistically extreme upward deviation (potential top)

Low percentile values –> statistically extreme downward deviation (potential bottom)

Price + VWMA confluence strengthens reversal context

Best used as part of a broader trading framework (market structure, order flow, etc.)

Tip: Look for percentile spikes at key HTF levels, after extended moves, or where liquidity sweeps occur. Strong moves into rare percentile territory may precede mean reversion.

Suggested settings

Default length: 100 bars

Thresholds: 95 / 5

Smoothing: 1–3 (optional)

Important note

This tool does not predict direction or guarantee outcomes. It provides statistical context for price extremes to help traders frame probability and timing. Always combine with sound risk management and other tools.

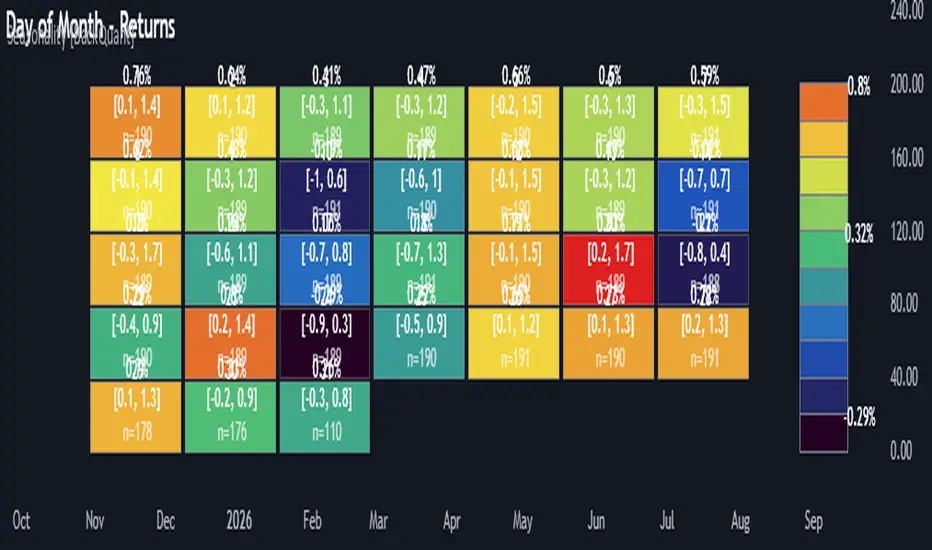

Multi-Mode Seasonality Map [BackQuant]Multi-Mode Seasonality Map

A fast, visual way to expose repeatable calendar patterns in returns, volatility, volume, and range across multiple granularities (Day of Week, Day of Month, Hour of Day, Week of Month). Built for idea generation, regime context, and execution timing.

What is “seasonality” in markets?

Seasonality refers to statistically repeatable patterns tied to the calendar or clock, rather than to price levels. Examples include specific weekdays tending to be stronger, certain hours showing higher realized volatility, or month-end flow boosting volumes. This tool measures those effects directly on your charted symbol.

Why seasonality matters

It’s orthogonal alpha: timing edges independent of price structure that can complement trend, mean reversion, or flow-based setups.

It frames expectations: when a session typically runs hot or cold, you size and pace risk accordingly.

It improves execution: entering during historically favorable windows, avoiding historically noisy windows.

It clarifies context: separating normal “calendar noise” from true anomaly helps avoid overreacting to routine moves.

How traders use seasonality in practice

Timing entries/exits : If Tuesday morning is historically weak for this asset, a mean-reversion buyer may wait for that drift to complete before entering.

Sizing & stops : If 13:00–15:00 shows elevated volatility, widen stops or reduce size to maintain constant risk.

Session playbooks : Build repeatable routines around the hours/days that consistently drive PnL.

Portfolio rotation : Compare seasonal edges across assets to schedule focus and deploy attention where the calendar favors you.

Why Day-of-Week (DOW) can be especially helpful

Flows cluster by weekday (ETF creations/redemptions, options hedging cadence, futures roll patterns, macro data releases), so DOW often encodes a stable micro-structure signal.

Desk behavior and liquidity provision differ by weekday, impacting realized range and slippage.

DOW is simple to operationalize: easy rules like “fade Monday afternoon chop” or “press Thursday trend extension” can be tested and enforced.

What this indicator does

Multi-mode heatmaps : Switch between Day of Week, Day of Month, Hour of Day, Week of Month .

Metric selection : Analyze Returns , Volatility ((high-low)/open), Volume (vs 20-bar average), or Range (vs 20-bar average).

Confidence intervals : Per cell, compute mean, standard deviation, and a z-based CI at your chosen confidence level.

Sample guards : Enforce a minimum sample size so thin data doesn’t mislead.

Readable map : Color palettes, value labels, sample size, and an optional legend for fast interpretation.

Scoreboard : Optional table highlights best/worst DOW and today’s seasonality with CI and a simple “edge” tag.

How it’s calculated (under the hood)

Per bar, compute the chosen metric (return, vol, volume %, or range %) over your lookback window.

Bucket that metric into the active calendar bin (e.g., Tuesday, the 15th, 10:00 hour, or Week-2 of month).

For each bin, accumulate sum , sum of squares , and count , then at render compute mean , std dev , and confidence interval .

Color scale normalizes to the observed min/max of eligible bins (those meeting the minimum sample size).

How to read the heatmap

Color : Greener/warmer typically implies higher mean value for the chosen metric; cooler implies lower.

Value label : The center number is the bin’s mean (e.g., average % return for Tuesdays).

Confidence bracket : Optional “ ” shows the CI for the mean, helping you gauge stability.

n = sample size : More samples = more reliability. Treat small-n bins with skepticism.

Suggested workflows

Pick the lens : Start with Analysis Type = Returns , Heatmap View = Day of Week , lookback ≈ 252 trading days . Note the best/worst weekdays and their CI width.

Sanity-check volatility : Switch to Volatility to see which bins carry the most realized range. Use that to plan stop width and trade pacing.

Check liquidity proxy : Flip to Volume , identify thin vs thick windows. Execute risk in thicker windows to reduce slippage.

Drill to intraday : Use Hour of Day to reveal opening bursts, lunchtime lulls, and closing ramps. Combine with your main strategy to schedule entries.

Calendar nuance : Inspect Week of Month and Day of Month for end-of-month, options-cycle, or data-release effects.

Codify rules : Translate stable edges into rules like “no fresh risk during bottom-quartile hours” or “scale entries during top-quartile hours.”

Parameter guidance

Analysis Period (Days) : 252 for a one-year view. Shorten (100–150) to emphasize the current regime; lengthen (500+) for long-memory effects.

Heatmap View : Start with DOW for robustness, then refine with Hour-of-Day for your execution window.

Confidence Level : 95% is standard; use 90% if you want wider coverage with fewer false “insufficient data” bins.

Min Sample Size : 10–20 helps filter noise. For Hour-of-Day on higher timeframes, consider lowering if your dataset is small.

Color Scheme : Choose a palette with good mid-tone contrast (e.g., Red-Green or Viridis) for quick thresholding.

Interpreting common patterns

Return-positive but low-vol bins : Favorable drift windows for passive adds or tight-stop trend continuation.

Return-flat but high-vol bins : Opportunity for mean reversion or breakout scalping, but manage risk accordingly.

High-volume bins : Better expected execution quality; schedule size here if slippage matters.

Wide CI : Edge is unstable or sample is thin; treat as exploratory until more data accumulates.

Best practices

Revalidate after regime shifts (new macro cycle, liquidity regime change, major exchange microstructure updates).

Use multiple lenses: DOW to find the day, then Hour-of-Day to refine the entry window.

Combine with your core setup signals; treat seasonality as a filter or weight, not a standalone trigger.

Test across assets/timeframes—edges are instrument-specific and may not transfer 1:1.

Limitations & notes

History-dependent: short histories or sparse intraday data reduce reliability.

Not causal: a hot Tuesday doesn’t guarantee future Tuesday strength; treat as probabilistic bias.

Aggregation bias: changing session hours or symbol migrations can distort older samples.