SwingTrade ADX Strategy v6This is a swing trading strategy that combines VWAP (Volume Weighted Average Price), ADX (Average Directional Index) for trend strength, and volume ratios to generate long/short entry and exit signals. It's designed for daily charts but can be adapted.

#### Key Features:

- **Entries**: Based on VWAP crossovers, rising/falling delta (price deviation from VWAP), ADX trend confirmation, and volume ratios.

- **Exits**: Dynamic exits when VWAP delta reverses after a peak.

- **Filters**: Optional toggles for VWAP signals, ADX, and volume. Backtest date range for custom periods.

- **Visuals**: VWAP line, signal shapes/labels, and an info panel showing key metrics (VWAP Delta %, ADX, Volume Ratio).

- **Alerts**: Built-in alerts for buy/sell entries and exits.

#### How to Use:

1. Apply to your chart (e.g., stocks, forex, crypto).

2. Adjust parameters in the settings (e.g., ADX threshold, volume period).

3. Enable/disable indicators as needed.

4. Backtest using the date filters and review equity curve.

**Disclaimer**: This is for educational purposes only. Past performance is not indicative of future results. Not financial advice—trade at your own risk. Backtest thoroughly and use with proper risk management.

Feedback welcome! If you find it useful, give it a like.

Strategy

Kairos BarakahTrade with precision during high-probability windows using this advanced Pine Script indicator, designed specifically for Indian Standard Time (IST). The tool identifies key reversal opportunities within a user-defined trading session, combining time-based reference levels, sequence-validated signals, and multi-factor win probability analysis for confident decision-making.

Key Features

1. Time-Based Reference Levels

Automatically sets high/low reference levels at a customizable start time (default: 19:00 IST).

Active trading window with adjustable duration (default: 135 minutes).

Clear visual reference lines for easy tracking.

2. Intelligent Signal Generation

Initial Signals:

Buy (B): Triggered when price closes above the reference high.

Sell (S): Triggered when price closes below the reference low.

Reversal Signals (R):

Valid only after an initial signal, ensuring proper sequence.

Buy Reversal: Price closes above reference high (after a Sell signal).

Sell Reversal: Price closes below reference low (after a Buy signal).

3. Multi-Dimensional Win Probability

Body Strength: Measures candle conviction (body size / total range).

Volume Confirmation: Compares current volume to 20-period average.

Trend Alignment: Uses EMA crosses (9/21) and RSI (14) for momentum.

Composite Score: Weighted blend of all factors, color-coded for quick interpretation:

🟢 >70%: High-confidence signal.

🟠 40-69%: Moderate confidence.

🔴 <40%: Weak signal.

4. Professional Visualization

Clean labels (B/S/R) at signal points.

Real-time reference table showing levels, active signal, and probabilities.

Customizable alerts for all signal types.

Why Use This Indicator?

IST-Optimized: Tailored for Indian market hours.

Rules-Based Reversals: Avoids false signals with strict sequence checks.

Data-Driven Confidence: Win probability metrics reduce guesswork.

Flexible Setup: Adjust time windows and parameters to fit your strategy.

Institutional Sessions Overlay (Asia/London/NY)Institutional Sessions Overlay is a professional TradingView indicator that visually highlights the main trading sessions (Asia, London, and New York) directly on your chart.

Customizable: Easily adjust session start and end times (including minutes) for each market.

Timezone Alignment: Shift session boxes using the timezone offset parameter so sessions match your chart’s timezone exactly.

Clear Visuals: Colored boxes and optional labels display session opens and closes for fast institutional market structure reference.

Toggle Labels: Show or hide session open/close labels with a single click for a clean or detailed look.

Intuitive UI: User-friendly grouped settings for efficient configuration.

This tool is designed for day traders, institutional traders, and anyone who wants to instantly recognize global session timing and ranges for SMC, ICT, and other session-based strategies.

How to use:

Set your chart to your local timezone.

Use the "Session timezone offset" setting if session boxes do not match actual session opens on your chart.

Adjust the hours and minutes for each session as needed.

Enable or disable labels in the “Display” settings group.

Tip: Use the overlay to spot session highs and lows, volatility windows, and institutional liquidity sweeps.

KST Strategy [Skyrexio]Overview

KST Strategy leverages Know Sure Thing (KST) indicator in conjunction with the Williams Alligator and Moving average to obtain the high probability setups. KST is used for for having the high probability to enter in the direction of a current trend when momentum is rising, Alligator is used as a short term trend filter, while Moving average approximates the long term trend and allows trades only in its direction. Also strategy has the additional optional filter on Choppiness Index which does not allow trades if market is choppy, above the user-specified threshold. Strategy has the user specified take profit and stop-loss numbers, but multiplied by Average True Range (ATR) value on the moment when trade is open. The strategy opens only long trades.

Unique Features

ATR based stop-loss and take profit. Instead of fixed take profit and stop-loss percentage strategy utilizes user chosen numbers multiplied by ATR for its calculation.

Configurable Trading Periods. Users can tailor the strategy to specific market windows, adapting to different market conditions.

Optional Choppiness Index filter. Strategy allows to choose if it will use the filter trades with Choppiness Index and set up its threshold.

Methodology

The strategy opens long trade when the following price met the conditions:

Close price is above the Alligator's jaw line

Close price is above the filtering Moving average

KST line of Know Sure Thing indicator shall cross over its signal line (details in justification of methodology)

If the Choppiness Index filter is enabled its value shall be less than user defined threshold

When the long trade is executed algorithm defines the stop-loss level as the low minus user defined number, multiplied by ATR at the trade open candle. Also it defines take profit with close price plus user defined number, multiplied by ATR at the trade open candle. While trade is in progress, if high price on any candle above the calculated take profit level or low price is below the calculated stop loss level, trade is closed.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.5, number of ATRs to calculate stop-loss level)

ATR Take Profit (by default = 3.5, number of ATRs to calculate take profit level)

Filter MA Type (by default = Least Squares MA, type of moving average which is used for filter MA)

Filter MA Length (by default = 200, length for filter MA calculation)

Enable Choppiness Index Filter (by default = true, setting to choose the optional filtering using Choppiness index)

Choppiness Index Threshold (by default = 50, Choppiness Index threshold, its value shall be below it to allow trades execution)

Choppiness Index Length (by default = 14, length used in Choppiness index calculation)

KST ROC Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #2 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #3 (by default = 20, value used in KST indicator calculation, more information in Justification of Methodology)

KST ROC Length #4 (by default = 30, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #1 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #2 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #3 (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

KST SMA Length #4 (by default = 15, value used in KST indicator calculation, more information in Justification of Methodology)

KST Signal Line Length (by default = 10, value used in KST indicator calculation, more information in Justification of Methodology)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is KST, Williams Alligator, Moving Average, ATR and Choppiness Index.

The KST (Know Sure Thing) is a momentum oscillator developed by Martin Pring. It combines multiple Rate of Change (ROC) values, smoothed over different timeframes, to identify trend direction and momentum strength. First of all, what is ROC? ROC (Rate of Change) is a momentum indicator that measures the percentage change in price between the current price and the price a set number of periods ago.

ROC = 100 * (Current Price - Price N Periods Ago) / Price N Periods Ago

In our case N is the KST ROC Length inputs from settings, here we will calculate 4 different ROCs to obtain KST value:

KST = ROC1_smooth × 1 + ROC2_smooth × 2 + ROC3_smooth × 3 + ROC4_smooth × 4

ROC1 = ROC(close, KST ROC Length #1), smoothed by KST SMA Length #1,

ROC2 = ROC(close, KST ROC Length #2), smoothed by KST SMA Length #2,

ROC3 = ROC(close, KST ROC Length #3), smoothed by KST SMA Length #3,

ROC4 = ROC(close, KST ROC Length #4), smoothed by KST SMA Length #4

Also for this indicator the signal line is calculated:

Signal = SMA(KST, KST Signal Line Length)

When the KST line rises, it indicates increasing momentum and suggests that an upward trend may be developing. Conversely, when the KST line declines, it reflects weakening momentum and a potential downward trend. A crossover of the KST line above its signal line is considered a buy signal, while a crossover below the signal line is viewed as a sell signal. If the KST stays above zero, it indicates overall bullish momentum; if it remains below zero, it points to bearish momentum. The KST indicator smooths momentum across multiple timeframes, helping to reduce noise and provide clearer signals for medium- to long-term trends.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

The next indicator is Moving Average. It has a lot of different types which can be chosen to filter trades and the Least Squares MA is used by default settings. Let's briefly explain what is it.

The Least Squares Moving Average (LSMA) — also known as Linear Regression Moving Average — is a trend-following indicator that uses the least squares method to fit a straight line to the price data over a given period, then plots the value of that line at the most recent point. It draws the best-fitting straight line through the past N prices (using linear regression), and then takes the endpoint of that line as the value of the moving average for that bar. The LSMA aims to reduce lag and highlight the current trend more accurately than traditional moving averages like SMA or EMA.

Key Features:

It reacts faster to price changes than most moving averages.

It is smoother and less noisy than short-term EMAs.

It can be used to identify trend direction, momentum, and potential reversal points.

ATR (Average True Range) is a volatility indicator that measures how much an asset typically moves during a given period. It was introduced by J. Welles Wilder and is widely used to assess market volatility, not direction.

To calculate it first of all we need to get True Range (TR), this is the greatest value among:

High - Low

abs(High - Previous Close)

abs(Low - Previous Close)

ATR = MA(TR, n) , where n is number of periods for moving average, in our case equals 14.

ATR shows how much an asset moves on average per candle/bar. A higher ATR means more volatility; a lower ATR means a calmer market.

The Choppiness Index is a technical indicator that quantifies whether the market is trending or choppy (sideways). It doesn't indicate trend direction — only the strength or weakness of a trend. Higher Choppiness Index usually approximates the sideways market, while its low value tells us that there is a high probability of a trend.

Choppiness Index = 100 × log10(ΣATR(n) / (MaxHigh(n) - MinLow(n))) / log10(n)

where:

ΣATR(n) = sum of the Average True Range over n periods

MaxHigh(n) = highest high over n periods

MinLow(n) = lowest low over n periods

log10 = base-10 logarithm

Now let's understand how these indicators work in conjunction and why they were chosen for this strategy. KST indicator approximates current momentum, when it is rising and KST line crosses over the signal line there is high probability that short term trend is reversing to the upside and strategy allows to take part in this potential move. Alligator's jaw (blue) line is used as an approximation of a short term trend, taking trades only above it we want to avoid trading against trend to increase probability that long trade is going to be winning.

Almost the same for Moving Average, but it approximates the long term trend, this is just the additional filter. If we trade in the direction of the long term trend we increase probability that higher risk to reward trade will hit the take profit. Choppiness index is the optional filter, but if it turned on it is used for approximating if now market is in sideways or in trend. On the range bounded market the potential moves are restricted. We want to decrease probability opening trades in such condition avoiding trades if this index is above threshold value.

When trade is open script sets the stop loss and take profit targets. ATR approximates the current volatility, so we can make a decision when to exit a trade based on current market condition, it can increase the probability that strategy will avoid the excessive stop loss hits, but anyway user can setup how many ATRs to use as a stop loss and take profit target. As was said in the Methodology stop loss level is obtained by subtracting number of ATRs from trade opening candle low, while take profit by adding to this candle's close.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2025.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 60%

Maximum Single Position Loss: -5.53%

Maximum Single Profit: +8.35%

Net Profit: +5175.20 USDT (+51.75%)

Total Trades: 120 (56.67% win rate)

Profit Factor: 1.747

Maximum Accumulated Loss: 1039.89 USDT (-9.1%)

Average Profit per Trade: 43.13 USDT (+0.6%)

Average Trade Duration: 27 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 1h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrexio commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation.

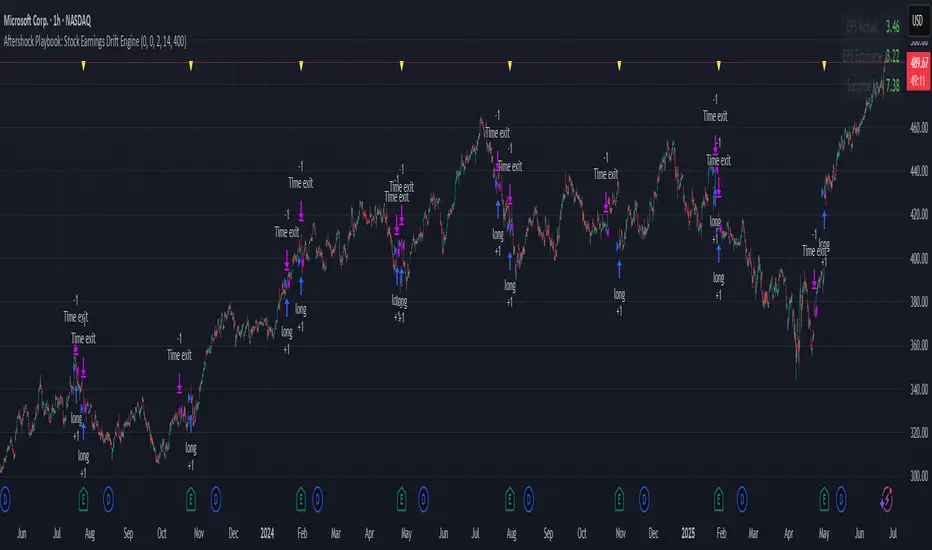

Aftershock Playbook: Stock Earnings Drift EngineStrategy type

Event-driven post-earnings momentum engine (long/short) built for single-stock charts or ADRs that publish quarterly results.

What it does

Detects the exact earnings bar (request.earnings, lookahead_off).

Scores the surprise and launches a position on that candle’s close.

Tracks PnL: if the first leg closes green, the engine automatically re-enters on the very next bar, milking residual drift.

Blocks mid-cycle trades after a loss until the next earnings release—keeping the risk contained to one cycle.

Think of it as a sniper that fires on the earnings pop, reloads once if the shot lands, then goes silent until the next report.

Core signal inputs

Component Default Purpose

EPS Surprise % +0 % / –5 % Minimum positive / negative shock to trigger longs/shorts.

Reverse signals? Off Quick flip for mean-reversion experiments.

Time Risk Mgt. Off Optional hard exit after 45 calendar days (auto-scaled to any TF).

Risk engine

ATR-based stop (ATR × 2 by default, editable).

Bar time stop (15-min → Daily: Have to select the bar value ).

No pyramiding beyond the built-in “double-tap”.

All positions sized as % of equity via Strategy Properties.

Visual aids

Yellow triangle marks the earnings bar.

Diagnostics table (top-right) shows last Actual, Estimate, and Surprise %.

Status-line tool-tips on every input.

Default inputs

Setting Value

Positive surprise ≥ 0 %

Negative surprise ≤ –5 %

ATR stop × 2

ATR length 50

Hold horizon 350 ( 1h timeframe chart bars)

Back-test properties

Initial capital 10 000

Order size 5 % of equity

Pyramiding 1 (internal re-entry only)

Commission 0.03 %

Slippage 5 ticks

Fills Bar magnifier ✔ · On bar close ✔ · Standard OHLC ✔

How to use

Add the script to any earnings-driven stock (AAPL, MSFT, TSLA…).

Turn on Time Risk Management if you want stricter risk management

Back-test different ATR multipliers to fit the stock’s volatility.

Sync commission & slippage with your broker before forward-testing.

Important notes

Works on every timeframe from 15 min to 1 D. Sweet spot around 30min/1h

All request.earnings() & request.security() calls use lookahead_off—zero repaint.

The “double-tap” re-entry occurs once per winning cycle to avoid drift-chasing loops.

Historical stats ≠ future performance. Size positions responsibly.

Out of the Noise Intraday Strategy with VWAP [YuL]This is my (naive) implementation of "Beat the Market An Effective Intraday Momentum Strategy for S&P500 ETF (SPY)" paper by Carlo Zarattini, Andrew Aziz, Andrea Barbon, so the credit goes to them.

It is supposed to run on SPY on 30-minute timeframe, there may be issues on other timeframes.

I've used settings that were used by the authors in the original paper to keep it close to the publication, but I understand that they are very aggressive and probably shouldn't be used like that.

Results are good, but not as good as they are stated in the paper (unsurprisingly?): returns are smaller and Sharpe is very low (which is actually weird given the returns and drawdown ratio), there are also margin calls if you enable margin check (and you should).

I have my own ideas of improvements which I will probably implement separately to keep this clean.

Price Statistical Strategy-Z Score V 1.01

Price Statistical Strategy – Z Score V 1.01

Overview

A technical breakdown of the logic and components of the “Price Statistical Strategy – Z Score V 1.01”.

This script implements a smoothed Z-Score crossover mechanism applied to the closing price to detect potential statistical deviations from local price mean. The strategy operates solely on price data (close) and includes signal spacing control and momentum-based candle filters. No volume-based or trend-detection components are included.

Core Methodology

The strategy is built on the statistical concept of Z-Score, which quantifies how far a value (closing price) is from its recent average, normalized by standard deviation. Two moving averages of the raw Z-Score are calculated: a short-term and a long-term smoothed version. The crossover between them generates long entries and exits.

Signal Conditions

Entry Condition:

A long position is opened when the short-term smoothed Z-Score crosses above the long-term smoothed Z-Score, and additional entry conditions are met.

Exit Condition:

The position is closed when the short-term Z-Score crosses below the long-term Z-Score, provided the exit conditions allow.

Signal Gapping:

A minimum number of bars (Bars gap between identical signals) must pass between repeated entry or exit signals to reduce noise.

Momentum Filter:

Entries are prevented during sequences of three or more consecutively bullish candles, and exits are prevented during three or more consecutively bearish candles.

Z-Score Function

The Z-Score is calculated as:

Z = (Close - SMA(Close, N)) / STDEV(Close, N)

Where N is the base period selected by the user.

Input Parameters

Enable Smoothed Z-Score Strategy

Enables or disables the Z-Score strategy logic. When disabled, no trades are executed.

Z-Score Base Period

Defines the number of bars used to calculate the simple moving average and standard deviation for the Z-Score. This value affects how responsive the raw Z-Score is to price changes.

Short-Term Smoothing

Sets the smoothing window for the short-term Z-Score. Higher values produce smoother short-term signals, reducing sensitivity to short-term volatility.

Long-Term Smoothing

Sets the smoothing window for the long-term Z-Score, which acts as the reference line in the crossover logic.

Bars gap between identical signals

Minimum number of bars that must pass before another signal of the same type (entry or exit) is allowed. This helps reduce redundant or overly frequent signals.

Trade Visualization Table

A table positioned at the bottom-right displays live PnL for open trades:

Entry Price

Unrealized PnL %

Text colors adapt based on whether unrealized profit is positive, negative, or neutral.

Technical Notes

This strategy uses only close prices — no trend indicators or volume components are applied.

All calculations are based on simple moving averages and standard deviation over user-defined windows.

Designed as a minimal, isolated Z-Score engine without confirmation filters or multi-factor triggers.

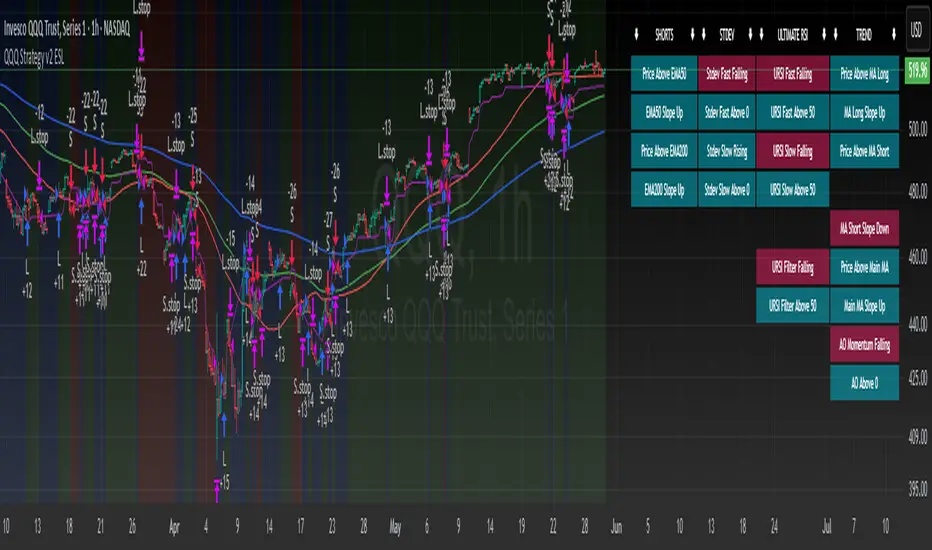

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

Smart Fib StrategySmart Fibonacci Strategy

This advanced trading strategy combines the power of adaptive SMA entries with Fibonacci-based exit levels to create a comprehensive trend-following system that self-optimizes based on historical market conditions. Credit goes to Julien_Eche who created the "Best SMA Finder" which received an Editors Pick award.

Strategy Overview

The Smart Fibonacci Strategy employs a two-pronged approach to trading:

1. Intelligent Entries: Uses a self-optimizing SMA (Simple Moving Average) to identify optimal entry points. The system automatically tests multiple SMA lengths against historical data to determine which period provides the most robust trading signals.

2. Fibonacci-Based Exits: Implements ATR-adjusted Fibonacci bands to establish precise exit targets, with risk-management options ranging from conservative to aggressive.

This dual methodology creates a balanced system that adapts to changing market conditions while providing clear visual reference points for trade management.

Key Features

- **Self-Optimizing Entries**: Automatically calculates the most profitable SMA length based on historical performance

- **Adjustable Risk Parameters**: Choose between low-risk and high-risk exit targets

- **Directional Flexibility**: Trade long-only, short-only, or both directions

- **Visualization Tools**: Customizable display of entry lines and exit bands

- **Performance Statistics**: Comprehensive stats table showing key metrics

- **Smoothing Option**: Reduces noise in the Fibonacci bands for cleaner signals

Trading Rules

Entry Signals

- **Long Entry**: When price crosses above the blue center line (optimal SMA)

- **Short Entry**: When price crosses below the blue center line (optimal SMA)

### Exit Levels

- **Low Risk Option**: Exit at the first Fibonacci band (1.618 * ATR)

- **High Risk Option**: Exit at the second Fibonacci band (2.618 * ATR)

Strategy Parameters

Display Settings

- Toggle visibility of the stats table and indicator components

Strategy Settings

- Select trading direction (long, short, or both)

- Choose exit method (low risk or high risk)

- Set minimum trades threshold for SMA optimization

SMA Settings

- Option to use auto-optimized or fixed-length SMA

- Customize SMA length when using fixed option

Fibonacci Settings

- Adjust ATR period and SMA basis for Fibonacci bands

- Enable/disable smoothing function

- Customize Fibonacci ratio multipliers

Appearance Settings

- Modify colors, line widths, and transparency

Optimization Methodology

The strategy employs a sophisticated optimization algorithm that:

1. Tests multiple SMA lengths against historical data

2. Evaluates performance based on trade count, profit factor, and win rate

3. Calculates a "robustness score" that balances profitability with statistical significance

4. Selects the SMA length with the highest robustness score

This ensures that the strategy's entry signals are continuously adapting to the most effective parameters for current market conditions.

Risk Management

Position sizing is fixed at $2,000 per trade, allowing for consistent exposure across all trading setups. The Fibonacci-based exit system provides two distinct risk management approaches:

- **Conservative Approach**: Using the first Fibonacci band for exits produces more frequent but smaller wins

- **Aggressive Approach**: Using the second Fibonacci band allows for larger potential gains at the cost of increased volatility

Ideal Usage

This strategy is best suited for:

- Trending markets with clear directional moves

- Timeframes from 4H to Daily for most balanced results

- Instruments with moderate volatility (stocks, forex, commodities)

Traders can further enhance performance by combining this strategy with broader market analysis to confirm the prevailing trend direction.

RCI Strategy [PineIndicators]RCI Strategy

This strategy leverages the Rank Correlation Index (RCI) — a statistical oscillator that measures the relationship between time and price rank — combined with a configurable moving average filter. It offers clean, rule-based entries and exits, and visually enhanced trade tracking via labeled markers and boxes on the chart.

The RCI Strategy is well-suited for momentum traders looking to capture directional shifts with confirmation through RCI smoothing.

Core Logic

1. Rank Correlation Index (RCI)

Measures how closely price changes correlate with time rankings.

Values range between -100 and +100.

Thresholds at ±80 help identify potential reversals or extremes.

2. RCI Smoothing via Moving Average

A moving average (MA) is applied to the RCI to smooth out fluctuations.

Supported MA types:

SMA

EMA

SMMA (RMA)

WMA

VWMA

Users can disable the smoothing by selecting "None".

Trade Entry Logic

Long Entry: RCI crosses above the selected moving average.

Short Entry: RCI crosses below the moving average.

Entries are restricted by trade direction settings:

Long Only

Short Only

Long & Short

Visual Features

RCI Panel Display

Plots RCI line and its moving average in a separate pane.

Horizontal guide lines at 0, +80, and -80 help visualize signal zones.

Trade Labels on Chart

Buy Label: Plotted when a long entry is executed.

Close Label: Plotted when any position is closed.

Triangle markers for visual emphasis on direction change.

Trade Visualization Boxes

A colored box is drawn between entry and exit prices.

Green = profitable trade; Red = losing trade.

Two horizontal lines connect entry and exit prices for reference.

Customization Parameters

RCI Source: Select input price for the RCI (default: close).

RCI Length: Set sensitivity of the oscillator.

MA Type and Length: Choose and configure the smoothing filter.

Trade Direction Mode: Define whether to allow Long, Short, or both.

Use Cases

Swing traders who want to trade directional reversals with statistical backing.

Traders seeking a clean and visual strategy based on rank momentum.

Environments where both trend and range dynamics occur.

Conclusion

The RCI Strategy is a non-repainting, rule-based trading model that combines rank correlation momentum with smoothed trend logic. Its clean visual markers, labeled trades, and flexible MA filters make it a valuable tool for discretionary and systematic traders alike.

Parabolic RSI Strategy [ChartPrime × PineIndicators]This strategy combines the strengths of the Relative Strength Index (RSI) with a Parabolic SAR logic applied directly to RSI values.

Full credit to ChartPrime for the original concept and indicator, licensed under the MPL 2.0.

It provides clear momentum-based trade signals using an innovative method that tracks RSI trend reversals via a customized Parabolic SAR, enhancing traditional oscillator strategies with dynamic trend confirmation.

How It Works

The system overlays a Parabolic SAR on the RSI, detecting trend shifts in RSI itself rather than on price, offering early reversal insight with visual and algorithmic clarity.

Core Components

1. RSI-Based Trend Detection

Calculates RSI using a customizable length (default: 14).

Uses upper and lower thresholds (default: 70/30) for overbought/oversold zones.

2. Parabolic SAR Applied to RSI

A custom Parabolic SAR function tracks momentum within the RSI, not price.

This allows the system to capture RSI trend reversals more responsively.

Configurable SAR parameters: Start, Increment, and Maximum acceleration.

3. Signal Generation

Long Entry: Triggered when the SAR flips below the RSI line.

Short Entry: Triggered when the SAR flips above the RSI line.

Optional RSI filter ensures that:

Long entries only occur above a minimum RSI (e.g. 50).

Short entries only occur below a maximum RSI.

Built-in logic prevents new positions from being opened against trend without prior exit.

Trade Modes & Controls

Choose from:

Long Only

Short Only

Long & Short

Optional setting to reverse positions on opposite signal (instead of waiting for a flat close).

Visual Features

1. RSI Plotting with Thresholds

RSI is displayed in a dedicated pane with overbought/oversold fill zones.

Custom horizontal lines mark threshold boundaries.

2. Parabolic SAR Overlay on RSI

SAR dots color-coded for trend direction.

Visible only when enabled by user input.

3. Entry & Exit Markers

Diamonds: Mark entry points (above for shorts, below for longs).

Crosses: Mark exit points.

Strategy Strengths

Provides early momentum reversal entries without relying on price candles.

Combines oscillator and trend logic without repainting.

Works well in both trending and mean-reverting markets.

Easy to configure with fine-tuned filter options.

Recommended Use Cases

Intraday or swing traders who want to catch RSI-based reversals early.

Traders seeking smoother signals than price-based Parabolic SAR entries.

Users of RSI looking to reduce false positives via trend tracking.

Customization Options

RSI Length and Thresholds.

SAR Start, Increment, and Maximum values.

Trade Direction Mode (Long, Short, Both).

Optional RSI filter and reverse-on-signal settings.

SAR dot color customization.

Conclusion

The Parabolic RSI Strategy is an innovative, non-repainting momentum strategy that enhances RSI-based systems with trend-confirming logic using Parabolic SAR. By applying SAR logic to RSI values, this strategy offers early, visualized, and filtered entries and exits that adapt to market dynamics.

Credit to ChartPrime for the original methodology, published under MPL-2.0.

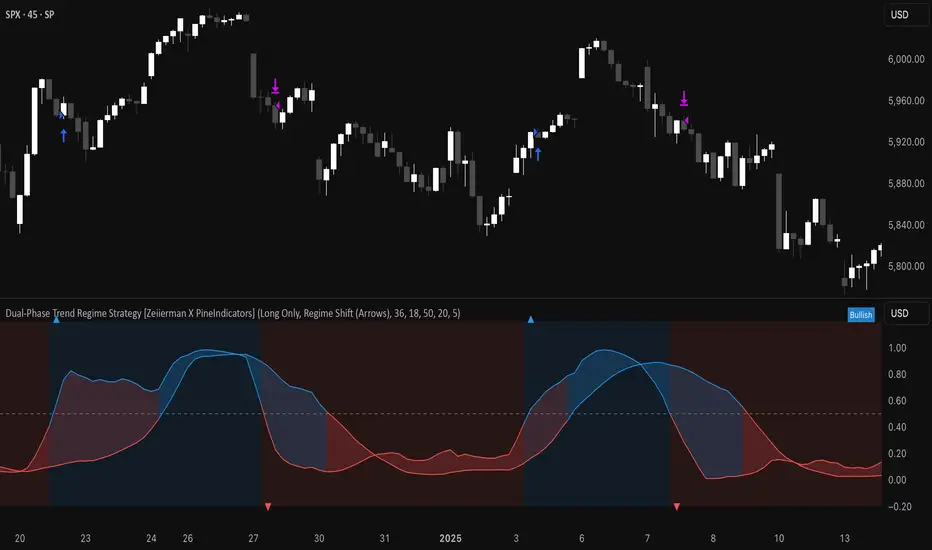

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

Reversal Strength Meter – Adib NooraniThe Reversal Strength Meter is an oscillator designed to identify potential reversal zones based on supply and demand dynamics. It uses smoothed stochastic logic to reduce noise and highlight areas where momentum may be weakening, signaling possible market turning points.

🔹 Smooth, noise-reduced stochastic oscillator

🔹 Custom zones to highlight potential supply and demand imbalances

🔹 Non-repainting, compatible across all timeframes and assets

🔹 Visual-only tool — intended to support discretionary trading decisions

This oscillator assists scalpers and intraday traders in tracking subtle shifts in momentum, helping them identify when a market may be preparing to reverse — always keeping in mind that trading is based on probabilities, not certainties.

📘 How to Use the Indicator Efficiently

For Reversal Trading:

Buy Setup

– When the blue line dips below the 20 level, wait for it to re-enter above 20.

– Look for reversal candlestick patterns (e.g., bullish engulfing, hammer, or morning star).

– Enter above the pattern’s high, with a stop loss below its low.

Sell Setup

– When the blue line rises above the 80 level, wait for it to re-enter below 80.

– Look for bearish candlestick patterns (e.g., bearish engulfing, inverted hammer, or evening star).

– Enter below the pattern’s low, with a stop loss above its high.

🛡 Risk Management Guidelines

Risk only 0.5% of your capital per trade

Book 50% profits at a 1:1 risk-reward ratio

Trail the remaining 50% using price action or other supporting indicators

Reversal Scalping Ribbon - Adib NooraniThe Reversal Scalping Ribbon is a trend-following overlay tool designed to visually identify potential reversal zones based on price extremes and dynamic volatility bands. It calculates adaptive upper and lower bands using price action and custom ATR logic, helping traders quickly assess market direction and possible turning points

🔹 Volatility-adjusted bands based on price highs/lows

🔹 Color-coded ribbons to indicate trend bias and potential reversal shifts

🔹 No repainting, works on all timeframes and assets

🔹 Visual-only display, no trade signals — supports discretion-based entries

This ribbon is designed for scalpers and intraday traders to spot reversal setups with clarity. It enhances your trading by showing real-time market bias without unnecessary distractions. By focusing on probabilities, it helps to improve decision-making in fast-paced environments

How to use the indicator efficiently

For Reversal Trading:

Buy: When price closes below the green ribbon with a red candle, then re-enters with a green candle. Enter above the high of the green candle with a stop loss below the lowest low of the recent green/red candles

Sell: When price closes above the red ribbon with a green candle, then re-enters with a red candle. Enter below the low of the red candle with a stop loss above the highest high of the recent red/green candles

Risk Management:

Limit risk to 0.5% of your capital per trade

Take 50% profit at a 1:1 risk-reward ratio

For the remaining 50%, trail using the lower edge of the green band for buys and the upper edge of the red band for sells

Moving Average Shift WaveTrend StrategyMoving Average Shift WaveTrend Strategy

🧭 Overview

The Moving Average Shift WaveTrend Strategy is a trend-following and momentum-based trading system designed to be overlayed on TradingView charts. It executes trades based on the confluence of multiple technical conditions—volatility, session timing, trend direction, and oscillator momentum—to deliver logical and systematic trade entries and exits.

🎯 Strategy Objectives

Enter trades aligned with the prevailing long-term trend

Exit trades on confirmed momentum reversals

Avoid false signals using session timing and volatility filters

Apply structured risk management with automatic TP, SL, and trailing stops

⚙️ Key Features

Selectable MA types: SMA, EMA, SMMA (RMA), WMA, VWMA

Dual-filter logic using a custom oscillator and moving averages

Session and volatility filters to eliminate low-quality setups

Trailing stop, configurable Take Profit / Stop Loss logic

“In-wave flag” prevents overtrading within the same trend wave

Visual clarity with color-shifting candles and entry/exit markers

📈 Trading Rules

✅ Long Entry Conditions:

Price is above the selected MA

Oscillator is positive and rising

200-period EMA indicates an uptrend

ATR exceeds its median value (sufficient volatility)

Entry occurs between 09:00–17:00 (exchange time)

Not currently in an active wave

🔻 Short Entry Conditions:

Price is below the selected MA

Oscillator is negative and falling

200-period EMA indicates a downtrend

All other long-entry conditions are inverted

❌ Exit Conditions:

Take Profit or Stop Loss is hit

Opposing signals from oscillator and MA

Trailing stop is triggered

🛡️ Risk Management Parameters

Pair: ETH/USD

Timeframe: 4H

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 2% of account equity (adjustable)

Total Trades: 224

Backtest Period: May 24, 2016 — April 7, 2025

Note: Risk parameters are fully customizable to suit your trading style and broker conditions.

🔧 Trading Parameters & Filters

Time Filter: Trades allowed only between 09:00–17:00 (exchange time)

Volatility Filter: ATR must be above its median value

Trend Filter: Long-term 200-period EMA

📊 Technical Settings

Moving Average

Type: SMA

Length: 40

Source: hl2

Oscillator

Length: 15

Threshold: 0.5

Risk Management

Take Profit: 1.5%

Stop Loss: 1.0%

Trailing Stop: 1.0%

👁️ Visual Support

MA and oscillator color changes indicate directional bias

Clear chart markers show entry and exit points

Trailing stops and risk controls are transparently managed

🚀 Strategy Improvements & Uniqueness

In-wave flag avoids repeated entries within the same trend phase

Filtering based on time, volatility, and trend ensures higher-quality trades

Dynamic high/low tracking allows precise trailing stop placement

Fully rule-based execution reduces emotional decision-making

💡 Inspirations & Attribution

This strategy is inspired by the excellent concept from:

ChartPrime – “Moving Average Shift”

It expands on the original idea with advanced trade filters and trailing logic.

Source reference:

📌 Summary

The Moving Average Shift WaveTrend Strategy offers a rule-based, reliable approach to trend trading. By combining trend and momentum filters with robust risk controls, it provides a consistent framework suitable for various market conditions and trading styles.

⚠️ Disclaimer

This script is for educational purposes only. Trading involves risk. Always use proper backtesting and risk evaluation before applying in live markets.

RSI Full [Titans_Invest]RSI Full

One of the most complete RSI indicators on the market.

While maintaining the classic RSI foundation, our indicator integrates multiple entry conditions to generate more accurate buy and sell signals.

All conditions are fully configurable, allowing complete customization to fit your trading strategy.

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

Overbought: When the RSI is above 70, indicating that the asset may be overbought.

Oversold: When the RSI is below 30, indicating that the asset may be oversold.

Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND/OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND/OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy the Spell!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

ZVOL — Z-Score Volume Heatmapⓩ ZVOL transforms raw volume into a statistically calibrated heatmap using Z-score thresholds. Unlike classic volume indicators that rely on fixed MA comparisons, ZVOL calculates how many standard deviations each volume bar deviates from its mean. This makes the reading adaptive across timeframes and assets, in order to distinguish meaningful crowd behavior from random volatility.

📊 The core display is a five-zone histogram, each encoded by color and statistical depth. Optional background shading mirrors these zones across the entire pane, revealing subtle compression or structural rhythm shifts across time. By grounding the volume reading in volatility-adjusted context, ZVOL inhibits impulsive trading tactics by compelling the structure, not the sentiment, to dictate the signal.

🥵 Heatmap Coloration:

🌚 Suppressed volume — congestion, coiling phases

🩱 Stable flow — early trend or resting volume

🏀 High activity — emerging pressure

💔 Extreme — possible climax or institutional print

🎗️ A dynamic Fibonacci-based 21:34-period EMA ribbon overlays the histogram. The fill area inverts color on crossover, providing a real-time read on tempo, expansion, or divergence between price structure and crowd effort.

💡 LTF Usage Suggestions:

• Confirm breakout legs when orange or red zones align with range exits

• Fade overextended moves when red bars appear into resistance

• Watch for rising EMAs and orange volume to front-run impulsive moves

• Combine with volatility suppression (e.g. ATR) to catch compression → expansion transitions

🥂 Ideal Pairings:

• OBVX Conviction Bias — to confirm directional intent behind volume shifts

• SUPeR TReND 2.718 — for directional filters

• ATR Turbulence Ribbon — to detect compression phases

👥 The OBVX Conviction Bias adds a second dimension to ZVOL by revealing whether crowd effort is aligning with price direction or diverging beneath the surface. While ZVOL identifies statistical anomalies in raw volume, OBVX tracks directional commitment using cumulative volume and moving average cross logic. Use them together to spot fake-outs, anticipate structure-confirmed breakouts, or time pullbacks with volume-based conviction.

🔬 ZVOL isn’t just a volume filter — it’s a structural lens. It reveals when crowd effort is meaningful, when it's fading, and when something is about to shift. Designed for structure-aware traders who care about context, not noise.

Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

Uptrick X PineIndicators: Z-Score Flow StrategyThis strategy is based on the Z-Score Flow Indicator developed by Uptrick. Full credit for the original concept and logic goes to Uptrick.

The Z-Score Flow Strategy combines statistical mean-reversion logic with trend filtering, RSI confirmation, and multi-mode trade execution, offering a flexible and structured approach to trading both reversals and trend continuations.

Core Concepts Behind Z-Score Flow

1. Z-Score Mean Reversion Logic

The Z-score measures how far current price deviates from its statistical mean, in standard deviations.

A high positive Z-score (e.g. > 2) suggests price is overbought and may revert downward.

A low negative Z-score (e.g. < -2) suggests price is oversold and may revert upward.

The strategy uses Z-score thresholds to trigger signals when price deviates far enough from its mean.

2. Trend Filtering with EMA

To prevent counter-trend entries, the strategy includes a trend filter based on a 50-period EMA:

Only allows long entries if price is below EMA (mean-reversion in downtrends).

Only allows short entries if price is above EMA (mean-reversion in uptrends).

3. RSI Confirmation and Lockout System

An RSI smoothing mechanism helps confirm signals and avoid whipsaws:

RSI must be below 30 and rising to allow buys.

RSI must be above 70 and falling to allow sells.

Once a signal occurs, it is "locked out" until RSI re-enters the neutral zone (30–70).

This avoids multiple signals in overextended zones and reduces overtrading.

Entry Signal Logic

A buy or sell is triggered when:

Z-score crosses below (buy) or above (sell) the threshold.

RSI smoothed condition is met (oversold and rising / overbought and falling).

The trend condition (EMA filter) aligns.

A cooldown period has passed since the last opposite trade.

This layered approach helps ensure signal quality and timing precision.

Trade Modes

The strategy includes three distinct trade modes to adapt to various market behaviors:

1. Standard Mode

Trades are opened using the Z-score + RSI + trend filter logic.

Each signal must pass all layered conditions.

2. Zero Cross Mode

Trades are based on the Z-score crossing zero.

This mode is useful in trend continuation setups, rather than mean reversion.

3. Trend Reversal Mode

Trades occur when the mean slope direction changes, i.e., basis line changes color.

Helps capture early trend shifts with less lag.

Each mode can be customized for long-only, short-only, or long & short execution.

Visual Components

1. Z-Score Mean Line

The basis (mean) line is colored based on slope direction.

Green = bullish slope, Purple = bearish slope, Gray = flat.

A wide shadow band underneath reflects current trend momentum.

2. Gradient Fill to Price

A gradient zone between price and the mean reflects:

Price above mean = bearish zone with purple overlay.

Price below mean = bullish zone with teal overlay.

This visual aid quickly reveals market positioning relative to equilibrium.

3. Signal Markers

"𝓤𝓹" labels appear for buy signals.

"𝓓𝓸𝔀𝓷" labels appear for sell signals.

These are colored and positioned according to trend context.

Customization Options

Z-Score Period & Thresholds: Define sensitivity to price deviations.

EMA Trend Filter Length: Filter entries with long-term bias.

RSI & Smoothing Periods: Fine-tune RSI confirmation conditions.

Cooldown Period: Prevent signal spam and enforce timing gaps.

Slope Index: Adjust how far back to compare mean slope.

Visual Settings: Toggle mean lines, gradients, and more.

Use Cases & Strategy Strengths

1. Mean-Reversion Trading

Ideal for catching pullbacks in trending markets or fading overextended price moves.

2. Trend Continuation or Reversal

With multiple trade modes, traders can choose between fading price extremes or trading slope momentum.

3. Signal Clarity and Risk Control

The combination of Z-score, RSI, EMA trend, and cooldown logic provides high-confidence signals with built-in filters.

Conclusion

The Z-Score Flow Strategy by Uptrick X PineIndicators is a versatile and structured trading system that:

Fuses statistical deviation (Z-score) with technical filters.

Provides both mean-reversion and trend-based entry logic.

Uses visual overlays and signal labels for clarity.

Prevents noise-driven trades via cooldown and lockout systems.

This strategy is well-suited for traders seeking a data-driven, multi-condition entry framework that can adapt to various market types.

Full credit for the original concept and indicator goes to Uptrick.

VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

Triangular Hull Moving Average [BigBeluga X PineIndicators]This strategy is based on the original Triangular Hull Moving Average (THMA) + Volatility indicator by BigBeluga. Full credit for the concept and design goes to BigBeluga.

The strategy blends smoothed trend-following logic using a Triangular Hull Moving Average with dynamic volatility overlays, providing actionable trade signals with responsive visual feedback. It's designed for traders who want a non-lagging trend filter while also monitoring market volatility in real time.

How the Strategy Works

1. Triangular Hull Moving Average (THMA) Core

At its core, the strategy uses a Triangular Hull Moving Average (THMA) — a variation of the traditional Hull Moving Average with triple-smoothing logic:

It combines multiple weighted moving averages (WMAs) to create a faster and smoother trend line.

This reduces lag without compromising trend accuracy.

The THMA reacts more responsively to price movements than classic MAs.

THMA Formula:

thma(_src, _length) =>

ta.wma(ta.wma(_src,_length / 3) * 3 - ta.wma(_src, _length / 2) - ta.wma(_src, _length), _length)

This logic filters out short-term noise while still being sensitive to genuine trend shifts.

2. Volatility-Enhanced Candle Plotting

An optional volatility mode overlays the chart with custom candles that incorporate volatility bands:

Wicks expand and contract dynamically based on market volatility.

The volatility value is computed using a HMA of high-low range over a user-defined length.

The candle bodies reflect THMA values, while the wicks reflect the current volatility spread.

This feature allows traders to visually gauge the strength of price moves and anticipate possible breakouts or slowdowns.

3. Trend Reversal Signal Detection

The strategy identifies trend reversals when the THMA line crosses over/under its own past value:

A bullish signal is triggered when THMA crosses above its value from two bars ago.

A bearish signal is triggered when THMA crosses below its value from two bars ago.

These shifts are marked on the chart with triangle-shaped signals for clear visibility.

This logic helps detect momentum shifts early and enables reactive trade entries.

Trade Entry & Exit Logic

Trade Modes Supported

Users can choose between:

Only Long – Enters long trades only.

Only Short – Enters short trades only.

Long & Short – Enables both directions.

Entry Conditions

Long Entry:

Triggered when a bullish crossover is detected.

Active only if the strategy mode allows long trades.

Short Entry:

Triggered when a bearish crossover is detected.

Active only if the strategy mode allows short trades.

Exit Conditions

In Only Long mode, the strategy closes long positions when a bearish signal appears.

In Only Short mode, the strategy closes short positions when a bullish signal appears.

In Long & Short mode, the strategy does not auto-close positions — instead, it opens new positions on each confirmed signal.

Dashboard Visualization

In the bottom-right corner of the chart, a live dashboard displays:

The current trend direction (🢁 for bullish, 🢃 for bearish).

The current volatility level as a percentage.

This helps traders quickly assess market status and adjust their decisions accordingly.

Customization Options

THMA Length: Adjust how smooth or reactive the trend detection should be.

Volatility Toggle & Length: Enable or disable volatility visualization and set sensitivity.

Color Settings: Choose colors for up/down trend visualization.

Trade Direction Mode: Limit the strategy to long, short, or both types of trades.

Use Cases & Strategy Strengths

1. Trend Following

Use the THMA-based candles and triangle signals to enter with momentum. The indicator adapts quickly, reducing lag and improving trade timing.

2. Volatility Monitoring

Visualize the strength of the trend with volatility wicks. Use expanding bands to confirm breakouts and contracting ones to detect weakening moves.

3. Signal Confirmation

Combine this tool with other indicators or use the trend shift triangles as confirmations for manual entries.

Conclusion

The THMA + Volatility Strategy is a non-repainting trend-following system that integrates:

Triangular Hull MA for advanced trend detection.

Real-time volatility visualization.

Clear entry signals based on trend reversals.

Configurable trade direction settings.

It is ideal for traders who:

Prefer smoothed price analysis.

Want to follow trends with precision.

Value visual volatility feedback for breakout detection.

Full credit for the original concept and indicator goes to BigBeluga.

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio