Asset vs Total Market Cap & Relative Strength Purpose

This indicator allows traders to compare a selected asset to the major market benchmarks:

BTC – primary crypto market leader

ETH – secondary crypto market leader

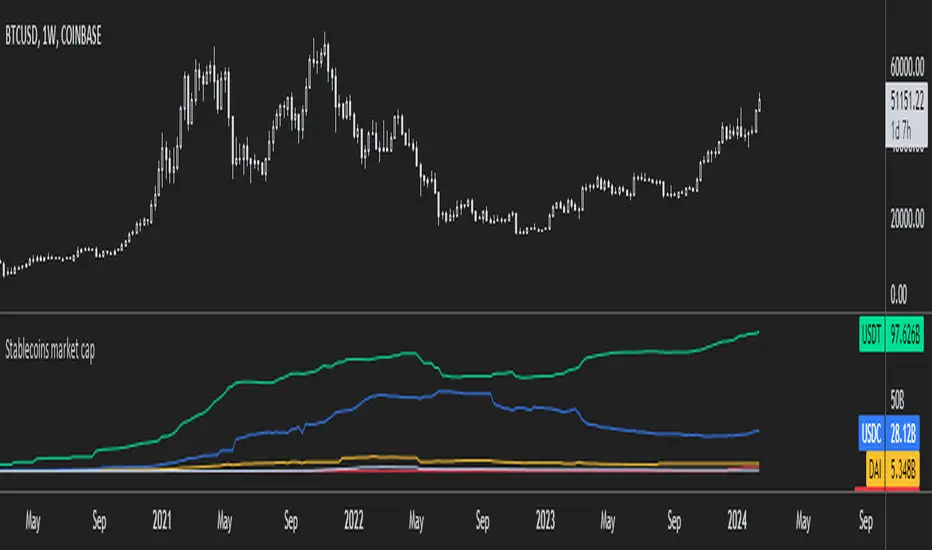

USDT.D – shows market risk-on vs risk-off sentiment

TOTAL – total crypto market capitalization, useful for overall market trends

It also provides relative strength calculations:

Rel. Strength = Asset % change - USDT.D % change

Rel. Strength vs Total = Asset % change - Total % change

This allows you to see if your asset is outperforming or underperforming broader benchmarks.

The table covers multiple timeframes, making it easy to scan both short-term and longer-term trends:

Row Timeframe

0 Current

1 15m

2 1H

3 4H

4 1D

Selected Asset / BTC / ETH:

Green for positive % change

Red for negative % change

Gradient intensity proportional to magnitude (maxAbsChange input)

USDT.D:

Orange if rising (risk-off)

Teal if falling (risk-on)

Total Market Cap / Rel. Strength:

Gradient reflects asset performance relative to total market, independent of USDT.D.

Positives

Compact dashboard: Everything is in one table for quick scanning.

Multi-timeframe comparison: Traders can instantly see short-term vs long-term strength.

Relative performance visualization: Gradients immediately highlight outperformers and underperformers.

Benchmark comparisons: Asset vs BTC, ETH, USDT.D, and Total Market Cap.

Independent Rel. Strength: Highlights whether the asset is outperforming even if the total market moves.

Customizable gradient sensitivity: maxAbsChange and maxRelChange allow tuning how “strong” the colors appear.

Chart plotting: Rel. Strength vs total market is plotted for further visual reference.

How to Use

Green table cells → strong positive movement

Red table cells → negative movement

Rel. Strength > 0 → asset outperforming

Rel. Strength < 0 → asset underperforming

Use table to compare relative performance vs BTC, ETH, and total market for informed trading decisions.

Индикатор Pine Script®