merge_pinbar_modifiedLibrary "merge_pinbar"

Published by @dandrideng

Modified by @RpNm1337

merge_pinbar: merge bars and check whether the bar is a pinbar

merge_pinbar(period, max_bars)

merge_pinbar: merge bars and check whether the bar is a pinbar

Parameters:

period (simple int)

max_bars (simple int)

Returns: array:

Индикаторы и стратегии

A_Taders_Edge_LIBRARYLibrary "A_Taders_Edge_LIBRARY"

RCI(_rciLength, _close, _interval, _outerMostRangeOfOscillator)

- You will see me using this a lot. DEFINITELY my favorite oscillator to utilize for SO many different things from timing entries/exits to determining trends.

Parameters:

_rciLength (int)

_close (float)

_interval (int)

_outerMostRangeOfOscillator (int)

Returns: - Outputs a single RCI value that will between (-)_outerMostRangeOfOscillator to (+)_outerMostRangeOfOscillator

InvalidTID(_close, _showInvalidAssets, _securityTickerid, _invalidArray)

- This is to add a table on the right of your chart that prints all the TickerID's that were either not formulated correctly in the scripts input or that is not a valid symbol and should be changed.

Parameters:

_close (float)

_showInvalidAssets (simple bool)

_securityTickerid (string)

_invalidArray (string )

Returns: - Does NOT return a value but rather the table with the invalid TickerID's from the scripts input that need to be changed.

LabelLocation(_firstLocation)

- This is ONLY for when you are wanting to print ALERT LABELS with the assets name for when an alert trigger occurs for that asset. There are a total of 40 assets that can be used in each copy of the script. You don't want labels from different assets printing on top of each other because you will not be able to read the asset name that the label is for. Ex. If you put your _firstLocation in the input settings as 1 and have 40 assets on this copy of the scanner then the first asset in the list is assigned to the location value 1 on the scale, and the 2nd in the list is assigned to location value 2...and so on. If your first location is set to 81 then the 1st asset is 81 and 2nd is 82 and so on.

Parameters:

_firstLocation (simple int)

Returns: - regardless of if you have the maximum amount of assets being screened (40 max), this export function will output 40 locations… So there needs to be 40 variables assigned to the tuple in this export function. What I mean by that is there needs to be 40 variables between the ' '. If you only have 20 assets in your scripts input settings, then only the first 20 variables within the ' ' Will be assigned to a value location and the other 20 will be assigned 'NA'.

SeparateTickerids(_string)

- You must form this single tickerID input string exactly as laid out in the water (a little gray circle at the end of the setting, that you hover your cursor over to read the details of). IF the string is formed correctly then it will break up. All of the tip rate is within the string into a total of 40 separate strings which will be all of the tickerIDs that the script is using in your MO scanner.

Parameters:

_string (simple string)

Returns: - this will output, 40 different security assets within the tuple output (ie. 40 variable within the ' ') regardless of if you were including 40 assets, to be screened in the MO Screener or not. if you have less than 40 assets, then once the variables are assigned to all of the tickerIDs, the rest of the variables will be assigned "NA".

TickeridForLabelsAndSecurity(_includeExchange, _ticker)

- this export function is used to output 2 tickerID strings. One is formulated to properly work in the request.security() function while the other is how it will appear on the asset name labels depending on how you form your assets string in the MO scanners input settings. Review the tooltip next to the setting, to learn how to form the string so that the asset name labels will appear how you want in the labels at the end of the line plots & the alert labels that would be triggered if the MO Scanner is set up to include Alert Trigger Labels.

Parameters:

_includeExchange (simple bool)

_ticker (simple string)

Returns: - this export function is used to output 2 tickerID strings. One is formulated to properly work in the request.security() function while the other is how it will appear on the asset name labels depending on how you form your assets string in the MO scanners input settings. Review the tooltip next to the setting, to learn how to form the string so that the asset name labels will appear how you want in the labels at the end of the line plots & the alert labels that would be triggered if the MO Scanner is set up to include Alert Trigger Labels.

PercentChange(_startingValue, _endingValue)

- this is a quick export function to calculate how much % change has occurred between the _startingValue and the _endingValue that you input into the export function.

Parameters:

_startingValue (float)

_endingValue (float)

Returns: - it will output a single percentage value between 0-100 with trailing numbers behind a decimal. If you want, only a certain amount of numbers behind the decimal, this export function needs to be put within a formatting function to do so. Explained in the MO Scanner INTRO VIDEO.

PrintedBarCount(_time, _barCntLength, _bcPmin)

- This export function will outfit the percentage of printed bars (that occurred within _barCntLength amount of time) out of the MAX amount of bars that potentially COULD HAVE been printed. Iexplanation in the MO Scanner INTRO VIDEO.

Parameters:

_time (int)

_barCntLength (int)

_bcPmin (int)

Returns: - Gives 2 outputs. The first is the total % of Printed Bars within the user set time period and second is true/false according to if the Printed BarCount % is above the _bcPmin threshold that you input into this export function.

CandlestickPatternsLibrary "CandlestickPatterns"

This library provides a wide range of candlestick patterns, and available for user to call each pattern individually. It's a comprehensive and common tool designed for traders seeking to raise their technical analysis, and it may help users identify key turning of price action in financial instruments. Credit to public technical “*All Candlestick Patterns*” indicator.

abandonedBaby(order, d1)

The "Abandoned Baby" candlestick pattern is a bullish/bearish pattern consists of three candles.

Parameters:

order (simple string) : (simple string) Pattern order type "bull" or "bear".

d1 (simple float) : (simple float) Previous candle's body percentage out of candle range. Optional argument, default is 5.

darkCloudCover(c1, n)

The "Dark Cloud Cover" is a bearish pattern consists of two candles.

Parameters:

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

doji(d0)

The "Doji" is neither bullish or bearish consists of one candles.

Parameters:

d0 (simple float) : (simple float) Current candle's body percentage out of candle range. Optional argument, default is 5.

dojiStar(order, c1, n, d0)

The "Doji Star" is a bullish/bearish pattern consists of two candles.

Parameters:

order (simple string) : (simple string) Pattern order type "bull" or "bear" .

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

d0 (simple float) : (simple float) Current candle's body percentage out of candle range. Optional argument, default is 5.

downsideTasukiGap(c2, c1, n)

The "Downside Tasuki Gap" is a bearish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) Previous candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

dragonflyDoji(d0)

The "Dragon Fly Doji" is a bullish pattern consists of one candle.

Parameters:

d0 (simple float) : (simple float) Current candle's body percentage out of candle range. Optional argument, default is 5.

engulfing(order, c1, c0, n)

The "Engulfing" is a bullish/bearish pattern consists of two candles.

Parameters:

order (simple string) : (simple string) Pattern order type "bull" or "bear".

c1 (simple bool) : (simple bool) Previous candle's body must be lower than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

eveningDojiStar(c2, c0, d1, n)

The "Evening Doji Star" is a bearish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

d1 (simple float) : (simple float) Previous candle's body percentage out of candle range. Optional argument, default is 5.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

eveningStar(c2, c1, c0, n)

The "Evening Star" is a bearish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) Previous candle's body must be lower than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

fallingThreeMethods(c4, c3, c2, c1, c0, n)

The "Falling Three Methods" is a bearish pattern consists of five candles.

Parameters:

c4 (simple bool) : (simple bool) 5th candle ago body must be higher than average. Optional argument, default is true.

c3 (simple bool) : (simple bool) 4th candle ago body must be lower than average. Optional argument, default is true.

c2 (simple bool) : (simple bool) 3rd candle ago body must be lower than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) 2nd candle ago body must be lower than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

Returns: (bool)

fallingWindow()

The "Falling Window" is a bearish pattern consists of two candles.

gravestoneDoji(d0)

The "Gravestone Doji" is a bearish pattern consists of one candle.

Parameters:

d0 (simple float) : (simple float) Current candle's body percentage out of candle range. Optional argument, default is 5.

hammer(c0, n)

The "Hammer" is a bullish pattern consists of one candle.

Parameters:

c0 (simple bool) : (simple bool) Current candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

hangingMan(c0, n)

The "Hanging Man" is a bearish pattern consists of one candle.

Parameters:

c0 (simple bool) : (simple bool) Current candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

haramiCross(order, c1, n)

The "Harami Cross" candlestick pattern is a bullish/bearish pattern consists of two candles.

Parameters:

order (string) : (simple string) Pattern order type "bull" or "bear".

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

harami(order, c1, c0, n)

The "Harami" candlestick pattern is a bullish/bearish pattern consists of two candles.

Parameters:

order (string) : (simple string) Pattern order type "bull" or "bear"

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

invertedHammer(c0, n)

The "Inverted Hammer" is a bullish pattern consists of one candle.

Parameters:

c0 (simple bool) : (simple bool) Current candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

kicking(order, c1, c0, n)

The "Kicking" candlestick pattern is a bullish/bearish pattern consists of two candles.

Parameters:

order (string) : (simple string) Pattern order type "bull" or "bear"

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

longLowerShadow(l0)

The "Long Lower Shadow" candlestick pattern is a bullish pattern consists of one candles.

Parameters:

l0 (simple float) : (simple float) Current candle's lower wick min percentage out of candle range. Optional argument, default is 75.

longUpperShadow(u0)

The "Long Upper Shadow" candlestick pattern is a bearish pattern consists of one candles.

Parameters:

u0 (simple float) : (simple float) Current candle's upper wick min percentage out of candle range. Optional argument, default is 75.

marubozuBlack(c0, n)

The "Marubozu Black" candlestick pattern is a bearish pattern consists of one candles.

Parameters:

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

marubozuWhite(c0, n)

The "Marubozu White" candlestick pattern is a bullish pattern consists of one candles.

Parameters:

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

morningDojiStar(c2, d1, c0, n)

The "Morning Doji Star" candlestick pattern is a bullish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average. Optional argument, default is true.

d1 (simple float) : (simple float) Previous candle's body percentage out of candle range. Optional argument, default is 5.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

morningStar(c2, c1, c0, n)

The "Morning Star" candlestick pattern is a bullish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) Previous candle's body must be lower than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Cuurent candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

onNeck(c1, c0, n)

The "On Neck" candlestick pattern is a bearish pattern consists of two candles.

Parameters:

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Cuurent candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

piercing(c1, n)

The "Piercing" candlestick pattern is a bullish pattern consists of two candles.

Parameters:

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

risingThreeMethods(c4, c3, c2, c1, c0, n)

The "Rising Three Methods" candlestick pattern is a bullish pattern consists of five candles.

Parameters:

c4 (simple bool) : (simple bool) 5th candle ago body must be higher than average. Optional argument, default is true.

c3 (simple bool) : (simple bool) 4th candle ago body must be Lower than average. Optional argument, default is true.

c2 (simple bool) : (simple bool) 3rd candle ago body must be Lower than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) 2nd candle ago body must be Lower than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

risingWindow()

The "Rising Window" candlestick pattern is a bullish pattern consists of two candle.

shootingStar(c0, n)

The "Shooting Star" candlestick pattern is a bearish pattern consists of one candle.

Parameters:

c0 (simple bool) : (simple bool) Current candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

spinningTopBlack(l0, u0)

The "Spinning Top Black" is neither bullish or bearish.

Parameters:

l0 (simple float) : (simple float) Current candle's lower wick min percentage out of candle range. Optional argument, default is 34.

u0 (simple float) : (simple float) Current candle's upper wick min percentage out of candle range. Optional argument, default is 34.

spinningTopWhite(l0, u0)

The "Spinning Top White" is neither bullish or bearish.

Parameters:

l0 (simple float) : (simple float) Current candle's lower wick min percentage out of candle range. Optional argument, default is 34.

u0 (simple float) : (simple float) Current candle's upper wick min percentage out of candle range. Optional argument, default is 34.

threeBlackCrows(c2, c1, c0, n)

The "Three Black Crows" candlestick pattern is a bearish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Cuurent candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

threeWhiteSoldiers(c2, c1, c0, n)

The "Three White Soldiers" candlestick pattern is a bullish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before previous candle's body must be higher than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

c0 (simple bool) : (simple bool) Cuurent candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

triStar(order, d2, d1, d0)

The "Tri Star" candlestick pattern is a bullish/bearish pattern consists of three candles.

Parameters:

order (simple string) : (simple string) Pattern order type "bull" or "bear".

d2 (simple float) : (simple float) Before previous candle's body percentage out of candle range. Optional argument, default is 5.

d1 (simple float) : (simple float) Previous candle's body percentage out of candle range. Optional argument, default is 5.

d0 (simple float) : (simple float) Current candle's body percentage out of candle range. Optional argument, default is 5.

tweezerBottom(c1, n)

The "Tweezer Bottom" candlestick pattern is a bullish pattern consists of two candles.

Parameters:

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

tweezerTop(c1, n)

The "Tweezer Top" candlestick pattern is a bearish pattern consists of two candles.

Parameters:

c1 (simple bool) : (simple bool) Previous candle's body must be higher than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

upsideTasukiGap(c2, c1, n)

The "Tri Star" candlestick pattern is a bullish pattern consists of three candles.

Parameters:

c2 (simple bool) : (simple bool) Before Previous candle's body must be higher than average. Optional argument, default is true.

c1 (simple bool) : (simple bool) Previous candle's body must be lower than average. Optional argument, default is true.

n (simple int) : (simple int) Length of average candle's body. Optional argument, default is 14.

LibrarySupertrendLibrary "LibrarySupertrend"

selective_ma(condition, source, length)

Parameters:

condition (bool)

source (float)

length (int)

trendUp(source)

Parameters:

source (float)

smoothrng(source, sampling_period, range_mult)

Parameters:

source (float)

sampling_period (simple int)

range_mult (float)

rngfilt(source, smoothrng)

Parameters:

source (float)

smoothrng (float)

fusion(overallLength, rsiLength, mfiLength, macdLength, cciLength, tsiLength, rviLength, atrLength, adxLength)

Parameters:

overallLength (simple int)

rsiLength (simple int)

mfiLength (simple int)

macdLength (simple int)

cciLength (simple int)

tsiLength (simple int)

rviLength (simple int)

atrLength (simple int)

adxLength (simple int)

zonestrength(amplitude, wavelength)

Parameters:

amplitude (int)

wavelength (simple int)

atr_anysource(source, atr_length)

Parameters:

source (float)

atr_length (simple int)

supertrend_anysource(source, factor, atr_length)

Parameters:

source (float)

factor (float)

atr_length (simple int)

TradingToolsLibraryLibrary "TradingToolsLibrary"

Easily create advanced entries, exits, filters and qualifiers to simulate strategies. Supports DCA (Dollar Cost Averaging) Lines, Stop Losses, Take Profits (with trailing or without) & ATR.

method deepCopy(this)

This creates a deep copy instead of a shallow copy of an entry_position. This does NOT deep copy the self_pyramiding_positions array reference, since only the master entry_position needs this to track the rest of its copies for efficiency reasons. This is to prevent a feedback loop.

Namespace types: entry_position

Parameters:

this (entry_position)

Returns: entry_position

method precision_fix(this, precision)

Convert a floating point number to a precise floating point number with digit precision to avoid floating point errors in quantity calculations.

Namespace types: series float, simple float, input float, const float

Parameters:

this (float)

precision (int)

Returns: float

xSellBuyMidInterpolation(_x, _high, _low, _sellRange, _buyRange)

Creates an interpolation for a sell range and buy range but with an emphasis on reaching the _low the closer to the middle of the _sell and _buy range you go.

Parameters:

_x (float) : is the value you want to use to control interpolation bewteen the _high and _low value. This will return the lowest percentage at the mid between high and low and highest percentage at the _high and _low.

_high (float)

_low (float)

_sellRange (float)

_buyRange (float)

Returns: an interpolated float between the _high and _low supplied.

xSellBuyInterpolation(_x, _high, _low, _sellRange, _buyRange)

Creates an interpolation a sell range and buy range

Parameters:

_x (float) : is the value you want to use to control interpolation bewteen the _high and _low value.

_high (float)

_low (float)

_sellRange (float)

_buyRange (float)

Returns: an interpolated float between the _high and _low supplied.

activate_entries_and_exits(_entries, _exits, _filters, _qualifiers, _equity)

Determines activation for entries or exits. Does not place the actual orders.

Parameters:

_entries (entry_position )

_exits (exit_position )

_filters (filter )

_qualifiers (qualifier )

_equity (equity_management)

Returns: void

create_entries_and_exits(_entries, _exits, _equity)

Creates actual entry and exit orders if activated

Parameters:

_entries (entry_position )

_exits (exit_position )

_equity (equity_management)

Returns: void

filter

Fields:

disabled (series__bool)

filter_for_entries_or_exits (series__string)

filter_for_groups (series__string)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

qualifier

Fields:

disabled (series__bool)

qualify_for_entries_or_exits (series__string)

qualify_for_groups (series__string)

disqualify (series__bool)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

expire_after_x_bars (series__integer)

use_expire_after_x_bars (series__bool)

use_expire_condition (series__bool)

use_override_expire_condition (series__bool)

expire_condition_operator (series__string)

expire_condition_source (series__float)

expire_compare_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_activate_value (series__string)

active (series__bool)

expire_after_bars_bar_index (series__integer)

expire_after_bars_bar_index_prior (series__integer)

expire_bar_count (series__integer)

expire_bar_changed (series__bool)

entry_position

Fields:

disabled (series__bool)

activate (series__bool)

active (series__bool)

override_occured (series__bool)

passDebug (array__bool)

initial_activation_price (series__float)

dca_done (series__bool)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

use_cash (series__bool)

use_percent_equity (series__bool)

percent_equity_amount (series__float)

cash_amount (series__float)

position_size (series__float)

total_position_size (series__float)

prior_total_position_size (series__float)

equity_remaining (series__float)

prior_equity_remaining (series__float)

initial_equity (series__float)

use_martingale (series__bool)

martingale_win_ratio (series__float)

martingale_lose_ratio (series__float)

martingale_win_limit (series__integer)

martingale_lose_limit (series__integer)

martingale_limit_reset_mode (series__string)

use_dynamic_percent_equity (series__bool)

dynamic_percent_equity_amount (series__float)

initial_dynamic_percent_equity_amount (series__float)

dynamic_percent_equity_source (series__float)

dynamic_percent_equity_min (series__float)

dynamic_percent_equity_max (series__float)

dynamic_percent_equity_source_sell_range (series__float)

dynamic_percent_equity_source_buy_range (series__float)

dynamic_equity_interpolation_method (series__string)

total_bars (series__integer)

bar_index_at_activate (series__integer)

bars_since_active (series__integer)

time_at_activate (series__integer)

time_since_active (series__integer)

bar_index_at_activated (series__integer)

bar_index_at_pyramid_change (series__integer)

name (series__string)

id (series__string)

group (series__string)

pyramiding_limit (series__integer)

self_pyramiding_limit (series__integer)

self_pyramiding_positions (array__|entry_position|#OBJ)

new_pyramid_cancels_dca (series__bool)

num_active_long_positions (series__integer)

num_active_short_positions (series__integer)

num_active_positions (series__integer)

position_remaining (series__float)

prior_position_remaining (series__float)

direction (series__string)

allow_flip_position (series__bool)

flip_occurred (series__bool)

ignore_flip (series__bool)

use_dca (series__bool)

dca_use_limit (series__bool)

dca_num_positions (series__integer)

dca_positions (array__float)

dca_deviation_percentage (series__float)

dca_scale (series__float)

dca_percentages (series__string)

dca_close_cancels (series__bool)

dca_active_positions (series__integer)

use_atr_deviation (series__bool)

dca_atr_length (series__integer)

dca_atr_mult (series__float)

dca_atr_updates_dca_positions (series__bool)

close_price_at_order (series__float)

dca_use_deviation_atr_min (series__bool)

dca_position_quantities (array__float)

use_dca_dynamic_percent_equity (series__bool)

dca_in_use (array__bool)

dca_activated (array__bool)

dca_money_used (array__float)

dca_lines (array__line)

dca_color (series__color)

show_dca_lines (series__bool)

atr_value (series__float)

atr_value_at_activation (series__float)

use_cooldown_bars (series__bool)

cooldown_bars (series__integer)

cooldown_bar_changed (series__bool)

cooldown_bar_index (series__integer)

cooldown_bar_index_prior (series__integer)

cooldown_bar_change_count (series__integer)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

exit_position

Fields:

disabled (series__bool)

id (series__string)

group (series__string)

exit_for_entries (series__string)

exit_for_groups (series__string)

total_bars (series__integer)

name (series__string)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

activate (series__bool)

active (series__bool)

reset_equity (series__bool)

use_limit (series__bool)

use_alerts (series__bool)

reset_entry_cooldowns (series__bool)

prevent_new_entries_on_partial_close (series__bool)

show_activation_zone (series__bool)

use_average_position (series__bool)

source_value (series__float)

trigger_x_times (series__integer)

amount_of_times_triggered (series__integer)

quantity_percent (series__float)

trade_qty (series__float)

exit_amount (series__float)

entries_exiting_for (array__|entry_position|#OBJ)

atr_value (series__float)

update_atr (series__bool)

use_activate_after_bars (series__bool)

show_activate_after_bars (series__bool)

activate_after_bars (series__integer)

activate_after_bars_bar_changed (series__bool)

activate_after_bars_bar_index (series__integer)

activate_after_bars_bar_index_prior (series__integer)

activate_after_bars_bar_change_count (series__integer)

all_conditions_pass (series__bool)

use_close_if_profit_only (series__bool)

profit_value (series__float)

exit_type (series__string)

exit_modifier (series__string)

update_atr_with_new_pyramid (series__bool)

percentage (series__float)

activation_percentage (series__float)

atr_multiplier (series__float)

use_cancel_if_percent (series__bool)

cancel_if_percent (series__float)

activation_value (series__float)

activation_value_crossed (series__bool)

exit_value (series__float)

hypo_long_exit_value (series__float)

hypo_short_exit_value (series__float)

close_exit_value (series__float)

debug (series__float)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

equity_management

Fields:

equity (series__float)

prior_equity (series__float)

position_used (series__float)

prior_position_used (series__float)

prevent_future_entries (series__bool)

minimum_order_size (series__float)

decimal_rounding_precision (series__integer)

direction (series__string)

show_order_info_in_comments (series__bool)

show_order_info_in_labels (series__bool)

allow_longs (series__bool)

allow_shorts (series__bool)

override_occured (series__bool)

flip_occured (series__bool)

num_concurrent_wins (series__integer)

num_concurrent_losses (series__integer)

first_entry (|entry_position|#OBJ)

num_win_trades (series__integer)

num_losing_trades (series__integer)

JapaneseCandlestickPatternsLibrary "JapaneseCandlestickPatterns"

Japanese Candlestick Patterns is a library of functions that enables the detection of popular Japanese candlestick patterns such as Doji, Hammer, and Engulfing, among others. The library provides a simple yet powerful way to analyze financial markets and make informed trading decisions. Japanese Candlestick Patterns library can help you identify potential trading opportunities.

isDojiCandle()

isGravestoneDojiCandle()

isDragonflyDojiCandle()

isEveningDojiStarCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isLongLeggedDojiCandle()

isMorningDojiStarCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isBullishCounterattackLinesCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isBearishCounterattackLinesCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isDarkCloudCoverCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isBullishEngulfingCandle()

isBearishEngulfingCandle()

isHammerCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isHangingManCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isHaramiBearishCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isHaramiBullishCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isInNeckCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isOnNeckCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isPiercingCandle(isDownTrend)

Parameters:

isDownTrend (bool)

threeBlackCrowsCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isThrustingNeckCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isUpsideGapTwoCrowsCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isAbandonedBabyTopCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isAbandonedBabyBottomCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isEveningStarCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isInvertedHammerCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isMorningStarCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isShootingStarCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isRisingThreeMethodsCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isFallingThreeMethodsCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isUpsideTasukiGapCandle(isUpTrend)

Parameters:

isUpTrend (bool)

isDownsideGapTasukiCandle(isDownTrend)

Parameters:

isDownTrend (bool)

isLongLowerShadowCandle()

isLongUpperShadowCandle()

gFancyMALibrary "gFancyMA"

printLbl(y, x, c, m, b, s)

Parameters:

y (float)

x (int)

c (color)

m (string)

b (bool)

s (string)

debugLibrary "debug"

Show Array or Matrix Elements In Table

Use anytime you want to see the elements in an array or a matrix displayed.

Effective debugger, particularly for strategies and complex logic structures.

Look in code to find instructions. Reach out if you need assistance.

Functionality includes:

Viewing the contents of an array or matrix on screen.

Track variables and variable updates using debug()

Track if and when local scopes fire using debugs()

Types Allowed:

string

float

int

string

debug(_col, _row, _name, _value, _msg, _ip)

Debug Variables in Matrix

Parameters:

_col (int) : (int) Assign Column

_row (int) : (int) Assign Row

_name (matrix) : (simple matrix) Matrix Name

_value (string) : (string) Assign variable as a string (str.tostring())

_msg (string)

_ip (int) : (int) (default 1) 1 for continuous updates. 2 for barstate.isnew updates. 3 for barstate.isconfirmed updates. -1 to only add once

Returns: Returns Variable _value output and _msg formatted as '_msg: variableOutput' in designated column and row

debug(_col, _row, _name, _value, _msg, _ip)

Parameters:

_col (int)

_row (int)

_name (matrix)

_value (float)

_msg (string)

_ip (int)

debug(_col, _row, _name, _value, _msg, _ip)

Parameters:

_col (int)

_row (int)

_name (matrix)

_value (int)

_msg (string)

_ip (int)

debug(_col, _row, _name, _value, _msg, _ip)

Parameters:

_col (int)

_row (int)

_name (matrix)

_value (bool)

_msg (string)

_ip (int)

debugs(_col, _row, _name, _msg)

Debug Scope in Matrix - Identify When Scope Is Accessed

Parameters:

_col (int) : (int) Column Number

_row (int) : (int) Row Number

_name (matrix) : (simple matrix) Matrix Name

_msg (string) : (string) Message

Returns: Message appears in debug panel using _col/_row as the identifier

viewArray(_arrayName, _pos, _txtSize, _tRows, s_index, s_border, _rowCol, bCol, _fillCond, _offset)

Array Element Display (Supports float , int , string , and bool )

Parameters:

_arrayName (float ) : ID of Array to be Displayed

_pos (string) : Position for Table

_txtSize (string) : Size of Table Cell Text

_tRows (int) : Number of Rows to Display Data In (columns will be calculated accordingly)

s_index (bool) : (Optional. Default True.) Show/Hide Index Numbers

s_border (bool) : (Optional. Default False.) Show/Hide Border

_rowCol (string)

bCol (color) : = (Optional. Default Black.) Frame/Border Color.

_fillCond (bool) : (Optional) Conditional statement. Function displays array only when true. For instances where size is not immediately known or indices are na. Default = true, indicating array size is set at bar_index 0.

_offset (int) : (Optional) Use to view historical array states. Default = 0, displaying realtime bar.

Returns: A Display of Array Values in a Table

viewArray(_arrayName, _pos, _txtSize, _tRows, s_index, s_border, _rowCol, bCol, _fillCond, _offset)

Parameters:

_arrayName (int )

_pos (string)

_txtSize (string)

_tRows (int)

s_index (bool)

s_border (bool)

_rowCol (string)

bCol (color)

_fillCond (bool)

_offset (int)

viewArray(_arrayName, _pos, _txtSize, _tRows, s_index, s_border, _rowCol, bCol, _fillCond, _offset)

Parameters:

_arrayName (string )

_pos (string)

_txtSize (string)

_tRows (int)

s_index (bool)

s_border (bool)

_rowCol (string)

bCol (color)

_fillCond (bool)

_offset (int)

viewArray(_arrayName, _pos, _txtSize, _tRows, s_index, s_border, _rowCol, bCol, _fillCond, _offset)

Parameters:

_arrayName (bool )

_pos (string)

_txtSize (string)

_tRows (int)

s_index (bool)

s_border (bool)

_rowCol (string)

bCol (color)

_fillCond (bool)

_offset (int)

viewMatrix(_matrixName, _pos, _txtSize, s_index, _resetIdx, s_border, bCol, _fillCond, _offset)

Matrix Element Display (Supports , , , and )

Parameters:

_matrixName (matrix) : ID of Matrix to be Displayed

_pos (string) : Position for Table

_txtSize (string) : Size of Table Cell Text

s_index (bool) : (Optional. Default True.) Show/Hide Index Numbers

_resetIdx (bool)

s_border (bool) : (Optional. Default False.) Show/Hide Border

bCol (color) : = (Optional. Default Black.) Frame/Border Color.

_fillCond (bool) : (Optional) Conditional statement. Function displays matrix only when true. For instances where size is not immediately known or indices are na. Default = true, indicating matrix size is set at bar_index 0.

_offset (int) : (Optional) Use to view historical matrix states. Default = 0, displaying realtime bar.

Returns: A Display of Matrix Values in a Table

viewMatrix(_matrixName, _pos, _txtSize, s_index, _resetIdx, s_border, bCol, _fillCond, _offset)

Parameters:

_matrixName (matrix)

_pos (string)

_txtSize (string)

s_index (bool)

_resetIdx (bool)

s_border (bool)

bCol (color)

_fillCond (bool)

_offset (int)

viewMatrix(_matrixName, _pos, _txtSize, s_index, _resetIdx, s_border, bCol, _fillCond, _offset)

Parameters:

_matrixName (matrix)

_pos (string)

_txtSize (string)

s_index (bool)

_resetIdx (bool)

s_border (bool)

bCol (color)

_fillCond (bool)

_offset (int)

viewMatrix(_matrixName, _pos, _txtSize, s_index, _resetIdx, s_border, bCol, _fillCond, _offset)

Parameters:

_matrixName (matrix)

_pos (string)

_txtSize (string)

s_index (bool)

_resetIdx (bool)

s_border (bool)

bCol (color)

_fillCond (bool)

_offset (int)

ATR_InfoWhat Is the Average True Range (ATR)?

The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

Each instrument per unit of time passes its average value of the true range, but there are moments when the volatility explodes or abruptly decays, these phenomena introduce large distortions into the average value of the true range.

The ATR_WPB function calculates the average value of the true range for the specified number of bars, while excluding paranormally large and paranormally small bars from the calculation of the average.

For example, if the instrument has passed a small ATR value, then it has many chances to continue moving, but if the instrument has passed its ATR value, then the chances of continuing to move are extremely low.

Library "ATR_Info"

ATR_Info: Calculates ATR without paranormal bars

ATR_WPB(source, period, psmall, pbig)

ATR_WPB: Calculates ATR without paranormal bars

Parameters:

source (float) : ATR_WPB: (series float) The sequence of data on the basis of which the ATP calculation will be made

period (int) : ATR_WPB: (int) Sequence size for ATR calculation

psmall (float) : ATR_WPB: (float) Coefficient for paranormally small bar

pbig (float) : ATR_WPB: (float) Coefficient for paranormally big bar

Returns: ATR_WPB: (float) ATR without paranormal bars

CandlesGroup_TypesLibrary "CandlesGroup_Types"

CandlesGroup Type allows you to efficiently store and access properties of all the candles in your chart.

You can easily manipulate large datasets, work with multiple timeframes, or analyze multiple symbols simultaneously. By encapsulating the properties of each candle within a CandlesGroup object, you gain a convenient and organized way to handle complex candlestick patterns and data.

For usage instructions and detailed examples, please refer to the comments and examples provided in the source code.

method init(_self)

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup)

method init(_self, propertyNames)

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup)

propertyNames (string )

method get(_self, key)

get values array from a given property name

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

key (string) : : key name of selected property. Default is "index"

Returns: values array

method size(_self)

get size of values array. By default it equals to current bar_index

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

Returns: size of values array

method push(_self, key, value)

push single value to specific property

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

key (string) : : key name of selected property

value (float) : : property value

Returns: CandlesGroup object

method push(_self, arr)

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup)

arr (float )

method populate(_self, ohlc)

populate ohlc to CandlesGroup

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

ohlc (float ) : : array of ohlc

Returns: CandlesGroup object

method populate(_self, values, propertiesNames)

populate values base on given properties Names

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

values (float ) : : array of property values

propertiesNames (string ) : : an array stores property names. Use as keys to get values

Returns: CandlesGroup object

method populate(_self)

populate values (default setup)

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

Returns: CandlesGroup object

method lookback(arr, bars_lookback)

get property value on previous candles. For current candle, use *.lookback()

Namespace types: float

Parameters:

arr (float ) : : array of selected property values

bars_lookback (int) : : number of candles lookback. 0 = current candle. Default is 0

Returns: single property value

method highest_within_bars(_self, hiSource, start, end, useIndex)

get the highest property value between specific candles

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

hiSource (string) : : key name of selected property

start (int) : : start bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true

end (int) : : end bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true. Default is 0

useIndex (bool) : : use index instead of lookback value. Default = false

Returns: the highest value within candles

method highest_within_bars(_self, returnWithIndex, hiSource, start, end, useIndex)

get the highest property value and bar index between specific candles

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

returnWithIndex (bool) : : the function only applicable when it is true

hiSource (string) : : key name of selected property

start (int) : : start bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true

end (int) : : end bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true. Default is 0

useIndex (bool) : : use index instead of lookback value. Default = false

Returns:

method highest_point_within_bars(_self, hiSource, start, end, useIndex)

get a Point object which contains highest property value between specific candles

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

hiSource (string) : : key name of selected property

start (int) : : start bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true

end (int) : : end bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true. Default is 0

useIndex (bool) : : use index instead of lookback value. Default = false

Returns: Point object contains highest property value

method lowest_within_bars(_self, loSource, start, end, useIndex)

get the lowest property value between specific candles

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

loSource (string) : : key name of selected property

start (int) : : start bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true

end (int) : : end bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true. Default is 0

useIndex (bool) : : use index instead of lookback value. Default = false

Returns: the lowest value within candles

method lowest_within_bars(_self, returnWithIndex, loSource, start, end, useIndex)

get the lowest property value and bar index between specific candles

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

returnWithIndex (bool) : : the function only applicable when it is true

loSource (string) : : key name of selected property

start (int) : : start bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true

end (int) : : end bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true. Default is 0

useIndex (bool) : : use index instead of lookback value. Default = false

Returns:

method lowest_point_within_bars(_self, loSource, start, end, useIndex)

get a Point object which contains lowest property value between specific candles

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

loSource (string) : : key name of selected property

start (int) : : start bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true

end (int) : : end bar for calculation. Default is candles lookback value from current candle. 'index' value is used if 'useIndex' = true. Default is 0

useIndex (bool) : : use index instead of lookback value. Default = false

Returns: Point object contains lowest property value

method time2bar(_self, t)

Convert UNIX time to bar index of active chart

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

t (int) : : UNIX time

Returns: bar index

method time2bar(_self, timezone, YYYY, MMM, DD, hh, mm, ss)

Convert timestamp to bar index of active chart. User defined timezone required

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

timezone (string) : : User defined timezone

YYYY (int) : : Year

MMM (int) : : Month

DD (int) : : Day

hh (int) : : Hour. Default is 0

mm (int) : : Minute. Default is 0

ss (int) : : Second. Default is 0

Returns: bar index

method time2bar(_self, YYYY, MMM, DD, hh, mm, ss)

Convert timestamp to bar index of active chart

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

YYYY (int) : : Year

MMM (int) : : Month

DD (int) : : Day

hh (int) : : Hour. Default is 0

mm (int) : : Minute. Default is 0

ss (int) : : Second. Default is 0

Returns: bar index

method get_prop_from_time(_self, key, t)

get single property value from UNIX time

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

key (string) : : key name of selected property

t (int) : : UNIX time

Returns: single property value

method get_prop_from_time(_self, key, timezone, YYYY, MMM, DD, hh, mm, ss)

get single property value from timestamp. User defined timezone required

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

key (string) : : key name of selected property

timezone (string) : : User defined timezone

YYYY (int) : : Year

MMM (int) : : Month

DD (int) : : Day

hh (int) : : Hour. Default is 0

mm (int) : : Minute. Default is 0

ss (int) : : Second. Default is 0

Returns: single property value

method get_prop_from_time(_self, key, YYYY, MMM, DD, hh, mm, ss)

get single property value from timestamp

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

key (string) : : key name of selected property

YYYY (int) : : Year

MMM (int) : : Month

DD (int) : : Day

hh (int) : : Hour. Default is 0

mm (int) : : Minute. Default is 0

ss (int) : : Second. Default is 0

Returns: single property value

method bar2time(_self, index)

Convert bar index of active chart to UNIX time

Namespace types: CandlesGroup

Parameters:

_self (CandlesGroup) : : CandlesGroup object

index (int) : : bar index

Returns: UNIX time

Point

A point on chart

Fields:

price (series float) : : price value

bar (series int) : : bar index

bartime (series int) : : time in UNIX format of bar

Property

Property object which contains values of all candles

Fields:

name (series string) : : name of property

values (float ) : : an array stores values of all candles. Size of array = bar_index

CandlesGroup

Candles Group object which contains properties of all candles

Fields:

propertyNames (string ) : : an array stores property names. Use as keys to get values

properties (Property ) : : array of Property objects

gFancyMALibrary "GalacticS2021"

printLbl(y, x, c, m, b)

Parameters:

y (float)

x (int)

c (color)

m (string)

b (bool)

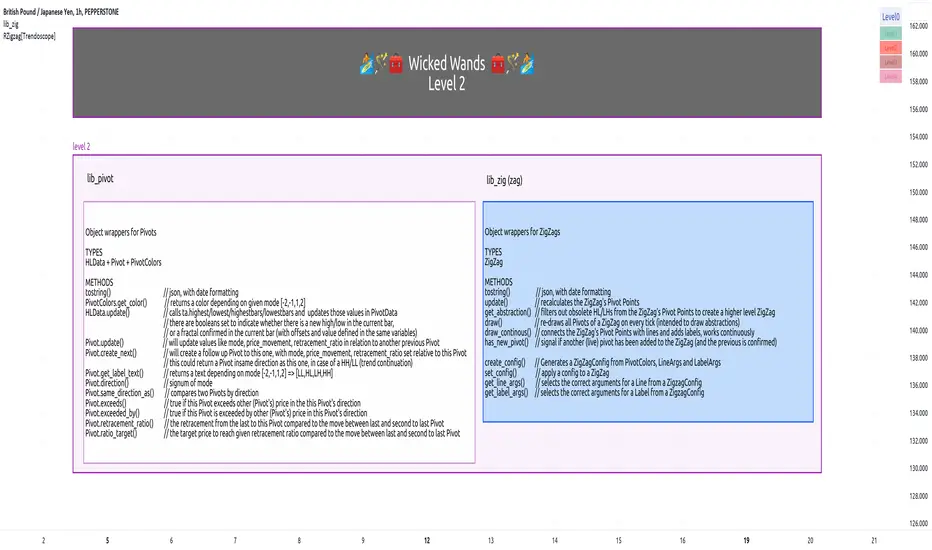

lib_zigLibrary "lib_zig"

Object oriented implementation of ZigZag

method tostring(this, date_format)

Namespace types: Zigzag

Parameters:

this (Zigzag)

date_format (simple string)

method update(this)

Namespace types: Zigzag

Parameters:

this (Zigzag)

method draw(this, colors)

Namespace types: Zigzag

Parameters:

this (Zigzag)

colors (PivotColors type from robbatt/lib_pivot/19)

Zigzag

Fields:

max_pivots (series__integer)

hldata (|robbatt/lib_pivot/19;HLData|#OBJ)

pivots (array__|robbatt/lib_pivot/19;Pivot|#OBJ)

lib_pivotLibrary "lib_pivot"

Object oriented implementation of Pivot methods.

method tostring(this)

Converts HLData to a json string representation

Namespace types: HLData

Parameters:

this (HLData) : HLData

Returns: string representation of Pivot

method tostring(this, date_format)

Namespace types: Pivot

Parameters:

this (Pivot)

date_format (simple string)

method tostring(this, date_format)

Namespace types: Pivot

Parameters:

this (Pivot )

date_format (simple string)

method get_color(this, mode)

Namespace types: PivotColors

Parameters:

this (PivotColors)

mode (int)

method get_label_text(this)

Namespace types: Pivot

Parameters:

this (Pivot)

method direction(this)

Namespace types: Pivot

Parameters:

this (Pivot)

method same_direction_as(this, other)

Namespace types: Pivot

Parameters:

this (Pivot)

other (Pivot)

method exceeds(this, price)

Namespace types: Pivot

Parameters:

this (Pivot)

price (float)

method exceeds(this, other)

Namespace types: Pivot

Parameters:

this (Pivot)

other (Pivot)

method exceeded_by(this, price)

Namespace types: Pivot

Parameters:

this (Pivot)

price (float)

method exceeded_by(this, other)

Namespace types: Pivot

Parameters:

this (Pivot)

other (Pivot)

method retracement_ratio(this, lastPivot, sec_lastPivot)

Namespace types: Pivot

Parameters:

this (Pivot)

lastPivot (Pivot)

sec_lastPivot (Pivot)

ratio_target(sec_lastPivot, lastPivot, target_ratio)

Parameters:

sec_lastPivot (Pivot)

lastPivot (Pivot)

target_ratio (float)

method update(this, ref_highest, ref_lowest)

Namespace types: HLData

Parameters:

this (HLData)

ref_highest (float)

ref_lowest (float)

method update(this, bar_time, bar_idx, price, prev)

Namespace types: Pivot

Parameters:

this (Pivot)

bar_time (int)

bar_idx (int)

price (float)

prev (Pivot)

method create_next(this, bar_time, bar_idx, price)

Namespace types: Pivot

Parameters:

this (Pivot)

bar_time (int)

bar_idx (int)

price (float)

HLData

HLData wraps the data received from ta.highest, ta.highestbars, ta.lowest, ta.lowestbars, as well as the reference sources

Fields:

length (series int) : lookback length for pivot points

highest_offset (series int) : offset to highest value bar

lowest_offset (series int) : offset to lowest value bar

highest (series float) : highest value within lookback bars

lowest (series float) : lowest value within lookback bars

new_highest (series bool) : update() will set this true if the current candle forms a new highest high at the last (current) bar of set period (length)

new_lowest (series bool) : update() will set this true if the current candle forms a new lowest low at the last (current) bar of set period (length)

new_highest_fractal (series bool) : update() will set this true if the current candle forms a new fractal high at the center of set period (length)

new_lowest_fractal (series bool) : update() will set this true if the current candle forms a new fractal low at the center of set period (length)

PivotColors

Pivot colors for different modes

Fields:

hh (series color) : Color for Pivot mode 2 (HH)

lh (series color) : Color for Pivot mode 1 (LH)

hl (series color) : Color for Pivot mode -1 (HL)

ll (series color) : Color for Pivot mode -2 (LL)

Pivot

Pivot additional pivot data around basic Point

Fields:

point (Point type from robbatt/lib_plot_objects/5)

mode (series int) : can be -2/-1/1/2 for LL/HL/LH/HH

price_movement (series float) : The price difference between this and the previous pivot point in the opposite direction

retracement_ratio (series float) : The ratio between this price_movement and the previous

prev (Pivot)

Global_Public_Holidays_23_24Library "Global_Public_Holidays_23_24"

NYSE_closed()

LSE_closed()

JPX_closed()

ASX_closed()

FX_closed()

lib_plot_objectsLibrary "lib_plot_objects"

library wrapping basic builtin object constructors, to be able to do calculations with points/lines/boxes/triangles/polygons via libraries and on securities. inspired by Trendoscope's ( and ) with added update mechanism to not have to recreate objects on every iteration for continously drawn items, automated xloc selection for coordinates, compatibility check for Points, added Triangle and Polygon types, object reflection via tostring to valid json (logging via webhook)

method assert_same_xloc(a, b, test)

checks two points for compatibility, i.e. having the same xloc

Namespace types: Point

Parameters:

a (Point)

b (Point)

test (Test type from robbatt/lib_unit/6)

method assert_same_xloc(a, b, test)

checks two lines for compatibility, i.e. having the same xloc

Namespace types: Line

Parameters:

a (Line)

b (Line)

test (Test type from robbatt/lib_unit/6)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: LineArgs

Parameters:

args (LineArgs)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: LabelArgs

Parameters:

args (LabelArgs)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: BoxArgs

Parameters:

args (BoxArgs)

method or_default(args)

checks args oject for being na, if so, provide a default instead

Namespace types: BoxTextArgs

Parameters:

args (BoxTextArgs)

method x(point, xloc)

automatically returns the correct x coordinate, based on the point's set xloc

Namespace types: Point

Parameters:

point (Point)

xloc (string)

method tostring(this, date_format)

converts object to json representation

Namespace types: Point

Parameters:

this (Point)

date_format (string)

method tostring(this, date_format)

converts object to json representation

Namespace types: Point

Parameters:

this (Point )

date_format (string)

method tostring(this)

converts object to json representation

Namespace types: LineArgs

Parameters:

this (LineArgs)

method tostring(this, date_format)

converts object to json representation

Namespace types: Line

Parameters:

this (Line)

date_format (string)

method tostring(this)

Namespace types: LabelArgs

Parameters:

this (LabelArgs)

method tostring(this, date_format)

Namespace types: Label

Parameters:

this (Label)

date_format (string)

method tostring(this, date_format)

Namespace types: LineFill

Parameters:

this (LineFill)

date_format (string)

method tostring(this)

Namespace types: BoxArgs

Parameters:

this (BoxArgs)

method tostring(this)

Namespace types: BoxTextArgs

Parameters:

this (BoxTextArgs)

method tostring(this, date_format)

Namespace types: Box

Parameters:

this (Box)

date_format (string)

method tostring(this, date_format)

Namespace types: Triangle

Parameters:

this (Triangle)

date_format (string)

method tostring(this, date_format)

Namespace types: TriangleFill

Parameters:

this (TriangleFill)

date_format (string)

method tostring(this, date_format)

Namespace types: Polygon

Parameters:

this (Polygon)

date_format (string)

method tostring(this, date_format)

Namespace types: PolygonFill

Parameters:

this (PolygonFill)

date_format (string)

method tostring(this, date_format)

Namespace types: Line

Parameters:

this (Line )

date_format (string)

method tostring(this, date_format)

Namespace types: Box

Parameters:

this (Box )

date_format (string)

method tostring(this, date_format)

Namespace types: Triangle

Parameters:

this (Triangle )

date_format (string)

method tostring(this, date_format)

Namespace types: Polygon

Parameters:

this (Polygon )

date_format (string)

method tostring(this, date_format)

Namespace types: PolygonFill

Parameters:

this (PolygonFill )

date_format (string)

method create_center(points)

Namespace types: Point

Parameters:

points (Point )

method create_center(this, other)

Namespace types: Point

Parameters:

this (Point)

other (Point)

method create_center(this)

Namespace types: Line

Parameters:

this (Line)

method create_line(this, other, args)

Namespace types: Point

Parameters:

this (Point)

other (Point)

args (LineArgs)

method create_triangle(this, b, c, args)

Namespace types: Point

Parameters:

this (Point)

b (Point)

c (Point)

args (LineArgs)

method create_triangle(this, c)

Namespace types: Line

Parameters:

this (Line)

c (Point)

method create_box(this, other, txt, args, text_args)

Namespace types: Point

Parameters:

this (Point)

other (Point)

txt (string)

args (BoxArgs)

text_args (BoxTextArgs)

method create_box(this, txt, args, text_args)

Namespace types: Line

Parameters:

this (Line)

txt (string)

args (BoxArgs)

text_args (BoxTextArgs)

method create_polygon(points, args)

Namespace types: Point

Parameters:

points (Point )

args (LineArgs)

method create_polygon(start, others, args)

Namespace types: Point

Parameters:

start (Point)

others (Point )

args (LineArgs)

method create_fill(this, other, fill_color)

Namespace types: Line

Parameters:

this (Line)

other (Line)

fill_color (color)

method create_fill(this, fill_color)

Namespace types: Triangle

Parameters:

this (Triangle)

fill_color (color)

method create_fill(this, fill_color)

Namespace types: Polygon

Parameters:

this (Polygon)

fill_color (color)

method create_label(this, txt, args, tooltip)

Namespace types: Point

Parameters:

this (Point)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Line

Parameters:

this (Line)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Box

Parameters:

this (Box)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Triangle

Parameters:

this (Triangle)

txt (string)

args (LabelArgs)

tooltip (string)

method create_label(this, txt, args, tooltip)

Namespace types: Polygon

Parameters:

this (Polygon)

txt (string)

args (LabelArgs)

tooltip (string)

method update(this, bar_time, bar_idx, price)

Namespace types: Point

Parameters:

this (Point)

bar_time (int)

bar_idx (int)

price (float)

method update(this, update)

Namespace types: Point

Parameters:

this (Point)

update (Point)

method update(this, point)

Namespace types: Label

Parameters:

this (Label)

point (Point)

method update(this, start, end)

Namespace types: Line

Parameters:

this (Line)

start (Point)

end (Point)

method update(this, left_top, right_bottom)

Namespace types: Box

Parameters:

this (Box)

left_top (Point)

right_bottom (Point)

method update(this, a, b, c)

Namespace types: Triangle

Parameters:

this (Triangle)

a (Point)

b (Point)

c (Point)

method update(this, points)

Namespace types: Polygon

Parameters:

this (Polygon)

points (Point )

method delete(this)

Namespace types: Line

Parameters:

this (Line)

method delete(this)

Namespace types: Label

Parameters:

this (Label)

method delete(this)

Namespace types: LineFill

Parameters:

this (LineFill)

method delete(this)

Namespace types: Box

Parameters:

this (Box)

method delete(this)

Namespace types: TriangleFill

Parameters:

this (TriangleFill)

method delete(this)

Namespace types: Triangle

Parameters:

this (Triangle)

method delete(this)

Namespace types: Polygon

Parameters:

this (Polygon)

method delete(this)

Namespace types: PolygonFill

Parameters:

this (PolygonFill)

method delete(this)

Namespace types: Line

Parameters:

this (Line )

method delete(this)

Namespace types: Label

Parameters:

this (Label )

method delete(this)

Namespace types: LineFill

Parameters:

this (LineFill )

method delete(this)

Namespace types: Box

Parameters:

this (Box )

method delete(this)

Namespace types: TriangleFill

Parameters:

this (TriangleFill )

method delete(this)

Namespace types: Polygon

Parameters:

this (Polygon )

method delete(this)

Namespace types: Triangle

Parameters:

this (Triangle )

method delete(this)

Namespace types: PolygonFill

Parameters:

this (PolygonFill )

method draw(this)

Namespace types: Label

Parameters:

this (Label)

method draw(this)

Namespace types: Line

Parameters:

this (Line)

method draw(this)

Namespace types: Box

Parameters:

this (Box)

method draw(this)

Namespace types: Triangle

Parameters:

this (Triangle)

method draw(this)

Namespace types: Polygon

Parameters:

this (Polygon)

method draw(this)

Namespace types: LineFill

Parameters:

this (LineFill)

method draw(this)

Namespace types: TriangleFill

Parameters:

this (TriangleFill)

method draw(this)

Namespace types: PolygonFill

Parameters:

this (PolygonFill)

Point

Fields:

bar_time (series int) : time based x coordinate

bar_idx (series int) : bar index based x coordinate

price (series float) : price based y coordinate

xloc (series string) : To select if x coordinate is represented by bar_idx or bar_time. Possible values: xloc.bar_index and xloc.bar_time. Default is xloc.bar_index.

LabelArgs

Fields:

text_color (series color) : Text color.

bg_color (series color) : Color of the label border and arrow.

text_font_family (series string) : The font family of the text. Optional. The default value is font.family_default. Possible values: font.family_default, font.family_monospace.

yloc (series string) : Possible values are yloc.price, yloc.abovebar, yloc.belowbar. If yloc=yloc.price, y argument specifies the price of the label position. If yloc=yloc.abovebar, label is located above bar. If yloc=yloc.belowbar, label is located below bar. Default is yloc.price.

style (series string) : Label style. Possible values: label.style_none, label.style_xcross, label.style_cross, label.style_triangleup, label.style_triangledown, label.style_flag, label.style_circle, label.style_arrowup, label.style_arrowdown, label.style_label_up, label.style_label_down, label.style_label_left, label.style_label_right, label.style_label_lower_left, label.style_label_lower_right, label.style_label_upper_left, label.style_label_upper_right, label.style_label_center, label.style_square, label.style_diamond, label.style_text_outline. Default is label.style_label_down.

size (series string) : Label size. Possible values: size.auto, size.tiny, size.small, size.normal, size.large, size.huge. Default value is size.normal.

text_align (series string) : Label text alignment. Possible values: text.align_left, text.align_center, text.align_right. Default value is text.align_center.

Label

Fields:

point (Point) : The Label coordinates

txt (series string) : Label text. Default is empty string.

args (LabelArgs) : Wrapper for reusable arguments for label.new()

tooltip (series string) : Hover to see tooltip label.

plot (series label) : The label object to be added and plotted via draw()

LineArgs

Fields:

line_color (series color) : Line color.

style (series string) : Line style. Possible values: line.style_solid, line.style_dotted, line.style_dashed, line.style_arrow_left, line.style_arrow_right, line.style_arrow_both.

width (series int) : Line width in pixels.

extend (series string) : f extend=extend.none, draws segment starting at point (x1, y1) and ending at point (x2, y2). If extend is equal to extend.right or extend.left, draws a ray starting at point (x1, y1) or (x2, y2), respectively. If extend=extend.both, draws a straight line that goes through these points. Default value is extend.none.

Line

Fields:

start (Point) : starting point of the line

end (Point)

args (LineArgs) : Wrapper for reusable arguments for line.new()

plot (series line) : The line object to be added and plotted via draw()

LineFill

Fields:

a (Line) : The first Line object

b (Line) : The second Line object

fill_color (series color) : The color used to fill the space between the lines.

plot (series linefill) : The linefill object to be added and plotted via draw()

BoxArgs

Fields:

border_color (series color) : Color of the four borders. Optional. The default is color.blue.

border_width (series int) : Width of the four borders, in pixels. Optional. The default is 1 pixel.

border_style (series string) : Style of the four borders. Possible values: line.style_solid, line.style_dotted, line.style_dashed. Optional. The default value is line.style_solid.

bg_color (series color) : Background color of the box. Optional. The default is color.blue.