TradingWolf Premium OscillatorsThe TradingWolf Premium Oscillators is a unique and enhanced selection of oscillators designed to help give you an edge on the markets.

Within this one indicator you will have access to RSI, Stochastic, MACD, Awesome Oscillator, Wavetrend, Zig Zag Pivots and DPO.

Including Divergence and Hidden Divergence signals for them.

Below each indicator is explained along with its enhancements to help you understand it better.

This script comes with the 'TradingWolf Premium' to get access, read the Author’s Instructions below.

There are extensive explanations on how to use these oscillators in our documentation on the website but we will give a simple overview here.

RSI

We try not to mess with these too much because if used correctly, they are very powerful tools. The main differences you will notice is that we have highlighted the areas where you should be paying attention to the oscillator with reversal/continuation zones.

The most popular feature from these will be the 4 divergences which can be toggled on or off in the settings.

Stochastic

Stochastic we have tried to keep as similar to the original as possible, main features are being able to select alternate timeframes for it to be calculated on as well as displaying divergences.

We have created a highlighted zone for when price enters the overbought/sold territory. A lot of traders will look for crossovers happening in these areas however from our tests we have discovered entering trades as the Stochastic comes out of these areas has hugely reduced losing trades, still not a perfect strategy but it does often show that the trend is showing weakening momentum and its commonly followed by a period of sideways action before continuing in a new direction.

MACD

We have calculated a dynamic extreme range for the MACD, you will notice the green/red bars as the bottom and top of the Oscillator. These levels help adjust with the assets volatility so they will work universally on all assets and timeframes. When these levels get more narrow, this indicates there is a potential larger move to come, similar thought process to a Bollinger band squeeze.

We like the Divergence signals you receive whilst in this OB/OS range as they give more confluence behind the divergence signal that price has over extended and is looking to retrace or consolidate.

Awesome Oscillator

The Awesome Oscillator is based on some pretty simple calculations but is hugely powerful.

The 3 main use cases are crossing the 0 value, showing weakening momentum and divergence signals.

We Particularly like the Divergence signals it gives us as they tend to be more accurate than any other oscillator.

Wavetrend

Wavetrend we try describe as a more dynamic Stochastic/MACD, it moves smoother and quicker without giving too many false signals.

Conditions we use the Wavetrend for are similar to the MACD where we are looking for crossovers or divergences in the extreme bands, these shouldn’t be used to trade alone and should be paired with other pieces of confluence for a higher probability trade however this is one of our favourites.

We also have a VWAP extreme detector which we pair with the Wavetrend, helping us identify areas where price should start cooling off.

Zig Zag

The main purpose of the standard Zig Zag is to analyse historical data to be able to observe cycle's in a market's movement, this requires a bit more explanation than we can include here so please refer to our documentation on the website for further guidance.

DPO

The detrended price oscillator is unlike other oscillators, such as the Stochastic or MACD the DPO is not a momentum indicator. It instead highlights peaks and troughs in price, which are used to estimate buy and sell points in line with the historical cycle.

We personally think this is the most under-rated oscillator out there, if you simply followed the DPO above 0 for long and below for short on higher timeframes you can outperform the buy and hold return of Bitcoin (BTCUSDT)...

This is just one simple way of using the DPO there are other more in depth methods of using it within our documentation.

Поиск скриптов по запросу "Cycle"

Bitcoin: Top & Bottom Mini-AlgoHere we have a mini-algorithm that tries to show absolute 4-year-cycle top and bottom zones for the case of the BraveNewCoin Liquid Index (BLX) for Bitcoin on the weekly (W) timeframe by using several oscillators as RSI, VPCI etc. employed with a custom logic. When the background gets red we might be near to a cycle peak, and when it gets green we might be near to the absolute bottom of the current cycle. Note that only absolute top/bottoms are indicated (at least since the end of 2013), so that the current strong drop in March 2020 was correctly not tagged, as it wasn't the lowest price of the current cycle.

It is best to combine this mini-algorithm with some of my boundary indicators for BLX, e.g. "Bitcoin: Price Action Integrals", for confluence . For the next peak one could then watch for the mini-algo to go red and for the price to hit the boundary. You can change the background transparency if you like to have this indicator be more unobstrusive on the chart.

For access please contact me via DM on TradingView or on Twitter (linked on my TradingView profile and my signature).

oscillator fast cryptosmart (Bands on Scale)The oscillator fast cryptosmart is a high-sensitivity momentum indicator designed to generate signals more rapidly than many traditional oscillators, such as the MACD. It is engineered to detect potential price breakouts by analyzing short-term market cycles.

At its core, the indicator uses a Detrended Price Oscillator (DPO) to remove the longer-term trend from price action, allowing it to focus purely on the underlying momentum cycles. It then calculates dynamic volatility bands around this oscillator line.

Signals are generated when momentum breaks out from a normal range, providing traders with an early warning of a potential acceleration in price.

How to Interpret the Signals:

Buy Signal (Green Vertical Line): A buy signal is generated when the oscillator's main line (yellow) crosses above its upper statistical band. This indicates a sharp surge in positive momentum, suggesting a potential upward move is beginning.

Sell Signal (Red Vertical Line): A sell signal is generated when the oscillator's main line crosses below its lower statistical band. This indicates a significant increase in negative momentum, suggesting a potential downward move is starting.

By focusing on momentum breakouts rather than lagging moving average crossovers, the oscillator fast cryptosmart aims to provide an edge in identifying opportunities in fast-moving markets.

Stacey Burke Signal Day LTE“Previously published as ‘Day Zero Fakeout Detector MTF’”

Stacey Burke Signal Day LTE

Automatic detection of Day Zero, Inside Days, and Outside Days for Stacey Burke’s intraday playbook

🔎 Stacey Burke’s Signal Days

This indicator highlights the key daily patterns that often lead to high-probability intraday setups in Stacey Burke’s methodology:

1️⃣ Day Zero

The reset days within a 3-day cycle (e.g. breakout → continuation → exhaustion/reversal).

Can mark the beginning of a new directional phase.

Trades back inside the prior range after a Peak Formation High (PFH) or Peak Formation Low (PFL).

Bias: Look for measured parabolic session moves. When combined with trend following indicators, these signal days can be very powerful.

2️⃣ Inside Day

A day where the entire range is contained within the prior day’s range.

Signals consolidation and energy build-up.

Often leads to explosive breakouts in the next session.

Bias: Trade breakouts of the inside day’s high/low or breakout reversal in the session at key timings in the direction of higher timeframe bias. When combined with trend following indicators, these signal days can be very powerful.

3️⃣ Outside Day (Engulfing Day)

`

A day where the range is larger than the prior day’s range, engulfing both high and low.

Marks trapped traders and fakeouts on both sides.

Often precedes strong continuations or sharp reversals from outside of the ranges.

Bias: Align trades with the true continuation move. When combined with trend following indicators, these signal days can be very powerful.

📌 How They Work Together

Day Zero → Signals the new cycle after PFH/PFL.

Inside Day → Signals compression → expect breakout setups.

Outside Day → Signals exhaustion/fakeouts → expect reversals or continuations.

Together, they give traders a clear daily roadmap for where liquidity sits and when to expect the highest-probability setups.

✅ Example in Practice

Market rallies for 3 days → PFH forms → Day Zero short bias.

Next day prints an Inside Day → watch for breakout continuation short, and breakout reversals.

Later, an Outside Day traps both longs and shorts → the following session offers a clean intraday reversal or continuation trade in line with the underlying MTF trend/bias.

⚙️ Features of This Indicator

Automatic detection of Day Zero, Inside Days, and Outside Days

Multi-Timeframe (MTF) support for cycle alignment

Visual markers for PFH/PFL and consolidation zones

Measured move projections for breakout targets

👉 Stacey Burke Signal Day LTE gives traders just a few of the most important signal days — Day Zero, Inside Day, and Outside Day — to structure their intraday trades around fake outs, breakouts, and reversals within the daily cycles of the week. (This is work in progress: Next up, FRD/FGD's, 3-day cycle detecting, 3DLs, 3DSs).

Bitcoin Pi Cycle Top Indicator - Daily Timeframe Only1 Day Timeframe Only

The Bitcoin Pi Cycle Top Indicator has garnered attention for its historical effectiveness in identifying the timing of Bitcoin's market cycle peaks with remarkable precision, typically within a margin of 3 days.

It utilizes a specific combination of moving averages—the 111-day moving average and a 2x multiple of the 350-day moving average—to signal potential tops in the Bitcoin market.

The 111-day moving average (MA): This shorter-term MA is chosen to reflect more recent price action and trends within the Bitcoin market.

The 350-day moving average (MA) multiplied by 2: This longer-term MA is adjusted to capture broader market trends and cycles over an extended period.

The key premise behind the Bitcoin Pi Cycle Top Indicator is that a potential market top for Bitcoin can be signaled when the 111-day MA crosses above the 350-day MA (which has been doubled). Historically, this crossover event has shown a remarkable correlation with the peaks of Bitcoin's price cycles, making it a tool of interest for traders and investors aiming to anticipate significant market shifts.

#Bitcoin

WaveTrend 3D█ OVERVIEW

WaveTrend 3D (WT3D) is a novel implementation of the famous WaveTrend (WT) indicator and has been completely redesigned from the ground up to address some of the inherent shortcomings associated with the traditional WT algorithm.

█ BACKGROUND

The WaveTrend (WT) indicator has become a widely popular tool for traders in recent years. WT was first ported to PineScript in 2014 by the user @LazyBear, and since then, it has ascended to become one of the Top 5 most popular scripts on TradingView.

The WT algorithm appears to have origins in a lesser-known proprietary algorithm called Trading Channel Index (TCI), created by AIQ Systems in 1986 as an integral part of their commercial software suite, TradingExpert Pro. The software’s reference manual states that “TCI identifies changes in price direction” and is “an adaptation of Donald R. Lambert’s Commodity Channel Index (CCI)”, which was introduced to the world six years earlier in 1980. Interestingly, a vestige of this early beginning can still be seen in the source code of LazyBear’s script, where the final EMA calculation is stored in an intermediate variable called “tci” in the code.

█ IMPLEMENTATION DETAILS

WaveTrend 3D is an alternative implementation of WaveTrend that directly addresses some of the known shortcomings of the indicator, including its unbounded extremes, susceptibility to whipsaw, and lack of insight into other timeframes.

In the canonical WT approach, an exponential moving average (EMA) for a given lookback window is used to assess the variability between price and two other EMAs relative to a second lookback window. Since the difference between the average price and its associated EMA is essentially unbounded, an arbitrary scaling factor of 0.015 is typically applied as a crude form of rescaling but still fails to capture 20-30% of values between the range of -100 to 100. Additionally, the trigger signal for the final EMA (i.e., TCI) crossover-based oscillator is a four-bar simple moving average (SMA), which further contributes to the net lag accumulated by the consecutive EMA calculations in the previous steps.

The core idea behind WT3D is to replace the EMA-based crossover system with modern Digital Signal Processing techniques. By assuming that price action adheres approximately to a Gaussian distribution, it is possible to sidestep the scaling nightmare associated with unbounded price differentials of the original WaveTrend method by focusing instead on the alteration of the underlying Probability Distribution Function (PDF) of the input series. Furthermore, using a signal processing filter such as a Butterworth Filter, we can eliminate the need for consecutive exponential moving averages along with the associated lag they bring.

Ideally, it is convenient to have the resulting probability distribution oscillate between the values of -1 and 1, with the zero line serving as a median. With this objective in mind, it is possible to borrow a common technique from the field of Machine Learning that uses a sigmoid-like activation function to transform our data set of interest. One such function is the hyperbolic tangent function (tanh), which is often used as an activation function in the hidden layers of neural networks due to its unique property of ensuring the values stay between -1 and 1. By taking the first-order derivative of our input series and normalizing it using the quadratic mean, the tanh function performs a high-quality redistribution of the input signal into the desired range of -1 to 1. Finally, using a dual-pole filter such as the Butterworth Filter popularized by John Ehlers, excessive market noise can be filtered out, leaving behind a crisp moving average with minimal lag.

Furthermore, WT3D expands upon the original functionality of WT by providing:

First-class support for multi-timeframe (MTF) analysis

Kernel-based regression for trend reversal confirmation

Various options for signal smoothing and transformation

A unique mode for visualizing an input series as a symmetrical, three-dimensional waveform useful for pattern identification and cycle-related analysis

█ SETTINGS

This is a summary of the settings used in the script listed in roughly the order in which they appear. By default, all default colors are from Google's TensorFlow framework and are considered to be colorblind safe.

Source: The input series. Usually, it is the close or average price, but it can be any series.

Use Mirror: Whether to display a mirror image of the source series; for visualizing the series as a 3D waveform similar to a soundwave.

Use EMA: Whether to use an exponential moving average of the input series.

EMA Length: The length of the exponential moving average.

Use COG: Whether to use the center of gravity of the input series.

COG Length: The length of the center of gravity.

Speed to Emphasize: The target speed to emphasize.

Width: The width of the emphasized line.

Display Kernel Moving Average: Whether to display the kernel moving average of the signal. Like PCA, an unsupervised Machine Learning technique whereby neighboring vectors are projected onto the Principal Component.

Display Kernel Signal: Whether to display the kernel estimator for the emphasized line. Like the Kernel MA, it can show underlying shifts in bias within a more significant trend by the colors reflected on the ribbon itself.

Show Oscillator Lines: Whether to show the oscillator lines.

Offset: The offset of the emphasized oscillator plots.

Fast Length: The length scale factor for the fast oscillator.

Fast Smoothing: The smoothing scale factor for the fast oscillator.

Normal Length: The length scale factor for the normal oscillator.

Normal Smoothing: The smoothing scale factor for the normal frequency.

Slow Length: The length scale factor for the slow oscillator.

Slow Smoothing: The smoothing scale factor for the slow frequency.

Divergence Threshold: The number of bars for the divergence to be considered significant.

Trigger Wave Percent Size: How big the current wave should be relative to the previous wave.

Background Area Transparency Factor: Transparency factor for the background area.

Foreground Area Transparency Factor: Transparency factor for the foreground area.

Background Line Transparency Factor: Transparency factor for the background line.

Foreground Line Transparency Factor: Transparency factor for the foreground line.

Custom Transparency: Transparency of the custom colors.

Total Gradient Steps: The maximum amount of steps supported for a gradient calculation is 256.

Fast Bullish Color: The color of the fast bullish line.

Normal Bullish Color: The color of the normal bullish line.

Slow Bullish Color: The color of the slow bullish line.

Fast Bearish Color: The color of the fast bearish line.

Normal Bearish Color: The color of the normal bearish line.

Slow Bearish Color: The color of the slow bearish line.

Bullish Divergence Signals: The color of the bullish divergence signals.

Bearish Divergence Signals: The color of the bearish divergence signals.

█ ACKNOWLEDGEMENTS

@LazyBear - For authoring the original WaveTrend port on TradingView

@PineCoders - For the beautiful color gradient framework used in this indicator

@veryfid - For the inspiration of using mirrored signals for cycle analysis and using multiple lookback windows as proxies for other timeframes

Financial Astrology Mercury LongitudeMercury energy influence the mind, the intellect and mental temperament, in mundane astrology is well know that rules: news, science, debating, trading, commerce, contracts. telecommunication, short-distance travels, among others. W. D. Gann discovered that the Mercury speed phases (stationary, retrograde, direct) transitions was very relevant as trading signals, he used the Sun conjunction retrograde Mercury to confirm the formation of top and bottoms that seems to be a relevant leading indicator in multiples markets.

As part of the Financial Astrology Research Group experiments, we created hundreds of machine learning models that try to predict daily trend direction for a research portfolio of 10 crypto-currencies and is confirmed that including the Mercury speed and aspects features (variables) in the models increase the accuracy in a consistent manner. Therefore, there is enough evidence that Mercury is one of the most powerful mid term trading cycles.

This is the first open source PIneScript indicator that is able to plot the Mercury Tropical Longitude for the years 2010-2030, we publish as open source in order to support and simplify the research of the amazing astro-traders community at TradingView that have been working manually with annotations and lines to represent the Mercury longitude zodiac signs entries and the speed phases transitions. That manual work is over. Let's move faster in our cycles research!

We encourage all astro traders to continue researching and sharing your ideas of astro cycles trading strategies with us and contribute your experiments at our Github Financial Stats exploration project

so we can improve the cosmic energy models that influence traders behaviours.

Note: The Mercury longitude is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the longitude is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart reference timezone.

Others astro trading indicators from Financial Astrology Research Group:

[blackcat] L2 Ehlers Cyber Cycle Trading StrategyLevel: 2

Background

John F. Ehlers introuced Cyber Cycle Trading Strategy in his "Cybernetic Analysis for Stocks and Futures" chapter 4 on 2004.

Function

With cyber cycle alone, the Trigger lags the Cycle by one bar, so that their crossing introduces at least another bar of lag. Finally, Dr Ehler concluded that we can’t execute the trade until the bar after the signal is observed. In total, that means our trade execution will be at least four bars late. If we are working with an eight-bar cycle, that means the signal will be exactly wrong. We could do better to buy when the signal says sell, and vice versa.

The difficulties arising from the lag suggest a way to build an automatic trading strategy. Suppose we choose to use the trading signal in the opposite direction of the signal. That will work if we can introduce lag so the correct signal will be given in the more general case, not just the case of an eight-bar cycle. Therefore, the Cyber Cycle trading strategy was introduced by Dr. Ehlers. It starts exactly the same as the Cyber Cycle Indicator. Dr. Ehlers then introduce the variable Signal, which is an exponential moving average of the Cycle variable. The exponential moving average generates the desired lag in the trading signal. The relationship between the alpha of an exponential moving average and lag is alpha2 = 1/ (Lag+1). This relationship is used to create the variable alpha2 in the code and the variable Signal using the exponential moving average. The trading signals using the variable Signal crossing itself delayed by one bar are exactly the opposite of the trading signals I would have used if there were no delay. But, since the variable Signal is delayed such that the net delay is less than half a cycle, the trading signals are correct to catch the next cyclic reversal. The idea of betting against the correct direction by waiting for the next cycle reversal can be pretty scary because that reversal may “never” happen because the market takes off in a trend. For this reason Dr. Ehlers included two lines of code that are escape mechanisms if we were wrong in our entry signal. These last two Signal lines of code reverse the trading position if we have been in the trade for more than eight bars and the trade has an open position loss.

Key Signal

Cycle ---> Cyber Cycle fast line

Cycle (2) ---> Cyber Cycle slow line

Signal ---> Trading signal fast line

Signal(1) ---> Trading signal slow line

Pros and Cons

100% John F. Ehlers definition translation of original work, even variable names are the same. This help readers who would like to use pine to read his book. If you had read his works, then you will be quite familiar with my code style.

Remarks

The 25th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Ehlers Stable Dominant Cycle Length [graylange]Stable Dominant Cycle Length – Adaptive Cycle Detection for Market Timing

This script calculates the dominant cycle length of the market using an improved version of John Ehlers' Hilbert Transform approach. Unlike traditional implementations, this version includes advanced smoothing techniques to reduce noise and prevent erratic spikes, making it more reliable for adaptive cycle-based strategies.

🔥 Key Features:

✅ Noise-Reduced Cycle Detection – Uses a Weighted Moving Average (WMA) detrending method instead of raw Hilbert Transform values to enhance stability.

✅ Adaptive Smoothing – Applies an Exponential Moving Average (EMA) to the instantaneous period, reducing excessive volatility in cycle length calculations.

✅ Phase Wrapping & Constraints – Clamps phase changes to prevent unrealistic cycle swings and division errors.

✅ Dynamic Cycle Adjustment – The dominant cycle length updates in real time, constrained within a reasonable range (6 to 50 bars) to avoid extreme peaks.

📌 How to Use It:

Identify Market Cycles – Use the dominant cycle length to determine optimal trend-following vs. mean-reversion strategies.

Enhance MESA Filters – Apply the detected cycle length to adjust Ehlers’ MESA Adaptive Moving Average (MAMA) dynamically.

Fine-Tune Alpha Settings – Reduce overfitting in cycle-based indicators by basing parameters on a stable dominant cycle estimate.

Fight Or Flight Index [log] - LTF [MethodAlgo]Introduction:

"Fight Or Flight" is a robust yet user-friendly indicator designed for long-term cycle analysis and gauging market sentiment. Excluded from our Premium Indicator Collection, we are delighted to offer this tool to the community for free.

Before Use:

- This is a first-layer analysis tool, identifying potential over/under-valued price areas, not predicting future market movements.

- Tailored for long-term investment analysis. Designed for use on timeframes "1D" and above; unsupported timeframes will display nothing.

- If the asset has less 2 years of data, indicator will display nothing.

Concept:

Fight Or Flight utilizes a 2-year Moving Average (MA) as a baseline (neon white), with reference lines at 2.5x and 5x of the MA (white and neon red). By tracking asset movements through bear and bull market cycles, the indicator simplifies the identification of these cycles for long-term investors.

Instructions:

- Supported timeframes: 1D, 3D, 1W, 2W, 3W, 9W, 1M, 3M, 6M, 12M; auto-adjusts MA parameters for listed timeframes for the same result.

- Recommended to use log chart for clearer views; supports all chart types but functions optimally in log mode. or the upper channel line will look odd (but not wrong).

- Set up advice: Use the indicator in a separate chart with a fixed timeframe.

UI:

- Neon White: Indicates market bottom, a 2-year MA auto-adjusted for the supported timeframe.

- Neon Red: Indicates market top, set at 5x the 2-year MA.

- White: Sits between the top and bottom lines, serving as a support, resistance, or equilibrium line.

- Filled Area: Red (Flight) signals an overheated market, suggesting an exit; White (Fight) denotes an undervalued market, suggesting an possible entry.

Use Case:

Traders can observe price levels in comparison to the MA levels provided by the indicator for cycle analysis:

- Below Neon White: Indicates undervalue, over-pessimistic market conditions; potential for outsized returns.

- Near or above Neon Red: Suggests an overvalued or overexcited market; plan your exit strategy.

Risk Disclaimer:

Trading is inherently risky; this indicator provides indications based on historical data, and past performance does not guarantee future results. Use it as part of your confluence reference and avoid making trading decisions solely based on one indicator.

Moonhub Cycle IndexMoonhub Cycle Index is a composite index derived from three popular technical analysis indicators: Moving Average Convergence Divergence (MACD), Schaff Trend Cycle (STC), and Detrended Price Oscillator (DPO). The indicator is designed to help identify potential trends and market sentiment by combining the unique characteristics of each indicator.

Key components of the indicator include:

Input Parameters:

COEMA Length (len_DIema): The length of the Exponential Moving Average (EMA) applied to the Custom Index. Default is set to 9.

COSMA Length (len_DIsma): The length of the Simple Moving Average (SMA) applied to the Custom Index. Default is set to 30.

Indicators:

MACD: A momentum oscillator that shows the relationship between two moving averages of a security's price. It is calculated using the difference between the 12-period and 26-period EMA, and a 9-period EMA (signal line) of the MACD.

STC: A cyclic indicator that identifies cyclical trends in the market. It is calculated using the Stochastic oscillator formula applied to the close, high, and low prices over a 10-period lookback window.

DPO: A price oscillator that eliminates the trend from price data to focus on underlying cycles. It is calculated using a custom function that shifts the price by half the length and subtracts the SMA from the shifted price.

Custom Index: The composite index is calculated by taking the average of the MACD line, STC, and DPO.

COEMA and COSMA: Exponential and Simple Moving Averages applied to the Custom Index using the lengths specified by the input parameters (len_DIema and len_DIsma).

Plots: The Custom Index, COEMA, and COSMA are plotted with different colors and line widths to visualize their interaction and provide insights into potential market trends.

This Custom Index Indicator can be useful for traders who want to analyze the market using a combination of these indicators to make more informed decisions. It can also help identify potential trends and market sentiment by combining the unique characteristics of each indicator.

Combo Backtest 123 Reversal & D_DSP (Detrended Synthetic Price) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Detrended Synthetic Price is a function that is in phase with the

dominant cycle of real price data. This DSP is computed by subtracting

a half-cycle exponential moving average (EMA) from the quarter cycle

exponential moving average.

See "MESA and Trading Market Cycles" by John Ehlers pages 64 - 70.

WARNING:

- For purpose educate only

- This script to change bars colors.

VACPWelles Wilder (delta phenomenon) a 4-day rotation indicator

PVAC is the acronym Alan uses for a four-day rotation cycle. The cycle itself is circularly continuous every days of the week, forever, including every holiday. Thus if, for instance, Monday was a P, Tuesday is V, Wednesday is A, Thursday is C. At this point the cycle repeats, with Friday being P, Saturday being V, Sunday being A, and the following Monday being C.

Having started, the cycle never changes. While each day tends to have the characteristics shown below, like all cycle tools, there are inversions, which will last a cycle or at times even more, and have reasonable odds of inverting regularly.

A trader who wants to incorporate a four-day rotation cycle into their work is encouraged to study for themselves whether this adds value.

Day: V-day Color: Red Characteristics: Closes well for bulls; Use your fleece bars Bar8 and Bar11; Bar8 open often a V-day return target; 'V' return comes early in day in bear moves, late in day in bullish moves

Day: A-day Color: Blue Characteristics: Closes poorly for bulls; Use your fleece bars 8 and 11; Generally 'A' shaped, but may have a kick-leg after 3pm

Day: C-day Color: Orange Characteristics: Consolidation day, aka 'consoly' day. It may not chop, but it may have an

accumulation or distribution quality to the action; Trade often and trade fast; Pattern traders fade 4HHs and 4LLs with backfill/pullbacks 3 bars later; Apexes and angulars tend to have less importance; Numerical traders trade after Bar8 open and use support one horizontal below, resistance one horizontal above; C-day opens often at the 25%; The afternoon action tends to be opposite to the morning action

Day: P-day Color: Green Characteristics: Often a trend day. Find the trend and enter it; Often opens at the 75%; Trade P-days against a quartile; Watch for price to be above/below the first apex: buy above or sell below ; Do not fade dead zone, minimal trading

[Bybit BTCUSD.P] 7Years Backtest Results. 2,609% +Non-Repainting📊 I. Strategy Overview: Trust Backed by Numbers

The ADX Sniper v12 strategy has been rigorously tested over 7 years, from November 14, 2018 to November 8, 2025, spanning every major cycle of the Bitcoin

BTCUSD.P futures market. This strategy successfully balances two often-conflicting goals: maximizing profitability while minimizing volatility, all supported by objective performance data.

This strategy has been validated across all Bitcoin (BTCUSD.P) futures market cycles over a 7-year period.

■ Visual Proof: Bar Replay Simulation

The chart above demonstrates actual entry and exit points captured via TradingView's Bar Replay feature. The green rectangle highlights the core profitable trading zone, showing where the strategy successfully captured sustained uptrends. This visual evidence confirms:

Confirmed buy/sell signals with exact execution prices (marked in red and blue)

No repainting or signal distortion after candle close

Consistent performance across multiple market cycles within the highlighted zone

💰 Core Performance Metrics:

Cumulative Return: 2,609.14% (compounded growth over 7 years)

Maximum Drawdown (MDD): 6.999% (preserving over 93% of capital)

Average Profit/Loss Ratio: 8.003 (industry-leading risk-reward efficiency)

Total Trades: 24 (focused exclusively on high-conviction opportunities)

Sortino Ratio: 11.486 (mathematically proving robustness and stability)

✅ This strategy has been validated across all Bitcoin BTCUSD.P futures market cycles over a 7-year period.

📊 I. 전략 개요: 숫자로 입증된 신뢰

ADX Sniper v12 전략은 2018년 11월 14일부터 2025년 11월 8일까지 약 7년간 비트코인 (BTCUSD.P) 선물 시장의 모든 주요 사이클을 거치며 엄격하게 검증되었습니다. 수익성 극대화와 변동성 최소화라는 상충되는 목표를 동시에 달성한 이 전략의 핵심 성과 지표를 객관적 데이터를 통해 확인하실 수 있습니다.

본 전략은 7년간의 모든 비트코인 (BTCUSD.P) 선물 시장 사이클에서 검증되었습니다.

■ 시각적 증명: 바 리플레이 시뮬레이션

위 차트는 TradingView의 바 리플레이 기능으로 포착된 실제 진입 및 청산 시점을 보여줍니다. 녹색 네모는 핵심 수익 구간을 표시하며, 전략이 지속적인 상승 추세를 성공적으로 포착한 영역을 나타냅니다. 본 시각 자료는 다음을 입증합니다:

정확한 체결 가격이 표기된 확정된 매수/매도 신호 (빨강색과 파랑색으로 표시)

캔들 종가 후 신호 왜곡이나 리페인팅 없음

강조 표시된 구간 내 여러 시장 사이클에 걸친 일관된 성과

💰 핵심 성과 지표:

누적 수익률: 2,609.14% (7년간 복리 성장 입증)

최대 낙폭 (MDD): 6.999% (7년간 자본의 93% 이상 보존)

평균 손익비: 8.003 (업계 최고 수준의 위험-보상 효율성)

총 거래 횟수: 24회 (고확신 기회에만 집중)

소르티노 비율: 11.486 (전략의 견고성과 안정성을 수학적으로 입증)

✅ 본 전략은 7년간의 모든 비트코인 (BTCUSD.P) 선물 시장 사이클에서 검증되었습니다.

🛡️ II. Core Philosophy: Cut Losses Short, Let Profits Run

Why MDD Stays Below 7% in a Volatile Market

The crypto futures market typically experiences daily volatility exceeding 10%, with most strategies enduring drawdowns between 30% and 50%. In stark contrast, this strategy has never exceeded a 7% account loss over seven years. This exceptional low MDD is achieved through deliberate design mechanisms, not luck:

🎯 Entry Filtering: The 'ADX Pop-up Filter' is the core component. It enables the strategy to strictly avoid trading when market conditions indicate major reversals or consolidation phases, thereby minimizing exposure to high-risk zones.

🏛️ Capital Preservation Priority: The strategy prioritizes investor psychological stability and capital preservation over pursuing maximum potential returns.

The Power of an 8.003 Profit Factor

The Profit Factor measures the ratio of total profitable trades to total losing trades. It's the most critical metric for assessing risk-adjusted returns.

A Profit Factor of 8.003 means that for every dollar lost, the strategy earns an average of eight dollars. This demonstrates the efficiency of a true trend-following strategy:

Cutting losses quickly (averaging $177,419 USD loss per trade)

Riding winners for maximum extension (averaging $1,419,920 USD profit per trade)

🛡️ II. 핵심 철학: 손실은 빠르게 자르고, 수익은 끝까지

암호화폐 시장에서 MDD <7%의 의미

암호화폐 선물 시장은 일일 변동성이 10%를 초과하는 경우가 빈번하며, 일반적인 전략들은 30~50%의 MDD를 겪습니다. 이와 극명한 대조로, 본 전략은 7년간 단 한 번도 7%를 초과하는 계좌 손실을 기록하지 않았습니다. 이렇게 극도로 낮은 MDD는 운이 아닌 체계적인 메커니즘을 통해 달성되었습니다:

🎯 진입 필터링: 'ADX 팝업 필터'가 핵심 구성 요소로, 시장 상황이 주요 반전이나 횡보를 나타낼 때 거래를 엄격히 회피하여 고위험 구간 노출을 최소화합니다.

🏛️ 자본 보존 우선: 본 전략은 최대 잠재 손실을 감수하기보다 투자자의 심리적 안정성과 자본 보존을 우선시하도록 설계되었습니다.

손익비 8.003의 힘

손익비는 '총 수익 거래'와 '총 손실 거래'의 비율로, 위험 조정 수익을 측정하는 핵심 지표입니다.

8.003이라는 값은 1달러를 잃을 때마다 평균적으로 8달러 이상을 벌어들이는 구조를 의미합니다. 이는 진정한 추세 추종 전략의 최대 효율성을 보여줍니다:

손실은 빠르게 자르고 ($177,419 USD 평균 손실)

수익은 최대한 연장합니다 ($1,419,920 USD 평균 수익)

🎯 III. Strategy Reliability and Structural Edge

The Secret of 24 Trades in 7 Years

Only 24 trades over 7 years signifies that this strategy ignores 99% of market volatility and targets only the 1% of 'most certain buying cycles'. This approach eliminates the drag from excessive trading:

❌ No commission bleed

❌ No slippage erosion

❌ No psychological wear from overtrading

📈 Long-Term Trend Following: The strategy analyzes Bitcoin's long-term price cycles to capture the onset of massive trends while remaining undisturbed by short-term market noise.

Non-Repainting Structure: Alignment of Reality and Simulation

🎬 Non-Repainting Proof Video Available

※↑ "If you wish, I can also show you a video as evidence of the non-repainting throughout the 7 years."

✅ Real-Time Trading Reliability: This strategy is built with a non-repainting structure, generating buy/sell signals only after each candle's closing price is confirmed.

✅ Preventing Data Exaggeration: This design ensures that backtest results do not 'repaint' or distort past performance, guaranteeing high correlation between simulated results and actual live trading environments.

✅ Live Trading Advantage: While simulations use closing prices, live trading may allow entry at more favorable prices before candle close, potentially yielding even better execution than backtest results.

🎯 III. 전략의 신뢰성과 구조적 우위

7년간 24회 거래의 비밀

7년간 단 24회의 거래는 시장 변동성의 99%를 무시하고 오직 1%의 '가장 확실한 매수 사이클'만을 타겟으로 한다는 것을 의미합니다. 이는 과도한 거래로 인한 문제를 근본적으로 제거합니다:

❌ 수수료 소모 없음

❌ 슬리피지 침식 없음

❌ 과도한 트레이딩으로 인한 심리적 소모 없음

📈 장기 추세 추종: 비트코인 가격 역사를 지배하는 장기 사이클 분석을 활용하여, 단기 시장 노이즈에 흔들리지 않고 대규모 추세의 시작점을 포착하는 데 집중합니다.

논-리페인팅 구조: 현실과 시뮬레이션의 일치

🎬 논-리페인팅 증명 영상 제공 가능

※↑ "원하신다면 7년간 리페인팅이 없음을 증명하는 영상도 보여드릴 수 있습니다."

✅ 실시간 거래 신뢰성: 본 전략은 논-리페인팅 구조로 구축되어, 캔들의 종가가 확정된 후에만 매수/매도 신호를 생성합니다.

✅ 데이터 과장 방지: 이러한 설계는 백테스트 결과가 과거 성과를 '리페인팅'하거나 과장하지 않도록 보장하며, 시뮬레이션 결과와 실제 라이브 거래 환경 간의 높은 상관관계를 보장합니다.

✅ 라이브 실행 우위 가능성: 시뮬레이션은 종가 기준이지만, 라이브 운영 시 캔들이 마감되기 전 더 유리한 가격에 진입할 수 있어 시뮬레이션 결과보다 더 나은 실행 성과를 얻을 가능성이 있습니다.

📈 IV. Performance Summary (November 14, 2018 - November 8, 2025)

| Metric | Value || Metric | Value |

|--------|-------|

| Initial Capital | $1,000,000 |

| Net Profit | +$26,091,383.74 |

| Cumulative Return | +2,609.14% |

| Maximum Drawdown | -6.999% |

| Total Trades | 24 |

| Winning Trades | 19 (79.17%) |

| Losing Trades | 5 (20.83%) |

| Avg Winning Trade | +$1,419,920.16 |

| Avg Losing Trade | -$177,419.86 |

| Profit Factor | 8.003 |

| Sortino Ratio | 11.486 |

| Win/Loss Ratio | 8.003 |

⚙️ Default Settings:

Slippage: 0 ticks

Commission: 0.333% (Bybit standard)

📈 IV. 성과 지표 요약 (2018년 11월 14일 ~ 2025년 11월 8일)

|| 지표 | 값 |

|--------|-------|

| 초기 자본 | $1,000,000 |

| 순이익 | +$26,091,383.74 |

| 누적 수익률 | +2,609.14% |

| 최대 낙폭 | -6.999% |

| 총 거래 횟수 | 24 |

| 수익 거래 | 19 (79.17%) |

| 손실 거래 | 5 (20.83%) |

| 평균 수익 거래 | +$1,419,920.16 |

| 평균 손실 거래 | -$177,419.86 |

| 손익비 | 8.003 |

| 소르티노 비율 | 11.486 |

| 평균 손익 비율 | 8.003 |

⚙️ 기본 설정:

슬리피지: 0틱 (기본값)

수수료: 0.333% (Bybit 표준)

👥 V. Who Is This Strategy For?

✅ Long-term Bitcoin investors seeking stable, low-drawdown returns

✅ Traders tired of overtrading who prefer surgical, sniper-style precision entries

✅ Investors seeking psychological stability by avoiding large account swings

✅ Data-driven decision makers who value proven performance over marketing claims

👥 V. 이 전략은 누구를 위한 것인가요?

✅ 안정적이고 낮은 낙폭의 수익을 추구하는 장기 비트코인 투자자

✅ 과도한 매매에 지친 트레이더로 저격수 스타일의 정밀한 진입을 선호하는 분

✅ 큰 계좌 변동을 피하여 심리적 안정성을 추구하는 투자자

✅ 주장보다 검증된 객관적 성과를 중시하는 데이터 기반 의사 결정자

🔒 VI. Access & Disclaimer

🔐 Access Type: Invite-Only (Protected Source Code)

💬 How to Get Access: Send a private message or leave a comment below

⚠️ Important Disclaimer:

Past performance does not guarantee future results. Cryptocurrency and futures trading involve substantial risk of loss. This strategy is provided for educational and informational purposes only. Users should conduct their own research and consult with a financial advisor before making investment decisions. The author is not responsible for any financial losses incurred from using this strategy.

🔒 VI. 접근 방법 및 면책사항

🔐 접근 유형: 초대 전용 (소스코드 보호)

💬 접근 방법: 비공개 메시지 또는 아래 댓글 남기기

⚠️ 중요 면책사항:

과거 성과가 미래 결과를 보장하지 않습니다. 암호화폐 및 선물 거래는 상당한 손실 위험을 수반합니다. 본 전략은 교육 및 정보 제공 목적으로만 제공됩니다. 사용자는 투자 결정을 내리기 전 자체 조사를 수행하고 재무 자문가와 상담해야 합니다. 저자는 본 전략 사용으로 인한 재정적 손실에 대해 책임지지 않습니다.

🏷️ VII. Tags

Bitcoin |Bitcoin | BTCUSD | BTCUSD.P | Bybit | DailyChart | LongTerm | TrendFollowing | ADX | NonRepainting | Strategy | BacktestProven | SevenYears | LowDrawdown | HighProfitFactor | StableReturns | CapitalPreservation | Ichimoku | DMI | SuperTrend | TechnicalAnalysis | Volatility | RiskManagement | AutoTrading | Futures | PerpetualFutures | AlgorithmicTrading | SystematicTrading | DataDriven | InviteOnly | ProtectedScript | SnipperTrading | HighConviction | MDD | SortinoRatio

🏷️ VII. 태그

비트코인 |비트코인 | BTCUSD | BTCUSD.P | 바이비트 | 일봉 | 장기투자 | 추세추종 | ADX | 논리페인팅 | 전략 | 백테스트검증 | 7년검증 | 저낙폭 | 고손익비 | 안정수익 | 자본보존 | 일목균형표 | DMI | 슈퍼트렌드 | 기술적분석 | 변동성 | 위험관리 | 자동매매 | 선물 | 무기한선물 | 알고리즘트레이딩 | 시스템트레이딩 | 데이터기반 | 초대전용 | 보호스크립트 | 저격수트레이딩 | 고확신 | MDD | 소르티노비율

📌 Note: This strategy is designed exclusively for Bybit BTCUSD.P perpetual futures on the 1-day (daily) timeframe. Performance may vary significantly on other symbols or timeframes.

📌 참고: 본 전략은 Bybit BTCUSD.P 무기한 선물 계약의 1일봉(Daily) 타임프레임에 전용으로 설계되었습니다. 다른 심볼이나 타임프레임에서는 성과가 크게 달라질 수 있습니다.

[Bybit BTCUSD.P] 7Years Backtest Results. 2,609% +Non-Repainting

📊 I. Strategy Overview: Trust Backed by Numbers

The ADX Sniper v12 strategy has been rigorously tested over 7 years, from November 14, 2018 to November 8, 2025, spanning every major cycle of the Bitcoin BTCUSD.P futures market. This strategy successfully balances two often-conflicting goals: maximizing profitability while minimizing volatility, all supported by objective performance data.

This strategy has been validated across all Bitcoin (BTCUSD.P) futures market cycles over a 7-year period.

■ Visual Proof: Bar Replay Simulation

The chart above demonstrates actual entry and exit points captured via TradingView's Bar Replay feature. The green rectangle highlights the core profitable trading zone, showing where the strategy successfully captured sustained uptrends. This visual evidence confirms:

1) Confirmed buy/sell signals with exact execution prices (marked in red and blue)

2) No repainting or signal distortion after candle close

3) Consistent performance across multiple market cycles within the highlighted zone

💰 Core Performance Metrics:

Cumulative Return : 2,609.14% (compounded growth over 7 years)

Maximum Drawdown (MDD) : 6.999% (preserving over 93% of capital)

Average Profit/Loss Ratio : 8.003 (industry-leading risk-reward efficiency)

Total Trades : 24 (focused exclusively on high-conviction opportunities)

Sortino Ratio : 11.486 (mathematically proving robustness and stability)

✅ This strategy has been validated across all Bitcoin BTCUSD.P futures market cycles over a 7-year period.

🛡️ II. Core Philosophy: Cut Losses Short, Let Profits Run

Why MDD Stays Below 7% in a Volatile Market

The crypto futures market typically experiences daily volatility exceeding 10%, with most strategies enduring drawdowns between 30% and 50%. In stark contrast, this strategy has never exceeded a 7% account loss over seven years. This exceptional low MDD is achieved through deliberate design mechanisms, not luck:

🎯 Entry Filtering: The 'ADX Pop-up Filter' is the core component. It enables the strategy to strictly avoid trading when market conditions indicate major reversals or consolidation phases, thereby minimizing exposure to high-risk zones.

🏛️ Capital Preservation Priority: The strategy prioritizes investor psychological stability and capital preservation over pursuing maximum potential returns.

The Power of an 8.003 Profit Factor

The Profit Factor measures the ratio of total profitable trades to total losing trades. It's the most critical metric for assessing risk-adjusted returns.

A Profit Factor of 8.003 means that for every dollar lost, the strategy earns an average of eight dollars. This demonstrates the efficiency of a true trend-following strategy:

Cutting losses quickly (averaging $177,419 USD loss per trade)

Riding winners for maximum extension (averaging $1,419,920 USD profit per trade)

🎯 III. Strategy Reliability and Structural Edge

The Secret of 24 Trades in 7 Years

Only 24 trades over 7 years signifies that this strategy ignores 99% of market volatility and targets only the 1% of 'most certain buying cycles'. This approach eliminates the drag from excessive trading:

❌ No commission bleed

❌ No slippage erosion

❌ No psychological wear from overtrading

📈 Long-Term Trend Following: The strategy analyzes Bitcoin's long-term price cycles to capture the onset of massive trends while remaining undisturbed by short-term market noise.

Non-Repainting Structure: Alignment of Reality and Simulation

🎬 Non-Repainting Proof Video Available

※↑ "If you wish, I can also show you a video as evidence of the non-repainting throughout the 7 years."

✅ Real-Time Trading Reliability: This strategy is built with a non-repainting structure, generating buy/sell signals only after each candle's closing price is confirmed.

✅ Preventing Data Exaggeration: This design ensures that backtest results do not 'repaint' or distort past performance, guaranteeing high correlation between simulated results and actual live trading environments.

✅ Live Trading Advantage: While simulations use closing prices, live trading may allow entry at more favorable prices before candle close, potentially yielding even better execution than backtest results.

📈 IV. Performance Summary (November 14, 2018 - November 8, 2025)

|| Metric | Value |

|--------|-------|

| Initial Capital | $1,000,000 |

| Net Profit | +$26,091,383.74 |

| Cumulative Return | +2,609.14% |

| Maximum Drawdown | -6.999% |

| Total Trades | 24 |

| Winning Trades | 19 (79.17%) |

| Losing Trades | 5 (20.83%) |

| Avg Winning Trade | +$1,419,920.16 |

| Avg Losing Trade | -$177,419.86 |

| Profit Factor | 8.003 |

| Sortino Ratio | 11.486 |

| Win/Loss Ratio | 8.003 |

⚙️ Default Settings:

Slippage: 0 ticks

Commission: 0.333% (Bybit standard)

👥 V. Who Is This Strategy For?

✅ Long-term Bitcoin investors seeking stable, low-drawdown returns

✅ Traders tired of overtrading who prefer surgical, sniper-style precision entries

✅ Investors seeking psychological stability by avoiding large account swings

✅ Data-driven decision makers who value proven performance over marketing claims

🔒 VI. Access & Disclaimer

🔐 Access Type: Invite-Only (Protected Source Code)

💬 How to Get Access: Send a private message or leave a comment below

⚠️ Important Disclaimer:

Past performance does not guarantee future results. Cryptocurrency and futures trading involve substantial risk of loss. This strategy is provided for educational and informational purposes only. Users should conduct their own research and consult with a financial advisor before making investment decisions. The author is not responsible for any financial losses incurred from using this strategy.

🏷️ VII. Tags

Bitcoin |Bitcoin | BTCUSD | BTCUSD.P | Bybit | DailyChart | LongTerm | TrendFollowing | ADX | NonRepainting | Strategy | BacktestProven | SevenYears | LowDrawdown | HighProfitFactor | StableReturns | CapitalPreservation | Ichimoku | DMI | SuperTrend | TechnicalAnalysis | Volatility | RiskManagement | AutoTrading | Futures | PerpetualFutures | AlgorithmicTrading | SystematicTrading | DataDriven | InviteOnly | ProtectedScript | SnipperTrading | HighConviction | MDD | SortinoRatio

📌 Note: This strategy is designed exclusively for Bybit BTCUSD.P perpetual futures on the 1-day (daily) timeframe. Performance may vary significantly on other symbols or timeframes.

Lunar calendar day Crypto Trading StrategyLunar calendar day Crypto Trading Strategy

This strategy explores the potential impact of the lunar calendar on cryptocurrency price cycles.

It implements a simple but unconventional rule:

Buy on the 5th day of each lunar month

Sell on the 26th day of the lunar month

No trades between January 1 (solar) and Lunar New Year’s Day (holiday buffer period)

Research background

Several academic studies have investigated the influence of lunar cycles on financial markets. Their findings suggest:

Returns tend to be higher around the full moon compared to the new moon.

Periods between the full moon and the waning phase often show stronger average returns than the waxing phase.

This strategy combines those observations into a practical implementation by testing fixed entry (lunar day 5) and exit (lunar day 26) points, while excluding the transition period from solar New Year to Lunar New Year, effectively capturing mid-month lunar effects.

How it works

The script includes a custom lunar date calculation function, reconstructing lunar months and days for each year (2020–2026).

On lunar day 5, the strategy opens a long position with 100% of equity.

On lunar day 26, the strategy closes the position.

No trades are executed between Jan 1 and Lunar New Year’s Day.

All trades include:

Commission: 0.1%

Slippage: 3 ticks

Position sizing uses the entire equity (100%) for simplicity, but this is not recommended for live trading.

Why this is original

Unlike mashups of built-in indicators, this script:

Implements a full lunar calendar system inside Pine Script.

Translates academic findings on lunar effects into an applied backtest.

Adds a realistic trading filter (holiday gap) based on cultural/seasonal calendar rules.

Provides researchers and traders with a framework to explore non-traditional, time-based signals.

Notes

This is an experimental, research-oriented strategy, not financial advice.

Results are highly dependent on the chosen period (2020–2026).

Using 100% equity per trade is for simplification only and is not a viable money management practice.

The purpose is to investigate whether cyclical patterns linked to lunar time can provide any statistical edge in ETHUSDT.

Bitcoin Logarithmic Growth Curve 2025 Z-Score"The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

snapshot

snapshot

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns."

Now with Z-Score calculation for easy and constant valuation classification of Bitcoin according to this metric.

Created for TRW

21DMA Structure Counter (EMA/SMA Option)21DMA Structure Counter (EMA/SMA Option)

Overview

The 21DMA Structure Counter is an advanced technical indicator that tracks consecutive periods where price action remains above a 21-period moving average structure. This indicator helps traders identify momentum phases and potential trend exhaustion points using statistical analysis.

Key Features

Moving Average Structure

- Configurable MA Type: Choose between EMA (Exponential Moving Average) or SMA (Simple Moving Average)

- 21-Period Default: Optimized for the widely-watched 21-period moving average

- Triple MA Structure: Tracks high, close, and low moving averages for comprehensive analysis

Statistical Analysis

- Cycle Counting: Automatically counts consecutive periods above the MA structure

- Historical Data: Maintains up to 2,500 historical cycles (approximately 10 years of daily data)

- Z-Score Calculation: Provides statistical context using mean and standard deviation

- Multiple Standard Deviation Levels: Displays +1, +2, and +3 standard deviation thresholds

Visual Indicators

Color-Coded Bars:

- Gray: Below 10-year average

- Yellow: Between average and +1 standard deviation

- Orange: Between +1 and +2 standard deviations

- Red: Between +2 and +3 standard deviations

- Fuchsia: Above +3 standard deviations (extreme readings)

Breadth Integration

- Multiple Breadth Options: NDFI, NDTH, NDTW (NASDAQ breadth indicators), or VIX

- Background Shading: Visual alerts when breadth reaches extreme levels

- High/Low Thresholds: Customizable levels for breadth analysis

- Real-time Display: Current breadth value shown in data table

Smart Reset Logic

- High Below Structure Reset: Automatically resets count when daily high falls below the lowest MA

- Flexible Hold Period: Continues counting during temporary weakness as long as structure isn't violated

- Precise Entry/Exit: Strict criteria for starting cycles, flexible for maintaining them

How to Use

Trend Identification

- Rising Counts: Indicate sustained momentum above key moving average structure

- Extreme Readings: Z-scores above +2 or +3 suggest potential trend exhaustion

- Historical Context: Compare current cycles to 10-year statistical averages

Risk Management

- Breadth Confirmation: Use breadth shading to confirm market-wide strength/weakness

- Statistical Extremes: Exercise caution when readings reach +3 standard deviations

- Reset Signals: Pay attention to structure violations for potential trend changes

Multi-Timeframe Application

- Daily Charts: Primary timeframe for swing trading and position management

- Weekly/Monthly: Longer-term trend analysis

- Intraday: Shorter-term momentum assessment (adjust MA period accordingly)

Settings

Moving Average Options

- Type: EMA or SMA selection

- Period: Default 21 (customizable)

- Reset Days: Days below structure required for reset

Visual Customization

- Standard Deviation Lines: Toggle and customize colors for +1, +2, +3 SD

- Breadth Selection: Choose from NDFI, NDTH, NDTW, or VIX

- Threshold Levels: Set custom high/low breadth thresholds

- Table Styling: Customize text colors, background, and font size

Technical Notes

- Data Retention: Maintains 2,500 historical cycles for robust statistical analysis

- Real-time Updates: Calculations update with each new bar

- Breadth Integration: Uses security() function to pull external breadth data

- Performance Optimized: Efficient array management prevents memory issues

Best Practices

1. Combine with Price Action: Use alongside support/resistance and chart patterns

2. Monitor Breadth Divergences: Watch for breadth weakness during strong readings

3. Respect Statistical Extremes: Exercise caution at +2/+3 standard deviation levels

4. Context Matters: Consider overall market environment and sector rotation

5. Risk Management: Use appropriate position sizing, especially at extreme readings

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis and proper risk management techniques.

Compatible with Pine Script v6 | Optimized for daily timeframes | Best used on major indices and liquid stocks

Bitcoin: Pi Cycle Top & Bottom | QuantumResearchBitcoin: Pi Cycle Top & Bottom | QuantumResearch

Adaptive Deviation Model for Bitcoin Macro Extremes

Bitcoin: Pi Cycle Top & Bottom by QuantumResearch is a proprietary interpretation of the famous Pi Cycle concept—enhanced with normalized deviation logic, adjustable thresholds, and visual clarity. Unlike traditional models that simply cross two moving averages, this tool calculates the dynamic spread between a short-term and amplified long-term exponential average, delivering a continuous score that adapts to Bitcoin's evolving volatility profile.

🧠 What Makes It Unique?

🔹 Pi Deviation Engine:

This creates a centered, symmetric oscillator that better visualizes overextended conditions—something the original Pi Cycle model does not offer.

🔹 Dynamic Zoning via Thresholds:

Users can set custom top and bottom thresholds to adjust sensitivity based on current market regimes, making it more flexible than static crossover models.

🔹 Gradient-Powered Area Fill:

The oscillator plot is filled with directional gradients that react to the score's magnitude, creating an intuitive visual spectrum between bullish and bearish extremes.

🔹 Macro-Focused, Overlay-Free:

The indicator runs in a clean subpanel, preserving chart space and allowing better integration into multi-layered macro dashboards.

🔹 Built for BTC’s Unique Structure:

The moving average lengths and logic are specifically calibrated to Bitcoin’s halving-driven cycles, unlike generic Pi models applied across asset classes.

🔍 Key Features

✅ Continuous Cycle Score (not binary crosses)

✅ Custom upper/lower thresholds for signal flexibility

✅ Visual gradient fill and background shading

✅ Zero chart clutter (non-overlay)

✅ Fully customizable moving average lengths

✅ Designed for macro cycle top/bottom detection

📌 Ideal For:

Long-term Bitcoin investors

Macro traders and analysts

Those seeking early warning signs of euphoria or despair

Anyone using on-chain + cyclical tools to time large market pivots

⚠️ Disclaimer

This indicator is for educational and research purposes only.

It does not provide financial advice or guarantees.

Past performance does not predict future behavior.

Always confirm with additional tools and analysis.

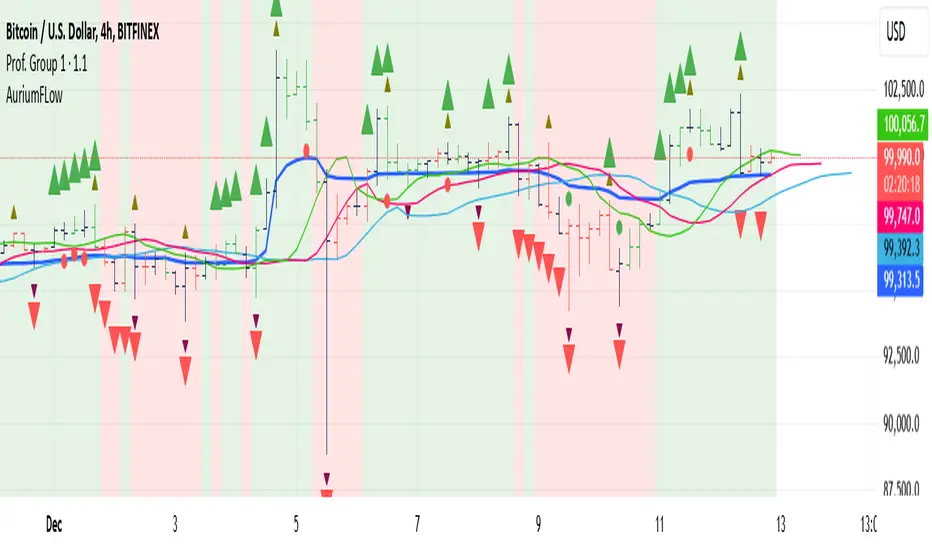

AuriumFlowAURIUM (GOLD-Weighted Average with Fractal Dynamics)

Aurium is a cutting-edge indicator that blends volume-weighted moving averages (VWMA), fractal geometry, and Fibonacci-inspired calculations to deliver a precise and holistic view of market trends. By dynamically adjusting to price and volume, Aurium uncovers key levels of confluence for trend reversals and continuations, making it a powerful tool for traders.

Key Features:

Dynamic Trendline (GOLD):

The central trendline is a weighted moving average based on price and volume, tuned using Fibonacci-based fast (34) and slow (144) exponential moving average lengths. This ensures the trendline adapts seamlessly to the flow of market dynamics.

Formula:

GOLD = VWMA(34) * Volume Factor + VWMA(144) * (1 - Volume Factor)

Fractal Highs and Lows:

Detects pivotal market points using a fractal lookback period (default 5, odd-numbered). Fractals identify local highs and lows over a defined window, capturing the structure of market cycles.

Trend Background Highlighting:

Bullish Zone: Price above the GOLD line with a green background.

Bearish Zone: Price below the GOLD line with a red background.

Buy and Sell Alerts:

Generates actionable signals when fractals align with GOLD. Bullish fractals confirm continuation or reversal in an uptrend, while bearish fractals validate a downtrend.

The Math Behind Aurium:

Volume-Weighted Adjustments:

By integrating volume into the calculation, Aurium dynamically emphasizes price levels with greater participation, giving traders insight into zones of institutional interest.

Formula:

VWMA = EMA(Close * Volume) / EMA(Volume)

Fractal Calculations:

Fractals are identified as local maxima (highs) or minima (lows) based on the surrounding bars, leveraging the natural symmetry in price behavior.

Fibonacci Relationships:

The 34 and 144 EMA lengths are Fibonacci numbers, offering a natural alignment with price cycles and market rhythms.

Ideal For:

Traders seeking a precise and intuitive indicator for aligning with trends and detecting reversals.

Strategies inspired by Bill Williams, with added volume and fractal-based insights.

Short-term scalpers and long-term trend-followers alike.

Unlock deeper market insights and trade with precision using Aurium!

AMD-PO3-Goldbach levels [promuckaj]This script is developed on time & price, algorithmic market theory that is well explained in the book "Demystifying ICT" by Hopiplaka.

Indicators main features:

*PO3 - Goldbach(IPDA) levels which is based on the size of a price range (dealing range) as a factor of power of three (3^n).

There is PO3 numbers starting from 3 to 177147 as predefined, but also there is field for custom one so that users can experiment.

By selecting the PO3 number script calculate range low and range high using PO3 formula based on the current price and represent it on the chart into multiple levels of Goldbach numbers. At each this levels it is expected to see price that form block, fair value gap etc..., as defined in concept by ICT.

Levels:

Ext => External range

Low => Range low

High => Range high

FVG => Fair value gap

RB => Rejection block

OB => Order block

LV => Liquidity void

BR => Breaker

MB => Mitigation block

*AMD (Accumulation, Manipulation, Distribution) cycles, that can be modified by changing timings and colors.

Using PO3-Goldbach levels to identify where at the current time profile price is, there can be done trades in line with AMD cycles.

Default timings are set for Forex pairs.

*FVG, HIPPO, Displacement is well known parts of a market structure, so those three are also implemented here with some possible changes for them (colors, extension, labels...).

FVG => Fair value gap, imbalances in the market, or when buying and selling are not equal, in most cases can become a magnet for the price.

HIPPO => Hidden interbank price point objective, invention by Hopiplaka to demonstrate meaning of this "hidden" order block. It basically take the wicks of 2 consecutive bars that create a fair value gap.

DISPLACEMENT => It is practically similar to FVG but with option to measure length and strength, where in combination it will calculate and mark candle by looking back to the bars to determine the candle range standard deviation.

FEATURES:

-Multiple PO3 numbers, including special option to set your custom one

-Color and style customization

-Main levels mode, only Low, High and Equilibrium levels

-PO3 table with all PO3 calcs from multiple numbers, and mark the same levels from multiple

-Option to shift DR up or down

-Option to show you always upper/lower main DR levels (Low/High/Eq.)

NOTE:

-First of all special thanks to fxdmn that gives me idea from his indicator, how to present this through my own script.

-GB levels requires the correct symbols price calculation to work properly, everything is done by auto calc, tested well on EURUSD,SP500,DXY,Gold and BTC.

Price Action AverageThis indicator is perfect for scalping in 1 minute, it consists of a channel and a line that is made up of the average of the highs and lows of the price in 12 and 64 cycles.

The channel has as its center a 7 cycles SMA, when the average line (Called Signal, the purple one) crosses the upper band it is time to make a Long.

If it crosses the lower band it is time to make a short, if the line returns to the channel a signal appears to close the operation.

The indicator works with all timeframes, I use it on the 1 hour chart and I do the trades in 1 minute.

PA-Adaptive TRIX Log [Loxx]PA-Adaptive TRIX Log is a Phase Accumulation Adaptive TRIX Log indicator. This adaptation smooths the signal to catch larger trends.

What is TRIX?

TRIX is a momentum oscillator that displays the percent rate of change of a TEMA . It was developed in the early 1980's by Jack Hutson, an editor for "Technical Analysis of Stocks and Commodities" magazine. With its triple smoothing, TRIX is designed to filter insignificant price movements. In his article he uses a logarithm of a price (which is in many versions, left out).

What is the Phase Accumulation Cycle?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included

Bar coloring

2 signal options

Alerts