Adaptive Fibonacci Pullback System -FibonacciFluxAdaptive Fibonacci Pullback System (AFPS) - FibonacciFlux

This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0). Original concepts by FibonacciFlux.

Abstract

The Adaptive Fibonacci Pullback System (AFPS) presents a sophisticated, institutional-grade algorithmic strategy engineered for high-probability trend pullback entries. Developed by FibonacciFlux, AFPS uniquely integrates a proprietary Multi-Fibonacci Supertrend engine (0.618, 1.618, 2.618 ratios) for harmonic volatility assessment, an Adaptive Moving Average (AMA) Channel providing dynamic market context, and a synergistic Multi-Timeframe (MTF) filter suite (RSI, MACD, Volume). This strategy transcends simple indicator combinations through its strict, multi-stage confluence validation logic. Historical simulations suggest that specific MTF filter configurations can yield exceptional performance metrics, potentially achieving Profit Factors exceeding 2.6 , indicative of institutional-level potential, while maintaining controlled risk under realistic trading parameters (managed equity risk, commission, slippage).

4 hourly MTF filtering

1. Introduction: Elevating Pullback Trading with Adaptive Confluence

Traditional pullback strategies often struggle with noise, false signals, and adapting to changing market dynamics. AFPS addresses these challenges by introducing a novel framework grounded in Fibonacci principles and adaptive logic. Instead of relying on static levels or single confirmations, AFPS seeks high-probability pullback entries within established trends by validating signals through a rigorous confluence of:

Harmonic Volatility Context: Understanding the trend's stability and potential turning points using the unique Multi-Fibonacci Supertrend.

Adaptive Market Structure: Assessing the prevailing trend regime via the AMA Channel.

Multi-Dimensional Confirmation: Filtering signals with lower-timeframe Momentum (RSI), Trend Alignment (MACD), and Market Conviction (Volume) using the MTF suite.

The objective is to achieve superior signal quality and adaptability, moving beyond conventional pullback methodologies.

2. Core Methodology: Synergistic Integration

AFPS's effectiveness stems from the engineered synergy between its core components:

2.1. Multi-Fibonacci Supertrend Engine: Utilizes specific Fibonacci ratios (0.618, 1.618, 2.618) applied to ATR, creating a multi-layered volatility envelope potentially resonant with market harmonics. The averaged and EMA-smoothed result (`smoothed_supertrend`) provides a robust, dynamic trend baseline and context filter.

// Key Components: Multi-Fibonacci Supertrend & Smoothing

average_supertrend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_supertrend = ta.ema(average_supertrend, st_smooth_length)

2.2. Adaptive Moving Average (AMA) Channel: Provides dynamic market context. The `ama_midline` serves as a key filter in the entry logic, confirming the broader trend bias relative to adaptive price action. Extended Fibonacci levels derived from the channel width offer potential dynamic S/R zones.

// Key Component: AMA Midline

ama_midline = (ama_high_band + ama_low_band) / 2

2.3. Multi-Timeframe (MTF) Filter Suite: An optional but powerful validation layer (RSI, MACD, Volume) assessed on a lower timeframe. Acts as a **validation cascade** – signals must pass all enabled filters simultaneously.

2.4. High-Confluence Entry Logic: The core innovation. A pullback entry requires a specific sequence and validation:

Price interaction with `average_supertrend` and recovery above/below `smoothed_supertrend`.

Price confirmation relative to the `ama_midline`.

Simultaneous validation by all enabled MTF filters.

// Simplified Long Entry Logic Example (incorporates key elements)

long_entry_condition = enable_long_positions and

(low < average_supertrend and close > smoothed_supertrend) and // Pullback & Recovery

(close > ama_midline and close > ama_midline) and // AMA Confirmation

(rsi_filter_long_ok and macd_filter_long_ok and volume_filter_ok) // MTF Validation

This strict, multi-stage confluence significantly elevates signal quality compared to simpler pullback approaches.

1hourly filtering

3. Realistic Implementation and Performance Potential

AFPS is designed for practical application, incorporating realistic defaults and highlighting performance potential with crucial context:

3.1. Realistic Default Strategy Settings:

The script includes responsible default parameters:

strategy('Adaptive Fibonacci Pullback System - FibonacciFlux', shorttitle = "AFPS", ...,

initial_capital = 10000, // Accessible capital

default_qty_type = strategy.percent_of_equity, // Equity-based risk

default_qty_value = 4, // Default 4% equity risk per initial trade

commission_type = strategy.commission.percent,

commission_value = 0.03, // Realistic commission

slippage = 2, // Realistic slippage

pyramiding = 2 // Limited pyramiding allowed

)

Note: The default 4% risk (`default_qty_value = 4`) requires careful user assessment and adjustment based on individual risk tolerance.

3.2. Historical Performance Insights & Institutional Potential:

Backtesting provides insights into historical behavior under specific conditions (always specify Asset/Timeframe/Dates when sharing results):

Default Performance Example: With defaults, historical tests might show characteristics like Overall PF ~1.38, Max DD ~1.16%, with potential Long/Short performance variance (e.g., Long PF 1.6+, Short PF < 1).

Optimized MTF Filter Performance: Crucially, historical simulations demonstrate that meticulous configuration of the MTF filters (particularly RSI and potentially others depending on market) can significantly enhance performance. Under specific, optimized MTF filter settings combined with appropriate risk management (e.g., 7.5% risk), historical tests have indicated the potential to achieve **Profit Factors exceeding 2.6**, alongside controlled drawdowns (e.g., ~1.32%). This level of performance, if consistently achievable (which requires ongoing adaptation), aligns with metrics often sought in institutional trading environments.

Disclaimer Reminder: These results are strictly historical simulations. Past performance does not guarantee future results. Achieving high performance requires careful parameter tuning, adaptation to changing markets, and robust risk management.

3.3. Emphasizing Risk Management:

Effective use of AFPS mandates active risk management. Utilize the built-in Stop Loss, Take Profit, and Trailing Stop features. The `pyramiding = 2` setting requires particularly diligent oversight. Do not rely solely on default settings.

4. Conclusion: Advancing Trend Pullback Strategies

The Adaptive Fibonacci Pullback System (AFPS) offers a sophisticated, theoretically grounded, and highly adaptable framework for identifying and executing high-probability trend pullback trades. Its unique blend of Fibonacci resonance, adaptive context, and multi-dimensional MTF filtering represents a significant advancement over conventional methods. While requiring thoughtful implementation and risk management, AFPS provides discerning traders with a powerful tool potentially capable of achieving institutional-level performance characteristics under optimized conditions.

Acknowledgments

Developed by FibonacciFlux. Inspired by principles of Fibonacci analysis, adaptive averaging, and multi-timeframe confirmation techniques explored within the trading community.

Disclaimer

Trading involves substantial risk. AFPS is an analytical tool, not a guarantee of profit. Past performance is not indicative of future results. Market conditions change. Users are solely responsible for their decisions and risk management. Thorough testing is essential. Deploy at your own considered risk.

Поиск скриптов по запросу "zone"

TMA StrategyThe **TMA Strategy** is a trend-following strategy that leverages **Smoothed Moving Averages (SMMA)** and **candlestick patterns** to identify high-probability trading opportunities. It is designed for traders who want to capture strong trends while minimizing noise from short-term fluctuations.

**Key Features:**

✔ **Multiple Smoothed Moving Averages (SMMA):** Uses 21, 50, 100, and 200-period SMMAs to identify market trends and key support/resistance zones.

✔ **Candlestick Pattern Confirmation:** Incorporates **3-line strike** and **engulfing candle** patterns to confirm trade entries.

✔ **Dynamic Trend Filter:** A **2-period EMA** ensures that trades align with the dominant trend, reducing false signals.

✔ **Customizable Session Filter:** Allows users to enable/disable trading within specific market sessions (New York, London, Tokyo, etc.), ensuring trades are executed only during high-liquidity hours.

✔ **Risk Management:** Uses predefined exit conditions based on EMA/SMMA crossovers to lock in profits and minimize losses.

**Trading Logic:**

📌 **Long Entry:**

- Bullish Engulfing or 3-Line Strike pattern appears.

- Price is above the 200 SMMA.

- 2 EMA confirms an uptrend.

- Trade executes if session filter allows.

📌 **Short Entry:**

- Bearish Engulfing or 3-Line Strike pattern appears.

- Price is below the 200 SMMA.

- 2 EMA confirms a downtrend.

- Trade executes if session filter allows.

📌 **Exit Conditions:**

- Long trades exit when EMA(2) crosses **below** SMMA(200).

- Short trades exit when EMA(2) crosses **above** SMMA(200).

**Ideal Markets & Timeframes:**

✅ Best suited for **Forex, Stocks, and Crypto** markets.

✅ Works well on **higher timeframes (15m, 1H, 4H, Daily)** for stronger trend confirmation.

📢 **Disclaimer:**

This strategy is for educational purposes only. Backtest results do not guarantee future performance. Always use proper risk management and test in a demo account before live trading.

🚀 **Try the TMA Strategy now and enhance your trend-following approach!**

Sunil BB Blast Heikin Ashi StrategySunil BB Blast Heikin Ashi Strategy

The Sunil BB Blast Heikin Ashi Strategy is a trend-following trading strategy that combines Bollinger Bands with Heikin-Ashi candles for precise market entries and exits. It aims to capitalize on price volatility while ensuring controlled risk through dynamic stop-loss and take-profit levels based on a user-defined Risk-to-Reward Ratio (RRR).

Key Features:

Trading Window:

The strategy operates within a user-defined time window (e.g., from 09:20 to 15:00) to align with market hours or other preferred trading sessions.

Trade Direction:

Users can select between Long Only, Short Only, or Long/Short trade directions, allowing flexibility depending on market conditions.

Bollinger Bands:

Bollinger Bands are used to identify potential breakout or breakdown zones. The strategy enters trades when price breaks through the upper or lower Bollinger Band, indicating a possible trend continuation.

Heikin-Ashi Candles:

Heikin-Ashi candles help smooth price action and filter out market noise. The strategy uses these candles to confirm trend direction and improve entry accuracy.

Risk Management (Risk-to-Reward Ratio):

The strategy automatically adjusts the take-profit (TP) level and stop-loss (SL) based on the selected Risk-to-Reward Ratio (RRR). This ensures that trades are risk-managed effectively.

Automated Alerts and Webhooks:

The strategy includes automated alerts for trade entries and exits. Users can set up JSON webhooks for external execution or trading automation.

Active Position Tracking:

The strategy tracks whether there is an active position (long or short) and only exits when price hits the pre-defined SL or TP levels.

Exit Conditions:

The strategy exits positions when either the take-profit (TP) or stop-loss (SL) levels are hit, ensuring risk management is adhered to.

Default Settings:

Trading Window:

09:20-15:00

This setting confines the strategy to the specified hours, ensuring trading only occurs during active market hours.

Strategy Direction:

Default: Long/Short

This allows for both long and short trades depending on market conditions. You can select "Long Only" or "Short Only" if you prefer to trade in one direction.

Bollinger Band Length (bbLength):

Default: 19

Length of the moving average used to calculate the Bollinger Bands.

Bollinger Band Multiplier (bbMultiplier):

Default: 2.0

Multiplier used to calculate the upper and lower bands. A higher multiplier increases the width of the bands, leading to fewer but more significant trades.

Take Profit Multiplier (tpMultiplier):

Default: 2.0

Multiplier used to determine the take-profit level based on the calculated stop-loss. This ensures that the profit target aligns with the selected Risk-to-Reward Ratio.

Risk-to-Reward Ratio (RRR):

Default: 1.0

The ratio used to calculate the take-profit relative to the stop-loss. A higher RRR means larger profit targets.

Trade Automation (JSON Webhooks):

Allows for integration with external systems for automated execution:

Long Entry JSON: Customizable entry condition for long positions.

Long Exit JSON: Customizable exit condition for long positions.

Short Entry JSON: Customizable entry condition for short positions.

Short Exit JSON: Customizable exit condition for short positions.

Entry Logic:

Long Entry:

The strategy enters a long position when:

The Heikin-Ashi candle shows a bullish trend (green close > open).

The price is above the upper Bollinger Band, signaling a breakout.

The previous candle also closed higher than it opened.

Short Entry:

The strategy enters a short position when:

The Heikin-Ashi candle shows a bearish trend (red close < open).

The price is below the lower Bollinger Band, signaling a breakdown.

The previous candle also closed lower than it opened.

Exit Logic:

Take-Profit (TP):

The take-profit level is calculated as a multiple of the distance between the entry price and the stop-loss level, determined by the selected Risk-to-Reward Ratio (RRR).

Stop-Loss (SL):

The stop-loss is placed at the opposite Bollinger Band level (lower for long positions, upper for short positions).

Exit Trigger:

The strategy exits a trade when either the take-profit or stop-loss level is hit.

Plotting and Visuals:

The Heikin-Ashi candles are displayed on the chart, with green candles for uptrends and red candles for downtrends.

Bollinger Bands (upper, lower, and basis) are plotted for visual reference.

Entry points for long and short trades are marked with green and red labels below and above bars, respectively.

Strategy Alerts:

Alerts are triggered when:

A long entry condition is met.

A short entry condition is met.

A trade exits (either via take-profit or stop-loss).

These alerts can be used to trigger notifications or webhook events for automated trading systems.

Notes:

The strategy is designed for use on intraday charts but can be applied to any timeframe.

It is highly customizable, allowing for tailored risk management and trading windows.

The Sunil BB Blast Heikin Ashi Strategy combines two powerful technical analysis tools (Bollinger Bands and Heikin-Ashi candles) with strong risk management, making it suitable for both beginners and experienced traders.

Feebacks are welcome from the users.

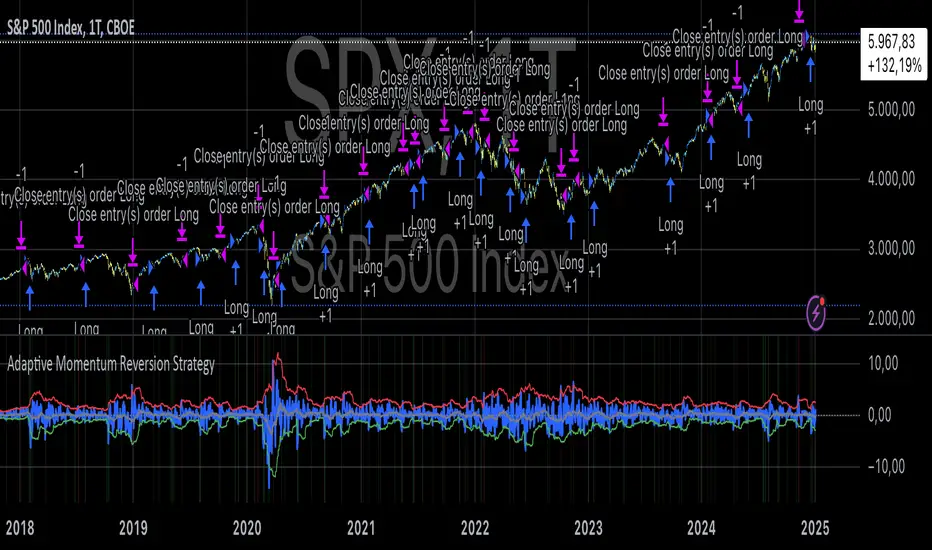

Adaptive Momentum Reversion StrategyThe Adaptive Momentum Reversion Strategy: An Empirical Approach to Market Behavior

The Adaptive Momentum Reversion Strategy seeks to capitalize on market price dynamics by combining concepts from momentum and mean reversion theories. This hybrid approach leverages a Rate of Change (ROC) indicator along with Bollinger Bands to identify overbought and oversold conditions, triggering trades based on the crossing of specific thresholds. The strategy aims to detect momentum shifts and exploit price reversions to their mean.

Theoretical Framework

Momentum and Mean Reversion: Momentum trading assumes that assets with a recent history of strong performance will continue in that direction, while mean reversion suggests that assets tend to return to their historical average over time (Fama & French, 1988; Poterba & Summers, 1988). This strategy incorporates elements of both, looking for periods when momentum is either overextended (and likely to revert) or when the asset’s price is temporarily underpriced relative to its historical trend.

Rate of Change (ROC): The ROC is a straightforward momentum indicator that measures the percentage change in price over a specified period (Wilder, 1978). The strategy calculates the ROC over a 2-period window, making it responsive to short-term price changes. By using ROC, the strategy aims to detect price acceleration and deceleration.

Bollinger Bands: Bollinger Bands are used to identify volatility and potential price extremes, often signaling overbought or oversold conditions. The bands consist of a moving average and two standard deviation bounds that adjust dynamically with price volatility (Bollinger, 2002).

The strategy employs two sets of Bollinger Bands: one for short-term volatility (lower band) and another for longer-term trends (upper band), with different lengths and standard deviation multipliers.

Strategy Construction

Indicator Inputs:

ROC Period: The rate of change is computed over a 2-period window, which provides sensitivity to short-term price fluctuations.

Bollinger Bands:

Lower Band: Calculated with a 18-period length and a standard deviation of 1.7.

Upper Band: Calculated with a 21-period length and a standard deviation of 2.1.

Calculations:

ROC Calculation: The ROC is computed by comparing the current close price to the close price from rocPeriod days ago, expressing it as a percentage.

Bollinger Bands: The strategy calculates both upper and lower Bollinger Bands around the ROC, using a simple moving average as the central basis. The lower Bollinger Band is used as a reference for identifying potential long entry points when the ROC crosses above it, while the upper Bollinger Band serves as a reference for exits, when the ROC crosses below it.

Trading Conditions:

Long Entry: A long position is initiated when the ROC crosses above the lower Bollinger Band, signaling a potential shift from a period of low momentum to an increase in price movement.

Exit Condition: A position is closed when the ROC crosses under the upper Bollinger Band, or when the ROC drops below the lower band again, indicating a reversal or weakening of momentum.

Visual Indicators:

ROC Plot: The ROC is plotted as a line to visualize the momentum direction.

Bollinger Bands: The upper and lower bands, along with their basis (simple moving averages), are plotted to delineate the expected range for the ROC.

Background Color: To enhance decision-making, the strategy colors the background when extreme conditions are detected—green for oversold (ROC below the lower band) and red for overbought (ROC above the upper band), indicating potential reversal zones.

Strategy Performance Considerations

The use of Bollinger Bands in this strategy provides an adaptive framework that adjusts to changing market volatility. When volatility increases, the bands widen, allowing for larger price movements, while during quieter periods, the bands contract, reducing trade signals. This adaptiveness is critical in maintaining strategy effectiveness across different market conditions.

The strategy’s pyramiding setting is disabled (pyramiding=0), ensuring that only one position is taken at a time, which is a conservative risk management approach. Additionally, the strategy includes transaction costs and slippage parameters to account for real-world trading conditions.

Empirical Evidence and Relevance

The combination of momentum and mean reversion has been widely studied and shown to provide profitable opportunities under certain market conditions. Studies such as Jegadeesh and Titman (1993) confirm that momentum strategies tend to work well in trending markets, while mean reversion strategies have been effective during periods of high volatility or after sharp price movements (De Bondt & Thaler, 1985). By integrating both strategies into one system, the Adaptive Momentum Reversion Strategy may be able to capitalize on both trending and reverting market behavior.

Furthermore, research by Chan (1996) on momentum-based trading systems demonstrates that adaptive strategies, which adjust to changes in market volatility, often outperform static strategies, providing a compelling rationale for the use of Bollinger Bands in this context.

Conclusion

The Adaptive Momentum Reversion Strategy provides a robust framework for trading based on the dual concepts of momentum and mean reversion. By using ROC in combination with Bollinger Bands, the strategy is capable of identifying overbought and oversold conditions while adapting to changing market conditions. The use of adaptive indicators ensures that the strategy remains flexible and can perform across different market environments, potentially offering a competitive edge for traders who seek to balance risk and reward in their trading approaches.

References

Bollinger, J. (2002). Bollinger on Bollinger Bands. McGraw-Hill Professional.

Chan, L. K. C. (1996). Momentum, Mean Reversion, and the Cross-Section of Stock Returns. Journal of Finance, 51(5), 1681-1713.

De Bondt, W. F., & Thaler, R. H. (1985). Does the Stock Market Overreact? Journal of Finance, 40(3), 793-805.

Fama, E. F., & French, K. R. (1988). Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96(2), 246-273.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

IU open equal to high/low strategyIU open equal to high/low strategy:

The "IU Open Equal to High/Low Strategy" is designed to identify and trade specific market conditions where the day's first price action shows a strong directional bias. This strategy automatically enters trades based on the relationship between the market's open price and its first high or low of the day.

Entry Conditions:

1. Long Entry: A long position is initiated when the first open price of the session equals the day's first low. This signals a potential upward move.

2. Short Entry: A short position is initiated when the first open price of the session equals the day's first high. This signals a potential downward move.

Exit Conditions:

1. Stop Loss (SL): For both long and short trades, the stop loss is calculated based on the low or high of the candle where the position was entered.

2. Take Profit (TP): The take profit is set using a Risk-to-Reward (RTR) ratio, which is customizable by the user. The TP is calculated relative to the entry price and the distance between the entry and the stop loss.

Additional Features:

- Plots are used to visualize the entry price, stop loss, and take profit levels directly on the chart, providing clear and actionable insights.

- Labels are displayed to indicate the occurrence of the "Open == Low" or "Open == High" conditions for easier identification of potential trade setups.

- A dynamic fill highlights the areas between the entry price and the stop loss or take profit, offering a clear visual representation of the trade's risk and reward zones.

This strategy is designed for traders looking to capitalize on directional momentum at the start of the trading session. It is customizable, allowing users to set their desired Risk-to-Reward ratio and tailor the strategy to fit their trading style.

Pavan CPR Strategy Pavan CPR Strategy (Pine Script)

The Pavan CPR Strategy is a trading system based on the Central Pivot Range (CPR), designed to identify price breakouts and generate long trade signals. This strategy uses key CPR levels (Pivot, Top CPR, and Bottom CPR) calculated from the daily high, low, and close to inform trade decisions. Here's an overview of how the strategy works:

Key Components:

CPR Calculation:

The strategy calculates three critical CPR levels for each trading day:

Pivot (P): The central value, calculated as the average of the high, low, and close prices.

Top Central Pivot (TC): The midpoint of the daily high and low, acting as the resistance level.

Bottom Central Pivot (BC): Derived from the pivot and the top CPR, providing a support level.

The script uses request.security to fetch these CPR values from the daily timeframe, even when applied on intraday charts.

Trade Entry Condition:

A long position is initiated when:

The current price crosses above the Top CPR level (TC).

The previous close was below the Top CPR level, signaling a breakout above a key resistance level.

This condition aims to capture upward momentum as the price breaks above a significant level.

Exit Strategy:

Take Profit: The position is closed with a profit target set 50 points above the entry price.

Stop Loss: A stop loss is placed at the Pivot level to protect against unfavorable price movements.

Visual Reference:

The script plots the three CPR levels on the chart:

Pivot: Blue line.

Top CPR (TC): Green line.

Bottom CPR (BC): Red line.

These plotted levels provide visual guidance for identifying potential support and resistance zones.

Use Case:

The Pavan CPR Strategy is ideal for intraday traders who want to capitalize on price movements and breakouts above critical CPR levels. It provides clear entry and exit signals based on price action and is best used in conjunction with proper risk management.

Note: The strategy is written in Pine Script v5 for use on TradingView, and it is recommended to backtest and optimize it for the asset or market you are trading.

XAUUSD 10-Minute StrategyThis XAUUSD 10-Minute Strategy is designed for trading Gold vs. USD on a 10-minute timeframe. By combining multiple technical indicators (MACD, RSI, Bollinger Bands, and ATR), the strategy effectively captures both trend-following and reversal opportunities, with adaptive risk management for varying market volatility. This approach balances high-probability entries with robust volatility management, making it suitable for traders seeking to optimise entries during significant price movements and reversals.

Key Components and Logic:

MACD (12, 26, 9):

Generates buy signals on MACD Line crossovers above the Signal Line and sell signals on crossovers below the Signal Line, helping to capture momentum shifts.

RSI (14):

Utilizes oversold (below 35) and overbought (above 65) levels as a secondary filter to validate entries and avoid overextended price zones.

Bollinger Bands (20, 2):

Uses upper and lower Bollinger Bands to identify potential overbought and oversold conditions, aiming to enter long trades near the lower band and short trades near the upper band.

ATR-Based Stop Loss and Take Profit:

Stop Loss and Take Profit levels are dynamically set as multiples of ATR (3x for stop loss, 5x for take profit), ensuring flexibility with market volatility to optimise exit points.

Entry & Exit Conditions:

Buy Entry: T riggered when any of the following conditions are met:

MACD Line crosses above the Signal Line

RSI is oversold

Price drops below the lower Bollinger Band

Sell Entry: Triggered when any of the following conditions are met:

MACD Line crosses below the Signal Line

RSI is overbought

Price moves above the upper Bollinger Band

Exit Strategy: Trades are closed based on opposing entry signals, with adaptive spread adjustments for realistic exit points.

Backtesting Configuration & Results:

Backtesting Period: July 21, 2024, to October 30, 2024

Symbol Info: XAUUSD, 10-minute timeframe, OANDA data source

Backtesting Capital: Initial capital of $700, with each trade set to 10 contracts (equivalent to approximately 0.1 lots based on the broker’s contract size for gold).

Users should confirm their broker's contract size for gold, as this may differ. This script uses 10 contracts for backtesting purposes, aligned with 0.1 lots on brokers offering a 100-contract specification.

Key Backtesting Performance Metrics:

Net Profit: $4,733.90 USD (676.27% increase)

Total Closed Trades: 526

Win Rate: 53.99%

Profit Factor: 1.44 (1.96 for Long trades, 1.14 for Short trades)

Max Drawdown: $819.75 USD (56.33% of equity)

Sharpe Ratio: 1.726

Average Trade: $9.00 USD (0.04% of equity per trade)

This backtest reflects realistic conditions, with a spread adjustment of 38 points and no slippage or commission applied. The settings aim to simulate typical retail trading conditions. However, please adjust the initial capital, contract size, and other settings based on your account specifics for best results.

Usage:

This strategy is tuned specifically for XAUUSD on a 10-minute timeframe, ideal for both trend-following and reversal trades. The ATR-based stop loss and take profit levels adapt dynamically to market volatility, optimising entries and exits in varied conditions. To backtest this script accurately, ensure your broker’s contract specifications for gold align with the parameters used in this strategy.

[ETH] Optimized Trend Strategy - Lorenzo SuperScalpStrategy Title: Optimized Trend Strategy - Lorenzo SuperScalp

Description:

The Optimized Trend Strategy is a comprehensive trading system tailored for Ethereum (ETH) and optimized for the 15-minute timeframe but adaptable to various timeframes. This strategy utilizes a combination of technical indicators—RSI, Bollinger Bands, and MACD—to identify and act on price trends efficiently, providing traders with actionable buy and sell signals based on market conditions.

Key Features:

Multi-Indicator Approach:

RSI (Relative Strength Index): Identifies overbought and oversold conditions to time market entries and exits.

Bollinger Bands: Acts as a dynamic support and resistance level, helping to pinpoint precise entry and exit zones.

MACD (Moving Average Convergence Divergence): Detects momentum changes through bullish and bearish crossovers.

Signal Conditions:

Buy Signal:

RSI is below 45 (indicating an oversold condition).

Price is near or below the lower Bollinger Band.

MACD bullish crossover occurs.

Sell Signal:

RSI is above 55 (indicating an overbought condition).

Price is near or above the upper Bollinger Band.

MACD bearish crossunder occurs.

Trade Execution Logic:

Long Trades: Opened when a buy signal flashes. If there’s an open short position, it is closed before opening a long.

Short Trades: Opened when a sell signal flashes. If there’s an open long position, it is closed before opening a short.

The strategy also ensures a minimum number of bars between consecutive trades to avoid rapid trading in choppy conditions.

Pyramiding Support:

Up to 3 consecutive trades in the same direction are allowed, enabling traders to scale into positions based on strong signals.

Visual Indicators:

RSI Levels: Dotted lines at 45 and 55 for quick reference to oversold and overbought levels.

Buy and Sell Signals: Visual markers on the chart indicate where trades are executed, ensuring clarity on entry and exit points.

Best Used For:

Swing Trading & Scalping: While optimized for the 15-minute timeframe, this strategy works across various timeframes, making it suitable for both short-term scalping and swing trading.

Crypto Trading: Tailored for Ethereum but effective for other cryptocurrencies due to its dynamic indicator setup.

Fibonacci & Bollinger Bands StrategyThis strategy combines Bollinger Bands and Fibonacci retracement/extension levels to identify potential entry and exit points in the market. Here’s a breakdown of each component and how the strategy works:

1. Bollinger Bands:

Bollinger Bands consist of a simple moving average (SMA) and two standard deviations (upper and lower bands) plotted above and below the SMA. The bands expand and contract based on market volatility.

Purpose in Strategy:

The lower band represents an area where the market might be oversold.

The upper band represents an area where the market might be overbought.

The price crossing these bands suggests overextended market conditions, which can be used to identify potential reversals.

2. Fibonacci Retracement and Extension Levels:

Fibonacci retracement levels are horizontal lines that indicate where price might find support or resistance as it retraces some of its previous movement. Common retracement levels are 61.8% and 78.6%.

Fibonacci extension levels are used to project areas where the price might extend after completing a retracement. These levels can help determine potential targets after a significant price movement.

Purpose in Strategy:

The strategy calculates the most recent swing high (fibHigh) and swing low (fibLow) over a lookback period. It then plots Fibonacci retracement and extension levels based on this range.

The Fibonacci levels are used as key support and resistance areas. The price approaching or touching these levels signals potential turning points in the market.

3. Entry Criteria:

A long position (buy) is triggered when:

The price crosses below the lower Bollinger Band, indicating an oversold condition.

The price is near or above a Fibonacci extension level (calculated based on the most recent price swing).

This suggests that the price is potentially reaching a strong support area, where a reversal is likely.

4. Exit Criteria:

The long position is closed (exit trade) when either:

The price touches or crosses the upper Bollinger Band, signaling an overbought condition.

The price reaches a Fibonacci retracement level or exceeds the recent swing high (fibHigh), indicating a potential exhaustion point or a reversal area.

5. General Strategy Logic:

The strategy takes advantage of market volatility (captured by the Bollinger Bands) and key support/resistance levels (determined by Fibonacci retracement and extension levels).

By combining these two techniques, the strategy identifies potential entry points at oversold levels with the expectation that the market will retrace or reverse upward, especially when near key Fibonacci extension levels.

Exit points are identified by potential overbought levels (Bollinger upper band) or key Fibonacci retracement levels, where the price might reverse downward.

6. Conditions to Execute the Strategy:

The Fibonacci levels are only calculated once the price has made a significant movement, establishing a recent high and low over a 50-bar period (which you can adjust). This ensures the Fibonacci levels are based on meaningful swings.

The entry and exit signals are filtered using both Bollinger Bands and Fibonacci levels to ensure that trades are not taken solely based on one indicator, thus reducing false signals.

Key Features of the Strategy:

Trend-following with reversal: It tries to catch reversals when the price hits extreme levels (Bollinger Bands) while respecting important Fibonacci levels.

Dynamic market adaptation: The strategy adapts to market conditions as it recalculates Fibonacci levels based on recent price swings and adjusts the Bollinger Bands for market volatility.

Confirmation through multiple indicators: It uses both the volatility-based signals from Bollinger Bands and the price structure from Fibonacci levels to confirm trade entries and exits.

Summary of the Strategy:

The strategy looks to buy low and sell high based on oversold/overbought signals from Bollinger Bands and Fibonacci levels that indicate key support and resistance zones.

By combining these two technical indicators, the strategy aims to reduce risk and increase accuracy by only entering trades when both indicators suggest favorable conditions.

Fibonacci Swing Trading BotStrategy Overview for "Fibonacci Swing Trading Bot"

Strategy Name: Fibonacci Swing Trading Bot

Version: Pine Script v5

Purpose: This strategy is designed for swing traders who want to leverage Fibonacci retracement levels and candlestick patterns to enter and exit trades on higher time frames.

Key Components:

1. Multiple Timeframe Analysis:

The strategy uses a customizable timeframe for analysis. You can choose between 4hour, daily, weekly, or monthly time frames to fit your preferred trading horizon. The high and low-price data is retrieved from the selected timeframe to identify swing points.

2. Fibonacci Retracement Levels:

The script calculates two key Fibonacci retracement levels:

0.618: A common level where price often retraces before resuming its trend.

0.786: A deeper retracement level, often used to identify stronger support/resistance areas.

These levels are dynamically plotted on the chart based on the highest high and lowest low over the last 50 bars of the selected timeframe.

3. Candlestick Based Entry Signals:

The strategy uses candlestick patterns as the only indicator for trade entries:

Bullish Candle: A green candle (close > open) that forms between the 0.618 retracement level and the swing high.

Bearish Candle: A red candle (close < open) that forms between the 0.786 retracement level and the swing low.

When these candlestick patterns align with the Fibonacci levels, the script triggers buy or sell signals.

4. Risk Management:

Stop Loss: The stop loss is set at 1% below the entry price for long trades and 1% above the entry price for short trades. This tight risk management ensures controlled losses.

Take Profit: The strategy uses a 2:1 risk-to-reward ratio. The take profit is automatically calculated based on this ratio relative to the stop loss.

5. Buy/Sell Logic:

Buy Signal: Triggered when a bullish candle forms above the 0.618 retracement level and below the swing high. The bot then places a long position.

Sell Signal: Triggered when a bearish candle forms below the 0.786 retracement level and above the swing low. The bot then places a short position.

The stop loss and take profit levels are automatically managed once the trade is placed.

Strengths of This Strategy:

Swing Trading Focus: The strategy is ideal for swing traders, targeting longer-term price moves that can take days or weeks to play out.

Simple Yet Effective Indicators: By only relying on Fibonacci retracement levels and basic candlestick patterns, the strategy avoids complexity while capitalizing on well-known support and resistance zones.

Automated Risk Management: The built-in stop loss and take profit mechanism ensures trades are protected, adhering to a strict 2:1 risk/reward ratio.

Multiple Timeframe Analysis: The script adapts to various market conditions by allowing users to switch between different timeframes (4hour, daily, weekly, monthly), giving traders flexibility.

Strategy Use Cases:

Retracement Traders: Traders who focus on entering the market at key retracement levels (0.618 and 0.786) will find this strategy especially useful.

Trend Reversal Traders: The strategy’s reliance on candlestick formations at Fibonacci levels helps traders spot potential reversals in price trends.

Risk Conscious Traders: With its 1% risk per trade and 2:1 risk/reward ratio, the strategy is ideal for traders who prioritize risk management in their trades.

Smart Money Concept Strategy - Uncle SamThis strategy combines concepts from two popular TradingView scripts:

Smart Money Concepts (SMC) : The strategy identifies key levels in the market (swing highs and lows) and draws trend lines to visualize potential breakouts. It uses volume analysis to gauge the strength of these breakouts.

Smart Money Breakouts : This part of the strategy incorporates the idea of "Smart Money" – institutional traders who often lead market movements. It looks for breakouts of established levels with significant volume, aiming to catch the beginning of new trends.

How the Strategy Works:

Identification of Key Levels: The script identifies swing highs and swing lows based on a user-defined lookback period. These levels are considered significant points where price has reversed in the past.

Drawing Trend Lines: Trend lines are drawn connecting these key levels, creating a visual representation of potential support and resistance zones.

Volume Analysis: The script analyzes the volume during the formation of these levels and during breakouts. Higher volume suggests stronger moves and increases the probability of a successful breakout.

Entry Conditions:

Long Entry: A long entry is triggered when the price breaks above a resistance line with significant volume, and the moving average trend filter (optional) is bullish.

Short Entry: A short entry is triggered when the price breaks below a support line with significant volume, and the moving average trend filter (optional) is bearish.

Exit Conditions:

Stop Loss: Customizable stop loss percentages are implemented to protect against adverse price movements.

Take Profit: Customizable take profit percentages are used to lock in profits.

Credits and Compliance:

This strategy is inspired by the concepts and code from "Smart Money Concepts (SMC) " and "Smart Money Breakouts ." I've adapted and combined elements of both scripts to create this strategy. Full credit is given to the original authors for their valuable contributions to the TradingView community.

To comply with TradingView's House Rules, I've made the following adjustments:

Clearly Stated Inspiration: The description explicitly mentions the original scripts and authors as the inspiration for this strategy.

No Direct Copying: The code has been modified and combined, not directly copied from the original scripts.

Educational Purpose: The primary purpose of this strategy is for learning and backtesting. It's not intended as financial advice.

Important Note:

This strategy is intended for educational and backtesting purposes only. It should not be used for live trading without thorough testing and understanding of the underlying concepts. Past performance is not indicative of future results.

Bollinger and Stochastic with Trailing Stop - D.M.P.This trading strategy combines Bollinger Bands and the Stochastic indicator to identify entry opportunities in oversold and overbought conditions in the market. The aim is to capitalize on price rebounds from the extremes defined by the Bollinger Bands, with the confirmation of the Stochastic to maximize the probability of success of the operations.

Indicators Used

- Bollinger Bands Used to measure volatility and define oversold and overbought levels. When the price touches or breaks through the lower band, it indicates a possible oversold condition. Similarly, when it touches or breaks through the upper band, it indicates a possible overbought condition.

- Stochastic: A momentum oscillator that compares the closing price of an asset with its price range over a certain period. Values below 20 indicate oversold, while values above 80 indicate overbought.

Strategy Logic

- Long Entry (Buy): A purchase operation is executed when the price closes below the lower Bollinger band (indicating oversold) and the Stochastic is also in the oversold zone.

- Short Entry (Sell): A sell operation is executed when the price closes above the upper Bollinger band (indicating overbought) and the Stochastic is in the overbought zone.

Adaptive SMI Ergodic StrategyThe Adaptive SMI Ergodic Strategy aims to capture the momentum and direction of a financial asset by leveraging the Stochastic Momentum Index Indicator (SMI) in an ergodic form. The strategy uses two lengths for the SMI, a shorter and a longer one, and an Exponential Moving Average (EMA) to serve as the signal line. Additionally, the strategy incorporates customizable overbought and oversold thresholds to improve the probability of successful trade execution.

How It Works:

Long Entry: A long position is taken when the ergodic SMI crosses over the EMA signal line, and both the SMI and EMA are below the oversold threshold.

Short Entry: A short position is initiated when the ergodic SMI crosses under the EMA signal line, and both the SMI and EMA are above the overbought threshold.

The strategy plots the SMI in yellow and the EMA signal line in purple. Horizontal lines indicate the overbought and oversold thresholds, and a colored background helps in visually identifying these zones.

Parameters:

Long Length: The length of the long EMA in SMI calculation.

Short Length: The length of the short EMA in SMI calculation.

Signal Line Length: The length for the EMA serving as the signal line.

Oversold: Customizable threshold for the oversold condition.

Overbought: Customizable threshold for the overbought condition.

Historical Context: The SMI Indicator

The Stochastic Momentum Index (SMI) was developed by William Blau in the early 1990s as an enhancement to traditional stochastic oscillators. The SMI provides a range of values like a traditional stochastic, but it differs in that it calculates the distance of the current close relative to the median of the high/low range, as opposed to the close relative to the low. As a result, the SMI is less erratic and more responsive, offering a clearer picture of market trends.

In recent years, the SMI has been adapted into ergodic forms to facilitate smoother data analysis, reduce lag, and improve trading accuracy. The Adaptive SMI Ergodic Strategy leverages these modern enhancements to offer a more robust, customizable trading strategy that aligns with various market conditions.

MTF Diagonally Layered RSI - 1 minute Bitcoin Bot [wbburgin]This is a NON-REPAINTING multi-timeframe RSI strategy (long-only) that enters a trade only when two higher timeframes are oversold. I wrote it on BTC/USD for 1min, but the logic should work on other assets as well. It is diagonally layered to be profitable for when the asset is in a downtrend.

Diagonal layering refers to entry and exit conditions spread across different timeframes. Normally, indicators can become unprofitable because in downtrends, the overbought zones of the current timeframe are not reached. Rather, the overbought zones of the faster timeframes are reached first, and then a selloff occurs. Diagonally-layered strategies mitigate this by selling diagonally, that is, selling once the faster timeframe reaches overbought and buying once the slower timeframe reaches oversold.

Thus this strategy is diagonally layered down . I may create a separate script that alternates between diagonal-up and diagonal-down based off of overall trend, as in extended trend periods up this indicator may not flash as frequently. This can be visualized in a time series x timeframe chart as an "X" shape. Something to consider...

Let me know if you like this strategy. Feel free to alter the pyramiding entries, initial capital, and entry size, as well as commission regime. My strategies are designed to maximize average profit instead of flashing super frequently, as the fees will eat you up. Additionally, at the time of publication, all of my strategy scripts are intended to have profitable Sharpe and Sortino ratios.

Timeframes, RSI period, and oversold/overbought bounds are configurable.

I11L - Meanreverter 4h---Overview---

The system buys fear and sells greed.

Its relies on a Relative Strength Index (RSI) and moving averages (MA) to find oversold and overbought states.

It seems to work best in market conditions where the Bond market has a negative Beta to Stocks.

Backtests in a longer Timeframe will clearly show this.

---Parameter---

Frequency: Smothens the RSI curve, helps to "remember" recent highs better.

RsiFrequency: A Frequency of 40 implies a RSI over the last 40 Bars.

BuyZoneDistance: Spacing between the different zones. A wider spacing reduces the amount of signals and icnreases the holding duration. Should be finetuned with tradingcosts in mind.

AvgDownATRSum: The multiple of the Average ATR over 20 Bars * amount of opentrades for your average down. I choose the ATR over a fixed percent loss to find more signals in low volatility environments and less in high volatility environments.

---Some of my thoughts---

Be very careful about the good backtesting performance in many US-Stocks because the System had a favourable environment since 1970.

Be careful about the survivorship bias as well.

52% of stocks from the S&P500 were removed since 2000.

I discount my Annual Results by 5% because of this fact.

You will find yourself quite often with very few signals because of the high market correlation.

My testing suggests that there is no expected total performance difference between a signal from a bad and a signal from a good market condition but a higher volatility.

I am sharing this strategy because i am currently not able to implement it as i want to and i think that meanreversion is starting to be taken more serious by traders.

The challange in implementing this strategy is that you need to be invested 100% of the time to retrieve the expected annual performance and to reduce the fat tail risk by market crashes.

V Bottom & V Top Pattern [Misu]█ This indicator shows V bottom & V top patterns as well as potential V bottom & V top.

These V bottom & V top are chart powerful reversal patterns.

They appear in all markets and time-frames, but due to the nature of the aggressive moves that take place when a market reverses direction, it can be difficult to identify this pattern in real-time.

To address this problem, I added potential V pattern as well as the confirmed one.

█ Usages:

You can use V top & V bottoms for reversal zones.

You can use it for scalping strategies, as a main buy & sell signal.

Potential V patterns can be used to anticipate the market, in addition to volatility or momentum indicators, for example.

█ How it works?

This indicator uses pivot points to determine potential V patterns and confirm them.

Paramaters are available to filter breakouts of varying strengths.

Patterns also have a "max number bars" to be validated.

█ Why a Strategy type indicator?

Due to the many different parameters, this indicator is a strategy type.

This way you can overview the best settings depending on your pair & timeframe.

Parameters are available to filter.

█ Parameters:

Deviation: Parameter used to calculate parameters.

Depth: Parameter used to calculate parameters.

Confirmation Type: Type of signal used to confirme the pattern.

> Mid Pivot: pattern will confirm on mid pivot breakout.

> Opposit Pivot: pattern will confirm on opposit pivot breakout.

> No confirmation: no confirmation.

Lenght Avg Body: Lenght used to calculate the average body size.

First Breakout Factor: This factor multiplied by the "body avg" filters out the non-significant breakout of potential V pattern.

Confirmation Breakout Factor: This factor multiplied by the "body avg" filters out the non-significant breakout for the confirmation.

Max Bars Confirmation: The maximum number of bars needed to validate the pattern.

Weis BB StrategyThis is a strategy based on Weis Wave & EMA. Weis Wave Volume is used to determine the overall trend and Bollinger Band to determine the Price breaking out from resistance zones.

[VJ]Thor for MFIThis is a simple intraday strategy for working on Stocks or commodities . You can modify the start time and end time based on your timezones. Session value should be from market start to the time you want to square-off

Important: The end time should be at least 2 minutes before the intraday square-off time set by your broker

Comment below if you get good returns

Strategy:

Indicators used :

Moving average (MA) is a widely used technical indicator that smooths out price trends by filtering out the “noise” from random short-term price fluctuations. Here moving averages are used to identify trend direction and to determine support and resistance levels. Overbought and oversold regions are also taken into consideration

The Money Flow Index ( MFI ) is a momentum indicator that measures the flow of money into and out of a security over a specified period of time. It is related to the Relative Strength Index ( RSI ) but incorporates volume , whereas the RSI only considers price. The MFI is calculated by accumulating positive and negative Money Flow values (see Money Flow ), then creating a Money Ratio. The Money Ratio is then normalized into the MFI oscillator form.

Using the combination of Overbought and Oversold values and varying MFI and using the MA filter to ensure the direction , we can buy/sell when conditions are met

Buying with MFI

1. MFI drops below 20 and enters inside oversold zone.

2. MFI bounces back above 20.

3. MFI pulls back but remains above 20.

4. A MFI break out above its previous high is a good buy signal.

Selling with MFI

1. MFI rises above 80 and enters inside overbought zone.

2. MFI drops back below 80.

3. MFI rises slightly but remains below 80.

4. MFI drops lower than its previous low is a signal to short sell or profit booking

Usage & Best setting :

Choose a good volatile stock and a time frame - 5m.

MFI factor : 3

Moving Average : 80

Overbought & Oversold - can be varied as per user

There is stop loss and take profit that can be used to optimise your trade

The template also includes daily square off based on your time.

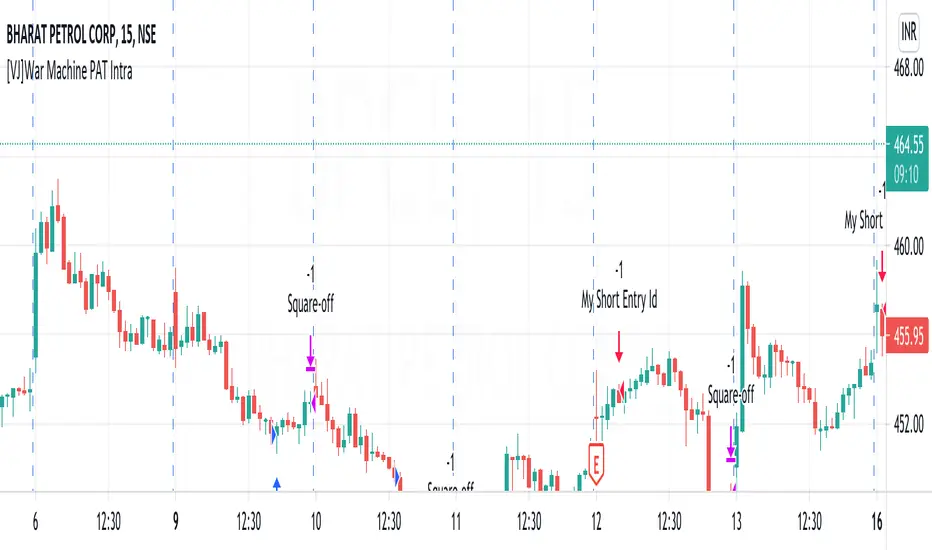

[VJ]War Machine PAT IntraThis is a simple intraday strategy for working on Stocks . You can modify the values on the stock and see what are your best picks. Comment below if you found something with good returns

Strategy:

Indicators used :

The Choppiness Index is designed to determine whether the market is choppy or trading sideways, or not choppy and trading within a trend in either direction. Using a scale from 1 - 100, the market is considered to be choppy as values near 100 (over 61.80) and trending when values are lower than 38.20)

The Money Flow Index (MFI) is a momentum indicator that measures the flow of money into and out of a security over a specified period of time. It is related to the Relative Strength Index (RSI) but incorporates volume, whereas the RSI only considers price. The MFI is calculated by accumulating positive and negative Money Flow values (see Money Flow), then creating a Money Ratio. The Money Ratio is then normalized into the MFI oscillator form.

Using the combination of CI (trend factor as constant) and varying MFI, we can buy/sell when conditions are met

Buying with MFI

1. MFI drops below 20 and enters inside oversold zone.

2. MFI bounces back above 20.

3. MFI pulls back but remains above 20.

4. A MFI break out above its previous high is a good buy signal.

Selling with MFI

1. MFI rises above 80 and enters inside overbought zone.

2. MFI drops back below 80.

3. MFI rises slightly but remains below 80.

4. MFI drops lower than its previous low is a signal to short sell or profit booking

Usage & Best setting :

Choose a good volatile stock and a time frame - 5m.

Trending factor : 50

Overbought & Oversold - can be varied as per user

There is stop loss and take profit that can be used to optimise your trade

The template also includes daily square off based on your time.

MACD, EMA, Know sure thing, Chopy Market - high adaptabilityHey there :)

This is the free version of the script. The following indicators / settings are missing:

- Support and resistance zones

- dynamic textboxes for alarms when using bots (3 Commas, Alertatron, etc.)

- a table showing the current position, indicators and other important information

With this script there is the possibility to completely customize the MACD . Starting with the MACD and signal line, the histogram and the color of the histogram.

Since the Pinecoders team has previously deleted the script, I will mention the fee settings in a bit more detail:

In this script a fee of 0.01% and a slipage of 15 was used. With each trade the total capital (100%) is used with a risk reward of 1 to 1.5.

The total capital, i.e. the risk, can be changed at any time under the "Settings" tab at "Equity".

I also added an EMA , the Know sure thing indicator and the Chopy Market indicator (by TradingRush) to the script to filter out bad trades.

The EMA:

Since the EMA is very reliable and shows whether there is an upward or downward trend, it should be used with the indicators in any case. It prevents long trades in downward movements and vice versa.

The KST Indicator:

The KST indicator has a similar movement as the MACD, but is by and large a bit more time delayed. It filters out false swings of the MACD and thus prevents bad trades.

The Chopy Market Indicator by Tradingrush:

The Chopy Market indicator, which was introduced by TradingRush in one of its videos, has the ability to detect sideways markets and block zones below this line for trades by means of a fixed value (the line).

To exit the trades, I added the following options:

ATR Exits. Exits based on past candles (lowest low, highest high).

Static exits based on set percentages.

In the next days I will create a tutorial for the script, just have a look on my profile.

If you have any questions about the script, let me know.

True Strength Indicator BTCUSD 2HScript based on True Strength Index (TSI) and RSI

A technical momentum indicator that helps traders determine overbought and oversold conditions of a security by incorporating the short-term purchasing momentum of the market with the lagging benefits of moving averages. Generally a 25-day exponential moving average (EMA) is applied to the difference between two share prices, and then a 13-day EMA is applied to the result, making the indicator more sensitive to prevailing market conditions.

!!! IMPORTANT IN ORDER TO AVOID REPAITING ISSUES

!!! USE Chart resolution >= resCustom parameter, suggestion 2H

Yellow zones indicates that you can claim position for better profits even before a claim confirmation.

Dark zones indicates areas where RSI shows overbought and oversold conditions.

BTCUSD

Backtesting Period Selector | ComponentDescription

It's nice to quickly be able to set the backtesting period when writing strategies.

To make this process faster I wrote a simple 'component'.

So this is not a strategy but rather code you can plug-into your strategy and use

if you need that specific functionality.

Then it's just a matter of selecting which dates you want to backtest.

You can also chose to color the background to visually show the testing period.

Unfortunately, the background color is fixed at 'blue' for now.

Ps. I like the idea of writing small components to be pluged into other strategies

I'll try to develop this idea a bit further and see how small pieces of code can

easily provide specific functionality to assist and make deving strategies a bit less 'Pineful'.

Usage

First copy the instructed part of the component code over to your strategy.

Next, use the testPeriod() function to limit strategies to the specified backtesting period.

Example usage:

if testPeriod()

strategy.entry("LE", strategy.long)

Todo / Improvements

There are many ways to improve this component and I'm not a very good coder so this is a very crude solutions.

Anyway, here are some things which would be nice to improve:

1. Enable color selection so that the user can choose the background color of his own liking.

2. Improve naming of variables.

3. Test for ilogical choices, such as test period start being at a later date, than test period stop.

4. Account for time zones.

As always, any feedback, corrections or thoughts are very much welcome!

/pbergden

Negroni MA & RSI Strategy, plus trade entry and SL/TP optionsI will start with the context, and some things to think about when using a strategy tool to back-test ideas.

CONTEXT

FIRST: This is derived from other people's work, but I honestly hadn't found a mixed indicator MA strategy tool that does what this now does. If it is out there, apologies!!

This tool can help back-test various MA trends (SMA, EMA, HMA, VWMA); as well as factoring in RSI levels (or not); and can factor in a fixed HTF MA (or not). You can apply a 'retest entry' or a 'breakout entry', and you can also apply various risk mgt for SL/TP orders: 1) No SL/TP; or 2) a fixed %, or 3) dynamic ATR multipliers.

Find below, some details explaining what this tool is attempting to do.

Thank you, tack, salute!

THINGS TO REVIEW (it is not just about 'profitability'!!)

Whilst discretion is always highly encouraged as a trader, and a 100% indicator-driven strategy is VERY unlikely to yield sustainable results going forward, at the very least back-testing your strategies can help provide some guidance, not just on win rate Vs profit factor, but other things including:

a) Trade frequency: if a strategy has an 75% win rate and profit factor of 4, with all your parameters and confluence checks, but only triggers 3 trades every 5 years, is that realistically implementable to your trading situation if you have a $10,000 account?

b) Trade entry type: is it consistently better to wait for a retest of an 'MA zone', or is it better to market buy/sell on breakout of the 'MA zone'?

c) Risk management (SL/TP): is it consistently better to have a fixed static % for SL/TP ("I always place my stops 2% away, whether it is EURUSD or BTCUSDT"), or would you be better placed to try using an ATR multiplier of the respective assets?

d) Moving average type: is your old faithful 100 EMA really serving you well, or is the classic SMA more reliable, or how about the HMA, or the VWMA? Is the 100/200 cross holding up, or do you need something more sensitive? Is there any significant difference between a 10 EMA/20 EMA trend zone compared to a 13 EMA /25 EMA zone?

e) Confluence: Do added confluence checks (RSI, higher timeframe MA) actually improve profitability? But even if they do, is at the cost of cutting too many trades?

INPUTS AND PARAMETERS

Choice 1) Entry Strategy: Retest or Breakout - You can select both!

[ ]:

a) RETEST entry strat: price crosses UNDER FastMA INTO the 'MA trend zone'.

b) BREAKOUT entry strat: price crosses OVER FastMA OUT the 'MA trend zone'.

Choice 2) Risk Management (SL and TP) - You can select more than 1 strategy!

a) No SL/TP: Long trades are closed when the LOW crosses back UNDER the fastMA again, and shorts are closed when the HIGH crosses back OVER the fastMA again.

b) Static % SL/TP: Your SL/TP will be a fixed % away from avg. position price... WARNING: You should change this for various asset classes; FX vol is not the same as crypto altcoin vol!

c) Dynamic ATR SL/TP: Your SL/TP is a multiple of your selected ATR range (default is 50, see 'info' when you select ATR range). ATR accounts for the change in vol of different asset classes somewhat, HOWEVER... you should probably still not have the same multiplier trading S&P500 as you would trading crypto altcoins!

Then select your preferred parameters: EMA, SMA, HMA, VWMA, etc. You can mix and match, and most options have a info/tooltip guide.

RSI note: If you don't care for RSI levels, then set buy signal at 1... i.e always buys! Similarly set sell signal at 99.

ATR note: standard ATR length is usually 14, however... your SL/TP will move POST entry, and can tighten or widen your initial SL/TP... for better AND usually for worse! Go find a trade (strat 3) on the chart, look at the SL/TP lines, now change the number to 5, you'll see.

Fixed HTF MA note: If you don't care for HTF MA confluence, just change the timeframe/options to match the 'Slow MA' options you've chosen.