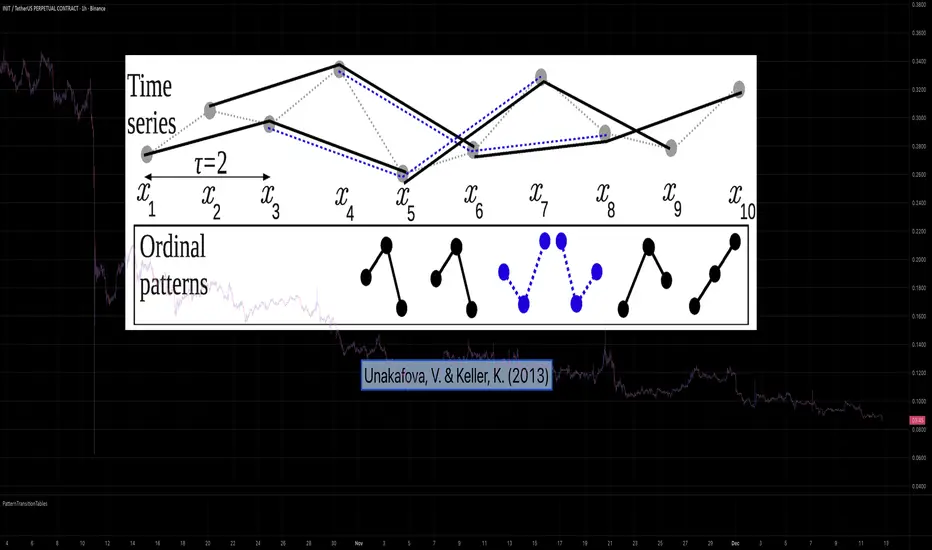

PatternTransitionTablesPatternTransitionTables Library

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 Overview

This library provides precomputed state transition tables to enable ultra-efficient, O(1) computation of Ordinal Patterns. It is designed specifically to support high-performance indicators calculating Permutation Entropy and related complexity measures.

💮 The Problem & Solution

Calculating Permutation Entropy, as introduced by Bandt and Pompe (2002), typically requires computing ordinal patterns within a sliding window at every time step. The standard successive-pattern method (Equations 2+3 in the paper) requires ≤ 4d-1 operations per update.

Unakafova and Keller (2013) demonstrated that successive ordinal patterns "overlap" significantly. By knowing the current pattern index and the relative rank (position l) of just the single new data point, the next pattern index can be determined via a precomputed look-up table. Computing l still requires d comparisons, but the table lookup itself is O(1), eliminating the need for d multiplications and d additions. This reduces total operations from ≤ 4d-1 to ≤ 2d per update (Table 4). This library contains these precomputed tables for orders d = 2 through d = 5.

🌸 --------- 2. THEORETICAL BACKGROUND --------- 🌸

💮 Permutation Entropy

Bandt, C., & Pompe, B. (2002). Permutation entropy: A natural complexity measure for time series.

doi.org

This concept quantifies the complexity of a system by comparing the order of neighbouring values rather than their magnitudes. It is robust against noise and non-linear distortions, making it ideal for financial time series analysis.

💮 Efficient Computation

Unakafova, V. A., & Keller, K. (2013). Efficiently Measuring Complexity on the Basis of Real-World Data.

doi.org

This library implements the transition function φ_d(n, l) described in Equation 5 of the paper. It maps a current pattern index (n) and the position of the new value (l) to the successor pattern, reducing the complexity of updates to constant time O(1).

🌸 --------- 3. LIBRARY FUNCTIONALITY --------- 🌸

💮 Data Structure

The library stores transition matrices as flattened 1D integer arrays. These tables are mathematically rigorous representations of the factorial number system used to enumerate permutations.

💮 Core Function: get_successor()

This is the primary interface for the library for direct pattern updates.

• Input: The current pattern index and the rank position of the incoming price data.

• Process: Routes the request to the specific transition table for the chosen order (d=2 to d=5).

• Output: The integer index of the next ordinal pattern.

💮 Table Access: get_table()

This function returns the entire flattened transition table for a specified dimension. This enables local caching of the table (e.g. in an indicator's init() method), avoiding the overhead of repeated library calls during the calculation loop.

💮 Supported Orders & Terminology

The parameter d is the order of ordinal patterns (following Bandt & Pompe 2002). Each pattern of order d contains (d+1) data points, yielding (d+1)! unique patterns:

• d=2: 3 points → 6 unique patterns, 3 successor positions

• d=3: 4 points → 24 unique patterns, 4 successor positions

• d=4: 5 points → 120 unique patterns, 5 successor positions

• d=5: 6 points → 720 unique patterns, 6 successor positions

Note: d=6 is not implemented. The resulting code size (approx. 191k tokens) exceeds the Pine Script limit of 100k tokens (as of 2025-12).

Statistics

LuxyEnergyIndexThe Luxy Energy Index (LEI) library provides functions to measure price movement exhaustion by analyzing three dimensions: Extension (distance from fair value), Velocity (speed of movement), and Volume (confirmation level).

LEI answers a different question than traditional momentum indicators: instead of "how far has price gone?" (like RSI), LEI asks "how tired is this move?"

This library allows Pine Script developers to integrate LEI calculations into their own indicators and strategies.

How to Import

//@version=6

indicator("My Indicator")

import OrenLuxy/LuxyEnergyIndex/1 as LEI

Main Functions

`lei(src)` → float

Returns the LEI value on a 0-100 scale.

src (optional): Price source, default is `close`

Returns : LEI value (0-100) or `na` if insufficient data (first 50 bars)

leiValue = LEI.lei()

leiValue = LEI.lei(hlc3) // custom source

`leiDetailed(src)` → tuple

Returns LEI with all component values for detailed analysis.

= LEI.leiDetailed()

Returns:

`lei` - Final LEI value (0-100)

`extension` - Distance from VWAP in ATR units

`velocity` - 5-bar price change in ATR units

`volumeZ` - Volume Z-Score

`volumeModifier` - Applied modifier (1.0 = neutral)

`vwap` - VWAP value used

Component Functions

| Function | Description | Returns |

|-----------------------------------|---------------------------------|---------------|

| `calcExtension(src, vwap)` | Distance from VWAP / ATR | float |

| `calcVelocity(src)` | 5-bar price change / ATR | float |

| `calcVolumeZ()` | Volume Z-Score | float |

| `calcVolumeModifier(volZ)` | Volume modifier | float (≥1.0) |

| `getVWAP()` | Auto-detects asset type | float |

Signal Functions

| Function | Description | Returns |

|---------------------------------------------|----------------------------------|-----------|

| `isExhausted(lei, threshold)` | LEI ≥ threshold (default 70) | bool |

| `isSafe(lei, threshold)` | LEI ≤ threshold (default 30) | bool |

| `crossedExhaustion(lei, threshold)` | Crossed into exhaustion | bool |

| `crossedSafe(lei, threshold)` | Crossed into safe zone | bool |

Utility Functions

| Function | Description | Returns |

|----------------------------|-------------------------|-----------|

| `getZone(lei)` | Zone name | string |

| `getColor(lei)` | Recommended color | color |

| `hasEnoughHistory()` | Data check | bool |

| `minBarsRequired()` | Required bars | int (50) |

| `version()` | Library version | string |

Interpretation Guide

| LEI Range | Zone | Meaning |

|-------------|--------------|--------------------------------------------------|

| 0-30 | Safe | Low exhaustion, move may continue |

| 30-50 | Caution | Moderate exhaustion |

| 50-70 | Warning | Elevated exhaustion |

| 70-100 | Exhaustion | High exhaustion, increased reversal risk |

Example: Basic Usage

//@version=6

indicator("LEI Example", overlay=false)

import OrenLuxy/LuxyEnergyIndex/1 as LEI

// Get LEI value

leiValue = LEI.lei()

// Plot with dynamic color

plot(leiValue, "LEI", LEI.getColor(leiValue), 2)

// Reference lines

hline(70, "High", color.red)

hline(30, "Low", color.green)

// Alert on exhaustion

if LEI.crossedExhaustion(leiValue) and barstate.isconfirmed

alert("LEI crossed into exhaustion zone")

Technical Details

Fixed Parameters (by design):

Velocity Period: 5 bars

Volume Period: 20 bars

Z-Score Period: 50 bars

ATR Period: 14

Extension/Velocity Weights: 50/50

Asset Support:

Stocks/Forex: Uses Session VWAP (daily reset)

Crypto: Uses Rolling VWAP (50-bar window) - auto-detected

Edge Cases:

Returns `na` until 50 bars of history

Zero volume: Volume modifier defaults to 1.0 (neutral)

Credits and Acknowledgments

This library builds upon established technical analysis concepts:

VWAP - Industry standard volume-weighted price measure

ATR by J. Welles Wilder Jr. (1978) - Volatility normalization

Z-Score - Statistical normalization method

Volume analysis principles from Volume Spread Analysis (VSA) methodology

Disclaimer

This library is provided for **educational and informational purposes only**. It does not constitute financial advice. Past performance does not guarantee future results. The exhaustion readings are probabilistic indicators, not guarantees of price reversal. Always conduct your own research and use proper risk management when trading.

KernelFunctionsLibrary "KernelFunctions"

This library provides non-repainting kernel functions for Nadaraya-Watson estimator implementations. This allows for easy substition/comparison of different kernel functions for one another in indicators. Furthermore, kernels can easily be combined with other kernels to create newer, more customized kernels.

rationalQuadratic(_src, _lookback, _relativeWeight, startAtBar)

Rational Quadratic Kernel - An infinite sum of Gaussian Kernels of different length scales.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_relativeWeight (simple float) : Relative weighting of time frames. Smaller values resut in a more stretched out curve and larger values will result in a more wiggly curve. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel.

startAtBar (simple int)

Returns: yhat The estimated values according to the Rational Quadratic Kernel.

gaussian(_src, _lookback, startAtBar)

Gaussian Kernel - A weighted average of the source series. The weights are determined by the Radial Basis Function (RBF).

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

startAtBar (simple int)

Returns: yhat The estimated values according to the Gaussian Kernel.

periodic(_src, _lookback, _period, startAtBar)

Periodic Kernel - The periodic kernel (derived by David Mackay) allows one to model functions which repeat themselves exactly.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Periodic Kernel.

locallyPeriodic(_src, _lookback, _period, startAtBar)

Locally Periodic Kernel - The locally periodic kernel is a periodic function that slowly varies with time. It is the product of the Periodic Kernel and the Gaussian Kernel.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Locally Periodic Kernel.

machine_learningLibrary "machine_learning"

euclidean(a, b)

Parameters:

a (array)

b (array)

manhattan(a, b)

Parameters:

a (array)

b (array)

cosine_similarity(a, b)

Parameters:

a (array)

b (array)

cosine_distance(a, b)

Parameters:

a (array)

b (array)

chebyshev(a, b)

Parameters:

a (array)

b (array)

minkowski(a, b, p)

Parameters:

a (array)

b (array)

p (float)

dot_product(a, b)

Parameters:

a (array)

b (array)

vector_norm(arr, p)

Parameters:

arr (array)

p (float)

sigmoid(x)

Parameters:

x (float)

sigmoid_derivative(x)

Parameters:

x (float)

tanh_derivative(x)

Parameters:

x (float)

relu(x)

Parameters:

x (float)

relu_derivative(x)

Parameters:

x (float)

leaky_relu(x, alpha)

Parameters:

x (float)

alpha (float)

leaky_relu_derivative(x, alpha)

Parameters:

x (float)

alpha (float)

elu(x, alpha)

Parameters:

x (float)

alpha (float)

gelu(x)

Parameters:

x (float)

swish(x, beta)

Parameters:

x (float)

beta (float)

softmax(arr)

Parameters:

arr (array)

apply_activation(arr, activation_type, alpha)

Parameters:

arr (array)

activation_type (string)

alpha (float)

normalize_minmax(arr, min_val, max_val)

Parameters:

arr (array)

min_val (float)

max_val (float)

normalize_zscore(arr, mean_val, std_val)

Parameters:

arr (array)

mean_val (float)

std_val (float)

normalize_matrix_cols(m)

Parameters:

m (matrix)

scaler_fit(arr, method)

Parameters:

arr (array)

method (string)

scaler_fit_matrix(m, method)

Parameters:

m (matrix)

method (string)

scaler_transform(scaler, arr)

Parameters:

scaler (ml_scaler)

arr (array)

scaler_transform_matrix(scaler, m)

Parameters:

scaler (ml_scaler)

m (matrix)

clip(x, lo, hi)

Parameters:

x (float)

lo (float)

hi (float)

clip_array(arr, lo, hi)

Parameters:

arr (array)

lo (float)

hi (float)

loss_mse(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_rmse(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_mae(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_binary_crossentropy(predicted, actual)

Parameters:

predicted (array)

actual (array)

loss_huber(predicted, actual, delta)

Parameters:

predicted (array)

actual (array)

delta (float)

gradient_step(weights, gradients, lr)

Parameters:

weights (array)

gradients (array)

lr (float)

adam_step(weights, gradients, m, v, lr, beta1, beta2, t, epsilon)

Parameters:

weights (array)

gradients (array)

m (array)

v (array)

lr (float)

beta1 (float)

beta2 (float)

t (int)

epsilon (float)

clip_gradients(gradients, max_norm)

Parameters:

gradients (array)

max_norm (float)

lr_decay(initial_lr, decay_rate, step)

Parameters:

initial_lr (float)

decay_rate (float)

step (int)

lr_cosine_annealing(initial_lr, min_lr, step, total_steps)

Parameters:

initial_lr (float)

min_lr (float)

step (int)

total_steps (int)

knn_create(k, distance_type)

Parameters:

k (int)

distance_type (string)

knn_fit(model, X, y)

Parameters:

model (ml_knn)

X (matrix)

y (array)

knn_predict(model, x)

Parameters:

model (ml_knn)

x (array)

knn_predict_proba(model, x)

Parameters:

model (ml_knn)

x (array)

knn_batch_predict(model, X)

Parameters:

model (ml_knn)

X (matrix)

linreg_fit(X, y)

Parameters:

X (matrix)

y (array)

ridge_fit(X, y, lambda)

Parameters:

X (matrix)

y (array)

lambda (float)

linreg_predict(model, x)

Parameters:

model (ml_linreg)

x (array)

linreg_predict_batch(model, X)

Parameters:

model (ml_linreg)

X (matrix)

linreg_score(model, X, y)

Parameters:

model (ml_linreg)

X (matrix)

y (array)

logreg_create(n_features, learning_rate, iterations)

Parameters:

n_features (int)

learning_rate (float)

iterations (int)

logreg_fit(model, X, y)

Parameters:

model (ml_logreg)

X (matrix)

y (array)

logreg_predict_proba(model, x)

Parameters:

model (ml_logreg)

x (array)

logreg_predict(model, x, threshold)

Parameters:

model (ml_logreg)

x (array)

threshold (float)

logreg_batch_predict(model, X, threshold)

Parameters:

model (ml_logreg)

X (matrix)

threshold (float)

nb_create(n_classes)

Parameters:

n_classes (int)

nb_fit(model, X, y)

Parameters:

model (ml_nb)

X (matrix)

y (array)

nb_predict_proba(model, x)

Parameters:

model (ml_nb)

x (array)

nb_predict(model, x)

Parameters:

model (ml_nb)

x (array)

nn_create(layers, activation)

Parameters:

layers (array)

activation (string)

nn_forward(model, x)

Parameters:

model (ml_nn)

x (array)

nn_predict_class(model, x)

Parameters:

model (ml_nn)

x (array)

accuracy(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

precision(y_true, y_pred, positive_class)

Parameters:

y_true (array)

y_pred (array)

positive_class (int)

recall(y_true, y_pred, positive_class)

Parameters:

y_true (array)

y_pred (array)

positive_class (int)

f1_score(y_true, y_pred, positive_class)

Parameters:

y_true (array)

y_pred (array)

positive_class (int)

r_squared(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

mse(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

rmse(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

mae(y_true, y_pred)

Parameters:

y_true (array)

y_pred (array)

confusion_matrix(y_true, y_pred, n_classes)

Parameters:

y_true (array)

y_pred (array)

n_classes (int)

sliding_window(data, window_size)

Parameters:

data (array)

window_size (int)

train_test_split(X, y, test_ratio)

Parameters:

X (matrix)

y (array)

test_ratio (float)

create_binary_labels(data, threshold)

Parameters:

data (array)

threshold (float)

lag_matrix(data, n_lags)

Parameters:

data (array)

n_lags (int)

signal_to_position(prediction, threshold_long, threshold_short)

Parameters:

prediction (float)

threshold_long (float)

threshold_short (float)

confidence_sizing(probability, max_size, min_confidence)

Parameters:

probability (float)

max_size (float)

min_confidence (float)

kelly_sizing(win_rate, avg_win, avg_loss, max_fraction)

Parameters:

win_rate (float)

avg_win (float)

avg_loss (float)

max_fraction (float)

sharpe_ratio(returns, risk_free_rate)

Parameters:

returns (array)

risk_free_rate (float)

sortino_ratio(returns, risk_free_rate)

Parameters:

returns (array)

risk_free_rate (float)

max_drawdown(equity)

Parameters:

equity (array)

atr_stop_loss(entry_price, atr, multiplier, is_long)

Parameters:

entry_price (float)

atr (float)

multiplier (float)

is_long (bool)

risk_reward_take_profit(entry_price, stop_loss, ratio)

Parameters:

entry_price (float)

stop_loss (float)

ratio (float)

ensemble_vote(predictions)

Parameters:

predictions (array)

ensemble_weighted_average(predictions, weights)

Parameters:

predictions (array)

weights (array)

smooth_prediction(current, previous, alpha)

Parameters:

current (float)

previous (float)

alpha (float)

regime_classifier(volatility, trend_strength, vol_threshold, trend_threshold)

Parameters:

volatility (float)

trend_strength (float)

vol_threshold (float)

trend_threshold (float)

ml_knn

Fields:

k (series int)

distance_type (series string)

X_train (matrix)

y_train (array)

ml_linreg

Fields:

coefficients (array)

intercept (series float)

lambda (series float)

ml_logreg

Fields:

weights (array)

bias (series float)

learning_rate (series float)

iterations (series int)

ml_nn

Fields:

layers (array)

weights (matrix)

biases (array)

weight_offsets (array)

bias_offsets (array)

activation (series string)

ml_nb

Fields:

class_priors (array)

means (matrix)

variances (matrix)

n_classes (series int)

ml_scaler

Fields:

min_vals (array)

max_vals (array)

means (array)

stds (array)

method (series string)

ml_train_result

Fields:

loss_history (array)

final_loss (series float)

converged (series bool)

iterations_run (series int)

ml_prediction

Fields:

class_label (series int)

probability (series float)

probabilities (array)

value (series float)

CEDEARDataLibrary "CEDEARData"

getUnderlying(cedearTicker)

Parameters:

cedearTicker (simple string)

getRatio(cedearTicker)

Parameters:

cedearTicker (simple string)

getCurrency(cedearTicker)

Parameters:

cedearTicker (simple string)

isValidCedear(cedearTicker)

Parameters:

cedearTicker (simple string)

RLSR logreg_support_libLibrary "logreg_support_lib"

sigmoid(z)

Parameters:

z (float)

prng01(seed1, seed2)

Parameters:

seed1 (float)

seed2 (float)

normalize(value, minval, maxval)

Parameters:

value (float)

minval (float)

maxval (float)

calcpercentilefast(arr, percentile)

Parameters:

arr (array)

percentile (float)

calcpercentile_series_sampled(s, length, percentile, stride)

Parameters:

s (float)

length (int)

percentile (float)

stride (int)

calcRangeWithLog(value, minval, maxval, uselog)

Parameters:

value (float)

minval (float)

maxval (float)

uselog (bool)

calcMomentumAdvanced(src, length, momType)

Parameters:

src (float)

length (simple int)

momType (string)

normalizeMomentumByType(rawMom, momType, momMin, momMax, momNorm)

Parameters:

rawMom (float)

momType (string)

momMin (float)

momMax (float)

momNorm (float)

normalizeMomentumByTypeExt(rawMom, momType, momMin, momMax, momNorm, bouncingdecay)

Parameters:

rawMom (float)

momType (string)

momMin (float)

momMax (float)

momNorm (float)

bouncingdecay (float)

calcrollingstddev(src, length)

Parameters:

src (float)

length (int)

addlog(buffer, level, msg)

Parameters:

buffer (string)

level (string)

msg (string)

calcfeaturecorrelation(x1, x2)

Parameters:

x1 (array)

x2 (array)

calcnoiseratio(src, lookback)

Parameters:

src (float)

lookback (int)

calccompatibilityscore(x1, x2)

Parameters:

x1 (array)

x2 (array)

getfuturereturn(offset, returnlookback)

Parameters:

offset (int)

returnlookback (int)

calculatema(source, length, matype)

Parameters:

source (float)

length (simple int)

matype (string)

adaptive_trigger_for_source(src, enabled, freeze, lookback, threshold, volahistory)

Parameters:

src (float)

enabled (bool)

freeze (bool)

lookback (int)

threshold (float)

volahistory (array)

checkadaptivetrigger5(s1, enabled1, freeze1, hist1, s2, enabled2, freeze2, hist2, s3, enabled3, freeze3, hist3, s4, enabled4, freeze4, hist4, s5, enabled5, freeze5, hist5, lookback, threshold)

Parameters:

s1 (float)

enabled1 (bool)

freeze1 (bool)

hist1 (array)

s2 (float)

enabled2 (bool)

freeze2 (bool)

hist2 (array)

s3 (float)

enabled3 (bool)

freeze3 (bool)

hist3 (array)

s4 (float)

enabled4 (bool)

freeze4 (bool)

hist4 (array)

s5 (float)

enabled5 (bool)

freeze5 (bool)

hist5 (array)

lookback (int)

threshold (float)

ring_start_index(rb_write_idx, rb_count, rb_cap)

Parameters:

rb_write_idx (int)

rb_count (int)

rb_cap (int)

reversalLibrary "reversals"

psar(af_start, af_increment, af_max)

Calculates Parabolic Stop And Reverse (SAR)

Parameters:

af_start (simple float) : Initial acceleration factor (Wilder's original: 0.02)

af_increment (simple float) : Acceleration factor increment per new extreme (Wilder's original: 0.02)

af_max (simple float) : Maximum acceleration factor (Wilder's original: 0.20)

Returns: SAR value (stop level for current trend)

fractals()

Detects Williams Fractal patterns (5-bar pattern)

Returns: Tuple with fractal values (na if no fractal)

swings(lookback, source_high, source_low)

Detects swing highs and swing lows using lookback period

Parameters:

lookback (simple int) : Number of bars on each side to confirm swing point

source_high (float) : Price series for swing high detection (typically high)

source_low (float) : Price series for swing low detection (typically low)

Returns: Tuple with swing point values (na if no swing)

pivot(tf)

Calculates classic/standard/floor pivot points

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotcam(tf)

Calculates Camarilla pivot points with 8 levels for short-term trading

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotdem(tf)

Calculates d-mark pivot points with conditional open/close logic

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels (only 3 levels)

pivotext(tf)

Calculates extended traditional pivot points with R4-R5 and S4-S5 levels

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotfib(tf)

Calculates Fibonacci pivot points using Fibonacci ratios

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotwood(tf)

Calculates Woodie's pivot points with weighted closing price

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

LibVeloLibrary "LibVelo"

This library provides a sophisticated framework for **Velocity

Profile (Flow Rate)** analysis. It measures the physical

speed of trading at specific price levels by relating volume

to the time spent at those levels.

## Core Concept: Market Velocity

Unlike Volume Profiles, which only answer "how much" traded,

Velocity Profiles answer "how fast" it traded.

It is calculated as:

`Velocity = Volume / Duration`

This metric (contracts per second) reveals hidden market

dynamics invisible to pure Volume or TPO profiles:

1. **High Velocity (Fast Flow):**

* **Aggression:** Initiative buyers/sellers hitting market

orders rapidly.

* **Liquidity Vacuum:** Price slips through a level because

order book depth is thin (low resistance).

2. **Low Velocity (Slow Flow):**

* **Absorption:** High volume but very slow price movement.

Indicates massive passive limit orders ("Icebergs").

* **Apathy:** Little volume over a long time. Lack of

interest from major participants.

## Architecture: Triple-Engine Composition

To ensure maximum performance while offering full statistical

depth for all metrics, this library utilises **object

composition** with a lazy evaluation strategy:

#### Engine A: The Master (`vpVol`)

* **Role:** Standard Volume Profile.

* **Purpose:** Maintains the "ground truth" of volume distribution,

price buckets, and ranges.

#### Engine B: The Time Container (`vpTime`)

* **Role:** specialized container for time duration (in ms).

* **Hack:** It repurposes standard volume arrays (specifically

`aBuy`) to accumulate time duration for each bucket.

#### Engine C: The Calculator (`vpVelo`)

* **Role:** Temporary scratchpad for derived metrics.

* **Purpose:** When complex statistics (like Value Area or Skewness)

are requested for **Velocity**, this engine is assembled

on-demand to leverage the full statistical power of `LibVPrf`

without rewriting complex algorithms.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

create(buckets, rangeUp, rangeLo, dynamic, valueArea, allot, estimator, cdfSteps, split, trendLen)

Construct a new `Velo` controller, initializing its engines.

Parameters:

buckets (int) : series int Number of price buckets ≥ 1.

rangeUp (float) : series float Upper price bound (absolute).

rangeLo (float) : series float Lower price bound (absolute).

dynamic (bool) : series bool Flag for dynamic adaption of profile ranges.

valueArea (int) : series int Percentage for Value Area (1..100).

allot (series AllotMode) : series AllotMode Allocation mode `Classic` or `PDF` (default `PDF`).

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : series PriceEst PDF model for distribution attribution (default `Uniform`).

cdfSteps (int) : series int Resolution for PDF integration (default 20).

split (series SplitMode) : series SplitMode Buy/Sell split for the master volume engine (default `Classic`).

trendLen (int) : series int Look‑back for trend factor in dynamic split (default 3).

Returns: Velo Freshly initialised velocity profile.

method clone(self)

Create a deep copy of the composite profile.

Namespace types: Velo

Parameters:

self (Velo) : Velo Profile object to copy.

Returns: Velo A completely independent clone.

method clear(self)

Reset all engines and accumulators.

Namespace types: Velo

Parameters:

self (Velo) : Velo Profile object to clear.

Returns: Velo Cleared profile (chaining).

method merge(self, srcVolBuy, srcVolSell, srcTime, srcRangeUp, srcRangeLo, srcVolCvd, srcVolCvdHi, srcVolCvdLo)

Merges external data (Volume and Time) into the current profile.

Automatically handles resizing and re-bucketing if ranges differ.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

srcVolBuy (array) : array Source Buy Volume bucket array.

srcVolSell (array) : array Source Sell Volume bucket array.

srcTime (array) : array Source Time bucket array (ms).

srcRangeUp (float) : series float Upper price bound of the source data.

srcRangeLo (float) : series float Lower price bound of the source data.

srcVolCvd (float) : series float Source Volume CVD final value.

srcVolCvdHi (float) : series float Source Volume CVD High watermark.

srcVolCvdLo (float) : series float Source Volume CVD Low watermark.

Returns: Velo `self` (chaining).

method addBar(self, offset)

Main data ingestion. Distributes Volume and Time to buckets.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

offset (int) : series int Offset of the bar to add (default 0).

Returns: Velo `self` (chaining).

method setBuckets(self, buckets)

Sets the number of buckets for the profile.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

buckets (int) : series int New number of buckets.

Returns: Velo `self` (chaining).

method setRanges(self, rangeUp, rangeLo)

Sets the price range for the profile.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

rangeUp (float) : series float New upper price bound.

rangeLo (float) : series float New lower price bound.

Returns: Velo `self` (chaining).

method setValueArea(self, va)

Set the percentage of volume/time for the Value Area.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

va (int) : series int New Value Area percentage (0..100).

Returns: Velo `self` (chaining).

method getBuckets(self)

Returns the current number of buckets in the profile.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns: series int The number of buckets.

method getRanges(self)

Returns the current price range of the profile.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns:

rangeUp series float The upper price bound of the profile.

rangeLo series float The lower price bound of the profile.

method getArrayBuyVol(self)

Returns the internal raw data array for **Buy Volume** directly.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns: array The internal array for buy volume.

method getArraySellVol(self)

Returns the internal raw data array for **Sell Volume** directly.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns: array The internal array for sell volume.

method getArrayTime(self)

Returns the internal raw data array for **Time** (in ms) directly.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns: array The internal array for time duration.

method getArrayBuyVelo(self)

Returns the internal raw data array for **Buy Velocity** directly.

Automatically executes _assemble() if data is dirty.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns: array The internal array for buy velocity.

method getArraySellVelo(self)

Returns the internal raw data array for **Sell Velocity** directly.

Automatically executes _assemble() if data is dirty.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

Returns: array The internal array for sell velocity.

method getBucketBuyVol(self, idx)

Returns the **Buy Volume** of a specific bucket.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

idx (int) : series int The index of the bucket.

Returns: series float The buy volume.

method getBucketSellVol(self, idx)

Returns the **Sell Volume** of a specific bucket.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

idx (int) : series int The index of the bucket.

Returns: series float The sell volume.

method getBucketTime(self, idx)

Returns the raw accumulated time (in ms) spent in a specific bucket.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

idx (int) : series int The index of the bucket.

Returns: series float The time in milliseconds.

method getBucketBuyVelo(self, idx)

Returns the **Buy Velocity** (Aggressive Buy Flow) of a bucket.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

idx (int) : series int The index of the bucket.

Returns: series float The buy velocity in .

method getBucketSellVelo(self, idx)

Returns the **Sell Velocity** (Aggressive Sell Flow) of a bucket.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

idx (int) : series int The index of the bucket.

Returns: series float The sell velocity in .

method getBktBnds(self, idx)

Returns the price boundaries of a specific bucket.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

idx (int) : series int The index of the bucket.

Returns:

up series float The upper price bound of the bucket.

lo series float The lower price bound of the bucket.

method getPoc(self, target)

Returns Point of Control (POC) information for the specified target metric.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns:

pocIdx series int The index of the POC bucket.

pocPrice series float The mid-price of the POC bucket.

method getVA(self, target)

Returns Value Area (VA) information for the specified target metric.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns:

vaUpIdx series int The index of the upper VA bucket.

vaUpPrice series float The upper price bound of the VA.

vaLoIdx series int The index of the lower VA bucket.

vaLoPrice series float The lower price bound of the VA.

method getMedian(self, target)

Returns the Median price for the specified target metric distribution.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns:

medianIdx series int The index of the bucket containing the median.

medianPrice series float The median price.

method getAverage(self, target)

Returns the weighted average price (VWAP/TWAP) for the specified target.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns:

avgIdx series int The index of the bucket containing the average.

avgPrice series float The weighted average price.

method getStdDev(self, target)

Returns the standard deviation for the specified target distribution.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns: series float The standard deviation.

method getSkewness(self, target)

Returns the skewness for the specified target distribution.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns: series float The skewness.

method getKurtosis(self, target)

Returns the excess kurtosis for the specified target distribution.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns: series float The excess kurtosis.

method getSegments(self, target)

Returns the fundamental unimodal segments for the specified target metric.

Calculates on-demand if the target is 'Velocity' and data changed.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns: matrix A 2-column matrix where each row is an pair.

method getCvd(self, target)

Returns Cumulative Volume/Velo Delta (CVD) information for the target metric.

Namespace types: Velo

Parameters:

self (Velo) : Velo The profile object.

target (series Metric) : Metric The data aspect to analyse (Volume, Time, Velocity).

Returns:

cvd series float The final delta value.

cvdHi series float The historical high-water mark of the delta.

cvdLo series float The historical low-water mark of the delta.

Velo

Velo Composite Velocity Profile Controller.

Fields:

_vpVol (VPrf type from AustrianTradingMachine/LibVPrf/2) : LibVPrf.VPrf Engine A: Master Volume source.

_vpTime (VPrf type from AustrianTradingMachine/LibVPrf/2) : LibVPrf.VPrf Engine B: Time duration container (ms).

_vpVelo (VPrf type from AustrianTradingMachine/LibVPrf/2) : LibVPrf.VPrf Engine C: Scratchpad for velocity stats.

_aTime (array) : array Pointer alias to `vpTime.aBuy` (Time storage).

_valueArea (series float) : int Percentage of total volume to include in the Value Area (1..100)

_estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : LibBrSt.PriceEst PDF model for distribution attribution.

_allot (series AllotMode) : AllotMode Attribution model (Classic or PDF).

_cdfSteps (series int) : int Integration resolution for PDF.

_isDirty (series bool) : bool Lazy evaluation flag for vpVelo.

TraderMathLibrary "TraderMath"

A collection of essential trading utilities and mathematical functions used for technical analysis,

including DEMA, Fisher Transform, directional movement, and ADX calculations.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

roundVal(val)

Constrains a value to the range .

Parameters:

val (float) : (float) Value to constrain.

Returns: (float) Value limited to the range .

fisherTransform(length)

Computes the Fisher Transform oscillator, enhancing turning point sensitivity.

Parameters:

length (int) : (int) Lookback length used to normalize price within the high-low range.

Returns: (float) Fisher Transform value.

dirmov(len)

Calculates the Plus and Minus Directional Movement components (DI+ and DI−).

Parameters:

len (simple int) : (int) Lookback length for directional movement.

Returns: (float ) Array containing .

adx(dilen, adxlen)

Computes the Average Directional Index (ADX) based on DI+ and DI−.

Parameters:

dilen (simple int) : (int) Lookback length for directional movement calculation.

adxlen (simple int) : (int) Smoothing length for ADX computation.

Returns: (float) Average Directional Index value (0–100).

ChainAggLib - library for aggregation of main chain tickersLibrary "ChainAggLib"

ChainAggLib — token -> main protocol coin (chain) and top-5 exchange tickers for volume aggregation.

Library only (no plots). All helpers are pure functions and do not modify globals.

norm_sym(s)

Parameters:

s (string)

get_base_from_symbol(full_symbol)

Parameters:

full_symbol (string)

get_chain_for_token(token_symbol)

Parameters:

token_symbol (string)

get_top5_exchange_tickers_for_chain(chain_code)

Parameters:

chain_code (string)

get_top5_exchange_tickers_for_token(token_symbol)

Parameters:

token_symbol (string)

join_tickers(arr)

Parameters:

arr (array)

contains_symbol(arr, symbol)

Parameters:

arr (array)

symbol (string)

contains_current(arr)

Parameters:

arr (array)

get_arr_for_current_token()

get_chain_for_current()

LibVPrfLibrary "LibVPrf"

This library provides an object-oriented framework for volume

profile analysis in Pine Script®. It is built around the `VProf`

User-Defined Type (UDT), which encapsulates all data, settings,

and statistical metrics for a single profile, enabling stateful

analysis with on-demand calculations.

Key Features:

1. **Object-Oriented Design (UDT):** The library is built around

the `VProf` UDT. This object encapsulates all profile data

and provides methods for its full lifecycle management,

including creation, cloning, clearing, and merging of profiles.

2. **Volume Allocation (`AllotMode`):** Offers two methods for

allocating a bar's volume:

- **Classic:** Assigns the entire bar's volume to the close

price bucket.

- **PDF:** Distributes volume across the bar's range using a

statistical price distribution model from the `LibBrSt` library.

3. **Buy/Sell Volume Splitting (`SplitMode`):** Provides methods

for classifying volume into buying and selling pressure:

- **Classic:** Classifies volume based on the bar's color (Close vs. Open).

- **Dynamic:** A specific model that analyzes candle structure

(body vs. wicks) and a short-term trend factor to

estimate the buy/sell share at each price level.

4. **Statistical Analysis (On-Demand):** Offers a suite of

statistical metrics calculated using a "Lazy Evaluation"

pattern (computed only when requested via `get...` methods):

- **Central Tendency:** Point of Control (POC), VWAP, and Median.

- **Dispersion:** Value Area (VA) and Population Standard Deviation.

- **Shape:** Skewness and Excess Kurtosis.

- **Delta:** Cumulative Volume Delta, including its

historical high/low watermarks.

5. **Structural Analysis:** Includes a parameter-free method

(`getSegments`) to decompose a profile into its fundamental

unimodal segments, allowing for modality detection (e.g.,

identifying bimodal profiles).

6. **Dynamic Profile Management:**

- **Auto-Fitting:** Profiles set to `dynamic = true` will

automatically expand their price range to fit new data.

- **Manipulation:** The resolution, price range, and Value Area

of a dynamic profile can be changed at any time. This

triggers a resampling process that uses a **linear

interpolation model** to re-bucket existing volume.

- **Assumption:** Non-dynamic profiles are fixed and will throw

a `runtime.error` if `addBar` is called with data

outside their initial range.

7. **Bucket-Level Access:** Provides getter methods for direct

iteration and analysis of the raw buy/sell volume and price

boundaries of each individual price bucket.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

create(buckets, rangeUp, rangeLo, dynamic, valueArea, allot, estimator, cdfSteps, split, trendLen)

Construct a new `VProf` object with fixed bucket count & range.

Parameters:

buckets (int) : series int number of price buckets ≥ 1

rangeUp (float) : series float upper price bound (absolute)

rangeLo (float) : series float lower price bound (absolute)

dynamic (bool) : series bool Flag for dynamic adaption of profile ranges

valueArea (int) : series int Percentage of total volume to include in the Value Area (1..100)

allot (series AllotMode) : series AllotMode Allocation mode `classic` or `pdf` (default `classic`)

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : series LibBrSt.PriceEst PDF model when `model == PDF`. (deflault = 'uniform')

cdfSteps (int) : series int even #sub-intervals for Simpson rule (default 20)

split (series SplitMode) : series SplitMode Buy/Sell determination (default `classic`)

trendLen (int) : series int Look‑back bars for trend factor (default 3)

Returns: VProf freshly initialised profile

method clone(self)

Create a deep copy of the volume profile.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object to copy

Returns: VProf A new, independent copy of the profile

method clear(self)

Reset all bucket tallies while keeping configuration intact.

Namespace types: VProf

Parameters:

self (VProf) : VProf profile object

Returns: VProf cleared profile (chaining)

method merge(self, srcABuy, srcASell, srcRangeUp, srcRangeLo, srcCvd, srcCvdHi, srcCvdLo)

Merges volume data from a source profile into the current profile.

If resizing is needed, it performs a high-fidelity re-bucketing of existing

volume using a linear interpolation model inferred from neighboring buckets,

preventing aliasing artifacts and ensuring accurate volume preservation.

Namespace types: VProf

Parameters:

self (VProf) : VProf The target profile object to merge into.

srcABuy (array) : array The source profile's buy volume bucket array.

srcASell (array) : array The source profile's sell volume bucket array.

srcRangeUp (float) : series float The upper price bound of the source profile.

srcRangeLo (float) : series float The lower price bound of the source profile.

srcCvd (float) : series float The final Cumulative Volume Delta (CVD) value of the source profile.

srcCvdHi (float) : series float The historical high-water mark of the CVD from the source profile.

srcCvdLo (float) : series float The historical low-water mark of the CVD from the source profile.

Returns: VProf `self` (chaining), now containing the merged data.

method addBar(self, offset)

Add current bar’s volume to the profile (call once per realtime bar).

classic mode: allocates all volume to the close bucket and classifies

by `close >= open`. PDF mode: distributes volume across buckets by the

estimator’s CDF mass. For `split = dynamic`, the buy/sell share per

price is computed via context-driven piecewise s(u).

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

offset (int) : series int To offset the calculated bar

Returns: VProf `self` (method chaining)

method setBuckets(self, buckets)

Sets the number of buckets for the volume profile.

Behavior depends on the `isDynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-bucketing to a new resolution.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

buckets (int) : series int The new number of buckets

Returns: VProf `self` (chaining)

method setRanges(self, rangeUp, rangeLo)

Sets the price range for the volume profile.

Behavior depends on the `dynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-bucketing existing volume.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

rangeUp (float) : series float The new upper price bound

rangeLo (float) : series float The new lower price bound

Returns: VProf `self` (chaining)

method setValueArea(self, valueArea)

Set the percentage of volume for the Value Area. If the value

changes, the profile is finalized again.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

valueArea (int) : series int The new Value Area percentage (0..100)

Returns: VProf `self` (chaining)

method getBktBuyVol(self, idx)

Get Buy volume of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns: series float Buy volume ≥ 0

method getBktSellVol(self, idx)

Get Sell volume of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns: series float Sell volume ≥ 0

method getBktBnds(self, idx)

Get Bounds of a bucket.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

idx (int) : series int Bucket index

Returns:

up series float The upper price bound of the bucket.

lo series float The lower price bound of the bucket.

method getPoc(self)

Get POC information.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

Returns:

pocIndex series int The index of the Point of Control (POC) bucket.

pocPrice. series float The mid-price of the Point of Control (POC) bucket.

method getVA(self)

Get Value Area (VA) information.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object

Returns:

vaUpIndex series int The index of the upper bound bucket of the Value Area.

vaUpPrice series float The upper price bound of the Value Area.

vaLoIndex series int The index of the lower bound bucket of the Value Area.

vaLoPrice series float The lower price bound of the Value Area.

method getMedian(self)

Get the profile's median price and its bucket index. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

medianIndex series int The index of the bucket containing the Median.

medianPrice series float The Median price of the profile.

method getVwap(self)

Get the profile's VWAP and its bucket index. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

vwapIndex series int The index of the bucket containing the VWAP.

vwapPrice series float The Volume Weighted Average Price of the profile.

method getStdDev(self)

Get the profile's volume-weighted standard deviation. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Standard deviation of the profile.

method getSkewness(self)

Get the profile's skewness. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Skewness of the profile.

method getKurtosis(self)

Get the profile's excess kurtosis. Calculates the value on-demand if stale.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns: series float The Kurtosis of the profile.

method getSegments(self)

Get the profile's fundamental unimodal segments. Calculates on-demand if stale.

Uses a parameter-free, pivot-based recursive algorithm.

Namespace types: VProf

Parameters:

self (VProf) : VProf The profile object.

Returns: matrix A 2-column matrix where each row is an pair.

method getCvd(self)

Cumulative Volume Delta (CVD) like metric over all buckets.

Namespace types: VProf

Parameters:

self (VProf) : VProf Profile object.

Returns:

cvd series float The final Cumulative Volume Delta (Total Buy Vol - Total Sell Vol).

cvdHi series float The running high-water mark of the CVD as volume was added.

cvdLo series float The running low-water mark of the CVD as volume was added.

VProf

VProf Bucketed Buy/Sell volume profile plus meta information.

Fields:

buckets (series int) : int Number of price buckets (granularity ≥1)

rangeUp (series float) : float Upper price range (absolute)

rangeLo (series float) : float Lower price range (absolute)

dynamic (series bool) : bool Flag for dynamic adaption of profile ranges

valueArea (series int) : int Percentage of total volume to include in the Value Area (1..100)

allot (series AllotMode) : AllotMode Allocation mode `classic` or `pdf`

estimator (series PriceEst enum from AustrianTradingMachine/LibBrSt/1) : LibBrSt.PriceEst Price density model when `model == PDF`

cdfSteps (series int) : int Simpson integration resolution (even ≥2)

split (series SplitMode) : SplitMode Buy/Sell split strategy per bar

trendLen (series int) : int Look‑back length for trend factor (≥1)

maxBkt (series int) : int User-defined number of buckets (unclamped)

aBuy (array) : array Buy volume per bucket

aSell (array) : array Sell volume per bucket

cvd (series float) : float Final Cumulative Volume Delta (Total Buy Vol - Total Sell Vol).

cvdHi (series float) : float Running high-water mark of the CVD as volume was added.

cvdLo (series float) : float Running low-water mark of the CVD as volume was added.

poc (series int) : int Index of max‑volume bucket (POC). Is `na` until calculated.

vaUp (series int) : int Index of upper Value‑Area bound. Is `na` until calculated.

vaLo (series int) : int Index of lower value‑Area bound. Is `na` until calculated.

median (series float) : float Median price of the volume distribution. Is `na` until calculated.

vwap (series float) : float Profile VWAP (Volume Weighted Average Price). Is `na` until calculated.

stdDev (series float) : float Standard Deviation of volume around the VWAP. Is `na` until calculated.

skewness (series float) : float Skewness of the volume distribution. Is `na` until calculated.

kurtosis (series float) : float Excess Kurtosis of the volume distribution. Is `na` until calculated.

segments (matrix) : matrix A 2-column matrix where each row is an pair. Is `na` until calculated.

LibBrStLibrary "LibBrSt"

This is a library for quantitative analysis, designed to estimate

the statistical properties of price movements *within* a single

OHLC bar, without requiring access to tick data. It provides a

suite of estimators based on various statistical and econometric

models, allowing for analysis of intra-bar volatility and

price distribution.

Key Capabilities:

1. **Price Distribution Models (`PriceEst`):** Provides a selection

of estimators that model intra-bar price action as a probability

distribution over the range. This allows for the

calculation of the intra-bar mean (`priceMean`) and standard

deviation (`priceStdDev`) in absolute price units. Models include:

- **Symmetric Models:** `uniform`, `triangular`, `arcsine`,

`betaSym`, and `t4Sym` (Student-t with fat tails).

- **Skewed Models:** `betaSkew` and `t4Skew`, which adjust

their shape based on the Open/Close position.

- **Model Assumptions:** The skewed models rely on specific

internal constants. `betaSkew` uses a fixed concentration

parameter (`BETA_SKEW_CONCENTRATION = 4.0`), and `t4Sym`/`t4Skew`

use a heuristic scaling factor (`T4_SHAPE_FACTOR`)

to map the distribution.

2. **Econometric Log-Return Estimators (`LogEst`):** Includes a set of

econometric estimators for calculating the volatility (`logStdDev`)

and drift (`logMean`) of logarithmic returns within a single bar.

These are unit-less measures. Models include:

- **Parkinson (1980):** A High-Low range estimator.

- **Garman-Klass (1980):** An OHLC-based estimator.

- **Rogers-Satchell (1991):** An OHLC estimator that accounts

for non-zero drift.

3. **Distribution Analysis (PDF/CDF):** Provides functions to work

with the Probability Density Function (`pricePdf`) and

Cumulative Distribution Function (`priceCdf`) of the

chosen price model.

- **Note on `priceCdf`:** This function uses analytical (exact)

calculations for the `uniform`, `triangular`, and `arcsine`

models. For all other models (e.g., `betaSkew`, `t4Skew`),

it uses **numerical integration (Simpson's rule)** as

an approximation of the cumulative probability.

4. **Mathematical Functions:** The library's Beta distribution

models (`betaSym`, `betaSkew`) are supported by an internal

implementation of the natural log-gamma function, which is

based on the Lanczos approximation.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

priceStdDev(estimator, offset)

Estimates **σ̂** (standard deviation) *in price units* for the current

bar, according to the chosen `PriceEst` distribution assumption.

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float σ̂ ≥ 0 ; `na` if undefined (e.g. zero range).

priceMean(estimator, offset)

Estimates **μ̂** (mean price) for the chosen `PriceEst` within the

current bar.

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float μ̂ in price units.

pricePdf(estimator, price, offset)

Probability-density under the chosen `PriceEst` model.

**Returns 0** when `p` is outside the current bar’s .

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

price (float) : series float Price level to evaluate.

offset (int) : series int To offset the calculated bar

Returns: series float Density value.

priceCdf(estimator, upper, lower, steps, offset)

Cumulative probability **between** `upper` and `lower` under

the chosen `PriceEst` model. Outside-bar regions contribute zero.

Uses a fast, analytical calculation for Uniform, Triangular, and

Arcsine distributions, and defaults to numerical integration

(Simpson's rule) for more complex models.

Parameters:

estimator (series PriceEst) : series PriceEst Distribution assumption (see enum).

upper (float) : series float Upper Integration Boundary.

lower (float) : series float Lower Integration Boundary.

steps (int) : series int # of sub-intervals for numerical integration (if used).

offset (int) : series int To offset the calculated bar.

Returns: series float Probability mass ∈ .

logStdDev(estimator, offset)

Estimates **σ̂** (standard deviation) of *log-returns* for the current bar.

Parameters:

estimator (series LogEst) : series LogEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float σ̂ (unit-less); `na` if undefined.

logMean(estimator, offset)

Estimates μ̂ (mean log-return / drift) for the chosen `LogEst`.

The returned value is consistent with the assumptions of the

selected volatility estimator.

Parameters:

estimator (series LogEst) : series LogEst Distribution assumption (see enum).

offset (int) : series int To offset the calculated bar

Returns: series float μ̂ (unit-less log-return).

LibWghtLibrary "LibWght"

This is a library of mathematical and statistical functions

designed for quantitative analysis in Pine Script. Its core

principle is the integration of a custom weighting series

(e.g., volume) into a wide array of standard technical

analysis calculations.

Key Capabilities:

1. **Universal Weighting:** All exported functions accept a `weight`

parameter. This allows standard calculations (like moving

averages, RSI, and standard deviation) to be influenced by an

external data series, such as volume or tick count.

2. **Weighted Averages and Indicators:** Includes a comprehensive

collection of weighted functions:

- **Moving Averages:** `wSma`, `wEma`, `wWma`, `wRma` (Wilder's),

`wHma` (Hull), and `wLSma` (Least Squares / Linear Regression).

- **Oscillators & Ranges:** `wRsi`, `wAtr` (Average True Range),

`wTr` (True Range), and `wR` (High-Low Range).

3. **Volatility Decomposition:** Provides functions to decompose

total variance into distinct components for market analysis.

- **Two-Way Decomposition (`wTotVar`):** Separates variance into

**between-bar** (directional) and **within-bar** (noise)

components.

- **Three-Way Decomposition (`wLRTotVar`):** Decomposes variance

relative to a linear regression into **Trend** (explained by

the LR slope), **Residual** (mean-reversion around the

LR line), and **Within-Bar** (noise) components.

- **Local Volatility (`wLRLocTotStdDev`):** Measures the total

"noise" (within-bar + residual) around the trend line.

4. **Weighted Statistics and Regression:** Provides a robust

function for Weighted Linear Regression (`wLinReg`) and a

full suite of related statistical measures:

- **Between-Bar Stats:** `wBtwVar`, `wBtwStdDev`, `wBtwStdErr`.

- **Residual Stats:** `wResVar`, `wResStdDev`, `wResStdErr`.

5. **Fallback Mechanism:** All functions are designed for reliability.

If the total weight over the lookback period is zero (e.g., in

a no-volume period), the algorithms automatically fall back to

their unweighted, uniform-weight equivalents (e.g., `wSma`

becomes a standard `ta.sma`), preventing errors and ensuring

continuous calculation.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

wSma(source, weight, length)

Weighted Simple Moving Average (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

the arithmetic mean if Σweight = 0.

wEma(source, weight, length)

Weighted EMA (exponential kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Exponential-kernel weighted mean; falls

back to classic EMA if Σweight = 0.

wWma(source, weight, length)

Weighted WMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic WMA if Σweight = 0.

wRma(source, weight, length)

Weighted RMA (Wilder kernel, α = 1/len).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Wilder-kernel weighted mean; falls back to

classic RMA if Σweight = 0.

wHma(source, weight, length)

Weighted HMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic HMA if Σweight = 0.

wRsi(source, weight, length)

Weighted Relative Strength Index.

Parameters:

source (float) : series float Price series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted RSI; uniform if Σw = 0.

wAtr(tr, weight, length)

Weighted ATR (Average True Range).

Implemented as WRMA on *true range*.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted ATR; uniform weights if Σw = 0.

wTr(tr, weight, length)

Weighted True Range over a window.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of TR; uniform if Σw = 0.

wR(r, weight, length)

Weighted High-Low Range over a window.

Parameters:

r (float) : series float High-Low per bar.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of range; uniform if Σw = 0.

wBtwVar(source, weight, length, biased)

Weighted Between Variance (biased/unbiased).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

variance series float The calculated between-bar variance (σ²btw), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wBtwStdDev(source, weight, length, biased)

Weighted Between Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σbtw uniform if Σw = 0.

wBtwStdErr(source, weight, length, biased)

Weighted Between Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²btw / N_eff) uniform if Σw = 0.

wTotVar(mu, sigma, weight, length, biased)

Weighted Total Variance (= between-group + within-group).

Useful when each bar represents an aggregate with its own

mean* and pre-estimated σ (e.g., second-level ranges inside a

1-minute bar). Assumes the *weight* series applies to both the

group means and their σ estimates.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

varBtw series float The between-bar variance component (σ²btw).

varWtn series float The within-bar variance component (σ²wtn).

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wTotStdDev(mu, sigma, weight, length, biased)

Weighted Total Standard Deviation.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).