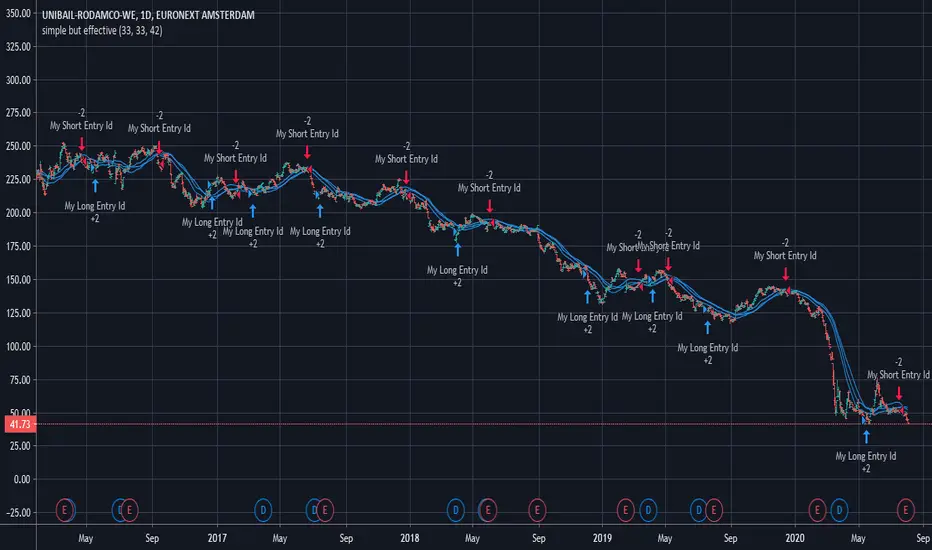

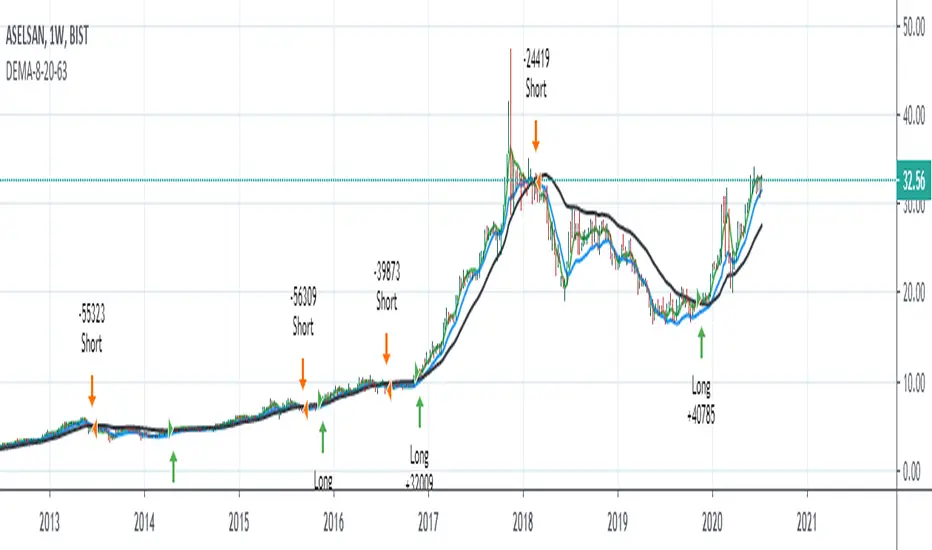

Random entry pointsIt is profitable strategy with random entry points.

A simple strategy involving random opening of trades. But such a strategy on large samples will demonstrate profit. Because the strategy adheres to the golden rule of trading: "Let profits rise and quickly stop losses."

Remember, exit points are very important. Many traders make the mistake of focusing all their attention on entry points.

Стратегия Pine Script®