CMF, RSI, CCI, MACD, OBV, Fisher, Stoch RSI, ADX (+DI/-DI)Eight normalized indicators are used in conjunction with the CMF, CCI, MACD, and Stoch RSI indicators. You can track buy and sell decisions by tracking swings. The zero line is for reversal tracking at -20, +20, +50, and +80. You can use any of the nine indicators individually or in combination.

Fisher

Fisher Transform Trend Navigator [QuantAlgo]🟢 Overview

The Fisher Transform Trend Navigator applies a logarithmic transformation to normalize price data into a Gaussian distribution, then combines this with volatility-adaptive thresholds to create a trend detection system. This mathematical approach helps traders identify high-probability trend changes and reversal points while filtering market noise in the ever-changing volatility conditions.

🟢 How It Works

The indicator's foundation begins with price normalization, where recent price action is scaled to a bounded range between -1 and +1:

highestHigh = ta.highest(priceSource, fisherPeriod)

lowestLow = ta.lowest(priceSource, fisherPeriod)

value1 = highestHigh != lowestLow ? 2 * (priceSource - lowestLow) / (highestHigh - lowestLow) - 1 : 0

value1 := math.max(-0.999, math.min(0.999, value1))

This normalized value then passes through the Fisher Transform calculation, which applies a logarithmic function to convert the data into a Gaussian normal distribution that naturally amplifies price extremes and turning points:

fisherTransform = 0.5 * math.log((1 + value1) / (1 - value1))

smoothedFisher = ta.ema(fisherTransform, fisherSmoothing)

The smoothed Fisher signal is then integrated with an exponential moving average to create a hybrid trend line that balances statistical precision with price-following behavior:

baseTrend = ta.ema(close, basePeriod)

fisherAdjustment = smoothedFisher * fisherSensitivity * close

fisherTrend = baseTrend + fisherAdjustment

To filter out false signals and adapt to market conditions, the system calculates dynamic threshold bands using volatility measurements:

dynamicRange = ta.atr(volatilityPeriod)

threshold = dynamicRange * volatilityMultiplier

upperThreshold = fisherTrend + threshold

lowerThreshold = fisherTrend - threshold

When price momentum pushes through these thresholds, the trend line locks onto the new level and maintains direction until the opposite threshold is breached:

if upperThreshold < trendLine

trendLine := upperThreshold

if lowerThreshold > trendLine

trendLine := lowerThreshold

🟢 Signal Interpretation

Bullish Candles (Green): indicate normalized price distribution favoring bulls with sustained buying momentum = Long/Buy opportunities

Bearish Candles (Red): indicate normalized price distribution favoring bears with sustained selling pressure = Short/Sell opportunities

Upper Band Zone: Area above middle level indicating statistically elevated trend strength with potential overbought conditions approaching mean reversion zones

Lower Band Zone: Area below middle level indicating statistically depressed trend strength with potential oversold conditions approaching mean reversion zones

Built-in Alert System: Automated notifications trigger when bullish or bearish states change, allowing you to act on significant developments without constantly monitoring the charts

Candle Coloring: Optional feature applies trend colors to price bars for visual consistency and clarity

Configuration Presets: Three parameter sets available - Default (balanced settings), Scalping (faster response with higher sensitivity), and Swing Trading (slower response with enhanced smoothing)

Color Customization: Four color schemes including Classic, Aqua, Cosmic, and Custom options for personalized chart aesthetics

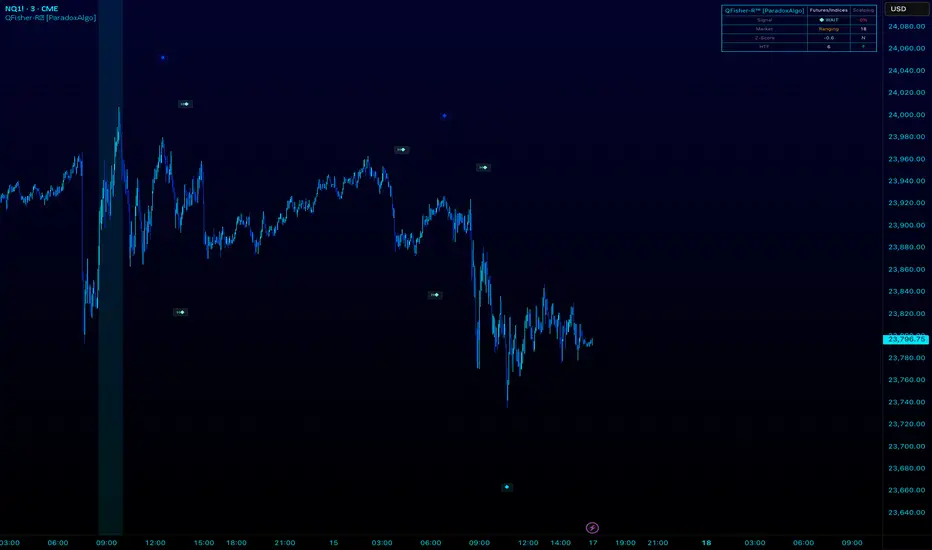

QFisher-R™ [ParadoxAlgo]QFISHER-R™ (Regime-Aware Fisher Transform)

A research/education tool that helps visualize potential momentum exhaustion and probable inflection zones using a quantitative, non-repainting Fisher framework with regime filters and multi-timeframe (MTF) confirmation.

What it does

Converts normalized price movement into a stabilized Fisher domain to highlight potential turning points.

Uses adaptive smoothing, robust (MAD/quantile) thresholds, and optional MTF alignment to contextualize extremes.

Provides a Reversal Probability Score (0–100) to summarize signal confluence (extreme, slope, cross, divergence, regime, and MTF checks).

Key features

Non-repainting logic (bar-close confirmation; security() with no lookahead).

Dynamic exhaustion bands (data-driven thresholds vs fixed ±2).

Adaptive smoothing (efficiency-ratio based).

Optional divergence tags on structurally valid pivots.

MTF confirmation (same logic computed on a higher timeframe).

Compact visuals with subtle plotting to reduce chart clutter.

Inputs (high level)

Source (e.g., HLC3 / Close / HA).

Core lookback, fast/slow range blend, and ER length.

Band sensitivity (robust thresholding).

MTF timeframe(s) and agreement requirement.

Toggle divergence & intrabar previews (default off).

Signals & Alerts

Turn Candidate (Up/Down) when multiple conditions align.

Trade-Grade Turn when score ≥ threshold and MTF agrees.

Divergence Confirmed when structural criteria are met.

Alerts are generated on confirmed bar close by default. Optional “preview” mode is available for experimentation.

How to use

Start on your preferred timeframe; optionally enable an HTF (e.g., 4×) for confirmation.

Look for RPS clusters near the exhaustion bands, slope inflections, and (optionally) divergences.

Combine with your own risk management, liquidity, and trend context.

Paper test first and calibrate thresholds to your instrument and timeframe.

Notes & limitations

This is not a buy/sell signal generator and does not predict future returns.

Readings can remain extreme during strong trends; use HTF context and your own filters.

Parameters are intentionally conservative by default; adjust carefully.

Compliance / Disclaimer

Educational & research tool only. Not financial advice. No recommendation to buy/sell any security or derivative.

Past performance, backtests, or examples (if any) are not indicative of future results.

Trading involves risk; you are responsible for your own decisions and risk management.

Built upon the Fisher Transform concept (Ehlers); all modifications, smoothing, regime logic, scoring, and visualization are original work by Paradox Algo.

Super Oscillator with Alerts by BigBlueCheeseSuper Oscillator with Alerts (by BigBlueCheese)

I got sick of eyeballing multiple oscillators generating output on different scales and interpreting them on the fly, so I picked 4 of my favs, 2 fisher transforms (fast & slow) The Squeeze & my own Market Rhythm Oscillator & made the Super Oscillator with Alerts which combines multiple indicators and oscillators to analyze market conditions and generate actionable trading signals.

The output is buy/sell/neutral signals and a color coded table summarizing indicator states (strong buy to strong sell etc). The color legend can be disabled once you get used to the color codes. The user can choose to watch the table output and its changing output, OR unclutter their screen by toggling the table off & just watching for the signals SO+ (buy), SO-(sell), SO?(neutral)

The combined signals are run through a scoring and weighting scheme that utilizes each indicators Z-scores, Min-Max normalization, and raw values which are all used in different parts of the scoring process.

A velocity filter (for more immediate/sensitive response) is available for the user to toggle on/off. The raw indicator values are classified into categories reflecting their current strength and are assigned momentum points.

Z-scores measure how far each oscillator's current value deviates from its mean in terms of standard deviations. Basically, the Z-scores focus on relative behavior, while momentum captures directional trends. Together, they provide a more nuanced view of market conditions. Large Z-scores increase the likelihood of stronger signals. The idea is to are amplify influence in extreme conditions whereas low Z scores will have minimal impact on the cumulative score, making signals less prone to noise.

Inputs and Their Contributions

1. Momentum: Controlled by the raw oscillator values and thresholds.

2. Min-Max: Automatically calculated based on the historical range of oscillators.

3. Velocity: Input: useVelocity (true/false) toggle. Weights: User-defined weights for velocity contribution.

4. Z-Score: Input: useZScore (true/false) toggle. Weights: User-defined weights for Z-score contribution.

The system combines momentum, Min-Max normalization, (and if enabled) velocity, and Z-scores, to generate dynamic and actionable trading signals that appear as markers on the chart indicating buy, sell, and neutral signals.

Alerts can also be triggered based on these signals.

Users can customize the weighting and inclusion of velocity and Z-scores to align the scoring system with their trading strategy and preferences.

If there is enough interest for some other preferred oscillator, I will substitute it for out my Market Rhythm Oscillator & republish with the code. LMK

For the curious out there, the Market Rhythm Oscillator (MRO) is a custom oscillator that analyzes price dynamics using a combination of weighted volatility-based calculations. It helps measure price momentum and potential exhaustion levels by identifying high and low volatility regions.

• Purpose: The MRO is particularly effective at identifying market trends and potential reversals by analyzing price extremes and their behavior over a defined lookback period.

• Calculation Components might include:

o Waveform Volatility Factor (WVF): Measures the price's deviation from its highest or lowest values within a given period.

o Bands and Smoothing:

Upper and lower bands based on standard deviations of WVF.

Smoothing is applied to the WVF for better trend clarity.

o Exhaustion Levels: Uses the MRO's trend length to calculate when the price action may become overextended.

Happy hunting but as always, not a trade recommendation, past results not indicative of future results, DYOR!

Dynamic Jurik RSX w/ Fisher Transform█ Introduction

The Dynamic Jurik RSX with Fisher Transform is a powerful and adaptive momentum indicator designed for traders who seek a non-laggy view of price movements. This script is based on the classic Jurik RSX (Relative Strength Index). It also includes features such as the dynamic overbought and oversold limits, the Inverse Fisher Transform, trend display, slope calculations, and the ability to color extremes for better clarity.

█ Key Features:

• RSX: The Relative Strength Index (RSX) in this script is based on Jurik’s RSX, which is smoother than the traditional RSI and aims to reduce noise and lag. This script calculates the RSX using an exponential smoothing technique and adaptive adjustments.

• Inverse Fisher Transform: This script can optionally apply the Inverse Fisher Transform to the RSX, which helps to normalize the RSX values, compressing them between -1 and 1. The inverse transformation makes it easier to spot extreme values (overbought and oversold conditions) by enhancing the visual clarity of those extremes. It also smooths the curve over a user-defined period in hopes of providing a more consistent signal.

• Dynamic Limits: The dynamic overbought and oversold limits are calculated based on the RSX's recent high and low values. The limits adjust dynamically depending on market conditions, making them more relevant to current price action.

• Slope Display: The slope of the RSX is calculated as the rate of change between the current and previous RSX value. The slope is displayed as dots when the slope exceeds the threshold designated by the user, providing visual cues for momentum shifts.

• Trend Coloring: Optionally, the user can also enable a trend-based display. It is simply based on current value of RSX versus the previous one. If RSX is rising then the trend is bullish, if not, then the trend is bearish.

• Coloring Extremes: Users can configure the RSX to color the chart when prices enter extreme conditions, such as overbought or oversold zones, providing visual cues for market reversals.

█ Attached Chart Notes:

• Top Panel: Enabled dynamic limits, Trend display, standard Jurik RSX with 20 lookback period, and Slope display.

• Middle Panel: Enabled dynamic limits, Extremes display, and standard Jurik RSX with 20 lookback period.

• Bottom Panel: Enabled dynamic limits, Trend display, Inverse Fisher Transform with 14 lookback period and 9 smoothing period. and Slope display.

█ Credits:

Special thanks to Everget for providing the original script. The script was also slightly modified based on updates from outside sources.

█ Disclaimer:

This script is for educational purposes only and should not be considered financial advice. Always conduct your own research and consult a professional before making any trading decisions.

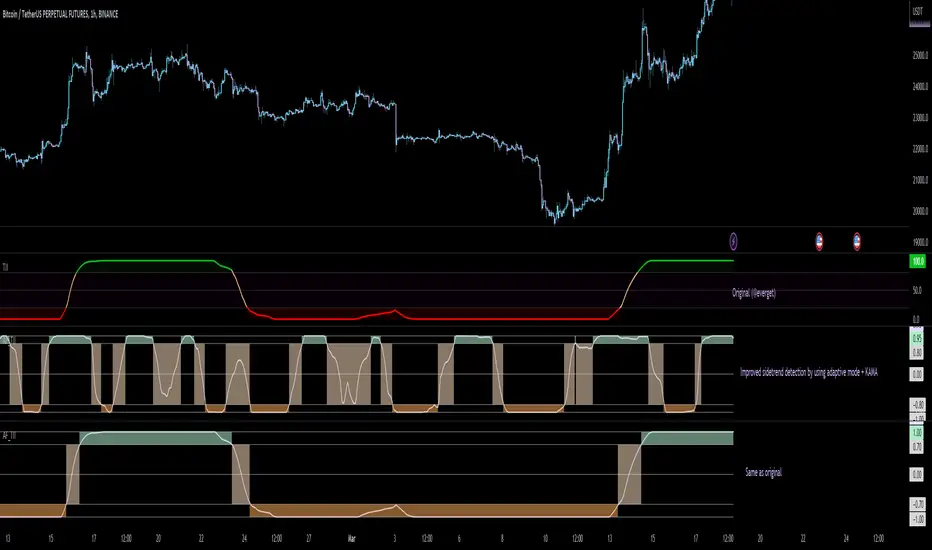

Adaptive Fisher [BackQuant]Adaptive Fisher

What is it at its core:

Custom Kaufman Adaptive Moving Average Smoothed Price Data, Fisher Transformation.

Why did we choose to make an Adaptive Fisher ?

The Adaptive Fisher Transformation Indicator is an advanced technical tool designed to signal potential turning points in market prices by transforming asset price data into a nearly Gaussian normal distribution. This transformation, initially conceptualized by John F. Ehlers, aims to make extreme price behavior, which could indicate potential market reversals, more identifiable. Unlike the standard distribution of asset prices, the Gaussian normal distribution provides a clearer framework for identifying price extremes and trends.

With that being considered there are key things to take into consideration:

As the transformation seeks to normalize price data, it's crucial to remember that asset prices inherently do not follow a normal distribution. Thus, traders should use this tool in conjunction with other analyses to confirm potential trading signals. The effectiveness can vary across different assets and market conditions, underscoring the importance of customization and adaptation to specific trading strategies. As the same for all tools, all must be backtested. Past performance is not a guarantee for future results.

Now for the Key Features

Normalization of Prices: The Adaptive Fisher Transformation normalizes price data, enhancing the visibility of turning points. This normalization is critical for identifying moments when the price movement is statistically significant, thereby aiding in decision-making.

Adaptivity through Kaufman's Adaptive Moving Average (KAMA): Unlike traditional indicators, this version employs KAMA to dynamically adjust to market volatility. By doing so, it smoothens the price data more effectively, providing signals that are more responsive to current market conditions.

Divergence Detection: It includes the capability to detect divergences between the indicator and price movement, a powerful signal of potential trend reversals. Traders can specify the length over which divergences are calculated, allowing for customization based on their trading strategy.

Visual Enhancements: The indicator features color gradients to delineate strength levels and extreme values, improving readability and the quick assessment of market conditions.

Customizable Smoothing Mechanism: To accommodate different assets and timeframes, the indicator includes an option to select from various moving averages for smoothing, with an Exponential Moving Average (EMA) recommended for its effectiveness.

Application and Interpretation:

Traders can utilise this tool to identify potential reversal points by looking for extreme values in the transformed price data. Changes in the direction of the indicator can also signal shifts in market trends.

The inclusion of a normalized Relative Strength Index (RSI) provides additional confluence, aiding traders in recognizing overbought and oversold conditions through color-coded background hues in the chart.

Alert conditions are programmed for various scenarios, including trend shifts, Fisher Transform crossings over the midline, and both regular and hidden divergences, enabling traders to react promptly to potential market movements.

Empirical Soundness

Mathematical Foundation in Gaussian Distribution: At its core, the Fisher Transformation's application to financial markets is based on transforming prices to conform more closely to a Gaussian normal distribution, which is a fundamental concept in statistics. This transformation aims to make the identification of price extremes more reliable. Empirical studies have shown that while raw financial data may not follow a normal distribution, the application of transformations can facilitate the identification of critical turning points in market data (Ehlers, John F., "Cybernetic Analysis for Stocks and Futures", Wiley & Sons, 2004).

Adaptivity through KAMA: The use of Kaufman's Adaptive Moving Average introduces a dynamic element to the indicator, allowing it to adjust to market volatility automatically. This adaptivity is particularly relevant in today's financial markets, where volatility patterns can shift rapidly due to economic news, geopolitical events, and changes in market sentiment. The empirical strength of KAMA lies in its foundational logic, designed to account for market noise and smoothing price data more effectively than traditional moving averages (Kaufman, Perry J., "Trading Systems and Methods", Wiley & Sons, 2013).

Innovative Divergence Detection Mechanism: Divergence detection adds an empirical layer to the Adaptive Fisher Transformation by highlighting discrepancies between price action and the indicator's performance. This feature is grounded in the principle that divergences can often precede reversals, providing early warning signs of potential shifts in market direction. The ability to customize the calculation length for divergences enables the indicator to be fine-tuned to the characteristics of specific assets or market conditions, enhancing its practical application.

User Inputs Explained:

Calculation Source (price): This input determines the base price used for calculations, typically the closing price (close). Traders can adjust this to open, high, low, or another average, tailoring the indicator to focus on specific aspects of price action.

Fisher Lookback (ftPeriod): Defines the period over which the Fisher Transform is calculated. A shorter period makes the indicator more sensitive to price movements, while a longer period smoothens the output, reducing sensitivity.

Make Fisher Adaptive (adapt): A boolean input that enables the adaptation feature of the Fisher Transform using KAMA. When set to true, it dynamically adjusts the Fisher Transform according to market volatility, enhancing its responsiveness to recent price changes.

Adaptive Period (length), Fast Length (fast), Slow Length (slow): These inputs configure the KAMA calculation, affecting its sensitivity to price movements. The length determines the lookback period for volatility calculation, while fast and slow set the speed of adjustment to market conditions.

Smooth Fisher (smooth): Allows for additional smoothing of the Fisher Transform output to reduce noise. This is particularly useful in highly volatile markets or when the indicator is too reactive to price changes.

Smoothing Type (modeSwitch) and Smooth Period (smoothlen): Determine the method and period for smoothing. Options include various moving averages (EMA, SMA, etc.), providing flexibility in how the smoothing is applied.

Show Fisher, Show Fisher Moving Average, Moving Average Period (malen): These inputs control the visibility of the Fisher Transform and its moving average on the chart, as well as the period of the moving average. This helps in identifying trends and the direction of the market.

Show Detected Trend Shifts (trendshift): Enables the highlighting of moments when the indicator suggests a potential shift in market trend, providing early signals for traders.

Show Fisher Strength levels (showextreme): Displays predefined levels indicating extreme values of the Fisher Transform, which could suggest overbought or oversold conditions.

Show Confluence RSI (showrsi), RSI Period (rsiPeriod): These inputs add a normalized Relative Strength Index to the chart for additional analysis, offering a secondary measure of market conditions.

Show Overbought and Oversold Signals: When enabled, the background color changes to highlight overbought or oversold conditions based on the RSI, aiding in visual identification of potential trading opportunities.

Use Case of Midline Crossover Fisher:

Midline Crossover Fisher: The Fisher Transform's midline crossover is a critical signal for traders. A crossover above the midline indicates a bullish market sentiment, suggesting that it might be a good time to consider entering a long position. Conversely, a crossover below the midline suggests bearish sentiment, potentially signaling an opportunity to go short. This is based on the principle that the Fisher Transform makes turning points more evident, and crossing the midline reflects a change in momentum.

Overbought and Oversold Hues:

RSI Overbought and Oversold Background Color: The background color feature for RSI OB (overbought) and OS (oversold) conditions enhances visual cues for market extremes. When the RSI exceeds upper thresholds (Above 70), indicating overbought conditions, the background will turn to warn traders of potential price reversals. Similarly, when the RSI falls below lower thresholds (Below 30), suggesting oversold conditions, green can highlight potential opportunities for buying.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

This is using the Midline Crossover:

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

GKD-C APA Adaptive Fisher Transform [Loxx]The Giga Kaleidoscope GKD-C APA Adaptive Fisher Transform is a confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-C APA Adaptive Fisher Transform

APA Adaptive Fisher Transform is an adaptive cycle Fisher Transform using Ehlers Autocorrelation Periodogram Algorithm to calculate the dominant cycle period.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

What is Fisher Transform?

The Fisher Transform is a technical indicator created by John F. Ehlers that converts prices into a Gaussian normal distribution.

The indicator highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, and the Average Directional Index (ADX).

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Multi-Ticker CC Backtest

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: Advance Trend Pressure as shown on the chart above

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Rex Oscillator

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

? Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

SuperTrend Fisher [AlgoAlpha]🚀🌟 Introducing the "Super Fisher" by AlgoAlpha, a sophisticated and versatile tool crafted for the discerning trader. This innovative indicator merges the precision of the Fisher Transform with the adaptability of the SuperTrend methodology, offering a fresh perspective on market analysis. 📈🔍

Key Features:

🔶 Customizable Settings: Tailor the indicator to your trading style with adjustable inputs like "Fair-value Period" and "EMA Length". Choose your preferred "Up Color" and "Down Color" for a personalized visual experience.

🔶 Advanced Fisher Transform: At the heart of this tool is the Fisher Transform, an algorithm renowned for pinpointing potential price reversals by normalizing asset prices.

🔶 Integrated SuperTrend Functionality: This feature adds a layer of trend analysis, using the refined Fisher Transform values to generate dynamic, trend-following signals.

🔶 Enhanced Visualization: Clearly distinguishable bullish and bearish market phases, thanks to the color-coded plots of Fisher Transform and SuperTrend values.

🔶 Overbought/Oversold Levels: Visual plots and fills for these levels provide additional insights into market extremities.

🔶 Configurable Alerts: Stay informed with alerts for critical market movements like crossing the zero line or the SuperTrend.

Logic:

The "Super Fisher" operates on a sophisticated algorithm:

1. Fisher Transform Calculation: It starts by calculating the Detrended Price Oscillator (DPO) and its standard deviation. These values are then transformed using the Fisher Transform formula, which is subsequently smoothed with a Hull Moving Average.

2. SuperTrend Integration: The SuperTrend function employs the Fisher Transform values to create a dynamic trend-following tool. It calculates upper and lower bands and determines which one to use for market direction based on whether the fisher is above or below the bands, offering an insightful view of the price trend.

3. Overbought/Oversold Identification: The tool plots specific levels to indicate overbought and oversold conditions, aiding in the identification of potential reversal points.

Here's a closer look at the core calculations:

Calculates the Fisher Transform:

value = 0.0

value := round_(.66 * ((src - low_) / (high_ - low_) - .5) + .67 * nz(value ))

fish1 = 0.0

fish1 := .5 * math.log((1 + value) / (1 - value)) + .5 * nz(fish1 )

fish1 := ta.hma(fish1, l)

Calculates the SuperTrend:

supertrend(factor, atrPeriod, srcc) =>

src = srcc

atr = atrr(srcc, atrPeriod)

upperBand = src + factor * atr

lowerBand = src - factor * atr

prevLowerBand = nz(lowerBand )

prevUpperBand = nz(upperBand )

lowerBand := lowerBand > prevLowerBand or srcc < prevLowerBand ? lowerBand : prevLowerBand

upperBand := upperBand < prevUpperBand or srcc > prevUpperBand ? upperBand : prevUpperBand

int direction = na

float superTrend = na

prevSuperTrend = superTrend

if na(atr )

direction := 1

else if prevSuperTrend == prevUpperBand

direction := srcc > upperBand ? -1 : 1

else

direction := srcc < lowerBand ? 1 : -1

superTrend := direction == -1 ? lowerBand : upperBand

How to Use:

📊 To maximize the potential of the "Super Fisher", follow these steps:

1. Customize Settings: Adjust the inputs to match your trading preferences. This includes setting the periods for the Fisher Transform and SuperTrend, as well as choosing colors for better visualization.

2. Analyze the Market: Observe the Fisher Transform and SuperTrend plots to gauge market direction. Pay special attention to color changes, as they indicate shifts in market sentiment.

3. Identify Extremes: Use the overbought and oversold plots to understand potential reversal points.

4. Set Alerts: Utilize the alert functionality to stay informed about significant market movements, ensuring you never miss an opportunity.

🔥 In summary the "Super Fisher" is a comprehensive market analysis tool designed to enhance your trading insights and decision-making process. 📉🌟🚨

Normalized Fisher Transformed VolumeGreetings Traders,

I am thrilled to introduce a game-changing tool that I've passionately developed to enhance your trading precision – the Normalized Fisher Transformed Volume indicator. Let's dive into the specifics and explore how this tool can empower you in the markets.

Unlocking Trading Precision:

Normalization and Transformation:

Normalize raw volume data to ensure a consistent scale for analysis.

The Fisher Transformation converts normalized volume data into a Gaussian distribution, providing enhanced insights into trend dynamics.

Flexible Modes for Tailored Strategies:

Choose from three distinct modes:

Volume T3 (MA) + Heatmap: Identify trends with T3 Moving Average and visualize volume strength with Heatmap.

Volume Percent Rank: Evaluate the position of current volume relative to historical data.

Volume T3 (MA) Percent Rank: Combine T3 Moving Average with percentile ranking for a comprehensive analysis.

Heatmap Visualization for Quick Insights:

Heatmap Zones and Lines visually represent volume strength relative to historical data.

Customize threshold multipliers and color options for precise Heatmap interpretation.

T3 Moving Average Integration:

Smoothed representation of volume trends with the T3 Moving Average enhances trend identification.

Percent Rank Analysis for Context:

Gauge the position of normalized volume within historical context using Percent Rank analysis.

User-Friendly Customization:

Easily adjust parameters such as length, T3 Moving Average length, Heatmap standard deviation length, and threshold multipliers.

Intuitive interface with colored bars and customizable background options for personalized analysis.

How to Use Effectively:

Mode Selection:

Identify your preferred trading strategy and select the mode that aligns with your approach.

Parameter Adjustment:

Fine-tune the indicator by adjusting parameters to match your preferred trading style.

Interpret Heatmap and T3 Analysis:

Leverage Heatmap and T3 Moving Average analysis to spot potential trend reversals, overbought/oversold conditions, and market sentiment shifts.

Conclusion:

The Normalized Fisher Transformed Volume indicator is not just a tool; it's your key to unlocking precision in trading. Crafted by Simwai, this indicator offers unique insights tailored to your specific trading needs. Dive in, explore its features, experiment with parameters, and let it guide you to more informed and precise trading decisions.

Trade wisely and prosper,

simwai

Fisher+ [OSC]The Fisher Transform Indicator is classified as an oscillator, meaning that its value swings above and below a central point. This characteristic allows traders to identify overbought and oversold conditions, providing potential clues about market reversals. As mentioned previously, it is an oscillator so the strength of the move is displayed by how long the fisher line stays above/below zero. Indicator can be used to aid in confluence near supply/demand zones.

White Line = Fisher

Red/Blue Line = Moving Average

--Changes color whether fisher line is above/below the MA

Red/Blue Shaded Line = Moving Average

--Changes color based on a smoothing factor

Red/Blue Shaded Fill = Asset in Overbought/Oversold Conditions

Red/Blue Circles = Asset in Extreme Overbought/Oversold Conditions

Red/Blue Triangles = MACD Signals Below/Above "0"

Divergence Labels = Asset Signaling Divergence

The moving average line will turn red/blue as long as the fisher line is below/above the moving average. The shaded MA line will switch colors based on if it is moving in an up/down trend. The MA can also be used as a signal and treated similar to an oscillator. Market trending conditions will either keep the MA below/above the dashed zero line.

MACD code credited to LazyBear's MACD Leader indicator. It is used to filter out/confirm any signals such as divergences. As long as the MACD Leader line is above both the MACD line and signal lines then it'll signal with with a triangle. MACD divergences will be added at a later time.

Limited Fisher Transformwhat is Limited Fisher Transform?

This indicator is a compressed version of the Fisher transform indicator between 100 and 0 values.

what it does?

It allows us to define overbought and oversold zones by compressing the values of the "fisher transform" indicator between 0 and 100. also these zones are the same for every timeframe and trading pair, just like RSI.

how it does it?

it use this formula:

x = fisher transform values

a = average

how to use it?

its use is indistinguishable from the standard fisher. You can use it to set alarms for overbought and oversold zones. so you will be notified when a possible opportunity arises in the market.

Adaptive Fisherized CMOIntroduction

Heyo, here is another no-repaint adaptive fisherized indicator.

I added Inverse Fisher Transform, Ehlers dominant cycle analysis and smoothing to the Chande Momentum Oscillator (CMO).

Usage

The CMO is a momentum oscillator which shows the usual movement of an asset.

I recommend to use it from a lower timeframe with a higher timeframe set.

Signals

(Signal mode will come soon.)

Zero Line

CMO crosses above zero line => enter long

CMO cross below zero line => ente short

Overbought/Oversold

CMO crosses above bottom band => enter long

CMO crosses under top band => enter short

MA (Maybe this signals will vary. Then, check update notes.)

CMO crosses above MA => enter long

CMO crosses below MA => enter short

Enjoy and share your experience with it!

More to read: CMO Explanationsp

Adaptive Fisherized KSTIntroduction

Heyo guys, here is a new adaptive fisherized indicator of me.

I applied Inverse Fisher Transform, Ehlers dominant cycle analysis,

smoothing and divergence analysis on the Know Sure Thing (KST) indicator.

Moreover, the indicator doesn't repaint.

Usage

I didn't backtest the indicator, but I recommend the 5–15 min timeframe.

It can be also used on other timeframs, but I have no experience with that.

The indicator has no special filter system, so you need to find an own combo in order to build a trading system.

A trend filter like KAMA or my Adaptive Fisherized Trend Intensity Index could fit well.

If you find a good combo, let me know it in the comments pls.

Signals

Zero Line

KST crossover 0 => Enter Long

KST crossunder 0 => Enter Short

Cross

KST crossover KST MA => Enter Long

KST crossunder KST MA => Enter Short

Cross Filtered

KST crossover KST MA and KST above 0 => Enter Long

KST crossunder KST MA and KST under 0 => Enter Short

KST crossunder 0 => Exit Long

KST crossover 0 => Exit Short

More to read: KST Explanation

Enjoy and let me know your opinion!

--

Credits to

- @tista

- @blackcat1402

- @DasanC

- @cheatcountry

Adaptive Fisherized Trend Intensity Index Introduction

Here, I modified the script "Trend Intensity Index" (TII) of @everyget.

TTI was developed by M.H. Pee, who also published other trend analysis indicators like the Trend Trigger/Continuation Factor

It helps to determine how strong the current trend is.

The stronger the trend, the higher the chance the price may continue moving in the current direction.

Features

Adaptive mode (based on Ehlers dominant cycle determination) => automatically determines the length

Inverse Fisher Transform => gives sharper signals

Customizable MA Types => discover the impact of different ma bases

Hann Window and NET smoothing => state-of-the-art smoothing

Trend Visualization => shows you the up/down/side trend

Usage

This indicator here offers a perfect trend filtering system. It is capable of up/down/side trend detection.

There are a lot of trend indicators which don't respect sidetrends, which makes this indicator pretty useful.

A lot of traders use trend-following trading systems.

A trader will usually make his/her entry in the market during a strong trend and ride it, until the TII provides an indication of a reversal.

For mean-revertive trading systems, you could use TII to just trade in side trend.

A lot of mean-revertive signal emitters like Bollinger Bands or RSI work most of the times better in side trend.

Furthermore, every timeframe could be used, but higher timeframes have more impact because trends are stronger there.

Signals

Green zone (Top) => Etablished bullish trend

"Peachy" Zone (Middle) => Sidetrend/flat market

Red Zone (Bottom) => Etablished bearish trend

Enjoy guys!

(Let me know your opinions!)

--

Credits to:

@blackcat1402

@DasanC

@cheatcountry

@everget

Adaptive Fisherized ROCIntroduction

Hello community, here I applied the Inverse Fisher Transform, Ehlers dominant cycle determination and smoothing methods on a simple Rate of Change (ROC) indicator

You have a lot of options to adjust the indicator.

Usage

The rate of change is most often used to measure the change in a security's price over time.

That's why it is a momentum indicator.

When it is positive, prices are accelerating upward; when negative, downward.

It is useable on every timeframe and could be a potential filter for you your trading system.

IMO it could help you to confirm entries or find exits (e.g. you have a long open, roc goes negative, you exit).

If you use a trend-following strategy, you could maybe look out for red zones in an in uptrend or green zones in a downtrend to confirm your entry on a pullback.

Signals

ROC above 0 => confirms bullish trend

ROC below 0 => confirms bearish trend

ROC hovers near 0 => price is consolidating

Enjoy! 🚀

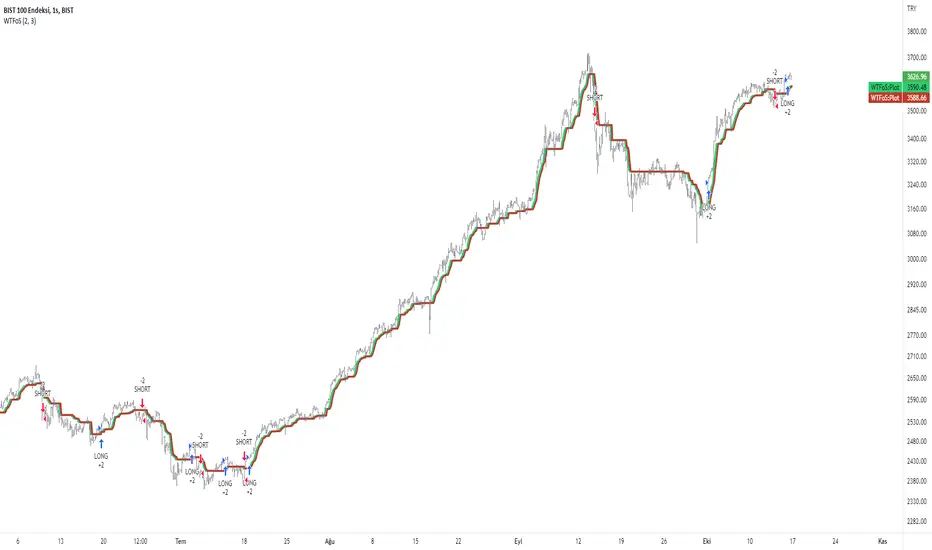

WilliamTrendFollower StrategyThis strategy is based on signals from the WilliamTrendFollower indicator.

You can optimize the parameters of this strategy as you wish. I hope you get the most accurate result.

About WilliamTrendFollower:

With this indicator, we try to catch the trends in price. With continued use of this indicator, we expect it to eventually escape horizontal positions and catch up with continuous trends.

Combined with the WilliamsR indicator and the exponential moving average indicator.

The WilliamsR Fisher Transforms are combined with the ATR indicator to create a line that lags behind the moving average value.

Since it is a tracking indicator, we created a line that is more connected to the price and itself.

In this way, a curve close to the price line is obtained in uptrends and downtrends.

In this indicator, if you choose the parameters correctly, you can easily bypass the horizontal positions. This gives you a safe visualization of support and resistance points as well.

From the settings of these indicators, you can set the multiplier and the exponential moving average period.

It works in all time intervals.

But it was calculated without volume , instead it was created using fisher transforms, moving averages, and the average true range .

WilliamTrendFollowerWith this indicator, we try to catch the trends in price. With continued use of this indicator, we expect it to eventually escape horizontal positions and catch up with continuous trends.

Combined with the WilliamsR indicator and the exponential moving average indicator.

The WilliamsR Fisher Transforms are combined with the ATR indicator to create a line that lags behind the moving average value.

Since it is a tracking indicator, we created a line that is more connected to the price and itself.

In this way, a curve close to the price line is obtained in uptrends and downtrends.

In this indicator, if you choose the parameters correctly, you can easily bypass the horizontal positions. This gives you a safe visualization of support and resistance points as well.

With this tracker, you can generate Buy and Sell signals and you can see them on the chart.

From the settings of these indicators, you can set the multiplier and the exponential moving average period.

It works in all time intervals.

But it was calculated without volume , instead it was created using fisher transforms, moving averages, and the average true range .

You can set an alarm for Buy and Sell orders.

You can see the processing entry and exit areas in a straight line.

The Fisher Transform indicator is an oscillator that helps identify trend reversals and can be applied to any financial instrument. J.F. Created by Ehlers

Gaussian Filter MACD [Loxx]Gaussian Filter MACD is a MACD that uses an 1-4 Pole Ehlers Gaussian Filter for its calculations. Compare this with Ehlers Fisher Transform.

What is Ehlers Gaussian filter?

This filter can be used for smoothing. It rejects high frequencies (fast movements) better than an EMA and has lower lag. published by John F. Ehlers in "Rocket Science For Traders". First implemented in Wealth-Lab by Dr René Koch.

A Gaussian filter is one whose transfer response is described by the familiar Gaussian bell-shaped curve. In the case of low-pass filters, only the upper half of the curve describes the filter. The use of gaussian filters is a move toward achieving the dual goal of reducing lag and reducing the lag of high-frequency components relative to the lag of lower-frequency components.

A gaussian filter with...

one pole is equivalent to an EMA filter.

two poles is equivalent to EMA ( EMA ())

three poles is equivalent to EMA ( EMA ( EMA ()))

and so on...

For an equivalent number of poles the lag of a Gaussian is about half the lag of a Butterworth filters: Lag = N * P / (2 * ¶2), where,

N is the number of poles, and

P is the critical period

Special initialization of filter stages ensures proper working in scans with as few bars as possible.

From Ehlers Book: "The first objective of using smoothers is to eliminate or reduce the undesired high-frequency components in the eprice data. Therefore these smoothers are called low-pass filters, and they all work by some form of averaging. Butterworth low-pass filtters can do this job, but nothing comes for free. A higher degree of filtering is necessarily accompanied by a larger amount of lag. We have come to see that is a fact of life."

References John F. Ehlers: "Rocket Science For Traders, Digital Signal Processing Applications", Chapter 15: "Infinite Impulse Response Filters"

Included

Loxx's Expanded Source Types

Signals, zero or signal crossing, signal crossing is very noisy

Alerts

Bar coloring

TheATR: Fisher Oscillator.Fisher Oscillator(FO).

The Fisher Oscillator is inspired by John Ehlers "Fisher Transform".

The oscillator highlights when prices have moved to an extreme, based on recent prices.

The FO may help in spotting turning points, in the short-medium trends of an asset, also, it helps in recognizing the asset's trends themselves, giving a picture of mkt conditions affected by less noise.

Fisher Oscillator Components.

Fisher V1 -> Main FO.

Fisher V2 -> Past Candle FO.

0-line threshold -> Directional Component.

How to read the Fisher Oscillator.

The FO is super easy to read by itself.. also, I coded some features which make it even easier to read.

It's suggestions, which we can call "Signals", come from 2 different sources, accessible thanks to the variable "Signals Type".

- 0-Line Crosses:

When the "Fisher V1" upcrosses the oscillator 0-line, the oscillator suggests a Long scenario.

When the "Fisher V1" downcrosses the oscillator 0-line, the oscillator suggests a Short scenario.

- Classic Lines Crosses:

When the "Fisher V1" upcrosses the "Fisher V2", the oscillator suggests a Long scenario.

When the "Fisher V1" downcrosses the "Fisher V2", the oscillator suggests a Short scenario.

Users will be able to recognise these Signals visually, thanks to some color customisation to the "Fisher V1" line, and thanks to the ability of the oscillator of plotting Signals.

TheATR Documentation regarding TheATR: Fisher Oscillator.

Researching and backtesting the FO, I noticed it's skill of being able to dynamically identify trend reversals with a nice degree of reliability.

Also, the FO's able to keep up with trends up to their tops/bottoms, as it's very responsive.

This makes the FO a trend-following oscillator in my personal view, because its nature of being very fast in detecting reversals will lead to many false reversals as well.

On the other face of this coin, if we look at the FO as a source for confirmations for a trend-following strategy, may be very useful.

To conclude, I would use the FO as a confirmation oscillator, in a trend-following strategy that needs to have other components.

Thanks for reading,

TheATR.

Fisher Transform of MACD w/ Quantile Bands [Loxx]Fisher Transform of MACD w/ Quantile Bands is a Fisher Transform indicator with Quantile Bands that takes as it's source a MACD. The MACD has two different source inputs for fast and slow moving averages.

What is Fisher Transform?

The Fisher Transform is a technical indicator created by John F. Ehlers that converts prices into a Gaussian normal distribution.

The indicator highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

What is Quantile Bands?

In statistics and the theory of probability, quantiles are cutpoints dividing the range of a probability distribution into contiguous intervals with equal probabilities, or dividing the observations in a sample in the same way. There is one less quantile than the number of groups created. Thus quartiles are the three cut points that will divide a dataset into four equal-size groups (cf. depicted example). Common quantiles have special names: for instance quartile, decile (creating 10 groups: see below for more). The groups created are termed halves, thirds, quarters, etc., though sometimes the terms for the quantile are used for the groups created, rather than for the cut points.

q-Quantiles are values that partition a finite set of values into q subsets of (nearly) equal sizes. There are q − 1 of the q-quantiles, one for each integer k satisfying 0 < k < q. In some cases the value of a quantile may not be uniquely determined, as can be the case for the median (2-quantile) of a uniform probability distribution on a set of even size. Quantiles can also be applied to continuous distributions, providing a way to generalize rank statistics to continuous variables. When the cumulative distribution function of a random variable is known, the q-quantiles are the application of the quantile function (the inverse function of the cumulative distribution function) to the values {1/q, 2/q, …, (q − 1)/q}.

What is MACD?

Moving average convergence divergence ( MACD ) is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. The MACD is calculated by subtracting the 26-period exponential moving average ( EMA ) from the 12-period EMA .

Included:

Zero-line and signal cross options for bar coloring, signals, and alerts

Alerts

Signals

Loxx's Expanded Source Types

35+ moving average types

Fisher Transform w/ Dynamic Zones [Loxx]What is Fisher Transform?

The Fisher Transform is a technical indicator created by John F. Ehlers that converts prices into a Gaussian normal distribution.

The indicator highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included

3 signal types

Bar coloring

Alerts

Channels fill

Loxx's Expanded Source Types

Fisher OscillatorThe indicator highlights when prices have moved to an extreme level, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

VHF Adaptive Fisher Transform [Loxx]VHF Adaptive Fisher Transform is an adaptive cycle Fisher Transform using a Vertical Horizontal Filter to calculate the volatility adjusted period.

What is VHF Adaptive Cycle?

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

What is Fisher Transform?

The Fisher Transform is a technical indicator created by John F. Ehlers that converts prices into a Gaussian normal distribution.

The indicator highlights when prices have moved to an extreme, based on recent prices. This may help in spotting turning points in the price of an asset. It also helps show the trend and isolate the price waves within a trend.

Included:

Zero-line and signal cross options for bar coloring

Customizable overbought/oversold thresh-holds

Alerts

Signals