Linear Regression (Log Scale)This code is a slightly modified version of Tradingviews' built-in "linear regression" script which can be correctly plotted on logarithmic charts.

Стандартное отклонение

Nic's VIX CorrelationIdentifies divergences in price action between the VIX (volatility index) and a ticker. Divergences can be a 'red flag' identifying lack of confidence in the price action.

Best used in with volume studies, across multiple time frames, and across multiple tickers.

Supports any volatility ticker (VIX, VXN, RVX).

Responsive Linear Regression ChannelsThis is a linear trend indicator that can:

- automagically adjust to different chart resolutions

- snap to day/session boundaries on intraday

- totally not do the above and use ye olde good fixed lookback window

- show the regression trend and its RMSE channels

- disregard the trend and just show the period average and standard deviation lines (often acting as support and resistance)

The main idea was to allow you to quickly view linear trends for different time periods without having to calculate the required amount of bars.

By default, you will be able to quickly switch between 1-3 months, 6 months, 1 year, 2 years and 5 years of data, as well as various daily lookback periods.

Please adjust resolution settings to your liking.

Caveats:

- More data means more noise and slower calculations.

- HLC3 source is recommended, especially at resolutions above hourly.

- Trend will be slightly different if you use extended hours.

- If you use extended hours and don't have a data subscription, trend will be SUBSTANTIALLY different, especially at smaller resolutions like 1m.

- You might want to use 3.5 days per week for crypto (it's 7 days by default).

Known problems:

- If you can't see the trendlines, scroll to the left or zoom out - the origin could be outside of your viewport.

- Futures' sessions start on the previous day. We currently snap only to day boundaries, not session breaks.

- UVXY and the like that have extremely high price datapoints. The calculations will be wrong on some resolutions.

- Replay can freeze circa bar_index 244 — disable smart lookback and keep your window under 240 bars if you encounter this.

ACKNOWLEDGEMENTS:

Many thanks to alexgrover for his extremely efficient functions (used with permission)

Neglected Volume by DGTVolume is one piece of information that is often neglected, however, learning to interpret volume brings many advantages and could be of tremendous help when it comes to analyzing the markets. In addition to technicians, fundamental investors also take notice of the numbers of shares traded for a given security.

What is Volume?

The volume represents all the recorded trades for a security that occurs in a given time interval. It is a measurement of the participation, enthusiasm, and interest in a given security. Think of volume as the force that drives the market. Volume substantiates, energizes, and empowers price. When volume increases, it confirms price direction; when volume decreases, it contradicts price direction.

In theory, increases in volume generally precede significant price movements. However, If the price is rising in an uptrend but the volume is reducing or unchanged, it may show that there’s little interest in the security, and the price may reverse.

A high volume usually indicates more interest in the security and the presence of institutional traders. However, a rapidly rising price in an uptrend accompanied by a huge volume may be a sign of exhaustion.

Traders usually look for breaks of support and resistance to enter positions. When security break critical levels without volume, you should consider the breakout suspect and prime for a reversal off the highs/lows

Volume spikes are often the result of news-driven events. Volume spike will often lead to sharp reversals since the moves are unsustainable due to the imbalance of supply and demand

note : there’s no centralized exchange where trades are recorded, so the volume data represents what happens at a particular exchange only

In most charting platforms, the volume indicator is presented as color-coded bars, green if the security closes up and red if the security closed lower, where the height of the bars show the amount of the recorded trades

Within this study, Relative Volume , Volume Weighted Bars and Volume Moving Average are presented, where Relative Volume relates current trading volume to past trading volume over long period, Volume Weighted Bars presents price bars colored based on short period past trading volume average, and Volume Moving Average is average of volume over shot period

Relative Volume is presented as color-coded bars similar to regular Volume indicator but uses four color codes instead two. Notable increases of volume are presented in green and red while average values with back and gray, hence adding ability to emphasis notable increases in the volume. It is kind of a like a radar for how "in-play" a security is. Users are allowed to change the threshold, default value is set to Fibonacci golden ration standard deviation away from its moving average.

Volume Weighted Bars, a study of Kıvanç Özbilgiç, aims to present if price movements are supported by Volume. Volume Weighted Bars are calculated based on shot period volume moving average which will reflect more recent changes in volume. Price actions with high volume will be displayed with darker colors, average volume values will remain as they are and low volume values will be indicated with lighter colors.

Volume Moving Average, Is short period volume moving average, aims to display visually the volume changes. Please not that Relative Volume bars are calculated based on standard deviation of long volume moving average.

What Else?

Apart from the volume itself, your ability to assess what volume is telling you in conjunction with price action can be a key factor in your ability to turn a profit in the market. It makes little sense to analyze the volume alone. To correctly interpret the volume data, it shall be seen in the light of what the price is doing. there are a lot of other indicators that are based on the volume data as well as price action. Analysing those volume indicators has always helped traders and investors to better understand what is happening in the market.

Here are the ones adapted with this study. Some of them used as a source for our aim, some adapted as they are with slight changes to fit visually to this study and please note that the numerical presentation may differ from their regular use

• On Balance Volume

• Divergence Indicator

• Correlation Coefficient

• Chaikin Money Flow

Shortly;

On Balance Volume

The On Balance Volume indicator, is a technical analysis indicator that relates volume flow to changes in a security’s price. It uses a cumulative total of positive and negative trading volume to predict the direction of price. The OBV is a volume-based momentum oscillator, so it is a leading indicator — it changes direction before the price

Granville, creator of OBV, proposed the theory that changes in volume precede price movements in a measurable way. He believed that volume was the main force behind major market moves and thought of OBV’s prediction of price changes as a compressed spring that expands rapidly when released.

It is believed that the OBV shows the interactions between the institutional and retail traders in the market

If the price makes a new high, the OBV should also make a new high. If the OBV makes a lower high when the price makes a higher high, there’s a classical bearish divergence — indicating that only the retail traders are buying. Another type of bearish divergence occurs when the price remains relatively quiet and fails to make a higher high but the OBV soars higher than the previous high — indicating that the institutional traders are accumulating short positions. On the other hand, if the price makes a lower low and the OBV makes a higher low, there is a classical bullish divergence, showing that the institutional traders don’t believe in that move

With this study, Momentum and Acceleration (optional) of OBV is calculated and presented, where momentum is most commonly referred to as a rate and measures the acceleration of the price and/or volume of a security. It is also referred to as a technical analysis indicator and oscillator that is able to determine market trends.

Additionally, smoothing functionality with Least Squares Method is added

Divergences especially, should always be noted as a possible reversal in the current trend, so the divergence indicator is adapted with this study where the Momentum of OBV is assumed as Oscillator with similar usages as to RSI. Divergence is most often used to track and analyze the momentum in an asset’s price and the odds of a price reversal within the current trend. The divergence indicator warns traders and technical analysts of changes in a price/volume trend, oftentimes that it is weakening or changing direction.

Correlation Coefficient

The correlation coefficient is a statistical measure of the strength of the relationship between the relative movements of two variables. A correlation of -1.0 shows a perfect negative correlation, while a correlation of 1.0 shows a perfect positive correlation. A correlation of 0.0 shows no linear relationship between the movement of the two variables. In other words, the closer the Correlation Coefficient is to 1.0, indicates the instruments will move up and down together as it is mostly expected with volume and price. So the Correlation Coefficient Indicator aims to display when the price and volume (on balance volume) is in correlation and when not. With this study blue represent positive correlation while orange negative correlation. The strength of the correlation is determined by the width of the bands, to emphasis the effect horizontal lines are drawn with values set to 0.5 and -0.5. the values above 0.5 (or below -0.5) shows stronger correlation.

Chaikin Money Flow , provide optionally as a companion indicator

The Chaikin money flow indicator (CMF) is a volume indicator that measures the money flow volume over a chosen period. The money flow volume is a measure of the volume and where the price closed relative to the trading session’s range. It comes from the idea that buying pressure is indicated by a rising volume and recurrent closes in the upper part of the session’s price range while selling pressure is demonstrated by an increasing volume and repeated closes in the lower part of the price range.

Both buying and selling pressures are accompanied by an increase in volume, but the location of the closing prices are in accordance with the direction of price

Special thanks to @InvestCHK and @hjsjshs , who have enormously contributed while preparing this study

related studies:

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

3 Leg Short Strangle BandsDraws 3 leg bands along with safe zone(green lines) based on input

1) Input ATR, Week Day, Current Market Close

2) Input ATR - Previous day 1H Max ATR

3) ADX < 25

4) Input Current Market Close

5) Trading Day - Mon/Tue/Wed/Thu/Fri - Bands distance calculated based on day M/Tu/F 2*(Max ATR), W/Th 1.5(ATR)

6) Safe zone green lines - CMPCls +/- (1.5 * Max ATR)

7) Leg 1 Upper Lower Legs - M/Tu/F - CMPCls +/-(2 * Max ATR), W/Th - CMPCls +/-(1.5 * ATR)

8) Leg 2 & 3 Calculates based on Leg 2 = Leg 1 +/- 100 pts distance, Leg 3 = Leg 2 +/- 100 pts distance'

9) All figures rounded to nearest 100's

10) Safe zone broken exit all positions

This is a popular technic used by Profitable traders on sideway markets for Intraday

One can keep 3K as SL per 1 set of 3 legs for better R:R

NIFTY VIX Bands1) The script takes current INDIA VIX as input Daily time frame for NIFTY

2) Used a Formula VIX Value / Square root of Time Period

3) Change Timeframe input accordingly 1 Year = 1, Monthly = 12, Weekly = 52, Daily = 365

4) based point 2 formula with 1 standard deviation it creates upper & lower range bands

5) This is generally used for option selling by big traders they go and sell above the band strikes

Standard Deviation Volatility HelperHere is a simple Standard Deviation Line based on supply and demand that will help you to find expected move easily. 3 Standart Deviation merged line available. Number of days and adjustable length.

Bollinger Bands Money Flow IndexThis script embodies the application of the Bollinger Band and Money Flow Index in John A. Bollinger's book "Bollinger on Bollinger Bands."

"Bollinger on Bollinger Bands" suggests a relatively method of analysis by applying the Bollinger Band to an indicator.

Here's one of the indicators, Money Flow Index.

Money Flow Index is an indicator of overbuying and overselling by reflecting the volume of transactions.

"Bollinger on Bollinger Bands" suggests using the Bollinger Band to create relative top and bottom lines for various indicators, such as Money Flow Index.

Original Money Flow Index is considered to be over-purchased if it is more than 80% and over-selling if it is less than 20%.

But if you put a bolinger band on it, you can set the standard for higher or lower over-selling and over-selling in a sustained bullish, bearish market.

This script uses the following values as the default values as recommended by "Bollinger on Bollinger Bands".

Money Flow Index for 10 days.

a bollinger band of forty days

standard deviation of 2

The above values are suitable for most stocks and markets, but sometimes there is too much or too little data inside the Bollinger Band.

It is recommended to modify each value little by little to adjust 85% to 90% of the total data to fit inside the Bollinger Band.

If the value is higher than the top line, it is considered over-purchased, and a red background color appears.

If the bottom line is crossed down, it is considered over-sold and the green background color appears.

MultiType Shifting Predictive Moving Averages (MA) CrossoverJust 2 Moving Averages with adjustable settings and shifting capability, plus signals and predicting continuations.

At the time of publish these different types of MAs are supported:

- SMA (Simple)

- EMA (Exponential)

- DEMA (Double Exponential)

- TEMA (Triple Exponential)

- RMA (Adjusted Exponential)

- WMA (Weighted)

- VWMA (Volume Weighted)

- SWMA (Symmetrically Weighted)

- HMA (Hull)

I'm looking forward to any idea about filtering the signals. Thanks.

Semi Deviation Point PercentThe Semi Deviation Point calculates the positive value as the standard deviation of only samples that has high value than the simple moving average. The negative value is the same standard deviation, but only uses the low value and multiply for -1.

After this calculate the value is divide by the value of simple moving average and multiplied by hundred to get a percent value from 0% to 100%.

The delta line is a simple moving average from the differences of the two values.

How it should be read?

If positive values are greater than negative values than the volatility is happen on higher prices and not lower.

If positive values are lower than negative values than the volatility is happen on lower prices and not higher.

If you know that in which market you would opt in? Is it less risk the prior?

Bollinger Band Volatility Spread VisualizerThis indicator was created to see the total dollar (or whatever currency pair) amount spread between the upper and lower Bollinger Bands. This knowledge of knowing this spread can be used to indicate upcoming periods of high volatility in a market. The fundamental idea behind predicting periods of high volatility is backed up by the idea that periods of low volatility are followed by periods of high volatility and vice versa.

Based on this knowledge, the numerical spread of the Bollinger Bands, as shown in the indicator, we can deduce that when the value is super low, we can expect a period of high volatility AKA: big move incoming.

This indicator is not fully finished because this was my first time coding in Pinescript and I wanted to post the basic indicator first.

My future plans for improving this indicator include:

Adding customization as an option to choose your personal BBands settings that this indicator is based off of

Potentially converting this indicator as a TradingView Strategy where a signal would go off when the spread reaches a certain threshold

Squeeze Momentum Indicator [LazyBear] vX by DGTModified version of Squeeze Momentum Indicator visualizing on Price Chart

author: LazyBear, modified by KıvançÖZBİLGİÇ

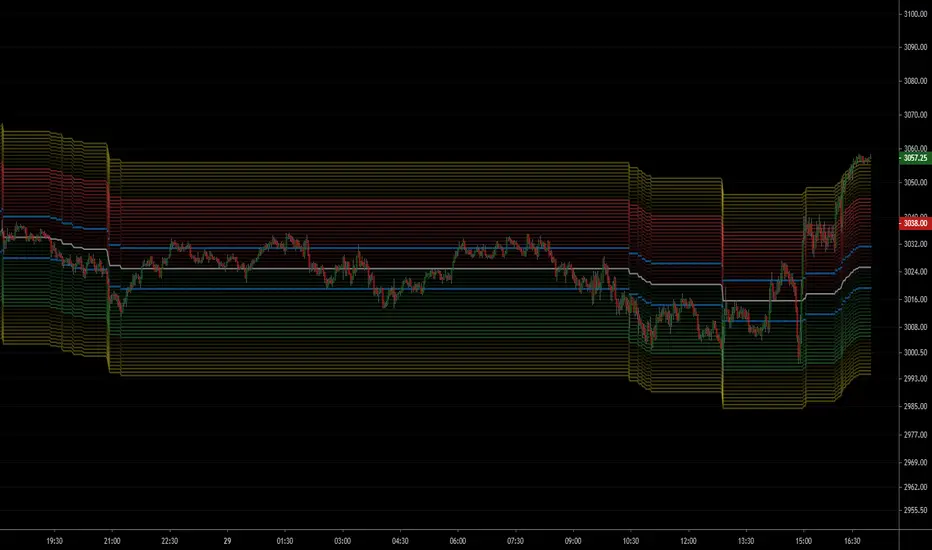

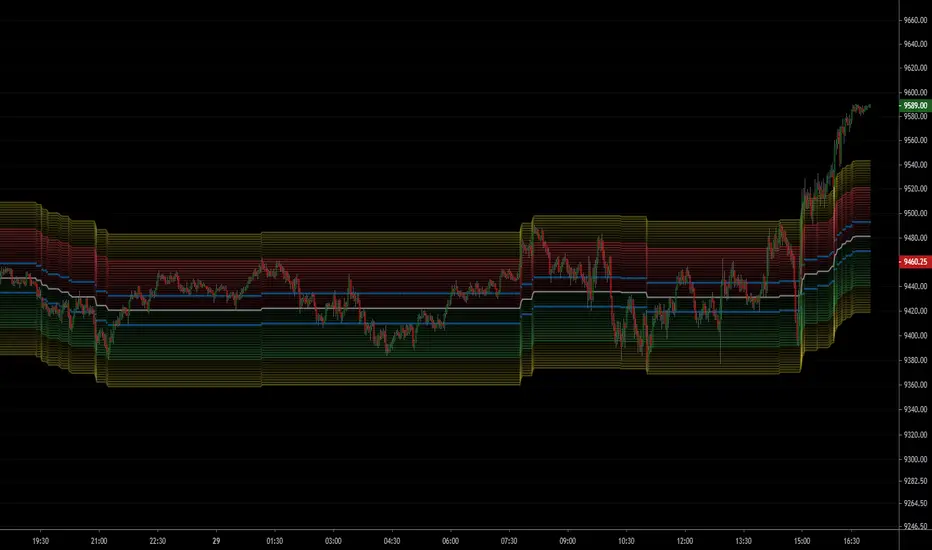

NSDT ES Midline Zones**DESIGNED FOR ES/MES** This script provides an easy visualization of potential reversion zones to take trades back to the intraday midline. A common use would be to enter a position once price reached the outer yellow zones and retreats to either the red zone (for a short toward the midline) or a green zone (for a long back to the midline).

NSDT NQ Midline Zones**DESIGNED FOR NQ/MNQ** This script provides an easy visualization of potential reversion zones to take trades back to the intraday midline. A common use would be to enter a position once price reached the outer yellow zones and retreats to either the red zone (for a short toward the midline) or a green zone (for a long back to the midline).

Basic BIASBasic BIAS

Deviation rate (bias), also known as deviation rate, or y-value for short, is an indicator to reflect the deviation degree between the price and MA in a certain period of time by calculating the percentage difference between the market index or closing price and a moving average, so as to obtain the possibility that the price will reverse or rebound due to deviation from moving average trend in case of severe fluctuation, and that the price will move within the normal fluctuation range Form the credibility of continuing the original potential.

The deviation rate is a percentage of the deviation degree (gap rate) between the price and ma.

The departure rate curve (bias) is a curve that connects the values of each bias into a line and obtains a wave extension curve with the value of 0 as the horizontal axis.

Trend Analysis IndicatorThe Trend Analysis Indicator was created by Adam White (Stocks & Commodities V. 10:8 (358-360)) and this is not to be confused with the Trend Analysis Index which was also created by Adam White. The stock is trending when it is above the signal and loses steam when it falls below the signal. Generally you should buy when it is above it's signal and sell when it goes below the signal.

Let me know if you would like me to write more scripts!

SPY Expected Move by VIXThis indicator shows 1 and 2 standard deviation price move from the VWAP based on VIX. Implied Volatility (IV) is being used extensively in the Option world to project the Expected Move for the underlying instrument. VIX is used as a proxy for SPY's IV for 30 days.

This indicator is meaningful only for SPY but can be used in any other instrument which has a strong correlation to SPY.

Better Bollinger BandsIt is a highly configurable Bollinger Bands implementation.

You can choose different moving averages: EMA, SMA, WMA, VWMA, RMA (Wilder's EMA), ZLEMA, HMA (Hull MA), ALMA

Select between standard or mean deviation

You can use "High" or "Low" for upper and lower bands, which makes them much better for dynamic support-resistance

You can shift (offset) right the bands to use it as support and resistance in the future

Historical Volatility Percentile + SMAHistorical Volatility Percentile tells you the percentage of the days from the past year (252 trading days) that have lower volatility than the current volatility.

I included a simple moving average as a signal line to show you how volatile the stock is at the moment.

I have included simple colors to let you know when to enter or exit a position.

Buy when price higher than EMA & historical volatility higher than SMA

Sell when price lower than EMA & historical volatility higher than SMA

Please let me know if you would like me to publish any other indicators! I always love to hear from you guys.

Volatility SkewThis indicator measure the historical skew of actual volatility for an individual security. It measure the volatility of up moves versus down moves over the period and gives a ratio. When the indicator is greater than one, it indicators that volatility is greater to the upside, when it is below 1 it indicates that volatility is skewed to the downside.

This is not comparable to the SKEW index, since that measures the implied volatility across option strikes, rather than using historical volatility.

Corrected Moving AverageThis moving average was originally developed by professor Andreas Uhl in 2005 (The paper in German: www.buero-uhl.de). Here is the guy himself: wavelab.at

The strength of the CMA is that the current value of the time series must exceed the current volatility-dependent threshold, so that the filter increases or falls, avoiding false signals in weak phases.

The straight line of CMA can be used for a ranging market identification

Mean Absolute Deviation BandsThe other way to build bands around price that uses Mean Absolute Deviation instead of Standard Deviation.

MAD is also a measure of variability, but less frequently used. MAD is better for use with distributions other than the Gaussian.

MAD is always less than or equal to Standard Deviation and the resulting bands are more tighter for the same parameters if we compare it to Bollinger Bands.

If you use band stops this can be useful.

VWAP y Standar DeviationThis script presents the real VWAP (Yellow line), in 50 period VWAP (Blue Line) and the 120 period VWAP (Red Line). Additionally, it presents the values of 1 and 1,618 standard deviations of the VWAP of 50 periods.

This confirmation allows to visualize the behavior of the price in realicon to the VWAP key indicator that represents the midpoint of the operating volumes in a period.

This script evaluates the deviation of the price in relation to the average of the volume traded in the different periods.

The indicator settings allow changing the length of the VWAP for custom settings. Standard deviations are determined based on VWAP 2. VWAP 1 is a reference for determining the global trend of movement in the established period.

The upper and lower limits of the representative Standard Deviation of 1.618 (Fibonacci Number) are used as confirmation of continuation of a trend once crossed by the price.

During the ranges the 1.618 limits of the Dev. Standard are used as entry and exit points of the operation (For this it is necessary to adjust the VWAP 2 to the studied temporality and the operated asset)